Comprehensive Taxation Report: Fringe Benefits, Employment and FBT

VerifiedAdded on 2019/10/31

|9

|2730

|168

Report

AI Summary

This report provides a comprehensive analysis of taxation, focusing on fringe benefits and employment duties, using the case of Charlie, an employee of Shine Homes Pty Ltd. The report examines various aspects of tax determination, including the impact of fringe benefits on assessable income. It delves into relevant legislation such as the Fringe Benefit Tax Assessment Act 1986 and the Income Tax Assessment Act 1997. The application section discusses the operational cost model for car fringe benefits, considering factors like traveling distance and private use. It also addresses employment duties of an itinerant nature, car parking fringe benefits, and FBT on accommodation, with references to legal precedents and taxation rulings. The report further explores the tax liability of Shine Homes related to providing various benefits to Charlie, including car usage, parking, and accommodation, in compliance with the relevant legislations. The report provides a clear understanding of the tax implications of fringe benefits and employment-related expenses.

Running head: TAXATION

Taxation

Name of the Student

Name of the University

Authors Note

Course ID

Taxation

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION

Table of Contents

Issue............................................................................................................................................2

Law.............................................................................................................................................2

Application.................................................................................................................................3

Employment duties of an Itinerant Nature:................................................................................5

Car parking fringe benefit:.........................................................................................................5

FBT on accommodation:............................................................................................................6

Conclusion..................................................................................................................................7

Reference List:...........................................................................................................................8

Table of Contents

Issue............................................................................................................................................2

Law.............................................................................................................................................2

Application.................................................................................................................................3

Employment duties of an Itinerant Nature:................................................................................5

Car parking fringe benefit:.........................................................................................................5

FBT on accommodation:............................................................................................................6

Conclusion..................................................................................................................................7

Reference List:...........................................................................................................................8

2TAXATION

Issue

The main issue of the study have been seen in terms of the evaluation of the different

aspects of tax determination of and know about the impact of Shine Homes and Charlie. This

has been further determined with the case study of Charlie who is an employee of Shiney

Holmes Pty Ltd. has been further seen with the real estate agent. On the contrary Holmes has

been able to perform business landscaping to provide 4 wheeler sedan car. As per “Section 6

of the Miscellaneous Taxation Rulings and Fringe Benefit Tax Assessment Act 1986” the

various types of the provision has been seen with the different types of the circumstances

defined under the fringe benefit taxation rulings (Rootes, 2014).

Law

a. “Section 6 of the Miscellaneous Taxation Rulings and Fringe Benefit Tax

Assessment Act 1986”

b. “Taxation rulings of MT 2027”

c. “Section 136 (1)”

d. “Sub-section 136 (1) of the Miscellaneous Taxation Rulings of 2027”

e. “Section 51 of the Income Tax Assessment Act 1997”

f. “Miscellaneous Taxation Rulings of 2027”

g. “Sub-division F of Division 3”

h. “Taxation rulings of IT 112”

i. “Section 51 of the Income Tax Assessment Act 1997”

j. “Newsom v Robertson (1952) 2 All ER 728; (1952)”

k. “Simon in Taylor v Provan (1975) AC 194”

l. “FBT Act 1986”

m. “Fringe Benefit Tax Act 1986”

n. “TR 94/25”

o. “Section 5 of the Fringe Benefit Tax Act 1986”

p. “Subsection 51 (1) of the Income Tax Assessment Act 1936”

q. “Subsection 51 (1) of the ITAA 1997”

r. “Section 5 of the Fringe Benefit Tax Act 1986”

s. “Tubemakers of Australia Ltd v. FC of T 93”

Issue

The main issue of the study have been seen in terms of the evaluation of the different

aspects of tax determination of and know about the impact of Shine Homes and Charlie. This

has been further determined with the case study of Charlie who is an employee of Shiney

Holmes Pty Ltd. has been further seen with the real estate agent. On the contrary Holmes has

been able to perform business landscaping to provide 4 wheeler sedan car. As per “Section 6

of the Miscellaneous Taxation Rulings and Fringe Benefit Tax Assessment Act 1986” the

various types of the provision has been seen with the different types of the circumstances

defined under the fringe benefit taxation rulings (Rootes, 2014).

