Management Accounting: Variance Analysis and Decision Making

VerifiedAdded on 2023/01/09

|12

|3395

|78

AI Summary

This document provides an overview of variance analysis in management accounting and its impact on decision making. It covers topics such as sales price and sales volume contribution variance, material price planning and operational variance, and the advantages and disadvantages of using variances. The case study of XLG is included to illustrate the concepts discussed.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

PART A...........................................................................................................................................3

Sales price and sales volume contribution variance....................................................................3

Material price planning and material price operational variance................................................5

Advantages and disadvantages of using variances......................................................................7

PART B...........................................................................................................................................9

Assessment of the make or buy decision for XLG......................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

PART A...........................................................................................................................................3

Sales price and sales volume contribution variance....................................................................3

Material price planning and material price operational variance................................................5

Advantages and disadvantages of using variances......................................................................7

PART B...........................................................................................................................................9

Assessment of the make or buy decision for XLG......................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

Management accounting is a very broad field that involves the overall management and

preparation of the different aspects associated with the costing etc. In this field, variance

analysis is of key importance that adds in the overall value of the business. The difference

between the standards that were set and the actual that is achieved is basically computed in

variance analysis (Rosyidi, 2019). In this report, the case study of XLG will be evaluated in

context of the different variances whose implementation will help in decision making. Further

the positive and negative aspects of using variance analysis will also be illustrated in the report.

MAIN BODY

PART A

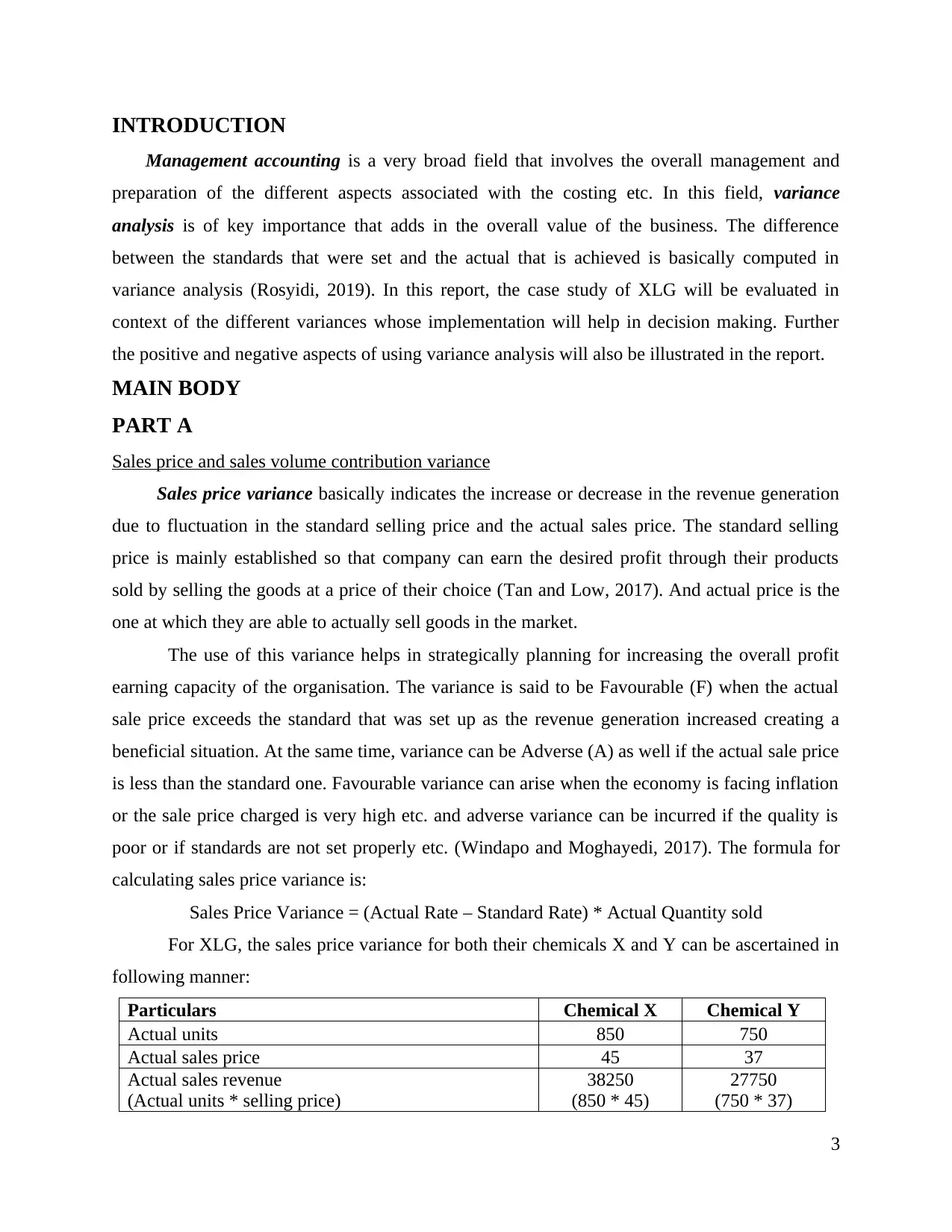

Sales price and sales volume contribution variance

Sales price variance basically indicates the increase or decrease in the revenue generation

due to fluctuation in the standard selling price and the actual sales price. The standard selling

price is mainly established so that company can earn the desired profit through their products

sold by selling the goods at a price of their choice (Tan and Low, 2017). And actual price is the

one at which they are able to actually sell goods in the market.

