Taxation Law Assignment: Compensation, CGT, and Property Taxation

VerifiedAdded on 2022/12/01

|19

|4992

|310

Homework Assignment

AI Summary

This assignment solution addresses two questions related to Australian taxation law. The first question analyzes the tax consequences for Sophie and Kate, focusing on compensation receipts. It examines whether lump-sum damages for loss of reputation, compensation for lost income, and reimbursement of legal fees are assessable income or subject to capital gains tax (CGT). The analysis references relevant tax rulings and case law. The second question examines the CGT implications for Joe and Amy regarding the disposal of a main residence, considering pre-CGT assets, deceased estate scenarios, and the taxpayer's residency. The solution applies relevant legislation and case law to determine the tax liabilities. The assignment covers key concepts such as assessable income, CGT events, and the main residence exemption.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Introduction:...........................................................................................................................2

Various Compensation Receipts:...........................................................................................2

Sophie Client:.........................................................................................................................2

2.1: Lump sum damages for potential loss of reputation.......................................................2

2.2: Compensation for the loss of income whilst the machine was being replaced:..............3

2.3: Reimbursement of Legal Fees:.......................................................................................4

3: Kate Client:............................................................................................................................5

3.1 A Lump sum payment for pain and suffering:.................................................................5

3.2 Payment of ongoing medical and cosmetic surgery costs................................................6

3.3 Interest on the lump sum payment...................................................................................6

Conclusion:............................................................................................................................7

Answer to question 2:.................................................................................................................8

Introduction:...........................................................................................................................8

Issues:.....................................................................................................................................8

Laws:......................................................................................................................................8

Application:..........................................................................................................................12

Conclusion:..........................................................................................................................13

References:...............................................................................................................................14

Table of Contents

Answer to question 1:.................................................................................................................2

Introduction:...........................................................................................................................2

Various Compensation Receipts:...........................................................................................2

Sophie Client:.........................................................................................................................2

2.1: Lump sum damages for potential loss of reputation.......................................................2

2.2: Compensation for the loss of income whilst the machine was being replaced:..............3

2.3: Reimbursement of Legal Fees:.......................................................................................4

3: Kate Client:............................................................................................................................5

3.1 A Lump sum payment for pain and suffering:.................................................................5

3.2 Payment of ongoing medical and cosmetic surgery costs................................................6

3.3 Interest on the lump sum payment...................................................................................6

Conclusion:............................................................................................................................7

Answer to question 2:.................................................................................................................8

Introduction:...........................................................................................................................8

Issues:.....................................................................................................................................8

Laws:......................................................................................................................................8

Application:..........................................................................................................................12

Conclusion:..........................................................................................................................13

References:...............................................................................................................................14

2TAXATION LAW

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Answer to question 1:

Introduction:

Issues:

1.1. The central issue that is discussed in the question regarding the tax consequences of

the lump sum damages, compensation associated to the loss of earnings and

reimbursement associated to the legal fees received by Sophie and Kate relating to the

damages would be held as assessable earnings under the “sec 6-5, ITAA 1997”.

1.2. Whether or not the capital gains that arises from the receipt of damages payment will

be considered as assessable earnings under “sec 118-37, ITAA 1997”.

Various Compensation Receipts:

Sophie Client:

2.1: Lump sum damages for potential loss of reputation

Laws:

As clarified in “Taxation Ruling of TR 95/35” the guiding principle about imposing

tax on income derived from the compensation receipts. This rule is applicable to those

taxpayers that receives money as receipts for compensation (Woellner et al., 2016). The

“Taxation Ruling of TR 95/35” is helpful in drawing the outcomes associated with the CGT

that relates to derivation of compensation payment and determine whether the sum received

must be taken into the account as the chargeable receipts for the receiver within the “Part

IIIA of the ITAA 1936”.

When it is noticed that the taxpayer receives any kind of compensation that is largely

related with the sale of underlying asset or any portion of underlying asset of a taxpayer the

compensation that is received under such circumstances would amount to consideration that

Answer to question 1:

Introduction:

Issues:

1.1. The central issue that is discussed in the question regarding the tax consequences of

the lump sum damages, compensation associated to the loss of earnings and

reimbursement associated to the legal fees received by Sophie and Kate relating to the

damages would be held as assessable earnings under the “sec 6-5, ITAA 1997”.

