Activity-Based Costing (ABC) Advantages and Disadvantages

VerifiedAdded on 2020/02/24

|9

|2796

|35

AI Summary

This assignment delves into the concept of Activity-Based Costing (ABC), examining its advantages and disadvantages. It highlights the importance of accurately allocating costs to products or services, emphasizing the potential for improved profitability through precise pricing strategies. The discussion also touches upon the limitations of ABC, such as the time and resources required for implementation, and the challenges associated with capturing all relevant activities within a business.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGEMENT ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

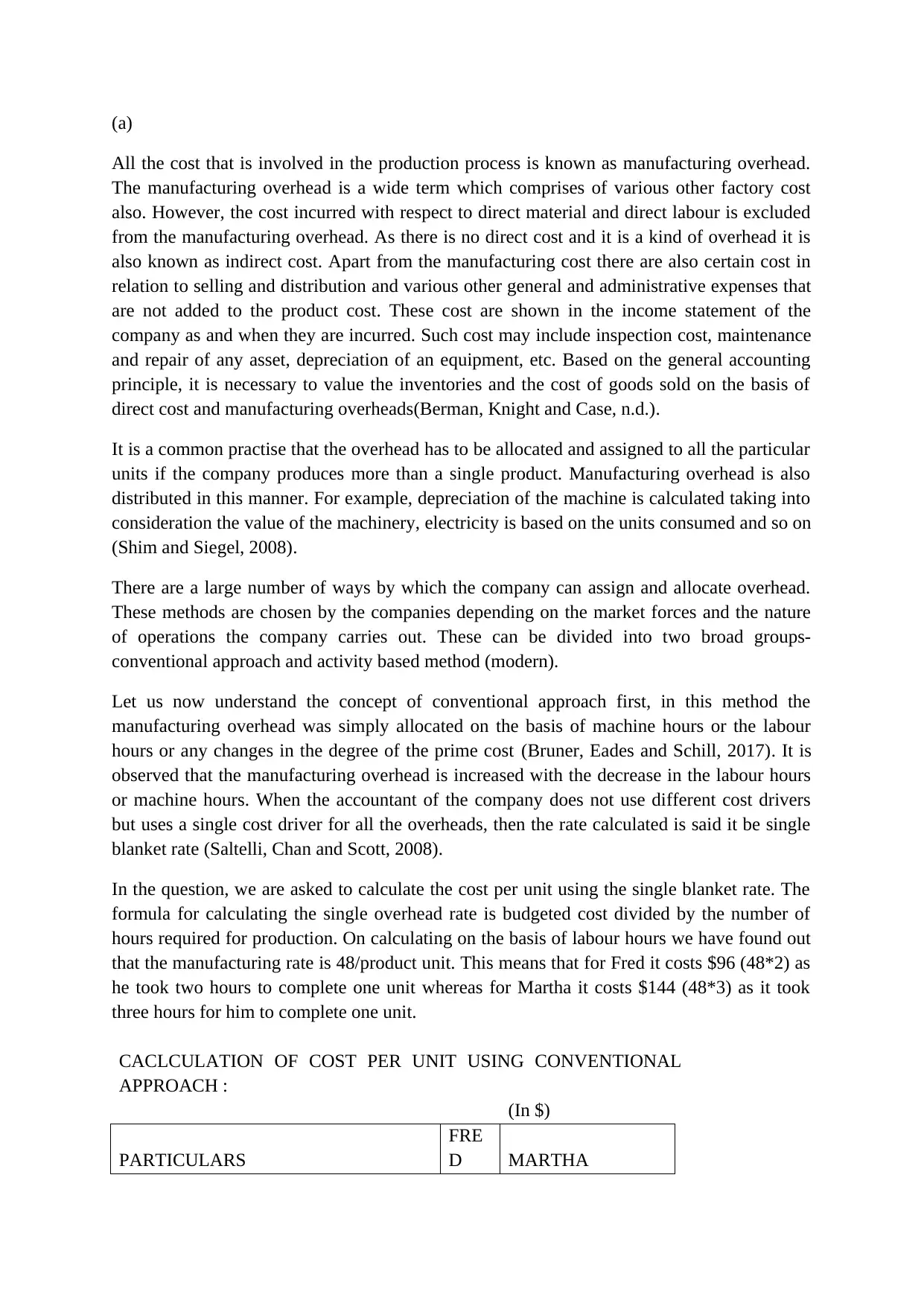

(a)

All the cost that is involved in the production process is known as manufacturing overhead.

