Malaysian tax system - Assignment

VerifiedAdded on 2021/02/19

|13

|3564

|26

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

TAXATION

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK...............................................................................................................................................1

Malaysian tax system:............................................................................................................1

Individual income tax payable in Malaysia:...........................................................................2

Comparisons of tax rate between current and prior year:.......................................................6

Implication of changes in tax rate on taxpayers in Malaysia:................................................8

CONCLUSION ...............................................................................................................................9

REFERENCE.................................................................................................................................10

INTRODUCTION...........................................................................................................................1

TASK...............................................................................................................................................1

Malaysian tax system:............................................................................................................1

Individual income tax payable in Malaysia:...........................................................................2

Comparisons of tax rate between current and prior year:.......................................................6

Implication of changes in tax rate on taxpayers in Malaysia:................................................8

CONCLUSION ...............................................................................................................................9

REFERENCE.................................................................................................................................10

INTRODUCTION

Taxation refers to term used in case relevant taxing authority or government impose a tax

on individuals, corporates etc. Taxation is one of the major source of revenue for government in

Malaysia. In country assessment of tax is based on current year basis and self assessment is main

feature of this tax system. Inland Revenue Board of Malaysia (IRBM) is main authority which is

responsible for tax collection in country. It also monitors and controls the regulatory requirement

in order to improve tax collection system. Specific rules and regulations are framed for different

taxpayers like individuals, body of individuals, trusts, corporates etc. In country for strict

compliance of rules and regulations of taxation, penalties and fines are prescribed (Desiana,

2019). This report provides an explanation about Malaysian tax system, structure of individual

income tax collection, recent change in tax rate system and a systematic comparison current and

previous tax rates. This report also contains implication of fluctuation of tax rates on Malaysian

tax payers.

TASK

Malaysian tax system:

Assessment system:

Malaysian taxation system contains rules, regulations, taxation policies, procedures,

forms and guidelines which covers all aspects of taxation and help to improve overall taxation

system of the country. Income earned, accrued income, income remitted to or derived from

country is taxable in hand of individual, company, body of individual etc. as the case may be. All

the tables used in report are obtained through official government website (Income Tax Rates,

2019). Incomes earned by residents in or outside the country are taxable, for example global

incomes and earnings of resident companies doing business of transportation (air or sea),

insurance, banking are taxable. Corporates are liable to pay GST, property gains tax, corporate

income tax etc. Rates of taxes are divided in different slabs according to the type and source of

income (Haron and Ayojimi, 2018). Individuals are responsible for self-taxation assessment in

Malaysia. Specific forms are prescribed for tax payers to submit their details in respect of

income.

1

Taxation refers to term used in case relevant taxing authority or government impose a tax

on individuals, corporates etc. Taxation is one of the major source of revenue for government in

Malaysia. In country assessment of tax is based on current year basis and self assessment is main

feature of this tax system. Inland Revenue Board of Malaysia (IRBM) is main authority which is

responsible for tax collection in country. It also monitors and controls the regulatory requirement

in order to improve tax collection system. Specific rules and regulations are framed for different

taxpayers like individuals, body of individuals, trusts, corporates etc. In country for strict

compliance of rules and regulations of taxation, penalties and fines are prescribed (Desiana,

2019). This report provides an explanation about Malaysian tax system, structure of individual

income tax collection, recent change in tax rate system and a systematic comparison current and

previous tax rates. This report also contains implication of fluctuation of tax rates on Malaysian

tax payers.

TASK

Malaysian tax system:

Assessment system:

Malaysian taxation system contains rules, regulations, taxation policies, procedures,

forms and guidelines which covers all aspects of taxation and help to improve overall taxation

system of the country. Income earned, accrued income, income remitted to or derived from

country is taxable in hand of individual, company, body of individual etc. as the case may be. All

the tables used in report are obtained through official government website (Income Tax Rates,

2019). Incomes earned by residents in or outside the country are taxable, for example global

incomes and earnings of resident companies doing business of transportation (air or sea),

insurance, banking are taxable. Corporates are liable to pay GST, property gains tax, corporate

income tax etc. Rates of taxes are divided in different slabs according to the type and source of

income (Haron and Ayojimi, 2018). Individuals are responsible for self-taxation assessment in

Malaysia. Specific forms are prescribed for tax payers to submit their details in respect of

income.

1

Year of assessment:

Assessment year refers to immediate year after financial year in which the income of the

previous year or the assessment of that particular financial year is assessed. Generally, tax

assessment is done by tax payers while considering current year income, however in some cases

brought forward income or previous sources are considered. In case of companies, for taxation

purpose no financial year is prescribed by The Companies Act, 2016. Financial year is fixed by

companies as per their discretion. Mostly companies prefer calendar year or quarter end such as

June 30, March 31 or September 30 as its financial year (Kraal, 2019). In case of a newly formed

company it is required to prepare their financial accounts within 18 months from the date of

incorporation. Thus if financial year is 01/04/2018 to 31/03/2019 (2018-19), then assessment

year would be 01/04/2019 to 31/03/2020 (2019-20).

Tax filing system:

Malaysian tax system is wholly based on e-fling tax system. IRBM or Inland Revenue

Board of Malaysia has issued regulations regarding applicability of e-filing tax system in

Malaysia. IRBM though their web portal named LHDN (Lembaga Hasil Dalam Negeri) has

launched e-filing system, in which a taxpayer can file and pay tax. The website link is

<http://edaftar.hasil.gov.my/>, which is currently popular and widely used by taxpayers in

Malaysian. It is very user friendly and simple manner of filing return. Along with this link

following link provide a details about how to fill return and pay tax:

https://www.researchgate.net/publication/

228915896_Tax_Efiling_Adoption_in_Malaysia_A_Conceptual_Model>

This allow users to calculate tax and file return (Wong, Chuah and Hope, 2019). It also

sends notification regarding filing return, payment of taxes and reminder about important dates

to tax payers.

Individual income tax payable in Malaysia:

A separate tax slab along with some reilef and exemptions are prescribed in Malaysia. In

context of individuals, there are two options are available for individuals (Married Couples) in

malaysia: First one is individual return and second is Jointly return (SETYONINGRUM and

PURWANTI, 2018). Tax is assessed on the basis of thier residential status also. Definition of

resident classifies individuals on criterias, as discussed below:

2

Assessment year refers to immediate year after financial year in which the income of the

previous year or the assessment of that particular financial year is assessed. Generally, tax

assessment is done by tax payers while considering current year income, however in some cases

brought forward income or previous sources are considered. In case of companies, for taxation

purpose no financial year is prescribed by The Companies Act, 2016. Financial year is fixed by

companies as per their discretion. Mostly companies prefer calendar year or quarter end such as

June 30, March 31 or September 30 as its financial year (Kraal, 2019). In case of a newly formed

company it is required to prepare their financial accounts within 18 months from the date of

incorporation. Thus if financial year is 01/04/2018 to 31/03/2019 (2018-19), then assessment

year would be 01/04/2019 to 31/03/2020 (2019-20).

