Taxable Income from Timber Removal

VerifiedAdded on 2020/03/04

|8

|2333

|57

AI Summary

This assignment delves into the tax implications of removing timber from land. It examines how payments received for timber rights or removal constitute assessable income under Australian tax law (specifically section 6). The example scenario involves Bill, who receives payment from a company to remove timber from his land. The analysis clarifies whether this income is considered ordinary business activity or subject to capital gains tax, emphasizing the importance of legal provisions in determining taxable income.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

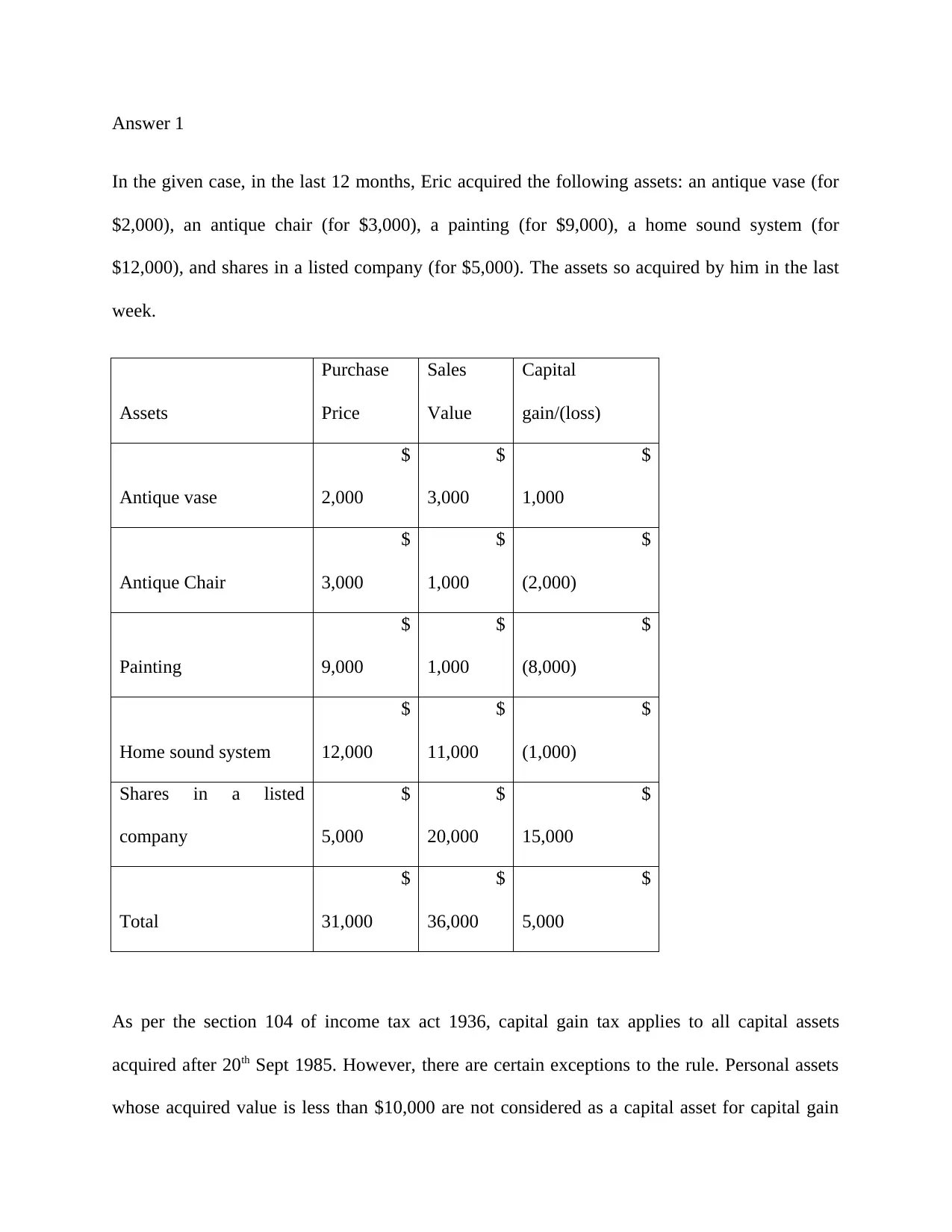

Answer 1

In the given case, in the last 12 months, Eric acquired the following assets: an antique vase (for

$2,000), an antique chair (for $3,000), a painting (for $9,000), a home sound system (for

$12,000), and shares in a listed company (for $5,000). The assets so acquired by him in the last

week.