The use of this variance helps in strategically planning for increasing the overall profit

earning capacity of the organisation. The variance is said to be Favourable (F) when the actual

sale price exceeds the standard that was set up as the revenue generation increased creating a

beneficial situation. At the same time, variance can be Adverse (A) as well if the actual sale price

is less than the standard one. Favourable variance can arise when the economy is facing inflation

or the sale price charged is very high etc. and adverse variance can be incurred if the quality is

poor or if standards are not set properly etc. (Windapo and Moghayedi, 2017). The formula for

calculating sales price variance is:

Sales Price Variance = (Actual Rate – Standard Rate) * Actual Quantity sold

For XLG, the sales price variance for both their chemicals X and Y can be ascertained in

following manner:

Particulars Chemical X Chemical Y

Actual units 850 750

Actual sales price 45 37

Actual sales revenue

(Actual units * selling price)

38250

(850 * 45)

27750

(750 * 37)

3

Management accounting is a very broad field that involves the overall management and

preparation of the different aspects associated with the costing etc. In this field, variance

analysis is of key importance that adds in the overall value of the business. The difference

between the standards that were set and the actual that is achieved is basically computed in

variance analysis (Rosyidi, 2019). In this report, the case study of XLG will be evaluated in

context of the different variances whose implementation will help in decision making. Further

the positive and negative aspects of using variance analysis will also be illustrated in the report.

MAIN BODY

PART A

Sales price and sales volume contribution variance

Sales price variance basically indicates the increase or decrease in the revenue generation

due to fluctuation in the standard selling price and the actual sales price. The standard selling

price is mainly established so that company can earn the desired profit through their products

sold by selling the goods at a price of their choice (Tan and Low, 2017). And actual price is the

one at which they are able to actually sell goods in the market.

The use of this variance helps in strategically planning for increasing the overall profit

earning capacity of the organisation. The variance is said to be Favourable (F) when the actual

sale price exceeds the standard that was set up as the revenue generation increased creating a

beneficial situation. At the same time, variance can be Adverse (A) as well if the actual sale price

is less than the standard one. Favourable variance can arise when the economy is facing inflation

or the sale price charged is very high etc. and adverse variance can be incurred if the quality is

poor or if standards are not set properly etc. (Windapo and Moghayedi, 2017). The formula for

calculating sales price variance is:

Sales Price Variance = (Actual Rate – Standard Rate) * Actual Quantity sold

For XLG, the sales price variance for both their chemicals X and Y can be ascertained in

following manner:

Particulars Chemical X Chemical Y

Actual units 850 750

Actual sales price 45 37

Actual sales revenue

(Actual units * selling price)

38250

(850 * 45)

27750

(750 * 37)

3

Standard price 35 30

Deviation in price

(Actual price – Standard price)

10

(45 – 35)

7

(37 – 30)

Actual units 850 750

Sales price variance

(Deviation in price * Actual units)

8500

(850 * 10)

5250

(750 * 7)

Total sales price variance (8500 + 5250) 13750 (F)

The tabulation above indicates that the total sale price variance for XLG is £13750 in

favourable position i.e. company is in a profitable situation and they have been able to do so

because the actual sale price is higher than the standard one.

Sales Volume contribution variance can be used to identify the differences in the

contribution i.e. profit that is earned by an organisation due to difference between the actual sales

and the estimates sales volume i.e. quantity. This variance actually helps in ascertaining that how

the variation in sales volume can actually affect the overall profits (Bai, 2016). There are two

methods of evaluating this variance i.e. to use absorption costing method by calculation of per

unit profit or by using marginal costing where the standard contribution on a per unit basis is

ascertained.

The favourable variance situation can arise when the total units sold are higher than the

budgeted ones and this can be due to increased demand, better quality of services etc. The

adverse variance can arise when the demand is not very high or when there is a better

competitive product etc. (Farkas, Kersting and Stephens, 2016). The formula that can be used to

calculate the sale volume contribution variance can be calculated as follows:

Sales volume contribution variance = (Actual Sales Units – Budgeted Sales Units) * Standard

margin

In consideration of the XLG Company, the statement for sales contribution variance can

be ascertained in following manner:

Particulars Chemical X Chemical Y

Actual sales units 850 750

Budgeted sales units 595 595

Difference

255

(850 – 595)

155

(750 – 595)

Standard margin 25 20

Sales volume variance

6375

(255 * 25)

3100

(155 * 20)

4

Deviation in price

(Actual price – Standard price)

10

(45 – 35)

7

(37 – 30)

Actual units 850 750

Sales price variance

(Deviation in price * Actual units)

8500

(850 * 10)

5250

(750 * 7)

Total sales price variance (8500 + 5250) 13750 (F)

The tabulation above indicates that the total sale price variance for XLG is £13750 in

favourable position i.e. company is in a profitable situation and they have been able to do so

because the actual sale price is higher than the standard one.

