Analysis of Telstra Corporation's Cash Flow, Other Comprehensive Income Statement and Corporate Income Tax | HI5020

VerifiedAdded on 2023/06/12

|14

|3333

|425

AI Summary

This report provides an analysis of Telstra Corporation's cash flow statement, other comprehensive income statement and corporate income tax. It includes a description of Telstra Corporation and its financial statements, a comparative analysis of the cash flow statement, and a description of the items in the other comprehensive income statement.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1

HI5020 Corporate Accounting

HI5020 Corporate Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2

Contents

Introduction......................................................................................................................................3

Description of Telstra Corporations Limited...................................................................................3

Section 1: Cash flow Statement.......................................................................................................4

Section 1.1: Important items listed in cash flow statement of Telstra Corporation and

understanding of each item of cash flow statement.....................................................................4

Section 1.2: Comparative analysis of three main activities of cash flow statement and its

evaluation.....................................................................................................................................6

Section 2: Analyses of the other Comprehensive income statement...............................................7

Section 2.1: Items reported in other comprehensive income statement.......................................7

Section 2.2: Description of each of the items of other comprehensive income statement...........8

Section 2.3: Reason why the above items are presented in other comprehensive income

statement......................................................................................................................................8

Section 3: Accounting for Corporate Income Tax...........................................................................8

Section 3.1: Tax Expenses reported in the latest financial year...................................................8

Section 3.2: Difference between the accounting tax expenses as per fixed tax rate and tax

expenses shown in profit and loss account..................................................................................8

Section 3.3: Deferred tax assets and deferred tax liabilities reported in the balance sheet..........9

Section 3.4: Current tax assets or income tax payable as reported in the balance sheet............10

Section 3.5: Income tax expense and income tax paid..............................................................11

Section 3.6: Self learning from the accounting of taxes............................................................11

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

Contents

Introduction......................................................................................................................................3

Description of Telstra Corporations Limited...................................................................................3

Section 1: Cash flow Statement.......................................................................................................4

Section 1.1: Important items listed in cash flow statement of Telstra Corporation and

understanding of each item of cash flow statement.....................................................................4

Section 1.2: Comparative analysis of three main activities of cash flow statement and its

evaluation.....................................................................................................................................6

Section 2: Analyses of the other Comprehensive income statement...............................................7

Section 2.1: Items reported in other comprehensive income statement.......................................7

Section 2.2: Description of each of the items of other comprehensive income statement...........8

Section 2.3: Reason why the above items are presented in other comprehensive income

statement......................................................................................................................................8

Section 3: Accounting for Corporate Income Tax...........................................................................8

Section 3.1: Tax Expenses reported in the latest financial year...................................................8

Section 3.2: Difference between the accounting tax expenses as per fixed tax rate and tax

expenses shown in profit and loss account..................................................................................8

Section 3.3: Deferred tax assets and deferred tax liabilities reported in the balance sheet..........9

Section 3.4: Current tax assets or income tax payable as reported in the balance sheet............10

Section 3.5: Income tax expense and income tax paid..............................................................11

Section 3.6: Self learning from the accounting of taxes............................................................11

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

3

Introduction

The financial statements developed by a business entity play a very critical role in

making significant decisions relating to its future expansion and growth. It depicts the financial

strength of an entity by providing an analysis of its major financial items such as assets,

liabilities and equity. The major financial statements that are developed by a business entity are

statement of profit and loss, balance sheet and cash flow statement. The business entities around

the world are required to develop and disclose their financial statements in their annual reports

and the relevant methods used for their preparation as per the international accounting standards.

The business entities operating within Australia also need to develop their financial statements as

per the international accounting standards. Australian business entities need to adopt the relevant

accounting standards of AASB for development and disclosure of their financial information.

In this context, the report has undertaken the analysis of financial statements and the

notes section of a public limited company listed on the ASX. The report has provided an analysis

of the cash flow statement of the selected company by providing an in-depth understanding of

each of its items such as operational, investment and financing activities. Also, it carries out an

analysis of the items reported in the income statement and also provides a discussion in relation

to the items that are not reported in the profit and loss statement of the company. In addition to

this, it also examines and evaluates the tax treatment provided in the latest financial statements of

the selected company. The company selected in this context is Telstra Corporations Limited a

recognized telecommunication entity in Australia listed on stock exchange.

Description of Telstra Corporations Limited

Telstra Corporation Limited is a recognized leading telecommunication and technology

company of Australia that is involved in providing telecommunication services within Australia

market. The company is involved in retail mobile, fixed voice and broadband services to its

consumers within Australia and at international level. The company by providing technology

efficient and content solutions has attained the position of largest and fastest mobile network

within the country. It is also actively involved in providing digital communication services to the

consumers of Australia. The company besides providing its operations within Australia and also

Introduction

The financial statements developed by a business entity play a very critical role in

making significant decisions relating to its future expansion and growth. It depicts the financial

strength of an entity by providing an analysis of its major financial items such as assets,

liabilities and equity. The major financial statements that are developed by a business entity are

statement of profit and loss, balance sheet and cash flow statement. The business entities around

the world are required to develop and disclose their financial statements in their annual reports

and the relevant methods used for their preparation as per the international accounting standards.

The business entities operating within Australia also need to develop their financial statements as

per the international accounting standards. Australian business entities need to adopt the relevant

accounting standards of AASB for development and disclosure of their financial information.

In this context, the report has undertaken the analysis of financial statements and the

notes section of a public limited company listed on the ASX. The report has provided an analysis

of the cash flow statement of the selected company by providing an in-depth understanding of

each of its items such as operational, investment and financing activities. Also, it carries out an

analysis of the items reported in the income statement and also provides a discussion in relation

to the items that are not reported in the profit and loss statement of the company. In addition to

this, it also examines and evaluates the tax treatment provided in the latest financial statements of

the selected company. The company selected in this context is Telstra Corporations Limited a

recognized telecommunication entity in Australia listed on stock exchange.

Description of Telstra Corporations Limited

Telstra Corporation Limited is a recognized leading telecommunication and technology

company of Australia that is involved in providing telecommunication services within Australia

market. The company is involved in retail mobile, fixed voice and broadband services to its

consumers within Australia and at international level. The company by providing technology

efficient and content solutions has attained the position of largest and fastest mobile network

within the country. It is also actively involved in providing digital communication services to the

consumers of Australia. The company besides providing its operations within Australia and also

4

has international presence across 20 countries. The company since its establishment is known to

providing innovative communication solutions to customers and improving their quality of life

and work with the help of better connection services. The major telecommunication product and

services provided by the company includes mobile phones, mobile devices and broadband

internet and entertainment products and services. The telecommunication and information

services provided by the company are utilized by businesses, governments, communities and

individuals within Australia and at international level (Annual report 2017: Telstra Corporation).