The manufacturing overhead is a wide term which comprises of various other factory cost

also. However, the cost incurred with respect to direct material and direct labour is excluded

from the manufacturing overhead. As there is no direct cost and it is a kind of overhead it is

also known as indirect cost. Apart from the manufacturing cost there are also certain cost in

relation to selling and distribution and various other general and administrative expenses that

are not added to the product cost. These cost are shown in the income statement of the

company as and when they are incurred. Such cost may include inspection cost, maintenance

and repair of any asset, depreciation of an equipment, etc. Based on the general accounting

principle, it is necessary to value the inventories and the cost of goods sold on the basis of

direct cost and manufacturing overheads(Berman, Knight and Case, n.d.).

It is a common practise that the overhead has to be allocated and assigned to all the particular

units if the company produces more than a single product. Manufacturing overhead is also

distributed in this manner. For example, depreciation of the machine is calculated taking into

consideration the value of the machinery, electricity is based on the units consumed and so on

(Shim and Siegel, 2008).

There are a large number of ways by which the company can assign and allocate overhead.

These methods are chosen by the companies depending on the market forces and the nature

of operations the company carries out. These can be divided into two broad groups-

conventional approach and activity based method (modern).

Let us now understand the concept of conventional approach first, in this method the

manufacturing overhead was simply allocated on the basis of machine hours or the labour

hours or any changes in the degree of the prime cost (Bruner, Eades and Schill, 2017). It is

observed that the manufacturing overhead is increased with the decrease in the labour hours

or machine hours. When the accountant of the company does not use different cost drivers

but uses a single cost driver for all the overheads, then the rate calculated is said it be single

blanket rate (Saltelli, Chan and Scott, 2008).

In the question, we are asked to calculate the cost per unit using the single blanket rate. The

formula for calculating the single overhead rate is budgeted cost divided by the number of

hours required for production. On calculating on the basis of labour hours we have found out

that the manufacturing rate is 48/product unit. This means that for Fred it costs $96 (48*2) as

he took two hours to complete one unit whereas for Martha it costs $144 (48*3) as it took

three hours for him to complete one unit.

CACLCULATION OF COST PER UNIT USING CONVENTIONAL

APPROACH :

(In $)

PARTICULARS

FRE

D MARTHA

All the cost that is involved in the production process is known as manufacturing overhead.

The manufacturing overhead is a wide term which comprises of various other factory cost

also. However, the cost incurred with respect to direct material and direct labour is excluded

from the manufacturing overhead. As there is no direct cost and it is a kind of overhead it is

also known as indirect cost. Apart from the manufacturing cost there are also certain cost in

relation to selling and distribution and various other general and administrative expenses that

are not added to the product cost. These cost are shown in the income statement of the

company as and when they are incurred. Such cost may include inspection cost, maintenance

and repair of any asset, depreciation of an equipment, etc. Based on the general accounting

principle, it is necessary to value the inventories and the cost of goods sold on the basis of

direct cost and manufacturing overheads(Berman, Knight and Case, n.d.).

It is a common practise that the overhead has to be allocated and assigned to all the particular

units if the company produces more than a single product. Manufacturing overhead is also

distributed in this manner. For example, depreciation of the machine is calculated taking into

consideration the value of the machinery, electricity is based on the units consumed and so on

(Shim and Siegel, 2008).

There are a large number of ways by which the company can assign and allocate overhead.

These methods are chosen by the companies depending on the market forces and the nature

of operations the company carries out. These can be divided into two broad groups-

conventional approach and activity based method (modern).

Let us now understand the concept of conventional approach first, in this method the

manufacturing overhead was simply allocated on the basis of machine hours or the labour

hours or any changes in the degree of the prime cost (Bruner, Eades and Schill, 2017). It is

observed that the manufacturing overhead is increased with the decrease in the labour hours

or machine hours. When the accountant of the company does not use different cost drivers

but uses a single cost driver for all the overheads, then the rate calculated is said it be single

blanket rate (Saltelli, Chan and Scott, 2008).

In the question, we are asked to calculate the cost per unit using the single blanket rate. The

formula for calculating the single overhead rate is budgeted cost divided by the number of

hours required for production. On calculating on the basis of labour hours we have found out

that the manufacturing rate is 48/product unit. This means that for Fred it costs $96 (48*2) as

he took two hours to complete one unit whereas for Martha it costs $144 (48*3) as it took

three hours for him to complete one unit.

