Time Value Concepts in Management Decisions

VerifiedAdded on 2021/06/18

|44

|10106

|153

AI Summary

The value of time value of money is as follows: FV=PV*[1+ (i/n)] (n*t) FV=Future value of money PV=Present value of money i=interest rate n=number of compounding periods per year t=number of years PV n T i n*t i/n 1+(i/n) [1+(i/n)](n*t) PV*[1+(

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: BUSINESS FINANCE

Business Finance

Student Name

University Name

Business Finance

Student Name

University Name

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2

BUSINESS FINANCE

Table of Contents

Task 1 Time value concepts in management decisions...................................................................3

Task 2:-..........................................................................................................................................11

Question 1......................................................................................................................................11

Question 2......................................................................................................................................11

Question 3......................................................................................................................................12

Question 4......................................................................................................................................21

Question 5......................................................................................................................................32

Question 6a....................................................................................................................................34

Question 6b....................................................................................................................................35

Question 7......................................................................................................................................36

Question 8......................................................................................................................................38

Question 9a and 9b........................................................................................................................38

Question 10....................................................................................................................................42

Question 11...................................................................................................................................47

Question 12....................................................................................................................................47

Question 13....................................................................................................................................48

References and Bibliography.........................................................................................................49

BUSINESS FINANCE

Table of Contents

Task 1 Time value concepts in management decisions...................................................................3

Task 2:-..........................................................................................................................................11

Question 1......................................................................................................................................11

Question 2......................................................................................................................................11

Question 3......................................................................................................................................12

Question 4......................................................................................................................................21

Question 5......................................................................................................................................32

Question 6a....................................................................................................................................34

Question 6b....................................................................................................................................35

Question 7......................................................................................................................................36

Question 8......................................................................................................................................38

Question 9a and 9b........................................................................................................................38

Question 10....................................................................................................................................42

Question 11...................................................................................................................................47

Question 12....................................................................................................................................47

Question 13....................................................................................................................................48

References and Bibliography.........................................................................................................49

3

BUSINESS FINANCE

Task 1 Time value concepts in management decisions

Answer a: Fundamentals of time value concepts

The Concept of time value of money indicates that value of money depreciates year after year.

It further reflects that at the present value of money is more than the future value. As per Chan

and Rate (2018), time value of money refers to the concept that the value of money at present is

more than the value the amount of money would have in the future. This is due to the potential

earning capacity of money. A certain amount of money would earn more amount of interest if it

is deposited at an earlier phase provided the rate of interest remains the same (Burns and Walker

2015).

For example, if $1000 is deposited at 10 percent interest for 1 year on 01.01.2018, it would earn

an interest of $100 and the total amount combining the principal and interest would come to

$1100 on 01.01.2019. Again, if the same amount of $1000 is deposited for 6 months on

01.07.2018, at 10 percent it would only yield at interest of 50. This means that the total amount

would come to $ 1050 on 01.01.2019.

The above example shows that money used earlier would bear more utility than used in

the future. One can point out that for same amount of money, the value of disbursement remains

the same but the utility or benefit that can be availed or purchased with that money will be less in

future. This difference is known as opportunity cost which a person incurs because he used a

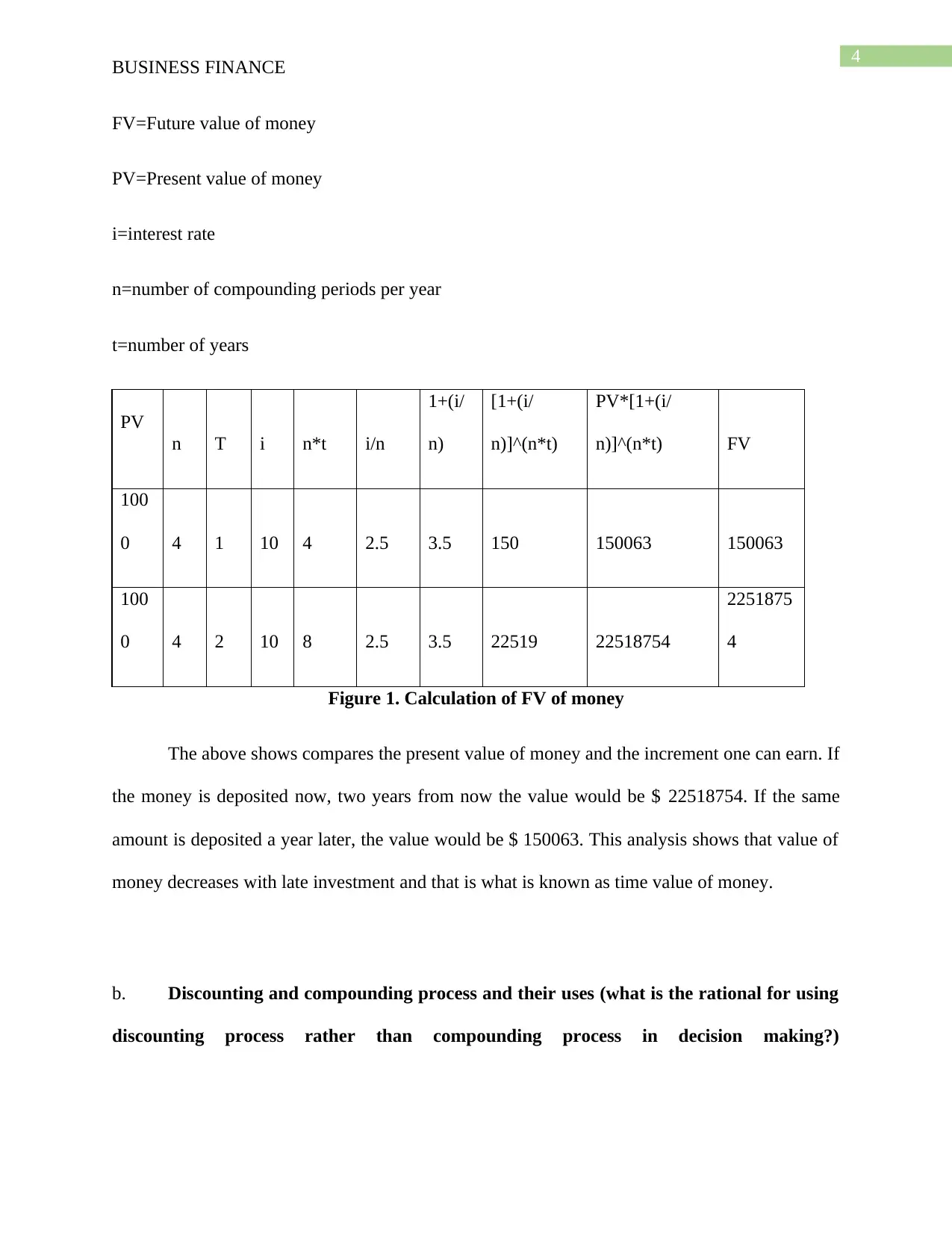

certain amount of money in the future. The value of time value of money is as follows:

FV=PV*[1+ (i/n)] ^ (n*t)

BUSINESS FINANCE

Task 1 Time value concepts in management decisions

Answer a: Fundamentals of time value concepts

The Concept of time value of money indicates that value of money depreciates year after year.

It further reflects that at the present value of money is more than the future value. As per Chan

and Rate (2018), time value of money refers to the concept that the value of money at present is

more than the value the amount of money would have in the future. This is due to the potential

earning capacity of money. A certain amount of money would earn more amount of interest if it

is deposited at an earlier phase provided the rate of interest remains the same (Burns and Walker

2015).

For example, if $1000 is deposited at 10 percent interest for 1 year on 01.01.2018, it would earn

an interest of $100 and the total amount combining the principal and interest would come to

$1100 on 01.01.2019. Again, if the same amount of $1000 is deposited for 6 months on

01.07.2018, at 10 percent it would only yield at interest of 50. This means that the total amount

would come to $ 1050 on 01.01.2019.

The above example shows that money used earlier would bear more utility than used in

the future. One can point out that for same amount of money, the value of disbursement remains

the same but the utility or benefit that can be availed or purchased with that money will be less in

future. This difference is known as opportunity cost which a person incurs because he used a

certain amount of money in the future. The value of time value of money is as follows:

FV=PV*[1+ (i/n)] ^ (n*t)

4

BUSINESS FINANCE

FV=Future value of money

PV=Present value of money

i=interest rate

n=number of compounding periods per year

t=number of years

PV

n T i n*t i/n

1+(i/

n)

[1+(i/

n)]^(n*t)

PV*[1+(i/

n)]^(n*t) FV

100

0 4 1 10 4 2.5 3.5 150 150063 150063

100

0 4 2 10 8 2.5 3.5 22519 22518754

2251875

4

Figure 1. Calculation of FV of money

The above shows compares the present value of money and the increment one can earn. If

the money is deposited now, two years from now the value would be $ 22518754. If the same

amount is deposited a year later, the value would be $ 150063. This analysis shows that value of

money decreases with late investment and that is what is known as time value of money.

b. Discounting and compounding process and their uses (what is the rational for using

discounting process rather than compounding process in decision making?)

BUSINESS FINANCE

FV=Future value of money

PV=Present value of money

i=interest rate

n=number of compounding periods per year

t=number of years

PV

n T i n*t i/n

1+(i/

n)

[1+(i/

n)]^(n*t)

PV*[1+(i/

n)]^(n*t) FV

100

0 4 1 10 4 2.5 3.5 150 150063 150063

100

0 4 2 10 8 2.5 3.5 22519 22518754

2251875

4

Figure 1. Calculation of FV of money

The above shows compares the present value of money and the increment one can earn. If

the money is deposited now, two years from now the value would be $ 22518754. If the same

amount is deposited a year later, the value would be $ 150063. This analysis shows that value of

money decreases with late investment and that is what is known as time value of money.

b. Discounting and compounding process and their uses (what is the rational for using

discounting process rather than compounding process in decision making?)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

5

BUSINESS FINANCE

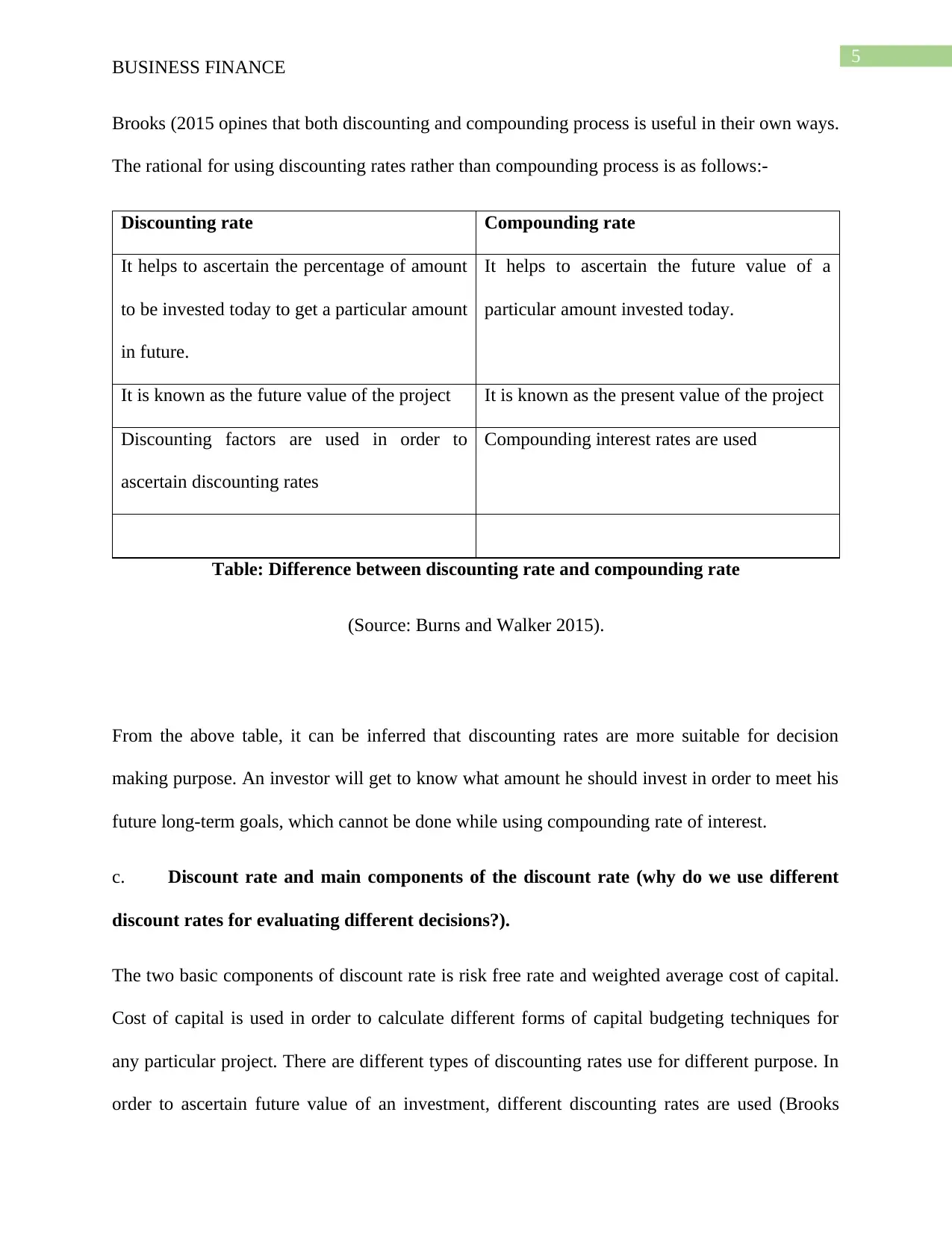

Brooks (2015 opines that both discounting and compounding process is useful in their own ways.

The rational for using discounting rates rather than compounding process is as follows:-

Discounting rate Compounding rate

It helps to ascertain the percentage of amount

to be invested today to get a particular amount

in future.

It helps to ascertain the future value of a

particular amount invested today.