Sales Volume contribution variance can be used to identify the differences in the

contribution i.e. profit that is earned by an organisation due to difference between the actual sales

and the estimates sales volume i.e. quantity. This variance actually helps in ascertaining that how

the variation in sales volume can actually affect the overall profits (Bai, 2016). There are two

methods of evaluating this variance i.e. to use absorption costing method by calculation of per

unit profit or by using marginal costing where the standard contribution on a per unit basis is

ascertained.

The favourable variance situation can arise when the total units sold are higher than the

budgeted ones and this can be due to increased demand, better quality of services etc. The

adverse variance can arise when the demand is not very high or when there is a better

competitive product etc. (Farkas, Kersting and Stephens, 2016). The formula that can be used to

calculate the sale volume contribution variance can be calculated as follows:

Sales volume contribution variance = (Actual Sales Units – Budgeted Sales Units) * Standard

margin

In consideration of the XLG Company, the statement for sales contribution variance can

be ascertained in following manner:

Particulars Chemical X Chemical Y

Actual sales units 850 750

Budgeted sales units 595 595

Difference

255

(850 – 595)

155

(750 – 595)

Standard margin 25 20

Sales volume variance

6375

(255 * 25)

3100

(155 * 20)

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Total sales volume contribution variance 9475 (F)

Therefore, the above calculation indicates that the overall sale volume contribution

variance for the XLG Company is favourable with £9475 and this is mainly due to the increased

number of units sold for both the chemicals than the expected ones.

Material price planning and material price operational variance

The material price variances are instrumental in ascertaining that how effectively and

correctly can the future prices of the product be estimated by the managers (Marzlin Marzuki and

Ismail, 2019). The material price planning variance indicates the effectiveness of the overall

planning of the managers where the comparison is made between the original budget developed

and the revised budget developed in realistic manner. This variance helps in ascertaining that

how effective was the planning earlier and also identifies the need to have a revised budget when

the existing budget is not in accordance with the current market conditions that are prevalent.

This is generally done when the standard that has been set was not in anticipation of the future

conditions or when some unforeseeable future condition arises that could not have been easily

predicted. The favourable planning variance can arise when the general market prices are higher

than the original prices that were set up and this can be due to increase in the requirement of the

product, change in market conditions etc. The adverse variance can arise when the original prices

are higher than the general prices and this is mainly due to decrease in demand, faulty setting up

of prices etc. (Messer, 2016). The formula for evaluation of this planning variance can be

presented in following manner:

Material Price Planning Variance = (Original budgeted price – Market Price at time of purchase)

* Quantity Purchased

For XLG Company the material price planning variance can be calculated in following manner:

Particulars Original

budget

Revised budget Actual

Chemical X 2.5 4.5 3.7

Chemical Y 2.5 4.5 3.7

Budgeted production 800 800 1600 (800 +

800)

Material price planning (4.5 - 2.5) 3200 (A)

5

Therefore, the above calculation indicates that the overall sale volume contribution

variance for the XLG Company is favourable with £9475 and this is mainly due to the increased

number of units sold for both the chemicals than the expected ones.

Material price planning and material price operational variance

The material price variances are instrumental in ascertaining that how effectively and

correctly can the future prices of the product be estimated by the managers (Marzlin Marzuki and

Ismail, 2019). The material price planning variance indicates the effectiveness of the overall

planning of the managers where the comparison is made between the original budget developed

and the revised budget developed in realistic manner. This variance helps in ascertaining that

how effective was the planning earlier and also identifies the need to have a revised budget when

the existing budget is not in accordance with the current market conditions that are prevalent.

This is generally done when the standard that has been set was not in anticipation of the future

conditions or when some unforeseeable future condition arises that could not have been easily

predicted. The favourable planning variance can arise when the general market prices are higher

than the original prices that were set up and this can be due to increase in the requirement of the

product, change in market conditions etc. The adverse variance can arise when the original prices

are higher than the general prices and this is mainly due to decrease in demand, faulty setting up

of prices etc. (Messer, 2016). The formula for evaluation of this planning variance can be

presented in following manner:

Material Price Planning Variance = (Original budgeted price – Market Price at time of purchase)

* Quantity Purchased

For XLG Company the material price planning variance can be calculated in following manner:

Particulars Original

budget

Revised budget Actual

Chemical X 2.5 4.5 3.7

Chemical Y 2.5 4.5 3.7

Budgeted production 800 800 1600 (800 +

800)

