Taxation Law Assignment: Taxation of Damages and Capital Gains

VerifiedAdded on 2022/12/16

|18

|5056

|225

Homework Assignment

AI Summary

This taxation law assignment analyzes the tax implications for Our Earth Pty Ltd, a company involved in manufacturing biodegradable coffee cups. The assignment addresses two key questions. The first question evaluates the tax liability of the company for compensatory damages received due to patent infringement and loss of profits, and the taxability of reimbursement of legal expenditure. It considers relevant laws such as "Division 6" and "section 25 (1), ITAA 1936" and determines that while damages for patent infringement are treated as capital receipts, damages for loss of profits are assessable income, and legal fee reimbursements are taxable recoupments. The second question examines the capital gains tax (CGT) implications of disposing of subdivided land, discussing pre-CGT and post-CGT assets and CGT event A1 under "section 104-10, ITAA 1997". The assignment applies these laws to the provided facts, calculating assessable income and determining the tax treatment of various receipts and expenditures. The conclusion summarizes the tax treatment of various financial transactions.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Issues:.....................................................................................................................................2

Laws:......................................................................................................................................2

Application:............................................................................................................................4

Conclusion:............................................................................................................................6

Answer to question 2:.................................................................................................................7

Issues:.....................................................................................................................................7

Laws:......................................................................................................................................7

Application:..........................................................................................................................10

Conclusion:..........................................................................................................................12

References:...............................................................................................................................14

Table of Contents

Answer to question 1:.................................................................................................................2

Issues:.....................................................................................................................................2

Laws:......................................................................................................................................2

Application:............................................................................................................................4

Conclusion:............................................................................................................................6

Answer to question 2:.................................................................................................................7

Issues:.....................................................................................................................................7

Laws:......................................................................................................................................7

Application:..........................................................................................................................10

Conclusion:..........................................................................................................................12

References:...............................................................................................................................14

2TAXATION LAW

Answer to question 1:

Issues:

Will the taxpayer be held liable for tax for the receipt of compensatory damages under

“Division 6” or “subsection 25 (1), ITAA 1936”? Is the receipt of interest from the damages

pay-out will be included into the assessable income of the Our Earth Pty Ltd? Will the

taxpayer be held liable for assessment purpose for the reimbursement of the legal expenditure

occurred by Our Earth Pty Ltd?

Laws:

Typical compensation receipts that are received by the taxpayer includes the

insurance payments, receipts by the business from another party that have failed to carry out

their contractual obligations, payment that are received for entering into the restrictive

covenants and loss of usage of money will be considered as income in nature (Woellner et al.,

2016). A compensation receipts that is received by a business as the right of seeking

compensation or due to the cause of action or any form of proceedings introduced by

business as the right or in relation to the underlying asset are treated as compensatory

receipts. Compensation received as the damages will be included into the assessable income

with respect to ordinary meaning of “Division 6 of the ITAA 1997” or will be included as

statutory income.

As defined in “section 25 (1), ITAA 1997” compensatory payments that are received

is considered taxable given the payments that are received is related to the loss of income,

particularly the profits or interest from previous years (Braithwaite & Reinhart, 2019). The

law court in the “Mc Laurin v FC of T (1961)” held that receipt of compensation was

considered taxable within the legislative provision of “subsection 25 (1), ITAA 1936” till the

portion of payment that is received was recognizable and assessable as income.

Answer to question 1:

Issues:

Will the taxpayer be held liable for tax for the receipt of compensatory damages under

“Division 6” or “subsection 25 (1), ITAA 1936”? Is the receipt of interest from the damages

pay-out will be included into the assessable income of the Our Earth Pty Ltd? Will the

taxpayer be held liable for assessment purpose for the reimbursement of the legal expenditure

occurred by Our Earth Pty Ltd?

Laws:

Typical compensation receipts that are received by the taxpayer includes the

insurance payments, receipts by the business from another party that have failed to carry out

their contractual obligations, payment that are received for entering into the restrictive

covenants and loss of usage of money will be considered as income in nature (Woellner et al.,

2016). A compensation receipts that is received by a business as the right of seeking

compensation or due to the cause of action or any form of proceedings introduced by

business as the right or in relation to the underlying asset are treated as compensatory

receipts. Compensation received as the damages will be included into the assessable income

with respect to ordinary meaning of “Division 6 of the ITAA 1997” or will be included as

statutory income.