Law

a. “Section 6 of the Miscellaneous Taxation Rulings and Fringe Benefit Tax

Assessment Act 1986”

b. “Taxation rulings of MT 2027”

c. “Section 136 (1)”

d. “Sub-section 136 (1) of the Miscellaneous Taxation Rulings of 2027”

e. “Section 51 of the Income Tax Assessment Act 1997”

f. “Miscellaneous Taxation Rulings of 2027”

g. “Sub-division F of Division 3”

h. “Taxation rulings of IT 112”

i. “Section 51 of the Income Tax Assessment Act 1997”

j. “Newsom v Robertson (1952) 2 All ER 728; (1952)”

k. “Simon in Taylor v Provan (1975) AC 194”

l. “FBT Act 1986”

m. “Fringe Benefit Tax Act 1986”

n. “TR 94/25”

o. “Section 5 of the Fringe Benefit Tax Act 1986”

p. “Subsection 51 (1) of the Income Tax Assessment Act 1936”

q. “Subsection 51 (1) of the ITAA 1997”

r. “Section 5 of the Fringe Benefit Tax Act 1986”

s. “Tubemakers of Australia Ltd v. FC of T 93”

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION

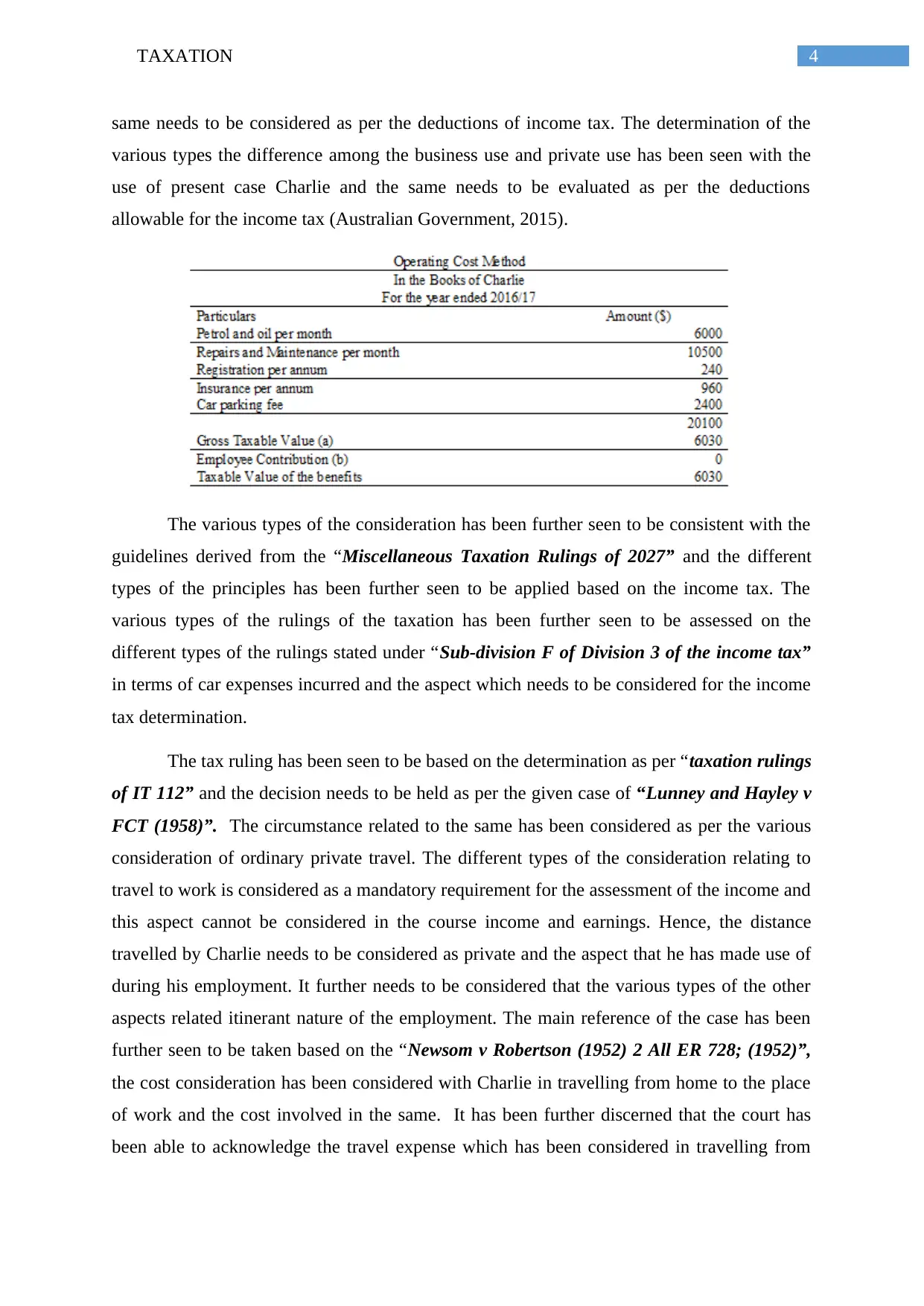

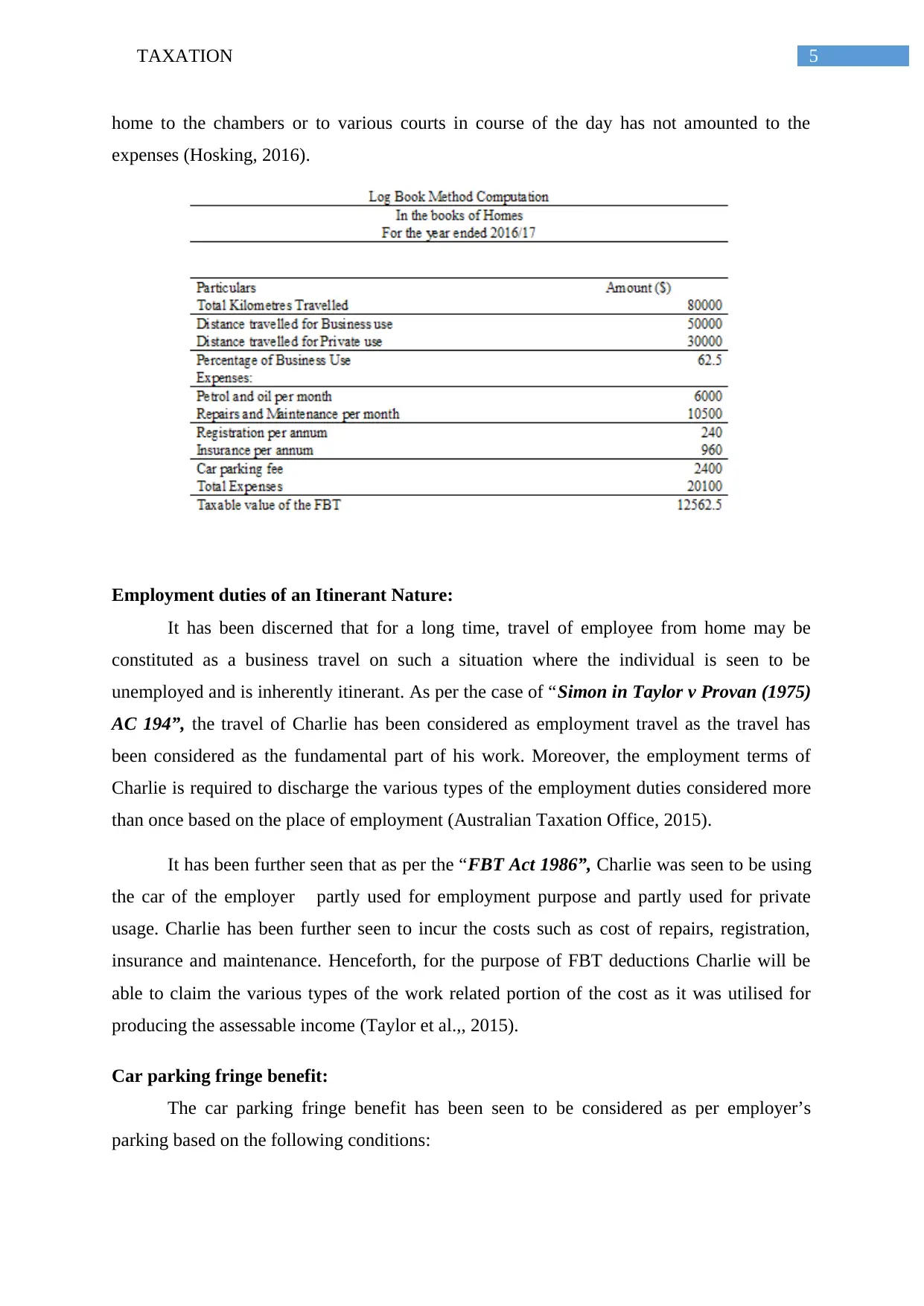

Application

As determined under “taxation rulings of MT 2027” under “sub section 136 (1)”, the

use of the assessable income will be considered based on the private usage. Despite of this, as

per “sub-section 136 (1)”, has stated on the various types of the operating cost as per the

valuation method has been used in the business and the same has been stated with the private

use made by the associate or the employees. As per the paragraph 3, the different types of the

“Miscellaneous Taxation Ruling” is required for the business in terms of recording in the

logbook and the same has been seen as an identical form of the document for the use in the

private use of a car and the same has been applied as per the operating cost methodology. It

has been further determined that the different types of the consideration made in the taxation

has been based on the travelling distance of Charlie with more than 50,000 km relating to

work. The operational cost model is applicable for the determination of the fringe benefit of

