The variable costs are raw materials

Added on 2022-09-08

11 Pages1342 Words16 Views

Running Head: ACCOUNTING 1

ACCOUNTING

ACCOUNTING

Running Head: ACCOUNTING

Contents

Question 1........................................................................................................................................3

Part a............................................................................................................................................3

Part b............................................................................................................................................4

Part c............................................................................................................................................4

Part D...........................................................................................................................................5

Part E)..........................................................................................................................................5

Question 2........................................................................................................................................6

A...................................................................................................................................................6

B...................................................................................................................................................7

Question 3........................................................................................................................................8

References......................................................................................................................................10

Contents

Question 1........................................................................................................................................3

Part a............................................................................................................................................3

Part b............................................................................................................................................4

Part c............................................................................................................................................4

Part D...........................................................................................................................................5

Part E)..........................................................................................................................................5

Question 2........................................................................................................................................6

A...................................................................................................................................................6

B...................................................................................................................................................7

Question 3........................................................................................................................................8

References......................................................................................................................................10

Running Head: ACCOUNTING

Question 1

Part a

Product costs

When the costs are incurred to create a product they are termed as the product costs. Such

costs are inclusive of direct labor, materials, supplies as well as consumable products, overheads.

The costs which are basically required to cater the service to the customer are known as the

product costs. For example, the example costs are inventory cost, trading costs (Spickova &

Myskova, 2015).

Period costs

There are certain costs which cannot be capitalized into prepaid expenses, or fixed assets.

In case of the period costs, the cost is more attached with the passage of time with a transactional

event. Most of the times, these costs are a part of income statement under the heading of selling

and administrative expenses category. For example, selling expenses and administrative

expenses such as salaries related to the production of the product.

Variable costs

Variable costs are costs that change as the quantity of the good or service that a business

produces changes. Variable costs are those costs that can fluctuate over the period and it can also

be recognized as summation of marginal costs over the units pmanufactured. The variable costs

are raw materials and purchases falling as te best example of variable costs (Klychova, Zakirova,

Zakirov & Valieva, 2015).

Fixed costs

Question 1

Part a

Product costs

When the costs are incurred to create a product they are termed as the product costs. Such

costs are inclusive of direct labor, materials, supplies as well as consumable products, overheads.

The costs which are basically required to cater the service to the customer are known as the

product costs. For example, the example costs are inventory cost, trading costs (Spickova &

Myskova, 2015).

Period costs

There are certain costs which cannot be capitalized into prepaid expenses, or fixed assets.

In case of the period costs, the cost is more attached with the passage of time with a transactional

event. Most of the times, these costs are a part of income statement under the heading of selling

and administrative expenses category. For example, selling expenses and administrative

expenses such as salaries related to the production of the product.

Variable costs

Variable costs are costs that change as the quantity of the good or service that a business

produces changes. Variable costs are those costs that can fluctuate over the period and it can also

be recognized as summation of marginal costs over the units pmanufactured. The variable costs

are raw materials and purchases falling as te best example of variable costs (Klychova, Zakirova,

Zakirov & Valieva, 2015).

