Taxation Law: FBT and Capital Gains Tax Analysis - HA3042 T1 2019

VerifiedAdded on 2023/03/30

|10

|2051

|167

Homework Assignment

AI Summary

This assignment delves into Taxation Law, focusing on Fringe Benefit Tax (FBT) and Capital Gains Tax (CGT). It analyzes a case study involving Lucinda's car fringe benefit, comparing the Statutory Formula Method and Operating Cost Method for FBT calculation. The assignment also examines Daniel's Capital Gains Tax implications from selling a house, artwork, yacht, and shares, determining net capital gain and tax liability. The analysis includes calculations, relevant sections from the Fringe Benefit Tax Assessment Act 1986 (Cth), and considerations for discounts, losses, and assessable income, providing a comprehensive overview of FBT and CGT principles.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Author Note

Taxation Law

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Answer No.1:

Issue:

FBT or the Fringe Benefit Tax is the benefit taxable that every employer is required to

supply to his employees in connection to the employment relation. In the present case study,

Lucinda is given car as a fringe benefit by his employer Spiceco pty Ltd. Here the issue to

determine how car will be affecting FBT for Spiceco. The determination is processed by way

of two types of methods called the Operating Cost method and the statutory formula method.

Rules for Fringe Benefit:

The assessment of FBT is provided in the provisions of the rules enumerated in the

Fringe Benefit Tax Assessment Act 1986 (Cth). As per sec. 136(1), the fringe benefit is given

and it has two aspects mainly a positive aspect and a negative aspect. In the event where the

benefit is granted by the employer or an associate to his employee or associate in a financial

year, it can be said to be a fringe benefit as per positive aspect. On the other hand, the

negative aspect regards that the Fringe benefit should not fall from Para F to Para S of the

said section.

Further, FB can be classified into Type 1 and Type 2 benefits. Type 1 benefits

comprises of benefits in which the cost is including GST. The value for FBT in the FY 2018-

2019 is 2.082*47% on these types of benefits. There are several types of fringe benefits and

Car Fringe benefits is one of the types. The Car Fringe Benefits is provided under sec. 7 of

FBTAA. It states that a car fringe benefit occurs when an employer provides a car to his

employee for using it personally. The calculations for Fringe benefit on car is given under

sec. 9(1) and sec. 10(2) where the statutory formula method and the Operation Cost method

are given respectively. It is the statutory formula method that is being generally used by the

Answer No.1:

Issue:

FBT or the Fringe Benefit Tax is the benefit taxable that every employer is required to

supply to his employees in connection to the employment relation. In the present case study,

Lucinda is given car as a fringe benefit by his employer Spiceco pty Ltd. Here the issue to

determine how car will be affecting FBT for Spiceco. The determination is processed by way

of two types of methods called the Operating Cost method and the statutory formula method.

Rules for Fringe Benefit:

The assessment of FBT is provided in the provisions of the rules enumerated in the

Fringe Benefit Tax Assessment Act 1986 (Cth). As per sec. 136(1), the fringe benefit is given

and it has two aspects mainly a positive aspect and a negative aspect. In the event where the

benefit is granted by the employer or an associate to his employee or associate in a financial

year, it can be said to be a fringe benefit as per positive aspect. On the other hand, the

negative aspect regards that the Fringe benefit should not fall from Para F to Para S of the

said section.

Further, FB can be classified into Type 1 and Type 2 benefits. Type 1 benefits

comprises of benefits in which the cost is including GST. The value for FBT in the FY 2018-

2019 is 2.082*47% on these types of benefits. There are several types of fringe benefits and

Car Fringe benefits is one of the types. The Car Fringe Benefits is provided under sec. 7 of

FBTAA. It states that a car fringe benefit occurs when an employer provides a car to his

employee for using it personally. The calculations for Fringe benefit on car is given under

sec. 9(1) and sec. 10(2) where the statutory formula method and the Operation Cost method

are given respectively. It is the statutory formula method that is being generally used by the

2TAXATION LAW

employer to determine FBT but it is in the discretion of the employer to use the Operating

Cost Method that decreases the taxable valuation of FB.

