HI6028 Taxation Law T3 2018: Partnership Income & FBT Analysis

VerifiedAdded on 2023/04/23

|13

|2737

|310

Homework Assignment

AI Summary

This assignment provides a detailed analysis of taxation law, focusing on partnership income assessment and fringe benefit tax implications. It addresses two key questions: the assessment of net income from a partnership under Section 90 of ITAA 1936, and the fringe benefit tax liability of an employer for benefits provided to an employee under Section 20 and Section 25 of FBTAA 1986. The first question involves determining the net income of a partnership, taking into account assessable income and allowable deductions, with specific attention to ordinary income, deductible repairs, and private expenses. The second question examines the fringe benefit tax consequences for both expense payments and housing benefits provided to an employee, including the calculation of taxable values based on market rates and employee contributions. The assignment uses relevant sections of the ITAA and FBTAA, along with case law and ATO rulings, to support its analysis and conclusions.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................7

References:...............................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................7

References:...............................................................................................................................10

2TAXATION LAW

Answer to question 1:

Issues

Are the taxpayers net income from the partnership made during the year of taxation

will be considered for assessment purpose under “sect 90, ITAA 1936”?

Rule:

For the purpose of income tax under “section 995-1, ITAA 1997” the definition of

partnership comprises of including the receipts made from the joint incomes of the property,

service contracts and business agreements (Tondani 2016). Conferring to the “section 995-

1”, partnership is better understood as the conducting of business activities as the partners or

getting the ordinary income and the statutory income together. To determine the partnership

net income reference should be made to the “section 90, ITAA 1936”. The net earnings of

partnership is in respect of the assessable income that is computed where the partnership was

the resident taxpayer after deducting the permissible deductions (Fairfield and Jorratt De Luis

2016).

The assessable income is held liable for taxation since it is added to the taxable

income. Mentioning “section 6-5, ITAA 1997” ordinary income includes the income made

from the ordinary concepts (Parker 2018). In “Scott v CT (1935)” the court stated that

income based on the ordinary concepts requires the characterization that whether the gain has

the character of income and are in adherence with the ordinary concepts.

A taxpayer is permitted under “section 8-1, ITAA 1997” to claim for deduction from

their taxable income any losses or outgoings that is necessarily occurred while carrying out

the business with the intent of producing taxable income or occurred in producing or gaining

the chargeable earnings (Grace 2018). However, under the “sect (8-1 (2))”, no deduction is

Answer to question 1:

Issues

Are the taxpayers net income from the partnership made during the year of taxation

will be considered for assessment purpose under “sect 90, ITAA 1936”?

Rule:

For the purpose of income tax under “section 995-1, ITAA 1997” the definition of

partnership comprises of including the receipts made from the joint incomes of the property,

service contracts and business agreements (Tondani 2016). Conferring to the “section 995-

1”, partnership is better understood as the conducting of business activities as the partners or

getting the ordinary income and the statutory income together. To determine the partnership

net income reference should be made to the “section 90, ITAA 1936”. The net earnings of

partnership is in respect of the assessable income that is computed where the partnership was

the resident taxpayer after deducting the permissible deductions (Fairfield and Jorratt De Luis

2016).

The assessable income is held liable for taxation since it is added to the taxable

income. Mentioning “section 6-5, ITAA 1997” ordinary income includes the income made

from the ordinary concepts (Parker 2018). In “Scott v CT (1935)” the court stated that

income based on the ordinary concepts requires the characterization that whether the gain has

the character of income and are in adherence with the ordinary concepts.

A taxpayer is permitted under “section 8-1, ITAA 1997” to claim for deduction from

their taxable income any losses or outgoings that is necessarily occurred while carrying out

the business with the intent of producing taxable income or occurred in producing or gaining

the chargeable earnings (Grace 2018). However, under the “sect (8-1 (2))”, no deduction is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

permitted to the taxpayer for the loss or expenses if it satisfies any of the negative limbs. In

other words, a deduction is not allowed under the negative limbs for the expenses that are

capital, private or domestic in nature.

As per the “sect 25-10” allowable deduction is permitted for the repairs conducted on

the premises or the depreciating assets that is mainly used for generating income (Stevenson

et al. 2017). According to the “ATO TR 97/23” the item under repair should be used for

producing income for the purpose of repairs to be allowed as deductible under the “section

25-10”. This includes the repairs carried out in the course of business or made to the rental

property (Chen, Qi and Schlagenhauf 2018). There is some maintenance work that are treated

as repair under “sect 25-10”. This includes the painting done on the business buildings to

remedy the present worsening and prohibit the future deterioration.

On the other hand, if the replacement done is the part of the assets is allowed as

deductible repairs. The court in “Samuel Jones & Co (Devondale) Ltd v IRC” held the

replacement of chimney of a factory with the similar dimensions formed the inseparable

portion of the overall asset (Braithwaite and Reinhart 2019). As per the ATO, if any business

assets that is bought for $20,000 or below can be claimed as immediate deduction.