Tax filing system:

Malaysian tax system is wholly based on e-fling tax system. IRBM or Inland Revenue

Board of Malaysia has issued regulations regarding applicability of e-filing tax system in

Malaysia. IRBM though their web portal named LHDN (Lembaga Hasil Dalam Negeri) has

launched e-filing system, in which a taxpayer can file and pay tax. The website link is

<http://edaftar.hasil.gov.my/>, which is currently popular and widely used by taxpayers in

Malaysian. It is very user friendly and simple manner of filing return. Along with this link

following link provide a details about how to fill return and pay tax:

https://www.researchgate.net/publication/

228915896_Tax_Efiling_Adoption_in_Malaysia_A_Conceptual_Model>

This allow users to calculate tax and file return (Wong, Chuah and Hope, 2019). It also

sends notification regarding filing return, payment of taxes and reminder about important dates

to tax payers.

Individual income tax payable in Malaysia:

A separate tax slab along with some reilef and exemptions are prescribed in Malaysia. In

context of individuals, there are two options are available for individuals (Married Couples) in

malaysia: First one is individual return and second is Jointly return (SETYONINGRUM and

PURWANTI, 2018). Tax is assessed on the basis of thier residential status also. Definition of

resident classifies individuals on criterias, as discussed below:

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

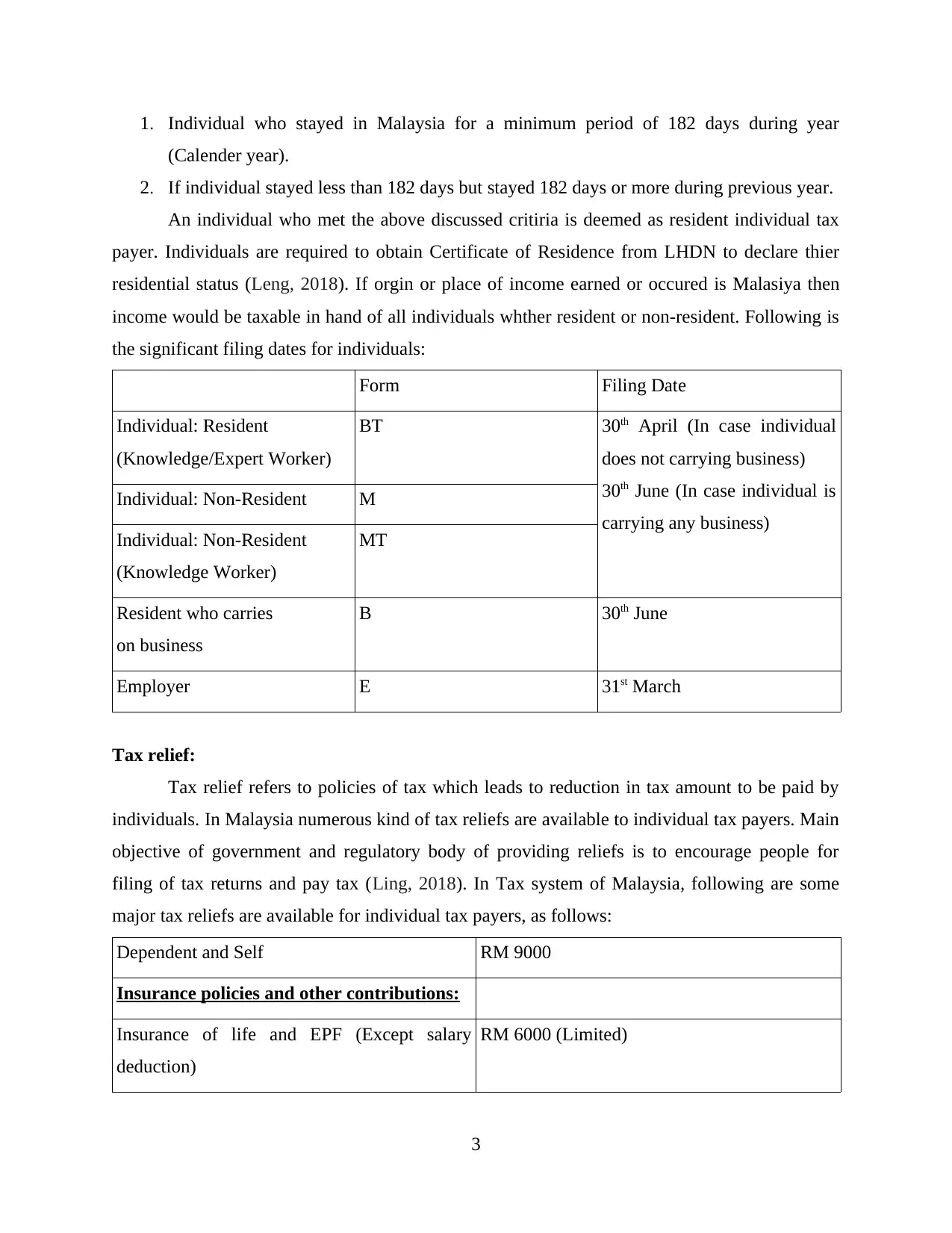

1. Individual who stayed in Malaysia for a minimum period of 182 days during year

(Calender year).

2. If individual stayed less than 182 days but stayed 182 days or more during previous year.

An individual who met the above discussed critiria is deemed as resident individual tax

payer. Individuals are required to obtain Certificate of Residence from LHDN to declare thier

residential status (Leng, 2018). If orgin or place of income earned or occured is Malasiya then

income would be taxable in hand of all individuals whther resident or non-resident. Following is

the significant filing dates for individuals:

Form Filing Date

Individual: Resident

(Knowledge/Expert Worker)

BT 30th April (In case individual

does not carrying business)

30th June (In case individual is

carrying any business)

Individual: Non-Resident M

Individual: Non-Resident

(Knowledge Worker)

MT

Resident who carries

on business

B 30th June

Employer E 31st March

Tax relief:

Tax relief refers to policies of tax which leads to reduction in tax amount to be paid by

individuals. In Malaysia numerous kind of tax reliefs are available to individual tax payers. Main

objective of government and regulatory body of providing reliefs is to encourage people for

filing of tax returns and pay tax (Ling, 2018). In Tax system of Malaysia, following are some

major tax reliefs are available for individual tax payers, as follows:

Dependent and Self RM 9000

Insurance policies and other contributions:

Insurance of life and EPF (Except salary

deduction)

RM 6000 (Limited)

3

(Calender year).

