LAW2453 Taxation 1: Report on Dave Granger's Tax Residency

VerifiedAdded on 2023/01/17

|12

|3024

|21

Report

AI Summary

This report, prepared for LAW2453 Taxation 1, examines the tax residency status of Dave Granger, an Australian citizen living abroad. The report delves into the four tests used to determine residency: the ordinary concepts test, domicile test, 183-day test, and superannuation test, analyzing Dave's situation against each. It concludes that Dave is a non-resident based on his circumstances, including his extended stay in Nepal and lack of ties to Australia. The report then addresses the taxation of income for non-residents, specifically focusing on the implications of Dave and his wife owning an investment property and shares in Australia. The report also includes a detailed timesheet outlining the work performed and reflective writing addressing key aspects of the assignment, including the analysis of client information and the overall learning experience.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Part A:........................................................................................................................................2

Introduction:...........................................................................................................................2

Determination of Residential Status:.........................................................................................2

Ordinary concepts Test:.........................................................................................................3

Domicile Test:........................................................................................................................4

The 183 days Test:.................................................................................................................5

Superannuation Test:..............................................................................................................5

Taxation of Income:...................................................................................................................6

Conclusion:............................................................................................................................6

Part 2: Time Sheet......................................................................................................................7

Part 3: Reflective Writing..........................................................................................................7

Answer to question 1:.............................................................................................................7

Answer to question 2:.............................................................................................................8

Answer to question 3:.............................................................................................................8

Answer to question 4:.............................................................................................................8

Answer to question 5:.............................................................................................................9

References:...............................................................................................................................10

Table of Contents

Part A:........................................................................................................................................2

Introduction:...........................................................................................................................2

Determination of Residential Status:.........................................................................................2

Ordinary concepts Test:.........................................................................................................3

Domicile Test:........................................................................................................................4

The 183 days Test:.................................................................................................................5

Superannuation Test:..............................................................................................................5

Taxation of Income:...................................................................................................................6

Conclusion:............................................................................................................................6

Part 2: Time Sheet......................................................................................................................7

Part 3: Reflective Writing..........................................................................................................7

Answer to question 1:.............................................................................................................7

Answer to question 2:.............................................................................................................8

Answer to question 3:.............................................................................................................8

Answer to question 4:.............................................................................................................8

Answer to question 5:.............................................................................................................9

References:...............................................................................................................................10

2TAXATION LAW

Part A:

Introduction:

As defined under “section 6 (1), ITAA 1936” the resident of Australian represents the

person that are living in Australia and also comprises of the person that have the domicile in

Australia, excluding the circumstances when the commissioner is content that the person’s

permanent place of abode is out of Australia (Woellner et al., 2016). For the foreign resident

under “section 6-5, (3)(a), ITAA 1997” it includes in the assessable income the ordinary

income that is obtained from the Australian sources. According to the “section 995-1, ITAA

1997” a foreign resident refers to the person that are not the resident of Australia within the

meaning of “ITAA 1936”. A non-resident is explained under “section 6 (1), ITAA 1936” that

includes person that are not the resident of Australia (Blakelock & King, 2017). Residency is

regarded as the means through which Australia exerts its authority to impose tax. For

individuals, there are four test that helps in determining the residential status namely;

a. Ordinary concepts test

b. Domicile Test

c. 183 day’s Test

d. Superannuation Test

The present report is based on determining the tax residency status for Dave’s and issues

related to the taxation during the relevant year.

Determination of Residential Status:

The definition related to the resident of Australia comprises of four distinct test and

the last test is clearly considered as objective. There are several number of cases that is

associated with the understanding of the first three test. The case laws provide an

understanding relating to the meaning of the terms that are used under “section 6 (1), ITAA

Part A:

Introduction:

As defined under “section 6 (1), ITAA 1936” the resident of Australian represents the

person that are living in Australia and also comprises of the person that have the domicile in

Australia, excluding the circumstances when the commissioner is content that the person’s

permanent place of abode is out of Australia (Woellner et al., 2016). For the foreign resident

under “section 6-5, (3)(a), ITAA 1997” it includes in the assessable income the ordinary

income that is obtained from the Australian sources. According to the “section 995-1, ITAA