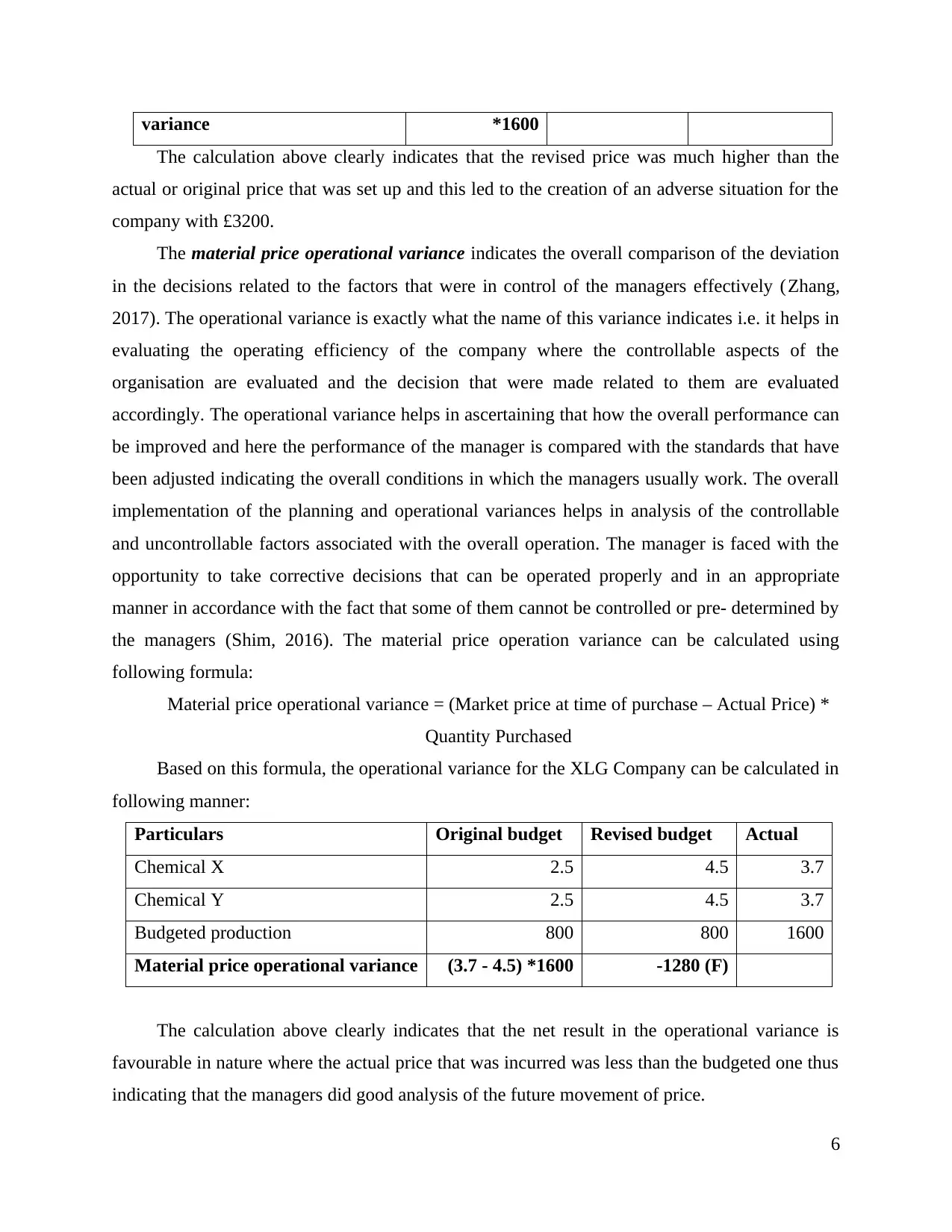

Material price planning (4.5 - 2.5) 3200 (A)

5

variance *1600

The calculation above clearly indicates that the revised price was much higher than the

actual or original price that was set up and this led to the creation of an adverse situation for the

company with £3200.

The material price operational variance indicates the overall comparison of the deviation

in the decisions related to the factors that were in control of the managers effectively (Zhang,

2017). The operational variance is exactly what the name of this variance indicates i.e. it helps in

evaluating the operating efficiency of the company where the controllable aspects of the

organisation are evaluated and the decision that were made related to them are evaluated

accordingly. The operational variance helps in ascertaining that how the overall performance can

be improved and here the performance of the manager is compared with the standards that have

been adjusted indicating the overall conditions in which the managers usually work. The overall

implementation of the planning and operational variances helps in analysis of the controllable

and uncontrollable factors associated with the overall operation. The manager is faced with the

opportunity to take corrective decisions that can be operated properly and in an appropriate

manner in accordance with the fact that some of them cannot be controlled or pre- determined by

the managers (Shim, 2016). The material price operation variance can be calculated using

following formula:

Material price operational variance = (Market price at time of purchase – Actual Price) *

Quantity Purchased

Based on this formula, the operational variance for the XLG Company can be calculated in

following manner:

Particulars Original budget Revised budget Actual

Chemical X 2.5 4.5 3.7

Chemical Y 2.5 4.5 3.7

Budgeted production 800 800 1600

Material price operational variance (3.7 - 4.5) *1600 -1280 (F)

The calculation above clearly indicates that the net result in the operational variance is

favourable in nature where the actual price that was incurred was less than the budgeted one thus

indicating that the managers did good analysis of the future movement of price.

6

The calculation above clearly indicates that the revised price was much higher than the

actual or original price that was set up and this led to the creation of an adverse situation for the

company with £3200.

The material price operational variance indicates the overall comparison of the deviation

in the decisions related to the factors that were in control of the managers effectively (Zhang,

2017). The operational variance is exactly what the name of this variance indicates i.e. it helps in

evaluating the operating efficiency of the company where the controllable aspects of the

organisation are evaluated and the decision that were made related to them are evaluated

accordingly. The operational variance helps in ascertaining that how the overall performance can

be improved and here the performance of the manager is compared with the standards that have

been adjusted indicating the overall conditions in which the managers usually work. The overall

implementation of the planning and operational variances helps in analysis of the controllable

and uncontrollable factors associated with the overall operation. The manager is faced with the

opportunity to take corrective decisions that can be operated properly and in an appropriate

manner in accordance with the fact that some of them cannot be controlled or pre- determined by

the managers (Shim, 2016). The material price operation variance can be calculated using

following formula:

Material price operational variance = (Market price at time of purchase – Actual Price) *

Quantity Purchased

Based on this formula, the operational variance for the XLG Company can be calculated in

following manner:

Particulars Original budget Revised budget Actual

Chemical X 2.5 4.5 3.7

Chemical Y 2.5 4.5 3.7

Budgeted production 800 800 1600

Material price operational variance (3.7 - 4.5) *1600 -1280 (F)

The calculation above clearly indicates that the net result in the operational variance is

favourable in nature where the actual price that was incurred was less than the budgeted one thus

indicating that the managers did good analysis of the future movement of price.

