Taxation Law Assignment - Holmes Institute T2 2019: Taxation Law

VerifiedAdded on 2022/12/18

|13

|2954

|1

Homework Assignment

AI Summary

This assignment delves into various aspects of taxation law, specifically focusing on capital gains tax (CGT) and depreciation. The first part of the assignment analyzes capital gains from the sale of a family home (pre-CGT asset), a car (personal use asset), business assets (small business CGT concessions), furniture, and paintings (collectibles). It applies relevant sections of the Income Tax Assessment Act 1997 (ITAA 1997) to determine the tax implications of each scenario. The second part examines depreciation deductions for a CNC machine used in a manufacturing business, considering the start time of depreciation, cost base, and relevant legal precedents like Yarmouth v France (1887). The assignment provides a detailed analysis of each situation, referencing relevant legislation and case law to support the conclusions.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to Question 2:................................................................................................................6

References:.................................................................................................................................9

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to Question 2:................................................................................................................6

References:.................................................................................................................................9

2TAXATION LAW

Answer to question 1:

A: The capital gain in relation to family home:

Capital gains tax can be defined as the set of rules that are mainly designed to

compute the capital gains that would be levied for tax under the income tax regime for the

sale of capital asset. Capital gains tax is not viewed as the separate tax (Jones 2015). The

legislation of CGT was introduced during 20th September 1985 with the objective of

imposing tax on gains that are made from the sale of assets purchased on or following the

date. Assets which are purchased before the 20/9/1985 are termed as the Pre-CGT asset and

gains that are originated from the sale of those assets are termed as non-taxable.

Accordingly, under the “sec 118-110, ITAA 1997” the main residence of the taxpayer

comprises of the dwelling that is exempted from capital gains tax (Grudnoff 2016). A

taxpayer is allowed to obtain the partial main residence if they subdivide and sell any part of

the property or they use the house for generating assessable income.

The case study states that Jasmine purchases a home in 1981 for $40,000 which

currently worth’s $650,000 at the time of sale. The house has been the main home of

residence for Jasmine from day when the interest of ownership was formed till the last day of

disposal. The main residence of Jasmine can be classified as the pre-CGT asset because the

house was bought in 1981 which is before the CGT legislation date of 20/9/1985. As a result,

the house will be regarded as the pre-CGT asset and gains made from the sale of home will

be is exempted from CGT,

B: Capital gain from the sale of car:

Under the “subdivision 108-C” personal use assets mainly includes the use of assets

that are completely for private purpose (Yuan 2016). The capital gains that are made from the

Answer to question 1:

A: The capital gain in relation to family home:

Capital gains tax can be defined as the set of rules that are mainly designed to

compute the capital gains that would be levied for tax under the income tax regime for the

sale of capital asset. Capital gains tax is not viewed as the separate tax (Jones 2015). The

legislation of CGT was introduced during 20th September 1985 with the objective of

imposing tax on gains that are made from the sale of assets purchased on or following the

date. Assets which are purchased before the 20/9/1985 are termed as the Pre-CGT asset and

gains that are originated from the sale of those assets are termed as non-taxable.

Accordingly, under the “sec 118-110, ITAA 1997” the main residence of the taxpayer

comprises of the dwelling that is exempted from capital gains tax (Grudnoff 2016). A

taxpayer is allowed to obtain the partial main residence if they subdivide and sell any part of

the property or they use the house for generating assessable income.

The case study states that Jasmine purchases a home in 1981 for $40,000 which

currently worth’s $650,000 at the time of sale. The house has been the main home of

residence for Jasmine from day when the interest of ownership was formed till the last day of

disposal. The main residence of Jasmine can be classified as the pre-CGT asset because the

house was bought in 1981 which is before the CGT legislation date of 20/9/1985. As a result,

the house will be regarded as the pre-CGT asset and gains made from the sale of home will

be is exempted from CGT,

B: Capital gain from the sale of car:

Under the “subdivision 108-C” personal use assets mainly includes the use of assets

that are completely for private purpose (Yuan 2016). The capital gains that are made from the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

sale of personal use assets is ignored if the assets has been acquired for lower than $10,000.