As defined in “section 25 (1), ITAA 1997” compensatory payments that are received

is considered taxable given the payments that are received is related to the loss of income,

particularly the profits or interest from previous years (Braithwaite & Reinhart, 2019). The

law court in the “Mc Laurin v FC of T (1961)” held that receipt of compensation was

considered taxable within the legislative provision of “subsection 25 (1), ITAA 1936” till the

portion of payment that is received was recognizable and assessable as income.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

In order to ascertain whether the receipt of compensation amounts to ordinary income

or capital receipts, it is entirely dependent on the nature of payment. When a compensation

payment received is carrying the nature of income with respect to the ordinary concepts then

“section 6-5, of the ITAA 1997” is applicable (Martin & Connor, 2017). For example, the

compensatory payments are considered assessable income when it is received as either

recurrent or periodic payments which is not in the form of instalments of lump sum.

As held in the case of “Californian Oil Products Ltd v Federal Commissioner of

Taxation (1934)” amount that are paid as damages, compensation or to cover the loss of

income occurred during the course of business of the company then it will be considered as

taxable income (Blakelock & King, 2017). The main reason for this is that it is a part of profit

that are derived from carrying on the business activities even though it is as a result of

unusual or extraordinary occasions or situations.

The taxation commissioner in “CT (Vic) v Phillips (1936)” passed its verdict by

stating that if the taxpayer receives a compensation that relates to the loss of business

revenues or commercial scheme and forms the substance of business activities, then the

compensation will be considered as the loss of capital asset (Barkoczy, 2016). Therefore,

because of the absence of countervailing examination then the receipts would be treated as

capital receipts. As held in the case of “FC of T v Spedley Securities Ltd (1988)” the federal

court stated that compensatory damages for goodwill was treated as capital item. The receipt

of compensation was treated as injury to capital asset.

Where a taxpayer receives interest as the part of compensatory amount then the

interest is considered as taxable income for the taxpayer under the normal provision of

income. The federal court in the case of “Whitaker v FCT (1998)” explained that post

judgement interest are regarded as having the character of interest is treated as income within

In order to ascertain whether the receipt of compensation amounts to ordinary income

or capital receipts, it is entirely dependent on the nature of payment. When a compensation

payment received is carrying the nature of income with respect to the ordinary concepts then

“section 6-5, of the ITAA 1997” is applicable (Martin & Connor, 2017). For example, the

compensatory payments are considered assessable income when it is received as either

recurrent or periodic payments which is not in the form of instalments of lump sum.

As held in the case of “Californian Oil Products Ltd v Federal Commissioner of

Taxation (1934)” amount that are paid as damages, compensation or to cover the loss of

income occurred during the course of business of the company then it will be considered as

taxable income (Blakelock & King, 2017). The main reason for this is that it is a part of profit

that are derived from carrying on the business activities even though it is as a result of

unusual or extraordinary occasions or situations.

The taxation commissioner in “CT (Vic) v Phillips (1936)” passed its verdict by

stating that if the taxpayer receives a compensation that relates to the loss of business

revenues or commercial scheme and forms the substance of business activities, then the

compensation will be considered as the loss of capital asset (Barkoczy, 2016). Therefore,

because of the absence of countervailing examination then the receipts would be treated as

capital receipts. As held in the case of “FC of T v Spedley Securities Ltd (1988)” the federal

court stated that compensatory damages for goodwill was treated as capital item. The receipt

of compensation was treated as injury to capital asset.

Where a taxpayer receives interest as the part of compensatory amount then the

interest is considered as taxable income for the taxpayer under the normal provision of

income. The federal court in the case of “Whitaker v FCT (1998)” explained that post

judgement interest are regarded as having the character of interest is treated as income within

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

ordinary concept (Anderson et al., 2016). It is noteworthy to denote that receipt of interest is

regarded as income under ordinary concepts where the compensation for lost earnings is

related, provided that the claimant has not suffered any damages he might have received the

interest that was awarded.

On the other hand, where the taxpayers are permitted to obtain deduction for the legal

expenditure that are available to the taxpayer under “section 8-1, ITAA 1997” then the

payment or the award in respect of the legal costs would be included into the taxpayer’s

taxable income in the form of recovery under “subdivision 20-A”. The legal expenses that

are awarded is usually paid to the taxpayer for indemnifying them or recipient is the

successful party for the cost of lawsuit (Sadiq, 2019). Therefore, the receipt of such legal

expenses are not treated as income under ordinary course. The legal expenditure is considered

as the taxable recoupment under “subsection 20-20 (2)”, which means that the amount which

is received is regarded as recoupment of loss or expenditure which is a taxable recoupment if

the taxpayer has received the amount as indemnity and the sum which is deductible for tax

purpose under the legislation of “ITAA 1936 or ITAA 1997” (Fry, 2017).

