Taxation Law Assignment Solution: Daniel & Olivia's Partnership

VerifiedAdded on 2023/04/21

|9

|1714

|371

Homework Assignment

AI Summary

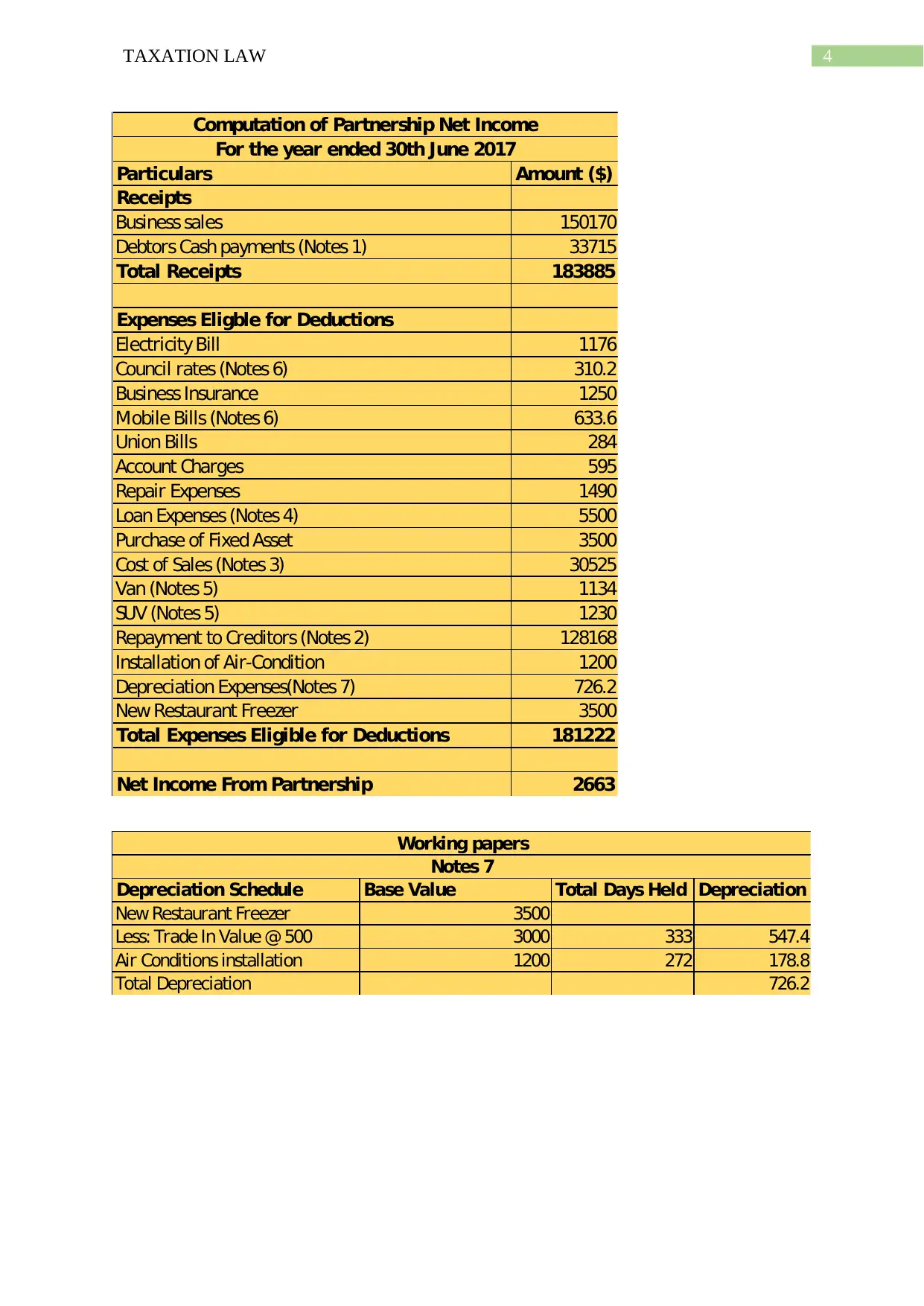

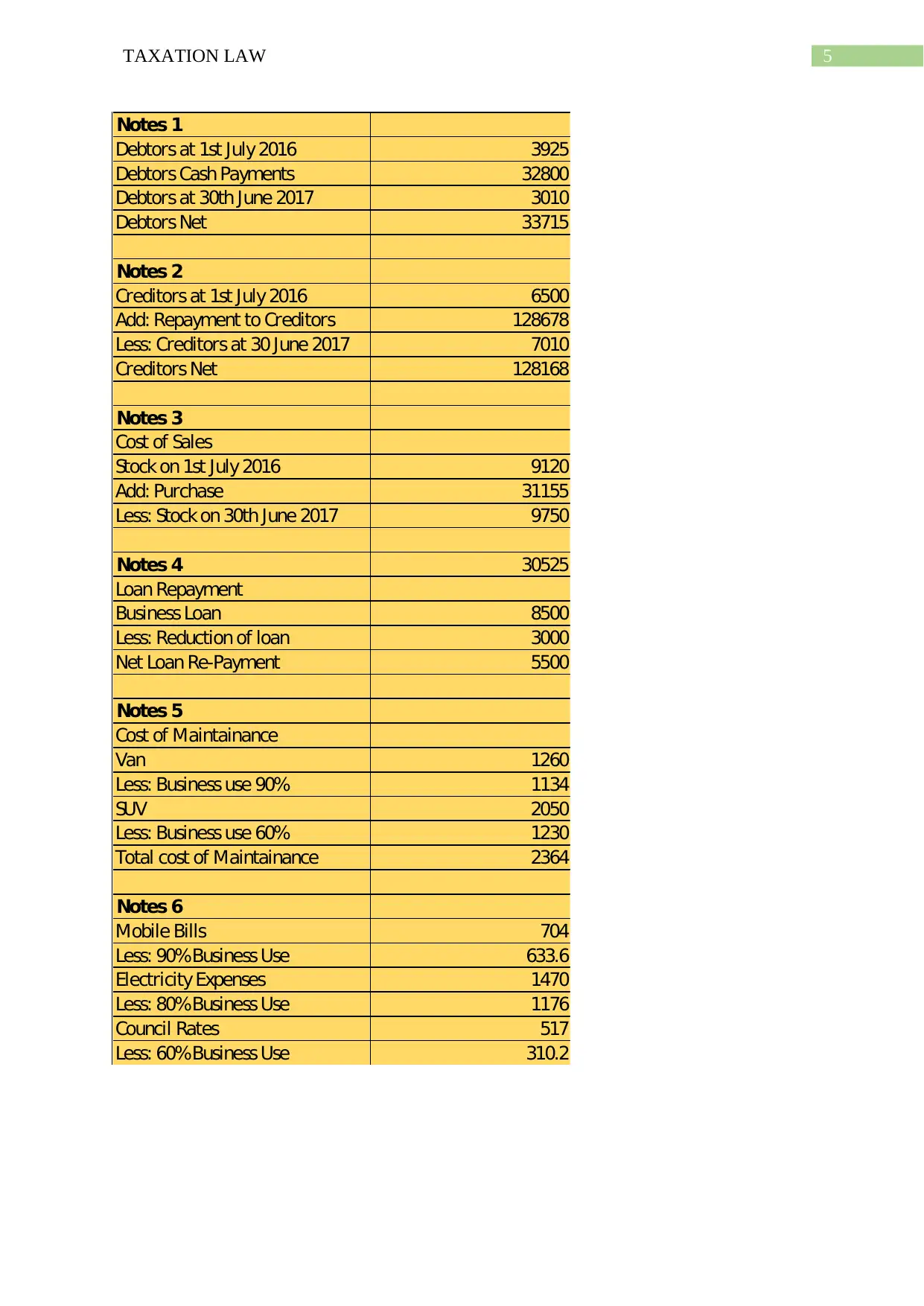

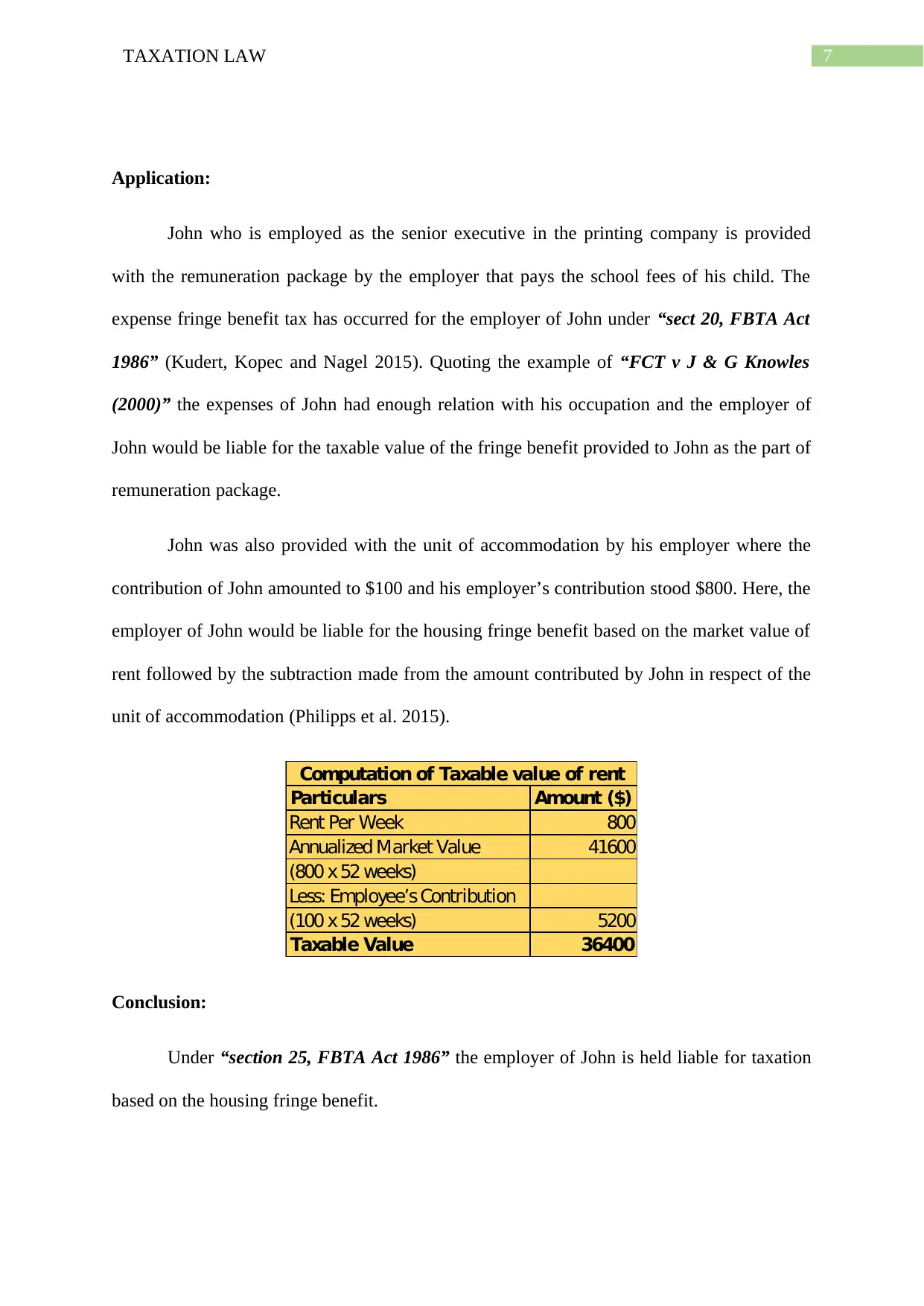

This assignment solution addresses two key taxation law issues. The first part analyzes the tax implications of a partnership business, including determining taxable income, allowable deductions, and the impact of drawings and asset purchases. It calculates the partnership's net income, detailing receipts, expenses, and depreciation. The second part examines fringe benefit tax, specifically expense payment and housing fringe benefits, and assesses the employer's tax liability. The solution references relevant legislation, including the ITA Act 1997 and FBTAA 1986, and provides calculations to determine taxable values. The assignment provides a comprehensive analysis of the taxation principles involved.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.