It is known as the future value of the project It is known as the present value of the project

Discounting factors are used in order to

ascertain discounting rates

Compounding interest rates are used

Table: Difference between discounting rate and compounding rate

(Source: Burns and Walker 2015).

From the above table, it can be inferred that discounting rates are more suitable for decision

making purpose. An investor will get to know what amount he should invest in order to meet his

future long-term goals, which cannot be done while using compounding rate of interest.

c. Discount rate and main components of the discount rate (why do we use different

discount rates for evaluating different decisions?).

The two basic components of discount rate is risk free rate and weighted average cost of capital.

Cost of capital is used in order to calculate different forms of capital budgeting techniques for

any particular project. There are different types of discounting rates use for different purpose. In

order to ascertain future value of an investment, different discounting rates are used (Brooks

BUSINESS FINANCE

Brooks (2015 opines that both discounting and compounding process is useful in their own ways.

The rational for using discounting rates rather than compounding process is as follows:-

Discounting rate Compounding rate

It helps to ascertain the percentage of amount

to be invested today to get a particular amount

in future.

It helps to ascertain the future value of a

particular amount invested today.

It is known as the future value of the project It is known as the present value of the project

Discounting factors are used in order to

ascertain discounting rates

Compounding interest rates are used

Table: Difference between discounting rate and compounding rate

(Source: Burns and Walker 2015).

From the above table, it can be inferred that discounting rates are more suitable for decision

making purpose. An investor will get to know what amount he should invest in order to meet his

future long-term goals, which cannot be done while using compounding rate of interest.

c. Discount rate and main components of the discount rate (why do we use different

discount rates for evaluating different decisions?).

The two basic components of discount rate is risk free rate and weighted average cost of capital.

Cost of capital is used in order to calculate different forms of capital budgeting techniques for

any particular project. There are different types of discounting rates use for different purpose. In

order to ascertain future value of an investment, different discounting rates are used (Brooks

6

BUSINESS FINANCE

2015).On the other hand, single discounting values are used to ascertain value of future cash

flows. On the other various discounting techniques, which are as follows:-

Discounted cash flows

Net Present Value

Internal rate of return

All the above types are suitable for different purposes. Net present value is used to ascertain

the excess of future inflows versus outflows. On the other hand, internal rate of return is used

to ascertain the rate of return from a particular project. In addition to this, payback period is

used to determine the time frame to get back the initial investment amount.

d. Use of time value in valuation of financial instruments such as bonds, equity and

preference shares.

There are various forms of financial instruments of time valuation. These can be in the

form of bonds, equity and preference shares. Bonds is generally consider as safe and fixed

money market instrument. Equity is considered as a capital market instrument and yields a high

rate of interest. On the other hand, preference shares also entitles a shareholder to get a fixed

percentage of dividend over a period of time (Faccio, Marchica and Mura 2016). There are

several advantages and disadvantages of these financial instruments which can further evaluated

with the help of the following table:-

Instruments Advantages Disadvantages

Equity 1. High rate of return

2. Limited liability

1. High risk

2. Depends on market

BUSINESS FINANCE

2015).On the other hand, single discounting values are used to ascertain value of future cash

flows. On the other various discounting techniques, which are as follows:-

Discounted cash flows

Net Present Value

Internal rate of return

All the above types are suitable for different purposes. Net present value is used to ascertain

the excess of future inflows versus outflows. On the other hand, internal rate of return is used

to ascertain the rate of return from a particular project. In addition to this, payback period is

used to determine the time frame to get back the initial investment amount.

d. Use of time value in valuation of financial instruments such as bonds, equity and

preference shares.

There are various forms of financial instruments of time valuation. These can be in the

form of bonds, equity and preference shares. Bonds is generally consider as safe and fixed

money market instrument. Equity is considered as a capital market instrument and yields a high

rate of interest. On the other hand, preference shares also entitles a shareholder to get a fixed

percentage of dividend over a period of time (Faccio, Marchica and Mura 2016). There are

several advantages and disadvantages of these financial instruments which can further evaluated

with the help of the following table:-

Instruments Advantages Disadvantages

Equity 1. High rate of return

2. Limited liability

1. High risk

2. Depends on market

7

BUSINESS FINANCE

fluctuation

3. High volatility

Bonds 1. Low volatility

2. Liquidity is high

3. Less risky investment

1. Reinvestment risk is

there

2. Fixed rate of interest

which can be lower

than market prices

3. The investors will lose

their money if the

company is declared

bankrupt

4. Exchange rate risk is

also there

Preference shares 1. Fixed rate of dividend

2. Less risky

1. No voting rights

2. Low rate of return

Table: Advantages and disadvantages of financial instruments

(Source: Delaney, Rich and Rose 2016)

From the above table, it can be inferred that all the given financial instruments have several

advantages and disadvantages. It will solely depend upon the investor in which financial

BUSINESS FINANCE

fluctuation

3. High volatility

Bonds 1. Low volatility

2. Liquidity is high

3. Less risky investment

1. Reinvestment risk is

there

2. Fixed rate of interest

which can be lower

than market prices

3. The investors will lose

their money if the

company is declared

bankrupt

4. Exchange rate risk is

also there

Preference shares 1. Fixed rate of dividend

2. Less risky

1. No voting rights

2. Low rate of return

Table: Advantages and disadvantages of financial instruments

(Source: Delaney, Rich and Rose 2016)

From the above table, it can be inferred that all the given financial instruments have several

advantages and disadvantages. It will solely depend upon the investor in which financial

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

BUSINESS FINANCE

instrument he/she will invest. Apart from this, it is choice of the investor whether he will choose

risk prone investments and risk free requirements according to the respective aims and objectives

(Finnerty 2013).

e. Capital budgeting and time value.

Delaney, Rich and Rose (2016) defined capital budgeting as the process in which

business organizations, especially large business organizations determine the potential

expenditure and return on investments which they can face in the future.

Time value of money is important for capital budgeting. There are various factors which affect

capital budgeting like time value, discount rates and converting values. Future value and present

value is critical in case of capital budgeting.

Using time value of money, an investor can understand the decision of investment in a project in

a better manner.

BUSINESS FINANCE

instrument he/she will invest. Apart from this, it is choice of the investor whether he will choose

risk prone investments and risk free requirements according to the respective aims and objectives

(Finnerty 2013).

e. Capital budgeting and time value.

Delaney, Rich and Rose (2016) defined capital budgeting as the process in which

business organizations, especially large business organizations determine the potential

expenditure and return on investments which they can face in the future.

Time value of money is important for capital budgeting. There are various factors which affect

capital budgeting like time value, discount rates and converting values. Future value and present

value is critical in case of capital budgeting.

Using time value of money, an investor can understand the decision of investment in a project in

a better manner.

9

BUSINESS FINANCE

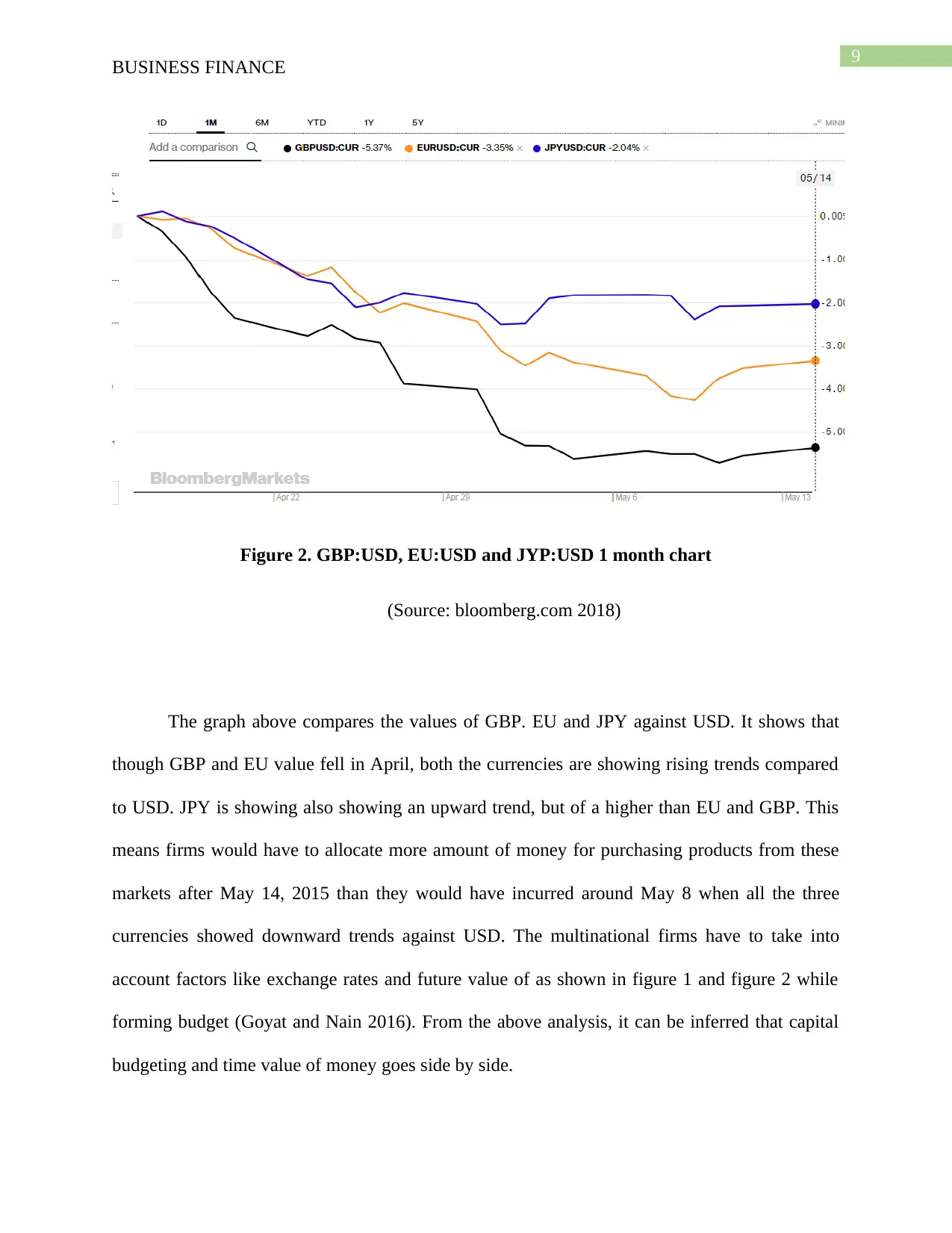

Figure 2. GBP:USD, EU:USD and JYP:USD 1 month chart

(Source: bloomberg.com 2018)

The graph above compares the values of GBP. EU and JPY against USD. It shows that

though GBP and EU value fell in April, both the currencies are showing rising trends compared

to USD. JPY is showing also showing an upward trend, but of a higher than EU and GBP. This

means firms would have to allocate more amount of money for purchasing products from these

markets after May 14, 2015 than they would have incurred around May 8 when all the three

currencies showed downward trends against USD. The multinational firms have to take into

account factors like exchange rates and future value of as shown in figure 1 and figure 2 while

forming budget (Goyat and Nain 2016). From the above analysis, it can be inferred that capital

budgeting and time value of money goes side by side.

BUSINESS FINANCE

Figure 2. GBP:USD, EU:USD and JYP:USD 1 month chart

(Source: bloomberg.com 2018)

The graph above compares the values of GBP. EU and JPY against USD. It shows that

though GBP and EU value fell in April, both the currencies are showing rising trends compared

to USD. JPY is showing also showing an upward trend, but of a higher than EU and GBP. This

means firms would have to allocate more amount of money for purchasing products from these

markets after May 14, 2015 than they would have incurred around May 8 when all the three

currencies showed downward trends against USD. The multinational firms have to take into

account factors like exchange rates and future value of as shown in figure 1 and figure 2 while

forming budget (Goyat and Nain 2016). From the above analysis, it can be inferred that capital

budgeting and time value of money goes side by side.

10

BUSINESS FINANCE

f. The other issues

There are various issues or disadvantages associated with time value of money. These can be as

follows:-

Calculation of Net Present value is sensitive with discounting rates- Net present value

is based on summation of all the respective discounted cash flow of any particular given

project. Therefore, any considerable percentage of increase or decrease of discounted

cash flows can reflect a wrong value of Net present Value (Brooks 2015).

Cannot use different rates of discounted cash flows- It is true that market rates cannot

be same for entire time horizon. It may happen that the risk is more in first year in

comparison with the second year. However, capital budgeting techniques of NPV, IRR

keeps the discounting rate same for the entire time horizon. This can be considered as

another issue of these methods.

Real options are excluded- The calculations of NPV or any capital budgeting technique

do not include real options which are there in a respective project. This can be considered

as a disadvantage of capital budgeting methods.

These are the disadvantages which are associated with time value of money.

BUSINESS FINANCE

f. The other issues

There are various issues or disadvantages associated with time value of money. These can be as

follows:-

Calculation of Net Present value is sensitive with discounting rates- Net present value

is based on summation of all the respective discounted cash flow of any particular given

project. Therefore, any considerable percentage of increase or decrease of discounted

cash flows can reflect a wrong value of Net present Value (Brooks 2015).

Cannot use different rates of discounted cash flows- It is true that market rates cannot

be same for entire time horizon. It may happen that the risk is more in first year in

comparison with the second year. However, capital budgeting techniques of NPV, IRR

keeps the discounting rate same for the entire time horizon. This can be considered as

another issue of these methods.

Real options are excluded- The calculations of NPV or any capital budgeting technique

do not include real options which are there in a respective project. This can be considered

as a disadvantage of capital budgeting methods.

These are the disadvantages which are associated with time value of money.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

11

BUSINESS FINANCE

Task 2:-

Question 1

Financial goals of Studebaker

There are several financial goals of Studebaker which are as follows:-

He wants to accumulate as much additional money as he could as he is planning an early

retirement in next 20 years or by 2038 at the age of 60.

He had a mortgage which he had to clear within next 20 years

He wanted to accumulate all the funds of the money market into one single life insurance

policy.

