Taxation Laws Assignment: Analyzing Tax Liabilities and Capital Gains

VerifiedAdded on 2022/12/28

|14

|3400

|63

Homework Assignment

AI Summary

This assignment solution addresses two key questions related to Australian taxation laws. Question 1 examines the tax implications for Our Earth Pty Ltd, focusing on whether compensatory damages for patent infringement, lost revenue, interest on damages, and reimbursement for legal expenses are considered assessable income. The analysis references relevant legislation, including the ITAA 1936 and ITAA 1997, and case law such as Californian Oil Products Ltd v Federal Commissioner of Taxation (1934) and FC of T v Spedley Securities Ltd (1988). The conclusion determines the tax treatment of each component. Question 2 explores capital gains tax (CGT) implications when a taxpayer sells subdivided land, considering whether it constitutes a simple realization of a capital asset or a profit-making undertaking, referencing Taxation Determination TD 97/3 and the case of Scottish Australian Mining Co Ltd v FC of T (1950). The solution differentiates between pre-CGT and post-CGT assets, and analyzes the tax treatment of land development. The assignment provides a comprehensive overview of the tax liabilities and capital gains for businesses, providing details of relevant case laws.

Running head: TAXATION LAWS

Taxation Laws

Name of the Student:

Name of the University:

Author’s Note

Taxation Laws

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

TAXATION LAWS

Table of Contents

Answer to Question 1......................................................................................................................2

Issues:..........................................................................................................................................2

Laws.............................................................................................................................................2

Application..................................................................................................................................4

Conclusion...................................................................................................................................6

Answer to Question 2......................................................................................................................7

Issues............................................................................................................................................7

Laws.............................................................................................................................................7

Application..................................................................................................................................9

Conclusion.....................................................................................................................................11

Reference.......................................................................................................................................12

TAXATION LAWS

Table of Contents

Answer to Question 1......................................................................................................................2

Issues:..........................................................................................................................................2

Laws.............................................................................................................................................2

Application..................................................................................................................................4

Conclusion...................................................................................................................................6

Answer to Question 2......................................................................................................................7

Issues............................................................................................................................................7

Laws.............................................................................................................................................7

Application..................................................................................................................................9

Conclusion.....................................................................................................................................11

Reference.......................................................................................................................................12

2

TAXATION LAWS

Answer to Question 1

Issues:

Will compensatory damages receipts be held liable for taxes under “Division 6” or

“subsection 25 (1), ITAA 1936”? Are the receipts of interest from damages pay out be included

in assessable income of Our Earth Pty Ltd? Will the reimbursement received by the taxpayer for

legal expenses undertaken be treated as assessable income?

Laws

A compensation receipt which is received by a business generally includes a right of

seeking compensation or for any action or proceedings introduced in the business or in relation

to an underlying asset of the business. These sort of compensation which is received by a

business are considered as compensatory receipts for the business. Compensation which is

received for any damages would be included in the assessable income with respect to ordinary

income under “Division 6 of the ITAA 1997” or the same can be included in statutory income.

As per the provisions which is stated under “section 25 (1), ITAA 1997” compensatory

payments would be considered taxable when the same is related to loss of revenue or profits

which relate to previous year. As per the case rulings of “Mc Laurin v FC of T (1961)” the

receipts of compensation would be considered taxable within the legislative rulings of

“subsection 25 (1), ITAA 1936”. The only consideration in this regard is that the payment

should be recognizable so that the same can be assessable for income (Bankman et al., 2018).

In order to ascertain whether the compensation for the losses would be treated as capital

receipts or ordinary income depends on nature of the payment. As per “section 6-5, of the ITAA

1997” the compensatory payments which is considered depends on the nature of income with

TAXATION LAWS

Answer to Question 1

Issues:

Will compensatory damages receipts be held liable for taxes under “Division 6” or

“subsection 25 (1), ITAA 1936”? Are the receipts of interest from damages pay out be included

in assessable income of Our Earth Pty Ltd? Will the reimbursement received by the taxpayer for

legal expenses undertaken be treated as assessable income?

Laws

A compensation receipt which is received by a business generally includes a right of

seeking compensation or for any action or proceedings introduced in the business or in relation

to an underlying asset of the business. These sort of compensation which is received by a

business are considered as compensatory receipts for the business. Compensation which is

received for any damages would be included in the assessable income with respect to ordinary

income under “Division 6 of the ITAA 1997” or the same can be included in statutory income.