2. If individual stayed less than 182 days but stayed 182 days or more during previous year.

An individual who met the above discussed critiria is deemed as resident individual tax

payer. Individuals are required to obtain Certificate of Residence from LHDN to declare thier

residential status (Leng, 2018). If orgin or place of income earned or occured is Malasiya then

income would be taxable in hand of all individuals whther resident or non-resident. Following is

the significant filing dates for individuals:

Form Filing Date

Individual: Resident

(Knowledge/Expert Worker)

BT 30th April (In case individual

does not carrying business)

30th June (In case individual is

carrying any business)

Individual: Non-Resident M

Individual: Non-Resident

(Knowledge Worker)

MT

Resident who carries

on business

B 30th June

Employer E 31st March

Tax relief:

Tax relief refers to policies of tax which leads to reduction in tax amount to be paid by

individuals. In Malaysia numerous kind of tax reliefs are available to individual tax payers. Main

objective of government and regulatory body of providing reliefs is to encourage people for

filing of tax returns and pay tax (Ling, 2018). In Tax system of Malaysia, following are some

major tax reliefs are available for individual tax payers, as follows:

Dependent and Self RM 9000

Insurance policies and other contributions:

Insurance of life and EPF (Except salary

deduction)

RM 6000 (Limited)

3

Deferred annuity RM 3000 (Limited)

Private Retirement Scheme RM 3000 (Limited)

Insurance premium paid by individuals in

respect of medical or education (Except salary

deduction)

RM 3000 (Limited)

Contribution towards SOCSO (Social Security

Organisation)

RM 250 (Limited)

For specific taxpayers:

Alimony payments/Wife/Husband RM 4000 (Limited)

Medical expenses: Parents, or RM 5000 (Limited)

Parent:

In respect of : Only One Mother : RM 1500

In respect of : Only One Father : RM 1500

RM 3000 (Limited)

Education fees: RM 7000 (Limited)

1. Except a degree at accounting, vocational,

Islamic financing, Masters in law, technical,

scientific, industrial skills of qualification

2. Masters Degree in respect of gaining any

qualifications or skills

Medical expenses: (for spouse/self/child) RM 6000 (Limited)

Case 1: Serious Diseases

Case 2: Complete medical examination

Lifestyle and Households:

For purchasing items:(for spouse/self/child)

Journals, newspaper, magazine, books, and

other reading materials (excluding restricted

RM 2500 (Limited)

4

Private Retirement Scheme RM 3000 (Limited)

Insurance premium paid by individuals in

respect of medical or education (Except salary

deduction)

RM 3000 (Limited)

Contribution towards SOCSO (Social Security

Organisation)

RM 250 (Limited)

For specific taxpayers:

Alimony payments/Wife/Husband RM 4000 (Limited)

Medical expenses: Parents, or RM 5000 (Limited)

Parent:

In respect of : Only One Mother : RM 1500

In respect of : Only One Father : RM 1500

RM 3000 (Limited)

Education fees: RM 7000 (Limited)

1. Except a degree at accounting, vocational,

Islamic financing, Masters in law, technical,

scientific, industrial skills of qualification

2. Masters Degree in respect of gaining any

qualifications or skills

Medical expenses: (for spouse/self/child) RM 6000 (Limited)

Case 1: Serious Diseases

Case 2: Complete medical examination

Lifestyle and Households:

For purchasing items:(for spouse/self/child)

Journals, newspaper, magazine, books, and

other reading materials (excluding restricted

RM 2500 (Limited)

4

materials of reading)

For purchasing items:(for spouse/self/child)

smartphone, mobiles or tablet, PC

For purchasing items:(for spouse/self/child)

Equipment of Sports, Memberships of Gym

Internet Bills

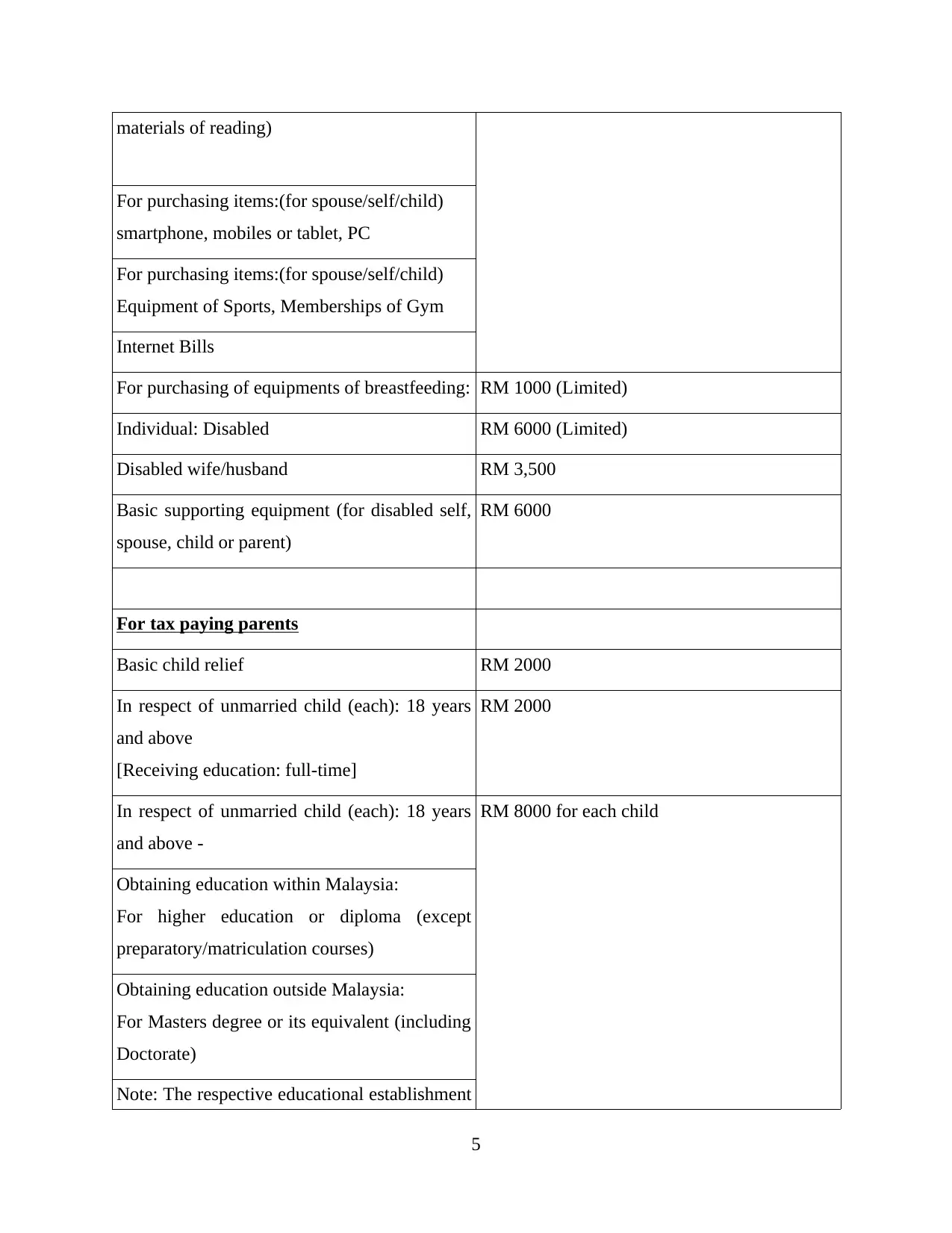

For purchasing of equipments of breastfeeding: RM 1000 (Limited)

