Disallowable Expenses

VerifiedAdded on 2019/11/20

|14

|1880

|392

Report

AI Summary

The assignment content discusses various tax-related issues and cases in Australian taxation law. The main topics covered include the allowability of legal expenses incurred during the winding up of a business, the claimability of input tax credits for advertisement expenses, and the computation of taxable income from a partnership. The cases discussed are FC of T v Snowden and Wilson Pty Ltd (1958) and Ronpibon Tin NL v FC of T. The assignment also references various Australian taxation laws, including the ITAA 1997 and GST Act 1999, as well as several academic sources.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TAXATION LAW THEORY AND PRACTICE

Taxation Law, Theory and Practice

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law, Theory and Practice

Name of the Student

Name of the University

Authors Note

Course ID

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1TAXATION LAW THEORY AND PRACTICE

Table of Contents

Answer to question 1:.................................................................................................................3

Answer to Issue I:.......................................................................................................................3

Issue:..........................................................................................................................................3

Laws:..........................................................................................................................................3

Applications:..............................................................................................................................3

Conclusion:................................................................................................................................4

Answer to Issue II:.....................................................................................................................4

Issue:..........................................................................................................................................4

Laws:..........................................................................................................................................4

Applications:..............................................................................................................................4

Conclusion:................................................................................................................................5

Answer to Issue III:....................................................................................................................5

Issue:..........................................................................................................................................5

Laws:..........................................................................................................................................5

Applications:..............................................................................................................................5

Conclusion:................................................................................................................................6

Answer to Issue IV:....................................................................................................................6

Issue:..........................................................................................................................................6

Laws:..........................................................................................................................................6

Applications:..............................................................................................................................6

Table of Contents

Answer to question 1:.................................................................................................................3

Answer to Issue I:.......................................................................................................................3

Issue:..........................................................................................................................................3

Laws:..........................................................................................................................................3

Applications:..............................................................................................................................3

Conclusion:................................................................................................................................4

Answer to Issue II:.....................................................................................................................4

Issue:..........................................................................................................................................4

Laws:..........................................................................................................................................4

Applications:..............................................................................................................................4

Conclusion:................................................................................................................................5

Answer to Issue III:....................................................................................................................5

Issue:..........................................................................................................................................5

Laws:..........................................................................................................................................5

Applications:..............................................................................................................................5

Conclusion:................................................................................................................................6

Answer to Issue IV:....................................................................................................................6

Issue:..........................................................................................................................................6

Laws:..........................................................................................................................................6

Applications:..............................................................................................................................6

2TAXATION LAW THEORY AND PRACTICE

Conclusion:................................................................................................................................7

Answer to question 2:.................................................................................................................7

Issue:..........................................................................................................................................7

Laws:..........................................................................................................................................7

Application:................................................................................................................................7

Conclusion:................................................................................................................................8

Answer to question 3:.................................................................................................................8

Answer to question 4................................................................................................................10

Reference List:.........................................................................................................................12

Conclusion:................................................................................................................................7

Answer to question 2:.................................................................................................................7

Issue:..........................................................................................................................................7

Laws:..........................................................................................................................................7

Application:................................................................................................................................7

Conclusion:................................................................................................................................8

Answer to question 3:.................................................................................................................8

Answer to question 4................................................................................................................10

Reference List:.........................................................................................................................12

3TAXATION LAW THEORY AND PRACTICE

Answer to question 1:

Answer to Issue I:

Issue:

From the existing scenario of moving the machinery from one site to another site it

can be said that the cost that is incurred can be considered for non-allowable deductions with

reference to “Section 8-1 of the ITAA 1997”.

