Individual Assignment: Taxation Law of Australia, Term 2, 2019

VerifiedAdded on 2022/12/29

|13

|3339

|59

Homework Assignment

AI Summary

This assignment solution addresses key aspects of Australian taxation law. It begins by analyzing the Commissioner's view on when a company can carry on a business and covers topics such as gift deductibility, top tax rates, capital gains tax (CGT), and the taxation of income. The solution also explores the differences between ordinary and statutory income, Medicare levy and Medicare levy surcharge, and residency requirements. The assignment then delves into specific deduction claims, evaluating the deductibility of various expenses, including HECS-HELP payments, work-related travel, book purchases, child care, and clothing. It concludes with a discussion of CGT events related to land leasing and capital gains.

Running head: TAXATION LAW

TAXATION LAW

Name of the Student:

Name of the University:

Author Note:

TAXATION LAW

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

ANSWER 1:

a) The taxation ruling 2019/11 provides the view of Commissioner on when can a company

can carry on a business by following the meaning of small business entity as laid down in

section 23 of the Income Tax Rates Act 19862, hereinafter referred to as ITRA 1986

applicable in the income years of 2015-16 and 2016-17 as well as according to section

328-110 of the Income Tax Assessment Act 1997, hereinafter referred to as ITAA 1997.

b) Division 303 of the Income Tax Assessment Act 1997 enumerates the legislation

pertaining to the gift deductibility or contributions deductibility.

c) The top tax rate applicable to an individual who is a residential taxpayer amounts to

54097 dollars in the taxation year of 2019-2020 and this rate is subjected to an extra 45%

of the amount in excess of 180,000 dollars4.

d) Section 118.5 of the Income Tax Assessment Act5 when perused provides that car as well

as motor cycle is not included in the capital gain tax.

e) Destruction or loss of any CGT asset is covered by CGT C1 event under section 104-20

of the ITAA6.

f) The current threshold which is free from taxation for any individual resident for a

taxation year is the income excess of 18200 $.

g) In the case of Hayes v FCT7, High Court decided that an income accruing against any

services provided by a tax payer previously will depict a CGT gain in case of an

assessable income. Moreover, any amount which an employee got from his employer for

1 TR 2019/1.

2 Income Tax Rates Act 1986 s 23.

3 Income Tax Assessment Act 1997 Div 30.

4 www.ato.gov.au, "Individual Income Tax Rates", Ato.Gov.Au (Webpage, 2019)

https://www.ato.gov.au/Rates/Individual-income-tax-rates/.

5 Income Tax Assessment Act 1997 s118.5.

6 Ibid s 104.20.

7 Hayes v FCT (1956) 96 CLR 47.

ANSWER 1:

a) The taxation ruling 2019/11 provides the view of Commissioner on when can a company

can carry on a business by following the meaning of small business entity as laid down in

section 23 of the Income Tax Rates Act 19862, hereinafter referred to as ITRA 1986

applicable in the income years of 2015-16 and 2016-17 as well as according to section

328-110 of the Income Tax Assessment Act 1997, hereinafter referred to as ITAA 1997.

b) Division 303 of the Income Tax Assessment Act 1997 enumerates the legislation

pertaining to the gift deductibility or contributions deductibility.

c) The top tax rate applicable to an individual who is a residential taxpayer amounts to

54097 dollars in the taxation year of 2019-2020 and this rate is subjected to an extra 45%

of the amount in excess of 180,000 dollars4.

d) Section 118.5 of the Income Tax Assessment Act5 when perused provides that car as well

as motor cycle is not included in the capital gain tax.

e) Destruction or loss of any CGT asset is covered by CGT C1 event under section 104-20

of the ITAA6.

f) The current threshold which is free from taxation for any individual resident for a

taxation year is the income excess of 18200 $.

g) In the case of Hayes v FCT7, High Court decided that an income accruing against any

services provided by a tax payer previously will depict a CGT gain in case of an

assessable income. Moreover, any amount which an employee got from his employer for

1 TR 2019/1.

2 Income Tax Rates Act 1986 s 23.

3 Income Tax Assessment Act 1997 Div 30.

4 www.ato.gov.au, "Individual Income Tax Rates", Ato.Gov.Au (Webpage, 2019)

https://www.ato.gov.au/Rates/Individual-income-tax-rates/.

5 Income Tax Assessment Act 1997 s118.5.

6 Ibid s 104.20.

7 Hayes v FCT (1956) 96 CLR 47.

2TAXATION LAW

his service will be considered as the capital gain of the assessable income of such

employee. Any income which an individual receive due to personal exertion will be

regarded as the ordinary income of such individual. However, a receipt accrued already

given by a past employer but not provided to the employee will be regarded as the capital

asset as the employee got it as huge money later on after it was accrued.

h) The differences between an ordinary income and a statutory income will be analyzed in

this answer. Any tax payer under the provisions enumerated under the division of taxable

income as per the taxation law has the option to earn two types of income called the

ordinary income and statutory income. Ordinary income means the salary of an

individual in his capacity as an employee. It also include any other kind of money which

he can earn by means of personal exertion whereas any type of income barring ordinary

income is known as that statutory income and it is included within the assessable income.