However, it is not a correct goal. There are few reasons behind it. These reasons are as follows:-

Opportunity costs are not taken into consideration

The annual costs will be 47,145.31 if the excess amount of money market is

introduced into one single life insurance policy.

Life insurance would give him only 6 percent interest, however, any long term

investment will give him around 7 percent rate of interest.

He should invest in safety funds and try to avoid market risks.

Therefore, the financial goals of Studebaker cannot be considered as effective.

Question 2

The given return has been calculated by assuming 6 percent return on the total amount invested

$550,000. This return is calculated on the basis of accumulation. With the help of this, total

accumulated value of the single insurance premium has been calculated.

BUSINESS FINANCE

Task 2:-

Question 1

Financial goals of Studebaker

There are several financial goals of Studebaker which are as follows:-

He wants to accumulate as much additional money as he could as he is planning an early

retirement in next 20 years or by 2038 at the age of 60.

He had a mortgage which he had to clear within next 20 years

He wanted to accumulate all the funds of the money market into one single life insurance

policy.

However, it is not a correct goal. There are few reasons behind it. These reasons are as follows:-

Opportunity costs are not taken into consideration

The annual costs will be 47,145.31 if the excess amount of money market is

introduced into one single life insurance policy.

Life insurance would give him only 6 percent interest, however, any long term

investment will give him around 7 percent rate of interest.

He should invest in safety funds and try to avoid market risks.

Therefore, the financial goals of Studebaker cannot be considered as effective.

Question 2

The given return has been calculated by assuming 6 percent return on the total amount invested

$550,000. This return is calculated on the basis of accumulation. With the help of this, total

accumulated value of the single insurance premium has been calculated.