Section 1: Cash flow Statement

Section 1.1: Important items listed in cash flow statement of Telstra Corporation and

understanding of each item of cash flow statement

Below table shows the important items that are listed in the cash flow statement of the

Telstra Corporation.

Important financial items of Cash Flow Statement

Telstra Corporation

For last three years ( 2015, 2016 and 2017)

Amount in $ million

Particulars 2017 2016 2015

Items of operating activity

Cash Received from customers

$

31,288.00

$

31,163.00

$

29,521.00

Cash payments made to suppliers and employees

$

(21,997.00)

$

(21,179.00)

$

(19,621.00)

Government grants received

$

235.00

$

182.00

$

166.00

Net placement of deposits by Auto home Inc. that

are not part of cash equivalents

$

-

$

(173.00)

$

-

Income taxes paid

$

(1,751.00)

$

(1,860.00)

$

(1,755.00)

has international presence across 20 countries. The company since its establishment is known to

providing innovative communication solutions to customers and improving their quality of life

and work with the help of better connection services. The major telecommunication product and

services provided by the company includes mobile phones, mobile devices and broadband

internet and entertainment products and services. The telecommunication and information

services provided by the company are utilized by businesses, governments, communities and

individuals within Australia and at international level (Annual report 2017: Telstra Corporation).

Section 1: Cash flow Statement

Section 1.1: Important items listed in cash flow statement of Telstra Corporation and

understanding of each item of cash flow statement

Below table shows the important items that are listed in the cash flow statement of the

Telstra Corporation.

Important financial items of Cash Flow Statement

Telstra Corporation

For last three years ( 2015, 2016 and 2017)

Amount in $ million

Particulars 2017 2016 2015

Items of operating activity

Cash Received from customers

$

31,288.00

$

31,163.00

$

29,521.00

Cash payments made to suppliers and employees

$

(21,997.00)

$

(21,179.00)

$

(19,621.00)

Government grants received

$

235.00

$

182.00

$

166.00

Net placement of deposits by Auto home Inc. that

are not part of cash equivalents

$

-

$

(173.00)

$

-

Income taxes paid

$

(1,751.00)

$

(1,860.00)

$

(1,755.00)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

5

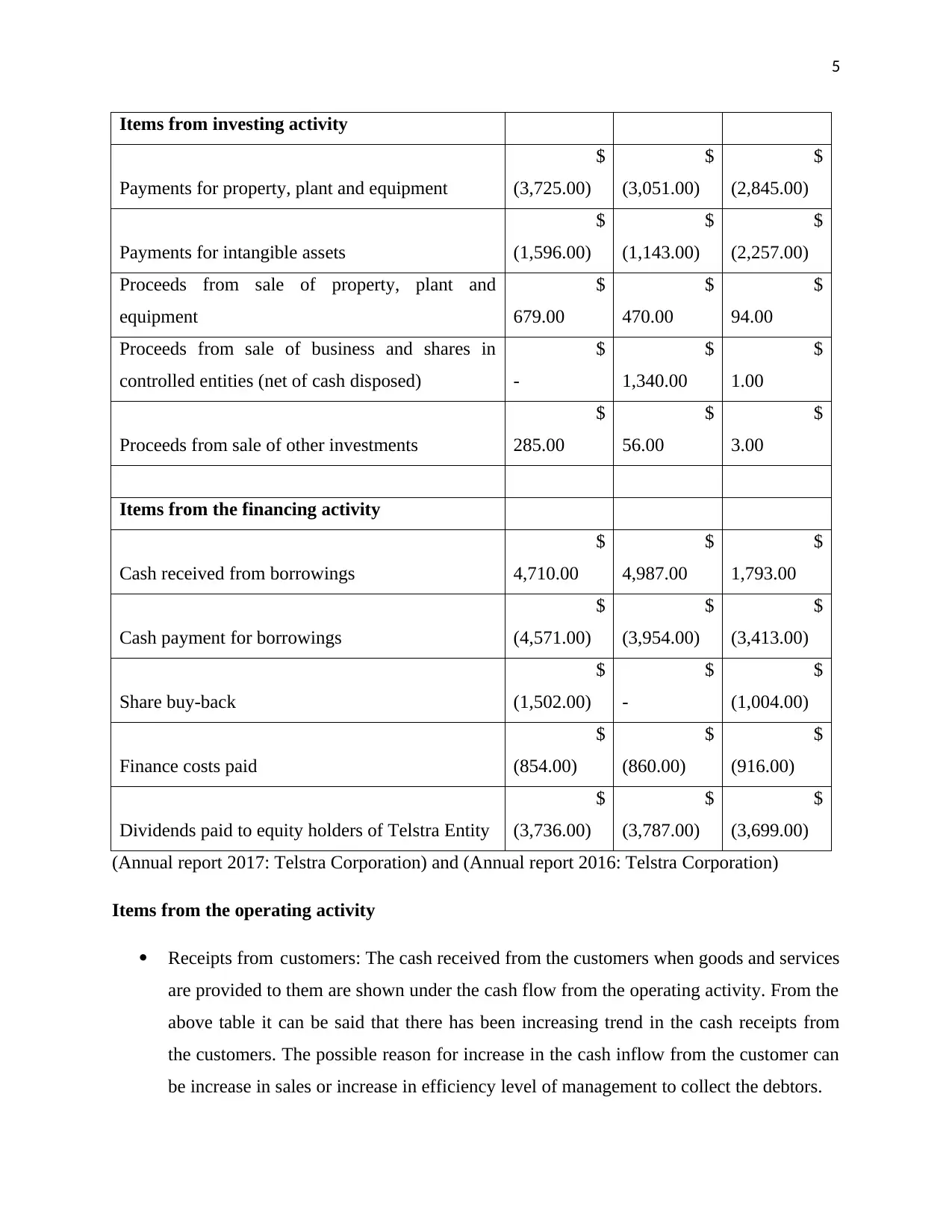

Items from investing activity

Payments for property, plant and equipment

$

(3,725.00)