Some examples of statutory income include dividends, redundancy payment, allowances

and CGT gains. For the purpose of assessing the ordinary income, any type of strict rule

is not followed but for statutory income, it is calculated by applying the provisions of the

statutes. Express mention in relation to ordinary income is not provided in the taxation

statute. However, statutory mention expressly is mandatory in order to consider a

statutory income as the assessable income8.

i) In this answer, point of differences between Medicare levy & Medicare levy surcharge

are enumerated. Many taxpayers are subjected to additional payment of taxes imposed on

regular income tax payable. Such additional taxes are Medicare levy and the Medicare

levy surcharge. Both of these taxes are applicable to the taxpayers. These are imposed

8 O’Connell, Ann. "Australia." (2017)Capital Gains Taxation. Edward Elgar Publishing.

his service will be considered as the capital gain of the assessable income of such

employee. Any income which an individual receive due to personal exertion will be

regarded as the ordinary income of such individual. However, a receipt accrued already

given by a past employer but not provided to the employee will be regarded as the capital

asset as the employee got it as huge money later on after it was accrued.

h) The differences between an ordinary income and a statutory income will be analyzed in

this answer. Any tax payer under the provisions enumerated under the division of taxable

income as per the taxation law has the option to earn two types of income called the

ordinary income and statutory income. Ordinary income means the salary of an

individual in his capacity as an employee. It also include any other kind of money which

he can earn by means of personal exertion whereas any type of income barring ordinary

income is known as that statutory income and it is included within the assessable income.

Some examples of statutory income include dividends, redundancy payment, allowances

and CGT gains. For the purpose of assessing the ordinary income, any type of strict rule

is not followed but for statutory income, it is calculated by applying the provisions of the

statutes. Express mention in relation to ordinary income is not provided in the taxation

statute. However, statutory mention expressly is mandatory in order to consider a

statutory income as the assessable income8.

i) In this answer, point of differences between Medicare levy & Medicare levy surcharge

are enumerated. Many taxpayers are subjected to additional payment of taxes imposed on

regular income tax payable. Such additional taxes are Medicare levy and the Medicare

levy surcharge. Both of these taxes are applicable to the taxpayers. These are imposed

8 O’Connell, Ann. "Australia." (2017)Capital Gains Taxation. Edward Elgar Publishing.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

under the Medicare Levy Act 19869 and the Income Tax Assessment Act10. The Medicare

levy surcharge has been incorporated aiming at encouraging the high income earners to

pay health care insurance indirectly decreasing the Medicare burden. The tax payers not

having any type of private health insurance are subjected to the Medicare levy surcharge.

This can be applied on the taxpayer’s total income together with fringe benefits for the

taxation year. The Medicare levy rate and the Medicare levy surcharge rate generally

ranges between 1%, 1.5 % and 1.25 %.

Answer 2:

The residency requirements are provided u/s 6(1) of the Income Tax Assessment Act11. It

involves three tests which are the domicile, residing and the super admission tests. Apart

from this 183 days test is also of consideration for assessing the taxation liability of an

individual who either lives in Australia or has some connection with it. These two tests

involve two types of principles provided under the said section. These principles are

‘permanent place of abode’ and the ‘usual place of abode’12. Though apparently both appears

to be of same meaning but they are different when considered as per the Australian taxation

law. This principle of place of abode is discussed in detail in the judgment of I.R.C. v.

Lysaght13 which states that place of abode means a residential property held by an individual

tax payer as its owner or lessor who is staying in such place with family.

Again the judgment of FC of T v Applegate14 case elaborates on the principle of

‘permanent place of abode’. In that case, it is seen that the ‘permanent place of abode’

9 Medicare Levy Act 1986.

10 Income Tax Assessment Act (Cth) 1936.

11 Income Tax Assessment Act (Cth) 1936 s 6.1.

12 Jones, Daryl. "Complexity of tax residency attracts review." (2018) Taxation in Australia 53.6: 296.

13 I.R.C. v. Lysaght (1928) A.C.234.

14 FC of T v Applegate 79 ATC 4307.

under the Medicare Levy Act 19869 and the Income Tax Assessment Act10. The Medicare

levy surcharge has been incorporated aiming at encouraging the high income earners to

pay health care insurance indirectly decreasing the Medicare burden. The tax payers not

having any type of private health insurance are subjected to the Medicare levy surcharge.

This can be applied on the taxpayer’s total income together with fringe benefits for the

taxation year. The Medicare levy rate and the Medicare levy surcharge rate generally

ranges between 1%, 1.5 % and 1.25 %.