the car and the same has been complied with the ‘sub-section 136 (1) of the Miscellaneous

Taxation Rulings of 2027” (Australian Trade Commission, 2015).

The main question has been seen in terms of the determination of taxation arise out of

the business and personal use. Henceforth, the car used by the employee was taken

exclusively in course in generating the assessable income of the employee. The various

considerations has been taken with various factors in assessing of the income which needs to

be produced as per the assessable income and done as per “sub section 136 (1)”. The study

has further followed the course of employment that has been able to provide the various types

of the business activity carried with the employment activity of the employee constituted with

the use of FBT. In addition to this, the car made by the associate has been taken into

consideration with the business which is carried out in a similar fashion and considered for

the purpose of business use.

As per the given in the case, Charlie has made use of the vehicle at the time of his

employment and this has been carried out with the business activities. Charlie has been

further seen to use the car in the production of the assessable income of the employee and the

same has been able to attract Fringe benefit Tax.

The various types of the test has been further seen to be based on the as per both

private and business for FBT and the same has been seen to be applicable with assessing the

deductibility rationale under “section 51 of the Income Tax Assessment Act 1997”. Different

types of the evidences has been inferred from use of car by the use of employment and the

Application

As determined under “taxation rulings of MT 2027” under “sub section 136 (1)”, the

use of the assessable income will be considered based on the private usage. Despite of this, as

per “sub-section 136 (1)”, has stated on the various types of the operating cost as per the