Application:

Evidences obtained from the case study of Our Earth Pty Ltd, suggest that the

company is engaged in the manufacturing of specially designed bio-degradable coffee cups

which is made from sustainable materials. However, Our Earth Pty Ltd noticed that the

Coffee Beans Pty Ltd had stolen the design of cups and sod the same to the overseas

customers for a cheaper price. Our Earth Pty Ltd took a legal action and received an amount

of $300,000 as the damages caused to the design of patent infringement. The compensation

payment that is received by Our Earth Pty Ltd is associated to the infringement of patent and

should be treated as compensation that is received in respect of right of seeking compensation

for causing an infringement breach to patent.

ordinary concept (Anderson et al., 2016). It is noteworthy to denote that receipt of interest is

regarded as income under ordinary concepts where the compensation for lost earnings is

related, provided that the claimant has not suffered any damages he might have received the

interest that was awarded.

On the other hand, where the taxpayers are permitted to obtain deduction for the legal

expenditure that are available to the taxpayer under “section 8-1, ITAA 1997” then the

payment or the award in respect of the legal costs would be included into the taxpayer’s

taxable income in the form of recovery under “subdivision 20-A”. The legal expenses that

are awarded is usually paid to the taxpayer for indemnifying them or recipient is the

successful party for the cost of lawsuit (Sadiq, 2019). Therefore, the receipt of such legal

expenses are not treated as income under ordinary course. The legal expenditure is considered

as the taxable recoupment under “subsection 20-20 (2)”, which means that the amount which

is received is regarded as recoupment of loss or expenditure which is a taxable recoupment if

the taxpayer has received the amount as indemnity and the sum which is deductible for tax

purpose under the legislation of “ITAA 1936 or ITAA 1997” (Fry, 2017).

Application:

Evidences obtained from the case study of Our Earth Pty Ltd, suggest that the

company is engaged in the manufacturing of specially designed bio-degradable coffee cups

which is made from sustainable materials. However, Our Earth Pty Ltd noticed that the

Coffee Beans Pty Ltd had stolen the design of cups and sod the same to the overseas

customers for a cheaper price. Our Earth Pty Ltd took a legal action and received an amount

of $300,000 as the damages caused to the design of patent infringement. The compensation

payment that is received by Our Earth Pty Ltd is associated to the infringement of patent and

should be treated as compensation that is received in respect of right of seeking compensation

for causing an infringement breach to patent.

5TAXATION LAW

To ascertain whether the compensatory damages are treated as ordinary income or

capital receipts, the decision is dependent on the nature of receipts which is received by Our

Earth Pty Ltd. Referring to the decision made in “CT (Vic) v Phillips (1936)” the

compensatory damages of $300,000 that is paid to Our Earth Pty Ltd is associated to business

loss or foundations of business activities (James, 2016). Consequently, the damages of

$300,000 should be treated as compensation payment for causing loss to capital asset. In

addition to this, due to the absence of countervailing examination, the damages or the receipts

is itself regarded as capital in nature.

With reference to the decision made in the case of “FC of T v Spedley Securities Ltd

(1988)”, in the present situation of Our Earth Pty Ltd, it can be stated that the sum of

$300,000 received amounts to recompense for causing damage to patent that itself was

regarded as capital in nature (Burton, 2017). Therefore, the sum of $300,000 is not included

for assessment purpose because it is an ordinary income and amounts to compensation for

causing injury to the capital asset.

In the later instances it is noticed that Our Earth Pty Ltd also received an amount of

$200,000 by Coffee Beans Pty Ltd for causing an expected loss of profits during the last 12

months. Referring to the decision made in “Californian Oil Products Ltd v Federal

Commissioner of Taxation (1934)” it can be stated that the amount of $200,000 paid to Our

Earth Pty Ltd as damages or to compensate for causing a loss of profit to the business in the

ordinary course is without a doubt amounts to income under the ordinary concepts of

“section 6-5, of the ITAA 1997” (Morgan & Castelyn, 2018).

Furthermore, Our Earth Pty Ltd was later reimbursed an amount of $40,000 which

was occurred as legal fees. The legal costs is awarded to Our Earth Pty Ltd in the form of

compensation to the successful party relating to the cost occurred for bringing lawsuit against

To ascertain whether the compensatory damages are treated as ordinary income or

capital receipts, the decision is dependent on the nature of receipts which is received by Our

Earth Pty Ltd. Referring to the decision made in “CT (Vic) v Phillips (1936)” the

compensatory damages of $300,000 that is paid to Our Earth Pty Ltd is associated to business

loss or foundations of business activities (James, 2016). Consequently, the damages of

$300,000 should be treated as compensation payment for causing loss to capital asset. In

addition to this, due to the absence of countervailing examination, the damages or the receipts

is itself regarded as capital in nature.