6

Advantages and disadvantages of using variances

The use of variance in the overall analysis of the performance has indeed been an extremely

utilised tool where the comparison of the actual performance with the standards that were set for

it helps the managers in clearly identifying what were the areas or decisions that went wrong

which in turn clearly evaluates the overall performance and decision- making of the responsible

managers (Bragg, 2016). This tool has always been used as this is measurable and helps in

qualitative assessment as well but there are certain advantages as well as disadvantages that are

inherent with the use of variance as a tool.

The major advantage of using variance is that the managers of the company are able to

develop better decisions and it helps in increasing control and monitoring as well. The

identification of the cause behind any adverse deviation helps the management in quickly

identifying hat what exactly is the area that needs to be improved or redeveloped in order to

remove the deviations. This can also lead to reduction in the average time and cost that is

incurred in the manufacturing of the products or in the completion of the overall activities that

are associated (Edwards, 2016). The top management, supervisors etc. can also motivate

employees to work harder in order to achieve the standards that have been set up. This mainly

indicates that the employees can objectify the entire process that they adopt where the key

activities that help them in the achievement of the goals are fostered and encouraged. Another

major advantages is that it helps in the maintenance of the financial stability in the company as

the computation of the variances mainly helps in the evaluation of the different financial factors

and when the conditions are not favourable for the organisation then measures like cost- cutting

etc. can be implemented (Collis, Holt and Hussey, 2017). Therefore these were the collective

advantages that use of variance analysis presents before the organisation.

The inherent disadvantages that are associated with the use of variance analysis are also

illustrative and numerous. It can be illustrated although this helps in identifying areas or

employees with ineffective performance but it also makes the managers more insensitive towards

those employees where they fail to consider any other aspects that might have also led to the

overall decline. Additionally the employees are motivated in a wrong manner where they begun

to focus on the achievement of standards only which make them lose their quality of work,

precisions level, customer satisfaction etc. (Graybeal, Franklin and Cooper, 2018). Ultimately all

of this leads to the increase in the complaints regarding the product and hence sales will also

7

The use of variance in the overall analysis of the performance has indeed been an extremely

utilised tool where the comparison of the actual performance with the standards that were set for

it helps the managers in clearly identifying what were the areas or decisions that went wrong

which in turn clearly evaluates the overall performance and decision- making of the responsible

managers (Bragg, 2016). This tool has always been used as this is measurable and helps in

qualitative assessment as well but there are certain advantages as well as disadvantages that are

inherent with the use of variance as a tool.

The major advantage of using variance is that the managers of the company are able to

develop better decisions and it helps in increasing control and monitoring as well. The

identification of the cause behind any adverse deviation helps the management in quickly

identifying hat what exactly is the area that needs to be improved or redeveloped in order to

remove the deviations. This can also lead to reduction in the average time and cost that is

incurred in the manufacturing of the products or in the completion of the overall activities that

are associated (Edwards, 2016). The top management, supervisors etc. can also motivate

employees to work harder in order to achieve the standards that have been set up. This mainly

indicates that the employees can objectify the entire process that they adopt where the key

activities that help them in the achievement of the goals are fostered and encouraged. Another

major advantages is that it helps in the maintenance of the financial stability in the company as

the computation of the variances mainly helps in the evaluation of the different financial factors

and when the conditions are not favourable for the organisation then measures like cost- cutting

etc. can be implemented (Collis, Holt and Hussey, 2017). Therefore these were the collective

advantages that use of variance analysis presents before the organisation.

The inherent disadvantages that are associated with the use of variance analysis are also

illustrative and numerous. It can be illustrated although this helps in identifying areas or

employees with ineffective performance but it also makes the managers more insensitive towards

those employees where they fail to consider any other aspects that might have also led to the

overall decline. Additionally the employees are motivated in a wrong manner where they begun

to focus on the achievement of standards only which make them lose their quality of work,

precisions level, customer satisfaction etc. (Graybeal, Franklin and Cooper, 2018). Ultimately all

of this leads to the increase in the complaints regarding the product and hence sales will also

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

decline resultantly. Another major disadvantage is the fact that the need to innovate and

creativity amongst the employees is diminished where they tend to follow only the standard

protocols and procedures that have been established in order to complete the work as quickly as

possible so that standards can be met. This technically curbs the long term growth of the

organisation (Jiambalvo, 2019).

In relation to the case undertaken of XLG as well, it can be adequately illustrates that the

calculation of the material price variances, the only relevant information available was that there

was a favourable material price variance of £27000. It can be said that the purchasing department

needs to be further analysed so that the variance can be illustrated as this alone is not adequate

source of information. The changing market conditions add to the uncertainty aspect along with

reliability concern and this is not entirely in control of the purchase department managers.