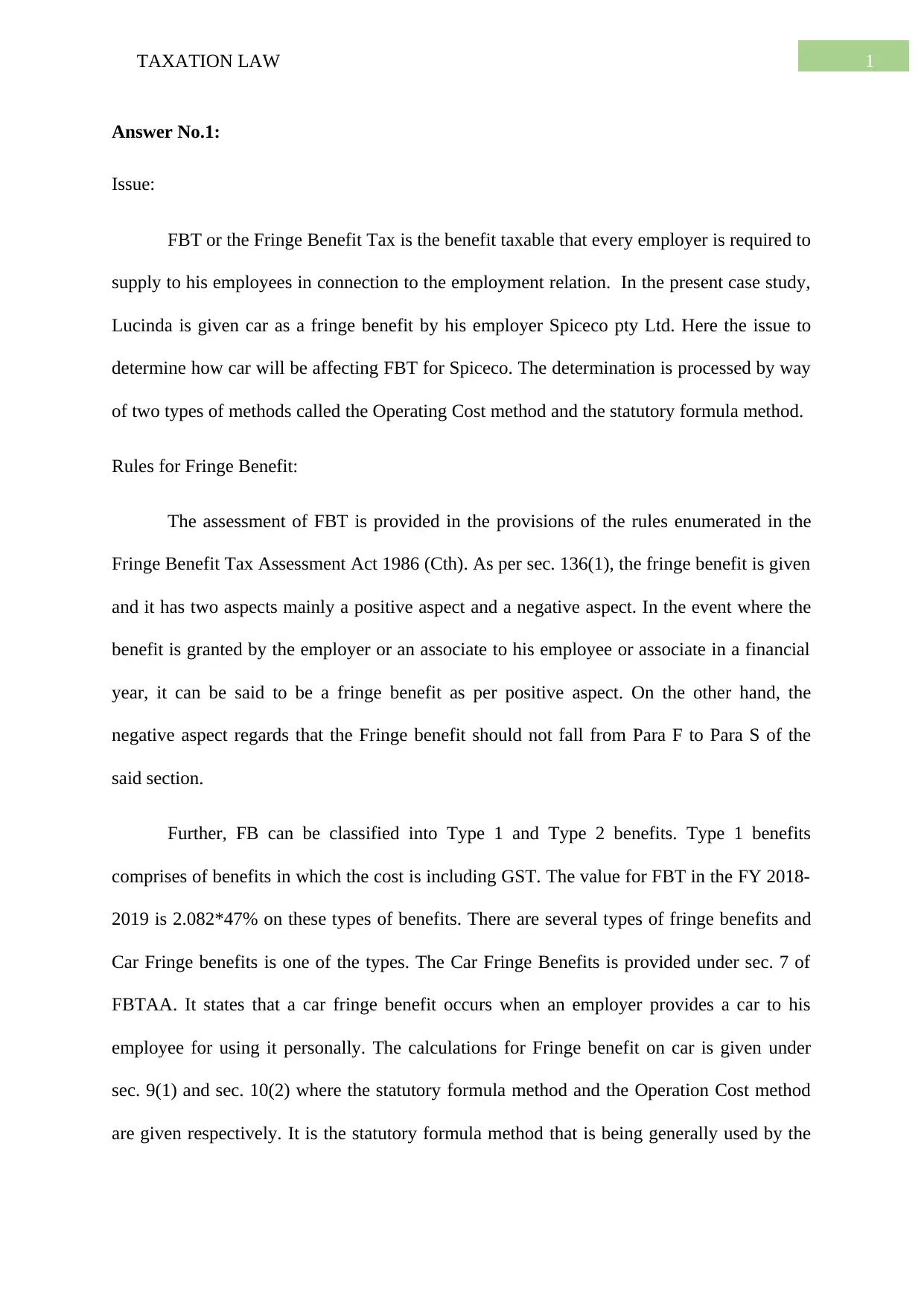

FBT can be calculated by using the Statutory Formula Method by employing the

following formula as given under sec9 (1);

0.2 is the flat rate which SFM uses. The car base value of the car is the car’s purchase

price. But, this base value can be decreased by the amount equal to any contribution made by

the employee to its purchase price. This has been provided in the Taxation Ruling TR 2011/3.

