Critically Discuss: Financial and Non-Financial Measures in Management

VerifiedAdded on 2020/02/05

|13

|4460

|68

Essay

AI Summary

This essay critically discusses the necessity of utilizing both traditional financial measures and non-financial measures for effective management. It delves into the significance of financial performance indicators like profitability statements, balance sheets, ratio analysis, and cash flow statements, while also evaluating non-financial performance measurement tools such as the balanced scorecard. The essay draws on various authors' viewpoints to analyze the strengths and weaknesses of both financial and non-financial performance indicators in managing firm performance, emphasizing the importance of a combined approach for long-term business success. The discussion also references specific articles to provide a comprehensive understanding of the topic.

FINANCIAL AND NON-FINANCIAL

MEASURES

MEASURES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

ESSAY.......................................................................................................................................3

INTRODUCTION......................................................................................................................3

Financial and Non-financial Measures.......................................................................................3

CONCLUSION........................................................................................................................10

REFERENCES.........................................................................................................................11

2

ESSAY.......................................................................................................................................3

INTRODUCTION......................................................................................................................3

Financial and Non-financial Measures.......................................................................................3

CONCLUSION........................................................................................................................10

REFERENCES.........................................................................................................................11

2

ESSAY

INTRODUCTION

Every business organization needs to determine their financial as well as non-

financial performance. Financial accounting aims at measuring the performance of business

in terms of finance management. Hence, it is a part of performance management.

Determining company’s profitability and financial position are the most important financial

measurement. Along with this, organizations also need to measure their non-financial

performance to achieve their set business targets and objectives. In the present essay, it will

be discussed that how firms make use of both the traditional financial measure and non-

financial measure in the performance management. The present essay will carry out the

critical discussion of traditional financial measures such as profitability statement, balance

sheet, ratio analysis and cash flow statement. Moreover, NFPI tools such as balance

scorecard, performance pyramid and building block model will be critically evaluated. The

critical discussion will be done as per the view points of different authors that help to

evaluate the significance and drawbacks of FPI and NFPI in managing firm's performance.

Financial performance measurement tools revolves around analysing organization's

spendings, revenues, profitability, liquidity, solvency, cash flow capacity and others. In other

words, it is a quantitative measurement. Thus, it does not reflect total manager's contribution

to the firms. NFPI will be greatly helpful in analysing overall managerial contribution. It will

assist users to determine long term business performance. Present essay will taken into

consideration that how financial tools provide assistance to measure organization

performance. Moreover, it describe the consequences of this analysis as per literature review.

However, it will discuss the importance and drawbacks of NFPI such as BS, performance

pyramid and building block model. The critical discussion of the FPI and NFPI will guide us

to managing business performance.

FINANCIAL AND NON-FINANCIAL MEASURES

According to White, Sondhi and Fried (2003), financial performance of the business

can be measured in monetary terms. Every business organization aims at maximizing their

profitability, long term survival and business growth. Enterprises make use of invested funds

to earn great amount of profits. Thus, all the operating activities have been done so as to get

good profitability. However, ability of the organization to run business for a long term period

is known as business survivals and measures the success of company. Furthermore, manager

3

INTRODUCTION

Every business organization needs to determine their financial as well as non-

financial performance. Financial accounting aims at measuring the performance of business

in terms of finance management. Hence, it is a part of performance management.

Determining company’s profitability and financial position are the most important financial

measurement. Along with this, organizations also need to measure their non-financial

performance to achieve their set business targets and objectives. In the present essay, it will

be discussed that how firms make use of both the traditional financial measure and non-

financial measure in the performance management. The present essay will carry out the

critical discussion of traditional financial measures such as profitability statement, balance

sheet, ratio analysis and cash flow statement. Moreover, NFPI tools such as balance

scorecard, performance pyramid and building block model will be critically evaluated. The

critical discussion will be done as per the view points of different authors that help to

evaluate the significance and drawbacks of FPI and NFPI in managing firm's performance.

Financial performance measurement tools revolves around analysing organization's

spendings, revenues, profitability, liquidity, solvency, cash flow capacity and others. In other

words, it is a quantitative measurement. Thus, it does not reflect total manager's contribution

to the firms. NFPI will be greatly helpful in analysing overall managerial contribution. It will

assist users to determine long term business performance. Present essay will taken into

consideration that how financial tools provide assistance to measure organization

performance. Moreover, it describe the consequences of this analysis as per literature review.

However, it will discuss the importance and drawbacks of NFPI such as BS, performance

pyramid and building block model. The critical discussion of the FPI and NFPI will guide us

to managing business performance.

FINANCIAL AND NON-FINANCIAL MEASURES

According to White, Sondhi and Fried (2003), financial performance of the business

can be measured in monetary terms. Every business organization aims at maximizing their

profitability, long term survival and business growth. Enterprises make use of invested funds

to earn great amount of profits. Thus, all the operating activities have been done so as to get

good profitability. However, ability of the organization to run business for a long term period

is known as business survivals and measures the success of company. Furthermore, manager

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

aims at running a successful business in order to make organizational growth. However, Chee

and et.al., (2006), said that non-financial measure includes internal operating measure as well

as employee and customer-oriented measures. Production volume, productivity, defects,

waste management, introducing new product, cycle time, operating efficiency and inventory

levels are internal measures. On contrary, according to Bharadwaj (2015), employee

satisfaction, staff turnover, workers training, skills, absence rate and safety measurement are

the employee oriented measures whilst market share, customer acquisition, retention, delivery

performance, waiting time and customer complaints are customer-oriented measures.

As per the view point of Minnis and Sutherland (2015), profitability statement helps

to determine the results of operating business functions. The author said that this statement

combines incurred business expenditures and revenues for a fixed period of time. The surplus

of incomes over the expenses will indicate profits for the enterprise and shows better

performance while excessive business payments contribute to loss and indicate poor

performance. According to Barnett, Michael and Robert (2012), high profitability indicates

better operational results while decreasing profitability is a sign of worst performance.

Moreover, it helps managers to determine the operating efficiency of business. However,

according to Titman, Martin and Keown (2015), it has been critically evaluated that the

statement does not provide information about the real business profits. The reason behind this

is that statement records transactions on accrual concept; hence, it represents artificial profits.

Under the accrual basis, transactions are recorded at the time of occurrence whether it has

been received in cash or not. Therefore, it is not a better measurement of company's

operational performance.