Assets

Purchase

Price

Sales

Value

Capital

gain/(loss)

Antique vase

$

2,000

$

3,000

$

1,000

Antique Chair

$

3,000

$

1,000

$

(2,000)

Painting

$

9,000

$

1,000

$

(8,000)

Home sound system

$

12,000

$

11,000

$

(1,000)

Shares in a listed

company

$

5,000

$

20,000

$

15,000

Total

$

31,000

$

36,000

$

5,000

As per the section 104 of income tax act 1936, capital gain tax applies to all capital assets

acquired after 20th Sept 1985. However, there are certain exceptions to the rule. Personal assets

whose acquired value is less than $10,000 are not considered as a capital asset for capital gain

In the given case, in the last 12 months, Eric acquired the following assets: an antique vase (for

$2,000), an antique chair (for $3,000), a painting (for $9,000), a home sound system (for

$12,000), and shares in a listed company (for $5,000). The assets so acquired by him in the last

week.

Assets

Purchase

Price

Sales

Value

Capital

gain/(loss)

Antique vase

$

2,000

$

3,000

$

1,000

Antique Chair

$

3,000

$

1,000

$

(2,000)

Painting

$

9,000

$

1,000

$

(8,000)

Home sound system

$

12,000

$

11,000

$

(1,000)

Shares in a listed

company

$

5,000

$

20,000

$

15,000

Total

$

31,000

$

36,000

$

5,000

As per the section 104 of income tax act 1936, capital gain tax applies to all capital assets

acquired after 20th Sept 1985. However, there are certain exceptions to the rule. Personal assets

whose acquired value is less than $10,000 are not considered as a capital asset for capital gain