Laws:

i. “Section 8-1 of the ITAA 1997”

ii. “British Insulated & Helsby Cables”

Applications:

As it has been evident from the existing situation that moving of machinery to new

site involves cost and it can be said that no permissible subtractions or deductions will be

permitted under section “8-1 of the ITAA 1997”. For the purpose of depreciation, moving

the machine to the new site can be said that it involves cost that ultimate results in increase in

the cost of machine. As held in “British Insulated & Helsby Cables” any form of cost

incurred at the time of transportation symbolizes a recurring advantage for the business by

shifting the machinery to new site (Barkoczy, 2016). According to the “Taxation ruling TD

93/126” installing the machine and starting the business functions results in cost involved in

moving the machine to new site and simultaneously forms the part of revenue. It must be

noted that cost involved in moving the machine to new site cannot be accounted as allowable

deductions.

Answer to question 1:

Answer to Issue I:

Issue:

From the existing scenario of moving the machinery from one site to another site it

can be said that the cost that is incurred can be considered for non-allowable deductions with

reference to “Section 8-1 of the ITAA 1997”.

Laws:

i. “Section 8-1 of the ITAA 1997”

ii. “British Insulated & Helsby Cables”

Applications:

As it has been evident from the existing situation that moving of machinery to new

site involves cost and it can be said that no permissible subtractions or deductions will be

permitted under section “8-1 of the ITAA 1997”. For the purpose of depreciation, moving

the machine to the new site can be said that it involves cost that ultimate results in increase in

the cost of machine. As held in “British Insulated & Helsby Cables” any form of cost

incurred at the time of transportation symbolizes a recurring advantage for the business by

shifting the machinery to new site (Barkoczy, 2016). According to the “Taxation ruling TD

93/126” installing the machine and starting the business functions results in cost involved in

moving the machine to new site and simultaneously forms the part of revenue. It must be

noted that cost involved in moving the machine to new site cannot be accounted as allowable

deductions.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4TAXATION LAW THEORY AND PRACTICE

Conclusion:

With reference to “Section 8-1 of the ITAA 1997”, it can be concluded that cost of

moving the machine will not be allowed as deductions since it is a capital expenditure.

Answer to Issue II:

Issue:

The issue brings forward the question whether or not the revaluation of asset to effect

insurance cover would form the part of allowable deductions under “Section 8-1 of ITAA

1997”.

Laws:

i. “Section 8-1 of the ITAA 1997”

Applications:

It can be said that cost originating from revaluation of asset to effect insurance cover

can be treated as permissible subtraction under “Section 8-1 of the ITAA 1997”. This is

because the expense of insurance cover is recurring in nature and it is directly linked with the

fixed asset (Kenny, 2013). While assessing the deductable nature of the expense it is

obligatory to make sure that whether such incurrence of expense in revaluation of asset

results in the income producing capability or it is merely occurred to protect the asset. If it

provides a provisional advantage to business in nature or it is recurring in nature than that

will be considered as deductions that are permissible in “Section 8-1 of the ITAA 1997”.

Conclusion:

With reference to “Section 8-1 of the ITAA 1997”, it can be concluded that cost of

moving the machine will not be allowed as deductions since it is a capital expenditure.

Answer to Issue II:

Issue:

The issue brings forward the question whether or not the revaluation of asset to effect

insurance cover would form the part of allowable deductions under “Section 8-1 of ITAA

1997”.

Laws:

i. “Section 8-1 of the ITAA 1997”

Applications:

It can be said that cost originating from revaluation of asset to effect insurance cover

can be treated as permissible subtraction under “Section 8-1 of the ITAA 1997”. This is

because the expense of insurance cover is recurring in nature and it is directly linked with the

fixed asset (Kenny, 2013). While assessing the deductable nature of the expense it is

obligatory to make sure that whether such incurrence of expense in revaluation of asset

results in the income producing capability or it is merely occurred to protect the asset. If it

provides a provisional advantage to business in nature or it is recurring in nature than that

will be considered as deductions that are permissible in “Section 8-1 of the ITAA 1997”.

5TAXATION LAW THEORY AND PRACTICE

Conclusion:

It can be concluded that cost of insurance cover will be treated as deductions that is

permissible under “Section 8-1 of the ITAA 1997” because it possess a recurring character

of expense.