Answer 2:

The residency requirements are provided u/s 6(1) of the Income Tax Assessment Act11. It

involves three tests which are the domicile, residing and the super admission tests. Apart

from this 183 days test is also of consideration for assessing the taxation liability of an

individual who either lives in Australia or has some connection with it. These two tests

involve two types of principles provided under the said section. These principles are

‘permanent place of abode’ and the ‘usual place of abode’12. Though apparently both appears

to be of same meaning but they are different when considered as per the Australian taxation

law. This principle of place of abode is discussed in detail in the judgment of I.R.C. v.

Lysaght13 which states that place of abode means a residential property held by an individual

tax payer as its owner or lessor who is staying in such place with family.

Again the judgment of FC of T v Applegate14 case elaborates on the principle of

‘permanent place of abode’. In that case, it is seen that the ‘permanent place of abode’

9 Medicare Levy Act 1986.

10 Income Tax Assessment Act (Cth) 1936.

11 Income Tax Assessment Act (Cth) 1936 s 6.1.

12 Jones, Daryl. "Complexity of tax residency attracts review." (2018) Taxation in Australia 53.6: 296.

13 I.R.C. v. Lysaght (1928) A.C.234.

14 FC of T v Applegate 79 ATC 4307.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

includes any place where an individual taxpayer stays having an intention to reside there for

a considerable period of time and not having any intention of leaving it. It is important to

refer to the case of F.C. of T. v. Jenkins15 to take into account and analyze the tax payer’s

intention.

The domicile of any person is referred in the principle of ‘usual place of abode’. For

instance, an accommodation which is rented can be considered to be a ‘usual place of abode’

provided the individual is staying in such place for a considerable period of time. This was

construed in the case of Levene v. I.R.C16.

Answer 3:

a) Under section 8.1 of the Income Tax Assessment Act17, it is stated that any expenditure in

connection with the income earning process of an individual can be assessed subjected to

deductions. Claim against such deduction can be claimed if the tax payer is able to show

such expenditure is not in connection with any domestic or personal reason instead

connected with income earning. In the current case scenario, payment for HECS- HELP

of 850 $ appears to be paid against a student loan which is again can be argued to be

personal nature. It not connected by any means with the individual’s assessable income

and deduction claim will not be allowed.

b) It has been stated under section 25.100 of the Income Tax Assessment Act18 expressly

provides that travelling related expenditure to the work place made by an individual will

be subjected to deduction. In the current scenario, the expense of 110$ incurred while

15 F.C. of T. v. Jenkins ATC 4098.

16 Levene v. I.R.C. (1928) A.C.217.

17 The Income Tax Assessment Act 1997 (Cth) s 8.1.

18 The Income Tax Assessment Act 1997 (Cth) s 25.100.

includes any place where an individual taxpayer stays having an intention to reside there for

a considerable period of time and not having any intention of leaving it. It is important to

refer to the case of F.C. of T. v. Jenkins15 to take into account and analyze the tax payer’s

intention.

The domicile of any person is referred in the principle of ‘usual place of abode’. For

instance, an accommodation which is rented can be considered to be a ‘usual place of abode’

provided the individual is staying in such place for a considerable period of time. This was

construed in the case of Levene v. I.R.C16.

Answer 3:

a) Under section 8.1 of the Income Tax Assessment Act17, it is stated that any expenditure in

connection with the income earning process of an individual can be assessed subjected to

deductions. Claim against such deduction can be claimed if the tax payer is able to show

such expenditure is not in connection with any domestic or personal reason instead

connected with income earning. In the current case scenario, payment for HECS- HELP

of 850 $ appears to be paid against a student loan which is again can be argued to be

personal nature. It not connected by any means with the individual’s assessable income

and deduction claim will not be allowed.

b) It has been stated under section 25.100 of the Income Tax Assessment Act18 expressly

provides that travelling related expenditure to the work place made by an individual will

be subjected to deduction. In the current scenario, the expense of 110$ incurred while

15 F.C. of T. v. Jenkins ATC 4098.

16 Levene v. I.R.C. (1928) A.C.217.

17 The Income Tax Assessment Act 1997 (Cth) s 8.1.

18 The Income Tax Assessment Act 1997 (Cth) s 25.100.

5TAXATION LAW

travelling from work place to university will be a deductible expense and hence subjected

to deduction.

c) Under section 8.1 of the Income Tax Assessment Act 1997 (Cth), it is stated that any

expenditure in connection with the income earning process of an individual can be

assessed subjected to deductions. Claim against such deduction can be claimed if the tax

payer is able to show such expenditure is not in connection with any domestic or personal

reason instead connected with income earning. This is also supported in the judgment

provided in the case of Lodge v Federal Commissioner of Taxation [1972] HCA 49. In

the present scenario, the cost against purchasing books of 200 $ is for knowledge

enhancement and improving skills by which a trainee accountant can help her in her

future job profile. Thus this amount of 200 $ is subjected to deduction as it is in

connection with earning income.