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

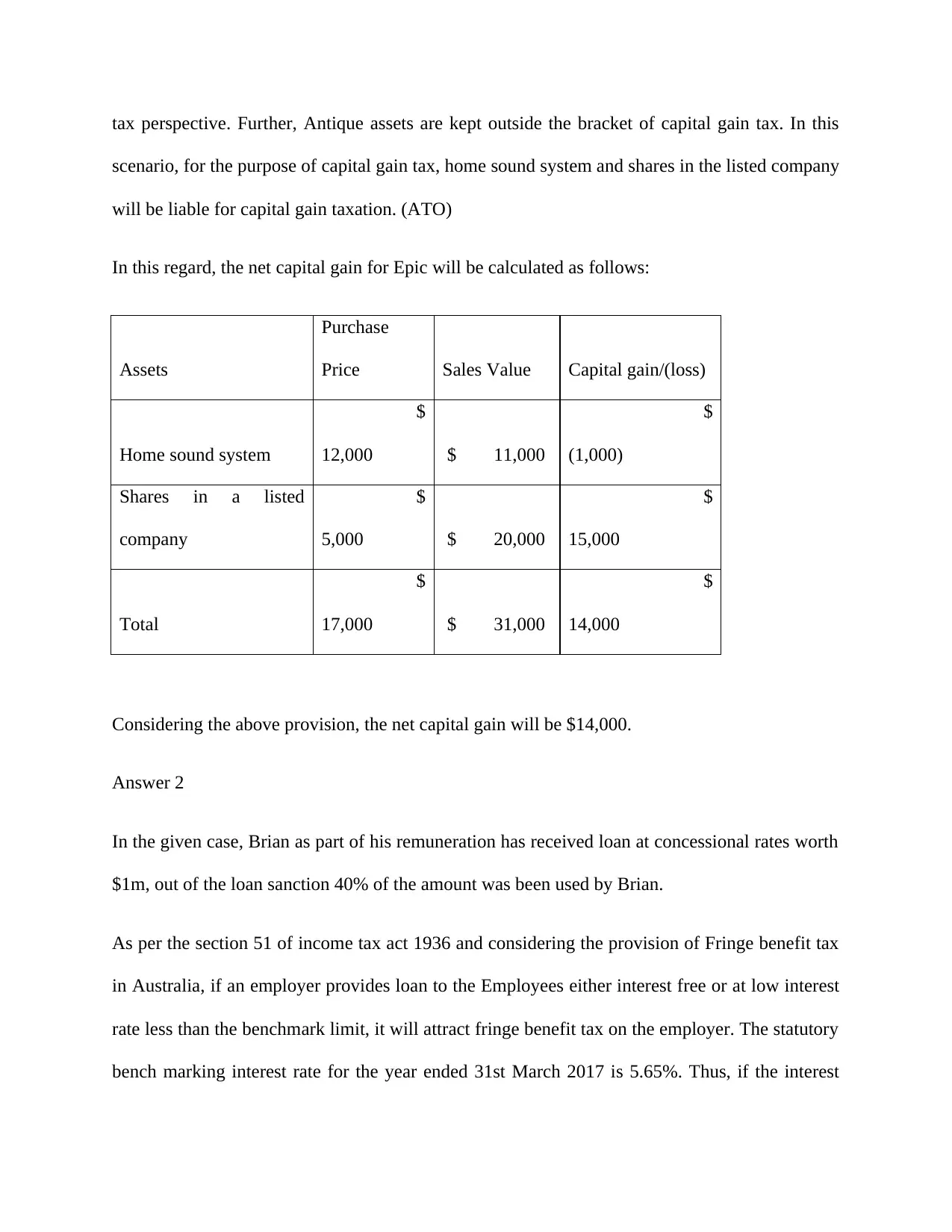

tax perspective. Further, Antique assets are kept outside the bracket of capital gain tax. In this

scenario, for the purpose of capital gain tax, home sound system and shares in the listed company

will be liable for capital gain taxation. (ATO)

In this regard, the net capital gain for Epic will be calculated as follows:

Assets

Purchase

Price Sales Value Capital gain/(loss)

Home sound system

$

12,000 $ 11,000

$

(1,000)

Shares in a listed

company

$

5,000 $ 20,000

$

15,000

Total

$

17,000 $ 31,000

$

14,000

Considering the above provision, the net capital gain will be $14,000.

Answer 2

In the given case, Brian as part of his remuneration has received loan at concessional rates worth

$1m, out of the loan sanction 40% of the amount was been used by Brian.

As per the section 51 of income tax act 1936 and considering the provision of Fringe benefit tax

in Australia, if an employer provides loan to the Employees either interest free or at low interest

rate less than the benchmark limit, it will attract fringe benefit tax on the employer. The statutory

bench marking interest rate for the year ended 31st March 2017 is 5.65%. Thus, if the interest

scenario, for the purpose of capital gain tax, home sound system and shares in the listed company

will be liable for capital gain taxation. (ATO)

In this regard, the net capital gain for Epic will be calculated as follows:

Assets

Purchase

Price Sales Value Capital gain/(loss)

Home sound system

$

12,000 $ 11,000

$

(1,000)

Shares in a listed

company

$

5,000 $ 20,000

$

15,000

Total

$

17,000 $ 31,000

$

14,000

Considering the above provision, the net capital gain will be $14,000.

Answer 2

In the given case, Brian as part of his remuneration has received loan at concessional rates worth

$1m, out of the loan sanction 40% of the amount was been used by Brian.

As per the section 51 of income tax act 1936 and considering the provision of Fringe benefit tax

in Australia, if an employer provides loan to the Employees either interest free or at low interest

rate less than the benchmark limit, it will attract fringe benefit tax on the employer. The statutory

bench marking interest rate for the year ended 31st March 2017 is 5.65%. Thus, if the interest

rate is less than the benchmarking rate, the differential amount will be treated as fringe benefit

and will be taxable in the hands of the employer.

The cumulative interest the employee will be paying in the year ending 31st March 2017 at an

interest rate of 1% per annum will be $3,396. On the other hand, if the employee would have

paid interest at the benchmark rate of 5.65% per annum, the interest rate that would be paid will

be 19,373. In this scenario, the employer is liable to pay fringe benefit tax on the extra benefit

that is provided to the employee in terms of interest rate differential worth $15,977. The fringe

benefit tax rate for the year ended 31st March 2017 is 49%. Thus, the fringe benefit tax that will

be paid by the employer in the given circumstances will be $7,829.