Answer to Issue III:

Issue:

This issue brings forward the subject that whether or not the cost of winding up

business will be considered as allowable under “Section 8-1 of the ITAA 1997”.

Laws:

i. “FC of T v Snowden and Wilson Pty Ltd (1958)”

ii. “Section 8-1 of the ITAA 1997”

Applications:

The issue brings forward matter that cost that is involved during the process of

winding up of business have took place in the business operations and will not be allowed as

deductions under “Section 8-1 of the ITAA 1997” (Krever, 2013). As defined in “Taxation

Ruling of ID 2004/367” legal cost incurred will be permitted as deductions that are

allowable. This is because the taxpayer occurred the expense at the time of carrying out the

business functions from which the taxpayer produces income. Citing the case of “FC of T v

Snowden and Wilson Pty Ltd (1958)” legal cost for opposing the winding up of petition

even though meeting the criteria of positive limbs will not be considered as deductions that

Conclusion:

It can be concluded that cost of insurance cover will be treated as deductions that is

permissible under “Section 8-1 of the ITAA 1997” because it possess a recurring character

of expense.

Answer to Issue III:

Issue:

This issue brings forward the subject that whether or not the cost of winding up

business will be considered as allowable under “Section 8-1 of the ITAA 1997”.

Laws:

i. “FC of T v Snowden and Wilson Pty Ltd (1958)”

ii. “Section 8-1 of the ITAA 1997”

Applications:

The issue brings forward matter that cost that is involved during the process of

winding up of business have took place in the business operations and will not be allowed as

deductions under “Section 8-1 of the ITAA 1997” (Krever, 2013). As defined in “Taxation

Ruling of ID 2004/367” legal cost incurred will be permitted as deductions that are

allowable. This is because the taxpayer occurred the expense at the time of carrying out the

business functions from which the taxpayer produces income. Citing the case of “FC of T v

Snowden and Wilson Pty Ltd (1958)” legal cost for opposing the winding up of petition

even though meeting the criteria of positive limbs will not be considered as deductions that

6TAXATION LAW THEORY AND PRACTICE

are allowed as they possess the feature of capital and goes right into the business structure

(Morgan et al., 2013).

Conclusion:

It can be concluded that cost that is incurred in opposing the petition of winding up

will not permitted as allowable business deductions under “Section 8-1 of the ITAA 1997”.

Answer to Issue IV:

Issue:

The issue introduces the matter of legal expense arising from the service of solicitor

for various business functions of the client can be claimed as allowable deduction under

“Section 8-1 of the ITAA 1997”.

Laws:

i. “Section 8-1 of the ITAA 1997”

Applications:

From the above discussed issue, the matter brings forward the question that whether

an individual taxpayer occurring a legal expenditure relating to business expense shall be

treated for deductions that are allowable defined under “Section 8-1 of the ITAA 1997”

(Cao et al., 2015). If a taxpayer incurred any legal outlay that is not related to business then it

will be considered as non-allowable deductions (Woellner, 2013). From the given context it

can be said that legal outlay incurred by the taxpayer would be allowed as permissible

deductions since they are part of the business and it is occurred in producing the assessable

income of the taxpayer.

are allowed as they possess the feature of capital and goes right into the business structure

(Morgan et al., 2013).

Conclusion:

It can be concluded that cost that is incurred in opposing the petition of winding up

will not permitted as allowable business deductions under “Section 8-1 of the ITAA 1997”.

Answer to Issue IV:

Issue:

The issue introduces the matter of legal expense arising from the service of solicitor

for various business functions of the client can be claimed as allowable deduction under

“Section 8-1 of the ITAA 1997”.

Laws:

i. “Section 8-1 of the ITAA 1997”

Applications:

From the above discussed issue, the matter brings forward the question that whether

an individual taxpayer occurring a legal expenditure relating to business expense shall be

treated for deductions that are allowable defined under “Section 8-1 of the ITAA 1997”

(Cao et al., 2015). If a taxpayer incurred any legal outlay that is not related to business then it

will be considered as non-allowable deductions (Woellner, 2013). From the given context it

can be said that legal outlay incurred by the taxpayer would be allowed as permissible

deductions since they are part of the business and it is occurred in producing the assessable

income of the taxpayer.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW THEORY AND PRACTICE

Conclusion:

It can be stated by concluding that legal expense derived from of the business

functions would be permitted in the form of deductions under “Section 8-1 of the ITAA

1997”.