1.2. Whether or not the capital gains that arises from the receipt of damages payment will

be considered as assessable earnings under “sec 118-37, ITAA 1997”.

Various Compensation Receipts:

Sophie Client:

2.1: Lump sum damages for potential loss of reputation

Laws:

As clarified in “Taxation Ruling of TR 95/35” the guiding principle about imposing

tax on income derived from the compensation receipts. This rule is applicable to those

taxpayers that receives money as receipts for compensation (Woellner et al., 2016). The

“Taxation Ruling of TR 95/35” is helpful in drawing the outcomes associated with the CGT

that relates to derivation of compensation payment and determine whether the sum received

must be taken into the account as the chargeable receipts for the receiver within the “Part

IIIA of the ITAA 1936”.

When it is noticed that the taxpayer receives any kind of compensation that is largely

related with the sale of underlying asset or any portion of underlying asset of a taxpayer the

compensation that is received under such circumstances would amount to consideration that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

is received for the disposal of the asset (Long et al., 2016). The judgement handed by the

federal court in “FC of T v Spedley Securities Ltd (1988)” noted that where the taxpayer

receives any compensation regarding the damage of business goodwill then the sum will be

held as capital receipt.

Application:

The evidences that is derived from the question relating to the situation of Sophie it is

found that she initiated a legal proceedings against Fracpro for delivering her with a faulty

calibration of laser machine. The compensation that was received by Sophie from Fracpro is

for loss of earnings and business reputation. The sum of $100,000 that is obtained by Sophie

must be regarded as the damages received for probable business goodwill loss. Denoting the

judgement that was handed by federal court in “FCT v Spedley Securities Ltd (1988)” the

amount of $100,000 obtained by Sophie will be held as compensation received for causing

damage to the business reputation and goodwill (Burns, 2017). The compensation amount is

regarded as the capital receipt and it is not taxable as the incomes under ordinary conception

of “sec 6-5, ITAA 1997”.

2.2: Compensation for the loss of income whilst the machine was being replaced:

Laws:

As explained under the “taxation determination ruling of TD 93/58” there are certain

circumstances where the compensation that are received by the taxpayer as the lump sum

compensation or the settlement payment will be regarded as assessable income (Campbell,

2018). Compensation that a taxpayer receives for the loss of income is usually considered as

taxable earnings under the “subsection 25 (1) of the ITAA 1936”, given that;

a. The payment that is received by the taxpayer amounts to the payment of

compensation regarding the loss of income or

is received for the disposal of the asset (Long et al., 2016). The judgement handed by the

federal court in “FC of T v Spedley Securities Ltd (1988)” noted that where the taxpayer

receives any compensation regarding the damage of business goodwill then the sum will be

held as capital receipt.

Application:

The evidences that is derived from the question relating to the situation of Sophie it is

found that she initiated a legal proceedings against Fracpro for delivering her with a faulty

calibration of laser machine. The compensation that was received by Sophie from Fracpro is

for loss of earnings and business reputation. The sum of $100,000 that is obtained by Sophie

must be regarded as the damages received for probable business goodwill loss. Denoting the

judgement that was handed by federal court in “FCT v Spedley Securities Ltd (1988)” the

amount of $100,000 obtained by Sophie will be held as compensation received for causing

damage to the business reputation and goodwill (Burns, 2017). The compensation amount is

regarded as the capital receipt and it is not taxable as the incomes under ordinary conception

of “sec 6-5, ITAA 1997”.

2.2: Compensation for the loss of income whilst the machine was being replaced:

Laws:

As explained under the “taxation determination ruling of TD 93/58” there are certain

circumstances where the compensation that are received by the taxpayer as the lump sum

compensation or the settlement payment will be regarded as assessable income (Campbell,

2018). Compensation that a taxpayer receives for the loss of income is usually considered as

taxable earnings under the “subsection 25 (1) of the ITAA 1936”, given that;

a. The payment that is received by the taxpayer amounts to the payment of

compensation regarding the loss of income or

5TAXATION LAW

b. Up to the extent that at a part of the lump sum payment can be recognized and

quantifiable as the income. This is generally possible when the parties either

impliedly or expressly agrees that the certain part of the payment is associated to the

loss of income nature.

