HI6028 Taxation Assignment: Case Studies of FBT and Capital Gains Tax

VerifiedAdded on 2023/01/07

|8

|2435

|41

Homework Assignment

AI Summary

This document presents a comprehensive solution to a taxation assignment, specifically addressing Fringe Benefits Tax (FBT) and Capital Gains Tax (CGT). The assignment includes two primary questions: the first delves into calculating the fringe tax liability for a company providing a car to an employee, considering both work-related travel and personal use, and applying relevant tax rates and calculations based on the provided data. The second question analyzes capital gains tax implications for various scenarios, including the sale of an antique painting, a car, a Harry Potter collection, a gold necklace, and a sculpture. The solution provides detailed explanations, references relevant tax legislation (FBTAA 1986, ITAA 1997), and applies ATO guidelines to determine the taxability and exemptions for each asset sale, including calculations of taxable amounts where applicable.

Taxation Theory, Practice &

Law

Law

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

QUESTION 1...................................................................................................................................3

QUESTION 2...................................................................................................................................5

REFERENCES................................................................................................................................8

QUESTION 1...................................................................................................................................3

QUESTION 2...................................................................................................................................5

REFERENCES................................................................................................................................8

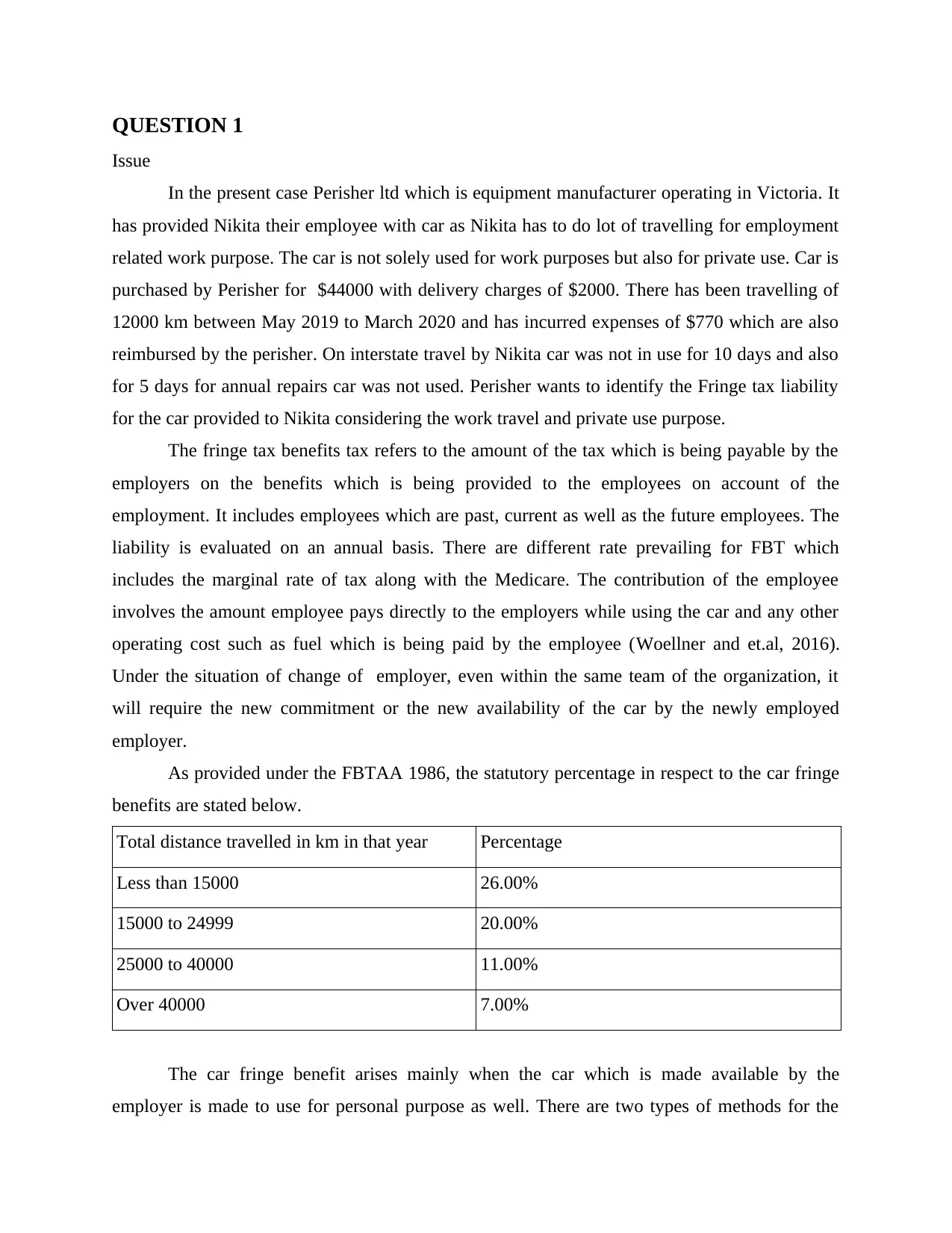

QUESTION 1

Issue

In the present case Perisher ltd which is equipment manufacturer operating in Victoria. It

has provided Nikita their employee with car as Nikita has to do lot of travelling for employment

related work purpose. The car is not solely used for work purposes but also for private use. Car is

purchased by Perisher for $44000 with delivery charges of $2000. There has been travelling of

12000 km between May 2019 to March 2020 and has incurred expenses of $770 which are also

reimbursed by the perisher. On interstate travel by Nikita car was not in use for 10 days and also

for 5 days for annual repairs car was not used. Perisher wants to identify the Fringe tax liability

for the car provided to Nikita considering the work travel and private use purpose.

The fringe tax benefits tax refers to the amount of the tax which is being payable by the