CACLCULATION OF COST PER UNIT USING CONVENTIONAL

APPROACH :

(In $)

PARTICULARS

FRE

D MARTHA

Production units 1000 5000

Direct materials 40 60

Direct labours 30 45

Manufacturing overheads 96 144

Total Cost Per Unit 166 249

Notes :

Total Manufacturing Costs $8,16,000

Total Hours Required 17000 hours

(1000 units of Fred *2 + 5000 units of

Martha*3 hours)

Manufacturing Overhead Per Hour =

Total Manufacturing

Costs

Total Hours

Manufacturing Overhead Per Hour = 816000

17000

=$48/hour

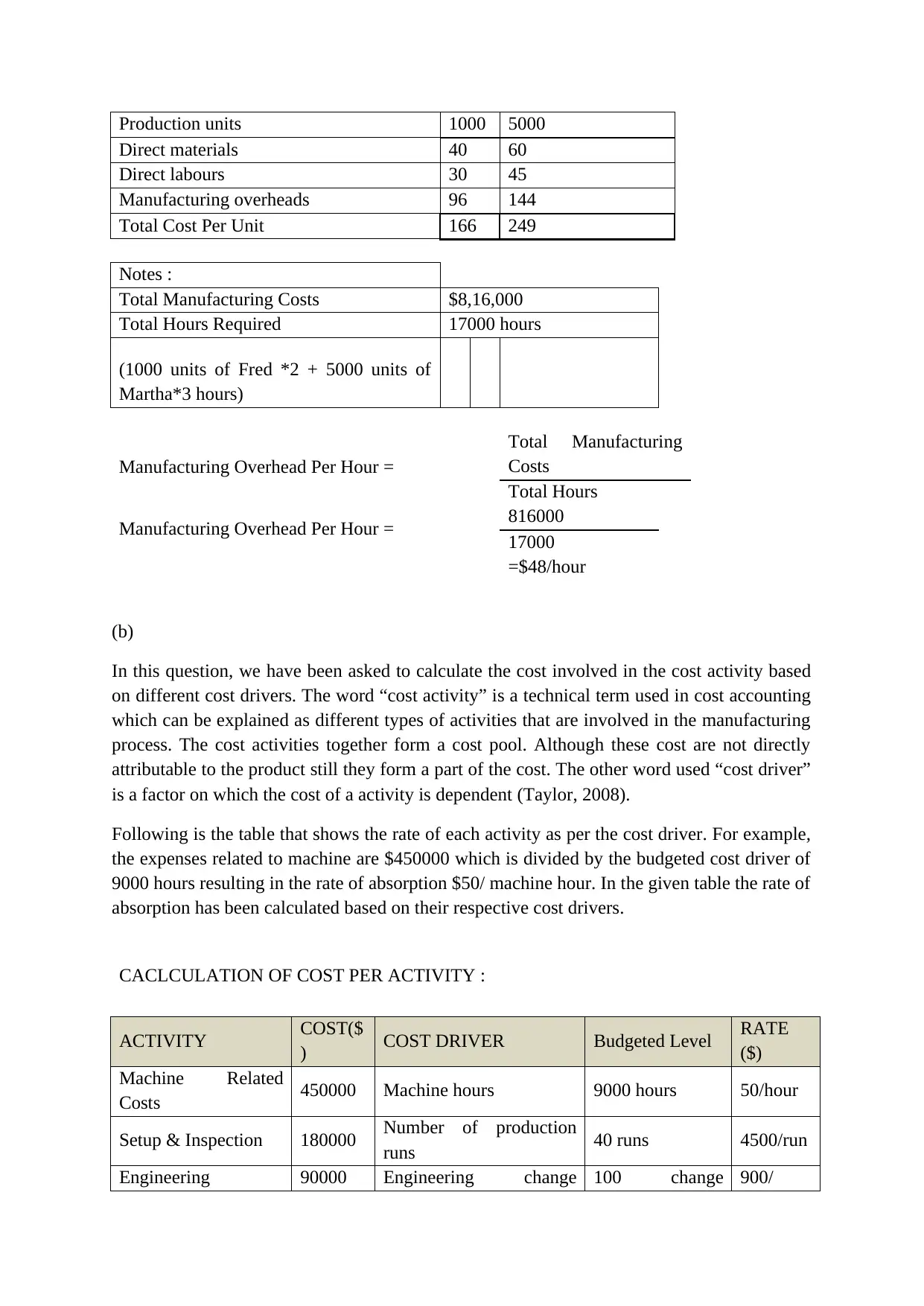

(b)

In this question, we have been asked to calculate the cost involved in the cost activity based

on different cost drivers. The word “cost activity” is a technical term used in cost accounting

which can be explained as different types of activities that are involved in the manufacturing

process. The cost activities together form a cost pool. Although these cost are not directly

attributable to the product still they form a part of the cost. The other word used “cost driver”

is a factor on which the cost of a activity is dependent (Taylor, 2008).