While under subdivision 108-C a loss derived from the personal use asset is completely

ignored. When a sale of assets takes place then there is a “CGT event A1” under “sec 104-10

(1), ITAA 1997”. Under “CGT event A1” a capital gain or loss is made.

A car was purchased by paying a purchase price of $31,000 in 2011 by Jasmine. The

car was eventually sold for $10,000. Under “subdivision 108-C” the car has been classified

as the personal use asset because Jasmine used the asset for her personal purpose.

Furthermore, the sale of car has led to “CGT event A1” under “sec 104-10 (1), ITAA 1997”

(Evans, Minas and Lim 2015). As noted, upon selling the car Jasmine suffers a loss. Under

the “subdivision 108-C”, the loss from sale of personal use car should be disregarded by

Jasmine.

C: Capital gains in relation to sale of business:

In order to qualify for the small business CGT concession, an entity must meet the

basic conditions for all the concessions (Ingles and Stewart 2015). This includes satisfying

any one of the following;

a. The entity was a small business entity with turnover of less than $2 million

b. An individual may not conduct its business but the CGT assets is used in business by

small business entity

c. An individual is the partner in the partnership entity which is a small business and the

CGT asset forms the interest in the partnership or the asset owned is used in

partnership business (Pope 2013).

To assist the small business on meeting the basic conditions, capital gains can be

lowered by applying numerous concessions listed under the “subdivision 152-A, ITAA

1997”. There are four available small business concessions;

sale of personal use assets is ignored if the assets has been acquired for lower than $10,000.

While under subdivision 108-C a loss derived from the personal use asset is completely

ignored. When a sale of assets takes place then there is a “CGT event A1” under “sec 104-10

(1), ITAA 1997”. Under “CGT event A1” a capital gain or loss is made.

A car was purchased by paying a purchase price of $31,000 in 2011 by Jasmine. The

car was eventually sold for $10,000. Under “subdivision 108-C” the car has been classified

as the personal use asset because Jasmine used the asset for her personal purpose.

Furthermore, the sale of car has led to “CGT event A1” under “sec 104-10 (1), ITAA 1997”

(Evans, Minas and Lim 2015). As noted, upon selling the car Jasmine suffers a loss. Under

the “subdivision 108-C”, the loss from sale of personal use car should be disregarded by

Jasmine.

C: Capital gains in relation to sale of business:

In order to qualify for the small business CGT concession, an entity must meet the

basic conditions for all the concessions (Ingles and Stewart 2015). This includes satisfying

any one of the following;

a. The entity was a small business entity with turnover of less than $2 million

b. An individual may not conduct its business but the CGT assets is used in business by

small business entity

c. An individual is the partner in the partnership entity which is a small business and the

CGT asset forms the interest in the partnership or the asset owned is used in

partnership business (Pope 2013).

To assist the small business on meeting the basic conditions, capital gains can be

lowered by applying numerous concessions listed under the “subdivision 152-A, ITAA

1997”. There are four available small business concessions;

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

a. 15-Year exemption under “Subdivision 152-B”

b. Reduction in capital gains by 50% under “Subdivision 152-C”

c. Retirement concessions under “Subdivision 152-D”

d. Rollover relief under “Subdivision 152-E”

The case study provides that Jasmine decides to retire from her small cleaning

business and she is returning back to UK. The business was sold for $125,000 which included

$65,000 for business equipment and $60,000 for goodwill. With regard to basic conditions

listed under “subdivision 152” her aggregate turnover of Jasmine’s business has been below

$2 million with net asset values not exceeding more than $6 million. The assets were active

asset at the time of disposal because they were used in carrying on the business. She will be

allowed to obtain small business concessions (Reinhardt and Steel 2016). Jasmine can obtain

a 15-year CGT exemption under “subdivision 152-C”. The assets were used by Jasmine for

more than 15-years and has also satisfied the basic conditions.

In regard to the business goodwill, a “CGT event C1” occurs when a business is

ceased on the permanent basis. When the business ends up on a permanent basis there is a

loss of business goodwill (Evans and Krever 2015). Similarly, in case of Jasmine, a “CGT

event C1” happened upon the sale of her business goodwill. Jasmine can obtain a 50%

reduction from her CGT under “subdivision 152-C”.