employers on the benefits which is being provided to the employees on account of the

employment. It includes employees which are past, current as well as the future employees. The

liability is evaluated on an annual basis. There are different rate prevailing for FBT which

includes the marginal rate of tax along with the Medicare. The contribution of the employee

involves the amount employee pays directly to the employers while using the car and any other

operating cost such as fuel which is being paid by the employee (Woellner and et.al, 2016).

Under the situation of change of employer, even within the same team of the organization, it

will require the new commitment or the new availability of the car by the newly employed

employer.

As provided under the FBTAA 1986, the statutory percentage in respect to the car fringe

benefits are stated below.

Total distance travelled in km in that year Percentage

Less than 15000 26.00%

15000 to 24999 20.00%

25000 to 40000 11.00%

Over 40000 7.00%

The car fringe benefit arises mainly when the car which is made available by the

employer is made to use for personal purpose as well. There are two types of methods for the

Issue

In the present case Perisher ltd which is equipment manufacturer operating in Victoria. It

has provided Nikita their employee with car as Nikita has to do lot of travelling for employment

related work purpose. The car is not solely used for work purposes but also for private use. Car is

purchased by Perisher for $44000 with delivery charges of $2000. There has been travelling of

12000 km between May 2019 to March 2020 and has incurred expenses of $770 which are also

reimbursed by the perisher. On interstate travel by Nikita car was not in use for 10 days and also

for 5 days for annual repairs car was not used. Perisher wants to identify the Fringe tax liability

for the car provided to Nikita considering the work travel and private use purpose.

The fringe tax benefits tax refers to the amount of the tax which is being payable by the

employers on the benefits which is being provided to the employees on account of the

employment. It includes employees which are past, current as well as the future employees. The

liability is evaluated on an annual basis. There are different rate prevailing for FBT which

includes the marginal rate of tax along with the Medicare. The contribution of the employee

involves the amount employee pays directly to the employers while using the car and any other

operating cost such as fuel which is being paid by the employee (Woellner and et.al, 2016).

Under the situation of change of employer, even within the same team of the organization, it

will require the new commitment or the new availability of the car by the newly employed

employer.

As provided under the FBTAA 1986, the statutory percentage in respect to the car fringe

benefits are stated below.