Following is the table that shows the rate of each activity as per the cost driver. For example,

the expenses related to machine are $450000 which is divided by the budgeted cost driver of

9000 hours resulting in the rate of absorption $50/ machine hour. In the given table the rate of

absorption has been calculated based on their respective cost drivers.

CACLCULATION OF COST PER ACTIVITY :

ACTIVITY COST($

) COST DRIVER Budgeted Level RATE

($)

Machine Related

Costs 450000 Machine hours 9000 hours 50/hour

Setup & Inspection 180000 Number of production

runs 40 runs 4500/run

Engineering 90000 Engineering change 100 change 900/

Direct materials 40 60

Direct labours 30 45

Manufacturing overheads 96 144

Total Cost Per Unit 166 249

Notes :

Total Manufacturing Costs $8,16,000

Total Hours Required 17000 hours

(1000 units of Fred *2 + 5000 units of

Martha*3 hours)

Manufacturing Overhead Per Hour =

Total Manufacturing

Costs

Total Hours

Manufacturing Overhead Per Hour = 816000

17000

=$48/hour

(b)

In this question, we have been asked to calculate the cost involved in the cost activity based

on different cost drivers. The word “cost activity” is a technical term used in cost accounting

which can be explained as different types of activities that are involved in the manufacturing

process. The cost activities together form a cost pool. Although these cost are not directly

attributable to the product still they form a part of the cost. The other word used “cost driver”

is a factor on which the cost of a activity is dependent (Taylor, 2008).

Following is the table that shows the rate of each activity as per the cost driver. For example,

the expenses related to machine are $450000 which is divided by the budgeted cost driver of

9000 hours resulting in the rate of absorption $50/ machine hour. In the given table the rate of

absorption has been calculated based on their respective cost drivers.

CACLCULATION OF COST PER ACTIVITY :

ACTIVITY COST($

) COST DRIVER Budgeted Level RATE

($)