valuation method has been used in the business and the same has been stated with the private

use made by the associate or the employees. As per the paragraph 3, the different types of the

“Miscellaneous Taxation Ruling” is required for the business in terms of recording in the

logbook and the same has been seen as an identical form of the document for the use in the

private use of a car and the same has been applied as per the operating cost methodology. It

has been further determined that the different types of the consideration made in the taxation

has been based on the travelling distance of Charlie with more than 50,000 km relating to

work. The operational cost model is applicable for the determination of the fringe benefit of

the car and the same has been complied with the ‘sub-section 136 (1) of the Miscellaneous

Taxation Rulings of 2027” (Australian Trade Commission, 2015).

The main question has been seen in terms of the determination of taxation arise out of

the business and personal use. Henceforth, the car used by the employee was taken

exclusively in course in generating the assessable income of the employee. The various

considerations has been taken with various factors in assessing of the income which needs to

be produced as per the assessable income and done as per “sub section 136 (1)”. The study

has further followed the course of employment that has been able to provide the various types

of the business activity carried with the employment activity of the employee constituted with

the use of FBT. In addition to this, the car made by the associate has been taken into

consideration with the business which is carried out in a similar fashion and considered for

the purpose of business use.

As per the given in the case, Charlie has made use of the vehicle at the time of his

employment and this has been carried out with the business activities. Charlie has been

further seen to use the car in the production of the assessable income of the employee and the

same has been able to attract Fringe benefit Tax.