If the employer would have released Brian from paying any interest rate on the loan amount that

has be utilized by him, the entire amount of interest calculated using the benchmarking rate, will

be treated as fringe benefit from the perspective of the employee and will be taxable in the hands

of the employee at the rate of 49%. In the circumstances, $19,373 will be treated as the fringe

benefit value and the fringe benefit tax would be $9,493. If the interest amount would have been

paid at the end of the loan period rather than paying in monthly installment, there would be no

change in the fringe benefit value for the employer.

If the employer would have released Brian from paying any interest rate on the loan amount that

has be utilized by him, the entire amount of interest calculated using the benchmarking rate, will

be treated as fringe benefit from the perspective of the employee and will be taxable in the hands

of the employee at the rate of 49%. In the circumstances, $19,373 will be treated as the fringe

benefit value and the fringe benefit tax would be $9,493.

Answer 3

and will be taxable in the hands of the employer.

The cumulative interest the employee will be paying in the year ending 31st March 2017 at an

interest rate of 1% per annum will be $3,396. On the other hand, if the employee would have

paid interest at the benchmark rate of 5.65% per annum, the interest rate that would be paid will

be 19,373. In this scenario, the employer is liable to pay fringe benefit tax on the extra benefit

that is provided to the employee in terms of interest rate differential worth $15,977. The fringe

benefit tax rate for the year ended 31st March 2017 is 49%. Thus, the fringe benefit tax that will

be paid by the employer in the given circumstances will be $7,829.

If the employer would have released Brian from paying any interest rate on the loan amount that

has be utilized by him, the entire amount of interest calculated using the benchmarking rate, will

be treated as fringe benefit from the perspective of the employee and will be taxable in the hands

of the employee at the rate of 49%. In the circumstances, $19,373 will be treated as the fringe

benefit value and the fringe benefit tax would be $9,493. If the interest amount would have been

paid at the end of the loan period rather than paying in monthly installment, there would be no

change in the fringe benefit value for the employer.

If the employer would have released Brian from paying any interest rate on the loan amount that

has be utilized by him, the entire amount of interest calculated using the benchmarking rate, will

be treated as fringe benefit from the perspective of the employee and will be taxable in the hands

of the employee at the rate of 49%. In the circumstances, $19,373 will be treated as the fringe

benefit value and the fringe benefit tax would be $9,493.