Machine Related

Costs 450000 Machine hours 9000 hours 50/hour

Setup & Inspection 180000 Number of production

runs 40 runs 4500/run

Engineering 90000 Engineering change 100 change 900/

orders orders order

Plant Related Costs 96000 Square footage of space 1920 sq. ft. 50/sq.ft

TOTAL 816000

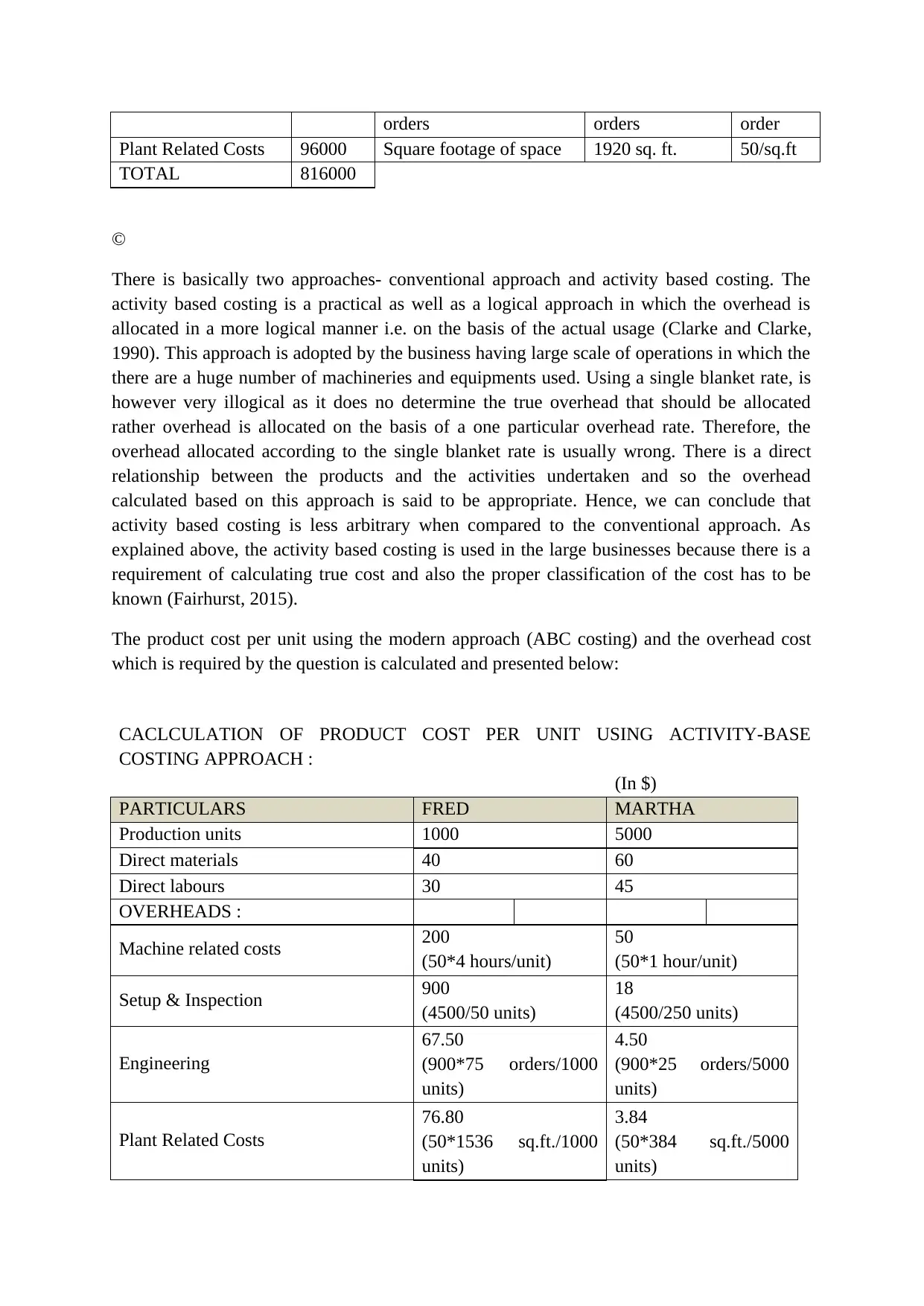

©

There is basically two approaches- conventional approach and activity based costing. The

activity based costing is a practical as well as a logical approach in which the overhead is

allocated in a more logical manner i.e. on the basis of the actual usage (Clarke and Clarke,

1990). This approach is adopted by the business having large scale of operations in which the

there are a huge number of machineries and equipments used. Using a single blanket rate, is

however very illogical as it does no determine the true overhead that should be allocated

rather overhead is allocated on the basis of a one particular overhead rate. Therefore, the

overhead allocated according to the single blanket rate is usually wrong. There is a direct

relationship between the products and the activities undertaken and so the overhead

calculated based on this approach is said to be appropriate. Hence, we can conclude that

activity based costing is less arbitrary when compared to the conventional approach. As

explained above, the activity based costing is used in the large businesses because there is a

requirement of calculating true cost and also the proper classification of the cost has to be

known (Fairhurst, 2015).

The product cost per unit using the modern approach (ABC costing) and the overhead cost

which is required by the question is calculated and presented below:

CACLCULATION OF PRODUCT COST PER UNIT USING ACTIVITY-BASE

COSTING APPROACH :

(In $)

PARTICULARS FRED MARTHA

Production units 1000 5000

Direct materials 40 60

Direct labours 30 45

OVERHEADS :

Machine related costs 200

(50*4 hours/unit)

50

(50*1 hour/unit)

Setup & Inspection 900

(4500/50 units)

18

(4500/250 units)

Engineering

67.50

(900*75 orders/1000

units)

4.50

(900*25 orders/5000

units)

Plant Related Costs

76.80

(50*1536 sq.ft./1000

units)

3.84

(50*384 sq.ft./5000

units)

Plant Related Costs 96000 Square footage of space 1920 sq. ft. 50/sq.ft

TOTAL 816000

©

There is basically two approaches- conventional approach and activity based costing. The

activity based costing is a practical as well as a logical approach in which the overhead is

allocated in a more logical manner i.e. on the basis of the actual usage (Clarke and Clarke,

1990). This approach is adopted by the business having large scale of operations in which the

there are a huge number of machineries and equipments used. Using a single blanket rate, is

however very illogical as it does no determine the true overhead that should be allocated

rather overhead is allocated on the basis of a one particular overhead rate. Therefore, the

overhead allocated according to the single blanket rate is usually wrong. There is a direct

relationship between the products and the activities undertaken and so the overhead

calculated based on this approach is said to be appropriate. Hence, we can conclude that

activity based costing is less arbitrary when compared to the conventional approach. As

explained above, the activity based costing is used in the large businesses because there is a

requirement of calculating true cost and also the proper classification of the cost has to be

known (Fairhurst, 2015).