Individual: Disabled RM 6000 (Limited)

Disabled wife/husband RM 3,500

Basic supporting equipment (for disabled self,

spouse, child or parent)

RM 6000

For tax paying parents

Basic child relief RM 2000

In respect of unmarried child (each): 18 years

and above

[Receiving education: full-time]

RM 2000

In respect of unmarried child (each): 18 years

and above -

RM 8000 for each child

Obtaining education within Malaysia:

For higher education or diploma (except

preparatory/matriculation courses)

Obtaining education outside Malaysia:

For Masters degree or its equivalent (including

Doctorate)

Note: The respective educational establishment

5

For purchasing items:(for spouse/self/child)

smartphone, mobiles or tablet, PC

For purchasing items:(for spouse/self/child)

Equipment of Sports, Memberships of Gym

Internet Bills

For purchasing of equipments of breastfeeding: RM 1000 (Limited)

Individual: Disabled RM 6000 (Limited)

Disabled wife/husband RM 3,500

Basic supporting equipment (for disabled self,

spouse, child or parent)

RM 6000

For tax paying parents

Basic child relief RM 2000

In respect of unmarried child (each): 18 years

and above

[Receiving education: full-time]

RM 2000

In respect of unmarried child (each): 18 years

and above -

RM 8000 for each child

Obtaining education within Malaysia:

For higher education or diploma (except

preparatory/matriculation courses)

Obtaining education outside Malaysia:

For Masters degree or its equivalent (including

Doctorate)

Note: The respective educational establishment

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

or university should be approved by

government authority

Disabled child RM 6000 for each child

Saving under SSPN's scheme RM 6000

Child care fees RM 1000

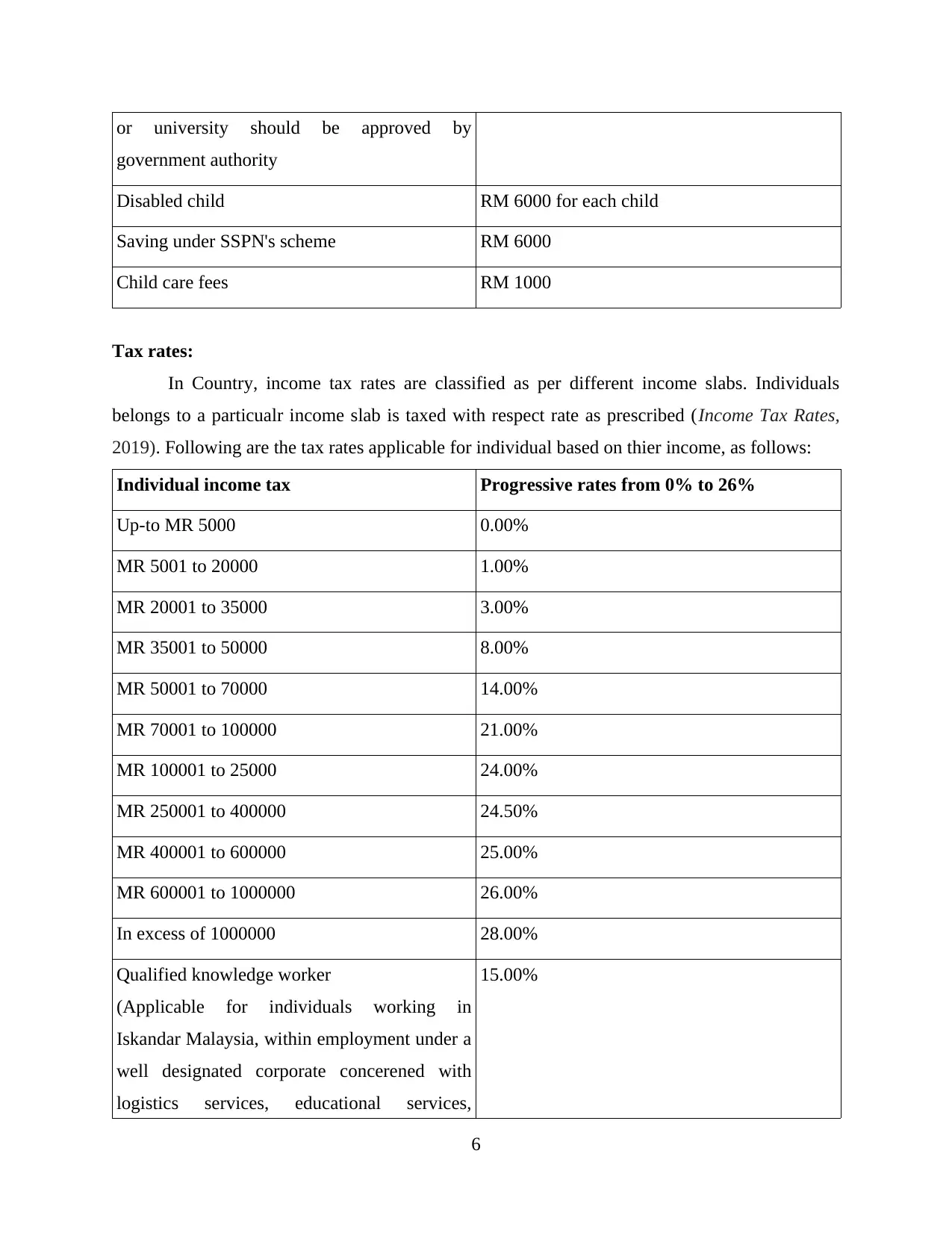

Tax rates:

In Country, income tax rates are classified as per different income slabs. Individuals

belongs to a particualr income slab is taxed with respect rate as prescribed (Income Tax Rates,

2019). Following are the tax rates applicable for individual based on thier income, as follows:

Individual income tax Progressive rates from 0% to 26%

Up-to MR 5000 0.00%

MR 5001 to 20000 1.00%

MR 20001 to 35000 3.00%

MR 35001 to 50000 8.00%

MR 50001 to 70000 14.00%

MR 70001 to 100000 21.00%

MR 100001 to 25000 24.00%

MR 250001 to 400000 24.50%

MR 400001 to 600000 25.00%

MR 600001 to 1000000 26.00%

In excess of 1000000 28.00%

Qualified knowledge worker

(Applicable for individuals working in

Iskandar Malaysia, within employment under a

well designated corporate concerened with

logistics services, educational services,

15.00%

6

government authority

Disabled child RM 6000 for each child

Saving under SSPN's scheme RM 6000

Child care fees RM 1000

Tax rates:

In Country, income tax rates are classified as per different income slabs. Individuals

belongs to a particualr income slab is taxed with respect rate as prescribed (Income Tax Rates,

2019). Following are the tax rates applicable for individual based on thier income, as follows:

Individual income tax Progressive rates from 0% to 26%

Up-to MR 5000 0.00%

MR 5001 to 20000 1.00%

MR 20001 to 35000 3.00%

MR 35001 to 50000 8.00%

MR 50001 to 70000 14.00%

MR 70001 to 100000 21.00%

MR 100001 to 25000 24.00%

MR 250001 to 400000 24.50%

MR 400001 to 600000 25.00%

MR 600001 to 1000000 26.00%

In excess of 1000000 28.00%

Qualified knowledge worker

(Applicable for individuals working in

Iskandar Malaysia, within employment under a

well designated corporate concerened with

logistics services, educational services,

15.00%

6

financial advisory, creative industries, green

technology, healthcare services and tourism)

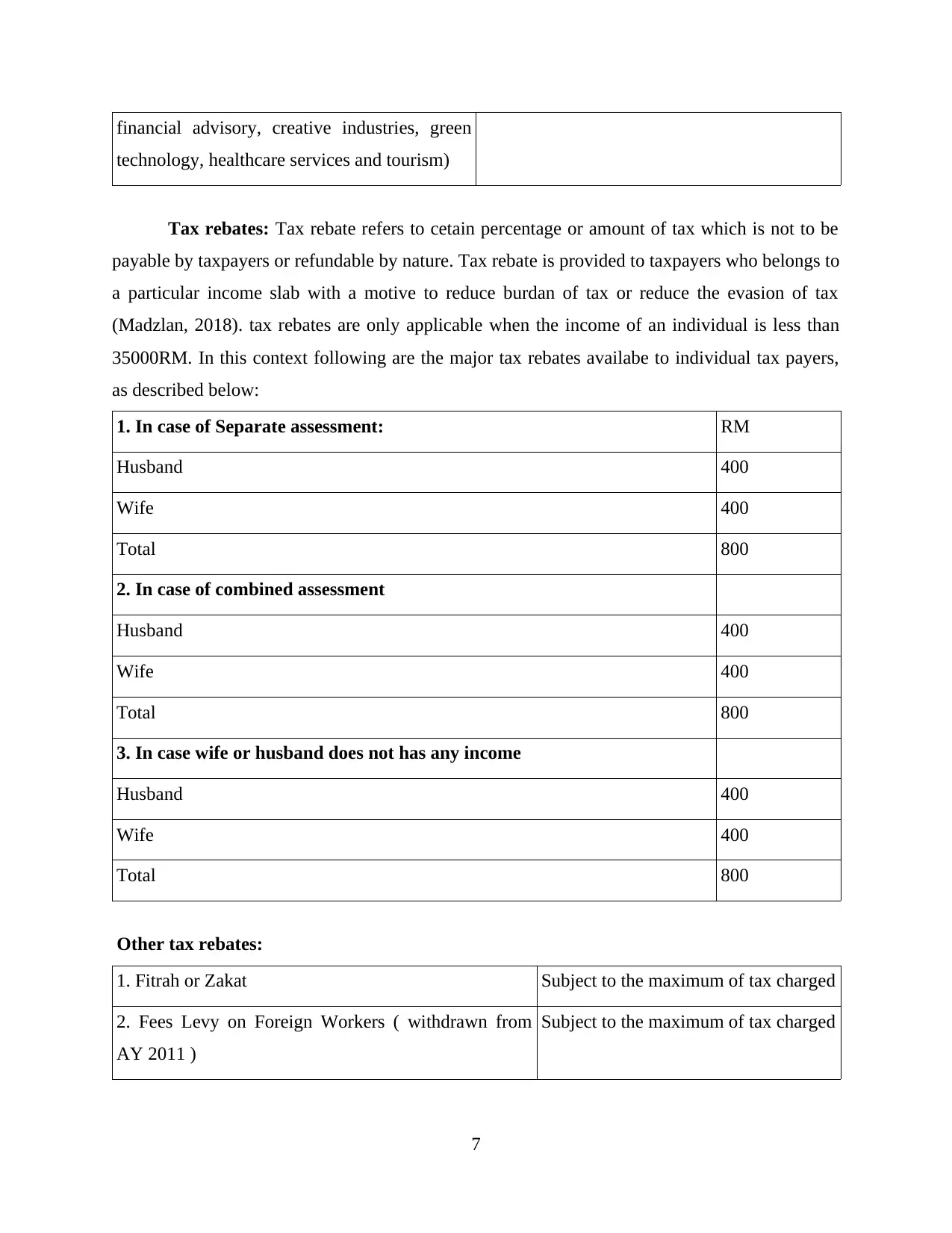

Tax rebates: Tax rebate refers to cetain percentage or amount of tax which is not to be

payable by taxpayers or refundable by nature. Tax rebate is provided to taxpayers who belongs to

a particular income slab with a motive to reduce burdan of tax or reduce the evasion of tax

(Madzlan, 2018). tax rebates are only applicable when the income of an individual is less than

35000RM. In this context following are the major tax rebates availabe to individual tax payers,

as described below:

1. In case of Separate assessment: RM

Husband 400

Wife 400

Total 800

2. In case of combined assessment

Husband 400

Wife 400

Total 800

3. In case wife or husband does not has any income

Husband 400

Wife 400

Total 800

Other tax rebates:

1. Fitrah or Zakat Subject to the maximum of tax charged

2. Fees Levy on Foreign Workers ( withdrawn from

AY 2011 )

Subject to the maximum of tax charged

7

technology, healthcare services and tourism)

Tax rebates: Tax rebate refers to cetain percentage or amount of tax which is not to be

payable by taxpayers or refundable by nature. Tax rebate is provided to taxpayers who belongs to

a particular income slab with a motive to reduce burdan of tax or reduce the evasion of tax

(Madzlan, 2018). tax rebates are only applicable when the income of an individual is less than

35000RM. In this context following are the major tax rebates availabe to individual tax payers,

as described below:

1. In case of Separate assessment: RM

Husband 400

Wife 400

Total 800

2. In case of combined assessment

Husband 400

Wife 400

Total 800

3. In case wife or husband does not has any income

Husband 400

Wife 400

Total 800

Other tax rebates:

1. Fitrah or Zakat Subject to the maximum of tax charged

2. Fees Levy on Foreign Workers ( withdrawn from

AY 2011 )