$

(3,051.00)

$

(2,845.00)

Payments for intangible assets

$

(1,596.00)

$

(1,143.00)

$

(2,257.00)

Proceeds from sale of property, plant and

equipment

$

679.00

$

470.00

$

94.00

Proceeds from sale of business and shares in

controlled entities (net of cash disposed)

$

-

$

1,340.00

$

1.00

Proceeds from sale of other investments

$

285.00

$

56.00

$

3.00

Items from the financing activity

Cash received from borrowings

$

4,710.00

$

4,987.00

$

1,793.00

Cash payment for borrowings

$

(4,571.00)

$

(3,954.00)

$

(3,413.00)

Share buy-back

$

(1,502.00)

$

-

$

(1,004.00)

Finance costs paid

$

(854.00)

$

(860.00)

$

(916.00)

Dividends paid to equity holders of Telstra Entity

$

(3,736.00)

$

(3,787.00)

$

(3,699.00)

(Annual report 2017: Telstra Corporation) and (Annual report 2016: Telstra Corporation)

Items from the operating activity

Receipts from customers: The cash received from the customers when goods and services

are provided to them are shown under the cash flow from the operating activity. From the

above table it can be said that there has been increasing trend in the cash receipts from

the customers. The possible reason for increase in the cash inflow from the customer can

be increase in sales or increase in efficiency level of management to collect the debtors.

Items from investing activity

Payments for property, plant and equipment

$

(3,725.00)

$

(3,051.00)

$

(2,845.00)

Payments for intangible assets

$

(1,596.00)

$

(1,143.00)

$

(2,257.00)

Proceeds from sale of property, plant and

equipment

$

679.00

$

470.00

$

94.00

Proceeds from sale of business and shares in

controlled entities (net of cash disposed)

$

-

$

1,340.00

$

1.00

Proceeds from sale of other investments

$

285.00

$

56.00

$

3.00

Items from the financing activity

Cash received from borrowings

$

4,710.00

$

4,987.00

$

1,793.00

Cash payment for borrowings

$

(4,571.00)

$

(3,954.00)

$

(3,413.00)

Share buy-back

$

(1,502.00)

$

-

$

(1,004.00)

Finance costs paid

$

(854.00)

$

(860.00)

$

(916.00)

Dividends paid to equity holders of Telstra Entity

$

(3,736.00)

$

(3,787.00)

$

(3,699.00)

(Annual report 2017: Telstra Corporation) and (Annual report 2016: Telstra Corporation)

Items from the operating activity

Receipts from customers: The cash received from the customers when goods and services

are provided to them are shown under the cash flow from the operating activity. From the

above table it can be said that there has been increasing trend in the cash receipts from

the customers. The possible reason for increase in the cash inflow from the customer can

be increase in sales or increase in efficiency level of management to collect the debtors.

6

Cash Payment to suppliers and employees: The main outflows of cash are payment made

to suppliers and employees. There has been increasing trend in cash payments that clearly

indicates increase in cost of goods sold because of increase in net sales from year 2015 to

2017.

Tax Payment: It can be seen from the above table that Telstra Corporation has been

paying taxes on regular basis (Baker and Nofsinger, 2010).

Items from the investing activity

Cash paid for buying the property, plant and equipment: It has been that Telstra

Corporation is regularly making investment in the plant, property and equipment so that it

can maintain necessary assets required for increasing the sales revenue. There has been

increase in cash paid for buying the property, plant and equipments.

Cash received from the sale of plant, property and equipment: Management at Telstra

Corporation is continuously involved in retiring its main assets after they have become

obsolete. It helps the Telstra to make enough cash for making investment in new plant,

property and equipments.

Cash received from the sale of business or share in any controlled entity: It has seen from

the above table that Telstra has sold its major business unit in year 2016 that has raised its

cash to $1340 million.

Items of Financing Activity

Cash receipts from the borrowings from the financial institutions: Telstra Corporation

uses debt as the major source of finance to fund their assets. Cash received from the

borrowing are regularly increasing that give an indication that Telstra is planning to make

debt source of capital as the major source of finance and make the Telstra a leverage

firm.

Cash payment for borrowing: As the debt capital rise through borrowing the fund from

the banks it also creates a responsibility to pay the borrowing on time. In this context, it

can be seen that Telstra has been paying the borrowing funds to banks on time and also

paying the finance cost together with it.

Cash Payment to suppliers and employees: The main outflows of cash are payment made

to suppliers and employees. There has been increasing trend in cash payments that clearly

indicates increase in cost of goods sold because of increase in net sales from year 2015 to

2017.

Tax Payment: It can be seen from the above table that Telstra Corporation has been

paying taxes on regular basis (Baker and Nofsinger, 2010).

Items from the investing activity

Cash paid for buying the property, plant and equipment: It has been that Telstra

Corporation is regularly making investment in the plant, property and equipment so that it

can maintain necessary assets required for increasing the sales revenue. There has been

increase in cash paid for buying the property, plant and equipments.

Cash received from the sale of plant, property and equipment: Management at Telstra

Corporation is continuously involved in retiring its main assets after they have become

obsolete. It helps the Telstra to make enough cash for making investment in new plant,

property and equipments.

Cash received from the sale of business or share in any controlled entity: It has seen from

the above table that Telstra has sold its major business unit in year 2016 that has raised its

cash to $1340 million.

Items of Financing Activity

Cash receipts from the borrowings from the financial institutions: Telstra Corporation

uses debt as the major source of finance to fund their assets. Cash received from the

borrowing are regularly increasing that give an indication that Telstra is planning to make

debt source of capital as the major source of finance and make the Telstra a leverage

firm.

Cash payment for borrowing: As the debt capital rise through borrowing the fund from

the banks it also creates a responsibility to pay the borrowing on time. In this context, it

can be seen that Telstra has been paying the borrowing funds to banks on time and also

paying the finance cost together with it.

7

Dividend payment: It has been seen that Telstra has been paying same level of dividend

to their shareholder with very less increase in total dividend (Baker and Nofsinger, 2010).