d) Under section 8.1 of the Income Tax Assessment Act19, it is stated that any expenditure in

connection with the income earning process of an individual can be assessed subjected to

deductions. Claim against such deduction can be claimed if the tax payer is able to show

such expenditure is not in connection with any domestic or personal reason instead

connected with income earning. This is also supported in the judgment provided in the

case of Lodge v Federal Commissioner of Taxation20. In the present scenario, the

expenditure for hiring child care during the evening classes of the trainee account will not

be subjected to deduction as it not anyway related to profession of such person being the

tax payer.

19 Ibid s 8.1.

20 Lodge v Federal Commissioner of Taxation [1972] HCA 49.

travelling from work place to university will be a deductible expense and hence subjected

to deduction.

c) Under section 8.1 of the Income Tax Assessment Act 1997 (Cth), it is stated that any

expenditure in connection with the income earning process of an individual can be

assessed subjected to deductions. Claim against such deduction can be claimed if the tax

payer is able to show such expenditure is not in connection with any domestic or personal

reason instead connected with income earning. This is also supported in the judgment

provided in the case of Lodge v Federal Commissioner of Taxation [1972] HCA 49. In

the present scenario, the cost against purchasing books of 200 $ is for knowledge

enhancement and improving skills by which a trainee accountant can help her in her

future job profile. Thus this amount of 200 $ is subjected to deduction as it is in

connection with earning income.

d) Under section 8.1 of the Income Tax Assessment Act19, it is stated that any expenditure in

connection with the income earning process of an individual can be assessed subjected to

deductions. Claim against such deduction can be claimed if the tax payer is able to show

such expenditure is not in connection with any domestic or personal reason instead

connected with income earning. This is also supported in the judgment provided in the

case of Lodge v Federal Commissioner of Taxation20. In the present scenario, the

expenditure for hiring child care during the evening classes of the trainee account will not

be subjected to deduction as it not anyway related to profession of such person being the

tax payer.

19 Ibid s 8.1.

20 Lodge v Federal Commissioner of Taxation [1972] HCA 49.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

e) Under section 8.1 of the Income Tax Assessment Act21, it is stated that any expenditure in

connection with the income earning process of an individual can be assessed subjected to

deductions. Claim against such deduction can be claimed if the tax payer is able to show

such expenditure is not in connection with any domestic or personal reason instead

connected with income earning. This is also supported in the judgment provided in the

case of Lodge v Federal Commissioner of Taxation [1972] HCA 49. In this case, the

expenditure of 250 $ for repairing the fridge is absolutely related to domestic reason and

not involves anything related to profession of such trainee accountant. Thus it cannot be

subjected to deduction.

f) Under section 8.1 of the Income Tax Assessment Act 1997 (Cth), it is stated that any

expenditure in connection with the income earning process of an individual can be

assessed subjected to deductions. Claim against such deduction can be claimed if the tax

payer is able to show such expenditure is not in connection with any domestic or personal

reason instead connected with income earning. This is also supported in the judgment

provided in the case of Lodge v Federal Commissioner of Taxation [1972] HCA 49. In

the present case, the expenditure of 145 $ against purchase of shirt and trousers though

they are to be worn at office is not related to profession anyhow. Thus it cannot be

claimed to be deducted.

g) Under section 8.1 of the Income Tax Assessment Act 1997 (Cth), it is stated that any

expenditure in connection with the income earning process of an individual can be

assessed subjected to deductions. Claim against such deduction can be claimed if the tax

payer is able to show such expenditure is not in connection with any domestic or personal

reason instead connected with income earning. This is also supported in the judgment

21 The Income Tax Assessment Act 1997 (Cth) s 8.1.

e) Under section 8.1 of the Income Tax Assessment Act21, it is stated that any expenditure in

connection with the income earning process of an individual can be assessed subjected to

deductions. Claim against such deduction can be claimed if the tax payer is able to show

such expenditure is not in connection with any domestic or personal reason instead

connected with income earning. This is also supported in the judgment provided in the

case of Lodge v Federal Commissioner of Taxation [1972] HCA 49. In this case, the

expenditure of 250 $ for repairing the fridge is absolutely related to domestic reason and

not involves anything related to profession of such trainee accountant. Thus it cannot be

subjected to deduction.

f) Under section 8.1 of the Income Tax Assessment Act 1997 (Cth), it is stated that any

expenditure in connection with the income earning process of an individual can be

assessed subjected to deductions. Claim against such deduction can be claimed if the tax

payer is able to show such expenditure is not in connection with any domestic or personal

reason instead connected with income earning. This is also supported in the judgment

provided in the case of Lodge v Federal Commissioner of Taxation [1972] HCA 49. In

the present case, the expenditure of 145 $ against purchase of shirt and trousers though

they are to be worn at office is not related to profession anyhow. Thus it cannot be

claimed to be deducted.