According to Fraser and Ormiston (2015), balance sheet is a tool to measure financial

performance of the company. It is a summarized statement of all the assets such as fixed as

well as current assets and all the liabilities in terms of both the long term and short term.

Assets are the sources that will be used to generate profits whilst liabilities are the outside

financial sources such as creditor’s bank loan, overdraft and accounts payable. Moreover, the

statement helps to determine the proportion of owner's share on the business assets that is

called equity. Thus, it helps to represent the financial position of business. On the contrary,

Bédard and Courteau (2015), critically evaluated that balance sheet is not a good performance

measurement as it is a time consuming process and determines financial status at a specified

date only. Likewise, Ongore and Kusa, (2013), said that initially, business needs to prepare

journal, ledger, trial balance, trading as well as profit and loss account for preparing balance

sheet; thus, it takes very much time. Further, in case of any mistakes in transaction recording

4

and et.al., (2006), said that non-financial measure includes internal operating measure as well

as employee and customer-oriented measures. Production volume, productivity, defects,

waste management, introducing new product, cycle time, operating efficiency and inventory

levels are internal measures. On contrary, according to Bharadwaj (2015), employee

satisfaction, staff turnover, workers training, skills, absence rate and safety measurement are

the employee oriented measures whilst market share, customer acquisition, retention, delivery

performance, waiting time and customer complaints are customer-oriented measures.

As per the view point of Minnis and Sutherland (2015), profitability statement helps

to determine the results of operating business functions. The author said that this statement

combines incurred business expenditures and revenues for a fixed period of time. The surplus

of incomes over the expenses will indicate profits for the enterprise and shows better

performance while excessive business payments contribute to loss and indicate poor

performance. According to Barnett, Michael and Robert (2012), high profitability indicates

better operational results while decreasing profitability is a sign of worst performance.

Moreover, it helps managers to determine the operating efficiency of business. However,

according to Titman, Martin and Keown (2015), it has been critically evaluated that the

statement does not provide information about the real business profits. The reason behind this

is that statement records transactions on accrual concept; hence, it represents artificial profits.

Under the accrual basis, transactions are recorded at the time of occurrence whether it has

been received in cash or not. Therefore, it is not a better measurement of company's

operational performance.

According to Fraser and Ormiston (2015), balance sheet is a tool to measure financial

performance of the company. It is a summarized statement of all the assets such as fixed as

well as current assets and all the liabilities in terms of both the long term and short term.

Assets are the sources that will be used to generate profits whilst liabilities are the outside

financial sources such as creditor’s bank loan, overdraft and accounts payable. Moreover, the

statement helps to determine the proportion of owner's share on the business assets that is

called equity. Thus, it helps to represent the financial position of business. On the contrary,

Bédard and Courteau (2015), critically evaluated that balance sheet is not a good performance

measurement as it is a time consuming process and determines financial status at a specified

date only. Likewise, Ongore and Kusa, (2013), said that initially, business needs to prepare

journal, ledger, trial balance, trading as well as profit and loss account for preparing balance

sheet; thus, it takes very much time. Further, in case of any mistakes in transaction recording

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

process, balance sheet does not indicate correct financial status. Thus, lack of data reliability

may also lead to take harmful managerial decision. This in turn, it will lead to take poor

managerial decisions and influence business operations in an adverse manner.

Another, according to Hu and et.al., (2012), ratio analysis is the best tool to measure

the financial performance of companies. It indicates the relationship between various

components of the financial position. Numerous ratios can be determined to analyse

company's performance such as profitability, liquidity, gearing and efficiency as well as

investors ratio. Profitability ratios such as gross margin and net margin identify the business

profit on total sales. Another, current and quick ratio measure company’s ability to discharge

their short term obligations; hence, good liquidity indicates better financial performance and

vice versa. However, solvency ratios such as debt-equity ratio and time to interest ratio

measure company's ability to pay off its long term liabilities. In addition to it, investors ratios

such as price to earnings ratio, growth ratio, enterprise value to revenue and EBIT measure

the possibility of future business growth whilst return on assets and equity are the

measurement of manager's efficiency and effectiveness. Thus, the ratio analysis greatly helps

to analyse, evaluate and interpret the overall financial performance and aids managers to take

qualified managerial decisions. On contrary to it, Kumbirai and Webb (2013), argued that

although ratio analysis examines the financial performance but it cannot be identified as a

better performance measurement tool due to its various limitations. One of the important

drawbacks of this technique is that it measures the historical business performance that does

not provide assistance to forecast the financial performance in the future context. Similarly,

Ic and et.al., (2015), mentioned that different organizations follow distinct accounting

principles; hence, comparison may not provide any meaningful result. In the present dynamic

environment, market changes impact the organization operations in a great manner while

ratio analysis does not consider it such as inflation. Different organizations follow distinct

accounting standards thus; it does not help in making comparative analysis. Further, it does

not provide assistance to the managers for taking strategic long term business decisions.

However, organizational success greatly depends upon the effectiveness of long term

managerial decisions. In addition to it, setting an ideal ratio for all types of industries is not

possible thus, target ratio cannot be determined. Therefore, it can be concluded that ratio

analysis cannot be considered as the best performance measurement tool due to existed

limitations.

5

may also lead to take harmful managerial decision. This in turn, it will lead to take poor

managerial decisions and influence business operations in an adverse manner.

Another, according to Hu and et.al., (2012), ratio analysis is the best tool to measure

the financial performance of companies. It indicates the relationship between various

components of the financial position. Numerous ratios can be determined to analyse

company's performance such as profitability, liquidity, gearing and efficiency as well as

investors ratio. Profitability ratios such as gross margin and net margin identify the business

profit on total sales. Another, current and quick ratio measure company’s ability to discharge

their short term obligations; hence, good liquidity indicates better financial performance and

vice versa. However, solvency ratios such as debt-equity ratio and time to interest ratio

measure company's ability to pay off its long term liabilities. In addition to it, investors ratios

such as price to earnings ratio, growth ratio, enterprise value to revenue and EBIT measure

the possibility of future business growth whilst return on assets and equity are the

measurement of manager's efficiency and effectiveness. Thus, the ratio analysis greatly helps

to analyse, evaluate and interpret the overall financial performance and aids managers to take

qualified managerial decisions. On contrary to it, Kumbirai and Webb (2013), argued that

although ratio analysis examines the financial performance but it cannot be identified as a

better performance measurement tool due to its various limitations. One of the important

drawbacks of this technique is that it measures the historical business performance that does

not provide assistance to forecast the financial performance in the future context. Similarly,

Ic and et.al., (2015), mentioned that different organizations follow distinct accounting

principles; hence, comparison may not provide any meaningful result. In the present dynamic

environment, market changes impact the organization operations in a great manner while

ratio analysis does not consider it such as inflation. Different organizations follow distinct

accounting standards thus; it does not help in making comparative analysis. Further, it does

not provide assistance to the managers for taking strategic long term business decisions.