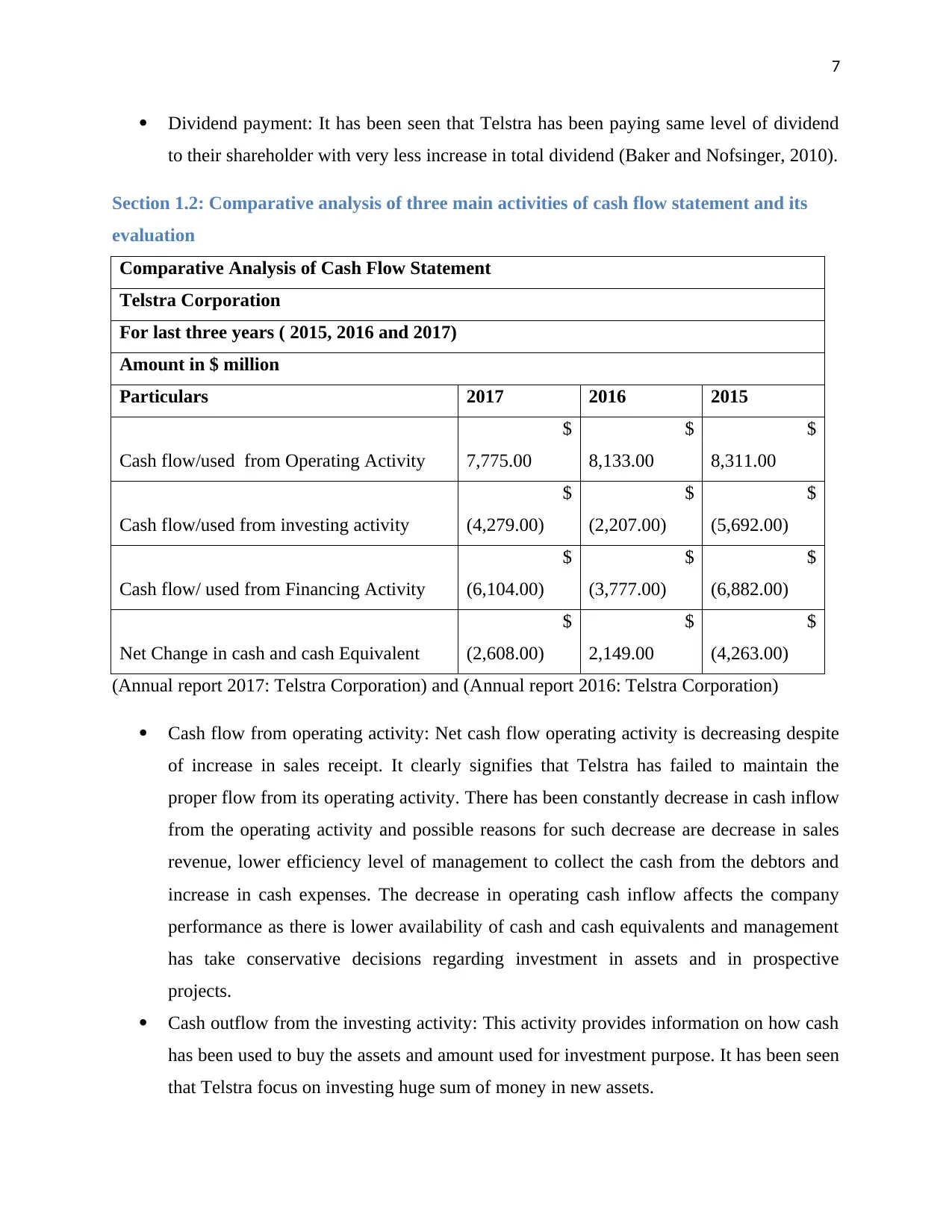

Section 1.2: Comparative analysis of three main activities of cash flow statement and its

evaluation

Comparative Analysis of Cash Flow Statement

Telstra Corporation

For last three years ( 2015, 2016 and 2017)

Amount in $ million

Particulars 2017 2016 2015

Cash flow/used from Operating Activity

$

7,775.00

$

8,133.00

$

8,311.00

Cash flow/used from investing activity

$

(4,279.00)

$

(2,207.00)

$

(5,692.00)

Cash flow/ used from Financing Activity

$

(6,104.00)

$

(3,777.00)

$

(6,882.00)

Net Change in cash and cash Equivalent

$

(2,608.00)

$

2,149.00

$

(4,263.00)

(Annual report 2017: Telstra Corporation) and (Annual report 2016: Telstra Corporation)

Cash flow from operating activity: Net cash flow operating activity is decreasing despite

of increase in sales receipt. It clearly signifies that Telstra has failed to maintain the

proper flow from its operating activity. There has been constantly decrease in cash inflow

from the operating activity and possible reasons for such decrease are decrease in sales

revenue, lower efficiency level of management to collect the cash from the debtors and

increase in cash expenses. The decrease in operating cash inflow affects the company

performance as there is lower availability of cash and cash equivalents and management

has take conservative decisions regarding investment in assets and in prospective

projects.

Cash outflow from the investing activity: This activity provides information on how cash

has been used to buy the assets and amount used for investment purpose. It has been seen

that Telstra focus on investing huge sum of money in new assets.

Dividend payment: It has been seen that Telstra has been paying same level of dividend

to their shareholder with very less increase in total dividend (Baker and Nofsinger, 2010).

Section 1.2: Comparative analysis of three main activities of cash flow statement and its

evaluation

Comparative Analysis of Cash Flow Statement

Telstra Corporation

For last three years ( 2015, 2016 and 2017)

Amount in $ million

Particulars 2017 2016 2015

Cash flow/used from Operating Activity

$

7,775.00

$

8,133.00

$

8,311.00

Cash flow/used from investing activity

$

(4,279.00)

$

(2,207.00)

$

(5,692.00)

Cash flow/ used from Financing Activity

$

(6,104.00)

$

(3,777.00)

$

(6,882.00)

Net Change in cash and cash Equivalent

$

(2,608.00)

$

2,149.00

$

(4,263.00)

(Annual report 2017: Telstra Corporation) and (Annual report 2016: Telstra Corporation)

Cash flow from operating activity: Net cash flow operating activity is decreasing despite

of increase in sales receipt. It clearly signifies that Telstra has failed to maintain the

proper flow from its operating activity. There has been constantly decrease in cash inflow

from the operating activity and possible reasons for such decrease are decrease in sales

revenue, lower efficiency level of management to collect the cash from the debtors and

increase in cash expenses. The decrease in operating cash inflow affects the company

performance as there is lower availability of cash and cash equivalents and management

has take conservative decisions regarding investment in assets and in prospective

projects.