The decision of the law court in “Allsop v FC of T (1965)” where the law court held

that the receipt received by the taxpayer included in the lump sum receipt also comprise of

the capital in nature (Burton, 2017). However, the ingredients of the payment can be

recognized as income and hence the portion of the payment that is related to income is

assessable.

Application:

An amount of $20,000 was received by Sophie in the form of compensation regarding

the loss of her income. The sum of $20,000 received as lump sum regarding the loss of

earnings would be viewed as having the nature of income and will be regarded as ordinary

earnings. Citing the verdict that was agreed in the “Allsop v FC of T (1965)” compensation

that Sophie got is linked with the loss of income (Yuan, 2016). The lump sum payment can

be recognized and quantifiable as the income. Compensation that Sophie has received for the

loss of income is usually considered as taxable earnings under the “subsection 25 (1) of the

ITAA 1936”.

2.3: Reimbursement of Legal Fees:

Laws:

A noteworthy explanation has been made in “section 118-37 (2)”, which puts forward

that capital gains or loss must be disregarded when a person receives any kind of payment as

the reimbursement for the outgoings incurred (Shaw, 2017). When the taxpayer gets the

b. Up to the extent that at a part of the lump sum payment can be recognized and

quantifiable as the income. This is generally possible when the parties either

impliedly or expressly agrees that the certain part of the payment is associated to the

loss of income nature.

The decision of the law court in “Allsop v FC of T (1965)” where the law court held

that the receipt received by the taxpayer included in the lump sum receipt also comprise of

the capital in nature (Burton, 2017). However, the ingredients of the payment can be

recognized as income and hence the portion of the payment that is related to income is

assessable.

Application:

An amount of $20,000 was received by Sophie in the form of compensation regarding

the loss of her income. The sum of $20,000 received as lump sum regarding the loss of

earnings would be viewed as having the nature of income and will be regarded as ordinary

earnings. Citing the verdict that was agreed in the “Allsop v FC of T (1965)” compensation

that Sophie got is linked with the loss of income (Yuan, 2016). The lump sum payment can

be recognized and quantifiable as the income. Compensation that Sophie has received for the

loss of income is usually considered as taxable earnings under the “subsection 25 (1) of the

ITAA 1936”.

2.3: Reimbursement of Legal Fees:

Laws:

A noteworthy explanation has been made in “section 118-37 (2)”, which puts forward

that capital gains or loss must be disregarded when a person receives any kind of payment as

the reimbursement for the outgoings incurred (Shaw, 2017). When the taxpayer gets the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