However, organizational success greatly depends upon the effectiveness of long term

managerial decisions. In addition to it, setting an ideal ratio for all types of industries is not

possible thus, target ratio cannot be determined. Therefore, it can be concluded that ratio

analysis cannot be considered as the best performance measurement tool due to existed

limitations.

5

As per the view point of Ormiston and Fraser (2013), cash flow statement is a

measurement of liquidity position. It identifies the cash inflow and outflow from various

operating, investing and financing activities. Operating activities refer to daily routine

functions such as trading activities while investing activities measure cash sources, its

applications from acquisition and sale of company's assets. Another, financing activities refer

to the collection and payment of financial sources such as debt and equity. Thus, the

statement helps to determine the cash changes between two different accounting periods in

order to determine liquidity. However, as per Healy and Palepu (2012), it has been critically

evaluated that the statement cannot be considered as a better tool of liquidity measurement.

The reason behind that is that cash is not the only component that affects the company's

liquidity position. Thus, the statement does not consider other components such as debtors,

accounts receivable, bank and inventory. Moreover, Robu and Toma, (2015), claimed that the

statement eliminates non-cash business expenses; hence, it does not measure the real

financial performance. Furthermore, such statement represents only the historical cash

changes and does not provide assistance to forecast the future cash flows. In addition, the

statement does not identify the net business earnings. Moreover, Ameer and Othman, (2012),

said that inter-industry comparison cannot be done by using this statement. Thus, it can be

said that cash flow statement is not a good financial measurement tool as it does not help

managers to take effective cash management decisions.

Therefore, it is clear that along with the evaluation of financial performance,

companies also need to determine their non-financial performance. The reason behind such

requirement is that financial performance does not help managers to take effective long term

decisions. Furthermore, financial performance only focuses on internal business control and

eliminates external business environment. Thus, objectives of organizational success and

growth prospectus cannot be achieved in a great manner. According to Boscia and McAfee

(2014), in the present dynamic and complex environment, strategic capabilities gain a

significant importance to improve company’s performance and get competitive advantageous.

NFPI includes management of human resources, quality of offered products and services,

brand awareness, company profile etc. As per the view point of Fu and Zeng (2015), workers

play an important role in the organization success as they provide services to the customers

and drive larger the sales and profits. Skilled, efficient, qualified and experienced employees

greatly contribute to improve business performance as they serve large number of customers

in an appropriate manner and result in enlarging the customer loyalty to a great extent.

6

measurement of liquidity position. It identifies the cash inflow and outflow from various

operating, investing and financing activities. Operating activities refer to daily routine

functions such as trading activities while investing activities measure cash sources, its

applications from acquisition and sale of company's assets. Another, financing activities refer

to the collection and payment of financial sources such as debt and equity. Thus, the

statement helps to determine the cash changes between two different accounting periods in

order to determine liquidity. However, as per Healy and Palepu (2012), it has been critically

evaluated that the statement cannot be considered as a better tool of liquidity measurement.

The reason behind that is that cash is not the only component that affects the company's

liquidity position. Thus, the statement does not consider other components such as debtors,

accounts receivable, bank and inventory. Moreover, Robu and Toma, (2015), claimed that the

statement eliminates non-cash business expenses; hence, it does not measure the real

financial performance. Furthermore, such statement represents only the historical cash

changes and does not provide assistance to forecast the future cash flows. In addition, the

statement does not identify the net business earnings. Moreover, Ameer and Othman, (2012),

said that inter-industry comparison cannot be done by using this statement. Thus, it can be

said that cash flow statement is not a good financial measurement tool as it does not help

managers to take effective cash management decisions.

Therefore, it is clear that along with the evaluation of financial performance,

companies also need to determine their non-financial performance. The reason behind such

requirement is that financial performance does not help managers to take effective long term

decisions. Furthermore, financial performance only focuses on internal business control and

eliminates external business environment. Thus, objectives of organizational success and

growth prospectus cannot be achieved in a great manner. According to Boscia and McAfee

(2014), in the present dynamic and complex environment, strategic capabilities gain a

significant importance to improve company’s performance and get competitive advantageous.

NFPI includes management of human resources, quality of offered products and services,

brand awareness, company profile etc. As per the view point of Fu and Zeng (2015), workers

play an important role in the organization success as they provide services to the customers

and drive larger the sales and profits. Skilled, efficient, qualified and experienced employees

greatly contribute to improve business performance as they serve large number of customers

in an appropriate manner and result in enlarging the customer loyalty to a great extent.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Another, Chee and et.al., (2006), said that success of many industries depends upon the

organization strategic capabilities such as human resources, intellectual business capital and

customer loyalty. Therefore, new product development, high level of customer satisfaction,

employee satisfaction and qualitative products provide assistance to the managers in

achieving business targets in a great manner. NFPI plays a crucial role as it determines the

market performance. All the organization operates in business external environment hence, it

is very important to analyse the external performance.

According to Boscia and McAfee (2014), Balance Scorecard (BSC) System highly

encourages taking efficient strategic decisions through focusing at achieving short term and

long term business objectives. In the context to financial measurement, it determines the

profitability while in context to market performance, it considers customers, employees,

innovations, product quality and opportunity of new product development to accomplish the

vision of company. According to Epstein and et.al., (2015), strategy map of BSC consists of

four perspectives that are financial, customer, internal process as well as learning and growth.

The top priority of BSC system is larger the business sales, reduce cost and increase profits

that come under the financial perspective, while increasing customer satisfaction, maintaining

service quality, attracting new customer, retaining existing customers and ensuring customer

loyalty are the customer perspective objectives. As per the view points of Vorhies, Orr and

Bush (2015), learning and growth perspective focuses on improving employee skills,

ensuring team building, satisfying employees, increasing staff turnover and lowering the

absence rate. On contrary, internal process consists of improving product and service quality,

operating successfully through handling operational difficulties and improving manager’s

efficiency. As per the view point of Humphreys, Gary and Trotman (2015), BSC system is

greatly helpful in the management of hospitality industry. The approach helps industry to

measure relationship between all the perspectives. For instance, high employee turnover will

help to improve product quality that will result in high consumer satisfaction and attract new

customers. This in turn will also result in improving customer loyalty and building brand

image. Thus, financial objectives of high sales, low cost and better profitability can be

achieved in a great manner.