Application:

Daniel and Olivia are carrying on the business as partners within the meaning of

“section 995-1, ITAA 1997” and during the year of 2017 the made receipts from the

partnership. The receipts included the business sales in the form of cash payment and also

included the receipt of payment from the debtors. Mentioning “section 6-5, ITAA 1997”, the

cash receipts and payments from debtor’s amounts to ordinary income which is made the

partners from the ordinary concepts. Citing “Scott v CT (1935)” the business receipts had the

character of income and are in adherence with the ordinary concepts.

permitted to the taxpayer for the loss or expenses if it satisfies any of the negative limbs. In

other words, a deduction is not allowed under the negative limbs for the expenses that are

capital, private or domestic in nature.

As per the “sect 25-10” allowable deduction is permitted for the repairs conducted on

the premises or the depreciating assets that is mainly used for generating income (Stevenson

et al. 2017). According to the “ATO TR 97/23” the item under repair should be used for

producing income for the purpose of repairs to be allowed as deductible under the “section

25-10”. This includes the repairs carried out in the course of business or made to the rental

property (Chen, Qi and Schlagenhauf 2018). There is some maintenance work that are treated

as repair under “sect 25-10”. This includes the painting done on the business buildings to

remedy the present worsening and prohibit the future deterioration.

On the other hand, if the replacement done is the part of the assets is allowed as

deductible repairs. The court in “Samuel Jones & Co (Devondale) Ltd v IRC” held the

replacement of chimney of a factory with the similar dimensions formed the inseparable

portion of the overall asset (Braithwaite and Reinhart 2019). As per the ATO, if any business

assets that is bought for $20,000 or below can be claimed as immediate deduction.

Application:

Daniel and Olivia are carrying on the business as partners within the meaning of

“section 995-1, ITAA 1997” and during the year of 2017 the made receipts from the

partnership. The receipts included the business sales in the form of cash payment and also

included the receipt of payment from the debtors. Mentioning “section 6-5, ITAA 1997”, the

cash receipts and payments from debtor’s amounts to ordinary income which is made the

partners from the ordinary concepts. Citing “Scott v CT (1935)” the business receipts had the

character of income and are in adherence with the ordinary concepts.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Daniel and Olivia reported certain partnership expenses such as council rates,

electricity bill, car expenses, union fees, loan repayment etc. These expenses were necessarily

occurred while carrying on the partnership business and hence will be allowed as deductible

expenses under the general provision of “sect 8-1, ITAA 1997”.

The partners also reported certain drawings of cash and goods for their private purpose. The

drawings made by Daniel and Olivia satisfies the negative limbs of “section (8-1 (2))” and

non-deductible because they are private in nature.

The repairs and maintenance in the form of shop painting will be allowable

deductions under “section 25-10”. The painting on the business premises was done to remedy

the present worsening and prohibit the future deterioration. Similarly, referring to “Samuel

Jones & Co (Devondale) Ltd v IRC” the replacement of refrigerator motor constitutes

deductible repairs under “section 25-10” (Kess, Grimaldi and Revels 2017). The business

also installed the air-condition for $1,200. The cost of air condition is below $20,000 of the

ATO stated rules for claiming immediate deduction. Referring to “section 90, ITAA 1936”

the net income of partnership less allowable deductions is computed below;

Daniel and Olivia reported certain partnership expenses such as council rates,

electricity bill, car expenses, union fees, loan repayment etc. These expenses were necessarily

occurred while carrying on the partnership business and hence will be allowed as deductible

expenses under the general provision of “sect 8-1, ITAA 1997”.

The partners also reported certain drawings of cash and goods for their private purpose. The

drawings made by Daniel and Olivia satisfies the negative limbs of “section (8-1 (2))” and

non-deductible because they are private in nature.

The repairs and maintenance in the form of shop painting will be allowable

deductions under “section 25-10”. The painting on the business premises was done to remedy

the present worsening and prohibit the future deterioration. Similarly, referring to “Samuel

Jones & Co (Devondale) Ltd v IRC” the replacement of refrigerator motor constitutes

deductible repairs under “section 25-10” (Kess, Grimaldi and Revels 2017). The business

also installed the air-condition for $1,200. The cost of air condition is below $20,000 of the

ATO stated rules for claiming immediate deduction. Referring to “section 90, ITAA 1936”