With reference to the decision made in the case of “FC of T v Spedley Securities Ltd

(1988)”, in the present situation of Our Earth Pty Ltd, it can be stated that the sum of

$300,000 received amounts to recompense for causing damage to patent that itself was

regarded as capital in nature (Burton, 2017). Therefore, the sum of $300,000 is not included

for assessment purpose because it is an ordinary income and amounts to compensation for

causing injury to the capital asset.

In the later instances it is noticed that Our Earth Pty Ltd also received an amount of

$200,000 by Coffee Beans Pty Ltd for causing an expected loss of profits during the last 12

months. Referring to the decision made in “Californian Oil Products Ltd v Federal

Commissioner of Taxation (1934)” it can be stated that the amount of $200,000 paid to Our

Earth Pty Ltd as damages or to compensate for causing a loss of profit to the business in the

ordinary course is without a doubt amounts to income under the ordinary concepts of

“section 6-5, of the ITAA 1997” (Morgan & Castelyn, 2018).

Furthermore, Our Earth Pty Ltd was later reimbursed an amount of $40,000 which

was occurred as legal fees. The legal costs is awarded to Our Earth Pty Ltd in the form of

compensation to the successful party relating to the cost occurred for bringing lawsuit against

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Coffee Beans Ltd. The reimbursement of legal fees cannot be treated as ordinary income.

Consequently, the reimbursement of the legal expenditure amounts to payment or award in

respect of the legal fees that must be included into the assessable income of Our Earth Pty

Ltd as taxable recoupment of expenses under “subdivision 20-A”. Therefore, the legal fees

that is received by Our Earth Pty should be considered as recoupment of loss or outgoings

that constitutes assessable recoupment.