Moreover, according to Perkins, Grey and Remmers, (2014), BSC works as an alarm

or warning indicator which shows negative business consequences earlier as well as helps to

identify the possibility of future operational difficulties. Furthermore, BSC will be considered

as an appropriate performance measurement tool for SMEs in the UK. It assists managers in

7

organization strategic capabilities such as human resources, intellectual business capital and

customer loyalty. Therefore, new product development, high level of customer satisfaction,

employee satisfaction and qualitative products provide assistance to the managers in

achieving business targets in a great manner. NFPI plays a crucial role as it determines the

market performance. All the organization operates in business external environment hence, it

is very important to analyse the external performance.

According to Boscia and McAfee (2014), Balance Scorecard (BSC) System highly

encourages taking efficient strategic decisions through focusing at achieving short term and

long term business objectives. In the context to financial measurement, it determines the

profitability while in context to market performance, it considers customers, employees,

innovations, product quality and opportunity of new product development to accomplish the

vision of company. According to Epstein and et.al., (2015), strategy map of BSC consists of

four perspectives that are financial, customer, internal process as well as learning and growth.

The top priority of BSC system is larger the business sales, reduce cost and increase profits

that come under the financial perspective, while increasing customer satisfaction, maintaining

service quality, attracting new customer, retaining existing customers and ensuring customer

loyalty are the customer perspective objectives. As per the view points of Vorhies, Orr and

Bush (2015), learning and growth perspective focuses on improving employee skills,

ensuring team building, satisfying employees, increasing staff turnover and lowering the

absence rate. On contrary, internal process consists of improving product and service quality,

operating successfully through handling operational difficulties and improving manager’s

efficiency. As per the view point of Humphreys, Gary and Trotman (2015), BSC system is

greatly helpful in the management of hospitality industry. The approach helps industry to

measure relationship between all the perspectives. For instance, high employee turnover will

help to improve product quality that will result in high consumer satisfaction and attract new

customers. This in turn will also result in improving customer loyalty and building brand

image. Thus, financial objectives of high sales, low cost and better profitability can be

achieved in a great manner.

Moreover, according to Perkins, Grey and Remmers, (2014), BSC works as an alarm

or warning indicator which shows negative business consequences earlier as well as helps to

identify the possibility of future operational difficulties. Furthermore, BSC will be considered

as an appropriate performance measurement tool for SMEs in the UK. It assists managers in

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

budgetary control, maintaining good relationship with the customers and taking strategic

decisions. Thus, BSC implementation greatly satisfies the need of SMEs rather than large

business organizations. On the contrary, Nørreklit and Mitchell, (2014), critically argued that

customer’s perspective gains top preference in BSC approach rather than finance perspective.

Further, all the BSC prospectus is correlated with each other and ultimately impacts the

financial performance. Thus, it can be said that it is more helpful in analysing the financial

business performance. Richard, Kirby and Chadwick (2013), argued that BSC is a very

difficult approach as it takes very much time and resources to implement. It essentially needs

for making strategy, establishing the relationship between all the perspectives, regular

reporting and dealing with the people; hence, it brings implementing difficulties to the

organization. Furthermore, practically workers do not understand the strategy clearly; hence,

it is a great disadvantage of BSC system.