As per the provisions which is stated under “section 25 (1), ITAA 1997” compensatory

payments would be considered taxable when the same is related to loss of revenue or profits

which relate to previous year. As per the case rulings of “Mc Laurin v FC of T (1961)” the

receipts of compensation would be considered taxable within the legislative rulings of

“subsection 25 (1), ITAA 1936”. The only consideration in this regard is that the payment

should be recognizable so that the same can be assessable for income (Bankman et al., 2018).

In order to ascertain whether the compensation for the losses would be treated as capital

receipts or ordinary income depends on nature of the payment. As per “section 6-5, of the ITAA

1997” the compensatory payments which is considered depends on the nature of income with

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

TAXATION LAWS

respect to ordinary concepts. As per the rulings which was held in “Californian Oil Products

Ltd v Federal Commissioner of Taxation (1934)” that any amount which is paid in ordinary

course of business for damages, losses of income would be considered under the purview of

taxation. The main reason due to which the verdict was provided as the profit was derived from

carrying out operations of the business even though the nature of the revenue is extraordinary in

nature.

The case of “CT (Vic) v Phillips (1936)” where a verdict was passed that if a taxpayer

receives compensation for loss of business revenue or commercial scheme and forms the

substances of business activity, then the amount which is received as compensation would be

considered as loss of capital assets. Therefore, if there is an absence of countervailing

examination than the receipts from the same would be treated as capital receipts. It was held in

the case rulings of “FC of T v Spedley Securities Ltd (1988)” that compensatory damages on

goodwill was considered as capital loss for the business. The compensation which was received

by the taxpayer was treated as an injury to the capital asset.

In the case where a taxpayer receives interest as compensation then the interest would be

treated as taxable amount for the taxpayer considering normal provisions. As per the opinion of

the federal court in the case “Whitaker v FCT (1998)” interest should be treated as income in

ordinary sense which is provided to the taxpayer as compensation for lost earnings.

The provisions of “section 8-1, ITAA 1997” states that the taxpayer would be eligible for

deductions for the legal expenses which is undertaken by the tax payer and then the payment or

the reward would also be included in the assessable income of the taxpayer in the form of

recovery under “subdivision 20-A”. The legal expenses which is awarded to the taxpayer is

TAXATION LAWS

respect to ordinary concepts. As per the rulings which was held in “Californian Oil Products

Ltd v Federal Commissioner of Taxation (1934)” that any amount which is paid in ordinary

course of business for damages, losses of income would be considered under the purview of

taxation. The main reason due to which the verdict was provided as the profit was derived from

carrying out operations of the business even though the nature of the revenue is extraordinary in

nature.

The case of “CT (Vic) v Phillips (1936)” where a verdict was passed that if a taxpayer

receives compensation for loss of business revenue or commercial scheme and forms the

substances of business activity, then the amount which is received as compensation would be

considered as loss of capital assets. Therefore, if there is an absence of countervailing

examination than the receipts from the same would be treated as capital receipts. It was held in

the case rulings of “FC of T v Spedley Securities Ltd (1988)” that compensatory damages on

goodwill was considered as capital loss for the business. The compensation which was received

by the taxpayer was treated as an injury to the capital asset.

In the case where a taxpayer receives interest as compensation then the interest would be

treated as taxable amount for the taxpayer considering normal provisions. As per the opinion of

the federal court in the case “Whitaker v FCT (1998)” interest should be treated as income in

ordinary sense which is provided to the taxpayer as compensation for lost earnings.

The provisions of “section 8-1, ITAA 1997” states that the taxpayer would be eligible for

deductions for the legal expenses which is undertaken by the tax payer and then the payment or

the reward would also be included in the assessable income of the taxpayer in the form of

recovery under “subdivision 20-A”. The legal expenses which is awarded to the taxpayer is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

TAXATION LAWS

usually paid to the for indemnifying them or recipient is the successful party for the cost of

lawsuit. It is therefore for these reasons that legal expenses are not included in income for

ordinary course of business. The legal expenses which is incurred under “subsection 20-20 (2)”,

is treated as taxable recoupment (Delany, 2013). This means that the amount which is received is

regarded as recoupment of loss or expenditure which is taxable if the taxpayer has received the

amount as indemnity and this sum is also deductible under the legislations of “ITAA 1936 or

ITAA 1997”.