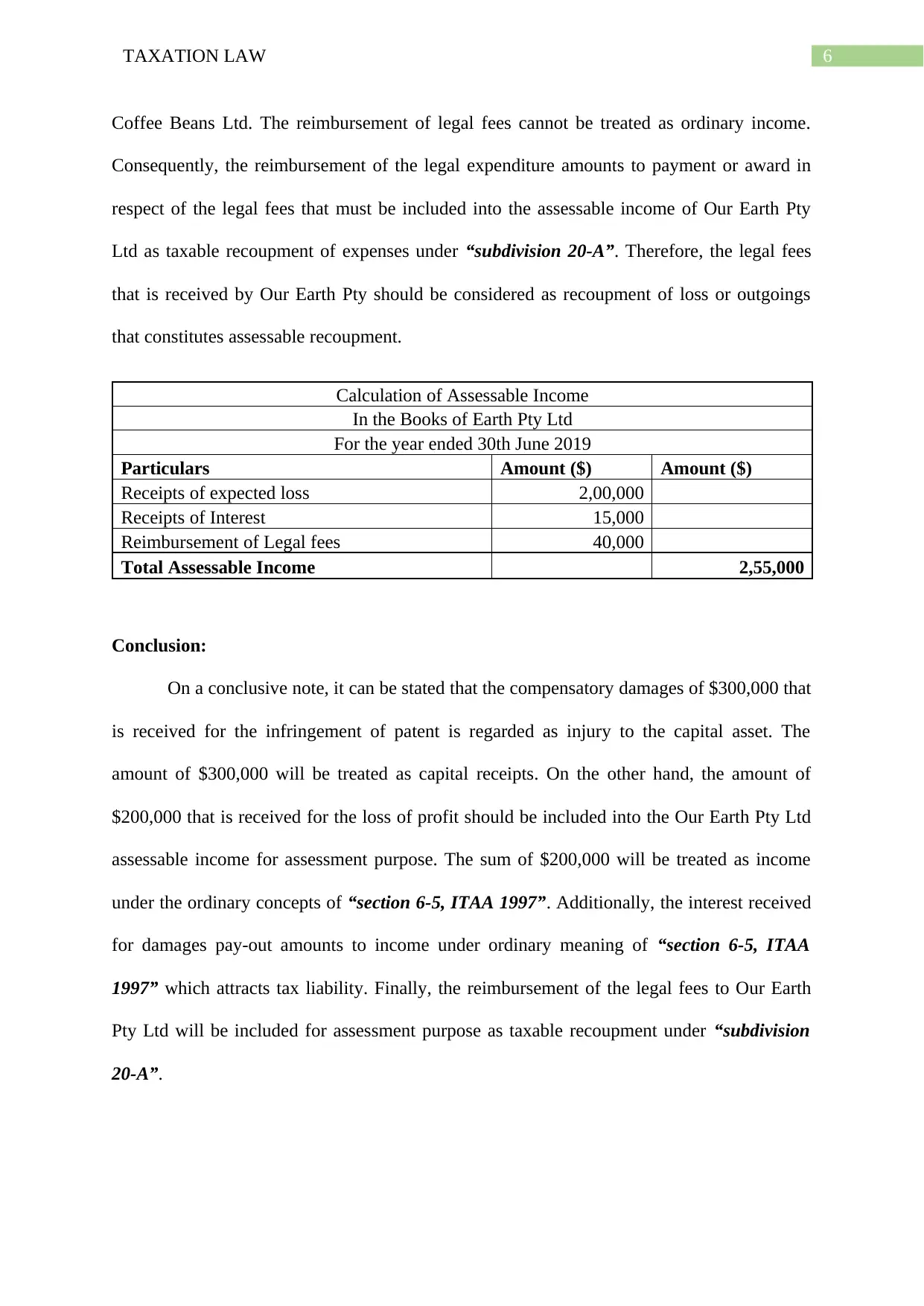

Calculation of Assessable Income

In the Books of Earth Pty Ltd

For the year ended 30th June 2019

Particulars Amount ($) Amount ($)

Receipts of expected loss 2,00,000

Receipts of Interest 15,000

Reimbursement of Legal fees 40,000

Total Assessable Income 2,55,000

Conclusion:

On a conclusive note, it can be stated that the compensatory damages of $300,000 that

is received for the infringement of patent is regarded as injury to the capital asset. The

amount of $300,000 will be treated as capital receipts. On the other hand, the amount of

$200,000 that is received for the loss of profit should be included into the Our Earth Pty Ltd

assessable income for assessment purpose. The sum of $200,000 will be treated as income

under the ordinary concepts of “section 6-5, ITAA 1997”. Additionally, the interest received

for damages pay-out amounts to income under ordinary meaning of “section 6-5, ITAA

1997” which attracts tax liability. Finally, the reimbursement of the legal fees to Our Earth

Pty Ltd will be included for assessment purpose as taxable recoupment under “subdivision

20-A”.

Coffee Beans Ltd. The reimbursement of legal fees cannot be treated as ordinary income.

Consequently, the reimbursement of the legal expenditure amounts to payment or award in

respect of the legal fees that must be included into the assessable income of Our Earth Pty

Ltd as taxable recoupment of expenses under “subdivision 20-A”. Therefore, the legal fees

that is received by Our Earth Pty should be considered as recoupment of loss or outgoings

that constitutes assessable recoupment.

Calculation of Assessable Income

In the Books of Earth Pty Ltd

For the year ended 30th June 2019

Particulars Amount ($) Amount ($)

Receipts of expected loss 2,00,000

Receipts of Interest 15,000

Reimbursement of Legal fees 40,000

Total Assessable Income 2,55,000

Conclusion:

On a conclusive note, it can be stated that the compensatory damages of $300,000 that

is received for the infringement of patent is regarded as injury to the capital asset. The

amount of $300,000 will be treated as capital receipts. On the other hand, the amount of

$200,000 that is received for the loss of profit should be included into the Our Earth Pty Ltd

assessable income for assessment purpose. The sum of $200,000 will be treated as income

under the ordinary concepts of “section 6-5, ITAA 1997”. Additionally, the interest received

for damages pay-out amounts to income under ordinary meaning of “section 6-5, ITAA

1997” which attracts tax liability. Finally, the reimbursement of the legal fees to Our Earth

Pty Ltd will be included for assessment purpose as taxable recoupment under “subdivision

20-A”.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Answer to question 2:

Issues:

Will the taxpayer be held liable for the capital gains tax relating to the gains made

from the disposal of subdivided land either under the “section 25 (1)” or “section 26 (a)” or

the taxpayer has simply realised the capital asset?

Laws:

Capital gains tax is generally applied to the assets that are purchased or events that are

happening before or after the 20th September 1985. Accordingly, the terms pre-CGT and post-

CGT is regularly used to refer the assets that are bought or events that takes place prior to or

following the date (Maley & Maley, 2018). The capital gains tax system is applied on the

realised amount of capital gains or losses that originates upon the sale of assets or from other

specified events. The first step to determine whether the transactions or events that happens

forms the subject of CGT is to ascertain whether the CGT event has taken place or not.

As a general rule, capital gains tax functions prospectively and it is applicable only if

the CGT event takes place for the assets that are purchased on or after the 20th September

1985. For majority of the CGT events there are certain exception, if the CGT asset is

purchased before 20th September 1985 then it will be treated as Pre-CGT asset and it is

exempted from the capital gains tax (Morgan et al., 2018). A capital gains or loss only

happens when the CGT event happens and involves the capital asset. A CGT event A1

happens under “section 104-10, ITAA 1997” to the CGT asset when the taxpayer sells the

asset. A CGT asset can be defined as any type of property, legal or equitable right which is

not regarded as property.