R refers to the payment if any made by the employee for the car as the operating cost like the

fuel charges, insurance payment and others. The cost operating method employs the

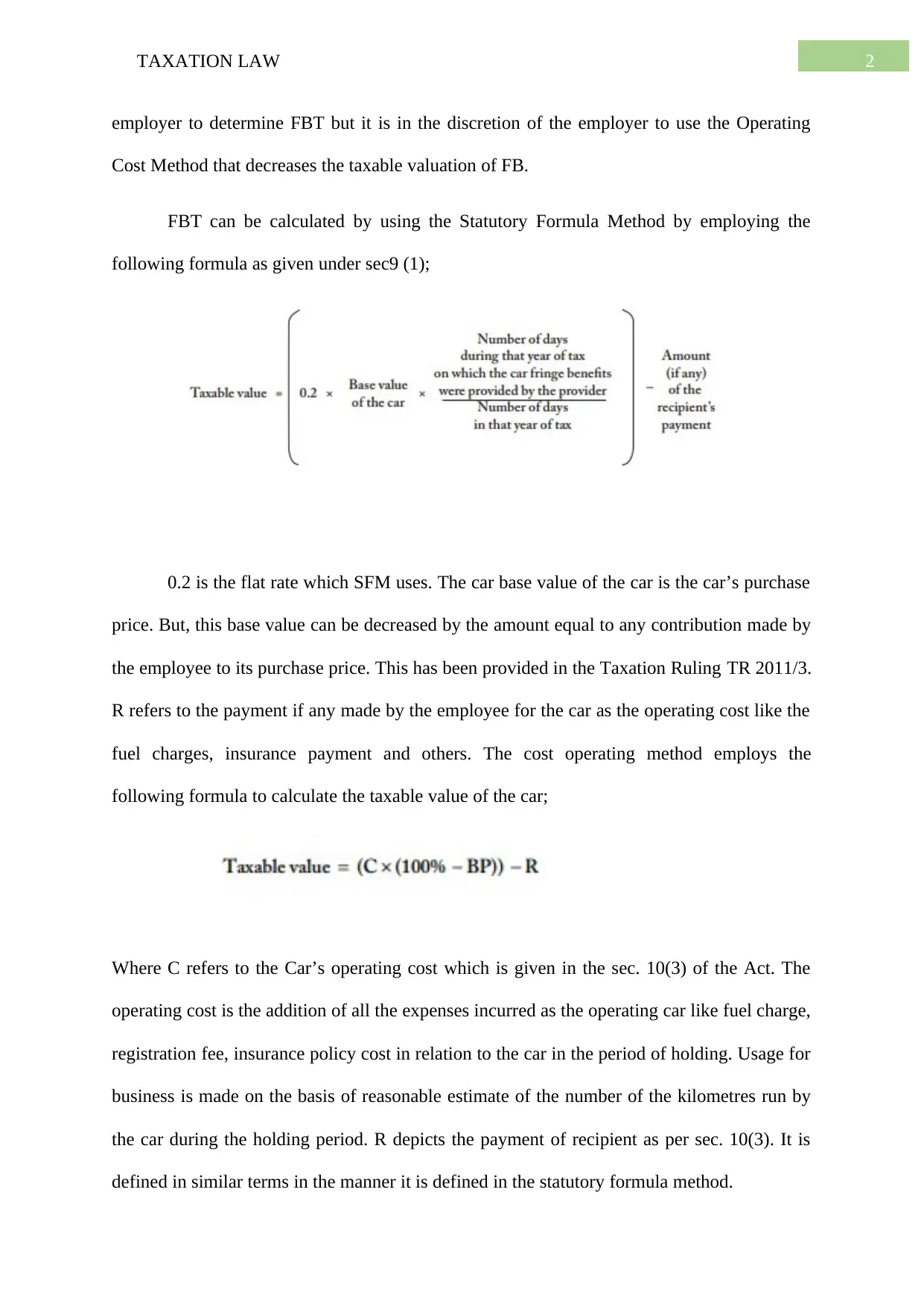

following formula to calculate the taxable value of the car;