The product cost per unit using the modern approach (ABC costing) and the overhead cost

which is required by the question is calculated and presented below:

CACLCULATION OF PRODUCT COST PER UNIT USING ACTIVITY-BASE

COSTING APPROACH :

(In $)

PARTICULARS FRED MARTHA

Production units 1000 5000

Direct materials 40 60

Direct labours 30 45

OVERHEADS :

Machine related costs 200

(50*4 hours/unit)

50

(50*1 hour/unit)

Setup & Inspection 900

(4500/50 units)

18

(4500/250 units)

Engineering

67.50

(900*75 orders/1000

units)

4.50

(900*25 orders/5000

units)

Plant Related Costs

76.80

(50*1536 sq.ft./1000

units)

3.84

(50*384 sq.ft./5000

units)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TOTAL COST PER UNIT 504.3 181.34

(d)

The price per unit of Fred was $199.20 whereas the price per unit of Martha was $298.8

when the firm was pricing its product @ 120% of the total manufacturing cost i.e. when it

was selling its products at a margin of 20%. Earlier, the cost was calculated based on the

conventional approach but after calculating the cost as per activity based costing, the product

cost will be as follows (it will still price it product @120% of the manufacturing cost)

(Galbraith, Downey and Kates, 2002)-

Price per unit of Fred = 120%*504.30= $605.16 per unit.

Price per unit of Martha= 120%*181.34= $217.60 per unit.

After this calculation is made , it has been observed that the profit of Fred has increased from

$33.20 per unit to $100.86 per unit whereas the profit of Martha has fallen from $49.80 per

unit to $36.28 per unit on adopting the ABC approach.

(e)

According to the conventional approach of costing, the overhead is allocated on the basis of

the volume of production. These may be dependent on the volume of the production hours or

even the machine hours consumed. Let us consider an example to understand this better,

suppose there is a small manufacture whose volume of production is a little low but there is a

huge expenditure of engineering cost, inspection cost, setup cost etc. If the manufacturer

directly allocates the overhead on the basis of production hours then the result derived from it

may be not reliable and may mislead them (Galbraith, Downey and Kates, 2002). This

approach is usually adopted by the manufacturers whose scale of operations is simple and

there are very less number of activities in which it is engaged. In such a situation where there

is no complexity, a manufacturer may use the single blanket overhead rate for valuation. In

case the manufacture is engaged in a number of complex activities, then it should not go for

conventional approach rather separate cost drivers is developed in order to carry out proper

valuation. If the overhead rate is wrongly charged from the customer then there may be arise

in price which could harm the business, therefore the decision of the management in regards

to selection of the method should be taken very carefully (TULSIAN, 2016). The

conventional approach prevents the true and fair presentation of cost of resource consumed

by the final product.

Conventional approach splits the total cost in two categories i.e. fixed cost as well as variable

cost which is not considered realistic in the case when the business grows. This approach is

not favourable for the manufacturing sectors as the valuation done by them is based on the

degree of completion (Holland and Torregrosa, 2008).

(d)

The price per unit of Fred was $199.20 whereas the price per unit of Martha was $298.8

when the firm was pricing its product @ 120% of the total manufacturing cost i.e. when it

was selling its products at a margin of 20%. Earlier, the cost was calculated based on the

conventional approach but after calculating the cost as per activity based costing, the product

cost will be as follows (it will still price it product @120% of the manufacturing cost)

(Galbraith, Downey and Kates, 2002)-

Price per unit of Fred = 120%*504.30= $605.16 per unit.

Price per unit of Martha= 120%*181.34= $217.60 per unit.

After this calculation is made , it has been observed that the profit of Fred has increased from

$33.20 per unit to $100.86 per unit whereas the profit of Martha has fallen from $49.80 per

unit to $36.28 per unit on adopting the ABC approach.

(e)

According to the conventional approach of costing, the overhead is allocated on the basis of

the volume of production. These may be dependent on the volume of the production hours or

even the machine hours consumed. Let us consider an example to understand this better,

suppose there is a small manufacture whose volume of production is a little low but there is a

huge expenditure of engineering cost, inspection cost, setup cost etc. If the manufacturer

directly allocates the overhead on the basis of production hours then the result derived from it

may be not reliable and may mislead them (Galbraith, Downey and Kates, 2002). This

approach is usually adopted by the manufacturers whose scale of operations is simple and

there are very less number of activities in which it is engaged. In such a situation where there

is no complexity, a manufacturer may use the single blanket overhead rate for valuation. In

case the manufacture is engaged in a number of complex activities, then it should not go for

conventional approach rather separate cost drivers is developed in order to carry out proper

valuation. If the overhead rate is wrongly charged from the customer then there may be arise

in price which could harm the business, therefore the decision of the management in regards

to selection of the method should be taken very carefully (TULSIAN, 2016). The

conventional approach prevents the true and fair presentation of cost of resource consumed

by the final product.

Conventional approach splits the total cost in two categories i.e. fixed cost as well as variable

cost which is not considered realistic in the case when the business grows. This approach is

not favourable for the manufacturing sectors as the valuation done by them is based on the

degree of completion (Holland and Torregrosa, 2008).