Total distance travelled in km in that year Percentage

Less than 15000 26.00%

15000 to 24999 20.00%

25000 to 40000 11.00%

Over 40000 7.00%

The car fringe benefit arises mainly when the car which is made available by the

employer is made to use for personal purpose as well. There are two types of methods for the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

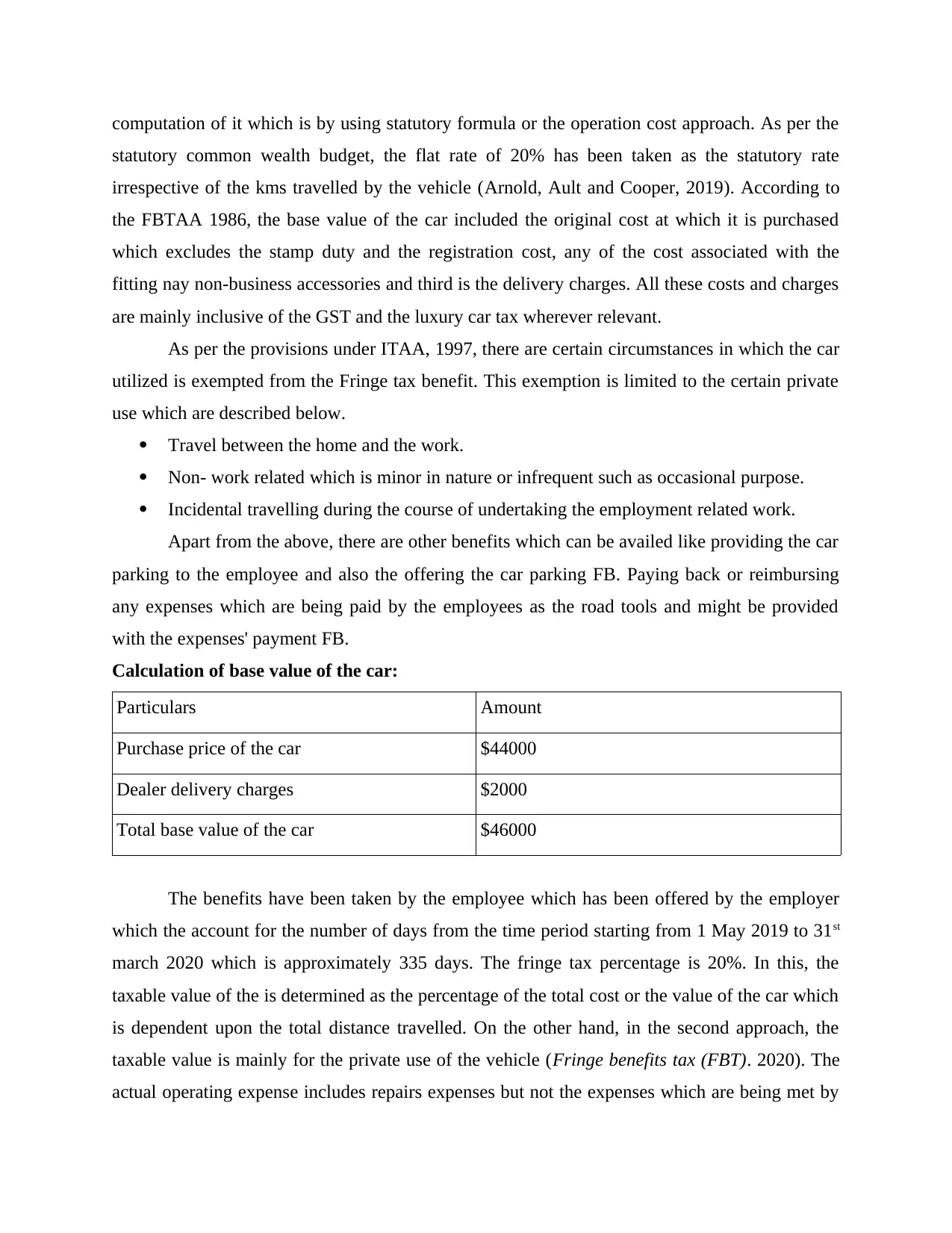

computation of it which is by using statutory formula or the operation cost approach. As per the

statutory common wealth budget, the flat rate of 20% has been taken as the statutory rate

irrespective of the kms travelled by the vehicle (Arnold, Ault and Cooper, 2019). According to

the FBTAA 1986, the base value of the car included the original cost at which it is purchased

which excludes the stamp duty and the registration cost, any of the cost associated with the

fitting nay non-business accessories and third is the delivery charges. All these costs and charges

are mainly inclusive of the GST and the luxury car tax wherever relevant.