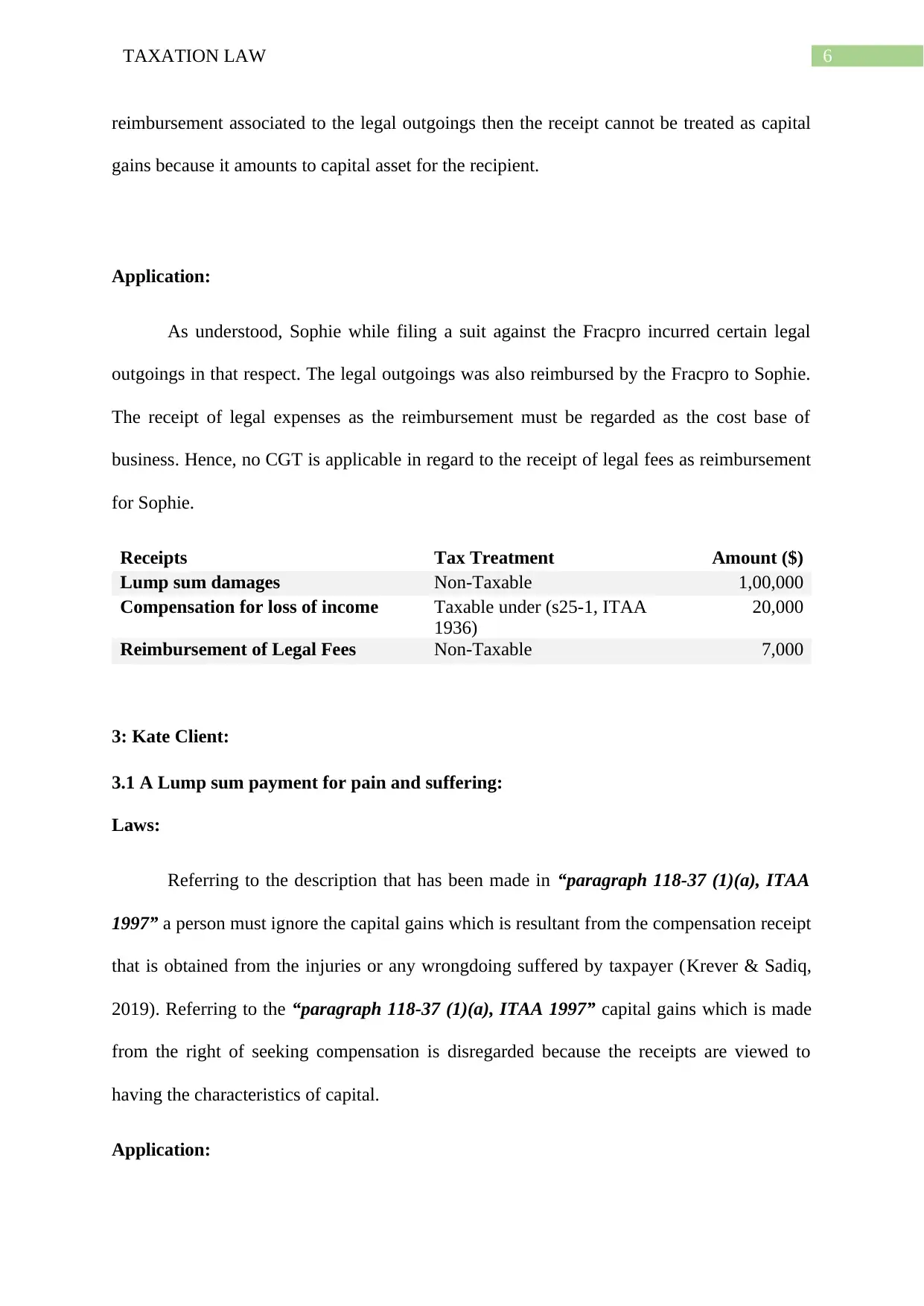

reimbursement associated to the legal outgoings then the receipt cannot be treated as capital

gains because it amounts to capital asset for the recipient.

Application:

As understood, Sophie while filing a suit against the Fracpro incurred certain legal

outgoings in that respect. The legal outgoings was also reimbursed by the Fracpro to Sophie.

The receipt of legal expenses as the reimbursement must be regarded as the cost base of

business. Hence, no CGT is applicable in regard to the receipt of legal fees as reimbursement

for Sophie.

Receipts Tax Treatment Amount ($)

Lump sum damages Non-Taxable 1,00,000

Compensation for loss of income Taxable under (s25-1, ITAA

1936)

20,000

Reimbursement of Legal Fees Non-Taxable 7,000

3: Kate Client:

3.1 A Lump sum payment for pain and suffering:

Laws:

Referring to the description that has been made in “paragraph 118-37 (1)(a), ITAA

1997” a person must ignore the capital gains which is resultant from the compensation receipt

that is obtained from the injuries or any wrongdoing suffered by taxpayer (Krever & Sadiq,

2019). Referring to the “paragraph 118-37 (1)(a), ITAA 1997” capital gains which is made

from the right of seeking compensation is disregarded because the receipts are viewed to

having the characteristics of capital.

Application:

reimbursement associated to the legal outgoings then the receipt cannot be treated as capital

gains because it amounts to capital asset for the recipient.