Application

As per the case study which is provided relates to a business which is engaged in

developing special designed coffee cups. The name of the company is Our Earth Pty Ltd and the

company is known for its sustainable practices in developing the products. It was noticed by the

management of the company that a company name Coffee Beans Pty Ltd had stolen the design of

the coffee cups and sold the products in overseas market (Martin, 2019). The product was

offered in the overseas market at a lower price as well with an intention to increase the sales of

the business. Therefore, the management of Our Earth Pty Ltd filed a legal suit which was won

and received an amount of $ 300,000 as compensation for the damage which was caused to the

patent rights of Our Earth Pty Ltd.

In order to ascertain whether the compensatory damages which is received by Our Earth

Pty Ltd is of capital nature or is ordinary income. The decision regarding the nature of payment

can be judged by applying the case laws of “CT (Vic) v Phillips (1936)” which shows that

amount $ 300,000 is associated with a core business function and is a business loss. The loss is

done to a capital asset and therefore the same would be treated as receipt of capital nature

(Gunnoe, 2014). In addition to this, there is an absence of countervailing examination so the

TAXATION LAWS

usually paid to the for indemnifying them or recipient is the successful party for the cost of

lawsuit. It is therefore for these reasons that legal expenses are not included in income for

ordinary course of business. The legal expenses which is incurred under “subsection 20-20 (2)”,

is treated as taxable recoupment (Delany, 2013). This means that the amount which is received is

regarded as recoupment of loss or expenditure which is taxable if the taxpayer has received the

amount as indemnity and this sum is also deductible under the legislations of “ITAA 1936 or

ITAA 1997”.

Application

As per the case study which is provided relates to a business which is engaged in

developing special designed coffee cups. The name of the company is Our Earth Pty Ltd and the

company is known for its sustainable practices in developing the products. It was noticed by the

management of the company that a company name Coffee Beans Pty Ltd had stolen the design of

the coffee cups and sold the products in overseas market (Martin, 2019). The product was

offered in the overseas market at a lower price as well with an intention to increase the sales of

the business. Therefore, the management of Our Earth Pty Ltd filed a legal suit which was won

and received an amount of $ 300,000 as compensation for the damage which was caused to the

patent rights of Our Earth Pty Ltd.

In order to ascertain whether the compensatory damages which is received by Our Earth

Pty Ltd is of capital nature or is ordinary income. The decision regarding the nature of payment

can be judged by applying the case laws of “CT (Vic) v Phillips (1936)” which shows that

amount $ 300,000 is associated with a core business function and is a business loss. The loss is

done to a capital asset and therefore the same would be treated as receipt of capital nature

(Gunnoe, 2014). In addition to this, there is an absence of countervailing examination so the