Cash outflow from the investing activity: This activity provides information on how cash

has been used to buy the assets and amount used for investment purpose. It has been seen

that Telstra focus on investing huge sum of money in new assets.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

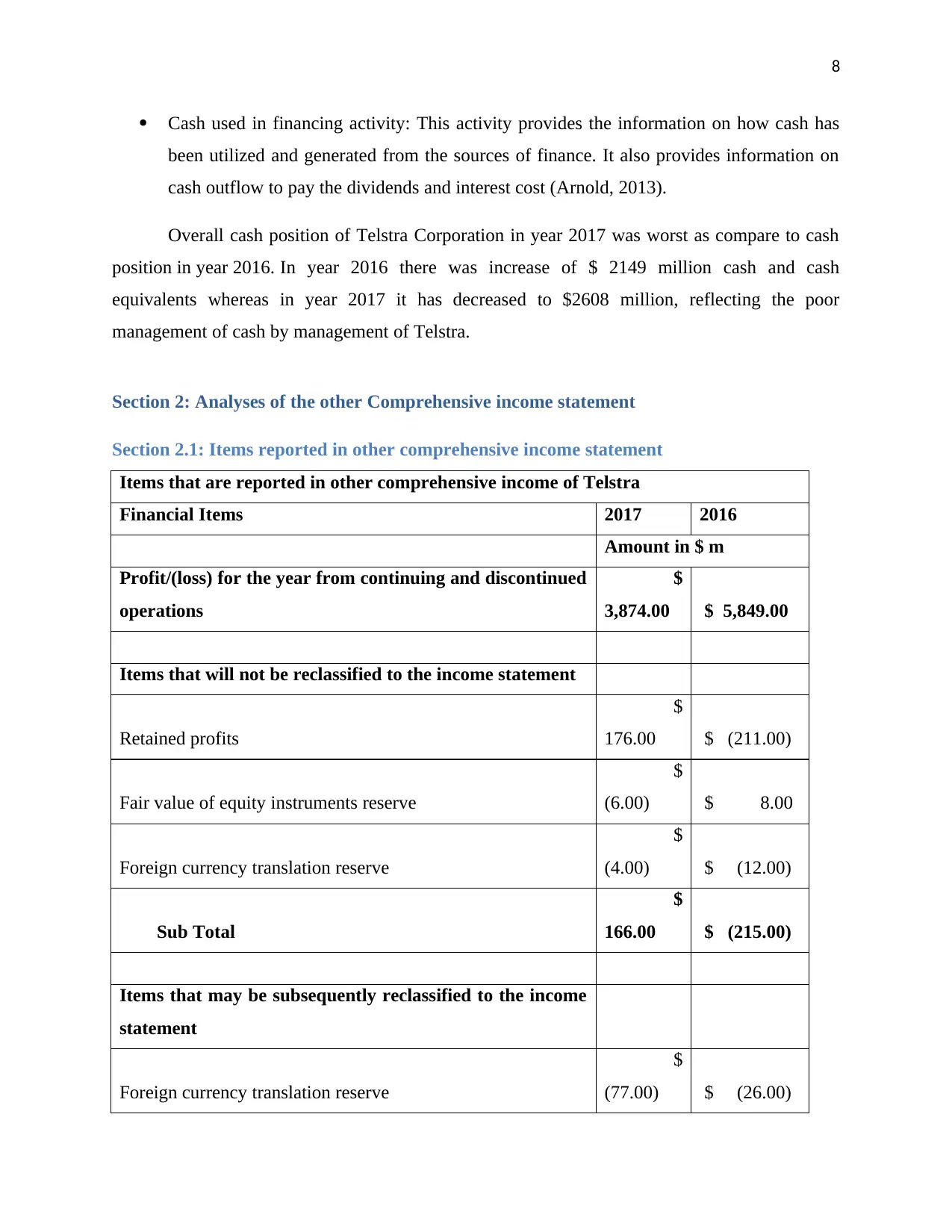

Cash used in financing activity: This activity provides the information on how cash has

been utilized and generated from the sources of finance. It also provides information on

cash outflow to pay the dividends and interest cost (Arnold, 2013).

Overall cash position of Telstra Corporation in year 2017 was worst as compare to cash

position in year 2016. In year 2016 there was increase of $ 2149 million cash and cash

equivalents whereas in year 2017 it has decreased to $2608 million, reflecting the poor

management of cash by management of Telstra.

Section 2: Analyses of the other Comprehensive income statement

Section 2.1: Items reported in other comprehensive income statement

Items that are reported in other comprehensive income of Telstra

Financial Items 2017 2016

Amount in $ m

Profit/(loss) for the year from continuing and discontinued

operations

$

3,874.00 $ 5,849.00

Items that will not be reclassified to the income statement

Retained profits

$

176.00 $ (211.00)

Fair value of equity instruments reserve

$

(6.00) $ 8.00

Foreign currency translation reserve

$

(4.00) $ (12.00)

Sub Total

$

166.00 $ (215.00)

Items that may be subsequently reclassified to the income

statement

Foreign currency translation reserve

$

(77.00) $ (26.00)

Cash used in financing activity: This activity provides the information on how cash has

been utilized and generated from the sources of finance. It also provides information on

cash outflow to pay the dividends and interest cost (Arnold, 2013).

Overall cash position of Telstra Corporation in year 2017 was worst as compare to cash

position in year 2016. In year 2016 there was increase of $ 2149 million cash and cash

equivalents whereas in year 2017 it has decreased to $2608 million, reflecting the poor

management of cash by management of Telstra.