Application:

As understood, Sophie while filing a suit against the Fracpro incurred certain legal

outgoings in that respect. The legal outgoings was also reimbursed by the Fracpro to Sophie.

The receipt of legal expenses as the reimbursement must be regarded as the cost base of

business. Hence, no CGT is applicable in regard to the receipt of legal fees as reimbursement

for Sophie.

Receipts Tax Treatment Amount ($)

Lump sum damages Non-Taxable 1,00,000

Compensation for loss of income Taxable under (s25-1, ITAA

1936)

20,000

Reimbursement of Legal Fees Non-Taxable 7,000

3: Kate Client:

3.1 A Lump sum payment for pain and suffering:

Laws:

Referring to the description that has been made in “paragraph 118-37 (1)(a), ITAA

1997” a person must ignore the capital gains which is resultant from the compensation receipt

that is obtained from the injuries or any wrongdoing suffered by taxpayer (Krever & Sadiq,

2019). Referring to the “paragraph 118-37 (1)(a), ITAA 1997” capital gains which is made

from the right of seeking compensation is disregarded because the receipts are viewed to

having the characteristics of capital.

Application:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

The questions presents the facts that Kate has received a lump sum money that she

has suffered out of pain and sufferings as well as undergoing a medical treatment. The

amount that Kate has received cannot be treated as the outcome of providing personal

services or from any business activities. The compensation amount that Kate has received

should be viewed that it has not been earned from rendering employment services. As a

substitute, the compensation amount that is received is only for the one-off payment that is

regarding the injuries suffered and do not hold any characteristics of repetition.

It can be assumed that Kate anticipated the payment but the anticipation was the

outcome of pain and sufferings that she sustained was for general damage rather than treating

the amount as the product of any personal exertion.

The compensation amount acquired by Kate was largely for the settlement for the

injuries. The amount of $120,000 amounts to a capital amount under “CGT event C2” (Lee,

2018). The amount was the product of “right to seek” compensation. Under the “sec 118-

37(1)(b), ITAA 1997” the capital gains resulting from the CGT event C2 must be disregarded

by Kate.

3.2 Payment of ongoing medical and cosmetic surgery costs

Laws:

The present case study highlights that Kate also received compensation for her

medical and surgery cost. The compensation that is received by Kate is the product of single

payment which lacks any characteristics of repetition. The amount received as compensation

cannot be regarded as carrying the characteristics of income obtained as the outcome of

individual services. In actual sense, the amount of $50,000 should be observed as the product

of capital receipt inside “paragraph 118-37(1)(a), ITAA 1997” (O’Connell, 2017). The

reason for considering the compensation receipt as capital because it is linked to her personal

The questions presents the facts that Kate has received a lump sum money that she

has suffered out of pain and sufferings as well as undergoing a medical treatment. The

amount that Kate has received cannot be treated as the outcome of providing personal

services or from any business activities. The compensation amount that Kate has received

should be viewed that it has not been earned from rendering employment services. As a

substitute, the compensation amount that is received is only for the one-off payment that is

regarding the injuries suffered and do not hold any characteristics of repetition.

It can be assumed that Kate anticipated the payment but the anticipation was the

outcome of pain and sufferings that she sustained was for general damage rather than treating

the amount as the product of any personal exertion.

The compensation amount acquired by Kate was largely for the settlement for the

injuries. The amount of $120,000 amounts to a capital amount under “CGT event C2” (Lee,

2018). The amount was the product of “right to seek” compensation. Under the “sec 118-

37(1)(b), ITAA 1997” the capital gains resulting from the CGT event C2 must be disregarded

by Kate.

3.2 Payment of ongoing medical and cosmetic surgery costs

Laws:

The present case study highlights that Kate also received compensation for her

medical and surgery cost. The compensation that is received by Kate is the product of single

payment which lacks any characteristics of repetition. The amount received as compensation

cannot be regarded as carrying the characteristics of income obtained as the outcome of

individual services. In actual sense, the amount of $50,000 should be observed as the product

of capital receipt inside “paragraph 118-37(1)(a), ITAA 1997” (O’Connell, 2017). The

reason for considering the compensation receipt as capital because it is linked to her personal

8TAXATION LAW

injury. The sum will be viewed as capital receipt with in the provision of “CGT event C2”

because it is the “right to seek” compensation.