5

TAXATION LAWS

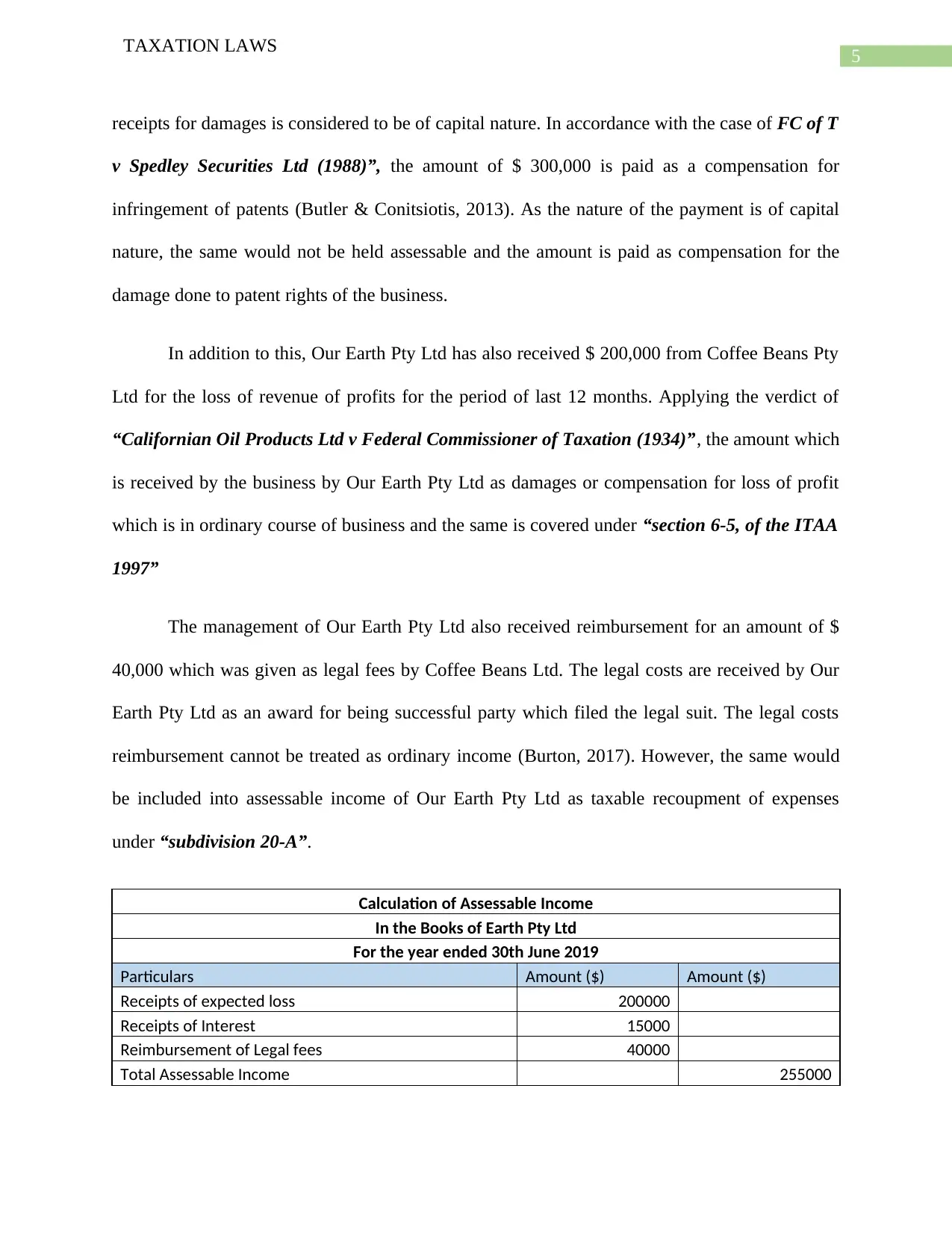

receipts for damages is considered to be of capital nature. In accordance with the case of FC of T

v Spedley Securities Ltd (1988)”, the amount of $ 300,000 is paid as a compensation for

infringement of patents (Butler & Conitsiotis, 2013). As the nature of the payment is of capital

nature, the same would not be held assessable and the amount is paid as compensation for the

damage done to patent rights of the business.

In addition to this, Our Earth Pty Ltd has also received $ 200,000 from Coffee Beans Pty

Ltd for the loss of revenue of profits for the period of last 12 months. Applying the verdict of

“Californian Oil Products Ltd v Federal Commissioner of Taxation (1934)”, the amount which

is received by the business by Our Earth Pty Ltd as damages or compensation for loss of profit

which is in ordinary course of business and the same is covered under “section 6-5, of the ITAA

1997”

The management of Our Earth Pty Ltd also received reimbursement for an amount of $

40,000 which was given as legal fees by Coffee Beans Ltd. The legal costs are received by Our

Earth Pty Ltd as an award for being successful party which filed the legal suit. The legal costs

reimbursement cannot be treated as ordinary income (Burton, 2017). However, the same would

be included into assessable income of Our Earth Pty Ltd as taxable recoupment of expenses

under “subdivision 20-A”.

Calculation of Assessable Income

In the Books of Earth Pty Ltd

For the year ended 30th June 2019

Particulars Amount ($) Amount ($)

Receipts of expected loss 200000

Receipts of Interest 15000

Reimbursement of Legal fees 40000

Total Assessable Income 255000

TAXATION LAWS

receipts for damages is considered to be of capital nature. In accordance with the case of FC of T

v Spedley Securities Ltd (1988)”, the amount of $ 300,000 is paid as a compensation for

infringement of patents (Butler & Conitsiotis, 2013). As the nature of the payment is of capital

nature, the same would not be held assessable and the amount is paid as compensation for the

damage done to patent rights of the business.

In addition to this, Our Earth Pty Ltd has also received $ 200,000 from Coffee Beans Pty

Ltd for the loss of revenue of profits for the period of last 12 months. Applying the verdict of

“Californian Oil Products Ltd v Federal Commissioner of Taxation (1934)”, the amount which

is received by the business by Our Earth Pty Ltd as damages or compensation for loss of profit

which is in ordinary course of business and the same is covered under “section 6-5, of the ITAA

1997”

The management of Our Earth Pty Ltd also received reimbursement for an amount of $

40,000 which was given as legal fees by Coffee Beans Ltd. The legal costs are received by Our

Earth Pty Ltd as an award for being successful party which filed the legal suit. The legal costs

reimbursement cannot be treated as ordinary income (Burton, 2017). However, the same would

be included into assessable income of Our Earth Pty Ltd as taxable recoupment of expenses

under “subdivision 20-A”.