Additionally, when the material price variance is classified into planning and operational

categories of variance, the usefulness of this tool increases as it helps in the analysis of elements

and factors of multiple nature (Hoch and et.al., 2018). The planning variance indicates those

elements that are uncontrollable and not in purview of the managers while the operational

variance indicates those elements which are completely under control and authority of the

managers. This collectively indicates the efficiency of the department as a whole and improves

the capabilities of the individual employees.

However there are certain aspects that need to be carefully planned in order to avoid any

serious consequences or failure. Organisations and the management in particular needs to

develop standards that is realistic and attainable and achievable as well. They cannot be vague or

overestimated/ underestimated either as this can lead to the reduction in the overall performance

and motivation level of the employees. It is also possible that the incurrence of variance can be

justified due to faulty planning or incorrect estimations and expectations etc. (Nishimura, 2019).

The revision of the entire standard that has been set up and analysing the factors again to set up a

new variance is a very costly and engaging process which needs to be avoided at all costs. It can

further lead to the major impacts on the overall budget of the company as well.

Therefore, in this manner the different aspects that are associated with the positive as well as

negative side of the implementation of the variance analysis tools has been critically analysed

and illustrated. It can be concluded that although variance analysis is not the most conclusive and

reliant tool but nonetheless, it helps in effective monitoring and measuring of the tools and the

8

creativity amongst the employees is diminished where they tend to follow only the standard

protocols and procedures that have been established in order to complete the work as quickly as

possible so that standards can be met. This technically curbs the long term growth of the

organisation (Jiambalvo, 2019).

In relation to the case undertaken of XLG as well, it can be adequately illustrates that the

calculation of the material price variances, the only relevant information available was that there

was a favourable material price variance of £27000. It can be said that the purchasing department

needs to be further analysed so that the variance can be illustrated as this alone is not adequate

source of information. The changing market conditions add to the uncertainty aspect along with

reliability concern and this is not entirely in control of the purchase department managers.

Additionally, when the material price variance is classified into planning and operational

categories of variance, the usefulness of this tool increases as it helps in the analysis of elements

and factors of multiple nature (Hoch and et.al., 2018). The planning variance indicates those

elements that are uncontrollable and not in purview of the managers while the operational

variance indicates those elements which are completely under control and authority of the

managers. This collectively indicates the efficiency of the department as a whole and improves

the capabilities of the individual employees.

However there are certain aspects that need to be carefully planned in order to avoid any

serious consequences or failure. Organisations and the management in particular needs to

develop standards that is realistic and attainable and achievable as well. They cannot be vague or

overestimated/ underestimated either as this can lead to the reduction in the overall performance

and motivation level of the employees. It is also possible that the incurrence of variance can be

justified due to faulty planning or incorrect estimations and expectations etc. (Nishimura, 2019).

The revision of the entire standard that has been set up and analysing the factors again to set up a

new variance is a very costly and engaging process which needs to be avoided at all costs. It can

further lead to the major impacts on the overall budget of the company as well.

Therefore, in this manner the different aspects that are associated with the positive as well as

negative side of the implementation of the variance analysis tools has been critically analysed

and illustrated. It can be concluded that although variance analysis is not the most conclusive and

reliant tool but nonetheless, it helps in effective monitoring and measuring of the tools and the

8

flexibility to introduce changes also increases (Vera and et.al., 2016). Effective monitoring and

correct implementation of this tool can help the company in utilising the benefits of variance

analysis without being affected by its significant disadvantages.