Where C refers to the Car’s operating cost which is given in the sec. 10(3) of the Act. The

operating cost is the addition of all the expenses incurred as the operating car like fuel charge,

registration fee, insurance policy cost in relation to the car in the period of holding. Usage for

business is made on the basis of reasonable estimate of the number of the kilometres run by

the car during the holding period. R depicts the payment of recipient as per sec. 10(3). It is

defined in similar terms in the manner it is defined in the statutory formula method.

employer to determine FBT but it is in the discretion of the employer to use the Operating

Cost Method that decreases the taxable valuation of FB.

FBT can be calculated by using the Statutory Formula Method by employing the

following formula as given under sec9 (1);

0.2 is the flat rate which SFM uses. The car base value of the car is the car’s purchase

price. But, this base value can be decreased by the amount equal to any contribution made by

the employee to its purchase price. This has been provided in the Taxation Ruling TR 2011/3.

R refers to the payment if any made by the employee for the car as the operating cost like the

fuel charges, insurance payment and others. The cost operating method employs the

following formula to calculate the taxable value of the car;

Where C refers to the Car’s operating cost which is given in the sec. 10(3) of the Act. The

operating cost is the addition of all the expenses incurred as the operating car like fuel charge,

registration fee, insurance policy cost in relation to the car in the period of holding. Usage for

business is made on the basis of reasonable estimate of the number of the kilometres run by

the car during the holding period. R depicts the payment of recipient as per sec. 10(3). It is

defined in similar terms in the manner it is defined in the statutory formula method.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Application:

Calculation as per the Statutory Formula Method

Base value=18000-1000=17000 as Lucinda had contributed 1000 to the purchase

price. Further, the car is being used throughout the year. Lucinda had made no contribution to

the recipient’s payment.

0.2*17000*365/365-0 = 3400

Operating Cost Method

For calculating the value of FB of the car as per the Operating cost method, input

interest and deemed depreciation are to be calculated. Deemed depreciation for a car in the

Financial Year of 2018- 2019 FBT is calculated by using the formula given in sec. 11(1)

where the interest rate of 25% is applied for a car purchased after 10th May 2006. Hence,

deemed depreciation= (17000*25%*365)/365= 4250.

Imputed interest for a car for the 2018- 2019 FBT year can be calculated by

employing the formula given in sec. 11(2) and the interest rate applied is 5.20 % (TD 2018/2)

for cars purchased after 10 th May 2006. Deemed interest= (17000*5.20 % * 365)/ 365= 884