g) Under section 8.1 of the Income Tax Assessment Act 1997 (Cth), it is stated that any

expenditure in connection with the income earning process of an individual can be

assessed subjected to deductions. Claim against such deduction can be claimed if the tax

payer is able to show such expenditure is not in connection with any domestic or personal

reason instead connected with income earning. This is also supported in the judgment

21 The Income Tax Assessment Act 1997 (Cth) s 8.1.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

provided in the case of Lodge v Federal Commissioner of Taxation [1972] HCA 49. In

the present case it is seen that 300 $ is expensed for legal purposes for writing a contract

related to employment with the new employer although related to profession of an

individual but it is not covered under assessable income of a taxpayer. Hence such

expense is not allowed to be deducted.

Answer 4:

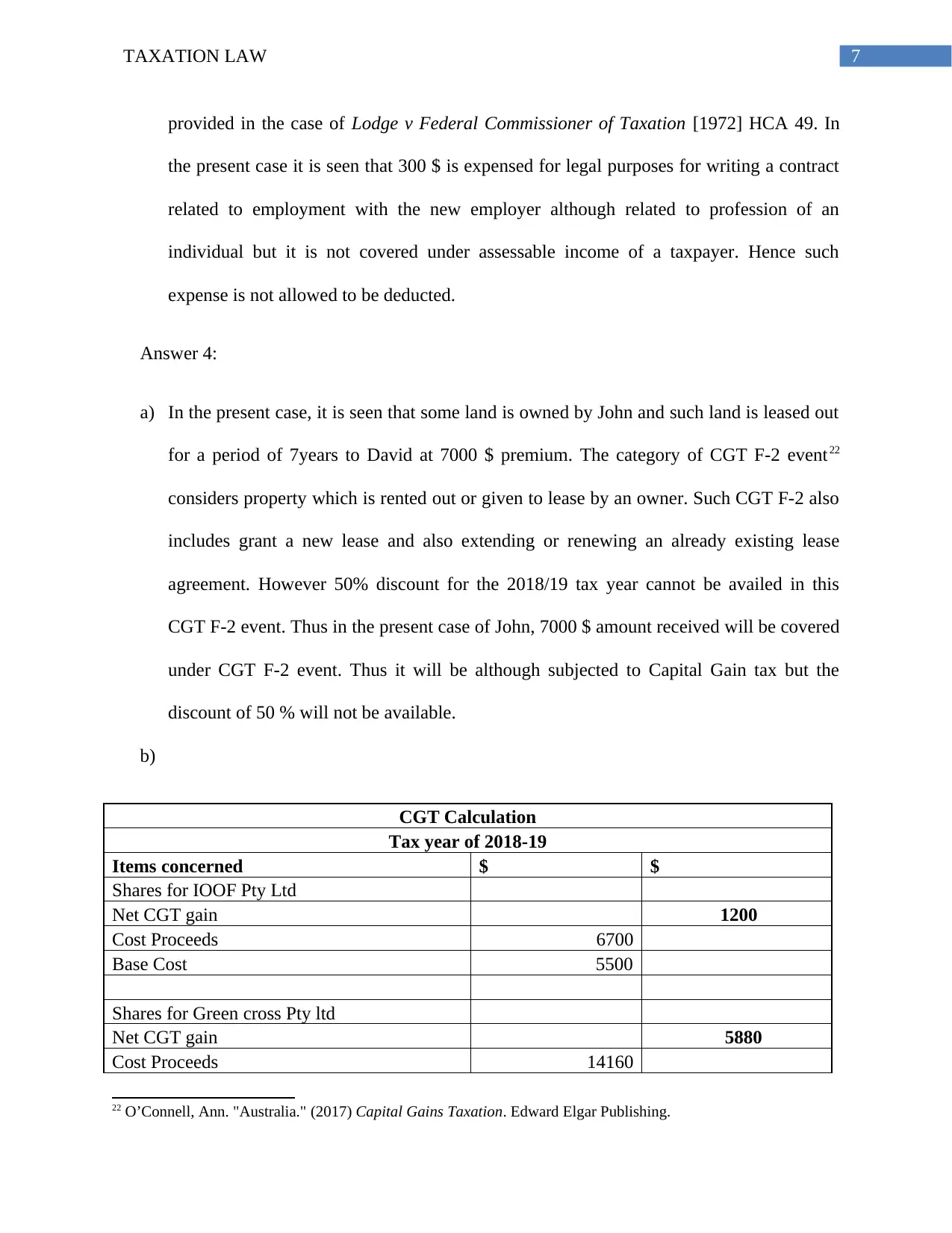

a) In the present case, it is seen that some land is owned by John and such land is leased out

for a period of 7years to David at 7000 $ premium. The category of CGT F-2 event22

considers property which is rented out or given to lease by an owner. Such CGT F-2 also

includes grant a new lease and also extending or renewing an already existing lease

agreement. However 50% discount for the 2018/19 tax year cannot be availed in this