Fixed costs

Running Head: ACCOUNTING

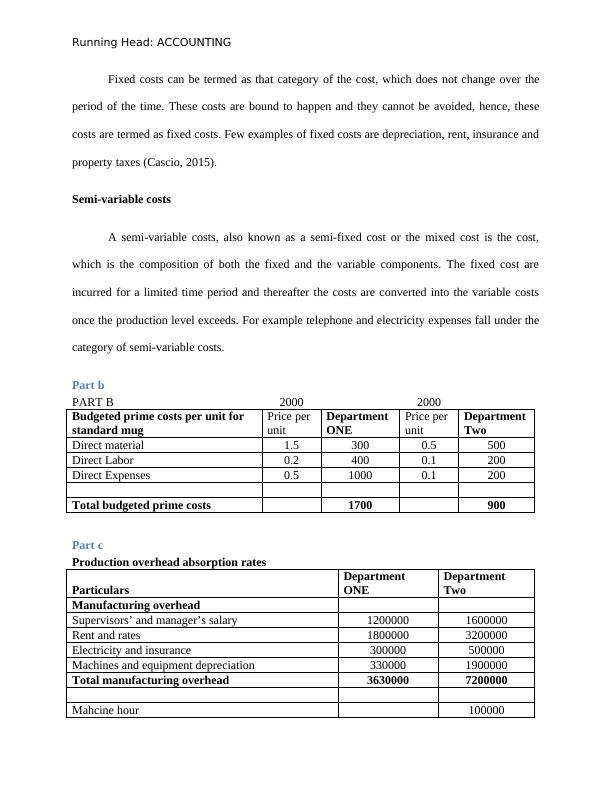

Fixed costs can be termed as that category of the cost, which does not change over the

period of the time. These costs are bound to happen and they cannot be avoided, hence, these

costs are termed as fixed costs. Few examples of fixed costs are depreciation, rent, insurance and

property taxes (Cascio, 2015).

Semi-variable costs

A semi-variable costs, also known as a semi-fixed cost or the mixed cost is the cost,

which is the composition of both the fixed and the variable components. The fixed cost are

incurred for a limited time period and thereafter the costs are converted into the variable costs

once the production level exceeds. For example telephone and electricity expenses fall under the

category of semi-variable costs.

Part b

PART B 2000 2000

Budgeted prime costs per unit for

standard mug

Price per

unit

Department

ONE

Price per

unit

Department

Two

Direct material 1.5 300 0.5 500

Direct Labor 0.2 400 0.1 200

Direct Expenses 0.5 1000 0.1 200

Total budgeted prime costs 1700 900

Part c

Production overhead absorption rates

Particulars

Department

ONE

Department

Two

Manufacturing overhead

Supervisors’ and manager’s salary 1200000 1600000

Rent and rates 1800000 3200000

Electricity and insurance 300000 500000

Machines and equipment depreciation 330000 1900000

Total manufacturing overhead 3630000 7200000

Mahcine hour 100000

Fixed costs can be termed as that category of the cost, which does not change over the

period of the time. These costs are bound to happen and they cannot be avoided, hence, these

costs are termed as fixed costs. Few examples of fixed costs are depreciation, rent, insurance and

property taxes (Cascio, 2015).

Semi-variable costs

A semi-variable costs, also known as a semi-fixed cost or the mixed cost is the cost,

which is the composition of both the fixed and the variable components. The fixed cost are

incurred for a limited time period and thereafter the costs are converted into the variable costs

once the production level exceeds. For example telephone and electricity expenses fall under the

category of semi-variable costs.

Part b

PART B 2000 2000

Budgeted prime costs per unit for

standard mug

Price per

unit

Department

ONE

Price per

unit

Department

Two

Direct material 1.5 300 0.5 500

Direct Labor 0.2 400 0.1 200

Direct Expenses 0.5 1000 0.1 200

Total budgeted prime costs 1700 900

Part c

Production overhead absorption rates

Particulars

Department

ONE

Department

Two

Manufacturing overhead

Supervisors’ and manager’s salary 1200000 1600000

Rent and rates 1800000 3200000

Electricity and insurance 300000 500000

Machines and equipment depreciation 330000 1900000

Total manufacturing overhead 3630000 7200000

Mahcine hour 100000

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Cost Management and Budgeting in Business Financelg...

|17

|2668

|203

Preparation of Income Statement and Analysislg...

|10

|1275

|50

Cost Accounting & Costing Methods | Assignmentlg...

|8

|2001

|82

Management Accountinglg...

|4

|437

|73

Management Accounting Costing Budgeting Assignmentlg...

|15

|3716

|148

Using Cost Information for Budgeting and Forecasting in the Management Accountinglg...

|18

|4731

|226