D: Capital gains in relation to sale of furniture:

According to the special rules of “sec 118-10 (3)” capital gains and capital loss

should be ignored when it is noticed that under the first element of the cost base of assets is

lower than $10k (Lignier and Evans 2014). Jasmine sold her furniture for $5,000 which she

purchased for $2,000. As evident the first element cost base of furniture is less than 10k.

a. 15-Year exemption under “Subdivision 152-B”

b. Reduction in capital gains by 50% under “Subdivision 152-C”

c. Retirement concessions under “Subdivision 152-D”

d. Rollover relief under “Subdivision 152-E”

The case study provides that Jasmine decides to retire from her small cleaning

business and she is returning back to UK. The business was sold for $125,000 which included

$65,000 for business equipment and $60,000 for goodwill. With regard to basic conditions

listed under “subdivision 152” her aggregate turnover of Jasmine’s business has been below

$2 million with net asset values not exceeding more than $6 million. The assets were active

asset at the time of disposal because they were used in carrying on the business. She will be

allowed to obtain small business concessions (Reinhardt and Steel 2016). Jasmine can obtain

a 15-year CGT exemption under “subdivision 152-C”. The assets were used by Jasmine for

more than 15-years and has also satisfied the basic conditions.

In regard to the business goodwill, a “CGT event C1” occurs when a business is

ceased on the permanent basis. When the business ends up on a permanent basis there is a

loss of business goodwill (Evans and Krever 2015). Similarly, in case of Jasmine, a “CGT

event C1” happened upon the sale of her business goodwill. Jasmine can obtain a 50%

reduction from her CGT under “subdivision 152-C”.

D: Capital gains in relation to sale of furniture:

According to the special rules of “sec 118-10 (3)” capital gains and capital loss

should be ignored when it is noticed that under the first element of the cost base of assets is

lower than $10k (Lignier and Evans 2014). Jasmine sold her furniture for $5,000 which she

purchased for $2,000. As evident the first element cost base of furniture is less than 10k.

5TAXATION LAW

Hence, under the “sec 118-10 (3)” Jasmine must disregard the capital gains from the

furniture in this context.

E: Capital gains on selling the paintings:

As per the “sec 108-10 (2), ITAA 1997” collectables include;

a. Artwork, jewellery, coin or antiques

b. A rare folio, books or manuscripts

c. Postage stamps

These assets are usually kept for the personal usage of the taxpayer. As per “sec 108-10

(1), ITAA 1997” capital gains and loss should be ignored when the first element of

collectibles cost base is lower than $500. Jasmine sold several paintings for $35,000 which

she has bought for $500. Paintings held by Jasmine is treated as collectibles under “sec 108-

10 (2), ITAA 1997”. “CGT event A1” happened when the paintings were sold by Jasmine. As

the cost paintings is $500 it fails to meet the first element of collectibles cost base

collectibles. The capital gains made from selling her painting is ignored in this context.