Subject to the maximum of tax charged

7

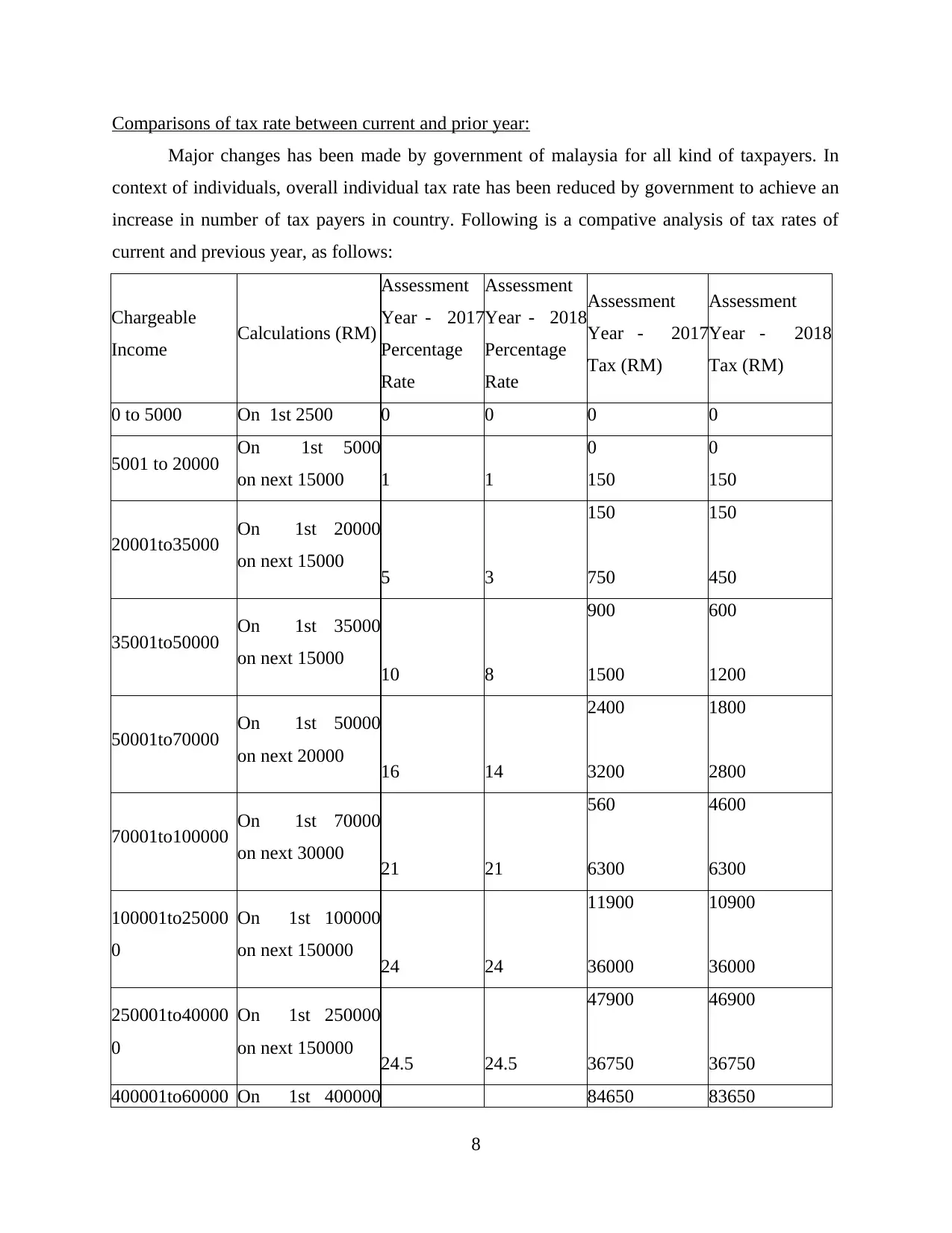

Comparisons of tax rate between current and prior year:

Major changes has been made by government of malaysia for all kind of taxpayers. In

context of individuals, overall individual tax rate has been reduced by government to achieve an

increase in number of tax payers in country. Following is a compative analysis of tax rates of

current and previous year, as follows:

Chargeable

Income Calculations (RM)

Assessment

Year - 2017

Percentage

Rate

Assessment

Year - 2018

Percentage

Rate

Assessment

Year - 2017

Tax (RM)

Assessment

Year - 2018

Tax (RM)

0 to 5000 On 1st 2500 0 0 0 0

5001 to 20000 On 1st 5000

on next 15000 1 1

0

150

0

150

20001to35000 On 1st 20000

on next 15000 5 3

150

750

150

450

35001to50000 On 1st 35000

on next 15000 10 8

900

1500

600

1200

50001to70000 On 1st 50000

on next 20000 16 14

2400

3200

1800

2800

70001to100000 On 1st 70000

on next 30000 21 21

560

6300

4600

6300

100001to25000

0

On 1st 100000

on next 150000 24 24

11900

36000

10900

36000

250001to40000

0

On 1st 250000

on next 150000 24.5 24.5

47900

36750

46900

36750

400001to60000 On 1st 400000 84650 83650

8

Major changes has been made by government of malaysia for all kind of taxpayers. In

context of individuals, overall individual tax rate has been reduced by government to achieve an

increase in number of tax payers in country. Following is a compative analysis of tax rates of

current and previous year, as follows:

Chargeable

Income Calculations (RM)

Assessment

Year - 2017

Percentage

Rate

Assessment

Year - 2018

Percentage

Rate

Assessment

Year - 2017

Tax (RM)

Assessment

Year - 2018

Tax (RM)

