HI6028 Taxation Law: Partnership Income and Employee Fringe Benefits

VerifiedAdded on 2023/04/21

|13

|2659

|360

Report

AI Summary

This assignment provides a detailed analysis of taxation law, focusing on partnership income and fringe benefits. It addresses the calculation of net partnership income, considering eligible deductions and ordinary income principles as per ITAA 1997. The report also examines an employer's liability under the Fringe Benefit Tax Assessment Act 1986 (FBTAA) for benefits provided to employees, including education fees and housing. It applies relevant sections of the FBTAA and case law to determine taxable values and potential deductions. The document concludes with calculations and explanations of tax liabilities for both the partnership and the employer, offering a comprehensive overview of these complex taxation issues. Desklib is a platform where you can find similar solved assignments and past papers.

Running head: TAXATION LAW

Taxation

Name of the Student

Name of the University

Authors Note

Course ID

Taxation

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer 1:...................................................................................................................................2

Answer 2:...................................................................................................................................7

References:...............................................................................................................................10

Table of Contents

Answer 1:...................................................................................................................................2

Answer 2:...................................................................................................................................7

References:...............................................................................................................................10

2TAXATION LAW

Answer 1:

Issues:

Considerable discussion in this section is all about the profit gained by the partnership

during the pertinent income year.

Rule:

Conferring to the “division 5 of ITAA 1936” partnership is defined as, the partners

are not liable for paying the taxes and also they are not considered as a single unit of

operation (Thuronyi 2014). “Section 91 of ITAA 1997” elaborates that an individual

taxpayer should always prepare their return files in order to highlight the amount of profit

distributed among the shareholders. Consequently “sec 92, ITA Act 1997” section highlights

that partners are liable for incurred loss as well as profits. “Section 995-1(1)” states

partnership is the meaning of continuing the same objective of earning profit throughout the

business. The profit obtained from the partnership is considered as wither ordinary or

statutory income.

Referring to “section 6-5(4)” and “section 6-10 (3), ITAA 1997” the taxpayer is

liable for taking the income and this should be according to the directions of the taxpayer

(Markle 2016). In reference with “sec 6-5, ITA Act 1997” ordinary income is considered

from the large part of the income of taxpayer. In “Scott v CT (1935)” the commissioner

stated there are different sort of principles those are used for understanding the gains from the

ordinary income. Any kind of business receipts that is made is taken into the account as

ordinary income based on “S-6-5, ITA Act 1997”.

Rendering to “Section 8-1 of ITA Act 1997” allows the taxpayer to avail the

deductions those are his personal outgoing expenses and also these expenses are generated

Answer 1:

Issues:

Considerable discussion in this section is all about the profit gained by the partnership

during the pertinent income year.

Rule:

Conferring to the “division 5 of ITAA 1936” partnership is defined as, the partners

are not liable for paying the taxes and also they are not considered as a single unit of

operation (Thuronyi 2014). “Section 91 of ITAA 1997” elaborates that an individual

taxpayer should always prepare their return files in order to highlight the amount of profit

distributed among the shareholders. Consequently “sec 92, ITA Act 1997” section highlights

that partners are liable for incurred loss as well as profits. “Section 995-1(1)” states

partnership is the meaning of continuing the same objective of earning profit throughout the

business. The profit obtained from the partnership is considered as wither ordinary or

statutory income.

Referring to “section 6-5(4)” and “section 6-10 (3), ITAA 1997” the taxpayer is

liable for taking the income and this should be according to the directions of the taxpayer

(Markle 2016). In reference with “sec 6-5, ITA Act 1997” ordinary income is considered

from the large part of the income of taxpayer. In “Scott v CT (1935)” the commissioner

stated there are different sort of principles those are used for understanding the gains from the

ordinary income. Any kind of business receipts that is made is taken into the account as

ordinary income based on “S-6-5, ITA Act 1997”.

Rendering to “Section 8-1 of ITA Act 1997” allows the taxpayer to avail the

deductions those are his personal outgoing expenses and also these expenses are generated

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

while maintaining the business objectives. Consequently, the negative aspect of the “Section

8-1 of ITA Act 1997” is, it doesn’t allow the taxpayer to maintain these deductions if he is

involving private, domestic or capital expenses (Hurst, Li and Pugsley 2014). Therefor if the

taxpayer is applying some sort of expenses those are falling under the capital, private or

domestic nature then he will be not be allowed the deductions.

According to ATO, the taxpayer is eligible in getting the deductions if their expenses

are below 20,000. Consequently, it makes the taxpayer eligible for obtaining the deductions

for repair of their assets (Nichols and Rothstein 2015). According to “Subsection 25-10 (1),

ITA Act 1997”, the taxpayer is permissible in getting the deductions for decorations,

deterioration and damages in any of their assets. In a similar manner “FC of T v Western

Suburbs Cinemas (1952)” states the taxpayer is not permissible in getting the deductions if

they are incurring capital expenses for repairs.