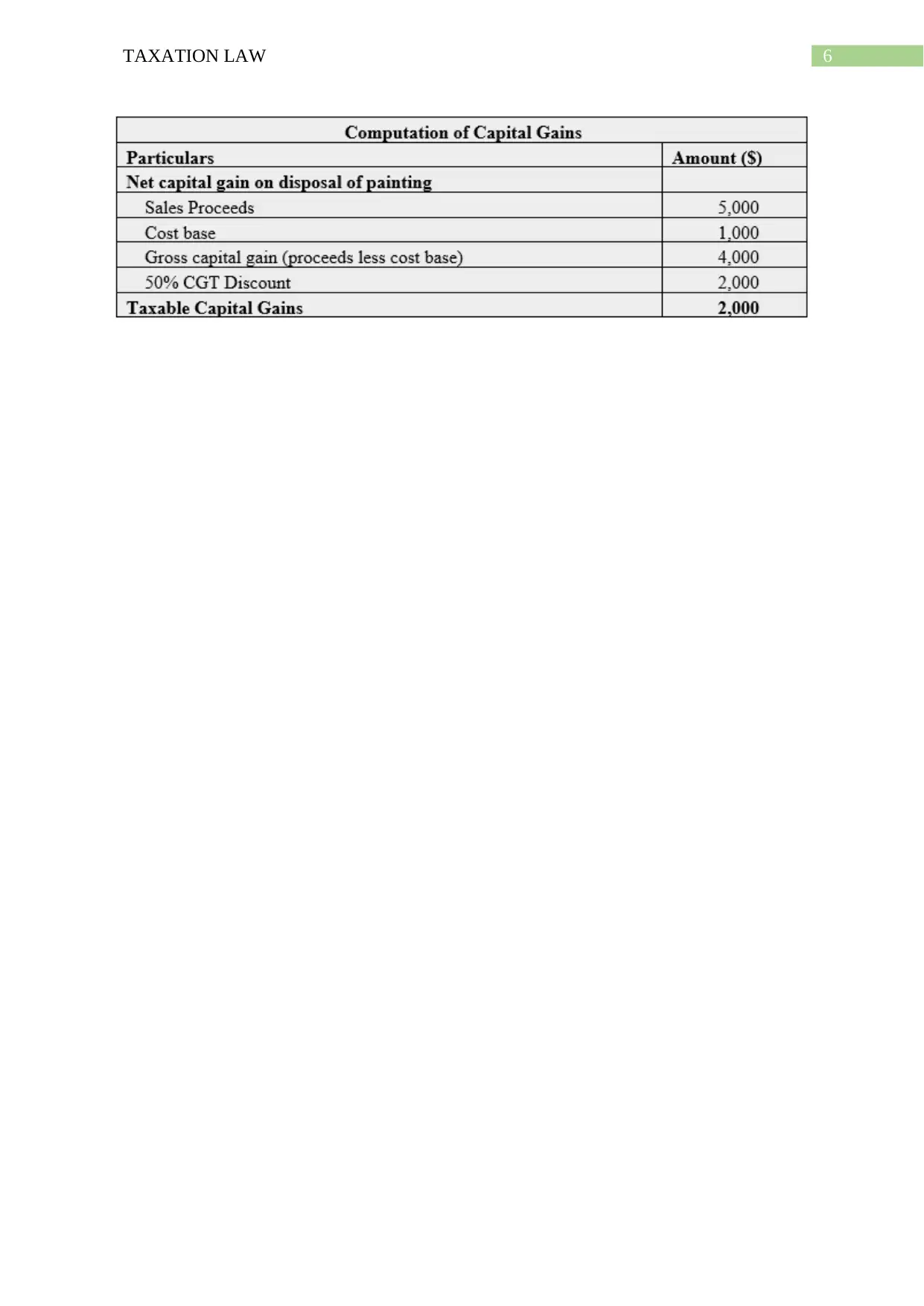

While one of Jasmine paintings cost $1,000 which was purchased directly from the

artist and was eventually sold for $5,000. The sale of painting has yielded capital gains for

Jasmine and the first element of cost base of collectible is also satisfied in this case. The

capital gains made will be considered for tax however Jasmine can avail 50% CGT discount

as it is presumed that the paintings were under the ownership for more than 12 months.

Hence, under the “sec 118-10 (3)” Jasmine must disregard the capital gains from the

furniture in this context.

E: Capital gains on selling the paintings:

As per the “sec 108-10 (2), ITAA 1997” collectables include;

a. Artwork, jewellery, coin or antiques

b. A rare folio, books or manuscripts

c. Postage stamps

These assets are usually kept for the personal usage of the taxpayer. As per “sec 108-10

(1), ITAA 1997” capital gains and loss should be ignored when the first element of

collectibles cost base is lower than $500. Jasmine sold several paintings for $35,000 which

she has bought for $500. Paintings held by Jasmine is treated as collectibles under “sec 108-

10 (2), ITAA 1997”. “CGT event A1” happened when the paintings were sold by Jasmine. As

the cost paintings is $500 it fails to meet the first element of collectibles cost base

collectibles. The capital gains made from selling her painting is ignored in this context.

While one of Jasmine paintings cost $1,000 which was purchased directly from the

artist and was eventually sold for $5,000. The sale of painting has yielded capital gains for

Jasmine and the first element of cost base of collectible is also satisfied in this case. The

capital gains made will be considered for tax however Jasmine can avail 50% CGT discount

as it is presumed that the paintings were under the ownership for more than 12 months.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Answer to Question 2:

Issues:

Is the taxpayer may be allowed to obtain depreciation deduction for the decline in the

value of the depreciating asset that is held under “s 40-25, ITA Act 1997”?