As per the provisions under ITAA, 1997, there are certain circumstances in which the car

utilized is exempted from the Fringe tax benefit. This exemption is limited to the certain private

use which are described below.

Travel between the home and the work.

Non- work related which is minor in nature or infrequent such as occasional purpose.

Incidental travelling during the course of undertaking the employment related work.

Apart from the above, there are other benefits which can be availed like providing the car

parking to the employee and also the offering the car parking FB. Paying back or reimbursing

any expenses which are being paid by the employees as the road tools and might be provided

with the expenses' payment FB.

Calculation of base value of the car:

Particulars Amount

Purchase price of the car $44000

Dealer delivery charges $2000

Total base value of the car $46000

The benefits have been taken by the employee which has been offered by the employer

which the account for the number of days from the time period starting from 1 May 2019 to 31st

march 2020 which is approximately 335 days. The fringe tax percentage is 20%. In this, the

taxable value of the is determined as the percentage of the total cost or the value of the car which

is dependent upon the total distance travelled. On the other hand, in the second approach, the

taxable value is mainly for the private use of the vehicle (Fringe benefits tax (FBT). 2020). The

actual operating expense includes repairs expenses but not the expenses which are being met by

statutory common wealth budget, the flat rate of 20% has been taken as the statutory rate

irrespective of the kms travelled by the vehicle (Arnold, Ault and Cooper, 2019). According to

the FBTAA 1986, the base value of the car included the original cost at which it is purchased

which excludes the stamp duty and the registration cost, any of the cost associated with the

fitting nay non-business accessories and third is the delivery charges. All these costs and charges

are mainly inclusive of the GST and the luxury car tax wherever relevant.

As per the provisions under ITAA, 1997, there are certain circumstances in which the car

utilized is exempted from the Fringe tax benefit. This exemption is limited to the certain private

use which are described below.

Travel between the home and the work.

Non- work related which is minor in nature or infrequent such as occasional purpose.

Incidental travelling during the course of undertaking the employment related work.

Apart from the above, there are other benefits which can be availed like providing the car

parking to the employee and also the offering the car parking FB. Paying back or reimbursing

any expenses which are being paid by the employees as the road tools and might be provided

with the expenses' payment FB.

Calculation of base value of the car:

Particulars Amount

Purchase price of the car $44000

Dealer delivery charges $2000

Total base value of the car $46000

The benefits have been taken by the employee which has been offered by the employer

which the account for the number of days from the time period starting from 1 May 2019 to 31st

march 2020 which is approximately 335 days. The fringe tax percentage is 20%. In this, the

taxable value of the is determined as the percentage of the total cost or the value of the car which

is dependent upon the total distance travelled. On the other hand, in the second approach, the

taxable value is mainly for the private use of the vehicle (Fringe benefits tax (FBT). 2020). The

actual operating expense includes repairs expenses but not the expenses which are being met by

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

insurance company, maintenance, fuel, registration and the insurance charges which is being

paid to offer fringe benefit and the leasing cost in case the car is on lease instead of being

purchased. It also includes any of the operating cost which is being paid by someone else. It has

been given in the case that the car has not only been used for the work purpose and the as on 1

May 2019, it has been purchased with an additional amount of delivery charges. Also, the

distance travelled is 12000 kms and Nikita has incurred expenses amounting to $770 in regard to

repairs.

Computation of fringe benefits taxable amount for Perisher

Taxable amount = tax rate * base value of the car * number of days of benefits / 365 days –

expenses incurred

= 20% * 46000 * 335/365 – 770

= 9200 * 0.918 – 770

= $7674

It could be evaluated that Perisher would be required to pay $7674 for fringe benefits

provided to the Nikita of car for both work related travel and personal use. When the value of

fringe benefits exceeds the threshold limit Nikita will be also required to pay tax in the annual

tax return for the benefits provided by the company.