Section 2: Analyses of the other Comprehensive income statement

Section 2.1: Items reported in other comprehensive income statement

Items that are reported in other comprehensive income of Telstra

Financial Items 2017 2016

Amount in $ m

Profit/(loss) for the year from continuing and discontinued

operations

$

3,874.00 $ 5,849.00

Items that will not be reclassified to the income statement

Retained profits

$

176.00 $ (211.00)

Fair value of equity instruments reserve

$

(6.00) $ 8.00

Foreign currency translation reserve

$

(4.00) $ (12.00)

Sub Total

$

166.00 $ (215.00)

Items that may be subsequently reclassified to the income

statement

Foreign currency translation reserve

$

(77.00) $ (26.00)

9

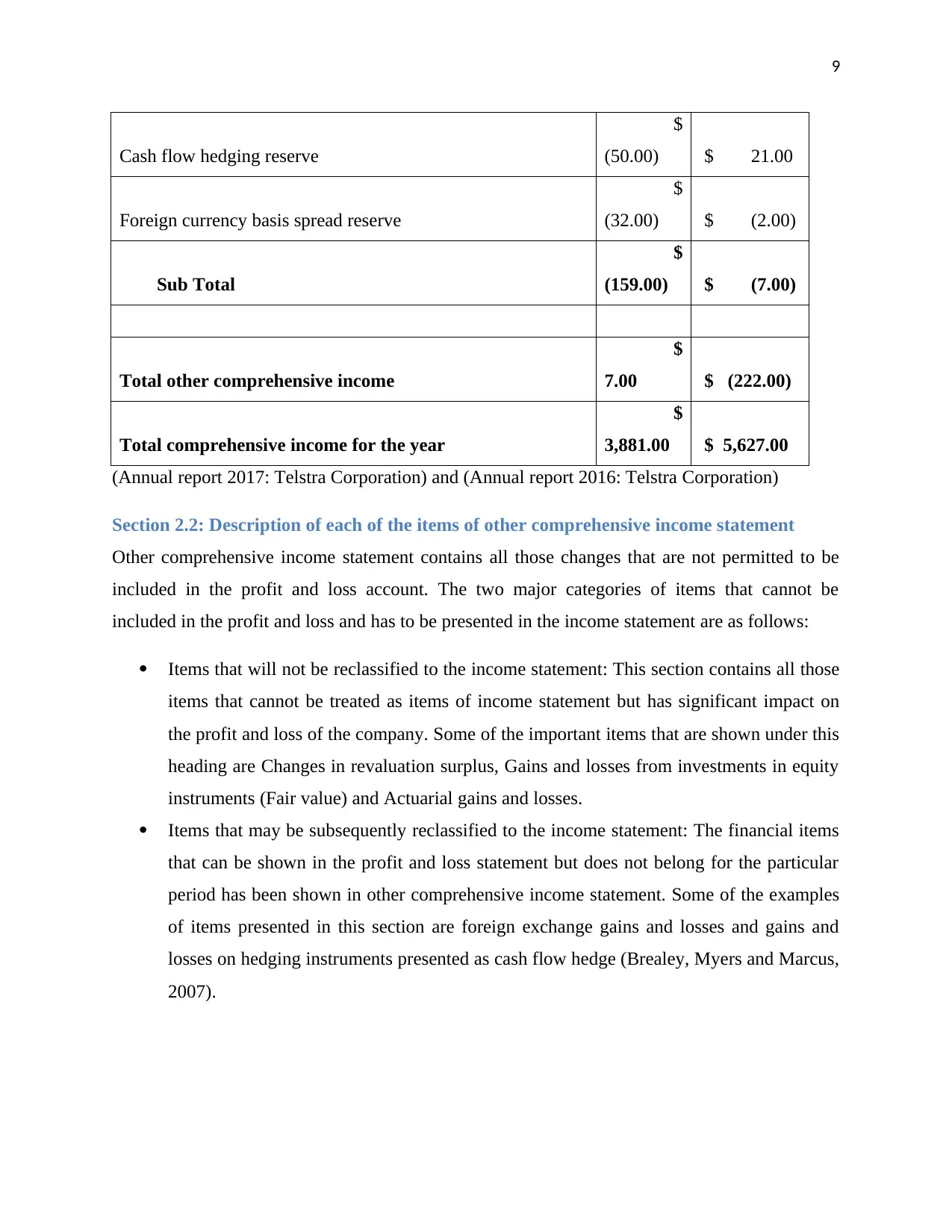

Cash flow hedging reserve

$

(50.00) $ 21.00

Foreign currency basis spread reserve

$

(32.00) $ (2.00)

Sub Total

$

(159.00) $ (7.00)

Total other comprehensive income

$

7.00 $ (222.00)

Total comprehensive income for the year

$

3,881.00 $ 5,627.00

(Annual report 2017: Telstra Corporation) and (Annual report 2016: Telstra Corporation)

Section 2.2: Description of each of the items of other comprehensive income statement

Other comprehensive income statement contains all those changes that are not permitted to be

included in the profit and loss account. The two major categories of items that cannot be

included in the profit and loss and has to be presented in the income statement are as follows:

Items that will not be reclassified to the income statement: This section contains all those

items that cannot be treated as items of income statement but has significant impact on

the profit and loss of the company. Some of the important items that are shown under this

heading are Changes in revaluation surplus, Gains and losses from investments in equity

instruments (Fair value) and Actuarial gains and losses.

Items that may be subsequently reclassified to the income statement: The financial items

that can be shown in the profit and loss statement but does not belong for the particular

period has been shown in other comprehensive income statement. Some of the examples

of items presented in this section are foreign exchange gains and losses and gains and

losses on hedging instruments presented as cash flow hedge (Brealey, Myers and Marcus,

2007).

Cash flow hedging reserve

$

(50.00) $ 21.00

Foreign currency basis spread reserve

$

(32.00) $ (2.00)

Sub Total

$

(159.00) $ (7.00)

Total other comprehensive income

$

7.00 $ (222.00)

Total comprehensive income for the year

$

3,881.00 $ 5,627.00

(Annual report 2017: Telstra Corporation) and (Annual report 2016: Telstra Corporation)

Section 2.2: Description of each of the items of other comprehensive income statement

Other comprehensive income statement contains all those changes that are not permitted to be

included in the profit and loss account. The two major categories of items that cannot be

included in the profit and loss and has to be presented in the income statement are as follows:

Items that will not be reclassified to the income statement: This section contains all those

items that cannot be treated as items of income statement but has significant impact on

the profit and loss of the company. Some of the important items that are shown under this

heading are Changes in revaluation surplus, Gains and losses from investments in equity

instruments (Fair value) and Actuarial gains and losses.

Items that may be subsequently reclassified to the income statement: The financial items

that can be shown in the profit and loss statement but does not belong for the particular

period has been shown in other comprehensive income statement. Some of the examples

of items presented in this section are foreign exchange gains and losses and gains and

losses on hedging instruments presented as cash flow hedge (Brealey, Myers and Marcus,

2007).

10

Section 2.3: Reason why the above items are presented in other comprehensive income

statement

The main reason why above items are shown in other comprehensive income statement is

that above items does not impact the current accounting profit but has significant impact on net

profit in any subsequent year and there are some items that does not belong to profit and loss

statement but impact the profit attributable to the equity shareholders.