Rule:

A taxpayer might be allowed under the provision of “s 40-25, ITA Act 1997” to get a

depreciation deduction for the “depreciating asset” equal to the decline in value which is

held for producing income. While “s 40-30 (1), ITA Act 1997” defines the “depreciating

asset” as something that has restricted effective life and they can be reasonably anticipated to

fall in terms of value based on the usage of asset (Marsden, Sadiq and Wilkins 2013). For a

taxpayer to get the deduction in “s 40-25, ITA Act 1997” for the “depreciating asset” it

becomes obligatory to know when the taxpayer has held the depreciating asset and

ascertaining the deduction is equivalent to the “decline in value” while considering the

income tax purpose. The law court in “Yarmouth v France (1887) 19 QBD 647” defined the

meaning of plant by stating that whatever the type of apparatus that a business uses for

conducting its activities (Woellner et al., 2016).

A tax payer under the “s 40-25 (2), ITA Act 1997” is allowed to get the deduction for

the “depreciating asset” that is completely used for assessable purpose (Sørensen and

Johnson 2015). Usually, an assessable purpose is only existent where the asset is used by

taxpayer for generating chargeable business earnings under “s40-25 (7), ITA Act 1997”.

An asset that are depreciating in nature held under the ownership of taxpayer begins

to fall in terms of value when it start time begins under “s 40-60 (1), ITA Act 1997”. For a

Answer to Question 2:

Issues:

Is the taxpayer may be allowed to obtain depreciation deduction for the decline in the

value of the depreciating asset that is held under “s 40-25, ITA Act 1997”?

Rule:

A taxpayer might be allowed under the provision of “s 40-25, ITA Act 1997” to get a

depreciation deduction for the “depreciating asset” equal to the decline in value which is

held for producing income. While “s 40-30 (1), ITA Act 1997” defines the “depreciating

asset” as something that has restricted effective life and they can be reasonably anticipated to

fall in terms of value based on the usage of asset (Marsden, Sadiq and Wilkins 2013). For a

taxpayer to get the deduction in “s 40-25, ITA Act 1997” for the “depreciating asset” it

becomes obligatory to know when the taxpayer has held the depreciating asset and

ascertaining the deduction is equivalent to the “decline in value” while considering the

income tax purpose. The law court in “Yarmouth v France (1887) 19 QBD 647” defined the

meaning of plant by stating that whatever the type of apparatus that a business uses for

conducting its activities (Woellner et al., 2016).

A tax payer under the “s 40-25 (2), ITA Act 1997” is allowed to get the deduction for

the “depreciating asset” that is completely used for assessable purpose (Sørensen and

Johnson 2015). Usually, an assessable purpose is only existent where the asset is used by

taxpayer for generating chargeable business earnings under “s40-25 (7), ITA Act 1997”.

An asset that are depreciating in nature held under the ownership of taxpayer begins

to fall in terms of value when it start time begins under “s 40-60 (1), ITA Act 1997”. For a

8TAXATION LAW

depreciating asset the start time happens when the asset is first utilized by taxpayer. It also

includes under “s 40-60 (2), ITAA 1997” whether the assets has been ready for utilization.

As per “Subdivision 40-C” in order to depreciate the depreciating asset it is necessary

to find out the cost of the asset (Ingles and Stewart 2018). As a general sense, the price paid

for purchase would form the part of cost base but other incidental cost such as installation and

delivery would be also included under the cost base. In “Broken Hill Co Pty v FCT (1970)”

minor cost incurred for re-arranging, removing or accommodating the new plant is counted

under the cost base of the “depreciating asset”.

“Sec 40-175, ITAA 1997” classifies cost of depreciating asset under two elements.

“Sec 40-180, ITAA 1997” states that the “first element” would generally include the price

paid for purchasing the asset (Kenny, Blissenden and Villios 2018). While “sec 40-190,

ITAA 1997” is associated with the “second element”, which comprises of deliver cost,

installation cost and capital improvement cost of the asset.