0 to 5000 On 1st 2500 0 0 0 0

5001 to 20000 On 1st 5000

on next 15000 1 1

0

150

0

150

20001to35000 On 1st 20000

on next 15000 5 3

150

750

150

450

35001to50000 On 1st 35000

on next 15000 10 8

900

1500

600

1200

50001to70000 On 1st 50000

on next 20000 16 14

2400

3200

1800

2800

70001to100000 On 1st 70000

on next 30000 21 21

560

6300

4600

6300

100001to25000

0

On 1st 100000

on next 150000 24 24

11900

36000

10900

36000

250001to40000

0

On 1st 250000

on next 150000 24.5 24.5

47900

36750

46900

36750

400001to60000 On 1st 400000 84650 83650

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

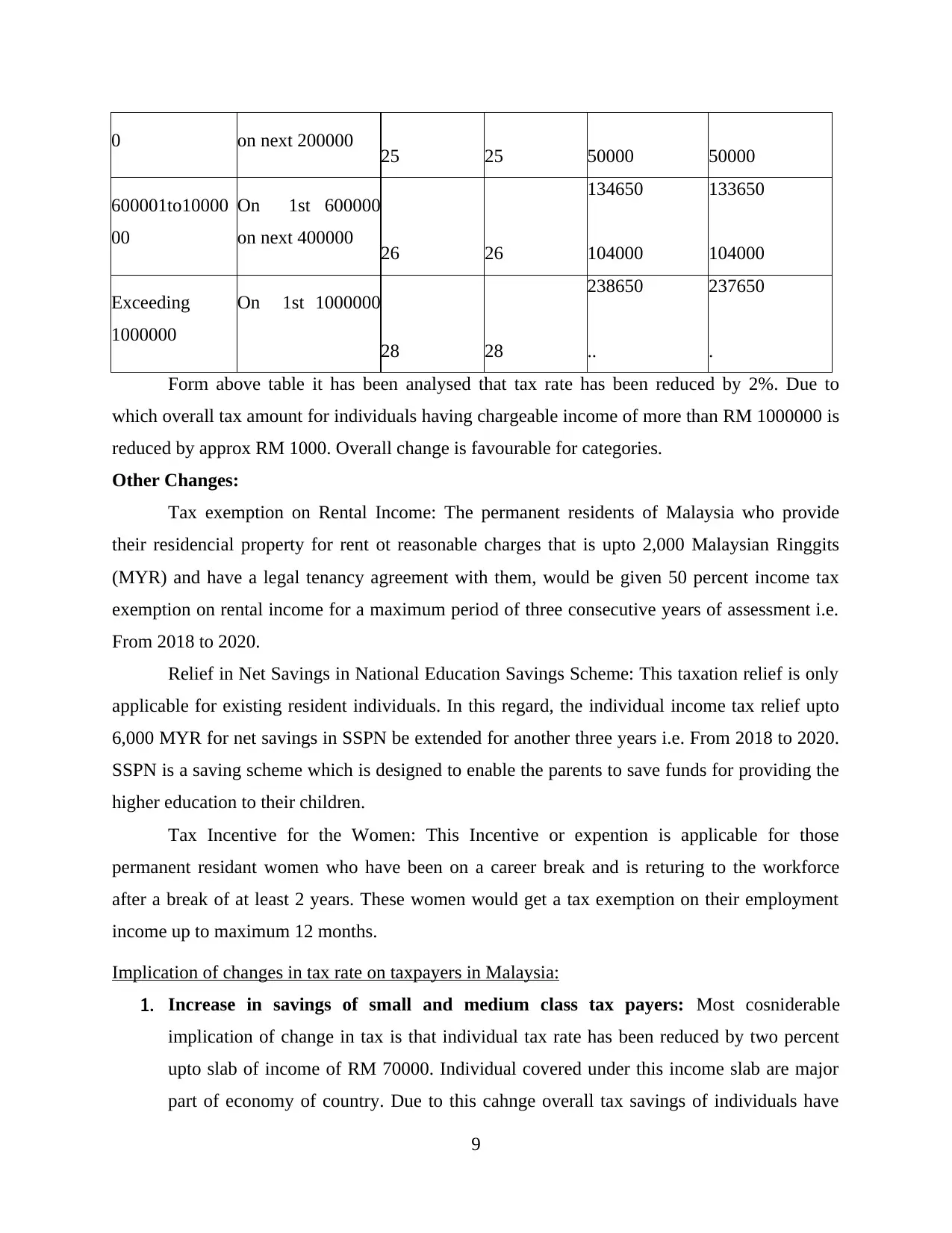

0 on next 200000 25 25 50000 50000

600001to10000

00

On 1st 600000

on next 400000 26 26

134650

104000

133650

104000

Exceeding

1000000

On 1st 1000000

28 28

238650

..

237650

.

Form above table it has been analysed that tax rate has been reduced by 2%. Due to

which overall tax amount for individuals having chargeable income of more than RM 1000000 is

reduced by approx RM 1000. Overall change is favourable for categories.

Other Changes:

Tax exemption on Rental Income: The permanent residents of Malaysia who provide

their residencial property for rent ot reasonable charges that is upto 2,000 Malaysian Ringgits

(MYR) and have a legal tenancy agreement with them, would be given 50 percent income tax

exemption on rental income for a maximum period of three consecutive years of assessment i.e.

From 2018 to 2020.

Relief in Net Savings in National Education Savings Scheme: This taxation relief is only

applicable for existing resident individuals. In this regard, the individual income tax relief upto

6,000 MYR for net savings in SSPN be extended for another three years i.e. From 2018 to 2020.

SSPN is a saving scheme which is designed to enable the parents to save funds for providing the

higher education to their children.

Tax Incentive for the Women: This Incentive or expention is applicable for those

permanent residant women who have been on a career break and is returing to the workforce

after a break of at least 2 years. These women would get a tax exemption on their employment

income up to maximum 12 months.

Implication of changes in tax rate on taxpayers in Malaysia:

1. Increase in savings of small and medium class tax payers: Most cosniderable

implication of change in tax is that individual tax rate has been reduced by two percent

upto slab of income of RM 70000. Individual covered under this income slab are major

part of economy of country. Due to this cahnge overall tax savings of individuals have

9

600001to10000

00

On 1st 600000

on next 400000 26 26

134650

104000

133650

104000

Exceeding

1000000

On 1st 1000000

28 28

238650

..

237650

.

Form above table it has been analysed that tax rate has been reduced by 2%. Due to

which overall tax amount for individuals having chargeable income of more than RM 1000000 is

reduced by approx RM 1000. Overall change is favourable for categories.

Other Changes:

Tax exemption on Rental Income: The permanent residents of Malaysia who provide

their residencial property for rent ot reasonable charges that is upto 2,000 Malaysian Ringgits

(MYR) and have a legal tenancy agreement with them, would be given 50 percent income tax

exemption on rental income for a maximum period of three consecutive years of assessment i.e.

From 2018 to 2020.

Relief in Net Savings in National Education Savings Scheme: This taxation relief is only

applicable for existing resident individuals. In this regard, the individual income tax relief upto

6,000 MYR for net savings in SSPN be extended for another three years i.e. From 2018 to 2020.

SSPN is a saving scheme which is designed to enable the parents to save funds for providing the

higher education to their children.

Tax Incentive for the Women: This Incentive or expention is applicable for those

permanent residant women who have been on a career break and is returing to the workforce

after a break of at least 2 years. These women would get a tax exemption on their employment

income up to maximum 12 months.

Implication of changes in tax rate on taxpayers in Malaysia:

1. Increase in savings of small and medium class tax payers: Most cosniderable

implication of change in tax is that individual tax rate has been reduced by two percent

upto slab of income of RM 70000. Individual covered under this income slab are major

part of economy of country. Due to this cahnge overall tax savings of individuals have

9

been increased (Sandran, P., 2018). Most of the individuals who get benefit of this

change are small and medium taxpayers. In long these change would lead to increase in

ratantion level of home currency. Thich change would be effective in promoting people

for filing return and payment of tax.

2. Increment in women employemnt: A initative step is taken through recent changes is

providing tax incentives to women who are coming back after a career gap (At least two

year). Due to these change women are encouraged to re join thier jobs which ultimately

leads to increase in women employement. Due to this share of women in economic

development has been slighlty increased.

3. Contribution in SSPN increased: In order to increase saving habits and promot

education of childerns government has extended the releif of upto MR 6000 on savings of

SSPN. Due to this contribution in SSPN in encreased over the year. In run it would be

usful in enahncing the education level of country.

4. Stimulation in consumer spending: Government has decreased employee contribution

percentage to EPF from 11 percent to 8 percent. Main motive of this change is to

stimulate spending of consumers. Due to this change in-hand salary income of

individuals has increased which also results in increase in circulation of cash in market.

Overall implication of changes in tax rates and polcies are in favour of taxpayers. From above

discussed implications it is clear that government wants to achieve increase in amount of tax

collection, women empowement, stimulate cosnumer spendings and increase education standards

in country.

CONCLUSION

From above report it has been articulated that tax system of Malaysia is well structured.