3.3 Interest on the lump sum payment

Laws:

The explanation that has been given in “Taxation Ruling of TR 95/35” evidently lays

down that when a taxpayer receives any kind of interest or any lump sum amount as the

outcome of any award for compensation then it will be regarded as the chargeable earnings in

regard to ordinary conceptions of “sec 6-5, ITAA 1997” (Minas et al., 2018).

Application:

Denoting the aforementioned explanation given under the “Taxation Ruling of TR

95/35” Kate reports the receipt of interest amounting to $7,000 on the lump sum payment of

compensation (Butler, 2016). The interest that is received by Kate will be viewed as the

product of ordinary earnings. The interest will be attracting a tax liability under “sec 6-5,

ITAA 1997”.

Receipts Tax Treatment Amount

($)

Lump sum payment for pain and

suffering

Exempted under (“S118-38 (a)), ITAA

1997”)

120000

Payment for medical and cosmetic

surgery

Exempted under (“S 118-37 (1) (b),

ITAA 1997”)

50000

Interest on lump sum payment Taxable under (“S 6-5, ITAA 1997”) 7000

Conclusion:

The lump sum payment as compensation that is received by Kate and Sophie mainly

forms the product of personal injuries and damages that is suffered by Sophie in her ordinary

business course. The compensation amount is treated as the capital receipt and it will be

injury. The sum will be viewed as capital receipt with in the provision of “CGT event C2”

because it is the “right to seek” compensation.

3.3 Interest on the lump sum payment

Laws:

The explanation that has been given in “Taxation Ruling of TR 95/35” evidently lays

down that when a taxpayer receives any kind of interest or any lump sum amount as the

outcome of any award for compensation then it will be regarded as the chargeable earnings in

regard to ordinary conceptions of “sec 6-5, ITAA 1997” (Minas et al., 2018).

Application:

Denoting the aforementioned explanation given under the “Taxation Ruling of TR

95/35” Kate reports the receipt of interest amounting to $7,000 on the lump sum payment of

compensation (Butler, 2016). The interest that is received by Kate will be viewed as the

product of ordinary earnings. The interest will be attracting a tax liability under “sec 6-5,

ITAA 1997”.

Receipts Tax Treatment Amount

($)

Lump sum payment for pain and

suffering

Exempted under (“S118-38 (a)), ITAA

1997”)

120000

Payment for medical and cosmetic

surgery

Exempted under (“S 118-37 (1) (b),

ITAA 1997”)

50000

Interest on lump sum payment Taxable under (“S 6-5, ITAA 1997”) 7000

Conclusion:

The lump sum payment as compensation that is received by Kate and Sophie mainly

forms the product of personal injuries and damages that is suffered by Sophie in her ordinary

business course. The compensation amount is treated as the capital receipt and it will be

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

considered as the exempted amount under the legislative provision of “sec 118-38 (a)” and

“sec 118-37 (1) (b), ITAA 1997”.

Answer to question 2:

Introduction:

Issues:

The main issue which is dealt in this question is there any kind of capital gains tax

consequences for Joe and Amy, the taxpayer, regarding the disposal of the main residence

provided that the;

a. The house was considered as the pre-CGT asset of the deceased

b. The house was utilized as the main residence of the deceased before he passed away

c. The taxpayer acquired the house in this situation on the basis of the estate of deceased

d. The taxpayer was residing in the property from the day when he passed away till the

day when the house was sold;

Laws:

As per the “Division 100-104, ITAA 1997” capital gains tax is viewed as the set of

rules that are main created to compute the gains which would be considered taxable as

income tax on the sale of the capital asset (Peiros & Smyth, 2017). Consequently, the

provision of capital gains tax is not regarded as the separate tax. The legislation of CGT was

established during 20th September 1985 with the objective of imposing tax on gains that are

earned from the selling the assets purchased or acquired on or following the aforementioned

date. Assets which is purchased or acquired before the 20/09/1985 are regarded as the “pre-

CGT assets” and any kind of gains that are earned from the sale of the pre-CGT asset are

simply excluded from the CGT regimes.

considered as the exempted amount under the legislative provision of “sec 118-38 (a)” and

“sec 118-37 (1) (b), ITAA 1997”.