QUESTION 2

Capital gain or the loss is difference between the amount paid for acquisition of asset and

the proceeds on sale of assets. When the assets are sold at price higher than at which they were

purchased it will be resulting in capital gain. Similarly if the sale proceeds are less than cost of

acquisition than it is capital loss (Burkhauser and Wilkins, 2016). When any capital asset is

disposed at gain capital gain tax is applicable except for the specific exemptions provided under

ITAA, 1997. There are two methods by which capital gain tax could be calculated which are

discounted method and one is indexation method. Capital gain tax is charged under ITAA 1997

and as per guidance provided by ATO. Capital gains and loss have to be reported in the income

tax return and has to pay CGT over gains. Though it is named differently as CGT but is part of

the income tax only and is not paid separately.

1. Antique painting sale

Taryn has sold a antique painting which was purchased by the father in August 1984 at

$2500. When any capital asset is sold which was gifted to the tax payer date of acquisition will

paid to offer fringe benefit and the leasing cost in case the car is on lease instead of being

purchased. It also includes any of the operating cost which is being paid by someone else. It has

been given in the case that the car has not only been used for the work purpose and the as on 1

May 2019, it has been purchased with an additional amount of delivery charges. Also, the

distance travelled is 12000 kms and Nikita has incurred expenses amounting to $770 in regard to

repairs.

Computation of fringe benefits taxable amount for Perisher

Taxable amount = tax rate * base value of the car * number of days of benefits / 365 days –

expenses incurred

= 20% * 46000 * 335/365 – 770

= 9200 * 0.918 – 770

= $7674

It could be evaluated that Perisher would be required to pay $7674 for fringe benefits

provided to the Nikita of car for both work related travel and personal use. When the value of

fringe benefits exceeds the threshold limit Nikita will be also required to pay tax in the annual

tax return for the benefits provided by the company.

QUESTION 2

Capital gain or the loss is difference between the amount paid for acquisition of asset and

the proceeds on sale of assets. When the assets are sold at price higher than at which they were

purchased it will be resulting in capital gain. Similarly if the sale proceeds are less than cost of

acquisition than it is capital loss (Burkhauser and Wilkins, 2016). When any capital asset is

disposed at gain capital gain tax is applicable except for the specific exemptions provided under

ITAA, 1997. There are two methods by which capital gain tax could be calculated which are

discounted method and one is indexation method. Capital gain tax is charged under ITAA 1997

and as per guidance provided by ATO. Capital gains and loss have to be reported in the income

tax return and has to pay CGT over gains. Though it is named differently as CGT but is part of

the income tax only and is not paid separately.

1. Antique painting sale

Taryn has sold a antique painting which was purchased by the father in August 1984 at

$2500. When any capital asset is sold which was gifted to the tax payer date of acquisition will

be taken as the date at which former purchased it. The painting is sold for $25000 which is

higher than the acquisition price. There has been capital gain of $22500 on the sale of acquisition

painting (Kennedy, T., and et.al., 2017). According to section 108 of ITAA, 1997 the capital gain

of $22500 is taxable for Taryn However, as per ATO guidance the capital gain tax is applicable

only over assets that have been purchased after September 20, 1985. As per the provisions of tax

law, capital gain tax is not applicable to capital gain over sale of antique painting as it was

acquired by father of Taryn before September 1985 though it was transferred to Taryn 5 years

ago. The gains over sale of antique painting by the Taryn is fully exempt and is not required to

be reported in the annual income tax return.

2. Car sale

The capital gain tax is applicable over all the assets which are sold by the assessor at

gains. However as per the ATO guidance some of the assets are exempt from capital gain tax. In

the exemption list provided by the ATO gains over sale of personal car is exempt from capital

gain. As per section 118.5 of ITAA, 1997 capital gain or over capital loss from the Motor cycles,

cars and valour decoration are disregarded for capital gain tax (Australia and Au, 2020).

Therefore as per the provisions of this Act and ATO guidance capital loss incurred by Taryn over

sale of the car is disregarded for the capital assets. The loss incurred over sale of car could not be

used by the Taryn over other taxable capital gains occurred during the year. The loss could not

be carry forwarded to next year. Therefore the capital loss incurred over car is disregarded and

will not be used for reducing capital gain tax liability.

3. Harry potter collection sale

As per the guidelines of ATO, all the assets which has been acquired since 20th

September 1985 are all subjected to the CGT. There are certain exemptions to capital assets.