Calculation of Assessable Income

In the Books of Earth Pty Ltd

For the year ended 30th June 2019

Particulars Amount ($) Amount ($)

Receipts of expected loss 200000

Receipts of Interest 15000

Reimbursement of Legal fees 40000

Total Assessable Income 255000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

TAXATION LAWS

Conclusion

The above discussion effectively shows that the compensatory damages which is received

by Our Earth Pty Ltd for damages of $ 300,000 which is for infringement of patents. The amount

of $ 300,000 would be treated as capital receipts. In addition to this, the amount of $ 200,000

which is received by Our Earth Pty Ltd is for loss of profits and the same would be treated as

ordinary income and would also be assessable for taxes. The sum of $200,000 will be treated as

income under the ordinary concepts of “section 6-5, ITAA 1997”. The legal charges which is

received by Our Earth Pty Ltd will be included for assessment of taxation under “subdivision

20-A”.

TAXATION LAWS

Conclusion

The above discussion effectively shows that the compensatory damages which is received

by Our Earth Pty Ltd for damages of $ 300,000 which is for infringement of patents. The amount

of $ 300,000 would be treated as capital receipts. In addition to this, the amount of $ 200,000

which is received by Our Earth Pty Ltd is for loss of profits and the same would be treated as

ordinary income and would also be assessable for taxes. The sum of $200,000 will be treated as

income under the ordinary concepts of “section 6-5, ITAA 1997”. The legal charges which is

received by Our Earth Pty Ltd will be included for assessment of taxation under “subdivision

20-A”.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

TAXATION LAWS

Answer to Question 2

Issues

Will the taxpayer be held liable for capital gain taxes when the taxpayer is selling off sub-

divided land under “section 25 (1)” or “section 26 (a)” or the taxpayer has simply realised the

capital asset?

Laws

Capital gains taxes are only applicable on sales of assets which have been purchased on

or after 20th September 1985. Any asset which is purchased before 20th September 1985 would be

treated as Pre-CGT asset and assets which are purchased after 20th September 1985 are

considered to be Post CGT asset. Capital gains is applicable where an amount is realised from

sale of a capital asset or from another specified event. The first step is to decide whether the

transaction or event forms a Subject of CGT and whether the event is ever taken out. As per

general rules, Capital gain taxes are applied prospectively and therefore it is only applicable if an

asset is disposed after 20th September 1985. A capital gain also arises when certain event takes

place under section 104-10, ITAA 1997” to the CGT asset when the taxpayer sells the asset. A

CGT asset is regarded as an asset which includes any type of property, legal or equitable right

which is not considered as a property.

There are several events which can be considered in relation to sub-division of land

which are kept for long time. These lands were basically used for agriculture purposes but have

been sold for residential development. In such a situation, the development of property on land

can be considered to make significant profits. In such cases three alternatives are established as

to how the profits are to be treated:

TAXATION LAWS

Answer to Question 2

Issues

Will the taxpayer be held liable for capital gain taxes when the taxpayer is selling off sub-

divided land under “section 25 (1)” or “section 26 (a)” or the taxpayer has simply realised the

capital asset?

Laws

Capital gains taxes are only applicable on sales of assets which have been purchased on

or after 20th September 1985. Any asset which is purchased before 20th September 1985 would be

treated as Pre-CGT asset and assets which are purchased after 20th September 1985 are

considered to be Post CGT asset. Capital gains is applicable where an amount is realised from

sale of a capital asset or from another specified event. The first step is to decide whether the

transaction or event forms a Subject of CGT and whether the event is ever taken out. As per

general rules, Capital gain taxes are applied prospectively and therefore it is only applicable if an

asset is disposed after 20th September 1985. A capital gain also arises when certain event takes

place under section 104-10, ITAA 1997” to the CGT asset when the taxpayer sells the asset. A

CGT asset is regarded as an asset which includes any type of property, legal or equitable right

which is not considered as a property.

There are several events which can be considered in relation to sub-division of land

which are kept for long time. These lands were basically used for agriculture purposes but have

been sold for residential development. In such a situation, the development of property on land

can be considered to make significant profits. In such cases three alternatives are established as

to how the profits are to be treated:

8

TAXATION LAWS

The subdivision and selling of land may be regarded as simple realisation of the capital

asset of the business.

The degree of land development would be such that it constitutes carrying the business

developments,

The activity of land development may go beyond simple realisation of land but not be

associated with performance of the business (Fullerton, 2017). In such a case, such

activities would be considered as profit deriving arrangements.