Application:

In accordance with the case discussed in this section Daniel and Olivia are keeping

the business objectives in order gain profit over their ordinary income and has been incurred

some receipts and outgoing expenditures. Sales and payments from the debtors are

considered as receipts. As per the “section 6-5, ITA Act 1997” the sales and payment

received from the debtors are the income gained from the business and this is according to the

concepts of ordinary income.

Two partners has drawn the amount of profit as follows $5600 AND $6000 from the

business. Along with these two amounts they have drawn $3200 amount for their private

purpose. According to “section 8-1 (2), ITA Act 1997”, as Daniel and Olivia has made these

outgoing expenses as private in nature so they are not allowed in getting the deductions under

the negative limbs (Fairfield and Jorratt De Luis 2016).

while maintaining the business objectives. Consequently, the negative aspect of the “Section

8-1 of ITA Act 1997” is, it doesn’t allow the taxpayer to maintain these deductions if he is

involving private, domestic or capital expenses (Hurst, Li and Pugsley 2014). Therefor if the

taxpayer is applying some sort of expenses those are falling under the capital, private or

domestic nature then he will be not be allowed the deductions.

According to ATO, the taxpayer is eligible in getting the deductions if their expenses

are below 20,000. Consequently, it makes the taxpayer eligible for obtaining the deductions

for repair of their assets (Nichols and Rothstein 2015). According to “Subsection 25-10 (1),

ITA Act 1997”, the taxpayer is permissible in getting the deductions for decorations,

deterioration and damages in any of their assets. In a similar manner “FC of T v Western

Suburbs Cinemas (1952)” states the taxpayer is not permissible in getting the deductions if

they are incurring capital expenses for repairs.

Application:

In accordance with the case discussed in this section Daniel and Olivia are keeping

the business objectives in order gain profit over their ordinary income and has been incurred

some receipts and outgoing expenditures. Sales and payments from the debtors are

considered as receipts. As per the “section 6-5, ITA Act 1997” the sales and payment

received from the debtors are the income gained from the business and this is according to the

concepts of ordinary income.

Two partners has drawn the amount of profit as follows $5600 AND $6000 from the

business. Along with these two amounts they have drawn $3200 amount for their private

purpose. According to “section 8-1 (2), ITA Act 1997”, as Daniel and Olivia has made these

outgoing expenses as private in nature so they are not allowed in getting the deductions under

the negative limbs (Fairfield and Jorratt De Luis 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