Answer to question 2:

Issue:

The existing issue brings forward the subject concerning the ascertainment of the

input tax credit resulting out of the occurrence of advertisement expense under “GSTR Act

1999”.

Laws:

i. Goods and Service Taxation Ruling of GSTR 2006/3

ii. Ronpibon Tin NL v FC of T

iii. Subsection 15-25

Application:

A guiding principle has been provided under the “GST ruling of GSTR 2006/3”

which is implemented to arrive at the input tax credit (Braithwaite, 2017). It is noteworthy to

denote that the creditable purpose and the original application of the ruling is defined in

“division 11-15 and 129 of the Goods and Service Tax Act 1999”. The above stated GST

ruling is implemented on all the taxable units that have been registered or they are required to

obtain the registration in order to acquire the monetary supplies that have exceeded the

agreed extent of the monetary acquisition and are regarded for input tax credit or reduced

Conclusion:

It can be stated by concluding that legal expense derived from of the business

functions would be permitted in the form of deductions under “Section 8-1 of the ITAA

1997”.

Answer to question 2:

Issue:

The existing issue brings forward the subject concerning the ascertainment of the

input tax credit resulting out of the occurrence of advertisement expense under “GSTR Act

1999”.

Laws:

i. Goods and Service Taxation Ruling of GSTR 2006/3

ii. Ronpibon Tin NL v FC of T

iii. Subsection 15-25

Application:

A guiding principle has been provided under the “GST ruling of GSTR 2006/3”

which is implemented to arrive at the input tax credit (Braithwaite, 2017). It is noteworthy to

denote that the creditable purpose and the original application of the ruling is defined in

“division 11-15 and 129 of the Goods and Service Tax Act 1999”. The above stated GST

ruling is implemented on all the taxable units that have been registered or they are required to

obtain the registration in order to acquire the monetary supplies that have exceeded the

agreed extent of the monetary acquisition and are regarded for input tax credit or reduced

8TAXATION LAW THEORY AND PRACTICE

amount of input tax credit. As it has been understood from the current scenario of Big Bank

Ltd outlay of $1,650,000 includes the cost of GST for advertisement.

As evident from the existing circumstances of Big Bank ltd Goods and Service

“taxation ruling of GSTR 2006/3” is applicable because the unit qualifies for the eligibility

of the input tax credit (Robin, 2017). The “GST Act 1999” states that a taxable entity can

introduce the claim of input tax credit for the supplies that includes GST derived in the

process of import. Citing the reference of “Ronpibon Tin NL v FC of T” to make the

eligible acquisition under “para 11-5 and 15-5” it is necessary to obtain creditable either in

parts or completely (Tran-Nam & Walpole, 2016). As stated under the “Section 11-15 or 15-

10” of the “GST Act 1999” an acquisition will be eligible as creditable given that the taxable

units brings forward the claims of input tax credit for the monetary supplies they make. It

must be understood that the advertisement expense that is incurred by Big Bank Ltd was for

the purpose of creditable acquisition (James, 2016). As it has been found that Big Bank Ltd

has gone past the financial acquisition threshold limit and it qualifies for claiming input tax

credit for the GST supplies that is made during the business process.

Conclusion:

It can be concluded that Big Bank Ltd would be considered eligible for claiming input

tax credit as per the “GSTR 2006/13” for the amount that is occurred for the advertisement

outlay on creditable acquisition.