There are several events where the taxpayers has the opportunity of sub-dividing and

selling the land that are kept mainly for the large amount of time. Such circumstances takes

Answer to question 2:

Issues:

Will the taxpayer be held liable for the capital gains tax relating to the gains made

from the disposal of subdivided land either under the “section 25 (1)” or “section 26 (a)” or

the taxpayer has simply realised the capital asset?

Laws:

Capital gains tax is generally applied to the assets that are purchased or events that are

happening before or after the 20th September 1985. Accordingly, the terms pre-CGT and post-

CGT is regularly used to refer the assets that are bought or events that takes place prior to or

following the date (Maley & Maley, 2018). The capital gains tax system is applied on the

realised amount of capital gains or losses that originates upon the sale of assets or from other

specified events. The first step to determine whether the transactions or events that happens

forms the subject of CGT is to ascertain whether the CGT event has taken place or not.

As a general rule, capital gains tax functions prospectively and it is applicable only if

the CGT event takes place for the assets that are purchased on or after the 20th September

1985. For majority of the CGT events there are certain exception, if the CGT asset is

purchased before 20th September 1985 then it will be treated as Pre-CGT asset and it is

exempted from the capital gains tax (Morgan et al., 2018). A capital gains or loss only

happens when the CGT event happens and involves the capital asset. A CGT event A1

happens under “section 104-10, ITAA 1997” to the CGT asset when the taxpayer sells the

asset. A CGT asset can be defined as any type of property, legal or equitable right which is

not regarded as property.

There are several events where the taxpayers has the opportunity of sub-dividing and

selling the land that are kept mainly for the large amount of time. Such circumstances takes

8TAXATION LAW

place where the land is entirely owned by the primary producers on the urban outskirts and

residential development implies that proper use of land can be made by building houses

rather than using for agricultural purpose (Black, 2018). In some situations, such kind of

property development can be treated as considerable where there is an opportunity of making

large amount of profit from the land. This introduces the question as how the profits that are

made from the sub-division and sale of land will be treated. Usually, there are three

alternatives;

a. The subdivision and selling of land may be qualified as the simple realisation of the

capital asset.

b. The degree of land development would be such that it constitutes carrying the

business of land development.

c. The land development might go beyond the simple realisation of the land but might be

short of requirement that are associated to performing the business, in such a situation

it will be considered as profit deriving arrangements or activities.

According to the “Taxation Determination TD 97/3” simple subdivision of land

cannot be treated as sale of land within the meaning of “section 104-10, ITAA 1997”.

Guidance has been provided under this ruling is that whether the proceeds that are derived

from the sale of isolated transaction will be regarded as income and hence assessable within

the “subsection 25 (1), ITAA 1936” (Martin, 2019). Before relying on the complete study, it

becomes necessary to ascertain whether the land development is treated as simple realisation.

Nevertheless, it is important to appreciate that if the land was actually purchased for making

profit upon resale or for development purpose, then the gains or income that are made from

the sale and land development will be treated as assessable ordinary income, irrespective of

the sale of land.

place where the land is entirely owned by the primary producers on the urban outskirts and

residential development implies that proper use of land can be made by building houses

rather than using for agricultural purpose (Black, 2018). In some situations, such kind of

property development can be treated as considerable where there is an opportunity of making

large amount of profit from the land. This introduces the question as how the profits that are

made from the sub-division and sale of land will be treated. Usually, there are three

alternatives;

a. The subdivision and selling of land may be qualified as the simple realisation of the

capital asset.

b. The degree of land development would be such that it constitutes carrying the

business of land development.

c. The land development might go beyond the simple realisation of the land but might be

short of requirement that are associated to performing the business, in such a situation

it will be considered as profit deriving arrangements or activities.

According to the “Taxation Determination TD 97/3” simple subdivision of land

cannot be treated as sale of land within the meaning of “section 104-10, ITAA 1997”.

Guidance has been provided under this ruling is that whether the proceeds that are derived

from the sale of isolated transaction will be regarded as income and hence assessable within

the “subsection 25 (1), ITAA 1936” (Martin, 2019). Before relying on the complete study, it

becomes necessary to ascertain whether the land development is treated as simple realisation.

Nevertheless, it is important to appreciate that if the land was actually purchased for making

profit upon resale or for development purpose, then the gains or income that are made from

the sale and land development will be treated as assessable ordinary income, irrespective of

the sale of land.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Profits which originates from performing or carrying the profit deriving scheme or

plan in relation to the property which is purchased prior to the introduction of the CGT or

Pre-CGT asset is mainly included in the assessable income within the legislation of “section

15-15, ITAA 1997”. The capital improvements that are made by the taxpayer on the capital

gains tax asset is subjected to CGT (Robin, 2019). Whereas, if the taxpayer upon purchasing

the land makes a substantial capital improvement after the purchase date then it will be added

to the cost base of asset for capital gains tax purpose.