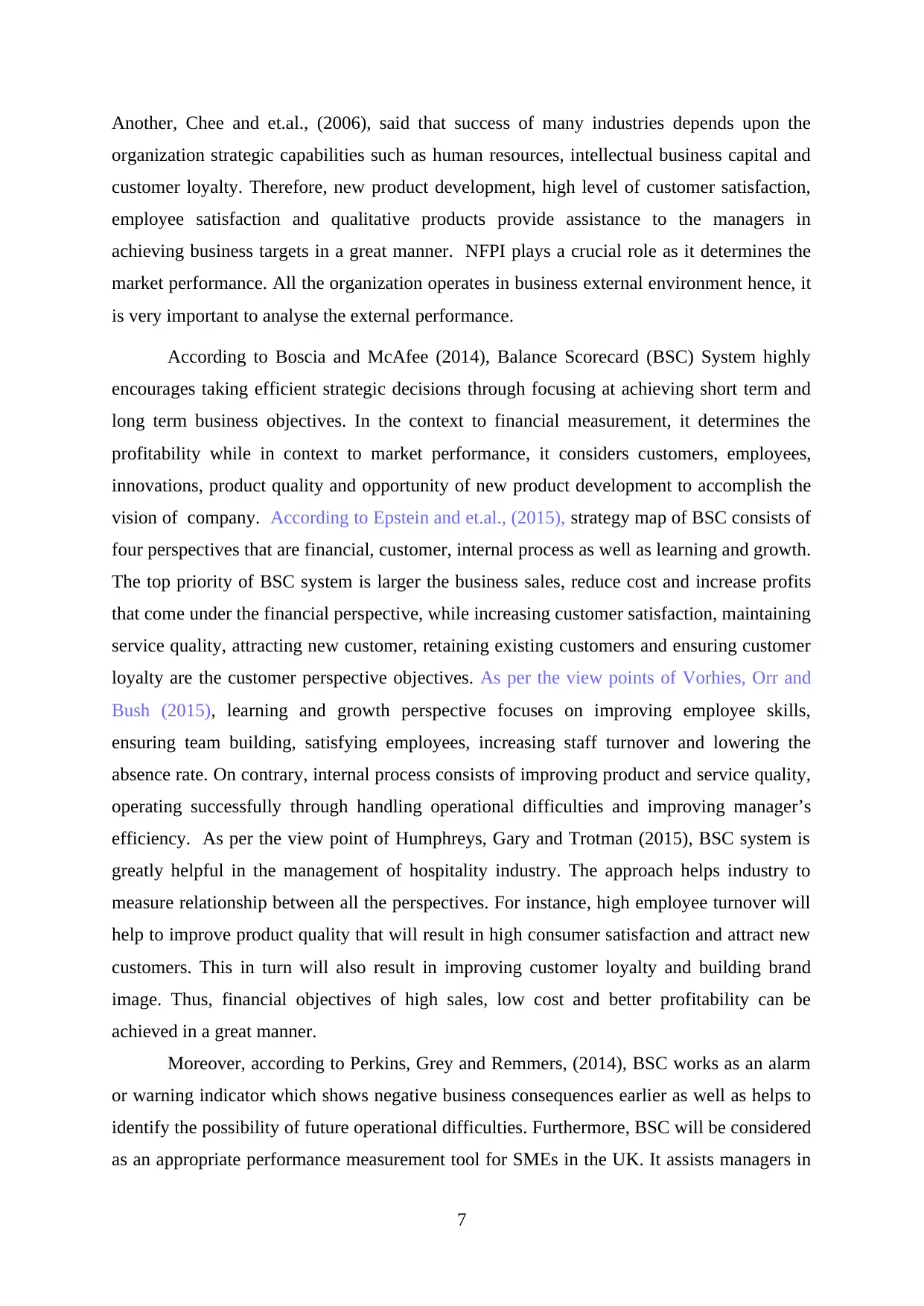

According to Istrate, Macovei and Bucur (2015), performance pyramid is the other

NFPI which incorporates both the financial and NFP as well. The pyramid consists of four

levels that are explained hereunder:

(Source: Non-financial performance indicators, n.d.)

As per the diagram, corporate vision is the top priority for all the corporations;

therefore, all the business functioning go towards achieving these targets. The vision

describes the ways of bringing long term success through building a strong competitive

position. Second level of pyramid measures the financial and marketing success of company

while third level describes the strategic objectives. Maximizing the customer satisfaction,

8

decisions. Thus, BSC implementation greatly satisfies the need of SMEs rather than large

business organizations. On the contrary, Nørreklit and Mitchell, (2014), critically argued that

customer’s perspective gains top preference in BSC approach rather than finance perspective.

Further, all the BSC prospectus is correlated with each other and ultimately impacts the

financial performance. Thus, it can be said that it is more helpful in analysing the financial

business performance. Richard, Kirby and Chadwick (2013), argued that BSC is a very

difficult approach as it takes very much time and resources to implement. It essentially needs

for making strategy, establishing the relationship between all the perspectives, regular

reporting and dealing with the people; hence, it brings implementing difficulties to the

organization. Furthermore, practically workers do not understand the strategy clearly; hence,

it is a great disadvantage of BSC system.

According to Istrate, Macovei and Bucur (2015), performance pyramid is the other

NFPI which incorporates both the financial and NFP as well. The pyramid consists of four

levels that are explained hereunder:

(Source: Non-financial performance indicators, n.d.)

As per the diagram, corporate vision is the top priority for all the corporations;

therefore, all the business functioning go towards achieving these targets. The vision

describes the ways of bringing long term success through building a strong competitive

position. Second level of pyramid measures the financial and marketing success of company

while third level describes the strategic objectives. Maximizing the customer satisfaction,

8

flexibility and productivity contribute to accomplish the organizational targets in a great

manner. The lowest level indicates the department performance in terms of quality, delivery,

cycle time and waste. Timely delivery, better quality, reducing the cycle time and waste will

indicate good department performance and vice versa. Thus, the pyramid is a NFPI that

analyses both the internal and external effectiveness. However, Watts and McNair-Connolly,

(2012), critically said that pyramid has certain drawbacks; hence, it is not a powerful

performance management tool. It majorly concentrates on the shareholders as well as

customers and does not consider the other stakeholders. Further, it does not make proper

analyse of firm’s performance; therefore, it cannot be used for the management purpose.