1997” a foreign resident refers to the person that are not the resident of Australia within the

meaning of “ITAA 1936”. A non-resident is explained under “section 6 (1), ITAA 1936” that

includes person that are not the resident of Australia (Blakelock & King, 2017). Residency is

regarded as the means through which Australia exerts its authority to impose tax. For

individuals, there are four test that helps in determining the residential status namely;

a. Ordinary concepts test

b. Domicile Test

c. 183 day’s Test

d. Superannuation Test

The present report is based on determining the tax residency status for Dave’s and issues

related to the taxation during the relevant year.

Determination of Residential Status:

The definition related to the resident of Australia comprises of four distinct test and

the last test is clearly considered as objective. There are several number of cases that is

associated with the understanding of the first three test. The case laws provide an

understanding relating to the meaning of the terms that are used under “section 6 (1), ITAA

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

1997” (Barkoczy, 2016). This is due the residency status of a person is ascertained through

case basis and relies on the particular facts and situations of the separate.

As evident in the current case of Dave he is an Australian citizen however moved to

Paris for structural engineering role where he married Olivia in 2007 and moved to Nepal in

2007. Dave regularly returned to Australia and returned temporarily to look after his ill

mother. To determine the residency status of Dave the following test are performed;

Ordinary concepts Test:

Whether a person is living in Australia is regarded as the main test to determine the

residency status. An individual would be treated as the Australian resident for the purpose of

tax if they usually lived in Australia, irrespective of their nationality, citizenship or their

location of permanent home (Fry, 2017). The court of law in “Applegate v FCT (1979)”

stated that permanent does not indicates endless and it is assessed every year. The taxpayer

here was treated as non-resident because he had the permanent place of abode out of

Australia.

A person is treated as Australian resident when their behaviour over the period

portrays a degree of continuousness, routine or habit which is in accordance with residing in

Australia. In the case of “Iyengar v FC of T (2011)” an engineer that took up the 2 year plus

overseas appointment, however maintained his family home and ties in Australia to which the

taxpayer ultimately returned and was held to be the Australian resident based on the ordinary

concepts (James, 2016). Within the ordinary concepts test Dave cannot be treated as the

Australian resident because has been living in Nepal from 2007 and holds no such ties with

Australia. The taxpayer here Dave has maintained his location and personal assets in Nepal

where he lives in a fully furnished home. Even though he returned to Australia 2016 his

1997” (Barkoczy, 2016). This is due the residency status of a person is ascertained through

case basis and relies on the particular facts and situations of the separate.

As evident in the current case of Dave he is an Australian citizen however moved to

Paris for structural engineering role where he married Olivia in 2007 and moved to Nepal in

2007. Dave regularly returned to Australia and returned temporarily to look after his ill

mother. To determine the residency status of Dave the following test are performed;

Ordinary concepts Test:

Whether a person is living in Australia is regarded as the main test to determine the

residency status. An individual would be treated as the Australian resident for the purpose of

tax if they usually lived in Australia, irrespective of their nationality, citizenship or their

location of permanent home (Fry, 2017). The court of law in “Applegate v FCT (1979)”

stated that permanent does not indicates endless and it is assessed every year. The taxpayer

here was treated as non-resident because he had the permanent place of abode out of

Australia.

A person is treated as Australian resident when their behaviour over the period

portrays a degree of continuousness, routine or habit which is in accordance with residing in

Australia. In the case of “Iyengar v FC of T (2011)” an engineer that took up the 2 year plus

overseas appointment, however maintained his family home and ties in Australia to which the

taxpayer ultimately returned and was held to be the Australian resident based on the ordinary

concepts (James, 2016). Within the ordinary concepts test Dave cannot be treated as the

Australian resident because has been living in Nepal from 2007 and holds no such ties with

Australia. The taxpayer here Dave has maintained his location and personal assets in Nepal

where he lives in a fully furnished home. Even though he returned to Australia 2016 his

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

behaviour did not reflected any continuity, routine or habit which is consistent with living in

Australia.