Inland Revenue Board of Malaysia (IRBM) is main authority of tax collection in country. It also

regulates the tax collection, compliance and other significant functions. Recent change in tax

rates and policies in Malaysia is favourable for individual tax payers. Main motive of providing

tax reliefs and rebate is to enhance the habit of filing tax and increase the number of taxpayers.

Contribution of individual though tax is essential for development and growth of country. Taxes

collected by taxpayers are used by government for education, infrastructure development, reduce

poverty, increase health standards and other social or economic purposes.

10

change are small and medium taxpayers. In long these change would lead to increase in

ratantion level of home currency. Thich change would be effective in promoting people

for filing return and payment of tax.

2. Increment in women employemnt: A initative step is taken through recent changes is

providing tax incentives to women who are coming back after a career gap (At least two

year). Due to these change women are encouraged to re join thier jobs which ultimately

leads to increase in women employement. Due to this share of women in economic

development has been slighlty increased.

3. Contribution in SSPN increased: In order to increase saving habits and promot

education of childerns government has extended the releif of upto MR 6000 on savings of

SSPN. Due to this contribution in SSPN in encreased over the year. In run it would be

usful in enahncing the education level of country.

4. Stimulation in consumer spending: Government has decreased employee contribution

percentage to EPF from 11 percent to 8 percent. Main motive of this change is to

stimulate spending of consumers. Due to this change in-hand salary income of

individuals has increased which also results in increase in circulation of cash in market.

Overall implication of changes in tax rates and polcies are in favour of taxpayers. From above

discussed implications it is clear that government wants to achieve increase in amount of tax

collection, women empowement, stimulate cosnumer spendings and increase education standards

in country.

CONCLUSION

From above report it has been articulated that tax system of Malaysia is well structured.

Inland Revenue Board of Malaysia (IRBM) is main authority of tax collection in country. It also

regulates the tax collection, compliance and other significant functions. Recent change in tax

rates and policies in Malaysia is favourable for individual tax payers. Main motive of providing

tax reliefs and rebate is to enhance the habit of filing tax and increase the number of taxpayers.

Contribution of individual though tax is essential for development and growth of country. Taxes

collected by taxpayers are used by government for education, infrastructure development, reduce

poverty, increase health standards and other social or economic purposes.

10

REFERENCE

Books and journal:

Desiana, R., 2019. SOURCES OF MALAYSIA’S INCOME AND ITS ALLOCATIONS IN

CONTEXT ISLAM'S PUBLIC FINANCIAL IN NEWEST ERA. Jurnal BAABU AL-

ILMI: Ekonomi dan Perbankan Syariah. 4(1). pp.19-35.

Haron, R. and Ayojimi, S. M., 2018. The impact of GST implementation on the Malaysian stock

market index volatility: An empirical approach. Journal of Asian Business and

Economic Studies.

Kraal, D., 2019. Petroleum industry tax incentives and energy policy implications: A comparison

between Australia, Malaysia, Indonesia and Papua New Guinea. Energy Policy. 126.

pp.212-222.

Leng, Y. K., 2018. Malaysia’s Budget 2019: The New Government’s Fiscal Priorities,

Challenges and Opportunities.

Ling, P. K., 2018. Economics and Environmental Implications of Carbon Taxation in Malaysia:

A Computable General Equilibrium Approach. In Proceedings of Asia Conference on

Business and Economic Studies (ACBES) by University of Economics Ho Chi Minh City

on 8th–9th Sep 2018 at Ho Chi Minh City, Vietnam (pp. 551-564). UEH Publishing

House.

Madzlan, M., 2018. A study on factors influencing the effectiveness of information content in

newspaper advertising in promoting government's new policy: Goods and services tax

(GST).

Sandran, P., 2018. A critical examination of planning issues surrounding the formulation of

public-private partnership toll road projects in Malaysia (Doctoral dissertation,

University of Sheffield).

SETYONINGRUM, D. and PURWANTI, E. Y., 2018. ANALISIS TAX BUOYANCY PADA

ASEAN-5 (INDONESIA, FILIPINA, MALAYSIA, SINGAPURA, DAN THAILAND)

TAHUN 2002-2016 (Doctoral dissertation, Fakultas Ekonomika dan Bisnis).

Wong, K. Y., Chuah, J. H. and Hope, C., 2019. As an emerging economy, should Malaysia adopt

carbon taxation?. Energy & Environment. 30(1). pp.91-108.

Online

Income Tax Rates, 2019. [Online]. Available Through:

<http://www.hasil.gov.my/bt_goindex.php

bt_kump=5&bt_skum=1&bt_posi=2&bt_unit=5000&bt_sequ=11&bt_lgv=2>

11

Books and journal:

Desiana, R., 2019. SOURCES OF MALAYSIA’S INCOME AND ITS ALLOCATIONS IN

CONTEXT ISLAM'S PUBLIC FINANCIAL IN NEWEST ERA. Jurnal BAABU AL-

ILMI: Ekonomi dan Perbankan Syariah. 4(1). pp.19-35.

Haron, R. and Ayojimi, S. M., 2018. The impact of GST implementation on the Malaysian stock

market index volatility: An empirical approach. Journal of Asian Business and

Economic Studies.

Kraal, D., 2019. Petroleum industry tax incentives and energy policy implications: A comparison

between Australia, Malaysia, Indonesia and Papua New Guinea. Energy Policy. 126.

pp.212-222.

Leng, Y. K., 2018. Malaysia’s Budget 2019: The New Government’s Fiscal Priorities,

Challenges and Opportunities.

Ling, P. K., 2018. Economics and Environmental Implications of Carbon Taxation in Malaysia:

A Computable General Equilibrium Approach. In Proceedings of Asia Conference on

Business and Economic Studies (ACBES) by University of Economics Ho Chi Minh City

on 8th–9th Sep 2018 at Ho Chi Minh City, Vietnam (pp. 551-564). UEH Publishing

House.

Madzlan, M., 2018. A study on factors influencing the effectiveness of information content in

newspaper advertising in promoting government's new policy: Goods and services tax

(GST).

Sandran, P., 2018. A critical examination of planning issues surrounding the formulation of

public-private partnership toll road projects in Malaysia (Doctoral dissertation,

University of Sheffield).

SETYONINGRUM, D. and PURWANTI, E. Y., 2018. ANALISIS TAX BUOYANCY PADA

ASEAN-5 (INDONESIA, FILIPINA, MALAYSIA, SINGAPURA, DAN THAILAND)

TAHUN 2002-2016 (Doctoral dissertation, Fakultas Ekonomika dan Bisnis).

Wong, K. Y., Chuah, J. H. and Hope, C., 2019. As an emerging economy, should Malaysia adopt

carbon taxation?. Energy & Environment. 30(1). pp.91-108.

Online

Income Tax Rates, 2019. [Online]. Available Through:

<http://www.hasil.gov.my/bt_goindex.php

bt_kump=5&bt_skum=1&bt_posi=2&bt_unit=5000&bt_sequ=11&bt_lgv=2>

11

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.