CGT F-2 event. Thus in the present case of John, 7000 $ amount received will be covered

under CGT F-2 event. Thus it will be although subjected to Capital Gain tax but the

discount of 50 % will not be available.

b)

CGT Calculation

Tax year of 2018-19

Items concerned $ $

Shares for IOOF Pty Ltd

Net CGT gain 1200

Cost Proceeds 6700

Base Cost 5500

Shares for Green cross Pty ltd

Net CGT gain 5880

Cost Proceeds 14160

22 O’Connell, Ann. "Australia." (2017) Capital Gains Taxation. Edward Elgar Publishing.

provided in the case of Lodge v Federal Commissioner of Taxation [1972] HCA 49. In

the present case it is seen that 300 $ is expensed for legal purposes for writing a contract

related to employment with the new employer although related to profession of an

individual but it is not covered under assessable income of a taxpayer. Hence such

expense is not allowed to be deducted.

Answer 4:

a) In the present case, it is seen that some land is owned by John and such land is leased out

for a period of 7years to David at 7000 $ premium. The category of CGT F-2 event22

considers property which is rented out or given to lease by an owner. Such CGT F-2 also

includes grant a new lease and also extending or renewing an already existing lease

agreement. However 50% discount for the 2018/19 tax year cannot be availed in this

CGT F-2 event. Thus in the present case of John, 7000 $ amount received will be covered

under CGT F-2 event. Thus it will be although subjected to Capital Gain tax but the

discount of 50 % will not be available.

b)