The fact that the taxpayer has acquired the fully furnished property overseas in Nepal,

Dave fails the ordinary concepts test and cannot be treated as the Australian resident under

“section 6 (1), ITAA 1997”.

Domicile Test:

With respect to the definition given under “section 6 (1), ITAA 1997” a person would

be treated as the Australian resident if they have their domicile in Australia except when the

commissioner can prove that they have established their permanent place of residence out of

Australia. The court of law in “FCT v Applegate (1979)” considered the meaning of

permanent place of abode (Sadiq, 2018). The taxation commissioner noticed that even though

Applegate has retained the Australian domicile, he had established the permanent place of

abode out of Australia. A person that leaves Australia on temporary basis to reside in

overseas nation and acquires the permanent place of dwelling out of Australia, then they

cease to be an Australian resident during their non-existence. In an another example of “Boer

v FC of T (2012)” the taxpayer was considered as the Australian resident all through their

stay in overseas because they did not establish the permanent place of residence out of

Australia (Robin & Barkoczy, 2019).

As evident in the current situation of Dave, even though he is born in Australia but he

has acquired a permanent place of residence out of Australia in Nepal. The taxpayer

continued to enjoy the culture and hiking in Nepal which proves that he has established the

permanent place of residence in Nepal. He also bought is clothing and personal effects and

sold his car as well. He also did not have any intention of returning back again neither he

behaviour did not reflected any continuity, routine or habit which is consistent with living in

Australia.

The fact that the taxpayer has acquired the fully furnished property overseas in Nepal,

Dave fails the ordinary concepts test and cannot be treated as the Australian resident under

“section 6 (1), ITAA 1997”.

Domicile Test:

With respect to the definition given under “section 6 (1), ITAA 1997” a person would

be treated as the Australian resident if they have their domicile in Australia except when the

commissioner can prove that they have established their permanent place of residence out of

Australia. The court of law in “FCT v Applegate (1979)” considered the meaning of

permanent place of abode (Sadiq, 2018). The taxation commissioner noticed that even though

Applegate has retained the Australian domicile, he had established the permanent place of

abode out of Australia. A person that leaves Australia on temporary basis to reside in

overseas nation and acquires the permanent place of dwelling out of Australia, then they

cease to be an Australian resident during their non-existence. In an another example of “Boer

v FC of T (2012)” the taxpayer was considered as the Australian resident all through their

stay in overseas because they did not establish the permanent place of residence out of

Australia (Robin & Barkoczy, 2019).

As evident in the current situation of Dave, even though he is born in Australia but he

has acquired a permanent place of residence out of Australia in Nepal. The taxpayer

continued to enjoy the culture and hiking in Nepal which proves that he has established the

permanent place of residence in Nepal. He also bought is clothing and personal effects and

sold his car as well. He also did not have any intention of returning back again neither he

5TAXATION LAW

intends to work in Australia again. Therefore, it can be stated that Dave does not meets the

criteria of Domicile Test and non-resident of Australia under “section 6 (1), ITAA 1936”.

The 183 days Test:

An individual that has been living in Australia for more than one half of the income

year or six months in the relevant income year would be treated as the Australian resident

unless the commissioner is content that the taxpayer has their permanent place of abode out

of Australia and has no intention of taking up the residency in Australia (Morgan & Castelyn,

2018).

As noticed Dave visited Australia for only 91 days in total. Under the 183 days’ test

Dave cannot be treated as Australian resident because he has not been physically present in

Australia for 183 days. In other words, Dave’s stay in Australia was less than 183 days or six

month of the relevant income year of 2018. Dave also clearly stated that neither he intends to

live in Australia nor he has any intention of returning back. He has established his permanent

place of abode out of Australian in Nepal. Therefore, Dave fails to meet the criteria of 183

day’s test and hence non-resident of Australia under “section 6 (1), ITAA 1936” (Morgan et

al., 2018).

Superannuation Test:

This test is applicable to the member of the commonwealth super fund that are

considered as the eligible employee and the family members are deemed to be Australian

resident (Robin, 2019). This test cannot be applied to Dave because he is not the member of

Superannuation fund.