Answer 3

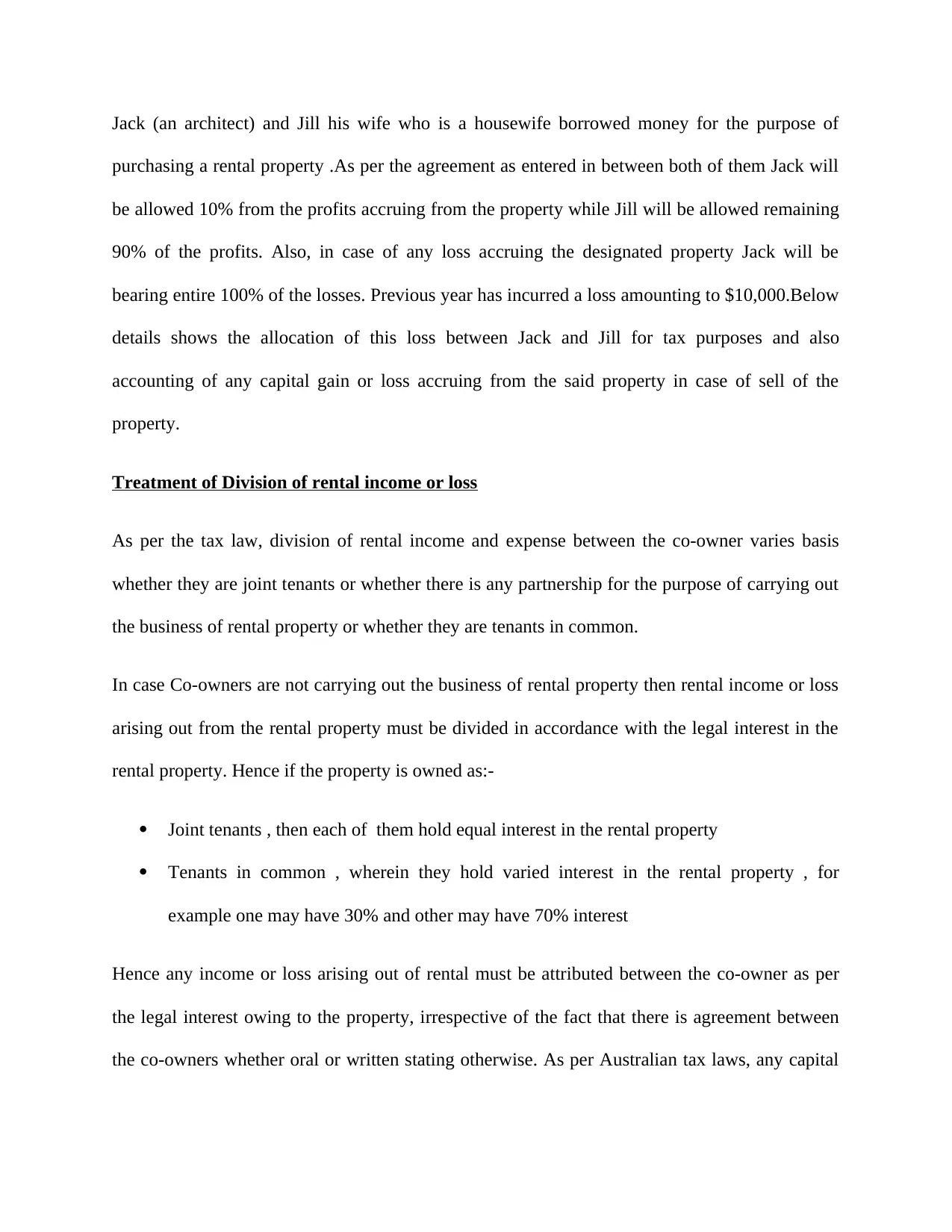

Jack (an architect) and Jill his wife who is a housewife borrowed money for the purpose of

purchasing a rental property .As per the agreement as entered in between both of them Jack will

be allowed 10% from the profits accruing from the property while Jill will be allowed remaining

90% of the profits. Also, in case of any loss accruing the designated property Jack will be

bearing entire 100% of the losses. Previous year has incurred a loss amounting to $10,000.Below

details shows the allocation of this loss between Jack and Jill for tax purposes and also

accounting of any capital gain or loss accruing from the said property in case of sell of the

property.

Treatment of Division of rental income or loss

As per the tax law, division of rental income and expense between the co-owner varies basis

whether they are joint tenants or whether there is any partnership for the purpose of carrying out

the business of rental property or whether they are tenants in common.

In case Co-owners are not carrying out the business of rental property then rental income or loss

arising out from the rental property must be divided in accordance with the legal interest in the

rental property. Hence if the property is owned as:-

Joint tenants , then each of them hold equal interest in the rental property

Tenants in common , wherein they hold varied interest in the rental property , for

example one may have 30% and other may have 70% interest

Hence any income or loss arising out of rental must be attributed between the co-owner as per

the legal interest owing to the property, irrespective of the fact that there is agreement between

the co-owners whether oral or written stating otherwise. As per Australian tax laws, any capital

purchasing a rental property .As per the agreement as entered in between both of them Jack will

be allowed 10% from the profits accruing from the property while Jill will be allowed remaining

90% of the profits. Also, in case of any loss accruing the designated property Jack will be

bearing entire 100% of the losses. Previous year has incurred a loss amounting to $10,000.Below

details shows the allocation of this loss between Jack and Jill for tax purposes and also

accounting of any capital gain or loss accruing from the said property in case of sell of the

property.

Treatment of Division of rental income or loss

As per the tax law, division of rental income and expense between the co-owner varies basis

whether they are joint tenants or whether there is any partnership for the purpose of carrying out

the business of rental property or whether they are tenants in common.