As per “Taxation Determination TD 97/3” simple sub-division of land cannot be treated as

sale of land within the meaning of “section 104-10, ITAA 1997”. The rulings specifies that the

proceeds which are derived from sale of land would be regarded as income which would be

assessable under “subsection 25 (1), ITAA 1936”.

The profits which is generated by performing a profit deriving scheme in relation to the

property which is purchased prior to introduction of CGT or Pre-CGT asset which is mainly

considered under assessable income as per the legislation of section 15-15, ITAA 1997”. The

improvements which are made on the land would also be considered for CGT provisions

(Schmalbeck, Zelenak & Lawsky, 2015). Any capital improvements which is made to the capital

asset after the purchase date would be added to the cost of the capital asset.

As per the case of “Scottish Australian Mining Co Ltd v FC of T (1950)” the federal court

passed its verdict that a significant profit was derived by the taxpayer from the sale of plot of

lands. The income which was generated by the taxpayer was held liable for taxes. As per the

commissioner of taxation, the profits which was generated by the taxpayer would either be

considered taxable under the “section 25 (1), ITAA 1936” as gains for development of land or

TAXATION LAWS

The subdivision and selling of land may be regarded as simple realisation of the capital

asset of the business.

The degree of land development would be such that it constitutes carrying the business

developments,

The activity of land development may go beyond simple realisation of land but not be

associated with performance of the business (Fullerton, 2017). In such a case, such

activities would be considered as profit deriving arrangements.

As per “Taxation Determination TD 97/3” simple sub-division of land cannot be treated as

sale of land within the meaning of “section 104-10, ITAA 1997”. The rulings specifies that the

proceeds which are derived from sale of land would be regarded as income which would be

assessable under “subsection 25 (1), ITAA 1936”.

The profits which is generated by performing a profit deriving scheme in relation to the

property which is purchased prior to introduction of CGT or Pre-CGT asset which is mainly

considered under assessable income as per the legislation of section 15-15, ITAA 1997”. The

improvements which are made on the land would also be considered for CGT provisions

(Schmalbeck, Zelenak & Lawsky, 2015). Any capital improvements which is made to the capital

asset after the purchase date would be added to the cost of the capital asset.

As per the case of “Scottish Australian Mining Co Ltd v FC of T (1950)” the federal court

passed its verdict that a significant profit was derived by the taxpayer from the sale of plot of

lands. The income which was generated by the taxpayer was held liable for taxes. As per the

commissioner of taxation, the profits which was generated by the taxpayer would either be

considered taxable under the “section 25 (1), ITAA 1936” as gains for development of land or

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

TAXATION LAWS

considered under the provisions of “section 26 (a)” as the profits that are made from the revenue

generating undertaking.

Therefore, the law makes it clear that acquisition of land and sale of the same would lead to

generation of revenue which would definitely treated as assessable income which would be in

ordinary course of business. The ultimate purpose of the taxpayer was to generate profits from

the disposal of land.

Application

The case study which is shown relates to the situation where Sam purchases 80 acres of

land at first and then 20 acres of land. The purpose if 20 acres of land was to expand the

agricultural operations. But after a certain time period, Sam lost his interest in agriculture and

decided to move to residential property development by selling off his lands. Sam got advice that

he should dispose off his lands by sub-dividing them so that more profits can be generated by

him.

The first step is to determine whether capital gains actually arises by considering the date

of purchase of lands plots (Posner, 2014). As per information Sam purchased first 80 acres of

land in 1984 and therefore the same is to be treated as pre-CGT asset (Enever, Isaac & Daley,

2014). It is also to be noted that no CGT would be applicable on the sale of 80 acres of land as

any gains would be exempted from the point of view of tax.

On the other hand, Sam purchased 20 acres of land in February 1985. The land should be

treated as the post-CGT asset because it is bought after the introduction of capital gains scheme

(Huizinga, Voget & Wagner, 2018). The process of Sub-division started in 2017 and the land

TAXATION LAWS

considered under the provisions of “section 26 (a)” as the profits that are made from the revenue

generating undertaking.

Therefore, the law makes it clear that acquisition of land and sale of the same would lead to

generation of revenue which would definitely treated as assessable income which would be in

ordinary course of business. The ultimate purpose of the taxpayer was to generate profits from

the disposal of land.

Application

The case study which is shown relates to the situation where Sam purchases 80 acres of

land at first and then 20 acres of land. The purpose if 20 acres of land was to expand the

agricultural operations. But after a certain time period, Sam lost his interest in agriculture and

decided to move to residential property development by selling off his lands. Sam got advice that

he should dispose off his lands by sub-dividing them so that more profits can be generated by

him.