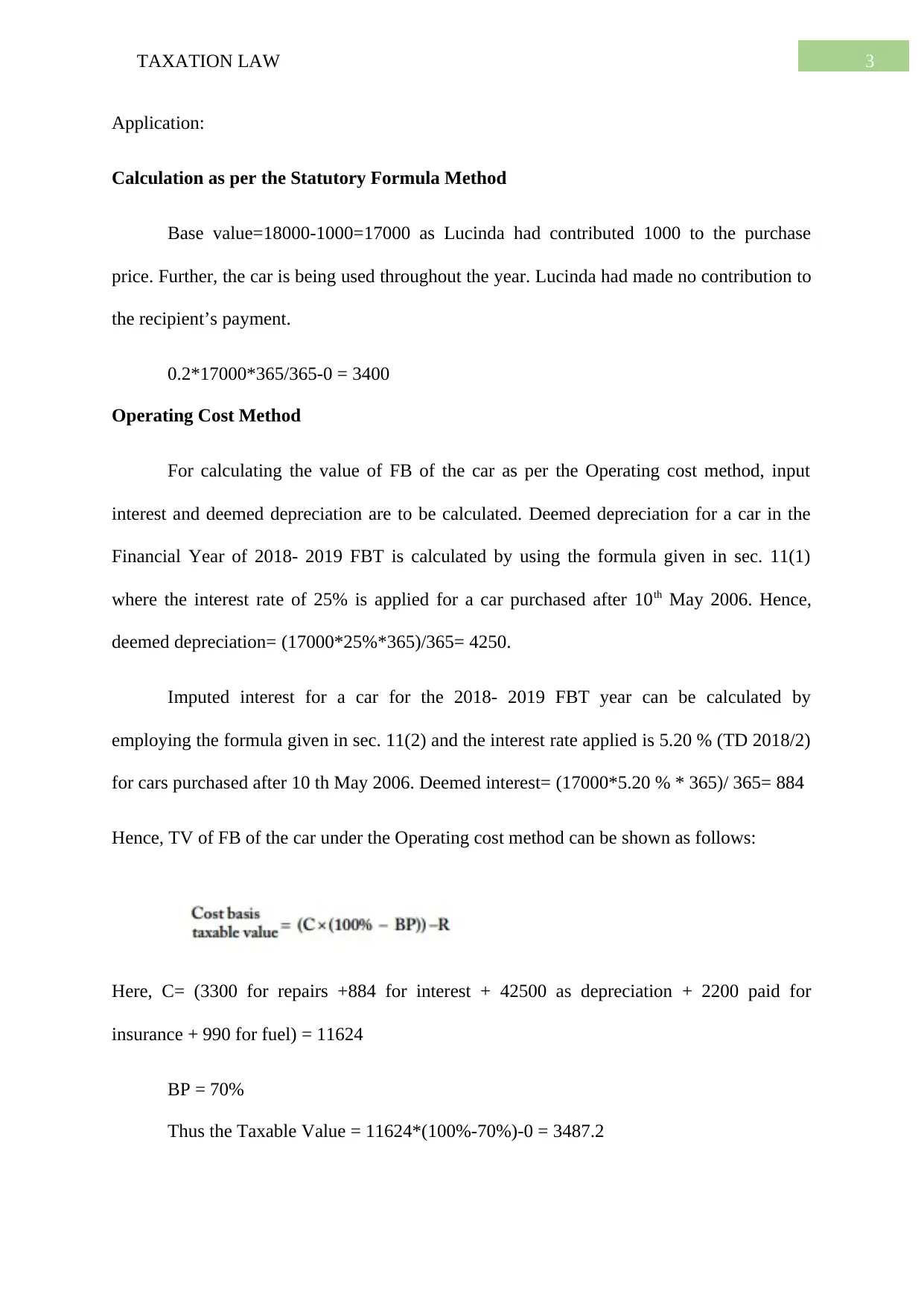

Hence, TV of FB of the car under the Operating cost method can be shown as follows:

Here, C= (3300 for repairs +884 for interest + 42500 as depreciation + 2200 paid for

insurance + 990 for fuel) = 11624

BP = 70%

Thus the Taxable Value = 11624*(100%-70%)-0 = 3487.2

Application:

Calculation as per the Statutory Formula Method

Base value=18000-1000=17000 as Lucinda had contributed 1000 to the purchase

price. Further, the car is being used throughout the year. Lucinda had made no contribution to

the recipient’s payment.

0.2*17000*365/365-0 = 3400

Operating Cost Method

For calculating the value of FB of the car as per the Operating cost method, input

interest and deemed depreciation are to be calculated. Deemed depreciation for a car in the

Financial Year of 2018- 2019 FBT is calculated by using the formula given in sec. 11(1)

where the interest rate of 25% is applied for a car purchased after 10th May 2006. Hence,

deemed depreciation= (17000*25%*365)/365= 4250.

Imputed interest for a car for the 2018- 2019 FBT year can be calculated by

employing the formula given in sec. 11(2) and the interest rate applied is 5.20 % (TD 2018/2)

for cars purchased after 10 th May 2006. Deemed interest= (17000*5.20 % * 365)/ 365= 884

Hence, TV of FB of the car under the Operating cost method can be shown as follows:

Here, C= (3300 for repairs +884 for interest + 42500 as depreciation + 2200 paid for

insurance + 990 for fuel) = 11624

BP = 70%

Thus the Taxable Value = 11624*(100%-70%)-0 = 3487.2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Hence, it is seen the Taxable Value as per statutory formula method is less, hence it is a better

method.