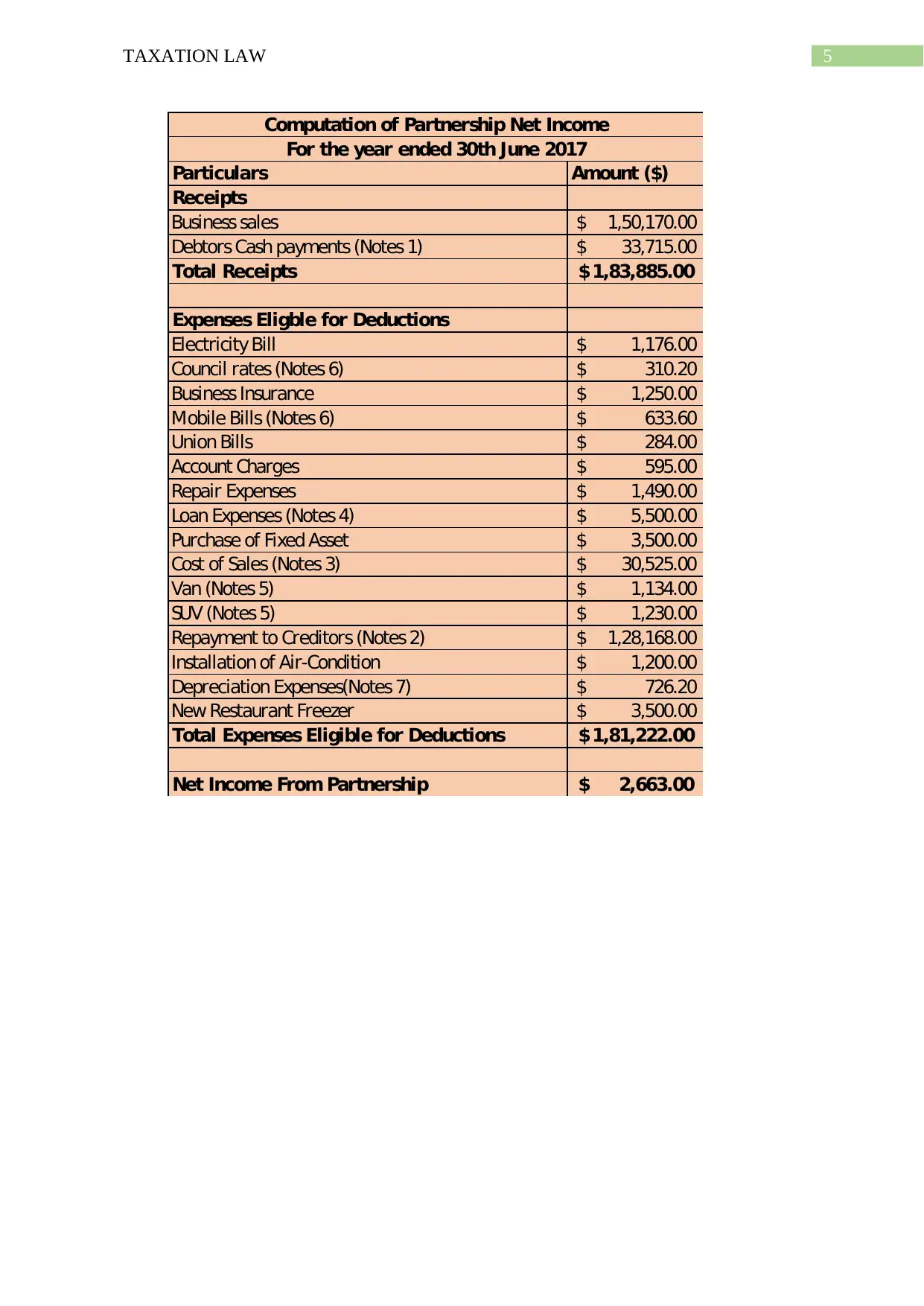

According to the ATO the taxpayers can claim for the money if the expenses for their

assets are below 20,000. In accordance with the case being discussed here, Daniel and Olivia

has spent $12, 00 for buying air conditioner. The actual value for the asset is less than 20,000

so the partnership is allowed to get the amount as deductions which will be considered as

their ordinary income.

The partnership also indulged the outgoing expense for painting a shop and repairing

the motor for refrigerator. According to the case of “FC of T v Western Suburbs Cinemas

(1952)” the expense mentioned above is considered as the capital outgoing expense (Tanzi

2014). Hence according to the ordinary income aspects this expense will be credited to the

partners as deductions as this is in capital in nature. Conferring to “sect 25-10, ITA Act

1997” this function can be stated. This calculation is stated in the bellow table with all the

important aspects-

According to the ATO the taxpayers can claim for the money if the expenses for their

assets are below 20,000. In accordance with the case being discussed here, Daniel and Olivia

has spent $12, 00 for buying air conditioner. The actual value for the asset is less than 20,000

so the partnership is allowed to get the amount as deductions which will be considered as

their ordinary income.

The partnership also indulged the outgoing expense for painting a shop and repairing

the motor for refrigerator. According to the case of “FC of T v Western Suburbs Cinemas

(1952)” the expense mentioned above is considered as the capital outgoing expense (Tanzi

2014). Hence according to the ordinary income aspects this expense will be credited to the

partners as deductions as this is in capital in nature. Conferring to “sect 25-10, ITA Act

1997” this function can be stated. This calculation is stated in the bellow table with all the

important aspects-

5TAXATION LAW

Particulars Amount ($)

Receipts

Business sales 1,50,170.00$

Debtors Cash payments (Notes 1) 33,715.00$

Total Receipts 1,83,885.00$

Expenses Eligble for Deductions

Electricity Bill 1,176.00$

Council rates (Notes 6) 310.20$

Business Insurance 1,250.00$

Mobile Bills (Notes 6) 633.60$

Union Bills 284.00$

Account Charges 595.00$

Repair Expenses 1,490.00$

Loan Expenses (Notes 4) 5,500.00$

Purchase of Fixed Asset 3,500.00$

Cost of Sales (Notes 3) 30,525.00$

Van (Notes 5) 1,134.00$

SUV (Notes 5) 1,230.00$

Repayment to Creditors (Notes 2) 1,28,168.00$

Installation of Air-Condition 1,200.00$

Depreciation Expenses(Notes 7) 726.20$

New Restaurant Freezer 3,500.00$

Total Expenses Eligible for Deductions 1,81,222.00$

Net Income From Partnership 2,663.00$

Computation of Partnership Net Income

For the year ended 30th June 2017

Particulars Amount ($)