Section 3: Accounting for Corporate Income Tax

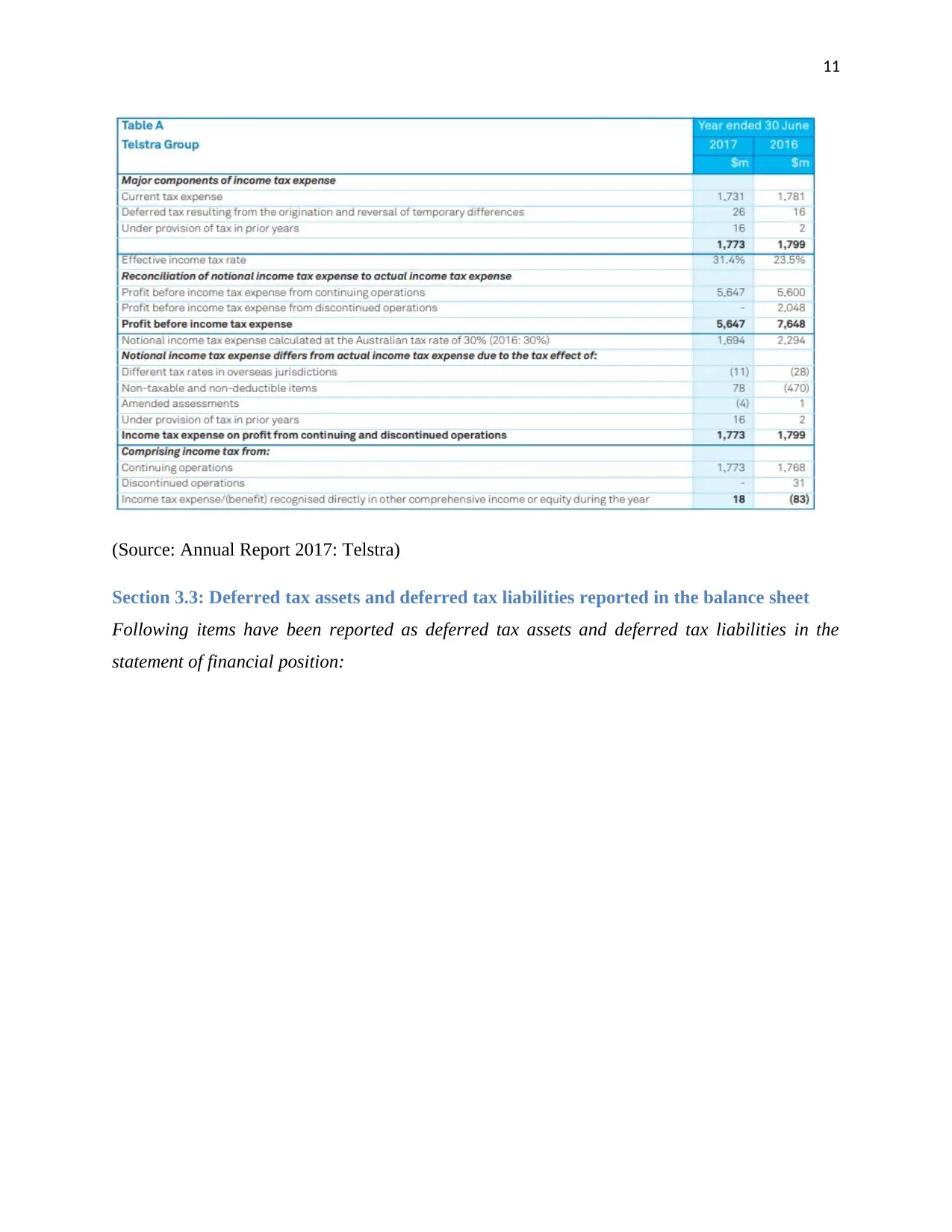

Section 3.1: Tax Expenses reported in the latest financial year

Telstra Corporation has reported corporate income tax of $1773 million dollar for year

2017 and $1768 million in year 2016. Income tax expenses has been reported in income

statement of the company and this amount represent the accounting tax expenses adjustable to

changes in tax expenses due to prior year items, tax on associates, impact of non deductible items

and any change in tax rate (Annual report 2017: Telstra Corporation).

Section 3.2: Difference between the accounting tax expenses as per fixed tax rate and tax

expenses shown in profit and loss account

On the basis of information presented in income statement and notes to account it can be

said that tax reported in income statement and tax calculated at flat rate of 30% is not similar.

The accounting tax expense is also called as notional tax expenses and it is adjustable to many

financial changes such as tax rate impact of other countries on profit of the company, any

changes due to tax of prior year and various non taxable and non deductible items (Deegan,

2013).

Section 2.3: Reason why the above items are presented in other comprehensive income

statement

The main reason why above items are shown in other comprehensive income statement is

that above items does not impact the current accounting profit but has significant impact on net

profit in any subsequent year and there are some items that does not belong to profit and loss

statement but impact the profit attributable to the equity shareholders.

Section 3: Accounting for Corporate Income Tax

Section 3.1: Tax Expenses reported in the latest financial year

Telstra Corporation has reported corporate income tax of $1773 million dollar for year

2017 and $1768 million in year 2016. Income tax expenses has been reported in income

statement of the company and this amount represent the accounting tax expenses adjustable to

changes in tax expenses due to prior year items, tax on associates, impact of non deductible items

and any change in tax rate (Annual report 2017: Telstra Corporation).

Section 3.2: Difference between the accounting tax expenses as per fixed tax rate and tax

expenses shown in profit and loss account

On the basis of information presented in income statement and notes to account it can be

said that tax reported in income statement and tax calculated at flat rate of 30% is not similar.