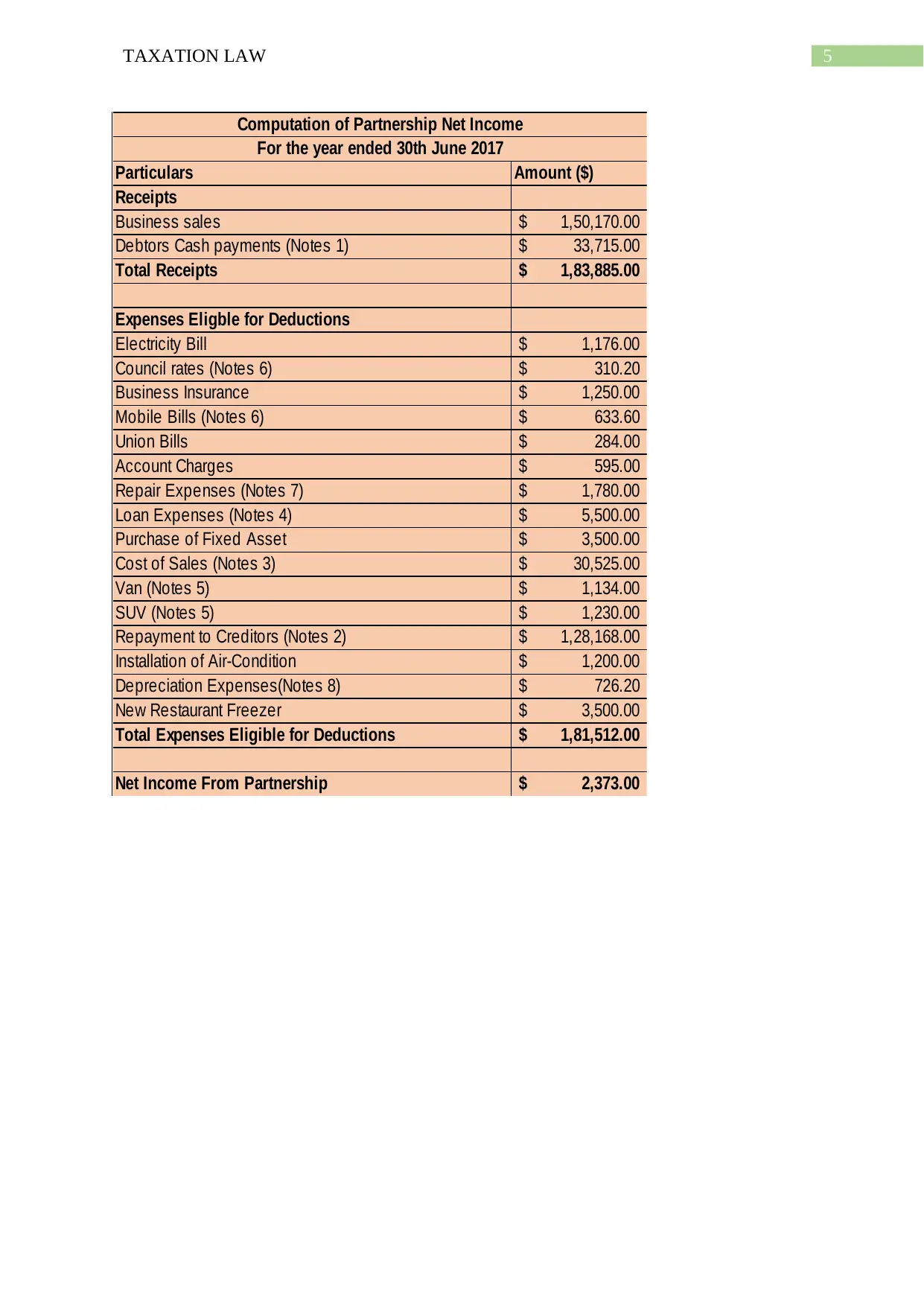

the net income of partnership less allowable deductions is computed below;

5TAXATION LAW

Particulars Amount ($)

Receipts

Business sales 1,50,170.00$

Debtors Cash payments (Notes 1) 33,715.00$

Total Receipts 1,83,885.00$

Expenses Eligble for Deductions

Electricity Bill 1,176.00$

Council rates (Notes 6) 310.20$

Business Insurance 1,250.00$

Mobile Bills (Notes 6) 633.60$

Union Bills 284.00$

Account Charges 595.00$

Repair Expenses (Notes 7) 1,780.00$

Loan Expenses (Notes 4) 5,500.00$

Purchase of Fixed Asset 3,500.00$

Cost of Sales (Notes 3) 30,525.00$

Van (Notes 5) 1,134.00$

SUV (Notes 5) 1,230.00$

Repayment to Creditors (Notes 2) 1,28,168.00$

Installation of Air-Condition 1,200.00$

Depreciation Expenses(Notes 8) 726.20$

New Restaurant Freezer 3,500.00$

Total Expenses Eligible for Deductions 1,81,512.00$

Net Income From Partnership 2,373.00$

Computation of Partnership Net Income

For the year ended 30th June 2017

Particulars Amount ($)