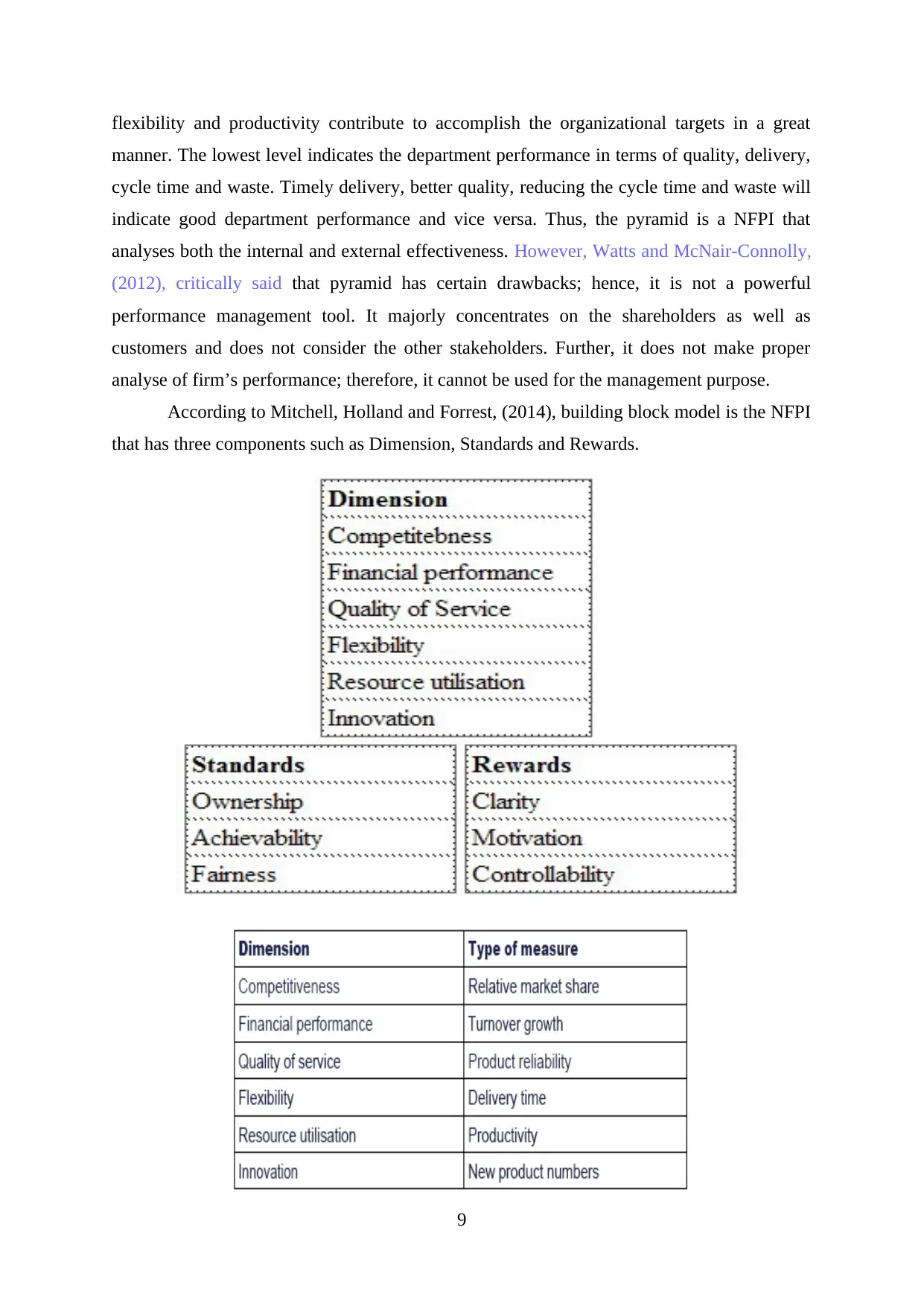

According to Mitchell, Holland and Forrest, (2014), building block model is the NFPI

that has three components such as Dimension, Standards and Rewards.

9

manner. The lowest level indicates the department performance in terms of quality, delivery,

cycle time and waste. Timely delivery, better quality, reducing the cycle time and waste will

indicate good department performance and vice versa. Thus, the pyramid is a NFPI that

analyses both the internal and external effectiveness. However, Watts and McNair-Connolly,

(2012), critically said that pyramid has certain drawbacks; hence, it is not a powerful

performance management tool. It majorly concentrates on the shareholders as well as

customers and does not consider the other stakeholders. Further, it does not make proper

analyse of firm’s performance; therefore, it cannot be used for the management purpose.

According to Mitchell, Holland and Forrest, (2014), building block model is the NFPI

that has three components such as Dimension, Standards and Rewards.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Source: Non-financial performance indicators, n.d.)

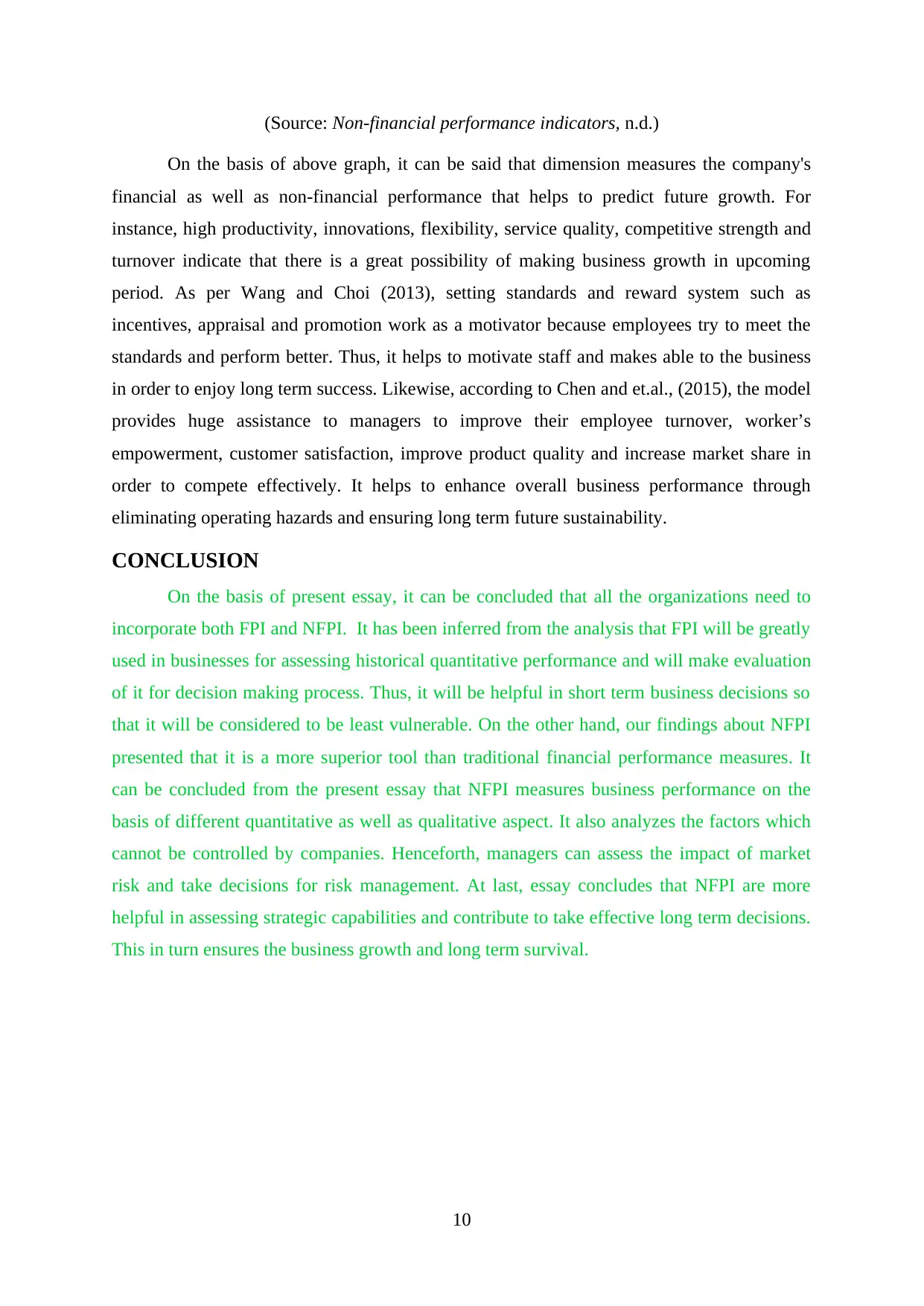

On the basis of above graph, it can be said that dimension measures the company's

financial as well as non-financial performance that helps to predict future growth. For

instance, high productivity, innovations, flexibility, service quality, competitive strength and

turnover indicate that there is a great possibility of making business growth in upcoming

period. As per Wang and Choi (2013), setting standards and reward system such as

incentives, appraisal and promotion work as a motivator because employees try to meet the

standards and perform better. Thus, it helps to motivate staff and makes able to the business

in order to enjoy long term success. Likewise, according to Chen and et.al., (2015), the model

provides huge assistance to managers to improve their employee turnover, worker’s

empowerment, customer satisfaction, improve product quality and increase market share in

order to compete effectively. It helps to enhance overall business performance through

eliminating operating hazards and ensuring long term future sustainability.