The various types of the test has been further seen to be based on the as per both

private and business for FBT and the same has been seen to be applicable with assessing the

deductibility rationale under “section 51 of the Income Tax Assessment Act 1997”. Different

types of the evidences has been inferred from use of car by the use of employment and the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION

same needs to be considered as per the deductions of income tax. The determination of the

various types the difference among the business use and private use has been seen with the

use of present case Charlie and the same needs to be evaluated as per the deductions

allowable for the income tax (Australian Government, 2015).

The various types of the consideration has been further seen to be consistent with the

guidelines derived from the “Miscellaneous Taxation Rulings of 2027” and the different

types of the principles has been further seen to be applied based on the income tax. The

various types of the rulings of the taxation has been further seen to be assessed on the

different types of the rulings stated under “Sub-division F of Division 3 of the income tax”

in terms of car expenses incurred and the aspect which needs to be considered for the income

tax determination.

The tax ruling has been seen to be based on the determination as per “taxation rulings

of IT 112” and the decision needs to be held as per the given case of “Lunney and Hayley v

FCT (1958)”. The circumstance related to the same has been considered as per the various

consideration of ordinary private travel. The different types of the consideration relating to

travel to work is considered as a mandatory requirement for the assessment of the income and

this aspect cannot be considered in the course income and earnings. Hence, the distance

travelled by Charlie needs to be considered as private and the aspect that he has made use of

during his employment. It further needs to be considered that the various types of the other

aspects related itinerant nature of the employment. The main reference of the case has been

further seen to be taken based on the “Newsom v Robertson (1952) 2 All ER 728; (1952)”,

the cost consideration has been considered with Charlie in travelling from home to the place

of work and the cost involved in the same. It has been further discerned that the court has

been able to acknowledge the travel expense which has been considered in travelling from

same needs to be considered as per the deductions of income tax. The determination of the

various types the difference among the business use and private use has been seen with the

use of present case Charlie and the same needs to be evaluated as per the deductions

allowable for the income tax (Australian Government, 2015).

The various types of the consideration has been further seen to be consistent with the

guidelines derived from the “Miscellaneous Taxation Rulings of 2027” and the different

types of the principles has been further seen to be applied based on the income tax. The

various types of the rulings of the taxation has been further seen to be assessed on the

different types of the rulings stated under “Sub-division F of Division 3 of the income tax”

in terms of car expenses incurred and the aspect which needs to be considered for the income

tax determination.

The tax ruling has been seen to be based on the determination as per “taxation rulings

of IT 112” and the decision needs to be held as per the given case of “Lunney and Hayley v

FCT (1958)”. The circumstance related to the same has been considered as per the various

consideration of ordinary private travel. The different types of the consideration relating to

travel to work is considered as a mandatory requirement for the assessment of the income and

this aspect cannot be considered in the course income and earnings. Hence, the distance

travelled by Charlie needs to be considered as private and the aspect that he has made use of

during his employment. It further needs to be considered that the various types of the other

aspects related itinerant nature of the employment. The main reference of the case has been

further seen to be taken based on the “Newsom v Robertson (1952) 2 All ER 728; (1952)”,

the cost consideration has been considered with Charlie in travelling from home to the place

of work and the cost involved in the same. It has been further discerned that the court has

been able to acknowledge the travel expense which has been considered in travelling from

5TAXATION

home to the chambers or to various courts in course of the day has not amounted to the

expenses (Hosking, 2016).

Employment duties of an Itinerant Nature:

It has been discerned that for a long time, travel of employee from home may be

constituted as a business travel on such a situation where the individual is seen to be

unemployed and is inherently itinerant. As per the case of “Simon in Taylor v Provan (1975)

AC 194”, the travel of Charlie has been considered as employment travel as the travel has

been considered as the fundamental part of his work. Moreover, the employment terms of

Charlie is required to discharge the various types of the employment duties considered more

than once based on the place of employment (Australian Taxation Office, 2015).

It has been further seen that as per the “FBT Act 1986”, Charlie was seen to be using

the car of the employer partly used for employment purpose and partly used for private

usage. Charlie has been further seen to incur the costs such as cost of repairs, registration,

insurance and maintenance. Henceforth, for the purpose of FBT deductions Charlie will be

able to claim the various types of the work related portion of the cost as it was utilised for

producing the assessable income (Taylor et al.,, 2015).