Net Fringe Benefit Tax as per this method = 3487.2*2.0802*47% =3409.41.

Answer 2 (a)

Analysis for Capital Gain Tax for Daniel

House located at Doncaster

Capital Gain Asset- Under the provisions enumerated under section 108.5, capital gain assets

means property. The assets are required to be owned after 20th September 1985. The house is

situated at Doncaster and is acquired after this date and hence it is a CGT asset.

Capital Gain Event: List of CGE is given under sec. 104.5. The most common of these is

event A1 given under s. 104.10 (1) and is triggered when CGA is being sold or gifted.

CGE A1 Timing – CGE A1 occurs on the day when asset is disposed off as per sec. 104.10

(2). Additionally, the time must be the date when contract of sale effected as found in

decision of McDonalds v FCT (1998). Hence, A1 of the house occurs on Saturday, 29th of

June 2019.

CG or CL = CP-CB

CP or the Capital proceeds is the amount the tax payer has already received or may get out of

the sale in connection with sec. 116.20. In the instant case, for the house, it appears to be

865,000 $. It has been modified or deducted by the fee of agent of sale of 15000 $ and results

into 850000 $.

Cost Base or CB is the value for buying and maintaining the assets as given as per section

110.25(1). It consists of five elements.

Element 1 as given in section 110.25 (2) denotes the price paid to acquire the house is 70000

$.

Discount - if a taxpayer is not a company and has acquired the asset before 20th September

1999 and hold it for minimum 12 months and discount can be claimed under section 115.

Total Capital Gain= (850000- 70000)- 50 % which amounts to 390000. But since, the house

is used a place of residence, the total CGT will be excluded according to section 118. 10.

Hence, it is seen the Taxable Value as per statutory formula method is less, hence it is a better

method.

Net Fringe Benefit Tax as per this method = 3487.2*2.0802*47% =3409.41.

Answer 2 (a)

Analysis for Capital Gain Tax for Daniel

House located at Doncaster

Capital Gain Asset- Under the provisions enumerated under section 108.5, capital gain assets

means property. The assets are required to be owned after 20th September 1985. The house is

situated at Doncaster and is acquired after this date and hence it is a CGT asset.

Capital Gain Event: List of CGE is given under sec. 104.5. The most common of these is

event A1 given under s. 104.10 (1) and is triggered when CGA is being sold or gifted.

CGE A1 Timing – CGE A1 occurs on the day when asset is disposed off as per sec. 104.10

(2). Additionally, the time must be the date when contract of sale effected as found in

decision of McDonalds v FCT (1998). Hence, A1 of the house occurs on Saturday, 29th of

June 2019.

CG or CL = CP-CB

CP or the Capital proceeds is the amount the tax payer has already received or may get out of

the sale in connection with sec. 116.20. In the instant case, for the house, it appears to be

865,000 $. It has been modified or deducted by the fee of agent of sale of 15000 $ and results

into 850000 $.

Cost Base or CB is the value for buying and maintaining the assets as given as per section

110.25(1). It consists of five elements.

Element 1 as given in section 110.25 (2) denotes the price paid to acquire the house is 70000

$.

Discount - if a taxpayer is not a company and has acquired the asset before 20th September

1999 and hold it for minimum 12 months and discount can be claimed under section 115.

Total Capital Gain= (850000- 70000)- 50 % which amounts to 390000. But since, the house

is used a place of residence, the total CGT will be excluded according to section 118. 10.

5TAXATION LAW

Moreover, the contract’s forfeiture occurs in the following year which is to be dealt in

2019/2020.

Artistic painting by Margaret Preston

Capital Gain Asset- as per section 118.10, a capital gain asset can be defined as a collectable.

The assets must be acquired after 20th September 1985. Since the painting is incurred on this

date and it is a collectable, thus it is a CGT asset.

Capital Gain Event- list of CGE is given as per section 104.5. The most general of these is

event A1 as given in section 104.10 (1) and is triggered when a CGA is sold or gifted. Sale of

Artistic piece of painting is A1 event.

CG or CL= CP – CB

Capital proceeds (CP) is the amount that tax payer has received or may get by the sale as

stated in given in section 116.20. Here for the painting, it is 125000 $.