Application:

John is carrying on the business of motor vehicle parts and accessories manufacturing

company. He purchases a CNC machine from Germany on 1st November 2014 by paying a

purchase price of $300,000. The CNC machine will be classified under “s 40-30 (1), ITA Act

1997” as “depreciating asset” which is reasonably anticipated to fall in terms of value based

on the usage of asset. Citing “Yarmouth v France (1887) 19 QBD 647” the machine has

been bought by John exclusively for the taxable purpose or for carrying on his business

activities (Ingles and Stewart 2018). Under “s 40-25 (2), ITA Act 1997” John is allowed to

get the deduction for the “decline in value” of the CNC machine that is completely used for

assessable purpose.

depreciating asset the start time happens when the asset is first utilized by taxpayer. It also

includes under “s 40-60 (2), ITAA 1997” whether the assets has been ready for utilization.

As per “Subdivision 40-C” in order to depreciate the depreciating asset it is necessary

to find out the cost of the asset (Ingles and Stewart 2018). As a general sense, the price paid

for purchase would form the part of cost base but other incidental cost such as installation and

delivery would be also included under the cost base. In “Broken Hill Co Pty v FCT (1970)”

minor cost incurred for re-arranging, removing or accommodating the new plant is counted

under the cost base of the “depreciating asset”.

“Sec 40-175, ITAA 1997” classifies cost of depreciating asset under two elements.

“Sec 40-180, ITAA 1997” states that the “first element” would generally include the price

paid for purchasing the asset (Kenny, Blissenden and Villios 2018). While “sec 40-190,

ITAA 1997” is associated with the “second element”, which comprises of deliver cost,

installation cost and capital improvement cost of the asset.

Application:

John is carrying on the business of motor vehicle parts and accessories manufacturing

company. He purchases a CNC machine from Germany on 1st November 2014 by paying a

purchase price of $300,000. The CNC machine will be classified under “s 40-30 (1), ITA Act

1997” as “depreciating asset” which is reasonably anticipated to fall in terms of value based

on the usage of asset. Citing “Yarmouth v France (1887) 19 QBD 647” the machine has

been bought by John exclusively for the taxable purpose or for carrying on his business

activities (Ingles and Stewart 2018). Under “s 40-25 (2), ITA Act 1997” John is allowed to

get the deduction for the “decline in value” of the CNC machine that is completely used for

assessable purpose.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Under the “s 40-60 (1), ITA Act 1997” the start time of CNC machine for the

“decline in value” is from 15th January onwards. Citing “s 40-60 (2), ITAA 1997” the assets

has been installed as ready for utilization by John from 15th January onwards.

Later it is noticed that John occurred several cost both prior to installation and

following the installation of the CNC machine. Referring to “Subdivision 40-C” to

depreciate the CNC machine or to claim the “decline in value” it is necessary to find out the

cost of the asset. Citing the example of “Broken Hill Co Pty v FCT (1970)” the cost base of

CNC machine would also include the minor incidental costs under the cost base element to

ascertain the total cost base of the asset (Kenny, Blissenden and Villios 2018).

Referring to “Sec 40-180, ITAA 1997” the “first element” would generally include

the price paid for purchasing the CNC machine. While citing “sec 40-190, ITAA 1997” under

the “second element” of the CNC machine the cost base would include the installation cost

of machine, capital improvement cost of machine such as adding the guiding rod for making

it more effective. These costs will be included in computing the capital allowances of the

CNC machine.