The federal court passed its verdict in “Scottish Australian Mining Co Ltd v FC of T

(1950)” by stating that the taxpayer derived a significant amount of profit upon the disposal

of subdivided lots (Robin & Barkoczy, 2019). The federal court held the taxpayer assessable

for the gains that are derived from the sale of numerous lots of land. According to the

commissioner of taxation, the profits were treated taxable income either under the “section

25 (1), ITAA 1936” in the form of gains made from performing the business of land

development or within the legislative provision of “section 26 (a)” as the profits that are

made from the revenue generating undertaking (Basu, 2016).

In an another example of “Federal Commissioner of Taxation v Whitfords Beach

Pty Ltd (1982)” the federal court held the taxpayer taxable for the gains made from the sale

of several plots of land (Payne, 2018). According to the taxation officer the profits were

treated taxable either under the “section 25 (1), ITAA 1936” in the form of gains made from

carrying the business of land development or within the legislative provision of “section 26

(a)” as the profits that are made from the revenue generating undertaking (Bankman et al.,

2018).

Once it is understood that the acquisition of land and sale gives rise to derivation of

profit which was not in the ordinary course of business or as the subject of ordinary business

Profits which originates from performing or carrying the profit deriving scheme or

plan in relation to the property which is purchased prior to the introduction of the CGT or

Pre-CGT asset is mainly included in the assessable income within the legislation of “section

15-15, ITAA 1997”. The capital improvements that are made by the taxpayer on the capital

gains tax asset is subjected to CGT (Robin, 2019). Whereas, if the taxpayer upon purchasing

the land makes a substantial capital improvement after the purchase date then it will be added

to the cost base of asset for capital gains tax purpose.

The federal court passed its verdict in “Scottish Australian Mining Co Ltd v FC of T

(1950)” by stating that the taxpayer derived a significant amount of profit upon the disposal

of subdivided lots (Robin & Barkoczy, 2019). The federal court held the taxpayer assessable

for the gains that are derived from the sale of numerous lots of land. According to the

commissioner of taxation, the profits were treated taxable income either under the “section

25 (1), ITAA 1936” in the form of gains made from performing the business of land

development or within the legislative provision of “section 26 (a)” as the profits that are

made from the revenue generating undertaking (Basu, 2016).

In an another example of “Federal Commissioner of Taxation v Whitfords Beach

Pty Ltd (1982)” the federal court held the taxpayer taxable for the gains made from the sale

of several plots of land (Payne, 2018). According to the taxation officer the profits were

treated taxable either under the “section 25 (1), ITAA 1936” in the form of gains made from

carrying the business of land development or within the legislative provision of “section 26

(a)” as the profits that are made from the revenue generating undertaking (Bankman et al.,

2018).

Once it is understood that the acquisition of land and sale gives rise to derivation of

profit which was not in the ordinary course of business or as the subject of ordinary business

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

activity, the income that is in question would be regarded as assessable earnings of the

taxpayer within the ordinary meaning provided the taxpayer has the ultimate purpose of

making profit while purchasing the land.

Application:

The case study of Sam introduces with the situation that a land of 80 acres and 20

acres was bought by him respectively. The additional 20 acres of land was mainly bought for

expanding the business functions. But after the sometime, Sam appeared disinterested in

carrying the business of agriculture since the ongoing drought conditions effected the

business. Sam instead of carrying the business decided to sell the land and retire from

agriculture business. After engaging the service of real estate agent he was advised that sub-

division of land will be helpful in obtaining the best price of the land. Based on the advice of

property development agent Sam as the primary producer decided to subdivide the land for

the purpose of residential development to explain the best use of land is for residential

purpose instead of doing farming.

At first to determine the capital gains tax it is necessary to take into the account the

purchase date of the asset for capital gains tax purpose. Sam bought the 80 acres of land in

the year 1984. Therefore, with respect to the provision of CGT the 80 acres of land will be

treated as pre-CGT asset. Since the 80 acres of land is a Pre-CGT asset, therefore, no capital

gains tax will be applied (Minas et al., 2018). The capital gains made from the sale of land

will be considered as exempted for tax purpose.

On the other hand, Sam also bought 20 acres of land adjoining to the farm land on

February 1995. The land should be treated as the post-CGT asset because it is bought after

the introduction of capital gains tax regimes (Olbert & Spengel, 2017). The subdivision

commenced in 2017 and the land was ultimately sold in April 2018. Therefore, capital gains

activity, the income that is in question would be regarded as assessable earnings of the

taxpayer within the ordinary meaning provided the taxpayer has the ultimate purpose of

making profit while purchasing the land.