PART B

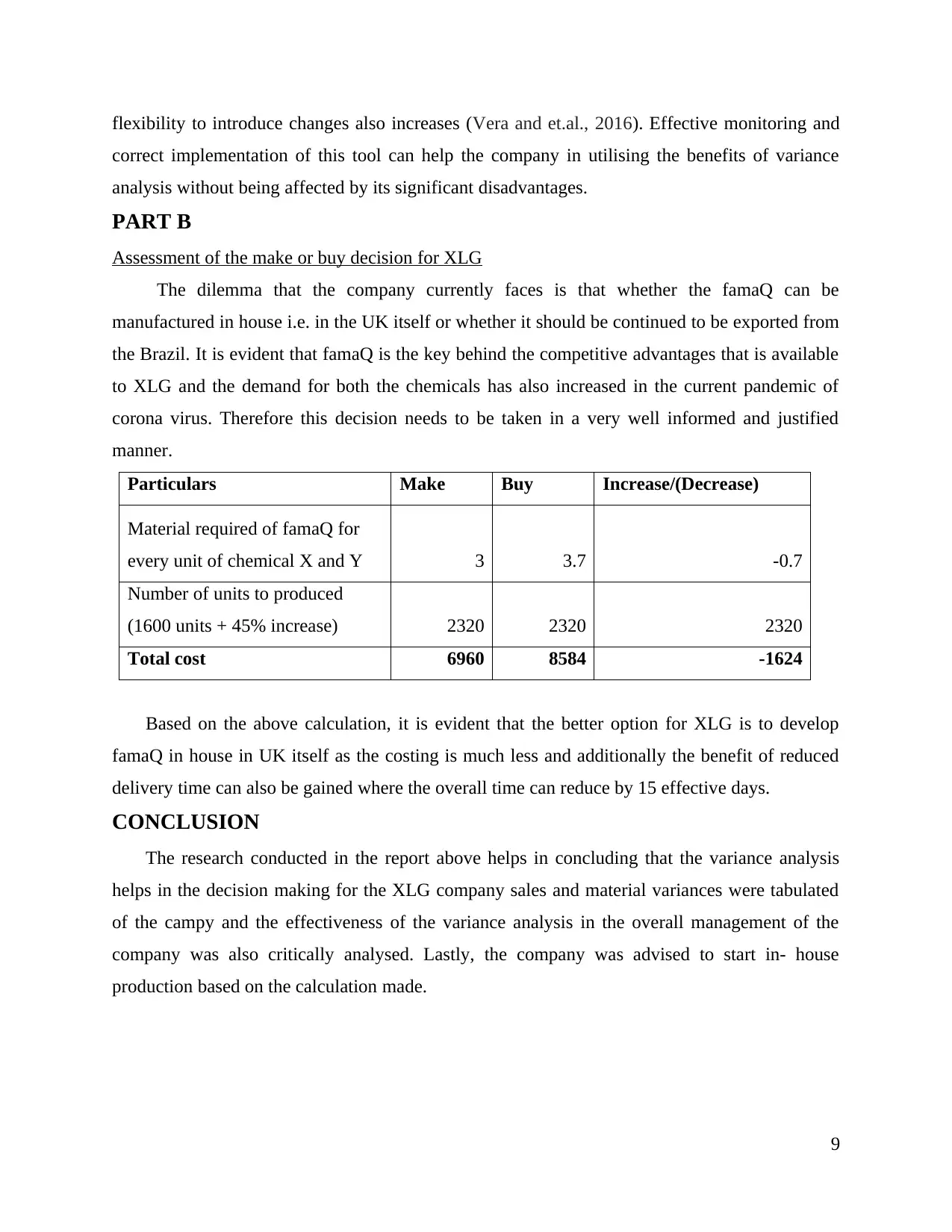

Assessment of the make or buy decision for XLG

The dilemma that the company currently faces is that whether the famaQ can be

manufactured in house i.e. in the UK itself or whether it should be continued to be exported from

the Brazil. It is evident that famaQ is the key behind the competitive advantages that is available

to XLG and the demand for both the chemicals has also increased in the current pandemic of

corona virus. Therefore this decision needs to be taken in a very well informed and justified

manner.

Particulars Make Buy Increase/(Decrease)

Material required of famaQ for

every unit of chemical X and Y 3 3.7 -0.7

Number of units to produced

(1600 units + 45% increase) 2320 2320 2320

Total cost 6960 8584 -1624

Based on the above calculation, it is evident that the better option for XLG is to develop

famaQ in house in UK itself as the costing is much less and additionally the benefit of reduced

delivery time can also be gained where the overall time can reduce by 15 effective days.

CONCLUSION

The research conducted in the report above helps in concluding that the variance analysis

helps in the decision making for the XLG company sales and material variances were tabulated

of the campy and the effectiveness of the variance analysis in the overall management of the

company was also critically analysed. Lastly, the company was advised to start in- house

production based on the calculation made.

9

correct implementation of this tool can help the company in utilising the benefits of variance

analysis without being affected by its significant disadvantages.

PART B

Assessment of the make or buy decision for XLG

The dilemma that the company currently faces is that whether the famaQ can be

manufactured in house i.e. in the UK itself or whether it should be continued to be exported from

the Brazil. It is evident that famaQ is the key behind the competitive advantages that is available

to XLG and the demand for both the chemicals has also increased in the current pandemic of

corona virus. Therefore this decision needs to be taken in a very well informed and justified

manner.

Particulars Make Buy Increase/(Decrease)

Material required of famaQ for

every unit of chemical X and Y 3 3.7 -0.7

Number of units to produced

(1600 units + 45% increase) 2320 2320 2320

Total cost 6960 8584 -1624

Based on the above calculation, it is evident that the better option for XLG is to develop

famaQ in house in UK itself as the costing is much less and additionally the benefit of reduced

delivery time can also be gained where the overall time can reduce by 15 effective days.

CONCLUSION

The research conducted in the report above helps in concluding that the variance analysis

helps in the decision making for the XLG company sales and material variances were tabulated

of the campy and the effectiveness of the variance analysis in the overall management of the

company was also critically analysed. Lastly, the company was advised to start in- house

production based on the calculation made.

9

REFERENCES

Books and Journals

Bai, G., 2016. Applying variance analysis to understand California hospitals' expense recovery

status by patient groups. Accounting Horizons. 30(2). pp.211-223

Bragg, S. M., 2016. Cost accounting fundamentals. Colorado, CO: Accounting Tools.

Collis, J., Holt, A. and Hussey, R., 2017. Business accounting. Palgrave.

Edwards, J.B., 2016. Modern gross profit analysis. Journal of Corporate Accounting &

Finance. 27(4). pp.45-55.

Farkas, M., Kersting, L. and Stephens, W., 2016. Modern Watch Company: An instructional

resource for presenting and learning actual, normal, and standard costing systems, and

variable and fixed overhead variance analysis. Journal of Accounting Education. 35.

pp.56-68.