12

BUSINESS FINANCE

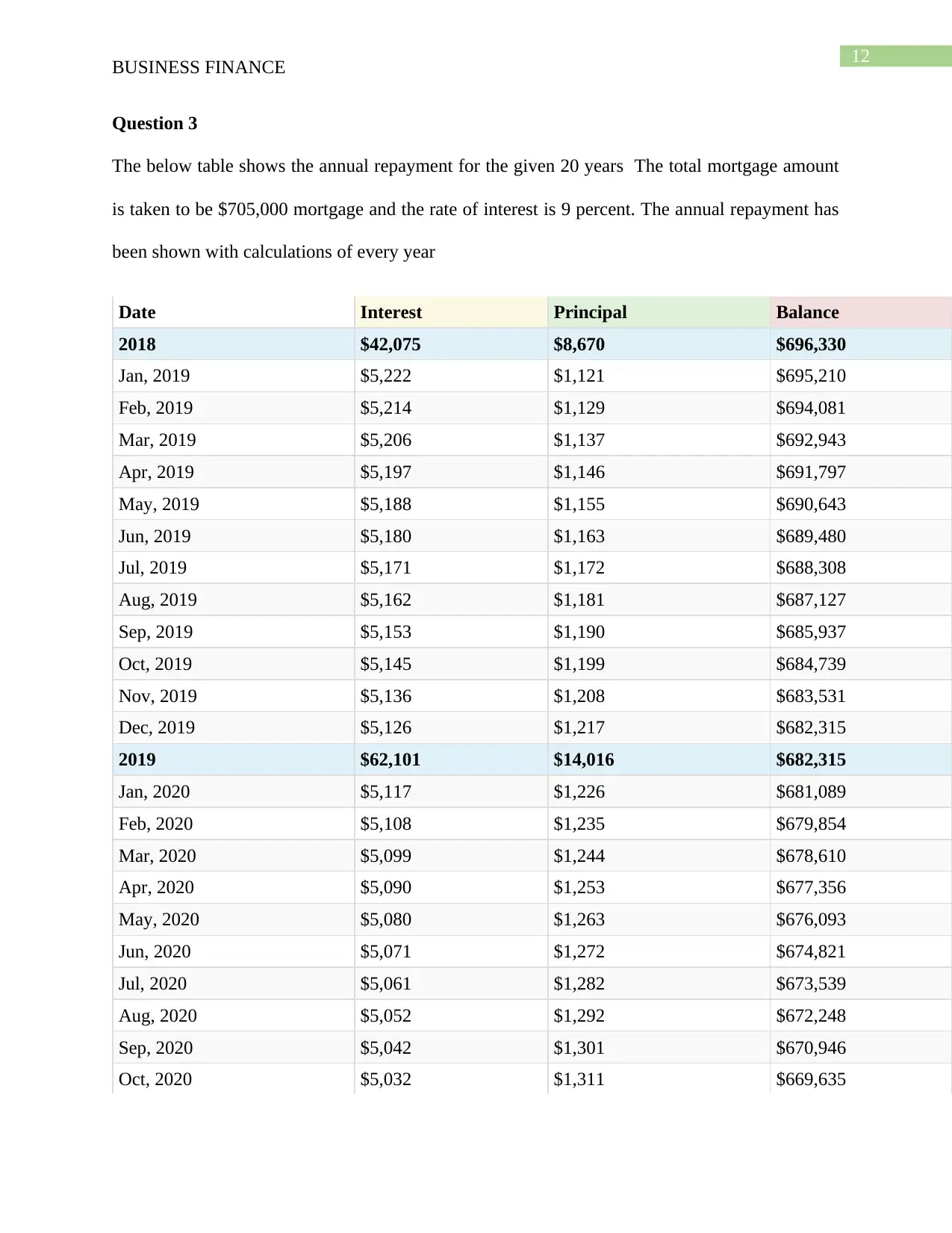

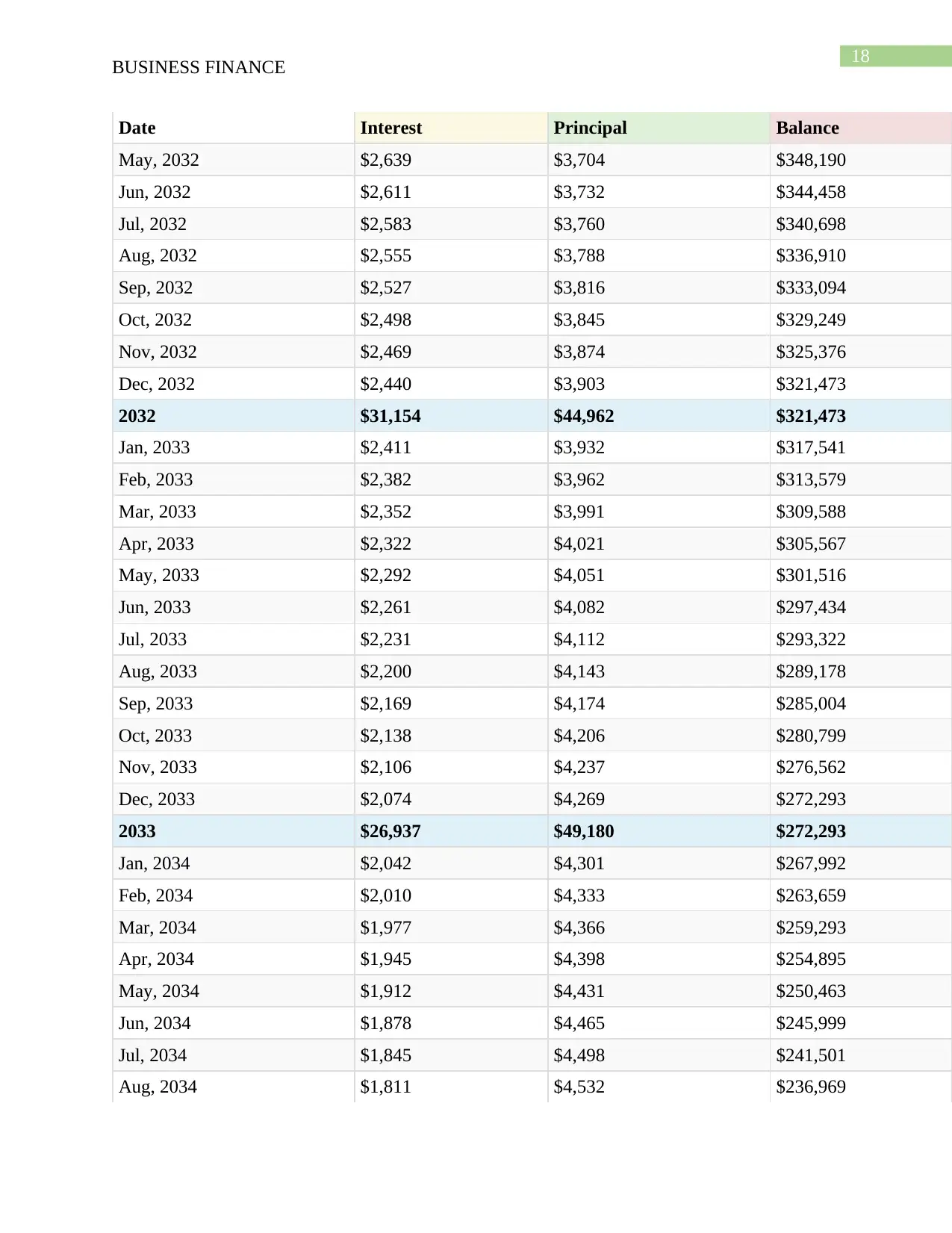

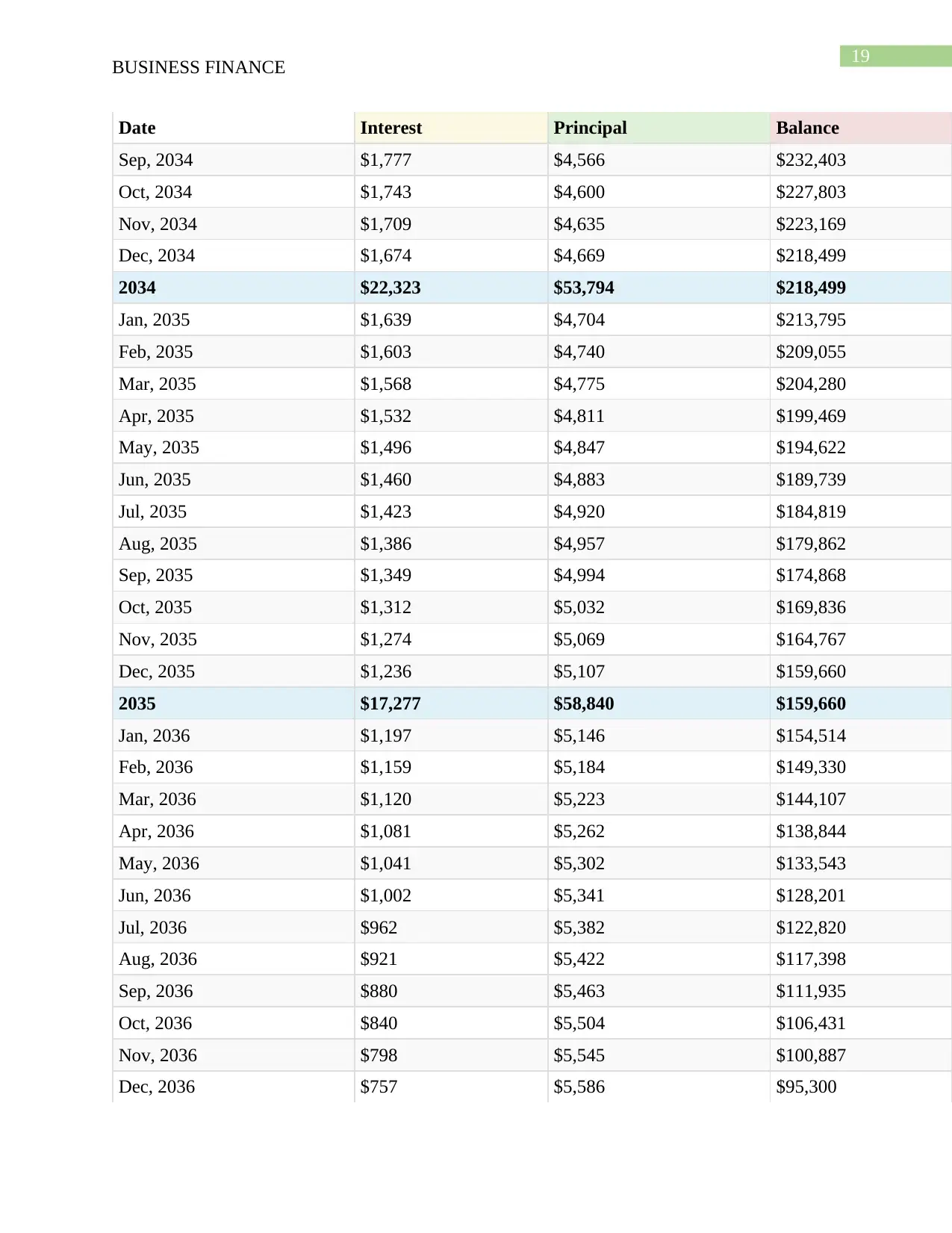

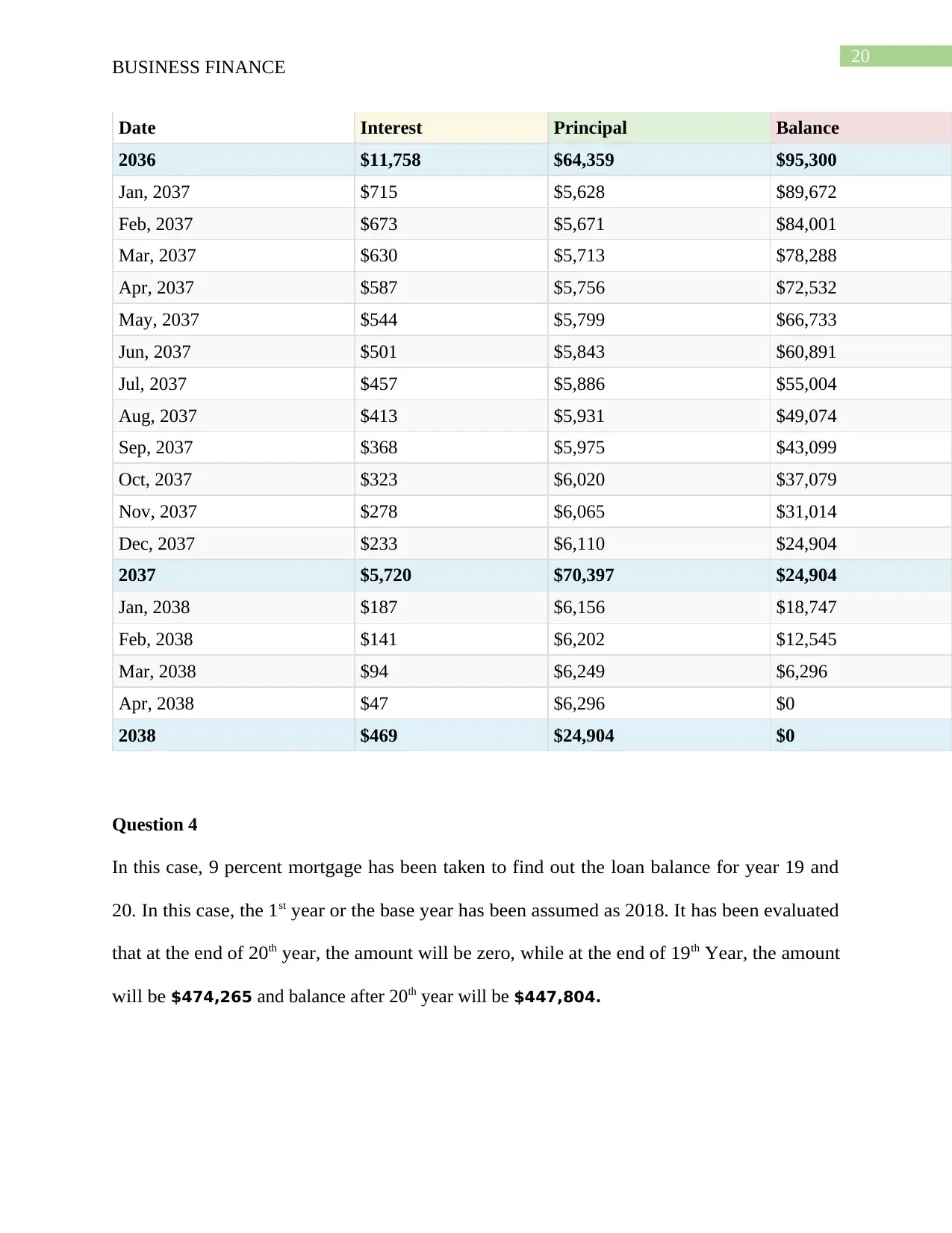

Question 3

The below table shows the annual repayment for the given 20 years The total mortgage amount

is taken to be $705,000 mortgage and the rate of interest is 9 percent. The annual repayment has

been shown with calculations of every year

Date Interest Principal Balance

2018 $42,075 $8,670 $696,330

Jan, 2019 $5,222 $1,121 $695,210

Feb, 2019 $5,214 $1,129 $694,081

Mar, 2019 $5,206 $1,137 $692,943

Apr, 2019 $5,197 $1,146 $691,797

May, 2019 $5,188 $1,155 $690,643

Jun, 2019 $5,180 $1,163 $689,480

Jul, 2019 $5,171 $1,172 $688,308

Aug, 2019 $5,162 $1,181 $687,127

Sep, 2019 $5,153 $1,190 $685,937

Oct, 2019 $5,145 $1,199 $684,739

Nov, 2019 $5,136 $1,208 $683,531

Dec, 2019 $5,126 $1,217 $682,315

2019 $62,101 $14,016 $682,315

Jan, 2020 $5,117 $1,226 $681,089

Feb, 2020 $5,108 $1,235 $679,854

Mar, 2020 $5,099 $1,244 $678,610

Apr, 2020 $5,090 $1,253 $677,356

May, 2020 $5,080 $1,263 $676,093

Jun, 2020 $5,071 $1,272 $674,821

Jul, 2020 $5,061 $1,282 $673,539

Aug, 2020 $5,052 $1,292 $672,248

Sep, 2020 $5,042 $1,301 $670,946

Oct, 2020 $5,032 $1,311 $669,635

BUSINESS FINANCE

Question 3

The below table shows the annual repayment for the given 20 years The total mortgage amount

is taken to be $705,000 mortgage and the rate of interest is 9 percent. The annual repayment has