The first step is to determine whether capital gains actually arises by considering the date

of purchase of lands plots (Posner, 2014). As per information Sam purchased first 80 acres of

land in 1984 and therefore the same is to be treated as pre-CGT asset (Enever, Isaac & Daley,

2014). It is also to be noted that no CGT would be applicable on the sale of 80 acres of land as

any gains would be exempted from the point of view of tax.

On the other hand, Sam purchased 20 acres of land in February 1985. The land should be

treated as the post-CGT asset because it is bought after the introduction of capital gains scheme

(Huizinga, Voget & Wagner, 2018). The process of Sub-division started in 2017 and the land

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

TAXATION LAWS

was disposed off in April 2018. Therefore, the revenue which is generated from sale of 20 acres

of land would be subjected to CGT.

In the case of Sam, the land development project would be generating significant amount

of revenue. By considering the provisions of Taxation Determination TD 97/3” the income

which is generated from the sale of plot of land would be considered as taxable under the

“subsection 25 (1), ITAA 1936”. The land which was sold was not actually purchased for

making profits by resale or for purpose of development (Zucman, 2015). The intention of making

profits developed at a later stage.

Referring to the case of Scottish Australian Mining Co Ltd v FC of T (1950)” Sam

makes considerable profits from sale of subdivided plots of land. Therefore, the profits which is

generated by Sam would be considered for Capital Gain Taxes under the provisions of “section

25 (1), ITAA 1936” in the form of gains made from carrying the business of land development or

within the legislative provision of “section 26 (a)” as the profits that are made from the revenue

generating undertaking.

The legal expenses which is undertaken by Sam and amount which is paid to property

agent would be deducted from the value of land which is considered for the purpose of taxes.

The gains which is generated from sale of land would be included in assessing the taxable

income of the taxpayer.