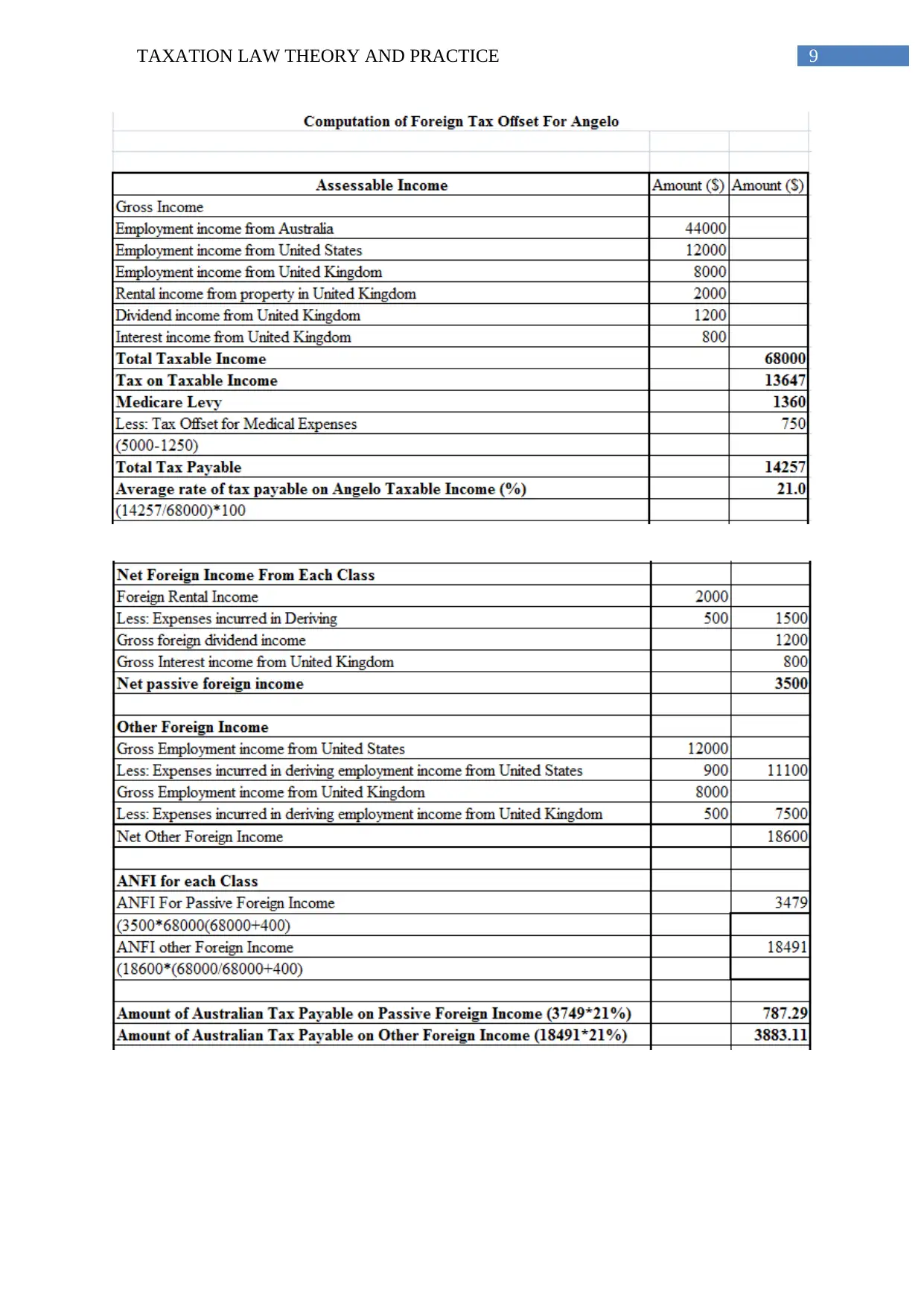

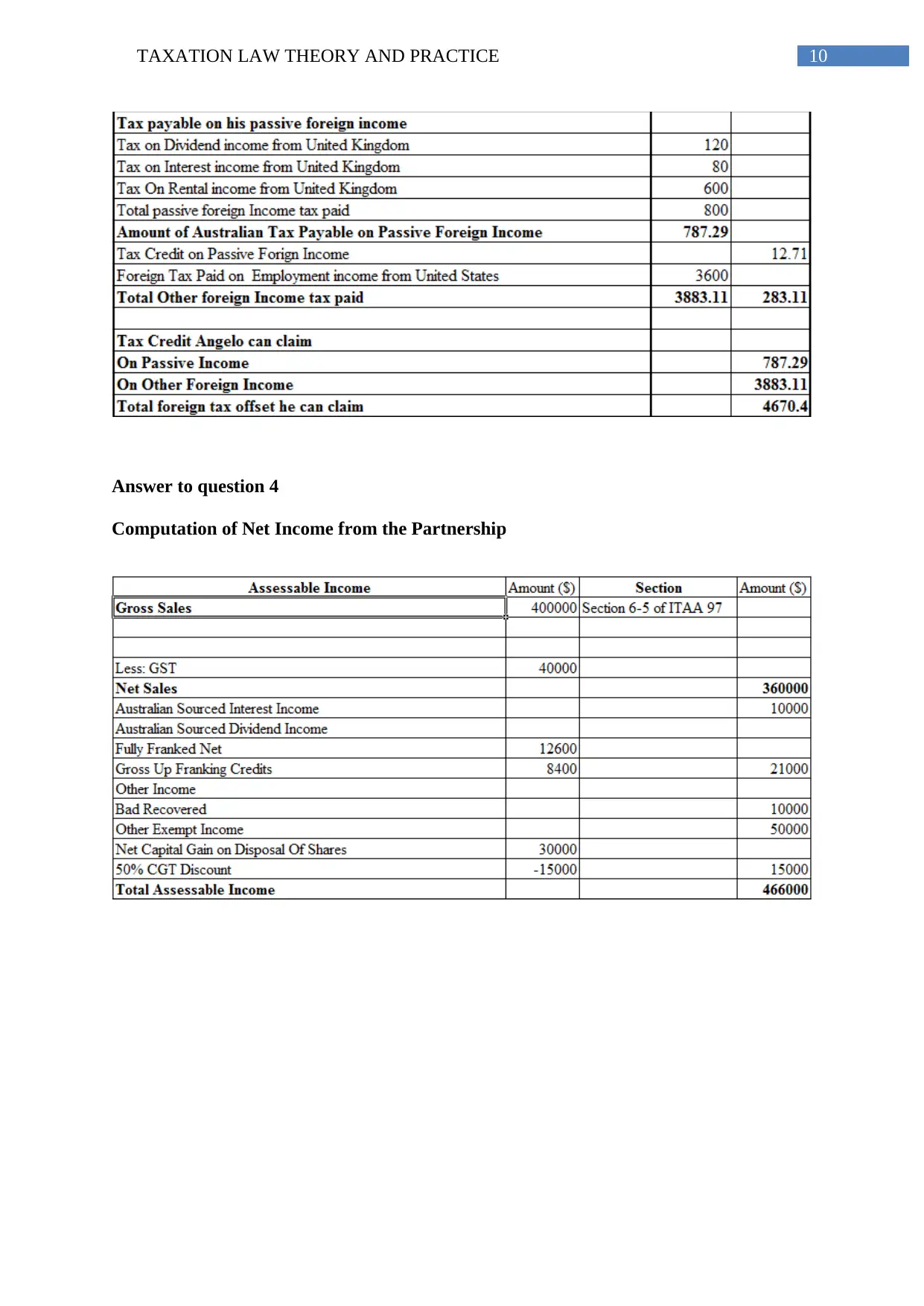

Answer to question 3:

Computation of Taxable Income of Angelo

amount of input tax credit. As it has been understood from the current scenario of Big Bank

Ltd outlay of $1,650,000 includes the cost of GST for advertisement.