been shown with calculations of every year

Date Interest Principal Balance

2018 $42,075 $8,670 $696,330

Jan, 2019 $5,222 $1,121 $695,210

Feb, 2019 $5,214 $1,129 $694,081

Mar, 2019 $5,206 $1,137 $692,943

Apr, 2019 $5,197 $1,146 $691,797

May, 2019 $5,188 $1,155 $690,643

Jun, 2019 $5,180 $1,163 $689,480

Jul, 2019 $5,171 $1,172 $688,308

Aug, 2019 $5,162 $1,181 $687,127

Sep, 2019 $5,153 $1,190 $685,937

Oct, 2019 $5,145 $1,199 $684,739

Nov, 2019 $5,136 $1,208 $683,531

Dec, 2019 $5,126 $1,217 $682,315

2019 $62,101 $14,016 $682,315

Jan, 2020 $5,117 $1,226 $681,089

Feb, 2020 $5,108 $1,235 $679,854

Mar, 2020 $5,099 $1,244 $678,610

Apr, 2020 $5,090 $1,253 $677,356

May, 2020 $5,080 $1,263 $676,093

Jun, 2020 $5,071 $1,272 $674,821

Jul, 2020 $5,061 $1,282 $673,539

Aug, 2020 $5,052 $1,292 $672,248

Sep, 2020 $5,042 $1,301 $670,946

Oct, 2020 $5,032 $1,311 $669,635

13

BUSINESS FINANCE

Date Interest Principal Balance

Nov, 2020 $5,022 $1,321 $668,315

Dec, 2020 $5,012 $1,331 $666,984

2020 $60,786 $15,331 $666,984

Jan, 2021 $5,002 $1,341 $665,643

Feb, 2021 $4,992 $1,351 $664,292

Mar, 2021 $4,982 $1,361 $662,932

Apr, 2021 $4,972 $1,371 $661,561

May, 2021 $4,962 $1,381 $660,179

Jun, 2021 $4,951 $1,392 $658,787

Jul, 2021 $4,941 $1,402 $657,385

Aug, 2021 $4,930 $1,413 $655,973

Sep, 2021 $4,920 $1,423 $654,549

Oct, 2021 $4,909 $1,434 $653,115

Nov, 2021 $4,898 $1,445 $651,671

Dec, 2021 $4,888 $1,456 $650,215

2021 $59,348 $16,769 $650,215

Jan, 2022 $4,877 $1,466 $648,749

Feb, 2022 $4,866 $1,477 $647,271

Mar, 2022 $4,855 $1,489 $645,783

Apr, 2022 $4,843 $1,500 $644,283

May, 2022 $4,832 $1,511 $642,772

Jun, 2022 $4,821 $1,522 $641,250

Jul, 2022 $4,809 $1,534 $639,716

Aug, 2022 $4,798 $1,545 $638,171

Sep, 2022 $4,786 $1,557 $636,614

Oct, 2022 $4,775 $1,568 $635,046

Nov, 2022 $4,763 $1,580 $633,465

Dec, 2022 $4,751 $1,592 $631,873

2022 $57,775 $18,342 $631,873

Jan, 2023 $4,739 $1,604 $630,269

BUSINESS FINANCE

Date Interest Principal Balance

Nov, 2020 $5,022 $1,321 $668,315

Dec, 2020 $5,012 $1,331 $666,984

2020 $60,786 $15,331 $666,984

Jan, 2021 $5,002 $1,341 $665,643

Feb, 2021 $4,992 $1,351 $664,292

Mar, 2021 $4,982 $1,361 $662,932

Apr, 2021 $4,972 $1,371 $661,561

May, 2021 $4,962 $1,381 $660,179

Jun, 2021 $4,951 $1,392 $658,787

Jul, 2021 $4,941 $1,402 $657,385

Aug, 2021 $4,930 $1,413 $655,973

Sep, 2021 $4,920 $1,423 $654,549

Oct, 2021 $4,909 $1,434 $653,115

Nov, 2021 $4,898 $1,445 $651,671

Dec, 2021 $4,888 $1,456 $650,215

2021 $59,348 $16,769 $650,215

Jan, 2022 $4,877 $1,466 $648,749

Feb, 2022 $4,866 $1,477 $647,271

Mar, 2022 $4,855 $1,489 $645,783

Apr, 2022 $4,843 $1,500 $644,283

May, 2022 $4,832 $1,511 $642,772

Jun, 2022 $4,821 $1,522 $641,250

Jul, 2022 $4,809 $1,534 $639,716

Aug, 2022 $4,798 $1,545 $638,171

Sep, 2022 $4,786 $1,557 $636,614

Oct, 2022 $4,775 $1,568 $635,046

Nov, 2022 $4,763 $1,580 $633,465

Dec, 2022 $4,751 $1,592 $631,873

2022 $57,775 $18,342 $631,873

Jan, 2023 $4,739 $1,604 $630,269

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

14

BUSINESS FINANCE

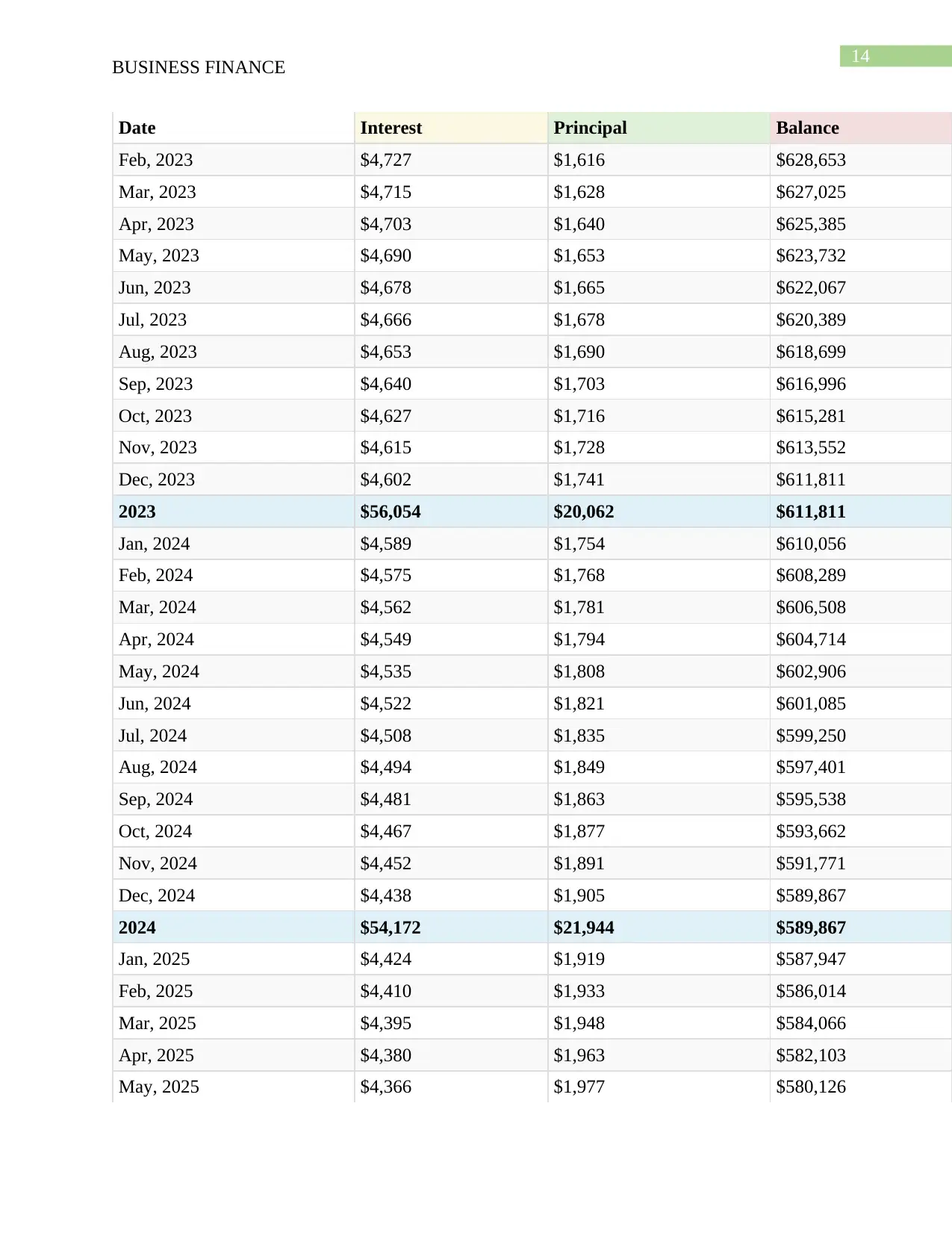

Date Interest Principal Balance

Feb, 2023 $4,727 $1,616 $628,653

Mar, 2023 $4,715 $1,628 $627,025

Apr, 2023 $4,703 $1,640 $625,385

May, 2023 $4,690 $1,653 $623,732

Jun, 2023 $4,678 $1,665 $622,067

Jul, 2023 $4,666 $1,678 $620,389

Aug, 2023 $4,653 $1,690 $618,699

Sep, 2023 $4,640 $1,703 $616,996

Oct, 2023 $4,627 $1,716 $615,281

Nov, 2023 $4,615 $1,728 $613,552

Dec, 2023 $4,602 $1,741 $611,811

2023 $56,054 $20,062 $611,811

Jan, 2024 $4,589 $1,754 $610,056

Feb, 2024 $4,575 $1,768 $608,289

Mar, 2024 $4,562 $1,781 $606,508

Apr, 2024 $4,549 $1,794 $604,714

May, 2024 $4,535 $1,808 $602,906

Jun, 2024 $4,522 $1,821 $601,085

Jul, 2024 $4,508 $1,835 $599,250

Aug, 2024 $4,494 $1,849 $597,401

Sep, 2024 $4,481 $1,863 $595,538

Oct, 2024 $4,467 $1,877 $593,662

Nov, 2024 $4,452 $1,891 $591,771

Dec, 2024 $4,438 $1,905 $589,867

2024 $54,172 $21,944 $589,867

Jan, 2025 $4,424 $1,919 $587,947

Feb, 2025 $4,410 $1,933 $586,014

Mar, 2025 $4,395 $1,948 $584,066

Apr, 2025 $4,380 $1,963 $582,103

May, 2025 $4,366 $1,977 $580,126

BUSINESS FINANCE

Date Interest Principal Balance

Feb, 2023 $4,727 $1,616 $628,653

Mar, 2023 $4,715 $1,628 $627,025

Apr, 2023 $4,703 $1,640 $625,385

May, 2023 $4,690 $1,653 $623,732

Jun, 2023 $4,678 $1,665 $622,067

Jul, 2023 $4,666 $1,678 $620,389

Aug, 2023 $4,653 $1,690 $618,699

Sep, 2023 $4,640 $1,703 $616,996