(f)

The advantages of adopting the activity based costing are as follows:

The activity based costing system helps the company to know its position to earn the

maximum margin of profit that it can earn. This analysis helps to determine the profits

that could be earned on the basis of different product lines, cost of the product and the

whole subsidiaries (Khan and Jain, 2014).

The activity based costing helps to evaluate and identify all the cost that will be

incurred if the firm takes the decision of in-house manufacturing. Therefore, it enables

to compare between the manufacturing and outsourcing and helps to take a decision

that would prove to be reasonable.

The segregation of the overhead at the plant wide level is considered to be better than

the cost of production between the different facilities.

All the cost incurred in the manufacturing process forms a part of the product cost,

some cost that are abnormal in nature also forms a part of the product cost such as

customer service cost, handling cost and others (Reilly and Brown, 2012). These cost

are then properly identified using the ABC approach and then it is seen whether the

customers are paying them sufficient profits.

The activity based costing enables a comparability between the cost incurred at

industry standards and the cost incurred individually by the firms. This helps the

company to have clear knowledge of the cost that is being incurred and the ways to

reduce the wasteful cost (Reilly and Brown, 2012).

(g)

The above advantages provide enough proof to say that the activity based costing is more

logical and reliable than the conventional approach. There are also certain limitations of the

activity based costing. They are-

1. There are a large number of cost pools used in this approach and therefore there is a

huge cost incurred in managing these cost pools. Therefore, we can say that although

this system has various advantages, it also expensive at the same time.

2. There Isa difficulty in the installation of the activity based costing system because the

system has to be installed across all the product lines and the facilities. The

installation requires an involvement of huge time which makes difficult for the

company to gain management support as well as budgetary support.

3. Activity based costing requires many relevant information from the various

departments of the company. As we know, the company has a large number of

departments therefore it becomes difficult to collect the input data.

4. ABC follows the project basis which means that the information is collected only

once and the such information is not used by any other operational situation other than

the current operational situation. Therefore, the ABC is used once and then it is

discarded.

5. It is a normal practise among the employees to report that the time spent on any

particular activity is equal to 100% of the time they have worked. But we all know

The advantages of adopting the activity based costing are as follows:

The activity based costing system helps the company to know its position to earn the

maximum margin of profit that it can earn. This analysis helps to determine the profits

that could be earned on the basis of different product lines, cost of the product and the

whole subsidiaries (Khan and Jain, 2014).

The activity based costing helps to evaluate and identify all the cost that will be

incurred if the firm takes the decision of in-house manufacturing. Therefore, it enables

to compare between the manufacturing and outsourcing and helps to take a decision

that would prove to be reasonable.

The segregation of the overhead at the plant wide level is considered to be better than

the cost of production between the different facilities.

All the cost incurred in the manufacturing process forms a part of the product cost,

some cost that are abnormal in nature also forms a part of the product cost such as

customer service cost, handling cost and others (Reilly and Brown, 2012). These cost

are then properly identified using the ABC approach and then it is seen whether the

customers are paying them sufficient profits.

The activity based costing enables a comparability between the cost incurred at

industry standards and the cost incurred individually by the firms. This helps the

company to have clear knowledge of the cost that is being incurred and the ways to

reduce the wasteful cost (Reilly and Brown, 2012).

(g)

The above advantages provide enough proof to say that the activity based costing is more

logical and reliable than the conventional approach. There are also certain limitations of the

activity based costing. They are-

1. There are a large number of cost pools used in this approach and therefore there is a

huge cost incurred in managing these cost pools. Therefore, we can say that although

this system has various advantages, it also expensive at the same time.

2. There Isa difficulty in the installation of the activity based costing system because the

system has to be installed across all the product lines and the facilities. The

installation requires an involvement of huge time which makes difficult for the

company to gain management support as well as budgetary support.

3. Activity based costing requires many relevant information from the various

departments of the company. As we know, the company has a large number of

departments therefore it becomes difficult to collect the input data.

4. ABC follows the project basis which means that the information is collected only

once and the such information is not used by any other operational situation other than

the current operational situation. Therefore, the ABC is used once and then it is

discarded.

5. It is a normal practise among the employees to report that the time spent on any

particular activity is equal to 100% of the time they have worked. But we all know

that they do not work 100% because there is a good idle time involved in it as well,

for example- lunch time, gossiping with the other employees, administrative

meetings, internet surfing and many more. In such a situation , the time for which they

have not actually worked also gets involved in the total time spent on an activity.