Receipts

Business sales 1,50,170.00$

Debtors Cash payments (Notes 1) 33,715.00$

Total Receipts 1,83,885.00$

Expenses Eligble for Deductions

Electricity Bill 1,176.00$

Council rates (Notes 6) 310.20$

Business Insurance 1,250.00$

Mobile Bills (Notes 6) 633.60$

Union Bills 284.00$

Account Charges 595.00$

Repair Expenses 1,490.00$

Loan Expenses (Notes 4) 5,500.00$

Purchase of Fixed Asset 3,500.00$

Cost of Sales (Notes 3) 30,525.00$

Van (Notes 5) 1,134.00$

SUV (Notes 5) 1,230.00$

Repayment to Creditors (Notes 2) 1,28,168.00$

Installation of Air-Condition 1,200.00$

Depreciation Expenses(Notes 7) 726.20$

New Restaurant Freezer 3,500.00$

Total Expenses Eligible for Deductions 1,81,222.00$

Net Income From Partnership 2,663.00$

Computation of Partnership Net Income

For the year ended 30th June 2017

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

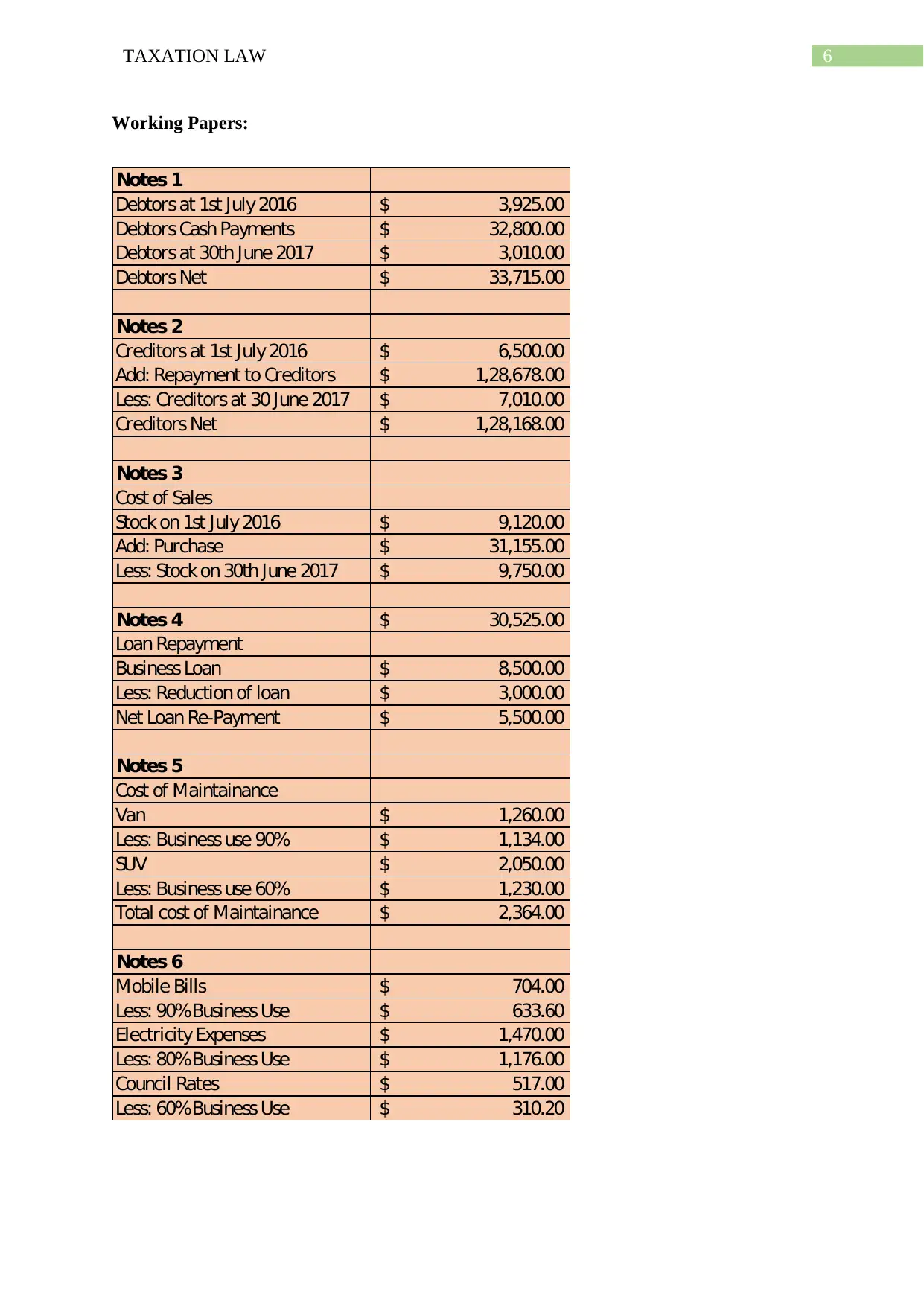

Working Papers:

Notes 1

Debtors at 1st July 2016 3,925.00$

Debtors Cash Payments 32,800.00$

Debtors at 30th June 2017 3,010.00$

Debtors Net 33,715.00$

Notes 2

Creditors at 1st July 2016 6,500.00$

Add: Repayment to Creditors 1,28,678.00$

Less: Creditors at 30 June 2017 7,010.00$

Creditors Net 1,28,168.00$

Notes 3

Cost of Sales

Stock on 1st July 2016 9,120.00$

Add: Purchase 31,155.00$

Less: Stock on 30th June 2017 9,750.00$

Notes 4 30,525.00$

Loan Repayment

Business Loan 8,500.00$

Less: Reduction of loan 3,000.00$

Net Loan Re-Payment 5,500.00$

Notes 5

Cost of Maintainance

Van 1,260.00$

Less: Business use 90% 1,134.00$

SUV 2,050.00$

Less: Business use 60% 1,230.00$

Total cost of Maintainance 2,364.00$

Notes 6

Mobile Bills 704.00$

Less: 90%Business Use 633.60$

Electricity Expenses 1,470.00$

Less: 80%Business Use 1,176.00$

Council Rates 517.00$

Less: 60%Business Use 310.20$

Working Papers:

Notes 1

Debtors at 1st July 2016 3,925.00$

Debtors Cash Payments 32,800.00$

Debtors at 30th June 2017 3,010.00$

Debtors Net 33,715.00$

Notes 2

Creditors at 1st July 2016 6,500.00$

Add: Repayment to Creditors 1,28,678.00$

Less: Creditors at 30 June 2017 7,010.00$

Creditors Net 1,28,168.00$

Notes 3

Cost of Sales

Stock on 1st July 2016 9,120.00$

Add: Purchase 31,155.00$

Less: Stock on 30th June 2017 9,750.00$

Notes 4 30,525.00$

Loan Repayment

Business Loan 8,500.00$

Less: Reduction of loan 3,000.00$

Net Loan Re-Payment 5,500.00$

Notes 5

Cost of Maintainance

Van 1,260.00$

Less: Business use 90% 1,134.00$

SUV 2,050.00$

Less: Business use 60% 1,230.00$

Total cost of Maintainance 2,364.00$

Notes 6

Mobile Bills 704.00$

Less: 90%Business Use 633.60$

Electricity Expenses 1,470.00$

Less: 80%Business Use 1,176.00$

Council Rates 517.00$

Less: 60%Business Use 310.20$

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

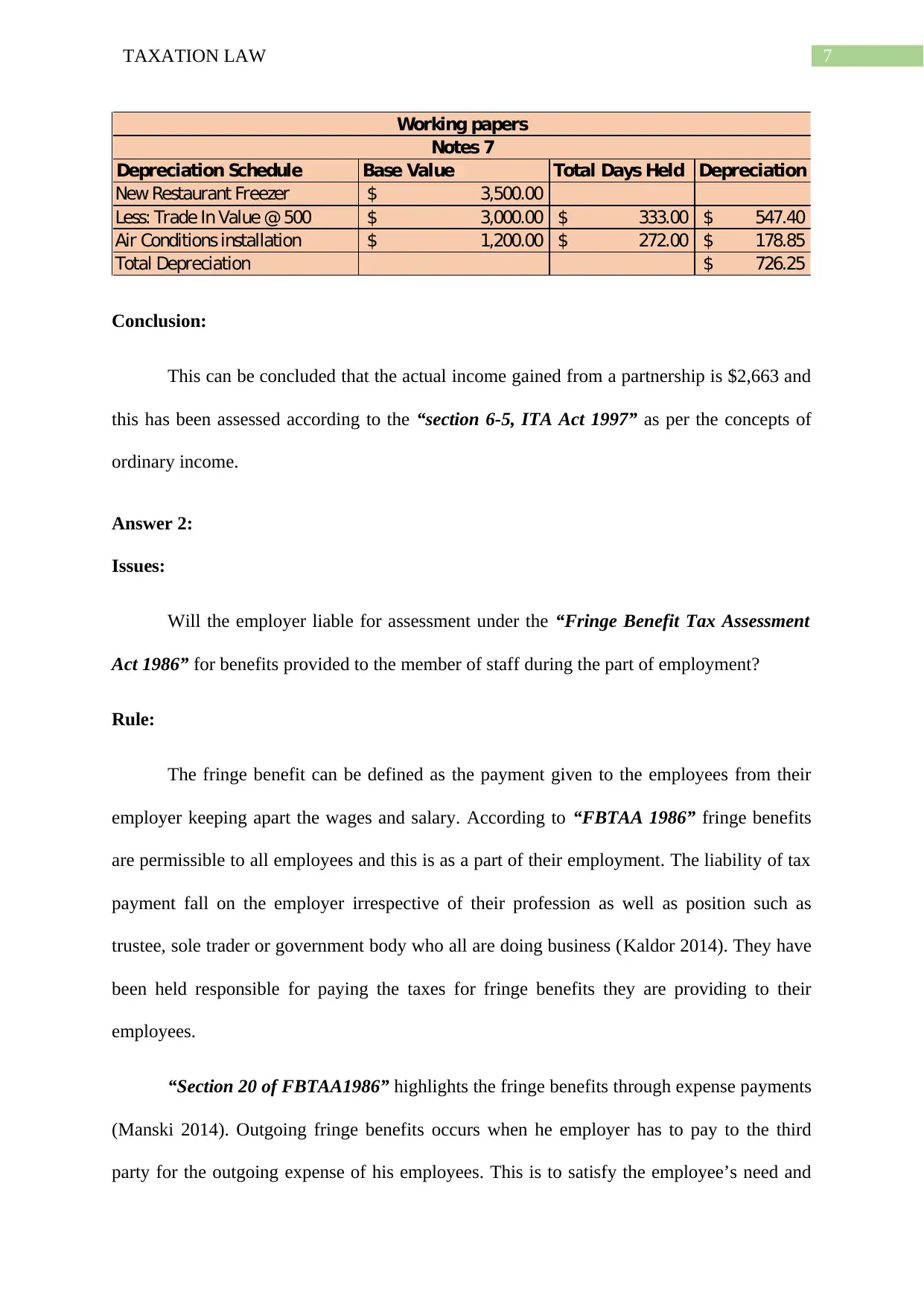

Depreciation Schedule Base Value Total Days Held Depreciation

New Restaurant Freezer 3,500.00$

Less: Trade In Value @ 500 3,000.00$ 333.00$ 547.40$

Air Conditions installation 1,200.00$ 272.00$ 178.85$

Total Depreciation 726.25$

Working papers

Notes 7

Conclusion:

This can be concluded that the actual income gained from a partnership is $2,663 and

this has been assessed according to the “section 6-5, ITA Act 1997” as per the concepts of

ordinary income.

Answer 2:

Issues:

Will the employer liable for assessment under the “Fringe Benefit Tax Assessment

Act 1986” for benefits provided to the member of staff during the part of employment?

Rule:

The fringe benefit can be defined as the payment given to the employees from their

employer keeping apart the wages and salary. According to “FBTAA 1986” fringe benefits

are permissible to all employees and this is as a part of their employment. The liability of tax

payment fall on the employer irrespective of their profession as well as position such as

trustee, sole trader or government body who all are doing business (Kaldor 2014). They have

been held responsible for paying the taxes for fringe benefits they are providing to their

employees.

“Section 20 of FBTAA1986” highlights the fringe benefits through expense payments

(Manski 2014). Outgoing fringe benefits occurs when he employer has to pay to the third

party for the outgoing expense of his employees. This is to satisfy the employee’s need and

Depreciation Schedule Base Value Total Days Held Depreciation

New Restaurant Freezer 3,500.00$

Less: Trade In Value @ 500 3,000.00$ 333.00$ 547.40$

Air Conditions installation 1,200.00$ 272.00$ 178.85$

Total Depreciation 726.25$

Working papers

Notes 7

Conclusion:

This can be concluded that the actual income gained from a partnership is $2,663 and

this has been assessed according to the “section 6-5, ITA Act 1997” as per the concepts of

ordinary income.

Answer 2:

Issues:

Will the employer liable for assessment under the “Fringe Benefit Tax Assessment

Act 1986” for benefits provided to the member of staff during the part of employment?

Rule:

The fringe benefit can be defined as the payment given to the employees from their

employer keeping apart the wages and salary. According to “FBTAA 1986” fringe benefits

are permissible to all employees and this is as a part of their employment. The liability of tax

payment fall on the employer irrespective of their profession as well as position such as

trustee, sole trader or government body who all are doing business (Kaldor 2014). They have

been held responsible for paying the taxes for fringe benefits they are providing to their

employees.

“Section 20 of FBTAA1986” highlights the fringe benefits through expense payments

(Manski 2014). Outgoing fringe benefits occurs when he employer has to pay to the third

party for the outgoing expense of his employees. This is to satisfy the employee’s need and

8TAXATION LAW

this is also falling under the fringe benefit that is being provided to the employees by the

employer. Outgoing fringe benefits mainly happens when the employer pays the amount as

reimbursement to the employee accordingly their usages. In contrary to these facts, tax

bearing amounts can be decreased if the employer provides a part of the fringe benefit costs.

Rendering to “subparagraph 65A (ii), FBTAA 1986” payment processed for the full

time education of the employee’s child is considered as the fringe benefit provided by the

employer as this is in relation with the occupation of the employee (Gaertner 2014). The

employer is liable to pay the tax for this kind of fringe benefit. As stated in “J & G Knowles

v FCT (2000)” the receiver of this fringe benefit should possess the relation between his

occupation and materialistic need for the benefit.

Mentioning the “section 25, FBTAA 1986” the housing fringe benefit is the rights to

use the house as general residence that has been provided by the employer to their employer

(Schizer 2014). This particular fringe benefit is also taxable and the value for this taxable is

determined through the market value of the unit of housing (Evers, Miller and Spengel 2015).

However, the value for housing is higher than what the employee has to pay to their employer

as a rental amount for that particular housing unit.

Applications:

John is getting the education fees for his child from his employer as the fringe benefit

as $15,000. According to the “sec 20, FBTAA 1986” this amount is paid by the employer of

John to him as this expense is being incurred as the third party payment for his child and also

this is in relation with his occupation with his employment (Alley et al. 2013). In reference to

“J & G Knowles v FCT (2000)” John holds a materialistic relation with the need for his

children, so according to the concepts of ordinary income and fringe benefits he is eligible for

getting the deductions in rental charges. Hence John will be responsible for FBT however; he

this is also falling under the fringe benefit that is being provided to the employees by the

employer. Outgoing fringe benefits mainly happens when the employer pays the amount as

reimbursement to the employee accordingly their usages. In contrary to these facts, tax

bearing amounts can be decreased if the employer provides a part of the fringe benefit costs.