CONCLUSION

On the basis of present essay, it can be concluded that all the organizations need to

incorporate both FPI and NFPI. It has been inferred from the analysis that FPI will be greatly

used in businesses for assessing historical quantitative performance and will make evaluation

of it for decision making process. Thus, it will be helpful in short term business decisions so

that it will be considered to be least vulnerable. On the other hand, our findings about NFPI

presented that it is a more superior tool than traditional financial performance measures. It

can be concluded from the present essay that NFPI measures business performance on the

basis of different quantitative as well as qualitative aspect. It also analyzes the factors which

cannot be controlled by companies. Henceforth, managers can assess the impact of market

risk and take decisions for risk management. At last, essay concludes that NFPI are more

helpful in assessing strategic capabilities and contribute to take effective long term decisions.

This in turn ensures the business growth and long term survival.

10

On the basis of above graph, it can be said that dimension measures the company's

financial as well as non-financial performance that helps to predict future growth. For

instance, high productivity, innovations, flexibility, service quality, competitive strength and

turnover indicate that there is a great possibility of making business growth in upcoming

period. As per Wang and Choi (2013), setting standards and reward system such as

incentives, appraisal and promotion work as a motivator because employees try to meet the

standards and perform better. Thus, it helps to motivate staff and makes able to the business

in order to enjoy long term success. Likewise, according to Chen and et.al., (2015), the model

provides huge assistance to managers to improve their employee turnover, worker’s

empowerment, customer satisfaction, improve product quality and increase market share in

order to compete effectively. It helps to enhance overall business performance through

eliminating operating hazards and ensuring long term future sustainability.

CONCLUSION

On the basis of present essay, it can be concluded that all the organizations need to

incorporate both FPI and NFPI. It has been inferred from the analysis that FPI will be greatly

used in businesses for assessing historical quantitative performance and will make evaluation

of it for decision making process. Thus, it will be helpful in short term business decisions so

that it will be considered to be least vulnerable. On the other hand, our findings about NFPI

presented that it is a more superior tool than traditional financial performance measures. It

can be concluded from the present essay that NFPI measures business performance on the

basis of different quantitative as well as qualitative aspect. It also analyzes the factors which

cannot be controlled by companies. Henceforth, managers can assess the impact of market

risk and take decisions for risk management. At last, essay concludes that NFPI are more

helpful in assessing strategic capabilities and contribute to take effective long term decisions.

This in turn ensures the business growth and long term survival.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Ameer, R. and Othman, R., 2012. Sustainability practices and corporate financial

performance: A study based on the top global corporations. Journal of Business Ethics.

108(1). pp. 61-79.

Barnett, Michael L. and Robert M. Salomon, 2012. "Does it pay to be really good?

Addressing the shape of the relationship between social and financial performance."

Strategic Management Journal. pp. 1304-1320.

Bédard, J. and Courteau, L., 2015. Benefits and costs of auditor's assurance: Evidence from

the review of quarterly financial statements. Contemporary Accounting Research.

32(1). pp. 308-335.

Bharadwaj, S., 2015. Developing new marketing strategy theory: addressing the limitations

of a singular focus on firm financial performance. AMS Review. 5(3-4). pp. 98-102.

Boscia, M. W. and McAfee, R. B., 2014. Using the balance scorecard approach: A group

exercise. Developments in Business Simulation and Experiential Learning. 35.

Chen, L. and et.al., 2015. Permeability prediction of shale matrix reconstructed using the

elementary building block model. Fuel. pp. 346-356.

Epstein, M. J., Buhovac, A. R. and Yuthas, K., 2015. Managing social, environmental and

financial performance simultaneously. Long Range Planning. 48(1). pp. 35-45.

Fraser, L. M. and Ormiston, A., 2015. Understanding Financial Statements. Prentice Hall.

Fu, G. and Zeng, P., 2015, June. The relationship between Corporate Social Performance and

Corporate Financial Performance: A literature review of twenty years (I). In Education

Management and Management Science: Proceedings of the International Conference

on Education Management and Management Science (ICEMMS 2014). CRC Press.

Healy, P. and Palepu, K., 2012. Business Analysis Valuation: Using Financial Statements.

Cengage Learning.

Hu, Z. and et.al., 2012. Improved in situ Hf isotope ratio analysis of zircon using newly

designed X skimmer cone and jet sample cone in combination with the addition of

nitrogen by laser ablation multiple collector ICP-MS. Journal of Analytical Atomic

Spectrometry. 27(9). pp.1391-1399.

Humphreys, K. A., Gary, M. S. and Trotman, K. T., 2015. Dynamic Decision Making Using

the Balance Scorecard Framework. The Accounting Review.

Ic, Y. T. and et.al., 2015. Development of a financial performance benchmarking model for

corporate firms. JOURNAL OF THE FACULTY OF ENGINEERING AND

ARCHITECTURE OF GAZI UNIVERSITY. 30(1). pp. 71-85.

11

Books and Journals

Ameer, R. and Othman, R., 2012. Sustainability practices and corporate financial

performance: A study based on the top global corporations. Journal of Business Ethics.

108(1). pp. 61-79.

Barnett, Michael L. and Robert M. Salomon, 2012. "Does it pay to be really good?

Addressing the shape of the relationship between social and financial performance."

Strategic Management Journal. pp. 1304-1320.

Bédard, J. and Courteau, L., 2015. Benefits and costs of auditor's assurance: Evidence from

the review of quarterly financial statements. Contemporary Accounting Research.

32(1). pp. 308-335.

Bharadwaj, S., 2015. Developing new marketing strategy theory: addressing the limitations

of a singular focus on firm financial performance. AMS Review. 5(3-4). pp. 98-102.

Boscia, M. W. and McAfee, R. B., 2014. Using the balance scorecard approach: A group

exercise. Developments in Business Simulation and Experiential Learning. 35.

Chen, L. and et.al., 2015. Permeability prediction of shale matrix reconstructed using the

elementary building block model. Fuel. pp. 346-356.

Epstein, M. J., Buhovac, A. R. and Yuthas, K., 2015. Managing social, environmental and

financial performance simultaneously. Long Range Planning. 48(1). pp. 35-45.