Car parking fringe benefit:

The car parking fringe benefit has been seen to be considered as per employer’s

parking based on the following conditions:

home to the chambers or to various courts in course of the day has not amounted to the

expenses (Hosking, 2016).

Employment duties of an Itinerant Nature:

It has been discerned that for a long time, travel of employee from home may be

constituted as a business travel on such a situation where the individual is seen to be

unemployed and is inherently itinerant. As per the case of “Simon in Taylor v Provan (1975)

AC 194”, the travel of Charlie has been considered as employment travel as the travel has

been considered as the fundamental part of his work. Moreover, the employment terms of

Charlie is required to discharge the various types of the employment duties considered more

than once based on the place of employment (Australian Taxation Office, 2015).

It has been further seen that as per the “FBT Act 1986”, Charlie was seen to be using

the car of the employer partly used for employment purpose and partly used for private

usage. Charlie has been further seen to incur the costs such as cost of repairs, registration,

insurance and maintenance. Henceforth, for the purpose of FBT deductions Charlie will be

able to claim the various types of the work related portion of the cost as it was utilised for

producing the assessable income (Taylor et al.,, 2015).

Car parking fringe benefit:

The car parking fringe benefit has been seen to be considered as per employer’s

parking based on the following conditions:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION

a. The car has been parked in the premise and the same was seen to be owned or leased

under the control of provider

b. The car had been seen to be parked exceeding four hours

c. The vehicle has been leased or owned as per the control of employee

d. The vehicle was given in respect to the employment of the employee

e. The car has been further seen to be used as per the travel between work and home for

minimum of one day

The same has been further seen to be evident with the aforementioned conditions. It

has been discerned that Charlie has parked his car at a secure area of parking which has

been considered from the employer and for the same Shine Homes has made a payment

of $ 200 every week. The main consideration has been further able to show that the car

was parked in the garage of Charlie and the same was under the control of the provider.

The vehicle was further provided to Charlie as per the terms of his employment. In

addition to this, Charlie was able to use the car for travelling from home to work every

day. Henceforth, the fringe will arise as per the deductions claimed with Charlie and

Homes with parking fees paid on behalf of the employee (Devos, 2014).

FBT on accommodation:

As per the “Fringe Benefit Tax Act 1986”, the main form of the provision has been

represented with the entertainment in form of accommodation, drink or recreation which is in

connection to the entertainment. As evident from the case stud, Charlie has encountered with

a minor accident was not able to use the vehicle for a total period of 2 weeks. This has been

further seen to be taken based on the wedding of Charlie and Shine Holmes, who under took

the decision for hiring of the car for that particular period and allow Charlie to attend his

honeymoon (Grantley Taylor & Richardson, 2013). The present circumstance has been

further seen to be considered as per the fringe benefit provision for tax, which has been able

to attract the tax liability for the entertainment of the employees and the non employees for a

weekend, thereby offering them a holiday. As per the given situation it has been further seen

that the different types of the rulings and the timing of the fringe benefit and the instalment of

fringe benefit has been taken into consideration based on “subsection 51 (1)”. As per the

rulings of taxation “TR 94/25”, the fringe benefit instalments is generally considered as per

generating assessable income seen to take place in conducting the business activities and the

amount of the same are seen to be deductible as per “subsection 51 (1) of the ITAA” (Meng,

2014).

a. The car has been parked in the premise and the same was seen to be owned or leased

under the control of provider

b. The car had been seen to be parked exceeding four hours

c. The vehicle has been leased or owned as per the control of employee

d. The vehicle was given in respect to the employment of the employee

e. The car has been further seen to be used as per the travel between work and home for

minimum of one day

The same has been further seen to be evident with the aforementioned conditions. It

has been discerned that Charlie has parked his car at a secure area of parking which has

been considered from the employer and for the same Shine Homes has made a payment

of $ 200 every week. The main consideration has been further able to show that the car

was parked in the garage of Charlie and the same was under the control of the provider.