The accounting tax expense is also called as notional tax expenses and it is adjustable to many

financial changes such as tax rate impact of other countries on profit of the company, any

changes due to tax of prior year and various non taxable and non deductible items (Deegan,

2013).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

11

(Source: Annual Report 2017: Telstra)

Section 3.3: Deferred tax assets and deferred tax liabilities reported in the balance sheet

Following items have been reported as deferred tax assets and deferred tax liabilities in the

statement of financial position:

(Source: Annual Report 2017: Telstra)

Section 3.3: Deferred tax assets and deferred tax liabilities reported in the balance sheet

Following items have been reported as deferred tax assets and deferred tax liabilities in the

statement of financial position:

12

(Annual report 2017: Telstra Corporation)

The difference in book profit and taxable profits give rise to timing differences and it can

be temporary or permanent in nature. The temporary timing differences are capable for reversing

in any subsequent year while permanent differences cannot be reversed. The timing difference of

treatment of expenses or income as per book and tax provisions give rise to deferred tax assets

and deferred tax liabilities. Deferred taxes assets refer to those assets are created to reduce the

future tax liabilities. It means company has to pay more taxes in current year and can avail future

tax credits on them. Deferred tax liabilities refer to those tax liabilities that are due in current

year but they are not paid or subsequent paid after the due date. This the reason why deferred tax

assets are recognised in balance sheet as there is reasonable confirmation that company will

realize these assets in subsequent year. While deferred tax liabilities are due to be paid in

subsequent year that create obligation on management to recognize as liabilities in balance sheet

(Brigham and Houston, 2012).

(Annual report 2017: Telstra Corporation)

The difference in book profit and taxable profits give rise to timing differences and it can

be temporary or permanent in nature. The temporary timing differences are capable for reversing

in any subsequent year while permanent differences cannot be reversed. The timing difference of

treatment of expenses or income as per book and tax provisions give rise to deferred tax assets

and deferred tax liabilities. Deferred taxes assets refer to those assets are created to reduce the

future tax liabilities. It means company has to pay more taxes in current year and can avail future

tax credits on them. Deferred tax liabilities refer to those tax liabilities that are due in current

year but they are not paid or subsequent paid after the due date. This the reason why deferred tax

assets are recognised in balance sheet as there is reasonable confirmation that company will

realize these assets in subsequent year. While deferred tax liabilities are due to be paid in

subsequent year that create obligation on management to recognize as liabilities in balance sheet

(Brigham and Houston, 2012).

13

Section 3.4: Current tax assets or income tax payable as reported in the balance sheet

The current tax payable reported by the Telstra in the statement of financial position was

$161 million for year 2017 and $176 million for year 2016. The amount of tax payable and tax

expense is not same because current tax payable represent the tax due to tax authorities while tax

expense shows the balance of tax calculated as per accounting policies and it also includes tax

payable (Annual report 2017: Telstra Corporation).

Section 3.5: Income tax expense and income tax paid

No, the income tax expenses shown in income statement is not same as income tax paid

reported in the cash flow statement because tax paid shown in cash flow statement represent that

cash outflow that has been actually paid to tax authorities and it can be related to previous year

or current year as well (Firer, 2012).

Section 3.6: Self learning from the accounting of taxes

It found very confusing the treatment of deferred tax assets and deferred tax liabilities by

Telstra and also it is interesting to that tax treatment done in normal accounting situation is

totally different from tax treatment as per tax provisions (Annual report 2017: Telstra

Corporation).

Conclusion

Understanding the financial statement of the company is very difficult task and it requires

high level of knowledge to extract the exact information required. In this report financial

information of Telstra has been examined from various points.

Section 3.4: Current tax assets or income tax payable as reported in the balance sheet

The current tax payable reported by the Telstra in the statement of financial position was

$161 million for year 2017 and $176 million for year 2016. The amount of tax payable and tax

expense is not same because current tax payable represent the tax due to tax authorities while tax

expense shows the balance of tax calculated as per accounting policies and it also includes tax

payable (Annual report 2017: Telstra Corporation).

Section 3.5: Income tax expense and income tax paid

No, the income tax expenses shown in income statement is not same as income tax paid

reported in the cash flow statement because tax paid shown in cash flow statement represent that

cash outflow that has been actually paid to tax authorities and it can be related to previous year

or current year as well (Firer, 2012).

Section 3.6: Self learning from the accounting of taxes

It found very confusing the treatment of deferred tax assets and deferred tax liabilities by

Telstra and also it is interesting to that tax treatment done in normal accounting situation is

totally different from tax treatment as per tax provisions (Annual report 2017: Telstra

Corporation).

Conclusion

Understanding the financial statement of the company is very difficult task and it requires

high level of knowledge to extract the exact information required. In this report financial

information of Telstra has been examined from various points.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

14

References

Annual Report 2016. Telstra Corporation. [Online]. Available at:

https://www.telstra.com.au/content/dam/tcom/about-us/investors/pdf-e/FY16-Annual-Report.pdf

[Accessed on: 23 May, 2018].

Annual report 2017. Telstra Corporation. [Online]. Available at:

https://www.telstra.com.au/content/dam/tcom/about-us/investors/pdf-e/Annual-Report-2017.PDF

[Accessed on: 23 May, 2018].

Arnold, G., 2013. Corporate financial management. Pearson Higher Ed.

Baker, H.K. and Nofsinger, J.R. 2010. Behavioral Finance: Investors, Corporations, and

Markets. John Wiley & Sons.

Brealey, R., Myers, S.C. and Marcus, A.J., 2007. Fundamentals of Corporate Finance. Mc Graw

Hill, New York.

Brigham, F., and Houston.J. 2012. Fundamentals of financial management. Cengage Learning.

Deegan, C., 2013. Financial accounting theory. McGraw-Hill Education Australia.

FIRER, C. et al. 2012. Fundamentals of Corporate Finance. 5th Edition. Berkshire.McGraw-Hill

Companies, Inc.

References

Annual Report 2016. Telstra Corporation. [Online]. Available at:

https://www.telstra.com.au/content/dam/tcom/about-us/investors/pdf-e/FY16-Annual-Report.pdf

[Accessed on: 23 May, 2018].

Annual report 2017. Telstra Corporation. [Online]. Available at:

https://www.telstra.com.au/content/dam/tcom/about-us/investors/pdf-e/Annual-Report-2017.PDF

[Accessed on: 23 May, 2018].

Arnold, G., 2013. Corporate financial management. Pearson Higher Ed.

Baker, H.K. and Nofsinger, J.R. 2010. Behavioral Finance: Investors, Corporations, and

Markets. John Wiley & Sons.

Brealey, R., Myers, S.C. and Marcus, A.J., 2007. Fundamentals of Corporate Finance. Mc Graw

Hill, New York.

Brigham, F., and Houston.J. 2012. Fundamentals of financial management. Cengage Learning.

Deegan, C., 2013. Financial accounting theory. McGraw-Hill Education Australia.

FIRER, C. et al. 2012. Fundamentals of Corporate Finance. 5th Edition. Berkshire.McGraw-Hill

Companies, Inc.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.