Receipts

Business sales 1,50,170.00$

Debtors Cash payments (Notes 1) 33,715.00$

Total Receipts 1,83,885.00$

Expenses Eligble for Deductions

Electricity Bill 1,176.00$

Council rates (Notes 6) 310.20$

Business Insurance 1,250.00$

Mobile Bills (Notes 6) 633.60$

Union Bills 284.00$

Account Charges 595.00$

Repair Expenses (Notes 7) 1,780.00$

Loan Expenses (Notes 4) 5,500.00$

Purchase of Fixed Asset 3,500.00$

Cost of Sales (Notes 3) 30,525.00$

Van (Notes 5) 1,134.00$

SUV (Notes 5) 1,230.00$

Repayment to Creditors (Notes 2) 1,28,168.00$

Installation of Air-Condition 1,200.00$

Depreciation Expenses(Notes 8) 726.20$

New Restaurant Freezer 3,500.00$

Total Expenses Eligible for Deductions 1,81,512.00$

Net Income From Partnership 2,373.00$

Computation of Partnership Net Income

For the year ended 30th June 2017

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

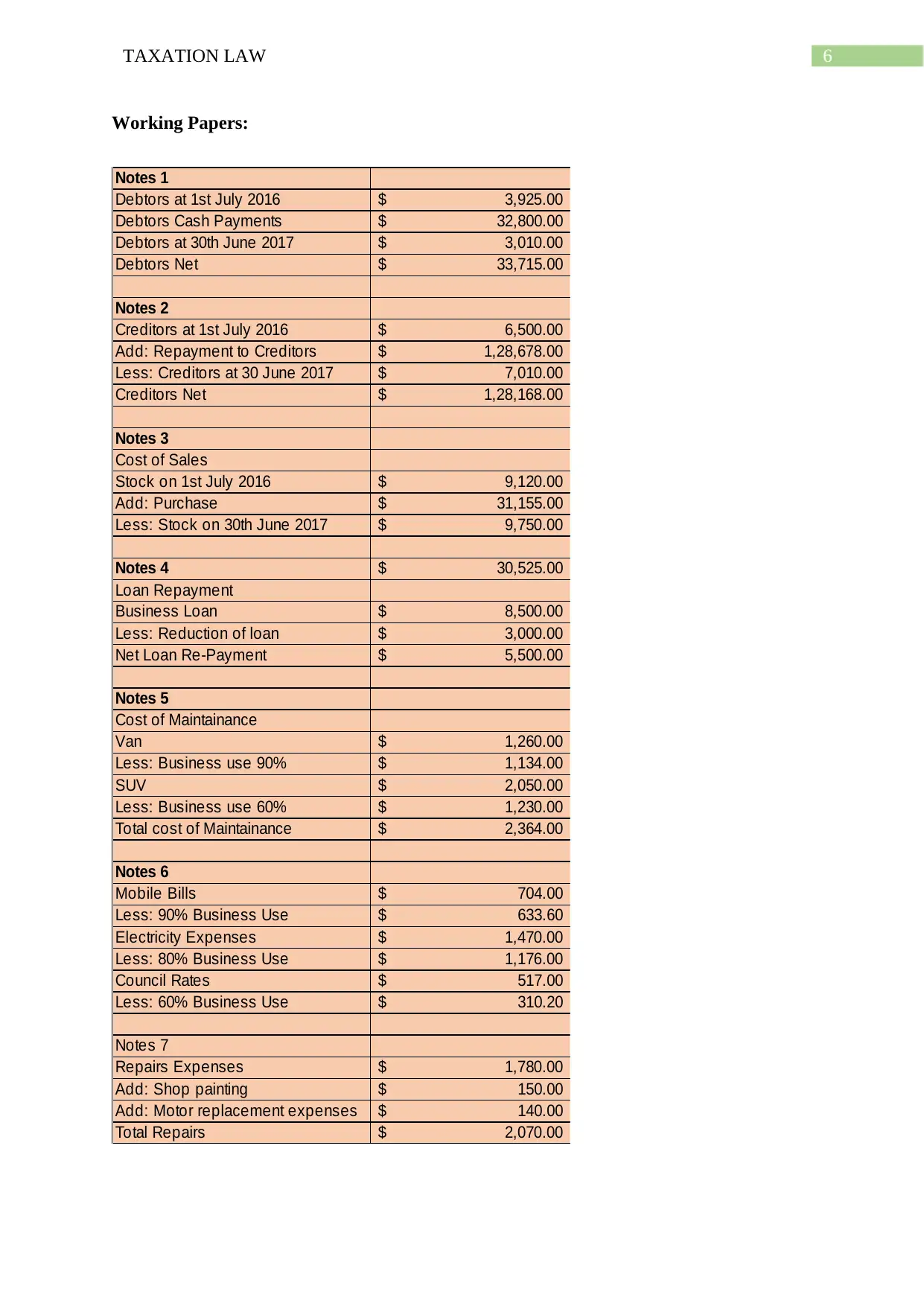

Working Papers:

Notes 1

Debtors at 1st July 2016 3,925.00$

Debtors Cash Payments 32,800.00$

Debtors at 30th June 2017 3,010.00$

Debtors Net 33,715.00$

Notes 2

Creditors at 1st July 2016 6,500.00$

Add: Repayment to Creditors 1,28,678.00$

Less: Creditors at 30 June 2017 7,010.00$

Creditors Net 1,28,168.00$

Notes 3

Cost of Sales

Stock on 1st July 2016 9,120.00$

Add: Purchase 31,155.00$

Less: Stock on 30th June 2017 9,750.00$

Notes 4 30,525.00$

Loan Repayment

Business Loan 8,500.00$

Less: Reduction of loan 3,000.00$

Net Loan Re-Payment 5,500.00$

Notes 5

Cost of Maintainance

Van 1,260.00$

Less: Business use 90% 1,134.00$

SUV 2,050.00$

Less: Business use 60% 1,230.00$

Total cost of Maintainance 2,364.00$

Notes 6

Mobile Bills 704.00$

Less: 90% Business Use 633.60$

Electricity Expenses 1,470.00$

Less: 80% Business Use 1,176.00$

Council Rates 517.00$

Less: 60% Business Use 310.20$

Notes 7

Repairs Expenses 1,780.00$

Add: Shop painting 150.00$

Add: Motor replacement expenses 140.00$

Total Repairs 2,070.00$

Working Papers:

Notes 1

Debtors at 1st July 2016 3,925.00$

Debtors Cash Payments 32,800.00$

Debtors at 30th June 2017 3,010.00$

Debtors Net 33,715.00$

Notes 2

Creditors at 1st July 2016 6,500.00$

Add: Repayment to Creditors 1,28,678.00$

Less: Creditors at 30 June 2017 7,010.00$

Creditors Net 1,28,168.00$

Notes 3

Cost of Sales

Stock on 1st July 2016 9,120.00$

Add: Purchase 31,155.00$

Less: Stock on 30th June 2017 9,750.00$

Notes 4 30,525.00$

Loan Repayment

Business Loan 8,500.00$

Less: Reduction of loan 3,000.00$

Net Loan Re-Payment 5,500.00$

Notes 5

Cost of Maintainance

Van 1,260.00$

Less: Business use 90% 1,134.00$

SUV 2,050.00$

Less: Business use 60% 1,230.00$

Total cost of Maintainance 2,364.00$

Notes 6

Mobile Bills 704.00$

Less: 90% Business Use 633.60$

Electricity Expenses 1,470.00$

Less: 80% Business Use 1,176.00$

Council Rates 517.00$

Less: 60% Business Use 310.20$

Notes 7

Repairs Expenses 1,780.00$

Add: Shop painting 150.00$

Add: Motor replacement expenses 140.00$

Total Repairs 2,070.00$

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

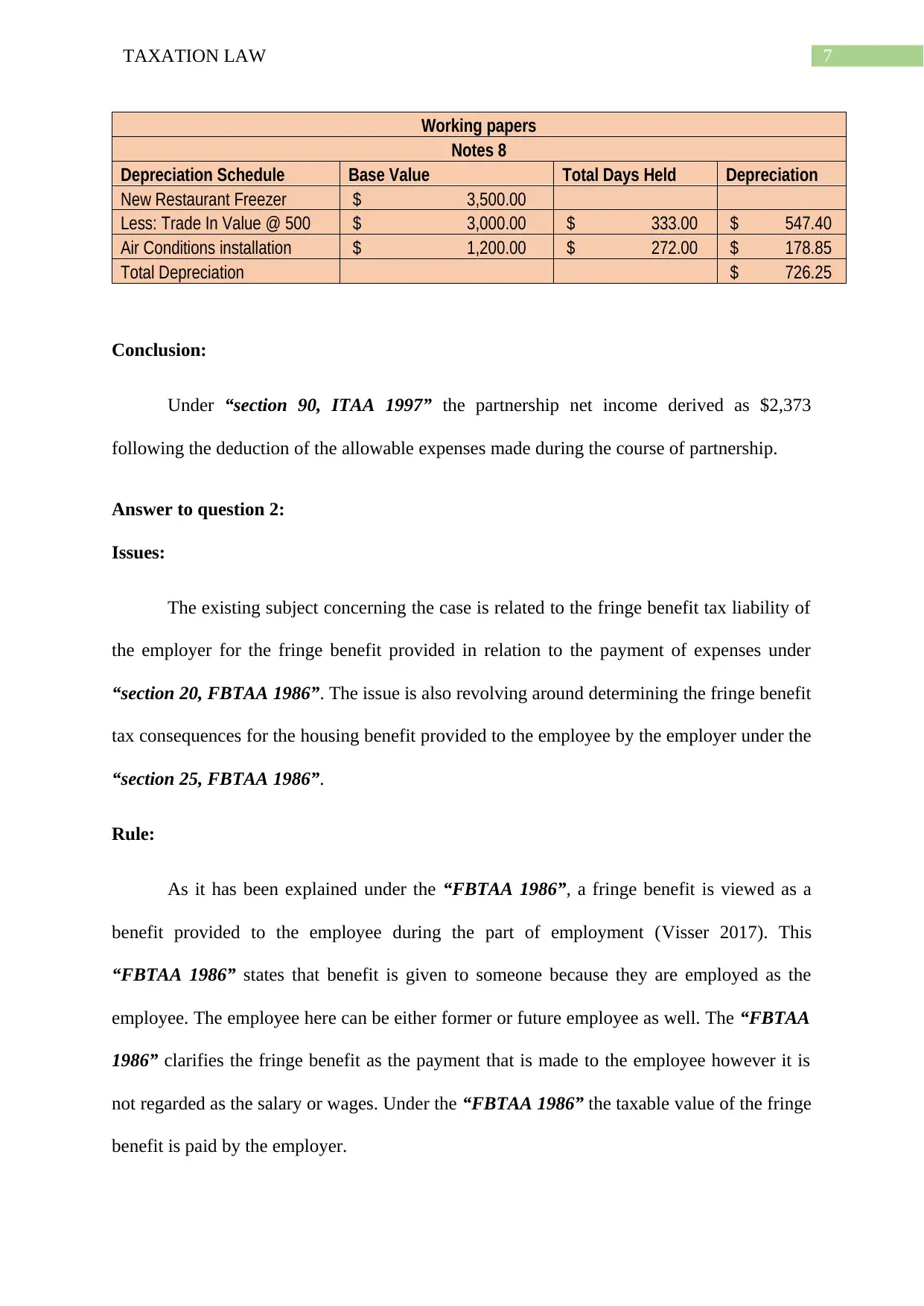

Working papers

Notes 8

Depreciation Schedule Base Value Total Days Held Depreciation

New Restaurant Freezer $ 3,500.00

Less: Trade In Value @ 500 $ 3,000.00 $ 333.00 $ 547.40

Air Conditions installation $ 1,200.00 $ 272.00 $ 178.85

Total Depreciation $ 726.25

Conclusion:

Under “section 90, ITAA 1997” the partnership net income derived as $2,373

following the deduction of the allowable expenses made during the course of partnership.