Answer to question 2:

Introduction:

Issues:

The main issue which is dealt in this question is there any kind of capital gains tax

consequences for Joe and Amy, the taxpayer, regarding the disposal of the main residence

provided that the;

a. The house was considered as the pre-CGT asset of the deceased

b. The house was utilized as the main residence of the deceased before he passed away

c. The taxpayer acquired the house in this situation on the basis of the estate of deceased

d. The taxpayer was residing in the property from the day when he passed away till the

day when the house was sold;

Laws:

As per the “Division 100-104, ITAA 1997” capital gains tax is viewed as the set of

rules that are main created to compute the gains which would be considered taxable as

income tax on the sale of the capital asset (Peiros & Smyth, 2017). Consequently, the

provision of capital gains tax is not regarded as the separate tax. The legislation of CGT was

established during 20th September 1985 with the objective of imposing tax on gains that are

earned from the selling the assets purchased or acquired on or following the aforementioned

date. Assets which is purchased or acquired before the 20/09/1985 are regarded as the “pre-

CGT assets” and any kind of gains that are earned from the sale of the pre-CGT asset are

simply excluded from the CGT regimes.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

In order to raise the CGT liability, there should be two conditions that must be met.

This includes;

a. There should be a CGT asset purchased following 20th September 1985

b. There should also be a CGT event under sec 104-5 such as the sale of the CGT asset

(King, 2016).

A capital gains or capital loss must be ignored under the “section 104-10 (5)(a)]” if the

asset is purchased prior to 20/9/1985.

The main residence in which a taxpayer lives is generally excluded from the capital

gains tax under “sec 118-110, ITAA 1997” (Brydges & Yuen, 2018). A taxpayer is permitted

to get the partial main residence exemption when they subdivide and sell a portion of their

main residence or if they use the house for making chargeable revenues. When it is noted that

a taxpayer makes the use of house for generating earnings and results in any kind of CGT

event, the taxpayer will be required to bring into the account the portion of the proceeds as

the capital gains or loss under “sec 118-190, ITAA 1997”.

There should always be the CGT event in respect of the CGT asset. CGT event

comprises of the different forms of transactions which can lead to capital gains or the capital

loss. A “CGT event A1” under “sec 104-10 (1), ITAA 1997” is mainly related with the sale

of CGT asset (Jones, 2017). A sale of CGT-asset event would in normal course originate

when the taxpayer enters in the contract of sale.

There are certain kinds of rules that are associated to the CGT and the demise of the

taxpayer. The general rule that is explained in the “sec 128-10, ITAA 1997” provides an

explanation that when the taxpayer dies, their legal heirs or their beneficiaries is assumed to

acquire the CGT assets on the day when the deceased taxpayer passes away (Blakelock &

King, 2017). On the other hand, when it is noticed that the pre-CGT asset of the deceased

In order to raise the CGT liability, there should be two conditions that must be met.

This includes;

a. There should be a CGT asset purchased following 20th September 1985

b. There should also be a CGT event under sec 104-5 such as the sale of the CGT asset

(King, 2016).

A capital gains or capital loss must be ignored under the “section 104-10 (5)(a)]” if the

asset is purchased prior to 20/9/1985.

The main residence in which a taxpayer lives is generally excluded from the capital

gains tax under “sec 118-110, ITAA 1997” (Brydges & Yuen, 2018). A taxpayer is permitted

to get the partial main residence exemption when they subdivide and sell a portion of their

main residence or if they use the house for making chargeable revenues. When it is noted that

a taxpayer makes the use of house for generating earnings and results in any kind of CGT

event, the taxpayer will be required to bring into the account the portion of the proceeds as

the capital gains or loss under “sec 118-190, ITAA 1997”.