Oct, 2023 $4,627 $1,716 $615,281

Nov, 2023 $4,615 $1,728 $613,552

Dec, 2023 $4,602 $1,741 $611,811

2023 $56,054 $20,062 $611,811

Jan, 2024 $4,589 $1,754 $610,056

Feb, 2024 $4,575 $1,768 $608,289

Mar, 2024 $4,562 $1,781 $606,508

Apr, 2024 $4,549 $1,794 $604,714

May, 2024 $4,535 $1,808 $602,906

Jun, 2024 $4,522 $1,821 $601,085

Jul, 2024 $4,508 $1,835 $599,250

Aug, 2024 $4,494 $1,849 $597,401

Sep, 2024 $4,481 $1,863 $595,538

Oct, 2024 $4,467 $1,877 $593,662

Nov, 2024 $4,452 $1,891 $591,771

Dec, 2024 $4,438 $1,905 $589,867

2024 $54,172 $21,944 $589,867

Jan, 2025 $4,424 $1,919 $587,947

Feb, 2025 $4,410 $1,933 $586,014

Mar, 2025 $4,395 $1,948 $584,066

Apr, 2025 $4,380 $1,963 $582,103

May, 2025 $4,366 $1,977 $580,126

15

BUSINESS FINANCE

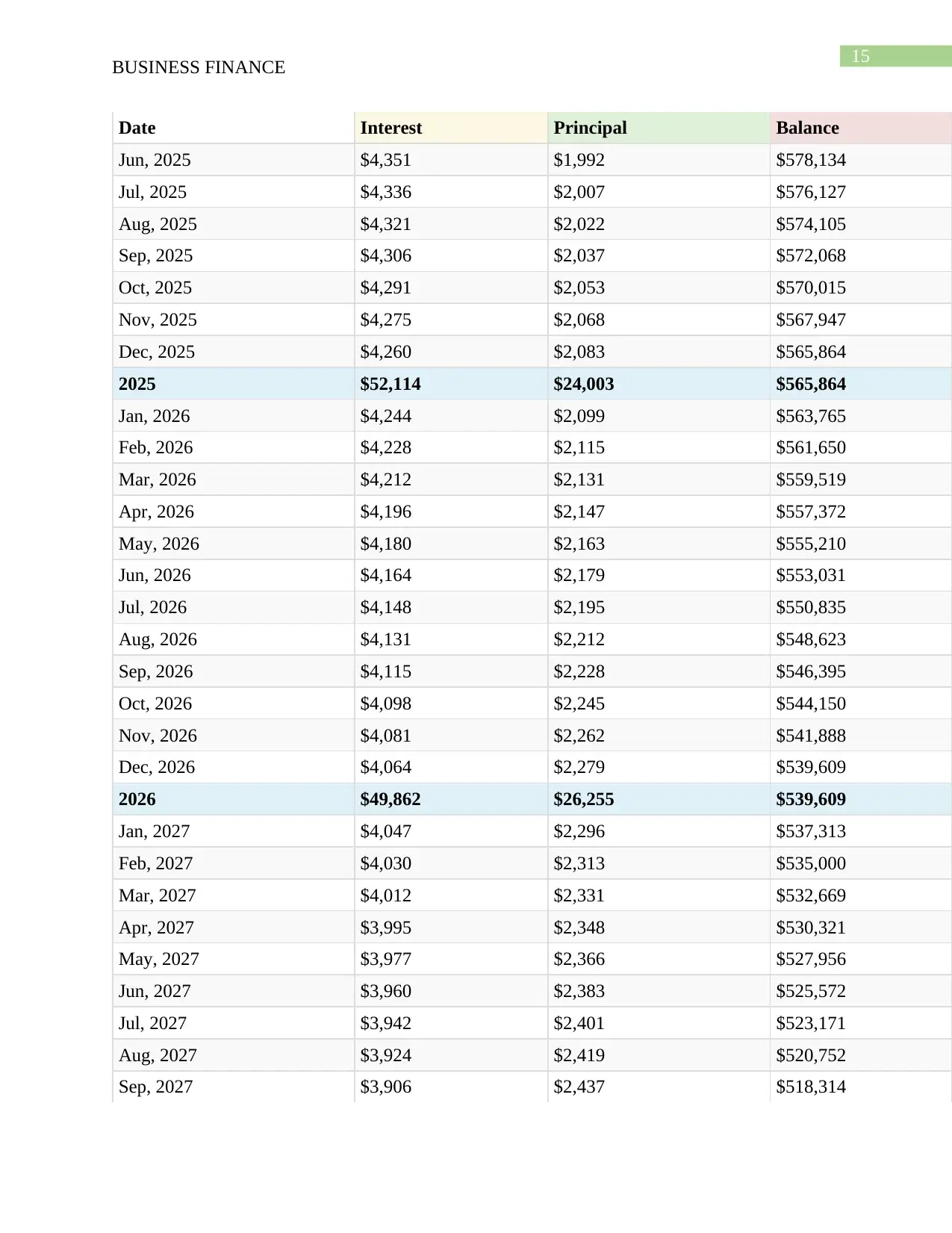

Date Interest Principal Balance

Jun, 2025 $4,351 $1,992 $578,134

Jul, 2025 $4,336 $2,007 $576,127

Aug, 2025 $4,321 $2,022 $574,105

Sep, 2025 $4,306 $2,037 $572,068

Oct, 2025 $4,291 $2,053 $570,015

Nov, 2025 $4,275 $2,068 $567,947

Dec, 2025 $4,260 $2,083 $565,864

2025 $52,114 $24,003 $565,864

Jan, 2026 $4,244 $2,099 $563,765

Feb, 2026 $4,228 $2,115 $561,650

Mar, 2026 $4,212 $2,131 $559,519

Apr, 2026 $4,196 $2,147 $557,372

May, 2026 $4,180 $2,163 $555,210

Jun, 2026 $4,164 $2,179 $553,031

Jul, 2026 $4,148 $2,195 $550,835

Aug, 2026 $4,131 $2,212 $548,623

Sep, 2026 $4,115 $2,228 $546,395

Oct, 2026 $4,098 $2,245 $544,150

Nov, 2026 $4,081 $2,262 $541,888

Dec, 2026 $4,064 $2,279 $539,609

2026 $49,862 $26,255 $539,609

Jan, 2027 $4,047 $2,296 $537,313

Feb, 2027 $4,030 $2,313 $535,000

Mar, 2027 $4,012 $2,331 $532,669

Apr, 2027 $3,995 $2,348 $530,321

May, 2027 $3,977 $2,366 $527,956

Jun, 2027 $3,960 $2,383 $525,572

Jul, 2027 $3,942 $2,401 $523,171

Aug, 2027 $3,924 $2,419 $520,752

Sep, 2027 $3,906 $2,437 $518,314

BUSINESS FINANCE

Date Interest Principal Balance

Jun, 2025 $4,351 $1,992 $578,134

Jul, 2025 $4,336 $2,007 $576,127

Aug, 2025 $4,321 $2,022 $574,105

Sep, 2025 $4,306 $2,037 $572,068

Oct, 2025 $4,291 $2,053 $570,015

Nov, 2025 $4,275 $2,068 $567,947

Dec, 2025 $4,260 $2,083 $565,864

2025 $52,114 $24,003 $565,864

Jan, 2026 $4,244 $2,099 $563,765

Feb, 2026 $4,228 $2,115 $561,650

Mar, 2026 $4,212 $2,131 $559,519

Apr, 2026 $4,196 $2,147 $557,372

May, 2026 $4,180 $2,163 $555,210

Jun, 2026 $4,164 $2,179 $553,031

Jul, 2026 $4,148 $2,195 $550,835

Aug, 2026 $4,131 $2,212 $548,623

Sep, 2026 $4,115 $2,228 $546,395

Oct, 2026 $4,098 $2,245 $544,150

Nov, 2026 $4,081 $2,262 $541,888

Dec, 2026 $4,064 $2,279 $539,609

2026 $49,862 $26,255 $539,609

Jan, 2027 $4,047 $2,296 $537,313

Feb, 2027 $4,030 $2,313 $535,000

Mar, 2027 $4,012 $2,331 $532,669

Apr, 2027 $3,995 $2,348 $530,321

May, 2027 $3,977 $2,366 $527,956

Jun, 2027 $3,960 $2,383 $525,572

Jul, 2027 $3,942 $2,401 $523,171

Aug, 2027 $3,924 $2,419 $520,752

Sep, 2027 $3,906 $2,437 $518,314

16

BUSINESS FINANCE

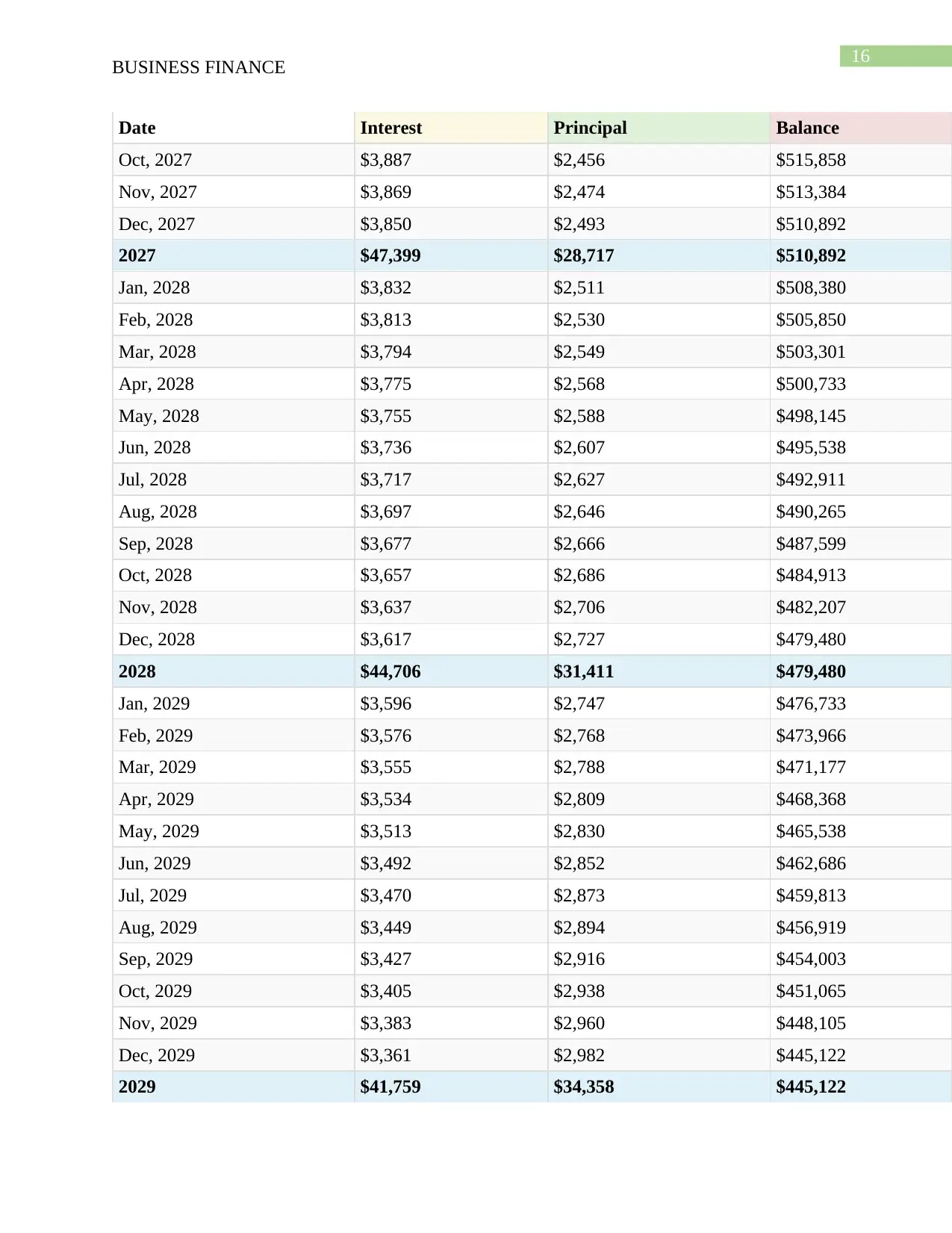

Date Interest Principal Balance

Oct, 2027 $3,887 $2,456 $515,858

Nov, 2027 $3,869 $2,474 $513,384

Dec, 2027 $3,850 $2,493 $510,892

2027 $47,399 $28,717 $510,892

Jan, 2028 $3,832 $2,511 $508,380

Feb, 2028 $3,813 $2,530 $505,850

Mar, 2028 $3,794 $2,549 $503,301

Apr, 2028 $3,775 $2,568 $500,733

May, 2028 $3,755 $2,588 $498,145

Jun, 2028 $3,736 $2,607 $495,538

Jul, 2028 $3,717 $2,627 $492,911

Aug, 2028 $3,697 $2,646 $490,265

Sep, 2028 $3,677 $2,666 $487,599

Oct, 2028 $3,657 $2,686 $484,913

Nov, 2028 $3,637 $2,706 $482,207

Dec, 2028 $3,617 $2,727 $479,480

2028 $44,706 $31,411 $479,480

Jan, 2029 $3,596 $2,747 $476,733

Feb, 2029 $3,576 $2,768 $473,966

Mar, 2029 $3,555 $2,788 $471,177

Apr, 2029 $3,534 $2,809 $468,368

May, 2029 $3,513 $2,830 $465,538

Jun, 2029 $3,492 $2,852 $462,686

Jul, 2029 $3,470 $2,873 $459,813

Aug, 2029 $3,449 $2,894 $456,919

Sep, 2029 $3,427 $2,916 $454,003

Oct, 2029 $3,405 $2,938 $451,065

Nov, 2029 $3,383 $2,960 $448,105

Dec, 2029 $3,361 $2,982 $445,122

2029 $41,759 $34,358 $445,122

BUSINESS FINANCE

Date Interest Principal Balance

Oct, 2027 $3,887 $2,456 $515,858

Nov, 2027 $3,869 $2,474 $513,384

Dec, 2027 $3,850 $2,493 $510,892

2027 $47,399 $28,717 $510,892

Jan, 2028 $3,832 $2,511 $508,380

Feb, 2028 $3,813 $2,530 $505,850

Mar, 2028 $3,794 $2,549 $503,301

Apr, 2028 $3,775 $2,568 $500,733

May, 2028 $3,755 $2,588 $498,145

Jun, 2028 $3,736 $2,607 $495,538

Jul, 2028 $3,717 $2,627 $492,911

Aug, 2028 $3,697 $2,646 $490,265