In case Co-owners are not carrying out the business of rental property then rental income or loss

arising out from the rental property must be divided in accordance with the legal interest in the

rental property. Hence if the property is owned as:-

Joint tenants , then each of them hold equal interest in the rental property

Tenants in common , wherein they hold varied interest in the rental property , for

example one may have 30% and other may have 70% interest

Hence any income or loss arising out of rental must be attributed between the co-owner as per

the legal interest owing to the property, irrespective of the fact that there is agreement between

the co-owners whether oral or written stating otherwise. As per Australian tax laws, any capital

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

gains or laws arising out of selling of rental property should be allocated on the basis as rental

income.

In given case law, Jack (an architect) and his wise Jill has purchased the property as Joint tenants

and the money is borrowed for the same purpose as Joint tenants. Hence both of them hold equal

legal interest in the rental property. However, there is a written agreement between them stating

Jill is entitled to 90% of profits while Jack is entitled to 10% of profits from the rental property

and in case of losses Jack is entitled to entire 100% of losses.

Conclusion:

Division of loss

As per the law stated above any rental income or loss is divided basis the legal interest of the co-

owners. Hence if the co-owners are joint tenants then each of the co-owner holds equal interest

in the rental property. As a result, as Jack and his wife Jill both are joint tenants having equal

legal interest in the property so last year loss amounting to $ 10,000 will be allocated equally

between Jack and Jill. I.e. $ 5,000 each and written agreement wrt distribution of profit or loss as

agreed between both them has no relevance.

Accounting of capital gain or Loss

Hence as per tax laws , since both Jack and Jill are co-owners as joint tenants and having equal

legal interest in the property hence any income or loss including capital gain or loss arising out

of this rental property will be allocated equally between them irrespective of any agreement

written between them. As a result, capital gain and loss will be accounted equally between Jack

and Jill as co-owners. (ATO)

income.

In given case law, Jack (an architect) and his wise Jill has purchased the property as Joint tenants

and the money is borrowed for the same purpose as Joint tenants. Hence both of them hold equal

legal interest in the rental property. However, there is a written agreement between them stating

Jill is entitled to 90% of profits while Jack is entitled to 10% of profits from the rental property

and in case of losses Jack is entitled to entire 100% of losses.

Conclusion:

Division of loss

As per the law stated above any rental income or loss is divided basis the legal interest of the co-

owners. Hence if the co-owners are joint tenants then each of the co-owner holds equal interest

in the rental property. As a result, as Jack and his wife Jill both are joint tenants having equal

legal interest in the property so last year loss amounting to $ 10,000 will be allocated equally

between Jack and Jill. I.e. $ 5,000 each and written agreement wrt distribution of profit or loss as

agreed between both them has no relevance.

Accounting of capital gain or Loss

Hence as per tax laws , since both Jack and Jill are co-owners as joint tenants and having equal

legal interest in the property hence any income or loss including capital gain or loss arising out

of this rental property will be allocated equally between them irrespective of any agreement

written between them. As a result, capital gain and loss will be accounted equally between Jack

and Jill as co-owners. (ATO)

Answer 4

There is a difference between tax avoidance and tax evasion. The tax avoidance event is

acceptable by law whereas the tax evasion attract penalties for government. The case IRC v

Duke of Westminster [1936] AC 1" was a tax avoidance case which came into picture in the year

1936. In the given case, the duke of Westminster it was decided that tax avoidance was

acceptable in law. In this case, the duke of Westminster was paying salary to his gardener on

weekly basis. Duke decided in a discussion with gardener that in spite of paying weekly wages,

they entered into an agreement where they will draw a covenant agreeing to pay an equal amount

to his salary. (Oxford Index)

In this scenario, the gardener will receive equal amount to what he was expecting from his

normal salary. But by entering into this agreement, duke was able to save his Income Tax

liability as during that period, through the help of covenant one can reduce the tax liability.

During this case, court judgment concluded that every human being rental to manage his affairs

which may help in reducing his tax liability payable to the tax authorities. As per the judge, if by

any means the taxpayer is able to determine any tax loopholes and able to save some tax, the tax

securities cannot compel the taxpayer to pay additional tax. (Adam, 2011)

After court judgment, Duke won the case and he was not supposed to pay any additional tax.