Which includes the main residence, motorcycle or car. It also involves any of the depreciating

assets which is mainly utilized for the taxable purpose like organizations equipments or any sort

of fittings in the property rented or any of the property which has been purchased before the

above stated date (Aquilina, 2019). Apart from this, there are certain items which are exempted

from the capital gain or loss which includes any type of collectibles which has been acquired by

the individual for less than or equal to $500. Therefore, the capital gain incurred on selling of

Harry Porter's collection by Taryn is completely exempted and there is no requirement of it being

reported.

higher than the acquisition price. There has been capital gain of $22500 on the sale of acquisition

painting (Kennedy, T., and et.al., 2017). According to section 108 of ITAA, 1997 the capital gain

of $22500 is taxable for Taryn However, as per ATO guidance the capital gain tax is applicable

only over assets that have been purchased after September 20, 1985. As per the provisions of tax

law, capital gain tax is not applicable to capital gain over sale of antique painting as it was

acquired by father of Taryn before September 1985 though it was transferred to Taryn 5 years

ago. The gains over sale of antique painting by the Taryn is fully exempt and is not required to

be reported in the annual income tax return.

2. Car sale

The capital gain tax is applicable over all the assets which are sold by the assessor at

gains. However as per the ATO guidance some of the assets are exempt from capital gain tax. In

the exemption list provided by the ATO gains over sale of personal car is exempt from capital

gain. As per section 118.5 of ITAA, 1997 capital gain or over capital loss from the Motor cycles,

cars and valour decoration are disregarded for capital gain tax (Australia and Au, 2020).

Therefore as per the provisions of this Act and ATO guidance capital loss incurred by Taryn over

sale of the car is disregarded for the capital assets. The loss incurred over sale of car could not be

used by the Taryn over other taxable capital gains occurred during the year. The loss could not

be carry forwarded to next year. Therefore the capital loss incurred over car is disregarded and

will not be used for reducing capital gain tax liability.

3. Harry potter collection sale

As per the guidelines of ATO, all the assets which has been acquired since 20th

September 1985 are all subjected to the CGT. There are certain exemptions to capital assets.

Which includes the main residence, motorcycle or car. It also involves any of the depreciating

assets which is mainly utilized for the taxable purpose like organizations equipments or any sort

of fittings in the property rented or any of the property which has been purchased before the

above stated date (Aquilina, 2019). Apart from this, there are certain items which are exempted

from the capital gain or loss which includes any type of collectibles which has been acquired by

the individual for less than or equal to $500. Therefore, the capital gain incurred on selling of

Harry Porter's collection by Taryn is completely exempted and there is no requirement of it being

reported.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4. Gold necklace sale

The gold necklace is included in the collectibles which is included in the capital gain tax

assets up to certain value. The collectible included items which is being utilized for the personal

use or for the purpose of fun or enjoyment. It will be disregarded only if it is purchased for less

than or equal to $500 before 16th December 1995 (Blakelock and King, 2017). If the asset is

disposed off as asset then the individual is exempted from paying CGT only if it satisfies the

condition of acquiring the asset on or before 16 December 1995. The capital losses can be used

to minimize the capital gain in the same year and the loss can be carried forward next year as

well. In the given case, Taryn has acquired the jewellery at $1200 which is more than the $500,

thus, it does not fall into the category of exempted capital gain or losses. Therefore, the asset will

be chargeable to tax.

5. Sculpture sale

The capital gain arises only when the individual enters into a contract of buying and

selling a particular item. When the cost of buying it exceeds the disposable value then it incurs

the capital loss and in the opposite situation where the disposable value is more than buying cost,

then it results into capital gain. The collectables include the paintings, all types of sculptures,

photographs, any property of similar type, jewellery, antiques, rare folios, postage stamps and so

forth (Capital gains tax. 2020). But there are also certain exemptions which are being their on

certain collectable items. First is item has been purchased for less or equal to $500, or the same

has been purchased before 16 December 1995 at $500 or less. In the given scenario, it can be

seen that the Taryn has bought the item on December 1994 which is before the 16 December

1995 and is assumed to have been acquired at $500 or less. Therefore, the capital gain arising

over the sell of the sculpture is exempted from capital gain tax and is also not required to report

it in its ITR.