Rendering to “subparagraph 65A (ii), FBTAA 1986” payment processed for the full

time education of the employee’s child is considered as the fringe benefit provided by the

employer as this is in relation with the occupation of the employee (Gaertner 2014). The

employer is liable to pay the tax for this kind of fringe benefit. As stated in “J & G Knowles

v FCT (2000)” the receiver of this fringe benefit should possess the relation between his

occupation and materialistic need for the benefit.

Mentioning the “section 25, FBTAA 1986” the housing fringe benefit is the rights to

use the house as general residence that has been provided by the employer to their employer

(Schizer 2014). This particular fringe benefit is also taxable and the value for this taxable is

determined through the market value of the unit of housing (Evers, Miller and Spengel 2015).

However, the value for housing is higher than what the employee has to pay to their employer

as a rental amount for that particular housing unit.

Applications:

John is getting the education fees for his child from his employer as the fringe benefit

as $15,000. According to the “sec 20, FBTAA 1986” this amount is paid by the employer of

John to him as this expense is being incurred as the third party payment for his child and also

this is in relation with his occupation with his employment (Alley et al. 2013). In reference to

“J & G Knowles v FCT (2000)” John holds a materialistic relation with the need for his

children, so according to the concepts of ordinary income and fringe benefits he is eligible for

getting the deductions in rental charges. Hence John will be responsible for FBT however; he

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

can decrease the liability for tax because his child is having the full time education which is

considered for being permissible in getting the deductions as fringe benefits.

John is also using the rented house that has been provided to him by his employer,

hence he is having the same right that his employer was pertaining to the property (Ambrus

and Kaufman 2014). Apart from this as John is the paying a part for the fringe benefit tax as

$100, whereas the market value of the property is $800, it is reducing the pressure on his

employer to pay the total amount of fringe benefit tax. The calculations is shown below-

Particulars Amount ($)

Rent Per Week 800

Annualized Market Value 41600

(800 x 52 weeks)

Less: Employee’s Contribution

(100 x 52 weeks) 5200

Taxable Value 36400

Computation of Taxable value of rent

Conclusion:

This can be concluded that the employer of John is easily lowering the amount of

fringe benefit tax as John is paying one part of it and that is known as the fringe benefit to

John as he is getting the house in a lowered rental amount.

can decrease the liability for tax because his child is having the full time education which is

considered for being permissible in getting the deductions as fringe benefits.

John is also using the rented house that has been provided to him by his employer,

hence he is having the same right that his employer was pertaining to the property (Ambrus

and Kaufman 2014). Apart from this as John is the paying a part for the fringe benefit tax as

$100, whereas the market value of the property is $800, it is reducing the pressure on his

employer to pay the total amount of fringe benefit tax. The calculations is shown below-

Particulars Amount ($)

Rent Per Week 800

Annualized Market Value 41600

(800 x 52 weeks)

Less: Employee’s Contribution

(100 x 52 weeks) 5200

Taxable Value 36400

Computation of Taxable value of rent

Conclusion:

This can be concluded that the employer of John is easily lowering the amount of

fringe benefit tax as John is paying one part of it and that is known as the fringe benefit to

John as he is getting the house in a lowered rental amount.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Alley, C., Coleman, J., Elliffe, C., Gousmett, M., Gupta, R., Hodson, A., Maples, A.,

Marriott, L., Marshall, T., Scrimgeour, F. and Tan, L.M., 2013. New Zealand taxation 2013:

Principles, cases and questions. Thomson Reuters.

(http://researcharchive.wintec.ac.nz/2613/)

Ambrus, R. and Kaufman, I., 2014. Tax-saving, innovative incentives for small and medium-

sized enterprises in Hungary. Journal of Economics and Business Research, 18(1), pp.33-42.

(https://www.ceeol.com/content-files/document-575753.pdf)

Evers, L., Miller, H. and Spengel, C., 2015. Intellectual property box regimes: effective tax

rates and tax policy considerations. International Tax and Public Finance, 22(3), pp.502-530.

(https://link.springer.com/article/10.1007/s10797-014-9328-x)

Fairfield, T. and Jorratt De Luis, M., 2016. Top Income Shares, Business Profits, and

Effective Tax Rates in Contemporary C hile. Review of Income and Wealth, 62, pp.S120-

S144.

(https://onlinelibrary.wiley.com/doi/abs/10.1111/roiw.12196)

Gaertner, F.B., 2014. CEO after‐tax compensation incentives and corporate tax

avoidance. Contemporary Accounting Research, 31(4), pp.1077-1102.

(https://onlinelibrary.wiley.com/doi/abs/10.1111/1911-3846.12058)

Hurst, E., Li, G. and Pugsley, B., 2014. Are household surveys like tax forms? Evidence from

income underreporting of the self-employed. Review of economics and statistics, 96(1),

pp.19-33. (https://www.mitpressjournals.org/doi/abs/10.1162/REST_a_00363)

Kaldor, N., 2014. Expenditure tax. Routledge.