Considering the provision of Australian tax laws, the principle that was decided in duke case is

relevant in Australia today as well. The Tax avoidance and tax evasion concept has been made

clear 1936 by Duke Case and it is still being followed in Australia. (Fisher, 2005)

Answer 5

There is a difference between tax avoidance and tax evasion. The tax avoidance event is

acceptable by law whereas the tax evasion attract penalties for government. The case IRC v

Duke of Westminster [1936] AC 1" was a tax avoidance case which came into picture in the year

1936. In the given case, the duke of Westminster it was decided that tax avoidance was

acceptable in law. In this case, the duke of Westminster was paying salary to his gardener on

weekly basis. Duke decided in a discussion with gardener that in spite of paying weekly wages,

they entered into an agreement where they will draw a covenant agreeing to pay an equal amount

to his salary. (Oxford Index)

In this scenario, the gardener will receive equal amount to what he was expecting from his

normal salary. But by entering into this agreement, duke was able to save his Income Tax

liability as during that period, through the help of covenant one can reduce the tax liability.

During this case, court judgment concluded that every human being rental to manage his affairs

which may help in reducing his tax liability payable to the tax authorities. As per the judge, if by

any means the taxpayer is able to determine any tax loopholes and able to save some tax, the tax

securities cannot compel the taxpayer to pay additional tax. (Adam, 2011)

After court judgment, Duke won the case and he was not supposed to pay any additional tax.

Considering the provision of Australian tax laws, the principle that was decided in duke case is

relevant in Australia today as well. The Tax avoidance and tax evasion concept has been made

clear 1936 by Duke Case and it is still being followed in Australia. (Fisher, 2005)

Answer 5

Bill is the owner of large parcel of land having lots of tall pine trees. Bill wants to use this land

for grazing sheep and hence intends to clear the trees. Logging company has agreed to pay $

1000 for every 100 meters timber as extracted from the land. Below details advises the bill

whether assessment will be made basis receipts as received from the arrangement. Also the

treatment if the payment is made $ 50,000 in lump sum for granting permission to the logging

company for the purpose of removal of timber from the land.

Below rule applies to :

Person engaged in forest operations and

Person not engaged in forest operations who dispose of timber

In case wherein taxpayer disposes the tress planted or tended for the purpose of sale , although

whole or part of business is constituted by the trees , the disposal is not carried out as ordinary

course of business , the value of trees becomes taxpayer’s assessable income

Thus as per section 6, royalties as received by the taxpayer by way of granting right to sell the

timber on taxpayer’s acquired land will be considered as assessable income of the taxpayer in the

year

Considering the provision of the above law, the amount that has been received by Bill from the

company for taking of timber from the land will be considered as taxable income in the hands of

Billy. The same will not be considered as an ordinary course of business for Billy. On the other

hand, if the company agrees to pay a lump sum amount worth $50,000 for taking off timber from

the land, the same will again be treated as assessable income in the hands of Billy and will be

taxable in his hands. (ATO)

for grazing sheep and hence intends to clear the trees. Logging company has agreed to pay $

1000 for every 100 meters timber as extracted from the land. Below details advises the bill

whether assessment will be made basis receipts as received from the arrangement. Also the

treatment if the payment is made $ 50,000 in lump sum for granting permission to the logging

company for the purpose of removal of timber from the land.

Below rule applies to :

Person engaged in forest operations and

Person not engaged in forest operations who dispose of timber

In case wherein taxpayer disposes the tress planted or tended for the purpose of sale , although

whole or part of business is constituted by the trees , the disposal is not carried out as ordinary

course of business , the value of trees becomes taxpayer’s assessable income

Thus as per section 6, royalties as received by the taxpayer by way of granting right to sell the

timber on taxpayer’s acquired land will be considered as assessable income of the taxpayer in the

year

Considering the provision of the above law, the amount that has been received by Bill from the

company for taking of timber from the land will be considered as taxable income in the hands of

Billy. The same will not be considered as an ordinary course of business for Billy. On the other

hand, if the company agrees to pay a lump sum amount worth $50,000 for taking off timber from

the land, the same will again be treated as assessable income in the hands of Billy and will be

taxable in his hands. (ATO)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Considering the provision of above laws, the amount that will be received by Billy from getting

the timber removed from the land will be taxable in his hands as normal assessable income.

the timber removed from the land will be taxable in his hands as normal assessable income.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.