As evident from the existing circumstances of Big Bank ltd Goods and Service

“taxation ruling of GSTR 2006/3” is applicable because the unit qualifies for the eligibility

of the input tax credit (Robin, 2017). The “GST Act 1999” states that a taxable entity can

introduce the claim of input tax credit for the supplies that includes GST derived in the

process of import. Citing the reference of “Ronpibon Tin NL v FC of T” to make the

eligible acquisition under “para 11-5 and 15-5” it is necessary to obtain creditable either in

parts or completely (Tran-Nam & Walpole, 2016). As stated under the “Section 11-15 or 15-

10” of the “GST Act 1999” an acquisition will be eligible as creditable given that the taxable

units brings forward the claims of input tax credit for the monetary supplies they make. It

must be understood that the advertisement expense that is incurred by Big Bank Ltd was for

the purpose of creditable acquisition (James, 2016). As it has been found that Big Bank Ltd

has gone past the financial acquisition threshold limit and it qualifies for claiming input tax

credit for the GST supplies that is made during the business process.

Conclusion:

It can be concluded that Big Bank Ltd would be considered eligible for claiming input

tax credit as per the “GSTR 2006/13” for the amount that is occurred for the advertisement

outlay on creditable acquisition.

Answer to question 3:

Computation of Taxable Income of Angelo

9TAXATION LAW THEORY AND PRACTICE

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10TAXATION LAW THEORY AND PRACTICE