CGT Calculation

Tax year of 2018-19

Items concerned $ $

Shares for IOOF Pty Ltd

Net CGT gain 1200

Cost Proceeds 6700

Base Cost 5500

Shares for Green cross Pty ltd

Net CGT gain 5880

Cost Proceeds 14160

22 O’Connell, Ann. "Australia." (2017) Capital Gains Taxation. Edward Elgar Publishing.

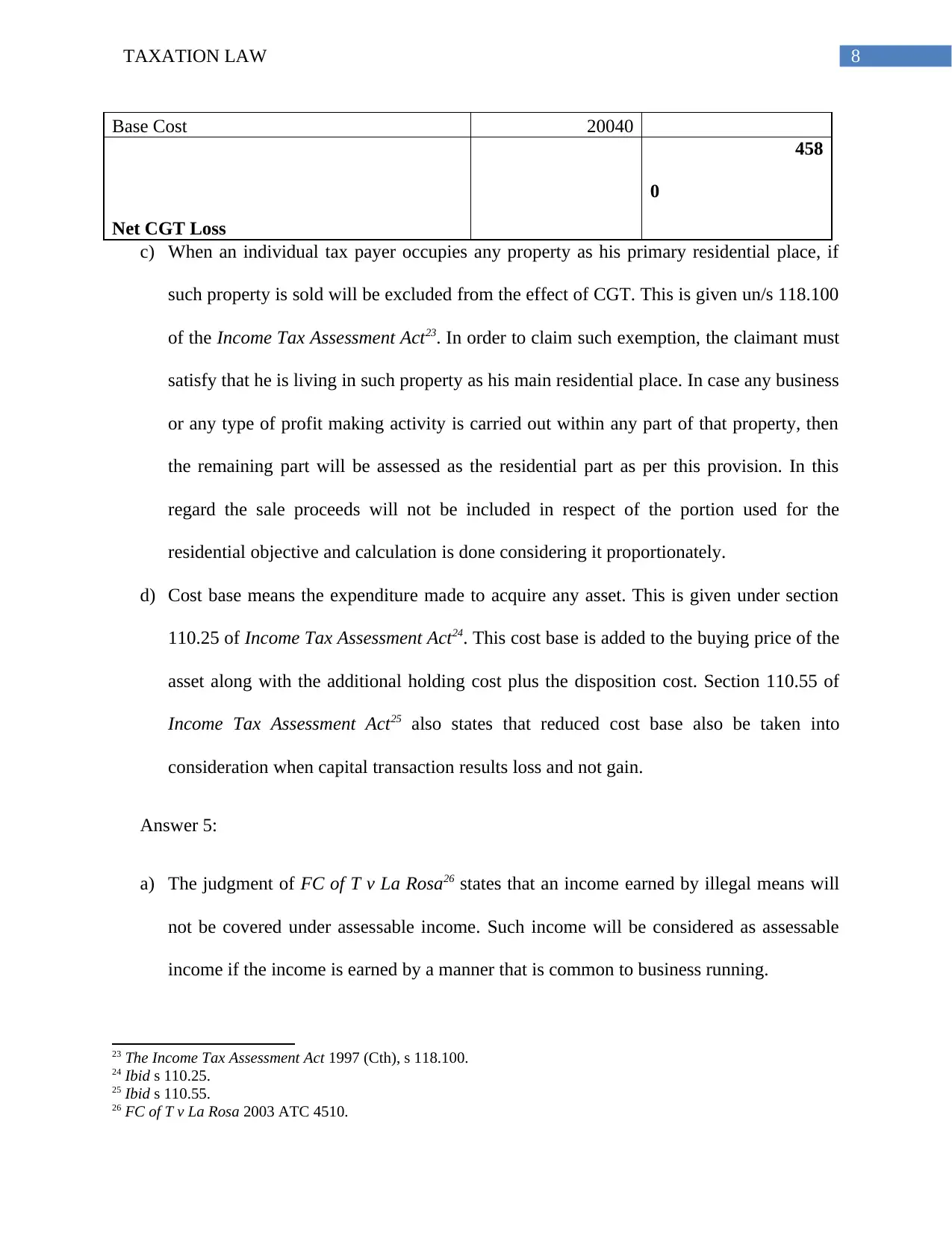

8TAXATION LAW

Base Cost 20040

Net CGT Loss

458

0

c) When an individual tax payer occupies any property as his primary residential place, if

such property is sold will be excluded from the effect of CGT. This is given un/s 118.100

of the Income Tax Assessment Act23. In order to claim such exemption, the claimant must

satisfy that he is living in such property as his main residential place. In case any business

or any type of profit making activity is carried out within any part of that property, then

the remaining part will be assessed as the residential part as per this provision. In this

regard the sale proceeds will not be included in respect of the portion used for the

residential objective and calculation is done considering it proportionately.

d) Cost base means the expenditure made to acquire any asset. This is given under section

110.25 of Income Tax Assessment Act24. This cost base is added to the buying price of the

asset along with the additional holding cost plus the disposition cost. Section 110.55 of

Income Tax Assessment Act25 also states that reduced cost base also be taken into

consideration when capital transaction results loss and not gain.

Answer 5:

a) The judgment of FC of T v La Rosa26 states that an income earned by illegal means will

not be covered under assessable income. Such income will be considered as assessable

income if the income is earned by a manner that is common to business running.

23 The Income Tax Assessment Act 1997 (Cth), s 118.100.

24 Ibid s 110.25.

25 Ibid s 110.55.

26 FC of T v La Rosa 2003 ATC 4510.

Base Cost 20040

Net CGT Loss

458

0

c) When an individual tax payer occupies any property as his primary residential place, if

such property is sold will be excluded from the effect of CGT. This is given un/s 118.100

of the Income Tax Assessment Act23. In order to claim such exemption, the claimant must

satisfy that he is living in such property as his main residential place. In case any business

or any type of profit making activity is carried out within any part of that property, then

the remaining part will be assessed as the residential part as per this provision. In this

regard the sale proceeds will not be included in respect of the portion used for the

residential objective and calculation is done considering it proportionately.

d) Cost base means the expenditure made to acquire any asset. This is given under section

110.25 of Income Tax Assessment Act24. This cost base is added to the buying price of the

asset along with the additional holding cost plus the disposition cost. Section 110.55 of

Income Tax Assessment Act25 also states that reduced cost base also be taken into

consideration when capital transaction results loss and not gain.

Answer 5:

a) The judgment of FC of T v La Rosa26 states that an income earned by illegal means will

not be covered under assessable income. Such income will be considered as assessable

income if the income is earned by a manner that is common to business running.

23 The Income Tax Assessment Act 1997 (Cth), s 118.100.

24 Ibid s 110.25.

25 Ibid s 110.55.

26 FC of T v La Rosa 2003 ATC 4510.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

b) An income earned by renting will be an ordinary income as per the judgment given in

Adelaide Fruit and Produce Exchange Co Ltd v DFC of T 27. However an income out of

gambling in a casino is not covered within usual business. This is supported by the

decision given in case of Evans v. F.C. of T28. In the present case, 500 $ as bank interest

and 2000 $ as income out of rent will be considered as assessable income of a resident

tax payer. However, income arising out of casino cannot be regarded as assessable

income.

c) Section 15.2 of the Income Tax Assessment Act 29states that any sum of money given by

an employer to his employee will be the employee’s assessable income. Hence in this

case, 500 $ given as allowance by the employer to his employee will be the assessable

income of the employee as per this section.

d) For a taxable income of 20000 $ Medicare levy cannot be allowed.

For income of 24900 $, the levy is 2 % of it, which is 498 $.

For income of 100, 000 $, levy is 2 % of it, which amounts to 2000 $.

e) For 25000 $ income, taxation rate as applicable is 19 % for income exceeding 18200 $.