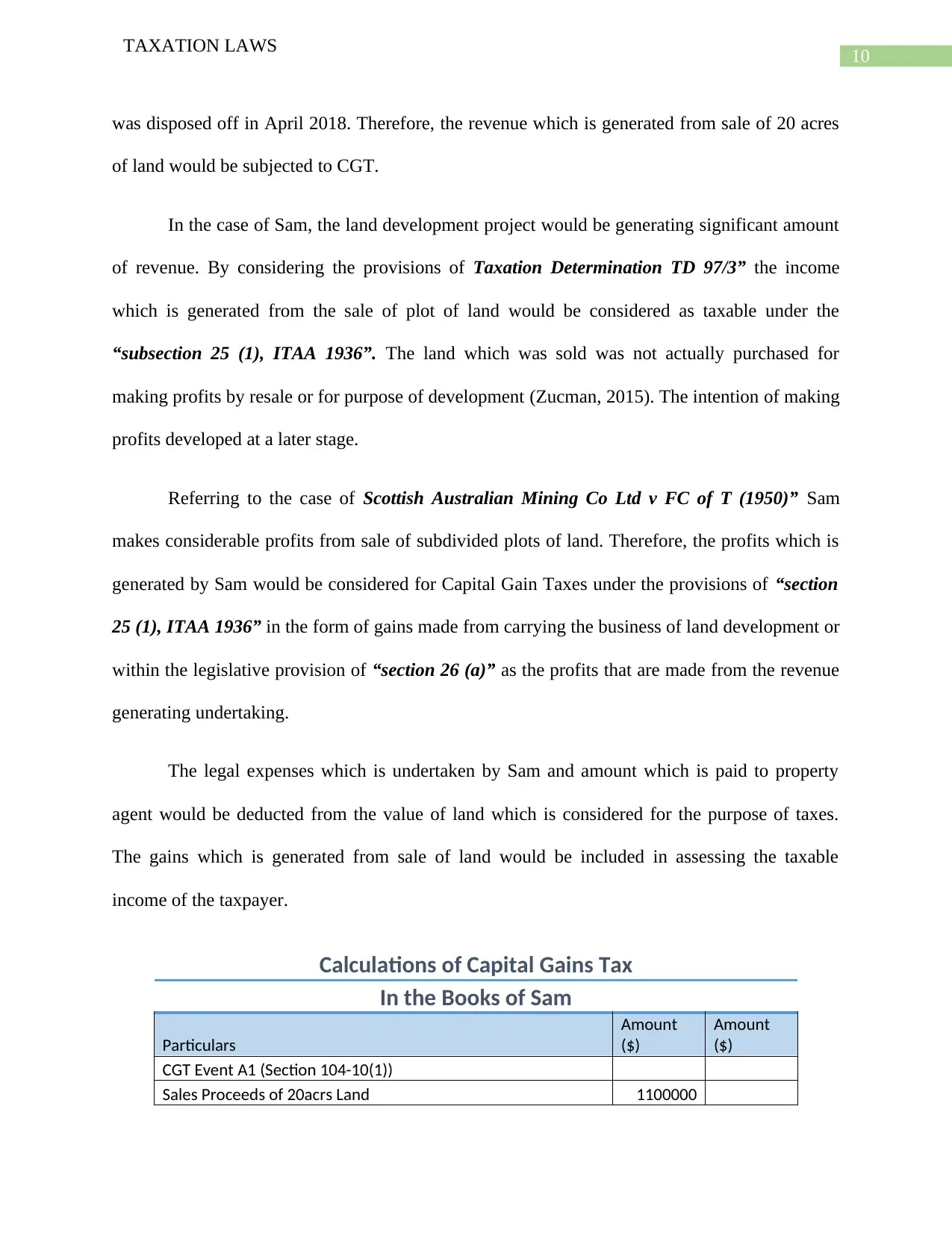

Calculations of Capital Gains Tax

In the Books of Sam

Particulars

Amount

($)

Amount

($)

CGT Event A1 (Section 104-10(1))

Sales Proceeds of 20acrs Land 1100000

TAXATION LAWS

was disposed off in April 2018. Therefore, the revenue which is generated from sale of 20 acres

of land would be subjected to CGT.

In the case of Sam, the land development project would be generating significant amount

of revenue. By considering the provisions of Taxation Determination TD 97/3” the income

which is generated from the sale of plot of land would be considered as taxable under the

“subsection 25 (1), ITAA 1936”. The land which was sold was not actually purchased for

making profits by resale or for purpose of development (Zucman, 2015). The intention of making

profits developed at a later stage.

Referring to the case of Scottish Australian Mining Co Ltd v FC of T (1950)” Sam

makes considerable profits from sale of subdivided plots of land. Therefore, the profits which is

generated by Sam would be considered for Capital Gain Taxes under the provisions of “section

25 (1), ITAA 1936” in the form of gains made from carrying the business of land development or

within the legislative provision of “section 26 (a)” as the profits that are made from the revenue

generating undertaking.

The legal expenses which is undertaken by Sam and amount which is paid to property

agent would be deducted from the value of land which is considered for the purpose of taxes.

The gains which is generated from sale of land would be included in assessing the taxable

income of the taxpayer.

Calculations of Capital Gains Tax

In the Books of Sam

Particulars

Amount

($)

Amount

($)

CGT Event A1 (Section 104-10(1))

Sales Proceeds of 20acrs Land 1100000

11

TAXATION LAWS

Agent Commission and Legal fees 45000

Total Sales Proceeds 1145000

Cost base item (Section 110-25 (1)

Element 1: Cost of Acqusition (section 110-25 (1) 110000

Element 4: Capital Enhancement Cost (section 110-25 (4)) 450000

Total Cost Base 560000

Net Capital Gains 585000

Conclusion

The analysis of the situation of Sam shows that the 80 acres land which was initially

purchased does not fall under the purview of CGT as the land was purchased before 1984 and

therefore the same would be considered as pre-CGT asset. While at the same time, 20 acres land

which was purchased on February 1985 would be considered as post CGT asset. The provisions

of taxation “section 25 (1) of the ITAA 1936” makes it clear that sale of subdivided plots of land

would be taxable in the form of gains which are made for carrying the business of land

development or any other legislature.

TAXATION LAWS

Agent Commission and Legal fees 45000

Total Sales Proceeds 1145000

Cost base item (Section 110-25 (1)

Element 1: Cost of Acqusition (section 110-25 (1) 110000

Element 4: Capital Enhancement Cost (section 110-25 (4)) 450000

Total Cost Base 560000

Net Capital Gains 585000

Conclusion

The analysis of the situation of Sam shows that the 80 acres land which was initially

purchased does not fall under the purview of CGT as the land was purchased before 1984 and

therefore the same would be considered as pre-CGT asset. While at the same time, 20 acres land

which was purchased on February 1985 would be considered as post CGT asset. The provisions

of taxation “section 25 (1) of the ITAA 1936” makes it clear that sale of subdivided plots of land

would be taxable in the form of gains which are made for carrying the business of land

development or any other legislature.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.