The gold necklace is included in the collectibles which is included in the capital gain tax

assets up to certain value. The collectible included items which is being utilized for the personal

use or for the purpose of fun or enjoyment. It will be disregarded only if it is purchased for less

than or equal to $500 before 16th December 1995 (Blakelock and King, 2017). If the asset is

disposed off as asset then the individual is exempted from paying CGT only if it satisfies the

condition of acquiring the asset on or before 16 December 1995. The capital losses can be used

to minimize the capital gain in the same year and the loss can be carried forward next year as

well. In the given case, Taryn has acquired the jewellery at $1200 which is more than the $500,

thus, it does not fall into the category of exempted capital gain or losses. Therefore, the asset will

be chargeable to tax.

5. Sculpture sale

The capital gain arises only when the individual enters into a contract of buying and

selling a particular item. When the cost of buying it exceeds the disposable value then it incurs

the capital loss and in the opposite situation where the disposable value is more than buying cost,

then it results into capital gain. The collectables include the paintings, all types of sculptures,

photographs, any property of similar type, jewellery, antiques, rare folios, postage stamps and so

forth (Capital gains tax. 2020). But there are also certain exemptions which are being their on

certain collectable items. First is item has been purchased for less or equal to $500, or the same

has been purchased before 16 December 1995 at $500 or less. In the given scenario, it can be

seen that the Taryn has bought the item on December 1994 which is before the 16 December

1995 and is assumed to have been acquired at $500 or less. Therefore, the capital gain arising

over the sell of the sculpture is exempted from capital gain tax and is also not required to report

it in its ITR.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Aquilina, J., 2019, November. Reforming and realigning Division 855 of the Income Tax

Assessment Act 1997 to give better effect to its policy objectives. In Australian Tax

Forum (Vol. 34, No. 1).

Arnold, B. J., Ault, H. J. and Cooper, G. eds., 2019. Comparative income taxation: a structural

analysis. Kluwer Law International BV.

Australia, D. P. and Au, J., 2020. The Australian Taxation Office makes a proactive start to

2020. International Tax Review.

Blakelock, S. and King, P., 2017. Taxation law: The advance of ATO data matching. Proctor,

The,. 37(6). p.18.

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2016. Top incomes and inequality in Australia:

reconciling recent estimates from household survey and tax return data.

Kennedy, T., and et.al., 2017. Does income inequality hinder economic growth? New evidence

using Australian taxation statistics. Economic Modelling. 65. pp.119-128.

Woellner, R. and et.al, 2016. Australian Taxation Law 2016. OUP Catalogue.

Online

Capital gains tax. 2020. [Online]. Available Through:<https://www.ato.gov.au/General/Capital-

gains-tax/CGT-assets-and-exemptions/#Personal_use_assets>.

Fringe benefits tax (FBT). 2020. [Online]. Available

Through:<https://www.ato.gov.au/law/view/document?DocID=SAV/FBTGEMP/

00008&PiT=99991231235958/>.

Books and Journals

Aquilina, J., 2019, November. Reforming and realigning Division 855 of the Income Tax

Assessment Act 1997 to give better effect to its policy objectives. In Australian Tax

Forum (Vol. 34, No. 1).

Arnold, B. J., Ault, H. J. and Cooper, G. eds., 2019. Comparative income taxation: a structural

analysis. Kluwer Law International BV.

Australia, D. P. and Au, J., 2020. The Australian Taxation Office makes a proactive start to

2020. International Tax Review.

Blakelock, S. and King, P., 2017. Taxation law: The advance of ATO data matching. Proctor,

The,. 37(6). p.18.

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2016. Top incomes and inequality in Australia:

reconciling recent estimates from household survey and tax return data.

Kennedy, T., and et.al., 2017. Does income inequality hinder economic growth? New evidence

using Australian taxation statistics. Economic Modelling. 65. pp.119-128.

Woellner, R. and et.al, 2016. Australian Taxation Law 2016. OUP Catalogue.

Online

Capital gains tax. 2020. [Online]. Available Through:<https://www.ato.gov.au/General/Capital-

gains-tax/CGT-assets-and-exemptions/#Personal_use_assets>.

Fringe benefits tax (FBT). 2020. [Online]. Available

Through:<https://www.ato.gov.au/law/view/document?DocID=SAV/FBTGEMP/

00008&PiT=99991231235958/>.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.