The vehicle was further provided to Charlie as per the terms of his employment. In

addition to this, Charlie was able to use the car for travelling from home to work every

day. Henceforth, the fringe will arise as per the deductions claimed with Charlie and

Homes with parking fees paid on behalf of the employee (Devos, 2014).

FBT on accommodation:

As per the “Fringe Benefit Tax Act 1986”, the main form of the provision has been

represented with the entertainment in form of accommodation, drink or recreation which is in

connection to the entertainment. As evident from the case stud, Charlie has encountered with

a minor accident was not able to use the vehicle for a total period of 2 weeks. This has been

further seen to be taken based on the wedding of Charlie and Shine Holmes, who under took

the decision for hiring of the car for that particular period and allow Charlie to attend his

honeymoon (Grantley Taylor & Richardson, 2013). The present circumstance has been

further seen to be considered as per the fringe benefit provision for tax, which has been able

to attract the tax liability for the entertainment of the employees and the non employees for a

weekend, thereby offering them a holiday. As per the given situation it has been further seen

that the different types of the rulings and the timing of the fringe benefit and the instalment of

fringe benefit has been taken into consideration based on “subsection 51 (1)”. As per the

rulings of taxation “TR 94/25”, the fringe benefit instalments is generally considered as per

generating assessable income seen to take place in conducting the business activities and the

amount of the same are seen to be deductible as per “subsection 51 (1) of the ITAA” (Meng,

2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION

The liability associated to the Fringe Benefit Tax for Shine Homes have taken place

with the various types of the common wealth legislations. As per “section 5 of the Fringe

Benefit Tax Act 1986”, tax is seen to be generally imposed based on the various

considerations made as per the FBT of an employer outstanding in a particular year. As

per the reference “Tubemakers of Australia Ltd v. FC of T 93” the fringe benefit sum

needs to be composed with the total amount incurred with the numerous FBT provided to

Charlie by Shine Homes (D’Ascenzo, 2015).

As per the given scenario, it has been further seen to be evident that the consideration

various types of the expenses such as honeymoon accommodation, parking fees, hiring

cost and the expenses incurred in producing or gaining of the taxable income. The main

consideration of this has been seen with the compliance with “subsection 51 (1) of the

ITAA 1997” and the expenses which has taken place in gaining or produced with the

assessable income for carrying of a business and this needs to be considered with the

deductible expenses (ATO, 2016).

Conclusion

The important considerations of the study have been able to highlight on the different

types of the benefits based on fringe benefit and the same is seen to be taxable as per “FBT

Act 1986”. The study has been further able to show the relevant case laws and sections

which is related to the car fringe benefit. The use of the vehicle by Charlie has been

constituted on accordance to the production of the assessable income from the employee and

the same is seen to attract high amount of “Fringe Benefit Tax”.

The liability associated to the Fringe Benefit Tax for Shine Homes have taken place

with the various types of the common wealth legislations. As per “section 5 of the Fringe

Benefit Tax Act 1986”, tax is seen to be generally imposed based on the various

considerations made as per the FBT of an employer outstanding in a particular year. As

per the reference “Tubemakers of Australia Ltd v. FC of T 93” the fringe benefit sum

needs to be composed with the total amount incurred with the numerous FBT provided to

Charlie by Shine Homes (D’Ascenzo, 2015).

As per the given scenario, it has been further seen to be evident that the consideration

various types of the expenses such as honeymoon accommodation, parking fees, hiring

cost and the expenses incurred in producing or gaining of the taxable income. The main

consideration of this has been seen with the compliance with “subsection 51 (1) of the

ITAA 1997” and the expenses which has taken place in gaining or produced with the

assessable income for carrying of a business and this needs to be considered with the

deductible expenses (ATO, 2016).

Conclusion

The important considerations of the study have been able to highlight on the different

types of the benefits based on fringe benefit and the same is seen to be taxable as per “FBT

Act 1986”. The study has been further able to show the relevant case laws and sections

which is related to the car fringe benefit. The use of the vehicle by Charlie has been

constituted on accordance to the production of the assessable income from the employee and

the same is seen to attract high amount of “Fringe Benefit Tax”.