Fraser, L. M. and Ormiston, A., 2015. Understanding Financial Statements. Prentice Hall.

Fu, G. and Zeng, P., 2015, June. The relationship between Corporate Social Performance and

Corporate Financial Performance: A literature review of twenty years (I). In Education

Management and Management Science: Proceedings of the International Conference

on Education Management and Management Science (ICEMMS 2014). CRC Press.

Healy, P. and Palepu, K., 2012. Business Analysis Valuation: Using Financial Statements.

Cengage Learning.

Hu, Z. and et.al., 2012. Improved in situ Hf isotope ratio analysis of zircon using newly

designed X skimmer cone and jet sample cone in combination with the addition of

nitrogen by laser ablation multiple collector ICP-MS. Journal of Analytical Atomic

Spectrometry. 27(9). pp.1391-1399.

Humphreys, K. A., Gary, M. S. and Trotman, K. T., 2015. Dynamic Decision Making Using

the Balance Scorecard Framework. The Accounting Review.

Ic, Y. T. and et.al., 2015. Development of a financial performance benchmarking model for

corporate firms. JOURNAL OF THE FACULTY OF ENGINEERING AND

ARCHITECTURE OF GAZI UNIVERSITY. 30(1). pp. 71-85.

11

Istrate, I. V., Macovei, S. and Bucur, M., 2015. The Role of Performance Pyramid in Sports

Management Case Study-The Athletics Section in CSM Onesti. Sport Science Review.

24(3-4). pp. 215-234.

Kumbirai, M. and Webb, R., 2013. A financial ratio analysis of commercial bank

performance in South Africa. African Review of Economics and Finance. 2(1). pp. 30-

53.

Minnis, M. and Sutherland, A., 2015. Financial statements as monitoring mechanisms:

Evidence from small commercial loans. Chicago Booth Research Paper. pp. 13-75.

Mitchell, M., Holland, J. H. and Forrest, S., 2014. Relative building-block fitness and the

building block hypothesis. D. Whitley, Foundations of Genetic Algorithms. pp. 109-

126.

Nørreklit, H. and Mitchell, F., 2014. Contemporary issues on the balance scorecard. Journal

of Accounting & Organizational Change.

Ongore, V.O. and Kusa, G.B., 2013. Determinants of financial performance of commercial

banks in Kenya. International Journal of Economics and Financial Issues. 3(1). p.

237.

Ormiston, A. and Fraser, L. M., 2013. Understanding financial statements. Pearson

Education.

Perkins, M., Grey, A. and Remmers, H., 2014. What do we really mean by “Balanced

Scorecard”?. International Journal of Productivity and Performance Management.

63(2). pp. 148-169.

Richard, O. C., Kirby, S. L. and Chadwick, K., 2013. The impact of racial and gender

diversity in management on financial performance: How participative strategy making

features can unleash a diversity advantage. The International Journal of Human

Resource Management. 24(13). pp. 2571-2582.

Robu, I. B. and Toma, C., 2015. The use of accounting conservatism in order to reflect the

true and the fair view of financial statements in the case of Romanian listed

companies. Global Journal on Humanities and Social Sciences.

Sainaghi, R., Phillips, P. and Corti, V., 2013. Measuring hotel performance: Using a balanced

scorecard perspectives’ approach. International Journal of Hospitality Management,

34, pp. 150-159.

Titman, S., Martin, J. D. and Keown, A. J., 2015. Financial management: Principles and

applications. Prentice Hall.

Vorhies, D.W., Orr, L.M. and Bush, V.D., 2015. Erratum to: Improving customer-focused

marketing capabilities and firm financial performance via marketing exploration and

exploitation. Academy of Marketing Science. Journal. 43(1). p. 136.

Wang, H. and Choi, J., 2013. A new look at the corporate social–financial performance

relationship the moderating roles of temporal and interdomain consistency in corporate

social performance. Journal of Management. 39(2). pp. 416-441.

12

Management Case Study-The Athletics Section in CSM Onesti. Sport Science Review.

24(3-4). pp. 215-234.

Kumbirai, M. and Webb, R., 2013. A financial ratio analysis of commercial bank

performance in South Africa. African Review of Economics and Finance. 2(1). pp. 30-

53.

Minnis, M. and Sutherland, A., 2015. Financial statements as monitoring mechanisms:

Evidence from small commercial loans. Chicago Booth Research Paper. pp. 13-75.

Mitchell, M., Holland, J. H. and Forrest, S., 2014. Relative building-block fitness and the

building block hypothesis. D. Whitley, Foundations of Genetic Algorithms. pp. 109-

126.

Nørreklit, H. and Mitchell, F., 2014. Contemporary issues on the balance scorecard. Journal

of Accounting & Organizational Change.

Ongore, V.O. and Kusa, G.B., 2013. Determinants of financial performance of commercial

banks in Kenya. International Journal of Economics and Financial Issues. 3(1). p.

237.

Ormiston, A. and Fraser, L. M., 2013. Understanding financial statements. Pearson

Education.

Perkins, M., Grey, A. and Remmers, H., 2014. What do we really mean by “Balanced

Scorecard”?. International Journal of Productivity and Performance Management.

63(2). pp. 148-169.

Richard, O. C., Kirby, S. L. and Chadwick, K., 2013. The impact of racial and gender

diversity in management on financial performance: How participative strategy making

features can unleash a diversity advantage. The International Journal of Human

Resource Management. 24(13). pp. 2571-2582.

Robu, I. B. and Toma, C., 2015. The use of accounting conservatism in order to reflect the

true and the fair view of financial statements in the case of Romanian listed

companies. Global Journal on Humanities and Social Sciences.

Sainaghi, R., Phillips, P. and Corti, V., 2013. Measuring hotel performance: Using a balanced

scorecard perspectives’ approach. International Journal of Hospitality Management,

34, pp. 150-159.

Titman, S., Martin, J. D. and Keown, A. J., 2015. Financial management: Principles and

applications. Prentice Hall.

Vorhies, D.W., Orr, L.M. and Bush, V.D., 2015. Erratum to: Improving customer-focused

marketing capabilities and firm financial performance via marketing exploration and

exploitation. Academy of Marketing Science. Journal. 43(1). p. 136.

Wang, H. and Choi, J., 2013. A new look at the corporate social–financial performance

relationship the moderating roles of temporal and interdomain consistency in corporate

social performance. Journal of Management. 39(2). pp. 416-441.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.