Answer to question 2:

Issues:

The existing subject concerning the case is related to the fringe benefit tax liability of

the employer for the fringe benefit provided in relation to the payment of expenses under

“section 20, FBTAA 1986”. The issue is also revolving around determining the fringe benefit

tax consequences for the housing benefit provided to the employee by the employer under the

“section 25, FBTAA 1986”.

Rule:

As it has been explained under the “FBTAA 1986”, a fringe benefit is viewed as a

benefit provided to the employee during the part of employment (Visser 2017). This

“FBTAA 1986” states that benefit is given to someone because they are employed as the

employee. The employee here can be either former or future employee as well. The “FBTAA

1986” clarifies the fringe benefit as the payment that is made to the employee however it is

not regarded as the salary or wages. Under the “FBTAA 1986” the taxable value of the fringe

benefit is paid by the employer.

Working papers

Notes 8

Depreciation Schedule Base Value Total Days Held Depreciation

New Restaurant Freezer $ 3,500.00

Less: Trade In Value @ 500 $ 3,000.00 $ 333.00 $ 547.40

Air Conditions installation $ 1,200.00 $ 272.00 $ 178.85

Total Depreciation $ 726.25

Conclusion:

Under “section 90, ITAA 1997” the partnership net income derived as $2,373

following the deduction of the allowable expenses made during the course of partnership.

Answer to question 2:

Issues:

The existing subject concerning the case is related to the fringe benefit tax liability of

the employer for the fringe benefit provided in relation to the payment of expenses under

“section 20, FBTAA 1986”. The issue is also revolving around determining the fringe benefit

tax consequences for the housing benefit provided to the employee by the employer under the

“section 25, FBTAA 1986”.

Rule:

As it has been explained under the “FBTAA 1986”, a fringe benefit is viewed as a

benefit provided to the employee during the part of employment (Visser 2017). This

“FBTAA 1986” states that benefit is given to someone because they are employed as the

employee. The employee here can be either former or future employee as well. The “FBTAA

1986” clarifies the fringe benefit as the payment that is made to the employee however it is

not regarded as the salary or wages. Under the “FBTAA 1986” the taxable value of the fringe

benefit is paid by the employer.

8TAXATION LAW

The expense payment fringe benefit under “section 20, FBTAA 1986” implies the

payment of expenses by the employer in discharge of the recipient obligations either whole or

in part to the amount to the third party that is occurred by the recipient. In addition to this,

“section 23 of the FBTAA 1986” is related with the taxable value of the expenditure

payment fringe benefit (Henry, Plesko and Utke 2018). Subjected to the “section 23, FBTAA

1986” the taxable value of the expense payment fringe benefit is related to the year in which

the benefit is provided. In other words, the employer would be liable for the chargeable value

of the expense payment fringe benefit made during the year of taxation.

Conferring to the “section 25 of the FBTAA 1986” the housing benefits is

subsistence for whole or part of the year of tax is the right of housing provided by the

provider (employer) to the recipient (employee) would be taken into account as the benefit

given by the employer to the recipient in relation to the taxation year.

The determination of the market value of the housing right is given under the “section

27 of the FBTAA 1986” (Easton 2015). As per the “sect 27 (1), FBTAA 1986” the

chargeable value of the market rental value represents the rights of using the accommodation

which is further reduced by the rental payments that is contributed by the employee.

Application:

The case study opens up with the information that the John worked as the executive in

the printing company. The employer here as the salary package paid the private school fess of

his child. The cost of school fees was $15,000. Following the payment of the school fees it

resulted in the expense payment fringe benefit under “section 20, FBTAA 1986” for the

employer of John. This implies the payment of expenses by the employer was in discharge of

the John responsibilities for the whole amount to the third party that is occurred by the

recipient in this case.

The expense payment fringe benefit under “section 20, FBTAA 1986” implies the

payment of expenses by the employer in discharge of the recipient obligations either whole or

in part to the amount to the third party that is occurred by the recipient. In addition to this,

“section 23 of the FBTAA 1986” is related with the taxable value of the expenditure

payment fringe benefit (Henry, Plesko and Utke 2018). Subjected to the “section 23, FBTAA

1986” the taxable value of the expense payment fringe benefit is related to the year in which

the benefit is provided. In other words, the employer would be liable for the chargeable value

of the expense payment fringe benefit made during the year of taxation.

Conferring to the “section 25 of the FBTAA 1986” the housing benefits is

subsistence for whole or part of the year of tax is the right of housing provided by the

provider (employer) to the recipient (employee) would be taken into account as the benefit

given by the employer to the recipient in relation to the taxation year.

The determination of the market value of the housing right is given under the “section

27 of the FBTAA 1986” (Easton 2015). As per the “sect 27 (1), FBTAA 1986” the

chargeable value of the market rental value represents the rights of using the accommodation

which is further reduced by the rental payments that is contributed by the employee.