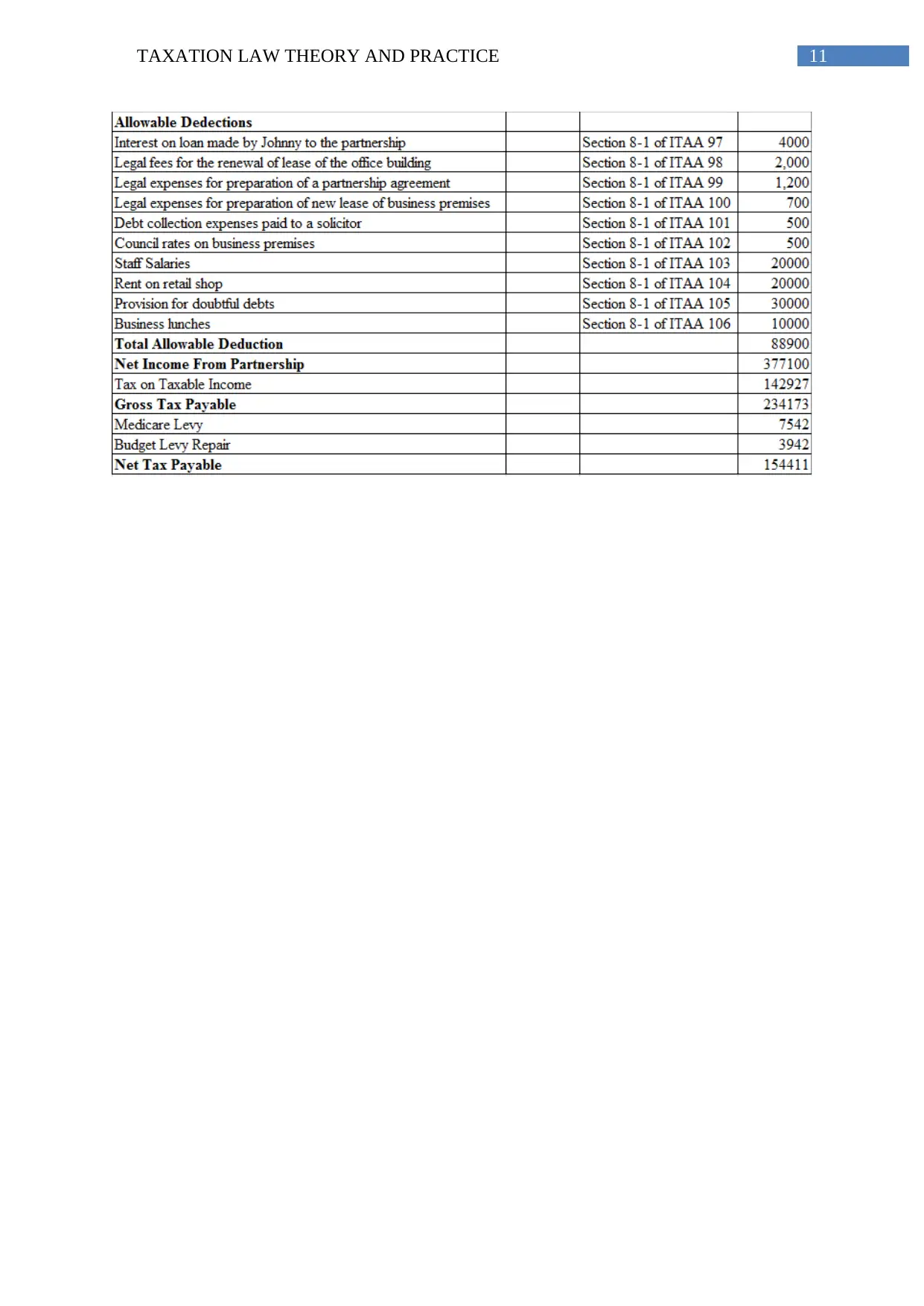

Answer to question 4

Computation of Net Income from the Partnership

Answer to question 4

Computation of Net Income from the Partnership

11TAXATION LAW THEORY AND PRACTICE

12TAXATION LAW THEORY AND PRACTICE

Reference List:

Barkoczy, S. (2016). Foundations of Taxation Law 2016. OUP Catalogue.

Braithwaite, V. (Ed.). (2017). Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., ... & Wende, S.

(2015). Understanding the economy-wide efficiency and incidence of major

Australian taxes. Treasury WP, 1.

James, K. (2016). The Australian Taxation Office perspective on work-related travel expense

deductions for academics. International Journal of Critical Accounting, 8(5-6), 345-

362.

Kenny, P. (2013). Australian tax 2013. Chatswood, N.S.W.: LexisNexis Butterworths.

Krever, R. (2013). Australian taxation law cases 2013. Pyrmont, N.S.W.: Thomson Reuters.

Morgan, A., Mortimer, C., & Pinto, D. (2013). A practical introduction to Australian taxation

law. North Ryde [N.S.W.]: CCH Australia.

ROBIN, H. (2017). AUSTRALIAN TAXATION LAW 2017. OXFORD University Press.

Tran-Nam, B., & Walpole, M. (2016). Tax disputes, litigation costs and access to tax

justice. eJournal of Tax Research, 14(2), 319.

Woellner, R. (2013). Australian taxation law select 2013. North Ryde, N.S.W.: CCH

Australia.

Reference List:

Barkoczy, S. (2016). Foundations of Taxation Law 2016. OUP Catalogue.

Braithwaite, V. (Ed.). (2017). Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., ... & Wende, S.

(2015). Understanding the economy-wide efficiency and incidence of major

Australian taxes. Treasury WP, 1.

James, K. (2016). The Australian Taxation Office perspective on work-related travel expense

deductions for academics. International Journal of Critical Accounting, 8(5-6), 345-

362.

Kenny, P. (2013). Australian tax 2013. Chatswood, N.S.W.: LexisNexis Butterworths.

Krever, R. (2013). Australian taxation law cases 2013. Pyrmont, N.S.W.: Thomson Reuters.

Morgan, A., Mortimer, C., & Pinto, D. (2013). A practical introduction to Australian taxation

law. North Ryde [N.S.W.]: CCH Australia.

ROBIN, H. (2017). AUSTRALIAN TAXATION LAW 2017. OXFORD University Press.

Tran-Nam, B., & Walpole, M. (2016). Tax disputes, litigation costs and access to tax

justice. eJournal of Tax Research, 14(2), 319.

Woellner, R. (2013). Australian taxation law select 2013. North Ryde, N.S.W.: CCH

Australia.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13TAXATION LAW THEORY AND PRACTICE

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.