Overall based on the above test conducted it can be stated that Dave has failed to meet

any of the residency test. Dave in this context will be treated as non-resident of Australia

under “section 6 (1), ITAA 1936”.

intends to work in Australia again. Therefore, it can be stated that Dave does not meets the

criteria of Domicile Test and non-resident of Australia under “section 6 (1), ITAA 1936”.

The 183 days Test:

An individual that has been living in Australia for more than one half of the income

year or six months in the relevant income year would be treated as the Australian resident

unless the commissioner is content that the taxpayer has their permanent place of abode out

of Australia and has no intention of taking up the residency in Australia (Morgan & Castelyn,

2018).

As noticed Dave visited Australia for only 91 days in total. Under the 183 days’ test

Dave cannot be treated as Australian resident because he has not been physically present in

Australia for 183 days. In other words, Dave’s stay in Australia was less than 183 days or six

month of the relevant income year of 2018. Dave also clearly stated that neither he intends to

live in Australia nor he has any intention of returning back. He has established his permanent

place of abode out of Australian in Nepal. Therefore, Dave fails to meet the criteria of 183

day’s test and hence non-resident of Australia under “section 6 (1), ITAA 1936” (Morgan et

al., 2018).

Superannuation Test:

This test is applicable to the member of the commonwealth super fund that are

considered as the eligible employee and the family members are deemed to be Australian

resident (Robin, 2019). This test cannot be applied to Dave because he is not the member of

Superannuation fund.

Overall based on the above test conducted it can be stated that Dave has failed to meet

any of the residency test. Dave in this context will be treated as non-resident of Australia

under “section 6 (1), ITAA 1936”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Taxation of Income:

According to the “section 6-5 (3)(a) of the ITAA 1997” non-residents are treated for

assessment based on their ordinary income and statutory income that are obtained from the

Australian sources (Burton, 2017). If the taxpayer were the non-resident all through the

income year and derived Australian sourced income, then the taxpayer would be required to

pay tax at the non-resident withholding rates for any income derived from Australia. Foreign

residents are generally imposed tax in Australia on income that are earned from the

investment sourced in Australia. If a non-resident receives the income from the Australian

sources, then they would be required to pay taxes on that income and lodge a tax return

(Miller & Oats, 2016). However, a non-resident of Australian would not be required to lodge

the tax return if the income only amounts to interest, unfranked dividends, fully franked

dividends or royalties from which the withholding tax can be withheld by the payer.

As evident in the current case of Dave it is noticed that Dave and Olivia bought an

investment property jointly in Australia. As Dave and Olivia have owned a real property in

Australia, should they make any income from that Australian property, Dave would be

required to declare the income in the Australian tax return. In the later instances it is noticed

that Dave also purchased shares in Australian listed company with Olivia. As Dave is a non-

resident of Australia and only derives income from the shares and investment property he

would be lodge tax return in Australia. The dividends from shares can be subjected

withholding as it is sourced in Australia.

Conclusion:

The report can be concluded by stating that Dave even though he was born in

Australia established home out of Australia in Nepal. Dave fails to meet any of the residential

test. Therefore, Dave in this context will be treated as non-resident of Australia under

“section 6 (1), ITAA 1936”. Furthermore, as Dave is a non-resident of Australia held shares

Taxation of Income:

According to the “section 6-5 (3)(a) of the ITAA 1997” non-residents are treated for

assessment based on their ordinary income and statutory income that are obtained from the

Australian sources (Burton, 2017). If the taxpayer were the non-resident all through the

income year and derived Australian sourced income, then the taxpayer would be required to

pay tax at the non-resident withholding rates for any income derived from Australia. Foreign

residents are generally imposed tax in Australia on income that are earned from the

investment sourced in Australia. If a non-resident receives the income from the Australian

sources, then they would be required to pay taxes on that income and lodge a tax return

(Miller & Oats, 2016). However, a non-resident of Australian would not be required to lodge

the tax return if the income only amounts to interest, unfranked dividends, fully franked

dividends or royalties from which the withholding tax can be withheld by the payer.