Sep, 2028 $3,677 $2,666 $487,599

Oct, 2028 $3,657 $2,686 $484,913

Nov, 2028 $3,637 $2,706 $482,207

Dec, 2028 $3,617 $2,727 $479,480

2028 $44,706 $31,411 $479,480

Jan, 2029 $3,596 $2,747 $476,733

Feb, 2029 $3,576 $2,768 $473,966

Mar, 2029 $3,555 $2,788 $471,177

Apr, 2029 $3,534 $2,809 $468,368

May, 2029 $3,513 $2,830 $465,538

Jun, 2029 $3,492 $2,852 $462,686

Jul, 2029 $3,470 $2,873 $459,813

Aug, 2029 $3,449 $2,894 $456,919

Sep, 2029 $3,427 $2,916 $454,003

Oct, 2029 $3,405 $2,938 $451,065

Nov, 2029 $3,383 $2,960 $448,105

Dec, 2029 $3,361 $2,982 $445,122

2029 $41,759 $34,358 $445,122

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

17

BUSINESS FINANCE

Date Interest Principal Balance

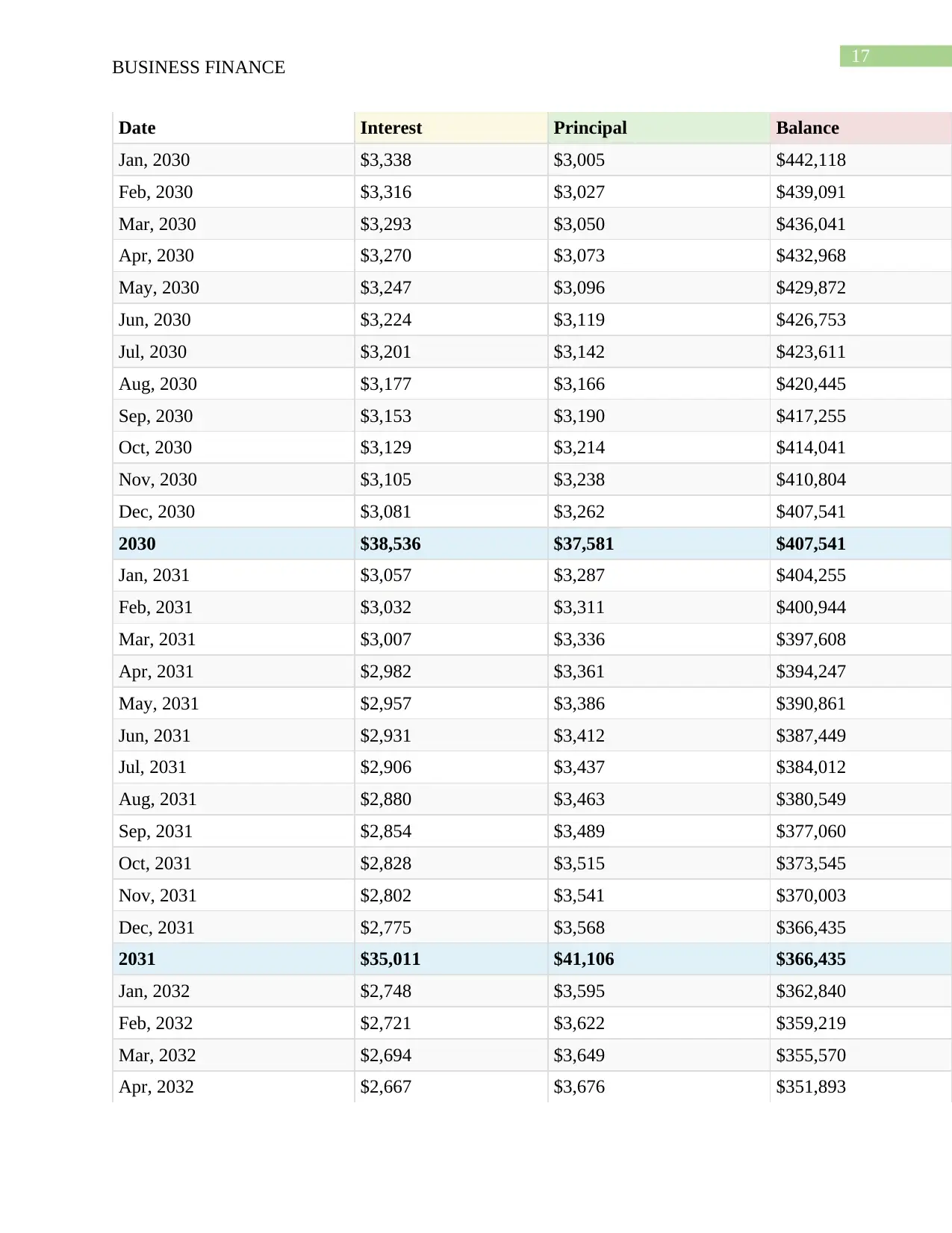

Jan, 2030 $3,338 $3,005 $442,118

Feb, 2030 $3,316 $3,027 $439,091

Mar, 2030 $3,293 $3,050 $436,041

Apr, 2030 $3,270 $3,073 $432,968

May, 2030 $3,247 $3,096 $429,872

Jun, 2030 $3,224 $3,119 $426,753

Jul, 2030 $3,201 $3,142 $423,611

Aug, 2030 $3,177 $3,166 $420,445

Sep, 2030 $3,153 $3,190 $417,255

Oct, 2030 $3,129 $3,214 $414,041

Nov, 2030 $3,105 $3,238 $410,804

Dec, 2030 $3,081 $3,262 $407,541

2030 $38,536 $37,581 $407,541

Jan, 2031 $3,057 $3,287 $404,255

Feb, 2031 $3,032 $3,311 $400,944

Mar, 2031 $3,007 $3,336 $397,608

Apr, 2031 $2,982 $3,361 $394,247

May, 2031 $2,957 $3,386 $390,861

Jun, 2031 $2,931 $3,412 $387,449

Jul, 2031 $2,906 $3,437 $384,012

Aug, 2031 $2,880 $3,463 $380,549

Sep, 2031 $2,854 $3,489 $377,060

Oct, 2031 $2,828 $3,515 $373,545

Nov, 2031 $2,802 $3,541 $370,003

Dec, 2031 $2,775 $3,568 $366,435

2031 $35,011 $41,106 $366,435

Jan, 2032 $2,748 $3,595 $362,840

Feb, 2032 $2,721 $3,622 $359,219

Mar, 2032 $2,694 $3,649 $355,570

Apr, 2032 $2,667 $3,676 $351,893

BUSINESS FINANCE

Date Interest Principal Balance

Jan, 2030 $3,338 $3,005 $442,118

Feb, 2030 $3,316 $3,027 $439,091

Mar, 2030 $3,293 $3,050 $436,041

Apr, 2030 $3,270 $3,073 $432,968

May, 2030 $3,247 $3,096 $429,872

Jun, 2030 $3,224 $3,119 $426,753

Jul, 2030 $3,201 $3,142 $423,611

Aug, 2030 $3,177 $3,166 $420,445

Sep, 2030 $3,153 $3,190 $417,255

Oct, 2030 $3,129 $3,214 $414,041

Nov, 2030 $3,105 $3,238 $410,804

Dec, 2030 $3,081 $3,262 $407,541

2030 $38,536 $37,581 $407,541

Jan, 2031 $3,057 $3,287 $404,255

Feb, 2031 $3,032 $3,311 $400,944

Mar, 2031 $3,007 $3,336 $397,608

Apr, 2031 $2,982 $3,361 $394,247

May, 2031 $2,957 $3,386 $390,861

Jun, 2031 $2,931 $3,412 $387,449

Jul, 2031 $2,906 $3,437 $384,012

Aug, 2031 $2,880 $3,463 $380,549

Sep, 2031 $2,854 $3,489 $377,060

Oct, 2031 $2,828 $3,515 $373,545

Nov, 2031 $2,802 $3,541 $370,003

Dec, 2031 $2,775 $3,568 $366,435

2031 $35,011 $41,106 $366,435

Jan, 2032 $2,748 $3,595 $362,840

Feb, 2032 $2,721 $3,622 $359,219

Mar, 2032 $2,694 $3,649 $355,570

Apr, 2032 $2,667 $3,676 $351,893

18

BUSINESS FINANCE

Date Interest Principal Balance

May, 2032 $2,639 $3,704 $348,190

Jun, 2032 $2,611 $3,732 $344,458

Jul, 2032 $2,583 $3,760 $340,698

Aug, 2032 $2,555 $3,788 $336,910

Sep, 2032 $2,527 $3,816 $333,094

Oct, 2032 $2,498 $3,845 $329,249

Nov, 2032 $2,469 $3,874 $325,376

Dec, 2032 $2,440 $3,903 $321,473

2032 $31,154 $44,962 $321,473

Jan, 2033 $2,411 $3,932 $317,541

Feb, 2033 $2,382 $3,962 $313,579

Mar, 2033 $2,352 $3,991 $309,588

Apr, 2033 $2,322 $4,021 $305,567

May, 2033 $2,292 $4,051 $301,516

Jun, 2033 $2,261 $4,082 $297,434

Jul, 2033 $2,231 $4,112 $293,322

Aug, 2033 $2,200 $4,143 $289,178

Sep, 2033 $2,169 $4,174 $285,004

Oct, 2033 $2,138 $4,206 $280,799

Nov, 2033 $2,106 $4,237 $276,562

Dec, 2033 $2,074 $4,269 $272,293

2033 $26,937 $49,180 $272,293

Jan, 2034 $2,042 $4,301 $267,992

Feb, 2034 $2,010 $4,333 $263,659

Mar, 2034 $1,977 $4,366 $259,293

Apr, 2034 $1,945 $4,398 $254,895

May, 2034 $1,912 $4,431 $250,463

Jun, 2034 $1,878 $4,465 $245,999

Jul, 2034 $1,845 $4,498 $241,501

Aug, 2034 $1,811 $4,532 $236,969

BUSINESS FINANCE

Date Interest Principal Balance

May, 2032 $2,639 $3,704 $348,190

Jun, 2032 $2,611 $3,732 $344,458

Jul, 2032 $2,583 $3,760 $340,698

Aug, 2032 $2,555 $3,788 $336,910

Sep, 2032 $2,527 $3,816 $333,094

Oct, 2032 $2,498 $3,845 $329,249

Nov, 2032 $2,469 $3,874 $325,376

Dec, 2032 $2,440 $3,903 $321,473

2032 $31,154 $44,962 $321,473

Jan, 2033 $2,411 $3,932 $317,541

Feb, 2033 $2,382 $3,962 $313,579

Mar, 2033 $2,352 $3,991 $309,588

Apr, 2033 $2,322 $4,021 $305,567

May, 2033 $2,292 $4,051 $301,516

Jun, 2033 $2,261 $4,082 $297,434

Jul, 2033 $2,231 $4,112 $293,322