References:

Alley, C., Coleman, J., Elliffe, C., Gousmett, M., Gupta, R., Hodson, A., Maples, A.,

Marriott, L., Marshall, T., Scrimgeour, F. and Tan, L.M., 2013. New Zealand taxation 2013:

Principles, cases and questions. Thomson Reuters.

(http://researcharchive.wintec.ac.nz/2613/)

Ambrus, R. and Kaufman, I., 2014. Tax-saving, innovative incentives for small and medium-

sized enterprises in Hungary. Journal of Economics and Business Research, 18(1), pp.33-42.

(https://www.ceeol.com/content-files/document-575753.pdf)

Evers, L., Miller, H. and Spengel, C., 2015. Intellectual property box regimes: effective tax

rates and tax policy considerations. International Tax and Public Finance, 22(3), pp.502-530.

(https://link.springer.com/article/10.1007/s10797-014-9328-x)

Fairfield, T. and Jorratt De Luis, M., 2016. Top Income Shares, Business Profits, and

Effective Tax Rates in Contemporary C hile. Review of Income and Wealth, 62, pp.S120-

S144.

(https://onlinelibrary.wiley.com/doi/abs/10.1111/roiw.12196)

Gaertner, F.B., 2014. CEO after‐tax compensation incentives and corporate tax

avoidance. Contemporary Accounting Research, 31(4), pp.1077-1102.

(https://onlinelibrary.wiley.com/doi/abs/10.1111/1911-3846.12058)

Hurst, E., Li, G. and Pugsley, B., 2014. Are household surveys like tax forms? Evidence from

income underreporting of the self-employed. Review of economics and statistics, 96(1),

pp.19-33. (https://www.mitpressjournals.org/doi/abs/10.1162/REST_a_00363)

Kaldor, N., 2014. Expenditure tax. Routledge.

11TAXATION LAW

(https://books.google.co.in/books?

hl=en&lr=&id=cR1IAwAAQBAJ&oi=fnd&pg=PP1&dq=Kaldor,+N.,

+2014.+Expenditure+tax.

+Routledge.&ots=Jb4IcymUcv&sig=rUlHprWQIrqcbcNgHKvO6df9UjQ#v=onepage&q=Ka

ldor%2C%20N.%2C%202014.%20Expenditure%20tax.%20Routledge.&f=false)

Manski, C.F., 2014. Identification of income–leisure preferences and evaluation of income

tax policy. Quantitative Economics, 5(1), pp.145-174.

(https://onlinelibrary.wiley.com/doi/abs/10.3982/QE262)

Markle, K., 2016. A comparison of the tax‐motivated income shifting of multinationals in

territorial and worldwide countries. Contemporary Accounting Research, 33(1), pp.7-43.

(https://onlinelibrary.wiley.com/doi/abs/10.1111/1911-3846.12148)

Nichols, A. and Rothstein, J., 2015. The earned income tax credit (eitc) (No. w21211).

National Bureau of Economic Research.

(https://www.nber.org/papers/w21211)

Schizer, D.M., 2014. Limiting Tax Expenditures. Tax L. Rev., 68, p.275.

(https://heinonline.org/HOL/LandingPage?handle=hein.journals/

taxlr68&div=11&id=&page=)

Tanzi, V., 2014. Inflation, indexation and interest income taxation. PSL Quarterly

Review, 29(116).

(https://ojs.uniroma1.it/index.php/PSLQuarterlyReview/article/view/11493)

Thuronyi, V., 2014. Comparative tax law.

(https://books.google.co.in/books?

hl=en&lr=&id=cR1IAwAAQBAJ&oi=fnd&pg=PP1&dq=Kaldor,+N.,

+2014.+Expenditure+tax.

+Routledge.&ots=Jb4IcymUcv&sig=rUlHprWQIrqcbcNgHKvO6df9UjQ#v=onepage&q=Ka

ldor%2C%20N.%2C%202014.%20Expenditure%20tax.%20Routledge.&f=false)

Manski, C.F., 2014. Identification of income–leisure preferences and evaluation of income

tax policy. Quantitative Economics, 5(1), pp.145-174.

(https://onlinelibrary.wiley.com/doi/abs/10.3982/QE262)

Markle, K., 2016. A comparison of the tax‐motivated income shifting of multinationals in

territorial and worldwide countries. Contemporary Accounting Research, 33(1), pp.7-43.

(https://onlinelibrary.wiley.com/doi/abs/10.1111/1911-3846.12148)

Nichols, A. and Rothstein, J., 2015. The earned income tax credit (eitc) (No. w21211).

National Bureau of Economic Research.

(https://www.nber.org/papers/w21211)

Schizer, D.M., 2014. Limiting Tax Expenditures. Tax L. Rev., 68, p.275.

(https://heinonline.org/HOL/LandingPage?handle=hein.journals/

taxlr68&div=11&id=&page=)

Tanzi, V., 2014. Inflation, indexation and interest income taxation. PSL Quarterly

Review, 29(116).

(https://ojs.uniroma1.it/index.php/PSLQuarterlyReview/article/view/11493)

Thuronyi, V., 2014. Comparative tax law.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.