As evident in the current case of Dave it is noticed that Dave and Olivia bought an

investment property jointly in Australia. As Dave and Olivia have owned a real property in

Australia, should they make any income from that Australian property, Dave would be

required to declare the income in the Australian tax return. In the later instances it is noticed

that Dave also purchased shares in Australian listed company with Olivia. As Dave is a non-

resident of Australia and only derives income from the shares and investment property he

would be lodge tax return in Australia. The dividends from shares can be subjected

withholding as it is sourced in Australia.

Conclusion:

The report can be concluded by stating that Dave even though he was born in

Australia established home out of Australia in Nepal. Dave fails to meet any of the residential

test. Therefore, Dave in this context will be treated as non-resident of Australia under

“section 6 (1), ITAA 1936”. Furthermore, as Dave is a non-resident of Australia held shares

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

in Australian listed company and also bought investment property together with Olivia. As a

result any such income derived from the shares and investment property would be subjected

to withholding in Australia and taxes may apply based on non-withholding rates.

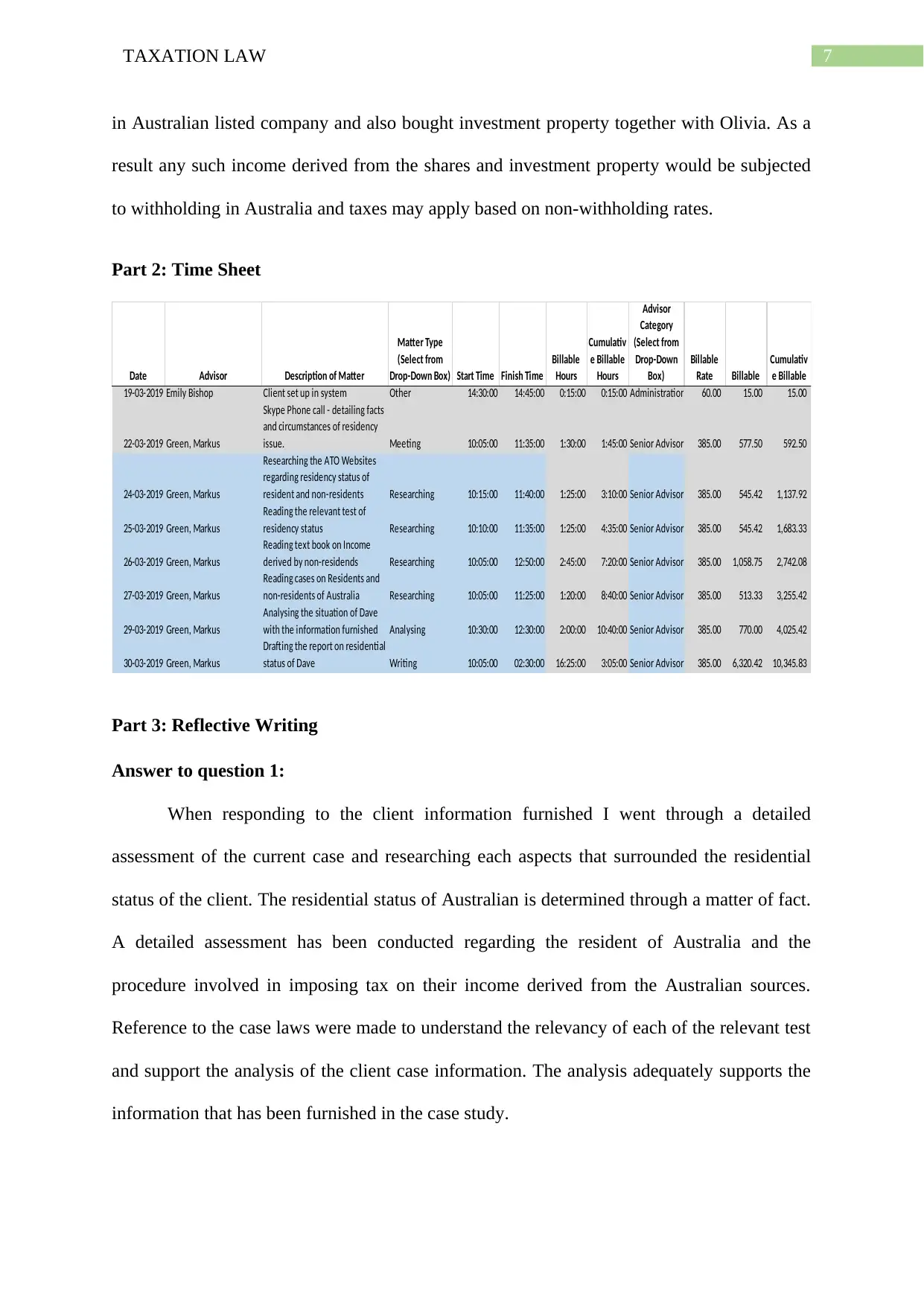

Part 2: Time Sheet

Date Advisor Description of Matter

Matter Type

(Select from

Drop-Down Box) Start Time Finish Time

Billable

Hours

Cumulativ

e Billable

Hours

Advisor

Category

(Select from

Drop-Down

Box)

Billable

Rate Billable

Cumulativ

e Billable

19-03-2019 Emily Bishop Client set up in system Other 14:30:00 14:45:00 0:15:00 0:15:00 Administration 60.00 15.00 15.00

22-03-2019 Green, Markus

Skype Phone call - detailing facts

and circumstances of residency

issue. Meeting 10:05:00 11:35:00 1:30:00 1:45:00 Senior Advisor 385.00 577.50 592.50

24-03-2019 Green, Markus

Researching the ATO Websites

regarding residency status of

resident and non-residents Researching 10:15:00 11:40:00 1:25:00 3:10:00 Senior Advisor 385.00 545.42 1,137.92

25-03-2019 Green, Markus

Reading the relevant test of

residency status Researching 10:10:00 11:35:00 1:25:00 4:35:00 Senior Advisor 385.00 545.42 1,683.33

26-03-2019 Green, Markus

Reading text book on Income