There should always be the CGT event in respect of the CGT asset. CGT event

comprises of the different forms of transactions which can lead to capital gains or the capital

loss. A “CGT event A1” under “sec 104-10 (1), ITAA 1997” is mainly related with the sale

of CGT asset (Jones, 2017). A sale of CGT-asset event would in normal course originate

when the taxpayer enters in the contract of sale.

There are certain kinds of rules that are associated to the CGT and the demise of the

taxpayer. The general rule that is explained in the “sec 128-10, ITAA 1997” provides an

explanation that when the taxpayer dies, their legal heirs or their beneficiaries is assumed to

acquire the CGT assets on the day when the deceased taxpayer passes away (Blakelock &

King, 2017). On the other hand, when it is noticed that the pre-CGT asset of the deceased

11TAXATION LAW

taxpayer is inherited, the new beneficiary under such kind of circumstances is assumed to

have acquired the asset based on the market value upon the day of the deceased taxpayer

demise.

“Sec 128-15, ITAA 1997” is related with the instances of inherited post-CGT assets.

Under “sec 128-15, ITAA 1997” when it is found that the post-CGT of the deceased taxpayer

is inherited then in such situation the beneficiary is viewed as to have acquired the asset on

the day of demise at the cost base of deceased taxpayer (Freudenberg et al., 2017). While

“sec 188-195” is associated with the instances of inherited main residence. When it is noticed

that the asset forms the main residence of the deceased and the same is not utilized for

generating assessable income, the cost base to the beneficiary denote the market value on day

when the deceased taxpayer passed away. Where the asset becomes the main dwelling of

residence for the deceased and the same has not been utilized for generating assessable

earnings, the beneficiary in this circumstances may inherit the exemption from the main

dwelling upon satisfying the certain criteria listed under “sec 188-195, ITAA 1997”.

Under the “Division 110, ITAA 1997” the cost base of the asset is usually ascertained

when the asset is passed to the taxpayer as the personal legal representative or the heir of the

deceased taxpayer (Kudrna, 2016). The division is mainly related to the ascertainment of cost

base of property that are used by the taxpayer as the main residence immediately following

the demise and not being used for generating assessable income. “Sec 128-15, ITAA 1997”

usually comprises of the cost base that are based on the market worth of the CGT asset.

“Sec 118-195, ITAA 1997” explains that the capital gains or loss that happens from

the CGT asset in respect of the dwelling is under some of the situation is ignored given the

taxpayer is regarded as the individual and the interest of ownership is passed among the

taxpayer is inherited, the new beneficiary under such kind of circumstances is assumed to

have acquired the asset based on the market value upon the day of the deceased taxpayer

demise.

“Sec 128-15, ITAA 1997” is related with the instances of inherited post-CGT assets.

Under “sec 128-15, ITAA 1997” when it is found that the post-CGT of the deceased taxpayer

is inherited then in such situation the beneficiary is viewed as to have acquired the asset on

the day of demise at the cost base of deceased taxpayer (Freudenberg et al., 2017). While

“sec 188-195” is associated with the instances of inherited main residence. When it is noticed

that the asset forms the main residence of the deceased and the same is not utilized for

generating assessable income, the cost base to the beneficiary denote the market value on day

when the deceased taxpayer passed away. Where the asset becomes the main dwelling of

residence for the deceased and the same has not been utilized for generating assessable

earnings, the beneficiary in this circumstances may inherit the exemption from the main

dwelling upon satisfying the certain criteria listed under “sec 188-195, ITAA 1997”.

Under the “Division 110, ITAA 1997” the cost base of the asset is usually ascertained

when the asset is passed to the taxpayer as the personal legal representative or the heir of the

deceased taxpayer (Kudrna, 2016). The division is mainly related to the ascertainment of cost

base of property that are used by the taxpayer as the main residence immediately following

the demise and not being used for generating assessable income. “Sec 128-15, ITAA 1997”

usually comprises of the cost base that are based on the market worth of the CGT asset.

“Sec 118-195, ITAA 1997” explains that the capital gains or loss that happens from

the CGT asset in respect of the dwelling is under some of the situation is ignored given the

taxpayer is regarded as the individual and the interest of ownership is passed among the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.