Application:

The case study of Sam introduces with the situation that a land of 80 acres and 20

acres was bought by him respectively. The additional 20 acres of land was mainly bought for

expanding the business functions. But after the sometime, Sam appeared disinterested in

carrying the business of agriculture since the ongoing drought conditions effected the

business. Sam instead of carrying the business decided to sell the land and retire from

agriculture business. After engaging the service of real estate agent he was advised that sub-

division of land will be helpful in obtaining the best price of the land. Based on the advice of

property development agent Sam as the primary producer decided to subdivide the land for

the purpose of residential development to explain the best use of land is for residential

purpose instead of doing farming.

At first to determine the capital gains tax it is necessary to take into the account the

purchase date of the asset for capital gains tax purpose. Sam bought the 80 acres of land in

the year 1984. Therefore, with respect to the provision of CGT the 80 acres of land will be

treated as pre-CGT asset. Since the 80 acres of land is a Pre-CGT asset, therefore, no capital

gains tax will be applied (Minas et al., 2018). The capital gains made from the sale of land

will be considered as exempted for tax purpose.

On the other hand, Sam also bought 20 acres of land adjoining to the farm land on

February 1995. The land should be treated as the post-CGT asset because it is bought after

the introduction of capital gains tax regimes (Olbert & Spengel, 2017). The subdivision

commenced in 2017 and the land was ultimately sold in April 2018. Therefore, capital gains

11TAXATION LAW

made from the sale of 20 acres of land will be subjected to capital gains tax as the post-CGT

asset.

In the current situation of Sam, the land development will be considered substantial

with the opportunity of making large sum of profits from the project. By referring to the

“Taxation Determination TD 97/3” it can be stated that to determine the profits and gains

made from the subdivided sale of land by Sam should be considered as income and hence

taxable under the “subsection 25 (1), ITAA 1936” (Huizinga et al., 2018). Before indulging

in the in depth analysis, it should be noted that the property was actually not purchased with

the objective of resale at profit or for the purpose of development. The intention of deriving

profit originated in the later phases.

Citing the decision made by the federal court in “Scottish Australian Mining Co Ltd

v FC of T (1950)” in case of Sam it can be stated that the taxpayer made a considerable

amount of profit from the sale of sub-divided allotments (Harding & Marten, 2018). As a

result Sam will be considered assessable for capital gains tax purpose in such situation for the

profits made from the sale of land either under the “section 25 (1), ITAA 1936” in the form

of gains made from carrying the business of land development or within the legislative

provision of “section 26 (a)” as the profits that are made from the revenue generating

undertaking (Sadiq & Sawyer, 2019).

With reference to the legislative provision of “section 25 (1)” the profits made from

the sale of 20 blocks of land constitutes taxable capital gains (Evans et al., 2015). This is

because Sam has went beyond the concept of simple realisation of capital asset and his

activities represents carrying the business of land development. Denoting the decision that

was made in the case of “Federal Commissioner of Taxation v Whitfords Beach Pty Ltd

(1982)” the wide-ranging development of land through rezoning and subdivision of land by

made from the sale of 20 acres of land will be subjected to capital gains tax as the post-CGT

asset.

In the current situation of Sam, the land development will be considered substantial

with the opportunity of making large sum of profits from the project. By referring to the

“Taxation Determination TD 97/3” it can be stated that to determine the profits and gains

made from the subdivided sale of land by Sam should be considered as income and hence

taxable under the “subsection 25 (1), ITAA 1936” (Huizinga et al., 2018). Before indulging

in the in depth analysis, it should be noted that the property was actually not purchased with

the objective of resale at profit or for the purpose of development. The intention of deriving

profit originated in the later phases.

Citing the decision made by the federal court in “Scottish Australian Mining Co Ltd

v FC of T (1950)” in case of Sam it can be stated that the taxpayer made a considerable

amount of profit from the sale of sub-divided allotments (Harding & Marten, 2018). As a

result Sam will be considered assessable for capital gains tax purpose in such situation for the

profits made from the sale of land either under the “section 25 (1), ITAA 1936” in the form

of gains made from carrying the business of land development or within the legislative

provision of “section 26 (a)” as the profits that are made from the revenue generating

undertaking (Sadiq & Sawyer, 2019).

With reference to the legislative provision of “section 25 (1)” the profits made from

the sale of 20 blocks of land constitutes taxable capital gains (Evans et al., 2015). This is

because Sam has went beyond the concept of simple realisation of capital asset and his

activities represents carrying the business of land development. Denoting the decision that

was made in the case of “Federal Commissioner of Taxation v Whitfords Beach Pty Ltd

(1982)” the wide-ranging development of land through rezoning and subdivision of land by

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.