Cost Base (CB) – the valuation of buying and maintenance of the assets as stated in Section

110.25 (1). It has got five elements.

E1 or the Element 1 as per section 110.25(2) is the price for acquiring the asset for the

painting of 15000 $.

Discount – when the Tax payer is not a company and the asset has been acquired before 20th

of September of 1999 and kept in hold for twelve months, then discount can be claimed as

per section 115.

Total Capital Gain for painting is $ (125000- 15000)- 50%= 55000 $.

Luxury Yacht

Capital Gain Asset- as per the rules given in section 108-20(2), capital gain asset can be

explained as any personal item of valuation more than 10000 $. The assets need to be

Moreover, the contract’s forfeiture occurs in the following year which is to be dealt in

2019/2020.

Artistic painting by Margaret Preston

Capital Gain Asset- as per section 118.10, a capital gain asset can be defined as a collectable.

The assets must be acquired after 20th September 1985. Since the painting is incurred on this

date and it is a collectable, thus it is a CGT asset.

Capital Gain Event- list of CGE is given as per section 104.5. The most general of these is

event A1 as given in section 104.10 (1) and is triggered when a CGA is sold or gifted. Sale of

Artistic piece of painting is A1 event.

CG or CL= CP – CB

Capital proceeds (CP) is the amount that tax payer has received or may get by the sale as

stated in given in section 116.20. Here for the painting, it is 125000 $.

Cost Base (CB) – the valuation of buying and maintenance of the assets as stated in Section

110.25 (1). It has got five elements.

E1 or the Element 1 as per section 110.25(2) is the price for acquiring the asset for the

painting of 15000 $.

Discount – when the Tax payer is not a company and the asset has been acquired before 20th

of September of 1999 and kept in hold for twelve months, then discount can be claimed as

per section 115.

Total Capital Gain for painting is $ (125000- 15000)- 50%= 55000 $.

Luxury Yacht

Capital Gain Asset- as per the rules given in section 108-20(2), capital gain asset can be

explained as any personal item of valuation more than 10000 $. The assets need to be

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

acquired after 20th of September of 1985. As per the facts of the case, it has been acquired

after the said date, it is a personal property and is bought for personal enjoyment, hence yacht

is a CGT asset.

Capital Gain Event- list of CGE is provided as per section 104.5. One of the most common

type of these is the A1 event as given in section 104.10 (1) and is triggered when CGA is

being sold or gifted. Sale of luxury yacht is an event A1.

CG or CL = CP- CB

CP or Capital proceeds denote the sum that tax payer has received or may get by the sale as

given in section 116.20. Here the CP for yacht is 60000 $.

Reduced Cost Base (RCB) is the valuation of buying and maintaining the asset. But element

3 is to be disregarded.

Element 1 of section 110.25(2) is the price required to acquire the asset which in this case is

110000 $.

Total Capital Loss is 110000- 60000= 50000.

This loss should not be used to offset any kind of CG loss in the coming year or present year

as given in section 108.20(2).

Shares in BHP mining company:

Capital Gain Asset as per rules in section 108.5, capital gain assets can be illustrated as any

property which is need to be acquired after 20th of September of 1985. Since the shares

belongs to BHP mining company, acquired after the above mentioned date and is a type of

property it is a CGT asset.

acquired after 20th of September of 1985. As per the facts of the case, it has been acquired

after the said date, it is a personal property and is bought for personal enjoyment, hence yacht

is a CGT asset.

Capital Gain Event- list of CGE is provided as per section 104.5. One of the most common

type of these is the A1 event as given in section 104.10 (1) and is triggered when CGA is

being sold or gifted. Sale of luxury yacht is an event A1.

CG or CL = CP- CB

CP or Capital proceeds denote the sum that tax payer has received or may get by the sale as

given in section 116.20. Here the CP for yacht is 60000 $.

Reduced Cost Base (RCB) is the valuation of buying and maintaining the asset. But element

3 is to be disregarded.

Element 1 of section 110.25(2) is the price required to acquire the asset which in this case is

110000 $.