Therefore, we can draw a conclusion that even though ABC system has many advantage

it also has certain disadvantages. Now, it totally depends on the scale of operations as

well as the nature of business to decide the compliance of various standards and

principles. It is however important for every company whether small or large to give a

clear picture of the costs and to charge a correct price from the customers as they are

considered as the king of the business and no business can survive in the long run without

their support.

for example- lunch time, gossiping with the other employees, administrative

meetings, internet surfing and many more. In such a situation , the time for which they

have not actually worked also gets involved in the total time spent on an activity.

Therefore, we can draw a conclusion that even though ABC system has many advantage

it also has certain disadvantages. Now, it totally depends on the scale of operations as

well as the nature of business to decide the compliance of various standards and

principles. It is however important for every company whether small or large to give a

clear picture of the costs and to charge a correct price from the customers as they are

considered as the king of the business and no business can survive in the long run without

their support.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES:

Berman, K., Knight, J. and Case, J. (n.d.). Financial intelligence for HR professionals.

Bruner, R., Eades, K. and Schill, M. (2017). Case studies in finance. Dubuque, IA: McGraw-

Hill Education.

Clarke, R. and Clarke, R. (1990). Strategic financial management. Homewood, Ill.: R.D.

Irwin.

Fairhurst, D. (2015). Using Excel for Business Analysis A Guide to Financial Modelling

Fundamenta. John Wiley & Sons.

Galbraith, J., Downey, D. and Kates, A. (2002). Designing dynamic organizations. New

York: AMACOM.

Hassani, B. (2016). Scenario analysis in risk management. Cham: Springer International

Publishing.

Holland, J. and Torregrosa, D. (2008). Capital budgeting. [Washington, D.C.]: Congress of

the U.S., Congressional Budget Office.

Khan, M. and Jain, P. (2014). Financial management. New Delhi: McGraw Hill Education.

Palepu, K., Healy, P. and Peek, E. (2016). Business analysis and valuation. Andover,

Hampshire, United Kingdom: Cengage Learning EMEA.

Phillips, J. (2014). Capm / pmp. New York: McGraw Hill.

Reilly, F. and Brown, K. (2012). Investment analysis & portfolio management. Mason, OH:

South-Western Cengage Learning.

Saltelli, A., Chan, K. and Scott, E. (2008). Sensitivity analysis. Chichester: John Wiley &

Sons, Ltd.

Saunders, A. and Cornett, M. (2017). Financial institutions management. New York:

McGraw-Hill Education.

Shim, J. and Siegel, J. (2008). Financial management. Hauppauge, N.Y.: Barron's

Educational Series.

Taylor, S. (2008). Modelling financial time series. New Jersey: World Scientific.

TULSIAN, B. (2016). TULSIAN'S FINANCIAL MANAGEMENT FOR CA-IPC (GROUP-I).

[S.l.]: S CHAND & CO LTD.

Berman, K., Knight, J. and Case, J. (n.d.). Financial intelligence for HR professionals.

Bruner, R., Eades, K. and Schill, M. (2017). Case studies in finance. Dubuque, IA: McGraw-

Hill Education.

Clarke, R. and Clarke, R. (1990). Strategic financial management. Homewood, Ill.: R.D.

Irwin.

Fairhurst, D. (2015). Using Excel for Business Analysis A Guide to Financial Modelling

Fundamenta. John Wiley & Sons.

Galbraith, J., Downey, D. and Kates, A. (2002). Designing dynamic organizations. New

York: AMACOM.

Hassani, B. (2016). Scenario analysis in risk management. Cham: Springer International

Publishing.

Holland, J. and Torregrosa, D. (2008). Capital budgeting. [Washington, D.C.]: Congress of

the U.S., Congressional Budget Office.

Khan, M. and Jain, P. (2014). Financial management. New Delhi: McGraw Hill Education.

Palepu, K., Healy, P. and Peek, E. (2016). Business analysis and valuation. Andover,

Hampshire, United Kingdom: Cengage Learning EMEA.

Phillips, J. (2014). Capm / pmp. New York: McGraw Hill.

Reilly, F. and Brown, K. (2012). Investment analysis & portfolio management. Mason, OH:

South-Western Cengage Learning.

Saltelli, A., Chan, K. and Scott, E. (2008). Sensitivity analysis. Chichester: John Wiley &

Sons, Ltd.

Saunders, A. and Cornett, M. (2017). Financial institutions management. New York:

McGraw-Hill Education.

Shim, J. and Siegel, J. (2008). Financial management. Hauppauge, N.Y.: Barron's

Educational Series.

Taylor, S. (2008). Modelling financial time series. New Jersey: World Scientific.

TULSIAN, B. (2016). TULSIAN'S FINANCIAL MANAGEMENT FOR CA-IPC (GROUP-I).

[S.l.]: S CHAND & CO LTD.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.