Application:

The case study opens up with the information that the John worked as the executive in

the printing company. The employer here as the salary package paid the private school fess of

his child. The cost of school fees was $15,000. Following the payment of the school fees it

resulted in the expense payment fringe benefit under “section 20, FBTAA 1986” for the

employer of John. This implies the payment of expenses by the employer was in discharge of

the John responsibilities for the whole amount to the third party that is occurred by the

recipient in this case.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Subjected to the “section 23, FBTAA 1986” the taxable value of the expense payment

fringe benefit is related to the year in which the school fees were paid by the John’s

employer. John’s employer would be liable for the chargeable value of the expense payment

fringe benefit made during the year of taxation.

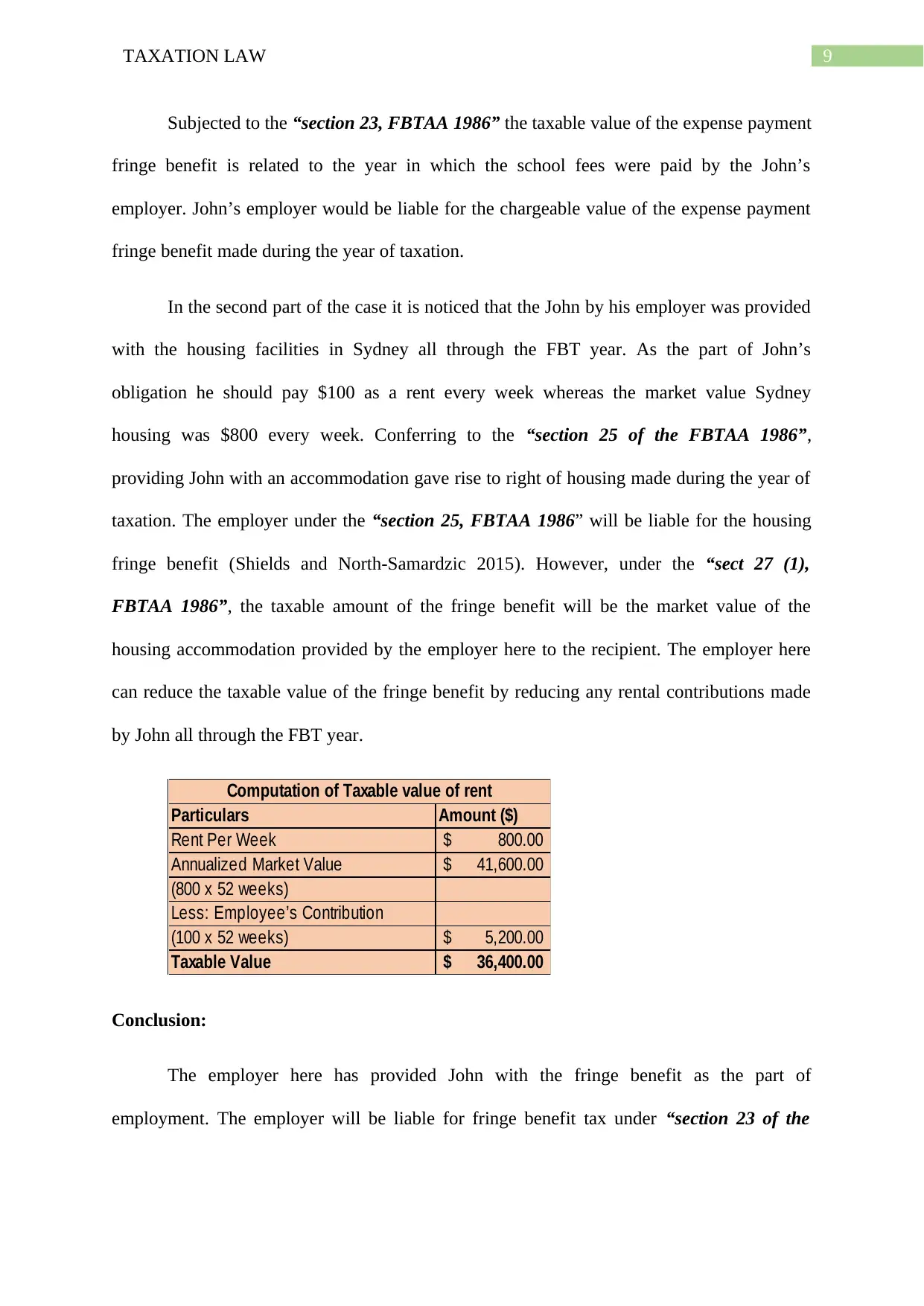

In the second part of the case it is noticed that the John by his employer was provided

with the housing facilities in Sydney all through the FBT year. As the part of John’s

obligation he should pay $100 as a rent every week whereas the market value Sydney

housing was $800 every week. Conferring to the “section 25 of the FBTAA 1986”,

providing John with an accommodation gave rise to right of housing made during the year of

taxation. The employer under the “section 25, FBTAA 1986” will be liable for the housing

fringe benefit (Shields and North-Samardzic 2015). However, under the “sect 27 (1),

FBTAA 1986”, the taxable amount of the fringe benefit will be the market value of the

housing accommodation provided by the employer here to the recipient. The employer here

can reduce the taxable value of the fringe benefit by reducing any rental contributions made

by John all through the FBT year.