derived by non-residends Researching 10:05:00 12:50:00 2:45:00 7:20:00 Senior Advisor 385.00 1,058.75 2,742.08

27-03-2019 Green, Markus

Reading cases on Residents and

non-residents of Australia Researching 10:05:00 11:25:00 1:20:00 8:40:00 Senior Advisor 385.00 513.33 3,255.42

29-03-2019 Green, Markus

Analysing the situation of Dave

with the information furnished Analysing 10:30:00 12:30:00 2:00:00 10:40:00 Senior Advisor 385.00 770.00 4,025.42

30-03-2019 Green, Markus

Drafting the report on residential

status of Dave Writing 10:05:00 02:30:00 16:25:00 3:05:00 Senior Advisor 385.00 6,320.42 10,345.83

Part 3: Reflective Writing

Answer to question 1:

When responding to the client information furnished I went through a detailed

assessment of the current case and researching each aspects that surrounded the residential

status of the client. The residential status of Australian is determined through a matter of fact.

A detailed assessment has been conducted regarding the resident of Australia and the

procedure involved in imposing tax on their income derived from the Australian sources.

Reference to the case laws were made to understand the relevancy of each of the relevant test

and support the analysis of the client case information. The analysis adequately supports the

information that has been furnished in the case study.

in Australian listed company and also bought investment property together with Olivia. As a

result any such income derived from the shares and investment property would be subjected

to withholding in Australia and taxes may apply based on non-withholding rates.

Part 2: Time Sheet

Date Advisor Description of Matter

Matter Type

(Select from

Drop-Down Box) Start Time Finish Time

Billable

Hours

Cumulativ

e Billable

Hours

Advisor

Category

(Select from

Drop-Down

Box)

Billable

Rate Billable

Cumulativ

e Billable

19-03-2019 Emily Bishop Client set up in system Other 14:30:00 14:45:00 0:15:00 0:15:00 Administration 60.00 15.00 15.00

22-03-2019 Green, Markus

Skype Phone call - detailing facts

and circumstances of residency

issue. Meeting 10:05:00 11:35:00 1:30:00 1:45:00 Senior Advisor 385.00 577.50 592.50

24-03-2019 Green, Markus

Researching the ATO Websites

regarding residency status of

resident and non-residents Researching 10:15:00 11:40:00 1:25:00 3:10:00 Senior Advisor 385.00 545.42 1,137.92