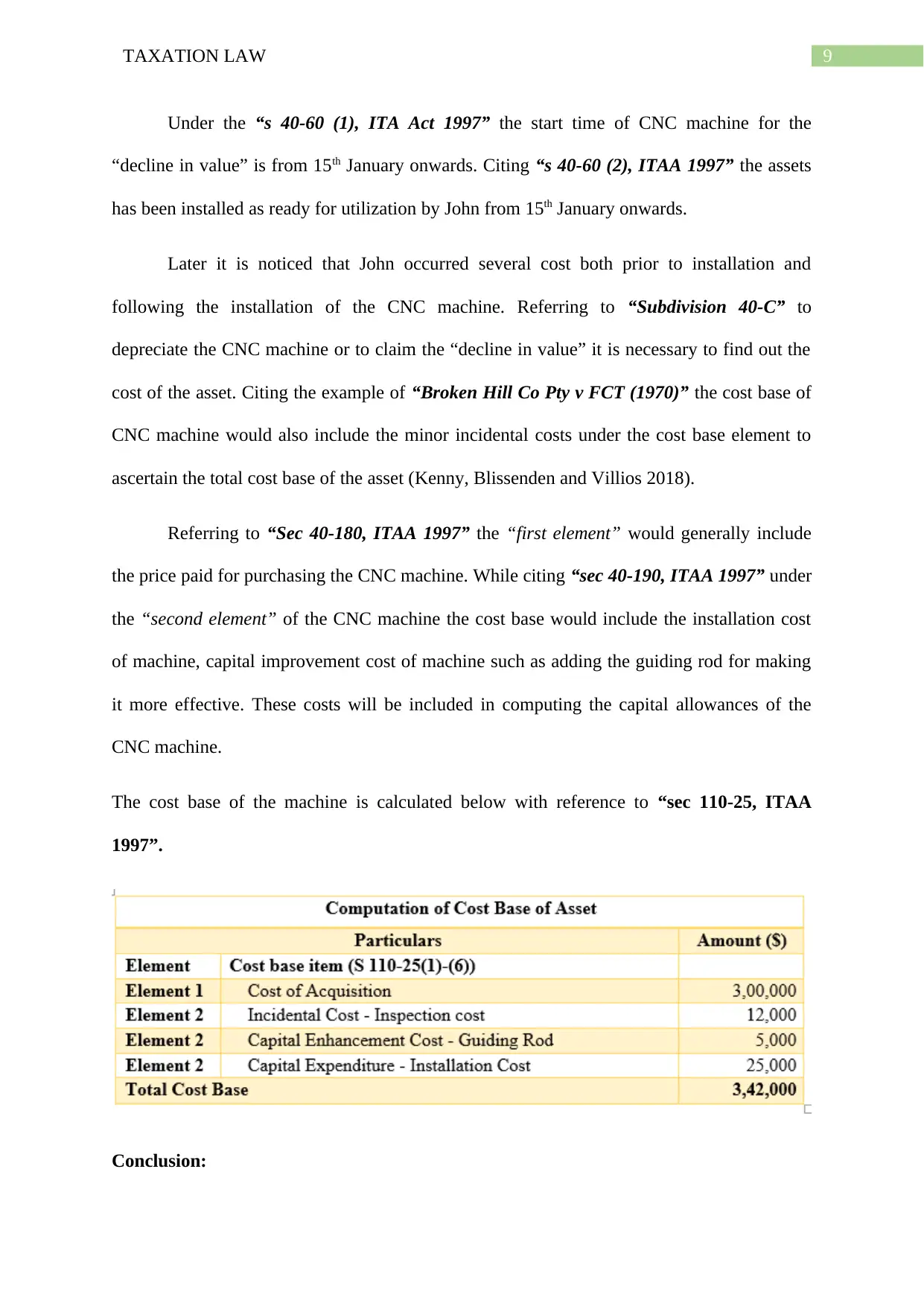

The cost base of the machine is calculated below with reference to “sec 110-25, ITAA

1997”.

Conclusion:

Under the “s 40-60 (1), ITA Act 1997” the start time of CNC machine for the

“decline in value” is from 15th January onwards. Citing “s 40-60 (2), ITAA 1997” the assets

has been installed as ready for utilization by John from 15th January onwards.

Later it is noticed that John occurred several cost both prior to installation and

following the installation of the CNC machine. Referring to “Subdivision 40-C” to

depreciate the CNC machine or to claim the “decline in value” it is necessary to find out the

cost of the asset. Citing the example of “Broken Hill Co Pty v FCT (1970)” the cost base of

CNC machine would also include the minor incidental costs under the cost base element to

ascertain the total cost base of the asset (Kenny, Blissenden and Villios 2018).

Referring to “Sec 40-180, ITAA 1997” the “first element” would generally include

the price paid for purchasing the CNC machine. While citing “sec 40-190, ITAA 1997” under

the “second element” of the CNC machine the cost base would include the installation cost

of machine, capital improvement cost of machine such as adding the guiding rod for making

it more effective. These costs will be included in computing the capital allowances of the

CNC machine.