8TAXATION

Reference List:

ATO. (2016). Luxury car tax. Australian Tax Office, 5. Retrieved from

https://www.ato.gov.au/Business/Luxury-car-tax/

Australian Government. (2015). Australian Taxation Office. Registerting for GST. Retrieved

from https://www.ato.gov.au/Business/GST/Registering-for-GST/

Australian Taxation Office. (2015). Yearly reports and returns | Australian Taxation Office.

Retrieved from https://www.ato.gov.au/Business/Yearly-reports-and-returns/

Australian Trade Commission. (2015). Australian Business Taxes. Retrieved from

http://www.austrade.gov.au/International/Invest/Guide-to-investing/Running-a-

business/Understanding-Australian-taxes/Australian-business-taxes

D’Ascenzo, M. (2015). Modernising the Australian Taxation Office: Vision, people, systems

and values. eJournal of Tax Research, 13(1), 361–377.

Devos, K. (2014). Do penalties and enforcement measures make taxpayers more compliant?-

The view of Australian tax evaders’. Journal of Business & Economics, 5(2), 265–284.

Retrieved from http://www.academicstar.us

Hosking, A. (2016). Australian Taxation Office adds voice authentication to its app.

Biometric Technology Today. https://doi.org/10.1016/S0969-4765(16)30038-8

Meng, S. (2014). How may a carbon tax transform Australian electricity industry? A CGE

analysis. Applied Economics, 46(8), 796–812.

https://doi.org/10.1080/00036846.2013.854302

Rootes, C. (2014). A referendum on the carbon tax? The 2013 Australian election, the

Greens, and the environment. Environmental Politics, 23(1), 166–173.

https://doi.org/10.1080/09644016.2014.878088

Taylor, G., & Richardson, G. (2013). The determinants of thinly capitalized tax avoidance

structures: Evidence from Australian firms. Journal of International Accounting,

Auditing and Taxation, 22(1), 12–25. https://doi.org/10.1016/j.intaccaudtax.2013.02.005

Taylor, G., Richardson, G., & Taplin, R. (2015). Determinants of tax haven utilization:

Evidence from Australian firms. Accounting and Finance, 55(2), 545–574.

https://doi.org/10.1111/acfi.12064

Reference List:

ATO. (2016). Luxury car tax. Australian Tax Office, 5. Retrieved from

https://www.ato.gov.au/Business/Luxury-car-tax/

Australian Government. (2015). Australian Taxation Office. Registerting for GST. Retrieved

from https://www.ato.gov.au/Business/GST/Registering-for-GST/

Australian Taxation Office. (2015). Yearly reports and returns | Australian Taxation Office.

Retrieved from https://www.ato.gov.au/Business/Yearly-reports-and-returns/

Australian Trade Commission. (2015). Australian Business Taxes. Retrieved from

http://www.austrade.gov.au/International/Invest/Guide-to-investing/Running-a-

business/Understanding-Australian-taxes/Australian-business-taxes

D’Ascenzo, M. (2015). Modernising the Australian Taxation Office: Vision, people, systems

and values. eJournal of Tax Research, 13(1), 361–377.

Devos, K. (2014). Do penalties and enforcement measures make taxpayers more compliant?-

The view of Australian tax evaders’. Journal of Business & Economics, 5(2), 265–284.

Retrieved from http://www.academicstar.us

Hosking, A. (2016). Australian Taxation Office adds voice authentication to its app.

Biometric Technology Today. https://doi.org/10.1016/S0969-4765(16)30038-8

Meng, S. (2014). How may a carbon tax transform Australian electricity industry? A CGE

analysis. Applied Economics, 46(8), 796–812.

https://doi.org/10.1080/00036846.2013.854302

Rootes, C. (2014). A referendum on the carbon tax? The 2013 Australian election, the

Greens, and the environment. Environmental Politics, 23(1), 166–173.

https://doi.org/10.1080/09644016.2014.878088

Taylor, G., & Richardson, G. (2013). The determinants of thinly capitalized tax avoidance

structures: Evidence from Australian firms. Journal of International Accounting,

Auditing and Taxation, 22(1), 12–25. https://doi.org/10.1016/j.intaccaudtax.2013.02.005

Taylor, G., Richardson, G., & Taplin, R. (2015). Determinants of tax haven utilization:

Evidence from Australian firms. Accounting and Finance, 55(2), 545–574.

https://doi.org/10.1111/acfi.12064

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.