25-03-2019 Green, Markus

Reading the relevant test of

residency status Researching 10:10:00 11:35:00 1:25:00 4:35:00 Senior Advisor 385.00 545.42 1,683.33

26-03-2019 Green, Markus

Reading text book on Income

derived by non-residends Researching 10:05:00 12:50:00 2:45:00 7:20:00 Senior Advisor 385.00 1,058.75 2,742.08

27-03-2019 Green, Markus

Reading cases on Residents and

non-residents of Australia Researching 10:05:00 11:25:00 1:20:00 8:40:00 Senior Advisor 385.00 513.33 3,255.42

29-03-2019 Green, Markus

Analysing the situation of Dave

with the information furnished Analysing 10:30:00 12:30:00 2:00:00 10:40:00 Senior Advisor 385.00 770.00 4,025.42

30-03-2019 Green, Markus

Drafting the report on residential

status of Dave Writing 10:05:00 02:30:00 16:25:00 3:05:00 Senior Advisor 385.00 6,320.42 10,345.83

Part 3: Reflective Writing

Answer to question 1:

When responding to the client information furnished I went through a detailed

assessment of the current case and researching each aspects that surrounded the residential

status of the client. The residential status of Australian is determined through a matter of fact.

A detailed assessment has been conducted regarding the resident of Australia and the

procedure involved in imposing tax on their income derived from the Australian sources.

Reference to the case laws were made to understand the relevancy of each of the relevant test

and support the analysis of the client case information. The analysis adequately supports the

information that has been furnished in the case study.

8TAXATION LAW

Answer to question 2:

Yes, I will be comfortable in giving my report to the employer. This is because the

report carries the quality of presentation that would help in gaining an easy understanding of

the client present situation and the content are relevant with the Australian taxation law.

Considering about my strength, I have command over my communication skills and possess

the adequate understanding of the issue which is discussed in this case study. The employer

here may look to begin with the issues that surround the case facts. The report will carry an

overall guide of the tax residency of Australia and would accompany a detailed research

regarding the four relevant test that are carried out to determine the residential status.

Answer to question 3:

As the tax advisor, it is difficult to entirely remain dependent on the word of a client

as there are certain situations where the client may not provide us with the relevant

information or may not disclose certain information. As a result of this, there may arise a

conflict of interest between the advisor and the client. The conflict of interest may also create

a harm on the professional relationship. To avoid any conflict of interest it is necessary to

educate the client regarding the importance of disclosing the all or relevant information and

should also make the client aware that non-disclosure of any vital information may potential

harm the outcome of the advice which may ultimately contribute to ambiguity and

uncertainty.

Answer to question 4:

On the basis of the information shared by the client a total of $10,345.83 would be

charged for the advice given to the client. The amount however cannot be considered

reasonable because beside conducting research and drafting of report there are other time

such as setting up meeting and conference adds up to the total time spent on analysing the

case facts.

Answer to question 2:

Yes, I will be comfortable in giving my report to the employer. This is because the

report carries the quality of presentation that would help in gaining an easy understanding of

the client present situation and the content are relevant with the Australian taxation law.

Considering about my strength, I have command over my communication skills and possess

the adequate understanding of the issue which is discussed in this case study. The employer

here may look to begin with the issues that surround the case facts. The report will carry an

overall guide of the tax residency of Australia and would accompany a detailed research

regarding the four relevant test that are carried out to determine the residential status.

Answer to question 3:

As the tax advisor, it is difficult to entirely remain dependent on the word of a client

as there are certain situations where the client may not provide us with the relevant

information or may not disclose certain information. As a result of this, there may arise a

conflict of interest between the advisor and the client. The conflict of interest may also create

a harm on the professional relationship. To avoid any conflict of interest it is necessary to

educate the client regarding the importance of disclosing the all or relevant information and

should also make the client aware that non-disclosure of any vital information may potential

harm the outcome of the advice which may ultimately contribute to ambiguity and

uncertainty.