Total Capital Loss is 110000- 60000= 50000.

This loss should not be used to offset any kind of CG loss in the coming year or present year

as given in section 108.20(2).

Shares in BHP mining company:

Capital Gain Asset as per rules in section 108.5, capital gain assets can be illustrated as any

property which is need to be acquired after 20th of September of 1985. Since the shares

belongs to BHP mining company, acquired after the above mentioned date and is a type of

property it is a CGT asset.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

CGE- list of CGE is provided in section 104.5. the most general type is the Event A1 given in

section 104.10(1) and is incurred when CGA is transferred by means of Sale or gift. Sale of

shares forms a CGT A1 event.

CGE A1 Timing- it happens on the particular day when the asset is disposed off as per

section 104.10 (2).

CG or CL = CP-CB.

CP- capital proceeds is the amount of money incurred by the Tax payer already or may be

received as per section 116.20. here CP for the shares amounts to 80000. It is to be decreased

by 750 as cost of brokerage.

Cost Base (CB)- value of buying and maintaining the asset is given in section 25(1) which

has got 5 elements.

Element E1 as given in section 110.25 (2) is the cost for acquiring the asset. It is for shares is

75000 dllars. It has got Element 2 as the stamp duty of 250 $. Interest E3 of CB is regarded as

the deductible expense as if included in to Cost Base, it may result into capital loss and RCB

is not being included in E 3.

CG= 79250-75250= 4000

Tax Return Loss of Previous Year

Tax loss is to be used to offset capital gain in the current year. It forms the 10000 $ loss that

will be reducing the Capital Gain for Daniel

Net Capital Gain for Daniel

Hous- 0

Painting – 55000

CGE- list of CGE is provided in section 104.5. the most general type is the Event A1 given in

section 104.10(1) and is incurred when CGA is transferred by means of Sale or gift. Sale of

shares forms a CGT A1 event.

CGE A1 Timing- it happens on the particular day when the asset is disposed off as per

section 104.10 (2).

CG or CL = CP-CB.

CP- capital proceeds is the amount of money incurred by the Tax payer already or may be

received as per section 116.20. here CP for the shares amounts to 80000. It is to be decreased

by 750 as cost of brokerage.

Cost Base (CB)- value of buying and maintaining the asset is given in section 25(1) which

has got 5 elements.

Element E1 as given in section 110.25 (2) is the cost for acquiring the asset. It is for shares is

75000 dllars. It has got Element 2 as the stamp duty of 250 $. Interest E3 of CB is regarded as

the deductible expense as if included in to Cost Base, it may result into capital loss and RCB

is not being included in E 3.

CG= 79250-75250= 4000

Tax Return Loss of Previous Year

Tax loss is to be used to offset capital gain in the current year. It forms the 10000 $ loss that

will be reducing the Capital Gain for Daniel

Net Capital Gain for Daniel

Hous- 0

Painting – 55000

8TAXATION LAW

Yatch- 0

HP shares- 4000

Loss – (10000)

Total- 49000

Answer 2b:

If there lies any CG made by Daniel it will get added to the assessable income as the

statutory income as provided in section 102. He is liable to pay for tax as per the current tax

slabs.

Answer 2 c:

When there lies a Capital Loss for Daniel, he can use it to offset Capital Gain in the

following year. It should not be to cause deduction to reduce the TI.

Yatch- 0

HP shares- 4000

Loss – (10000)

Total- 49000

Answer 2b:

If there lies any CG made by Daniel it will get added to the assessable income as the

statutory income as provided in section 102. He is liable to pay for tax as per the current tax

slabs.

Answer 2 c:

When there lies a Capital Loss for Daniel, he can use it to offset Capital Gain in the

following year. It should not be to cause deduction to reduce the TI.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

References:

Fringe Benefit Tax Assessment Act 1986 (CTH)

Income Tax Assessment Act 1997 (Cth)

Taxation Ruling 2011/3

TD 2018/2

References:

Fringe Benefit Tax Assessment Act 1986 (CTH)

Income Tax Assessment Act 1997 (Cth)

Taxation Ruling 2011/3

TD 2018/2

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.