Graybeal, P., Franklin, M. and Cooper, D., 2018. Distinguish between Financial and Managerial

Accounting. Principles of Accounting, Volume 2: Managerial Accounting

Hoch, J. E. and et.al., 2018. Do ethical, authentic, and servant leadership explain variance above

and beyond transformational leadership? A meta-analysis. Journal of Management. 44(2).

pp.501-529.

Jiambalvo, J., 2019. Managerial accounting. John Wiley & Sons.

Marzlin Marzuki, N.A.R. and Ismail, J., 2019. Benefits and limitations of variance analysis in

management accounting. ACCOUNTING BULLETIN. p.15.

Messer, R., 2016. Teaching Variance Analysis for Cost Accounting: How to Achieve above Par

Performance. In Advances in Accounting Education: Teaching and Curriculum

Innovations. Emerald Group Publishing Limited.

Nishimura, A., 2019. Profit opportunity, strategic innovation, and management accounting.

In Management, uncertainty, and accounting (pp. 97-127). Palgrave Macmillan,

Singapore

Rosyidi, C.N., 2019, August. Make or Buy Decision with Price and Quality Dependent Demand.

In Proceedings of the International Manufacturing Engineering Conference & The Asia

Pacific Conference on Manufacturing Systems (pp. 272-277). Springer, Singapore.

Shim, J. K., 2016. Accounting and finance for the nonfinancial executive: An Integrated

Resource Management Guide for the 21st Century. CRC Press

10

Books and Journals

Bai, G., 2016. Applying variance analysis to understand California hospitals' expense recovery

status by patient groups. Accounting Horizons. 30(2). pp.211-223

Bragg, S. M., 2016. Cost accounting fundamentals. Colorado, CO: Accounting Tools.

Collis, J., Holt, A. and Hussey, R., 2017. Business accounting. Palgrave.

Edwards, J.B., 2016. Modern gross profit analysis. Journal of Corporate Accounting &

Finance. 27(4). pp.45-55.

Farkas, M., Kersting, L. and Stephens, W., 2016. Modern Watch Company: An instructional

resource for presenting and learning actual, normal, and standard costing systems, and

variable and fixed overhead variance analysis. Journal of Accounting Education. 35.

pp.56-68.

Graybeal, P., Franklin, M. and Cooper, D., 2018. Distinguish between Financial and Managerial

Accounting. Principles of Accounting, Volume 2: Managerial Accounting

Hoch, J. E. and et.al., 2018. Do ethical, authentic, and servant leadership explain variance above

and beyond transformational leadership? A meta-analysis. Journal of Management. 44(2).

pp.501-529.

Jiambalvo, J., 2019. Managerial accounting. John Wiley & Sons.

Marzlin Marzuki, N.A.R. and Ismail, J., 2019. Benefits and limitations of variance analysis in

management accounting. ACCOUNTING BULLETIN. p.15.

Messer, R., 2016. Teaching Variance Analysis for Cost Accounting: How to Achieve above Par

Performance. In Advances in Accounting Education: Teaching and Curriculum

Innovations. Emerald Group Publishing Limited.

Nishimura, A., 2019. Profit opportunity, strategic innovation, and management accounting.

In Management, uncertainty, and accounting (pp. 97-127). Palgrave Macmillan,

Singapore

Rosyidi, C.N., 2019, August. Make or Buy Decision with Price and Quality Dependent Demand.

In Proceedings of the International Manufacturing Engineering Conference & The Asia

Pacific Conference on Manufacturing Systems (pp. 272-277). Springer, Singapore.

Shim, J. K., 2016. Accounting and finance for the nonfinancial executive: An Integrated

Resource Management Guide for the 21st Century. CRC Press

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Tan, B.S. and Low, K.Y., 2017. Budgeting Practice in Singapore–An Exploratory Study Using a

Survey. Asia Pacific Management Accounting Journal. 12(1). pp.77-103.

Vera, O. D. and et.al., 2016. Assessing psychology students’ difficulties in elementary variance

analysis. Revista Diálogo Educacional. 16(48). pp.487-511.

Windapo, A. and Moghayedi, A., 2017. BUILDING MATERIAL PRICE DIFFERENTIATION

IN SOUTH AFRICA: THE ROLE OF RETAILERS AND LOCATION. WELCOME TO

DELEGATES IRC 2017. p.447.

Zhang, C., 2017. The Application of Variance Analysis in FP&A Organizations: Survey

Evidence and Recommendations for Enhancement. Journal of Accounting and

Finance. 17(8). pp.54-70.

11

Survey. Asia Pacific Management Accounting Journal. 12(1). pp.77-103.

Vera, O. D. and et.al., 2016. Assessing psychology students’ difficulties in elementary variance

analysis. Revista Diálogo Educacional. 16(48). pp.487-511.

Windapo, A. and Moghayedi, A., 2017. BUILDING MATERIAL PRICE DIFFERENTIATION

IN SOUTH AFRICA: THE ROLE OF RETAILERS AND LOCATION. WELCOME TO

DELEGATES IRC 2017. p.447.

Zhang, C., 2017. The Application of Variance Analysis in FP&A Organizations: Survey

Evidence and Recommendations for Enhancement. Journal of Accounting and

Finance. 17(8). pp.54-70.

11

12

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.