Answer to question 4:

On the basis of the information shared by the client a total of $10,345.83 would be

charged for the advice given to the client. The amount however cannot be considered

reasonable because beside conducting research and drafting of report there are other time

such as setting up meeting and conference adds up to the total time spent on analysing the

case facts.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Answer to question 5:

Out of 13 I would like to grade 12 marks to my report component because the report

provides an adequate understanding of the legal issues relating to taxation law. The report has

the ability to synthesise the material and constructed a persuasive argument.

Answer to question 5:

Out of 13 I would like to grade 12 marks to my report component because the report

provides an adequate understanding of the legal issues relating to taxation law. The report has

the ability to synthesise the material and constructed a persuasive argument.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Barkoczy, S. (2016). Foundations of taxation law 2016. OUP Catalogue.

Blakelock, S., & King, P. (2017). Taxation law: The advance of ATO data

matching. Proctor, The, 37(6), 18.

Burton, M. (2017). A Review of Judicial References to the Dictum of Jordan CJ, Expressed

in Scott v. Commissioner of Taxation, in Elaborating the Meaning of Income for the

Purposes of the Australian Income Tax. J. Austl. Tax'n, 19, 50.

Fry, M. (2017). Australian taxation of offshore hubs: an examination of the law on the ability

of Australia to tax economic activity in offshore hubs and the position of the

Australian Taxation Office. The APPEA Journal, 57(1), 49-63.

James, K. (2016). The Australian Taxation Office perspective on work-related travel expense

deductions for academics. International Journal of Critical Accounting, 8(5-6), 345-

362.

Miller, A., & Oats, L. (2016). Principles of international taxation. Bloomsbury Publishing.

Morgan, A., & Castelyn, D. (2018). Taxation Education in Secondary Schools. J.

Australasian Tax Tchrs. Ass'n, 13, 307.

Morgan, A., Mortimer, C., & Pinto, D. (2018). A practical introduction to Australian

taxation law 2018. Oxford University Press.

Robin & Barkoczy Woellner (Stephen & Murphy, Shirley Et Al.). (2019). Australian

Taxation Law Select 2019: Legislation and Commentary. OXFORD University Press.

Robin, H. (2019). Australian Taxation Law 2019. Oxford University Press.

Sadiq, K. (2018). Australian Tax Law Cases 2018. Thomson Reuters.

References:

Barkoczy, S. (2016). Foundations of taxation law 2016. OUP Catalogue.

Blakelock, S., & King, P. (2017). Taxation law: The advance of ATO data

matching. Proctor, The, 37(6), 18.

Burton, M. (2017). A Review of Judicial References to the Dictum of Jordan CJ, Expressed

in Scott v. Commissioner of Taxation, in Elaborating the Meaning of Income for the

Purposes of the Australian Income Tax. J. Austl. Tax'n, 19, 50.

Fry, M. (2017). Australian taxation of offshore hubs: an examination of the law on the ability

of Australia to tax economic activity in offshore hubs and the position of the

Australian Taxation Office. The APPEA Journal, 57(1), 49-63.

James, K. (2016). The Australian Taxation Office perspective on work-related travel expense

deductions for academics. International Journal of Critical Accounting, 8(5-6), 345-

362.

Miller, A., & Oats, L. (2016). Principles of international taxation. Bloomsbury Publishing.

Morgan, A., & Castelyn, D. (2018). Taxation Education in Secondary Schools. J.

Australasian Tax Tchrs. Ass'n, 13, 307.

Morgan, A., Mortimer, C., & Pinto, D. (2018). A practical introduction to Australian

taxation law 2018. Oxford University Press.

Robin & Barkoczy Woellner (Stephen & Murphy, Shirley Et Al.). (2019). Australian

Taxation Law Select 2019: Legislation and Commentary. OXFORD University Press.

Robin, H. (2019). Australian Taxation Law 2019. Oxford University Press.

Sadiq, K. (2018). Australian Tax Law Cases 2018. Thomson Reuters.

11TAXATION LAW

Woellner, R., Barkoczy, S., Murphy, S., Evans, C., & Pinto, D. (2016). Australian Taxation

Law 2016. OUP Catalogue.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C., & Pinto, D. (2016). Australian Taxation

Law 2016. OUP Catalogue.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.