Particulars Amount ($)

Rent Per Week 800.00$

Annualized Market Value 41,600.00$

(800 x 52 weeks)

Less: Employee’s Contribution

(100 x 52 weeks) 5,200.00$

Taxable Value 36,400.00$

Computation of Taxable value of rent

Conclusion:

The employer here has provided John with the fringe benefit as the part of

employment. The employer will be liable for fringe benefit tax under “section 23 of the

Subjected to the “section 23, FBTAA 1986” the taxable value of the expense payment

fringe benefit is related to the year in which the school fees were paid by the John’s

employer. John’s employer would be liable for the chargeable value of the expense payment

fringe benefit made during the year of taxation.

In the second part of the case it is noticed that the John by his employer was provided

with the housing facilities in Sydney all through the FBT year. As the part of John’s

obligation he should pay $100 as a rent every week whereas the market value Sydney

housing was $800 every week. Conferring to the “section 25 of the FBTAA 1986”,

providing John with an accommodation gave rise to right of housing made during the year of

taxation. The employer under the “section 25, FBTAA 1986” will be liable for the housing

fringe benefit (Shields and North-Samardzic 2015). However, under the “sect 27 (1),

FBTAA 1986”, the taxable amount of the fringe benefit will be the market value of the

housing accommodation provided by the employer here to the recipient. The employer here

can reduce the taxable value of the fringe benefit by reducing any rental contributions made

by John all through the FBT year.

Particulars Amount ($)

Rent Per Week 800.00$

Annualized Market Value 41,600.00$

(800 x 52 weeks)

Less: Employee’s Contribution

(100 x 52 weeks) 5,200.00$

Taxable Value 36,400.00$

Computation of Taxable value of rent

Conclusion:

The employer here has provided John with the fringe benefit as the part of

employment. The employer will be liable for fringe benefit tax under “section 23 of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

FBTAA 1986” and “section 27 (1), FBTAA 1986” less the rental contributions made by

John during the FBT year.

FBTAA 1986” and “section 27 (1), FBTAA 1986” less the rental contributions made by

John during the FBT year.

11TAXATION LAW

References:

Braithwaite, V. and Reinhart, M., 2019. The Taxpayers' Charter: Does the Australian Tax

Office comply and who benefits?.

Chen, D., Qi, S. and Schlagenhauf, D., 2018. Corporate income tax, legal form of

organization, and employment. American Economic Journal: Macroeconomics, 10(4),

pp.270-304.

Easton, B., 2015. Distibution of pre-tax top personal incomes. Policy Quarterly, 11(1).

Fairfield, T. and Jorratt De Luis, M., 2016. Top Income Shares, Business Profits, and

Effective Tax Rates in Contemporary C hile. Review of Income and Wealth, 62, pp.S120-

S144.

Grace, K., 2018. The impact of personal income tax rates on the employment decisions of

small businesses. Journal of Entrepreneurship and Public Policy, 7(1), pp.74-104.

Henry, E., Plesko, G.A. and Utke, S., 2018. Tax Policy and Organizational Form: Assessing

the Effects of the Tax Cuts and Jobs Act.

Kess, S., Grimaldi, J.R. and Revels, J.A., 2017. Financial, Legal, and Tax Concerns about

Long-Term Care. The CPA Journal, 87(5), p.64.

Parker, H., 2018. Instead of the Dole: An enquiry into integration of the tax and benefit

systems. Routledge.

Shields, J. and North-Samardzic, A., 2015. 10 Employee benefits. Managing Employee

Performance and Reward: Concepts, Practices, Strategies, p.218.

References:

Braithwaite, V. and Reinhart, M., 2019. The Taxpayers' Charter: Does the Australian Tax

Office comply and who benefits?.

Chen, D., Qi, S. and Schlagenhauf, D., 2018. Corporate income tax, legal form of

organization, and employment. American Economic Journal: Macroeconomics, 10(4),

pp.270-304.

Easton, B., 2015. Distibution of pre-tax top personal incomes. Policy Quarterly, 11(1).

Fairfield, T. and Jorratt De Luis, M., 2016. Top Income Shares, Business Profits, and

Effective Tax Rates in Contemporary C hile. Review of Income and Wealth, 62, pp.S120-

S144.

Grace, K., 2018. The impact of personal income tax rates on the employment decisions of

small businesses. Journal of Entrepreneurship and Public Policy, 7(1), pp.74-104.

Henry, E., Plesko, G.A. and Utke, S., 2018. Tax Policy and Organizational Form: Assessing

the Effects of the Tax Cuts and Jobs Act.

Kess, S., Grimaldi, J.R. and Revels, J.A., 2017. Financial, Legal, and Tax Concerns about

Long-Term Care. The CPA Journal, 87(5), p.64.

Parker, H., 2018. Instead of the Dole: An enquiry into integration of the tax and benefit

systems. Routledge.

Shields, J. and North-Samardzic, A., 2015. 10 Employee benefits. Managing Employee

Performance and Reward: Concepts, Practices, Strategies, p.218.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.