The cost base of the machine is calculated below with reference to “sec 110-25, ITAA

1997”.

Conclusion:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

The analysis performed above can be concluded by stating that a decline in value of

the CNC machine is allowable to be claimed as depreciation by John under “s 40-25, ITA

Act 1997”. The machine was exclusively bought by John for taxable purpose for use in

derivation of business income.

The analysis performed above can be concluded by stating that a decline in value of

the CNC machine is allowable to be claimed as depreciation by John under “s 40-25, ITA

Act 1997”. The machine was exclusively bought by John for taxable purpose for use in

derivation of business income.

11TAXATION LAW

References:

Evans, C. and Krever, R., 2015. Tax reviews in Australia: a short primer. Tax Reviews in

Australia: A Short Primer (July 12, 2015). Australian Business Tax Reform in Retrospect and

Prospect, pp.4-11.

Evans, C., Minas, J. and Lim, Y., 2015. Taxing personal capital gains in Australia: An

alternative way forward. Austl. Tax F., 30, p.735.

Grudnoff, M., 2016. CGT main residence exemption. Why removing the tax concession for

homes over $2 million is good for the budget, the economy and fairness. Policy Brief.

Australia Institute, Canberra.

Ingles, D. and Stewart, M., 2015. Superannuation tax concessions and the age pension: a

principled approach to savings taxation. Tax and Transfer Policy Institute-Working Paper, 7.

Ingles, D. and Stewart, M., 2018, October. Australia's company tax: Options for fiscally

sustainable reform. In Australian Tax Forum (Vol. 33, No. 1).

Jones, S., 2015. Your primary residence and CGT: capital gains tax. Tax Breaks

Newsletter, 2015(351), pp.5-6.

Kenny, P., Blissenden, M. and Villios, S., 2018. Australian Tax 2018.

Lignier, P. and Evans, C., 2014, August. The rise and rise of tax compliance costs for the

small business sector in Australia. In Australian Tax Forum (Vol. 27, No. 3, pp. 615-672).

Marsden, S., Sadiq, K. and Wilkins, T., 2013. Small business entity tax concessions: Through

the eyes of the practitioner. Revenue Law Journal, 22(1), p.6731.

Pope, J., 2013. The compliance costs of taxation in Australia and tax simplification: The

issues. Australian Journal of Management, 18(1), pp.69-89.

References:

Evans, C. and Krever, R., 2015. Tax reviews in Australia: a short primer. Tax Reviews in

Australia: A Short Primer (July 12, 2015). Australian Business Tax Reform in Retrospect and

Prospect, pp.4-11.

Evans, C., Minas, J. and Lim, Y., 2015. Taxing personal capital gains in Australia: An

alternative way forward. Austl. Tax F., 30, p.735.

Grudnoff, M., 2016. CGT main residence exemption. Why removing the tax concession for

homes over $2 million is good for the budget, the economy and fairness. Policy Brief.

Australia Institute, Canberra.

Ingles, D. and Stewart, M., 2015. Superannuation tax concessions and the age pension: a

principled approach to savings taxation. Tax and Transfer Policy Institute-Working Paper, 7.

Ingles, D. and Stewart, M., 2018, October. Australia's company tax: Options for fiscally

sustainable reform. In Australian Tax Forum (Vol. 33, No. 1).

Jones, S., 2015. Your primary residence and CGT: capital gains tax. Tax Breaks

Newsletter, 2015(351), pp.5-6.

Kenny, P., Blissenden, M. and Villios, S., 2018. Australian Tax 2018.

Lignier, P. and Evans, C., 2014, August. The rise and rise of tax compliance costs for the

small business sector in Australia. In Australian Tax Forum (Vol. 27, No. 3, pp. 615-672).

Marsden, S., Sadiq, K. and Wilkins, T., 2013. Small business entity tax concessions: Through

the eyes of the practitioner. Revenue Law Journal, 22(1), p.6731.

Pope, J., 2013. The compliance costs of taxation in Australia and tax simplification: The

issues. Australian Journal of Management, 18(1), pp.69-89.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.