University Financial Analysis: Tesco Plc Performance and F Score

VerifiedAdded on 2022/08/22

|6

|887

|10

Report

AI Summary

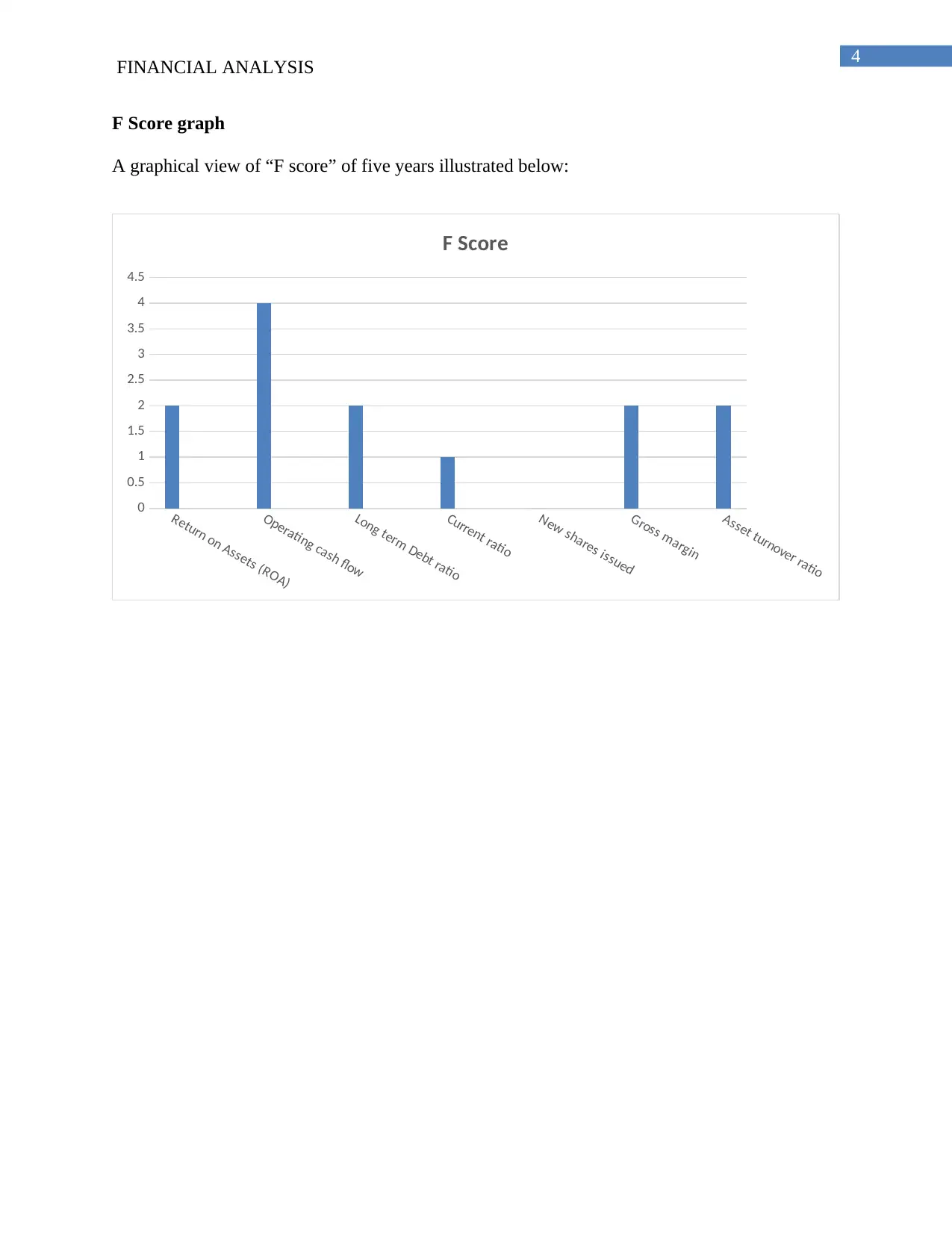

This report presents a financial analysis of Tesco Plc, evaluating its performance using various financial metrics and the F score. The introduction explains the concept of the F score, a measure of accuracy used in financial analysis. The analysis covers profitability ratios, including return on assets (ROA), operating cash flow, leverage, liquidity, and operating ratios. The report assesses Tesco's performance over several years, providing F scores for each metric based on its trend. The analysis highlights key findings, such as the company's ability to utilize assets, cash generation from operating activities, and debt levels. The conclusion summarizes the company's financial health based on the analysis and F score calculations, supported by references to relevant financial literature and a graphical representation of the F score trends over five years.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.