Thus,

{(25,000$ – 18,200$) * 19%} = (6,800$ * 19%) = 1,292$.

So, gross tax payable= 1292 $.

For 40,000 $ income, the taxation rate applicable is 3572$, 32.5% above 37000$.

Thus,

3,572$ + {(40,000-37,000) * 32.5%} = {3,572$ + (3000$ *32.5% )} = ($3,572 + $975)=

4547 $.

27 Adelaide Fruit and Produce Exchange Co Ltd v DFC of T (1932) 2 ATD 1.

28 Evans v. F.C. of T. 89 ATC 4540.

29 The Income Tax Assessment Act 1997 (Cth) s15.2.

b) An income earned by renting will be an ordinary income as per the judgment given in

Adelaide Fruit and Produce Exchange Co Ltd v DFC of T 27. However an income out of

gambling in a casino is not covered within usual business. This is supported by the

decision given in case of Evans v. F.C. of T28. In the present case, 500 $ as bank interest

and 2000 $ as income out of rent will be considered as assessable income of a resident

tax payer. However, income arising out of casino cannot be regarded as assessable

income.

c) Section 15.2 of the Income Tax Assessment Act 29states that any sum of money given by

an employer to his employee will be the employee’s assessable income. Hence in this

case, 500 $ given as allowance by the employer to his employee will be the assessable

income of the employee as per this section.

d) For a taxable income of 20000 $ Medicare levy cannot be allowed.

For income of 24900 $, the levy is 2 % of it, which is 498 $.

For income of 100, 000 $, levy is 2 % of it, which amounts to 2000 $.

e) For 25000 $ income, taxation rate as applicable is 19 % for income exceeding 18200 $.

Thus,

{(25,000$ – 18,200$) * 19%} = (6,800$ * 19%) = 1,292$.

So, gross tax payable= 1292 $.

For 40,000 $ income, the taxation rate applicable is 3572$, 32.5% above 37000$.

Thus,

3,572$ + {(40,000-37,000) * 32.5%} = {3,572$ + (3000$ *32.5% )} = ($3,572 + $975)=

4547 $.

27 Adelaide Fruit and Produce Exchange Co Ltd v DFC of T (1932) 2 ATD 1.

28 Evans v. F.C. of T. 89 ATC 4540.

29 The Income Tax Assessment Act 1997 (Cth) s15.2.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

So, gross tax payable= 4547 dollars.

For 95000 $, taxation rate applied is 20797$ and 37 percent above 90000 $.

Thus,

20797$+ {(95000-90000)$*37%= 20797$ + 5000$ * 37%= 20797$+ 1850$= 22647$

So, gross tax payable= 22647 dollars.

So, gross tax payable= 4547 dollars.

For 95000 $, taxation rate applied is 20797$ and 37 percent above 90000 $.

Thus,

20797$+ {(95000-90000)$*37%= 20797$ + 5000$ * 37%= 20797$+ 1850$= 22647$

So, gross tax payable= 22647 dollars.

11TAXATION LAW

References:

Books and Journals:

O’Connell, Ann. "Australia." (2017) Capital Gains Taxation. Edward Elgar Publishing

Jones, Daryl. "Complexity of tax residency attracts review." (2018) Taxation in Australia 53.6:

296

Cases:

Adelaide Fruit and Produce Exchange Co Ltd v DFC of T (1932) 2 ATD 1

Evans v. F.C. of T. 89 ATC 4540

F.C. of T. v. Jenkins 82 ATC 4098

FC of T v Applegate 79 ATC 4307

FC of T v La Rosa 2003 ATC 4510

Hayes v FCT (1956) 96 CLR 47

I.R.C. v. Lysaght (1928) A.C.234

Levene v. I.R.C.(1928) A.C.217

Lodge v Federal Commissioner of Taxation [1972] HCA 49

Legislation:

The Income Tax Assessment Act 1936 (Cth)

The Income Tax Assessment Act 1997 (Cth)

References:

Books and Journals:

O’Connell, Ann. "Australia." (2017) Capital Gains Taxation. Edward Elgar Publishing

Jones, Daryl. "Complexity of tax residency attracts review." (2018) Taxation in Australia 53.6:

296

Cases:

Adelaide Fruit and Produce Exchange Co Ltd v DFC of T (1932) 2 ATD 1

Evans v. F.C. of T. 89 ATC 4540

F.C. of T. v. Jenkins 82 ATC 4098

FC of T v Applegate 79 ATC 4307

FC of T v La Rosa 2003 ATC 4510

Hayes v FCT (1956) 96 CLR 47

I.R.C. v. Lysaght (1928) A.C.234

Levene v. I.R.C.(1928) A.C.217

Lodge v Federal Commissioner of Taxation [1972] HCA 49

Legislation:

The Income Tax Assessment Act 1936 (Cth)

The Income Tax Assessment Act 1997 (Cth)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.