Aug, 2033 $2,200 $4,143 $289,178

Sep, 2033 $2,169 $4,174 $285,004

Oct, 2033 $2,138 $4,206 $280,799

Nov, 2033 $2,106 $4,237 $276,562

Dec, 2033 $2,074 $4,269 $272,293

2033 $26,937 $49,180 $272,293

Jan, 2034 $2,042 $4,301 $267,992

Feb, 2034 $2,010 $4,333 $263,659

Mar, 2034 $1,977 $4,366 $259,293

Apr, 2034 $1,945 $4,398 $254,895

May, 2034 $1,912 $4,431 $250,463

Jun, 2034 $1,878 $4,465 $245,999

Jul, 2034 $1,845 $4,498 $241,501

Aug, 2034 $1,811 $4,532 $236,969

19

BUSINESS FINANCE

Date Interest Principal Balance

Sep, 2034 $1,777 $4,566 $232,403

Oct, 2034 $1,743 $4,600 $227,803

Nov, 2034 $1,709 $4,635 $223,169

Dec, 2034 $1,674 $4,669 $218,499

2034 $22,323 $53,794 $218,499

Jan, 2035 $1,639 $4,704 $213,795

Feb, 2035 $1,603 $4,740 $209,055

Mar, 2035 $1,568 $4,775 $204,280

Apr, 2035 $1,532 $4,811 $199,469

May, 2035 $1,496 $4,847 $194,622

Jun, 2035 $1,460 $4,883 $189,739

Jul, 2035 $1,423 $4,920 $184,819

Aug, 2035 $1,386 $4,957 $179,862

Sep, 2035 $1,349 $4,994 $174,868

Oct, 2035 $1,312 $5,032 $169,836

Nov, 2035 $1,274 $5,069 $164,767

Dec, 2035 $1,236 $5,107 $159,660

2035 $17,277 $58,840 $159,660

Jan, 2036 $1,197 $5,146 $154,514

Feb, 2036 $1,159 $5,184 $149,330

Mar, 2036 $1,120 $5,223 $144,107

Apr, 2036 $1,081 $5,262 $138,844

May, 2036 $1,041 $5,302 $133,543

Jun, 2036 $1,002 $5,341 $128,201

Jul, 2036 $962 $5,382 $122,820

Aug, 2036 $921 $5,422 $117,398

Sep, 2036 $880 $5,463 $111,935

Oct, 2036 $840 $5,504 $106,431

Nov, 2036 $798 $5,545 $100,887

Dec, 2036 $757 $5,586 $95,300

BUSINESS FINANCE

Date Interest Principal Balance

Sep, 2034 $1,777 $4,566 $232,403

Oct, 2034 $1,743 $4,600 $227,803

Nov, 2034 $1,709 $4,635 $223,169

Dec, 2034 $1,674 $4,669 $218,499

2034 $22,323 $53,794 $218,499

Jan, 2035 $1,639 $4,704 $213,795

Feb, 2035 $1,603 $4,740 $209,055

Mar, 2035 $1,568 $4,775 $204,280

Apr, 2035 $1,532 $4,811 $199,469

May, 2035 $1,496 $4,847 $194,622

Jun, 2035 $1,460 $4,883 $189,739

Jul, 2035 $1,423 $4,920 $184,819

Aug, 2035 $1,386 $4,957 $179,862

Sep, 2035 $1,349 $4,994 $174,868

Oct, 2035 $1,312 $5,032 $169,836

Nov, 2035 $1,274 $5,069 $164,767

Dec, 2035 $1,236 $5,107 $159,660

2035 $17,277 $58,840 $159,660

Jan, 2036 $1,197 $5,146 $154,514

Feb, 2036 $1,159 $5,184 $149,330

Mar, 2036 $1,120 $5,223 $144,107

Apr, 2036 $1,081 $5,262 $138,844

May, 2036 $1,041 $5,302 $133,543

Jun, 2036 $1,002 $5,341 $128,201

Jul, 2036 $962 $5,382 $122,820

Aug, 2036 $921 $5,422 $117,398

Sep, 2036 $880 $5,463 $111,935

Oct, 2036 $840 $5,504 $106,431

Nov, 2036 $798 $5,545 $100,887

Dec, 2036 $757 $5,586 $95,300

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

20

BUSINESS FINANCE

Date Interest Principal Balance

2036 $11,758 $64,359 $95,300

Jan, 2037 $715 $5,628 $89,672

Feb, 2037 $673 $5,671 $84,001

Mar, 2037 $630 $5,713 $78,288

Apr, 2037 $587 $5,756 $72,532

May, 2037 $544 $5,799 $66,733

Jun, 2037 $501 $5,843 $60,891

Jul, 2037 $457 $5,886 $55,004

Aug, 2037 $413 $5,931 $49,074

Sep, 2037 $368 $5,975 $43,099

Oct, 2037 $323 $6,020 $37,079

Nov, 2037 $278 $6,065 $31,014

Dec, 2037 $233 $6,110 $24,904

2037 $5,720 $70,397 $24,904

Jan, 2038 $187 $6,156 $18,747

Feb, 2038 $141 $6,202 $12,545

Mar, 2038 $94 $6,249 $6,296

Apr, 2038 $47 $6,296 $0

2038 $469 $24,904 $0

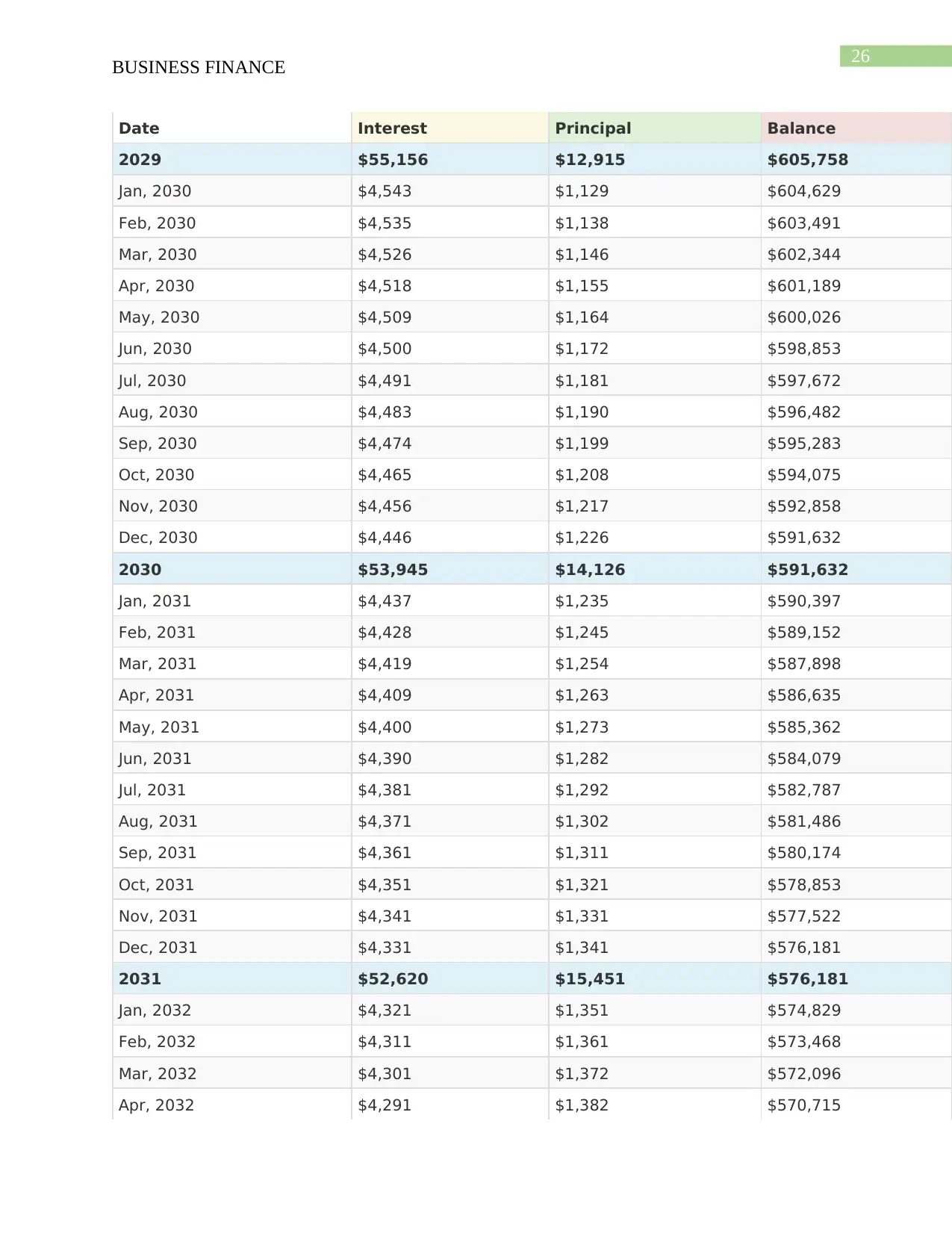

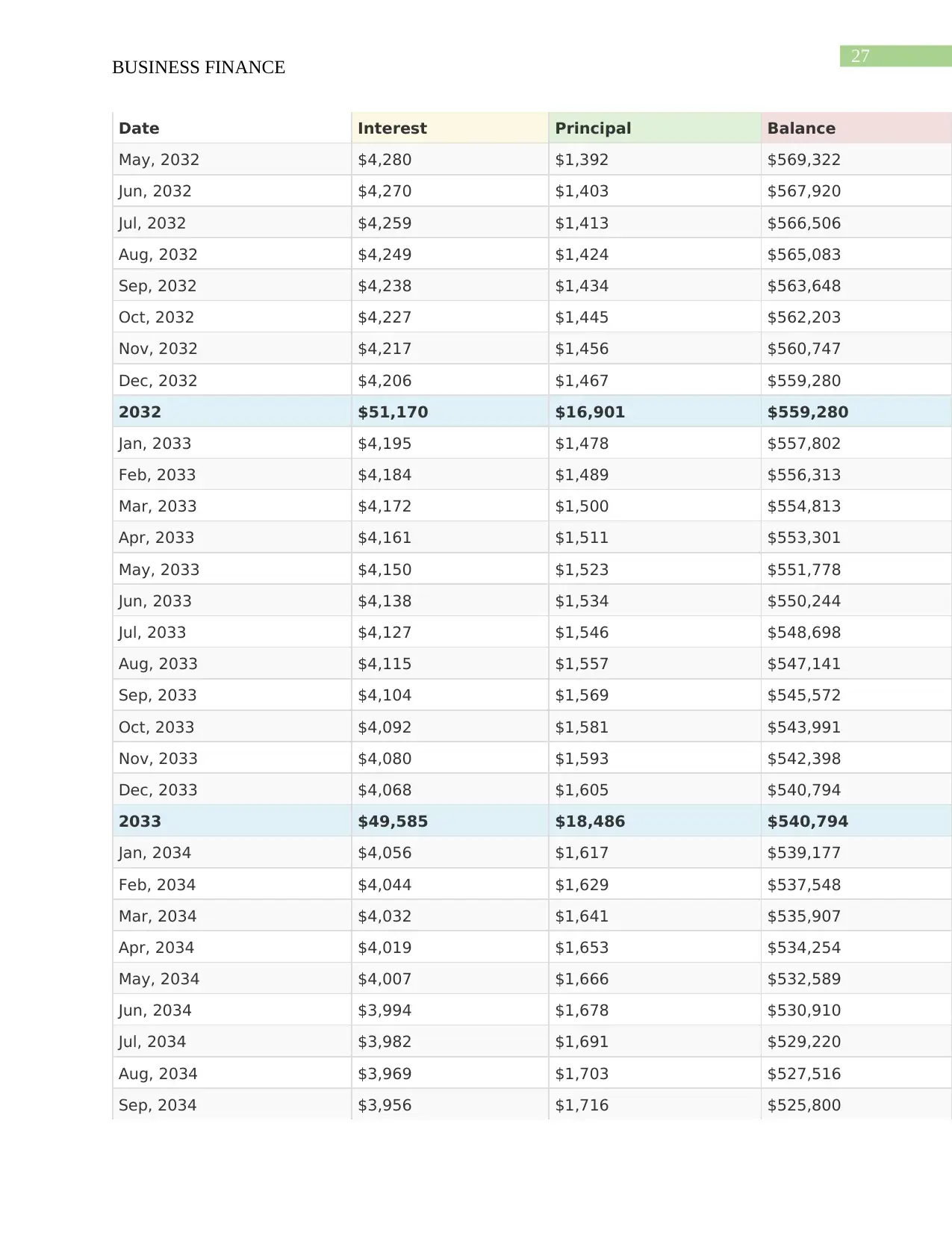

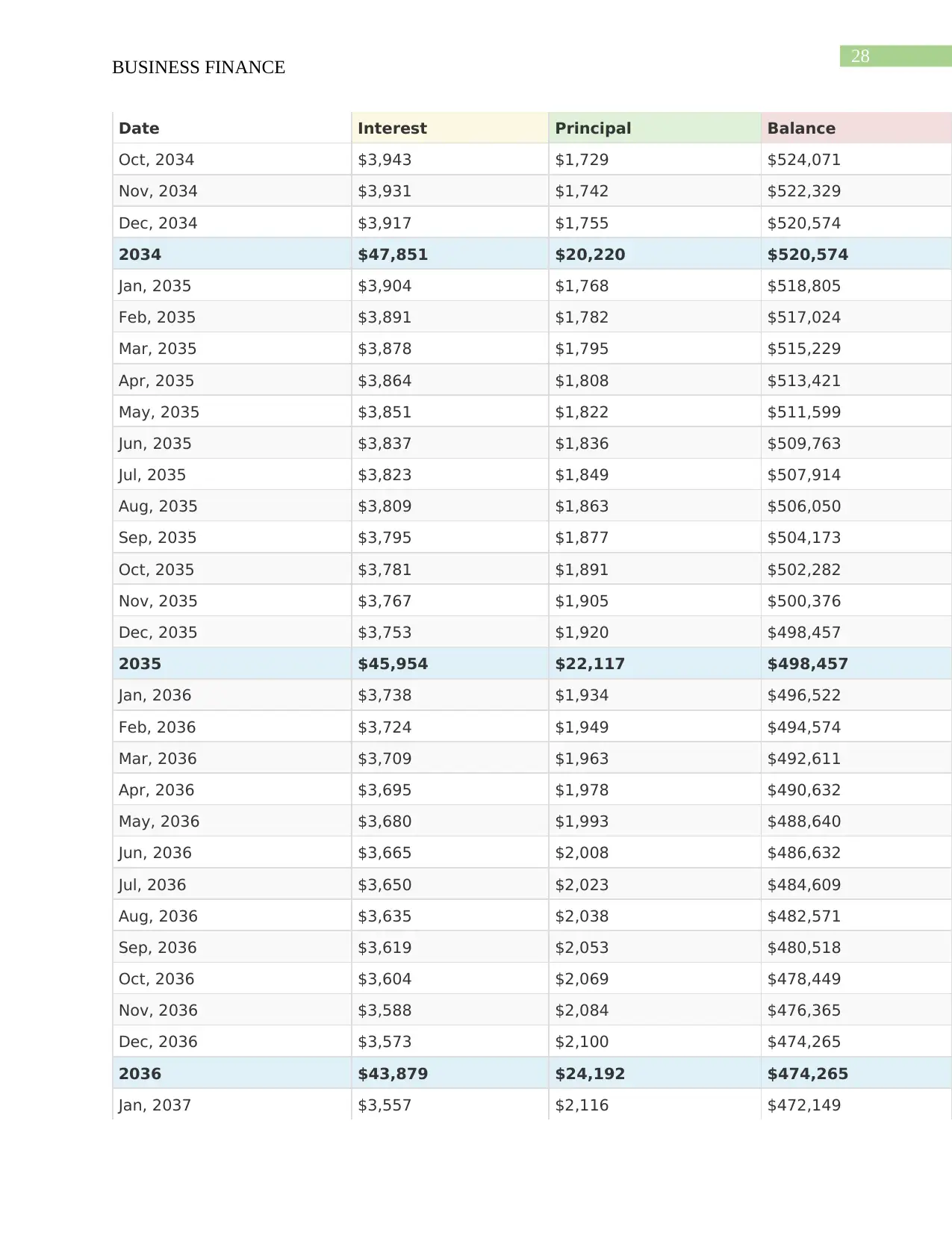

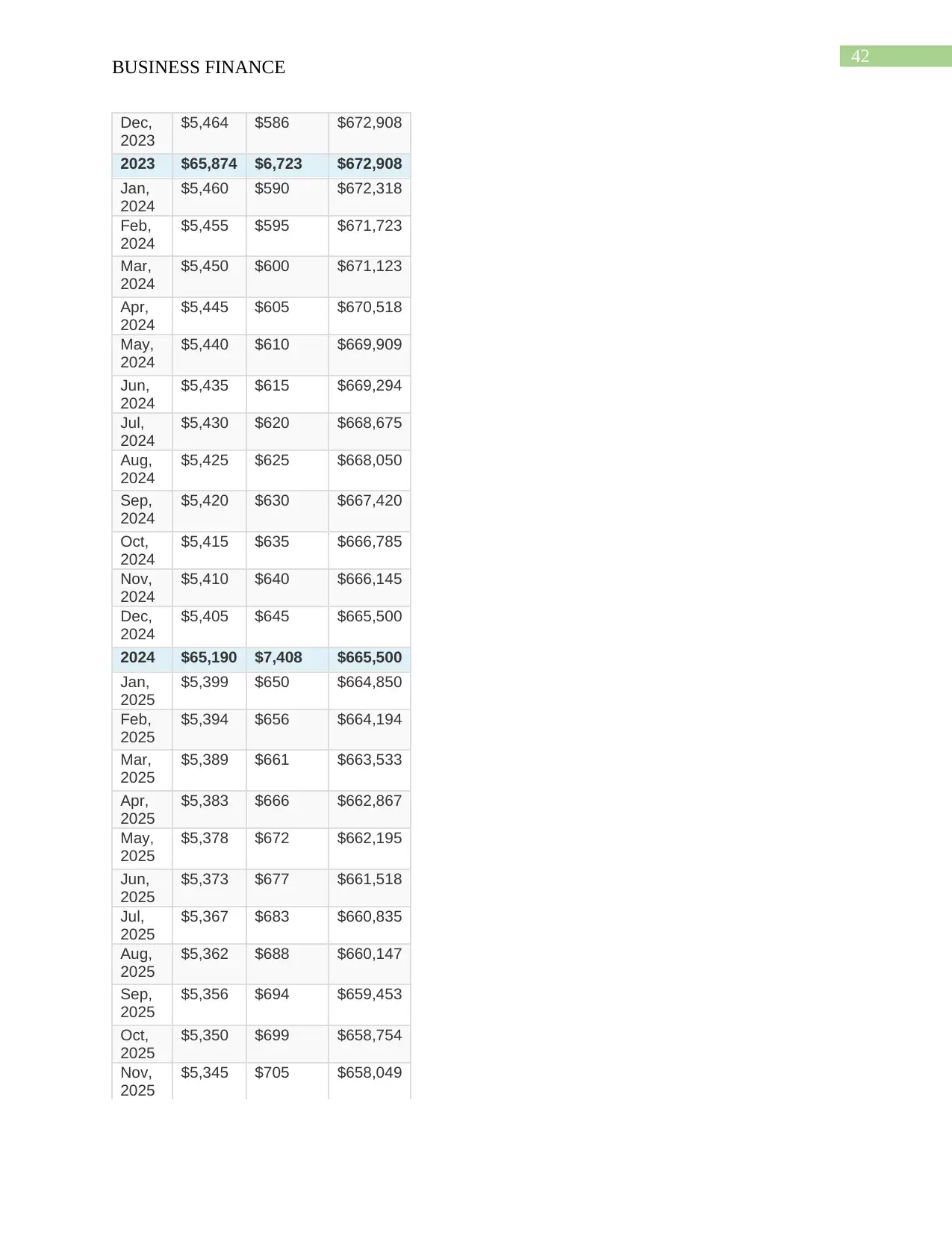

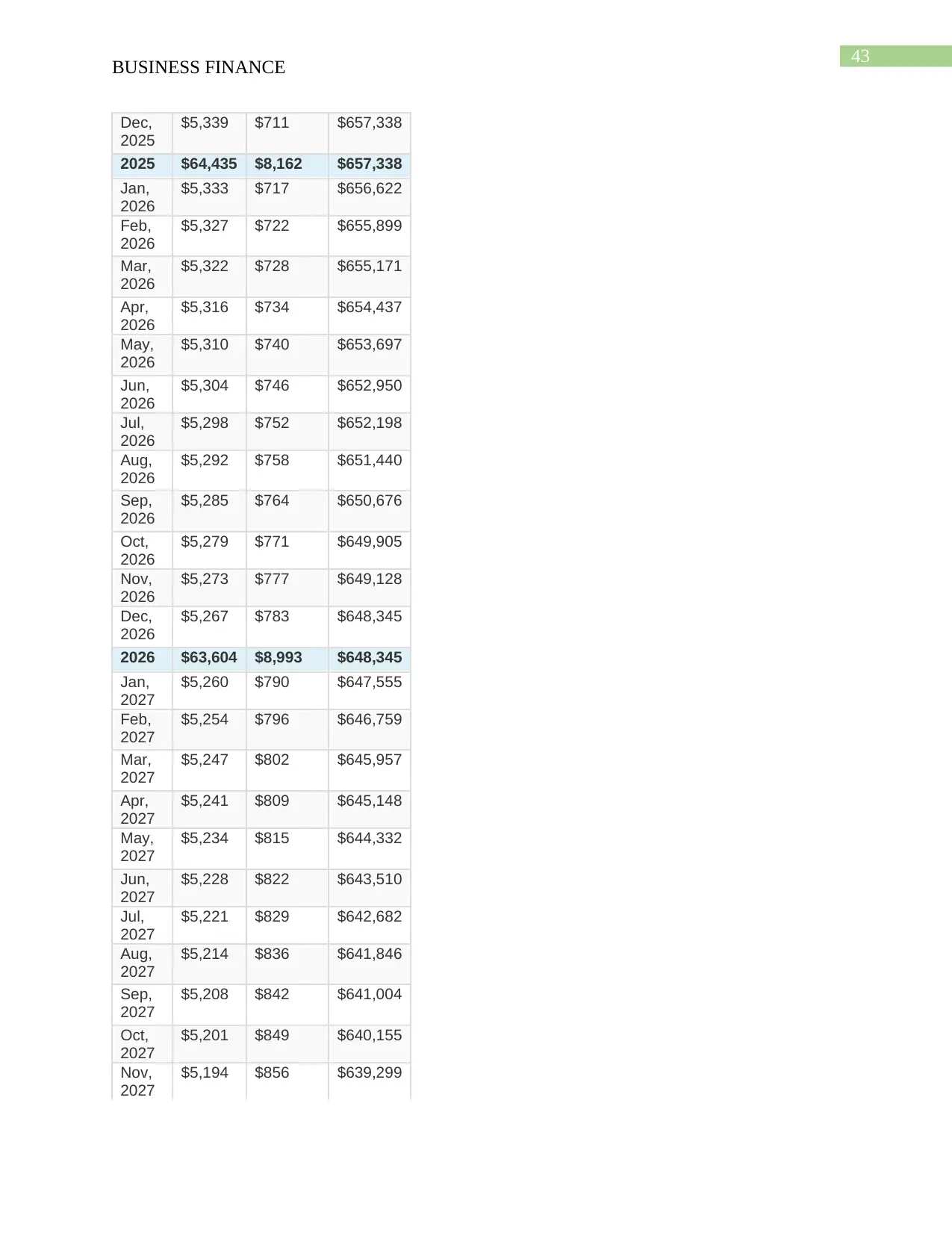

Question 4

In this case, 9 percent mortgage has been taken to find out the loan balance for year 19 and

20. In this case, the 1 st year or the base year has been assumed as 2018. It has been evaluated

that at the end of 20 th year, the amount will be zero, while at the end of 19 th Year, the amount

will be $474,265 and balance after 20th year will be $447,804.

BUSINESS FINANCE

Date Interest Principal Balance

2036 $11,758 $64,359 $95,300

Jan, 2037 $715 $5,628 $89,672

Feb, 2037 $673 $5,671 $84,001

Mar, 2037 $630 $5,713 $78,288

Apr, 2037 $587 $5,756 $72,532

May, 2037 $544 $5,799 $66,733

Jun, 2037 $501 $5,843 $60,891

Jul, 2037 $457 $5,886 $55,004

Aug, 2037 $413 $5,931 $49,074

Sep, 2037 $368 $5,975 $43,099

Oct, 2037 $323 $6,020 $37,079

Nov, 2037 $278 $6,065 $31,014

Dec, 2037 $233 $6,110 $24,904

2037 $5,720 $70,397 $24,904

Jan, 2038 $187 $6,156 $18,747

Feb, 2038 $141 $6,202 $12,545

Mar, 2038 $94 $6,249 $6,296

Apr, 2038 $47 $6,296 $0

2038 $469 $24,904 $0

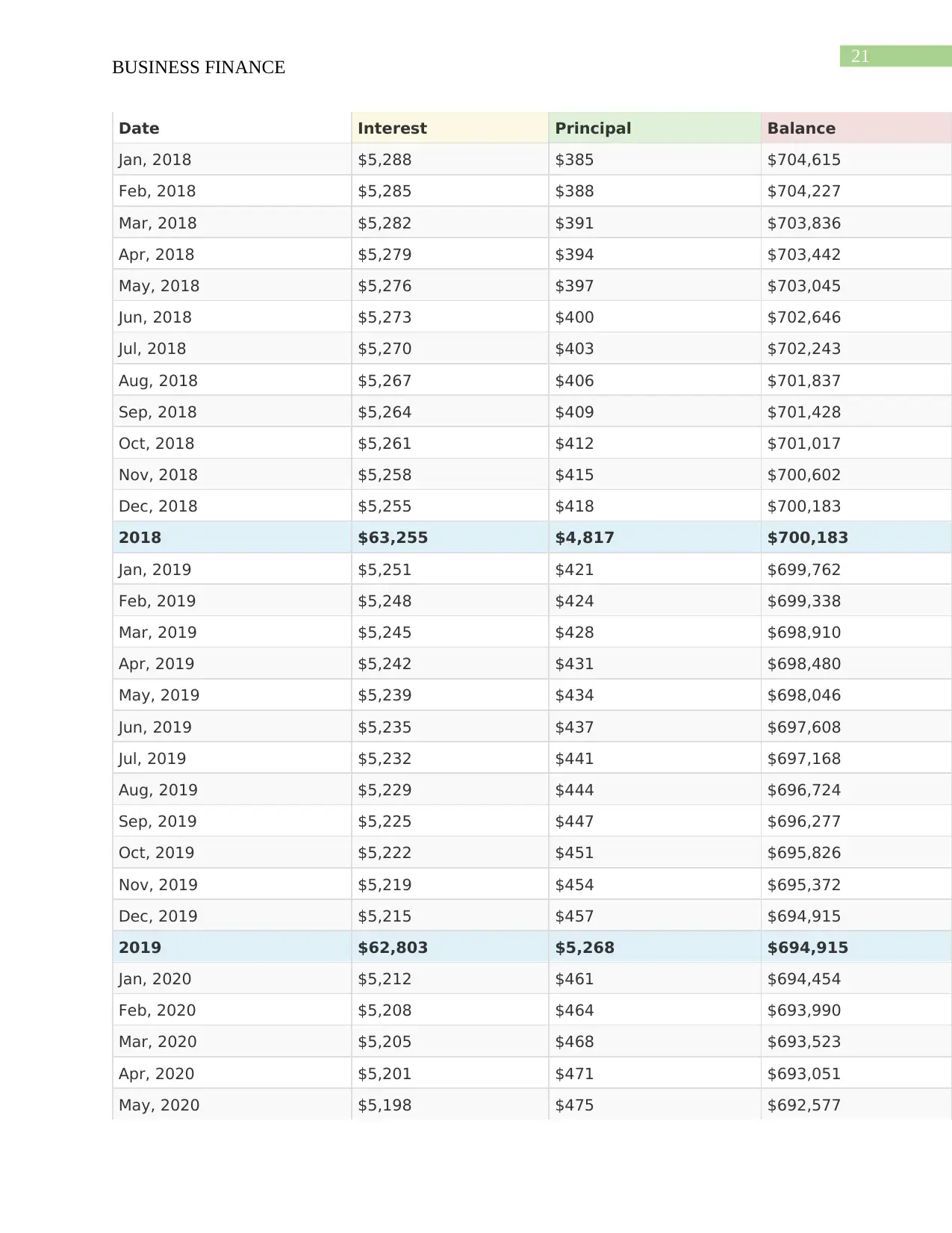

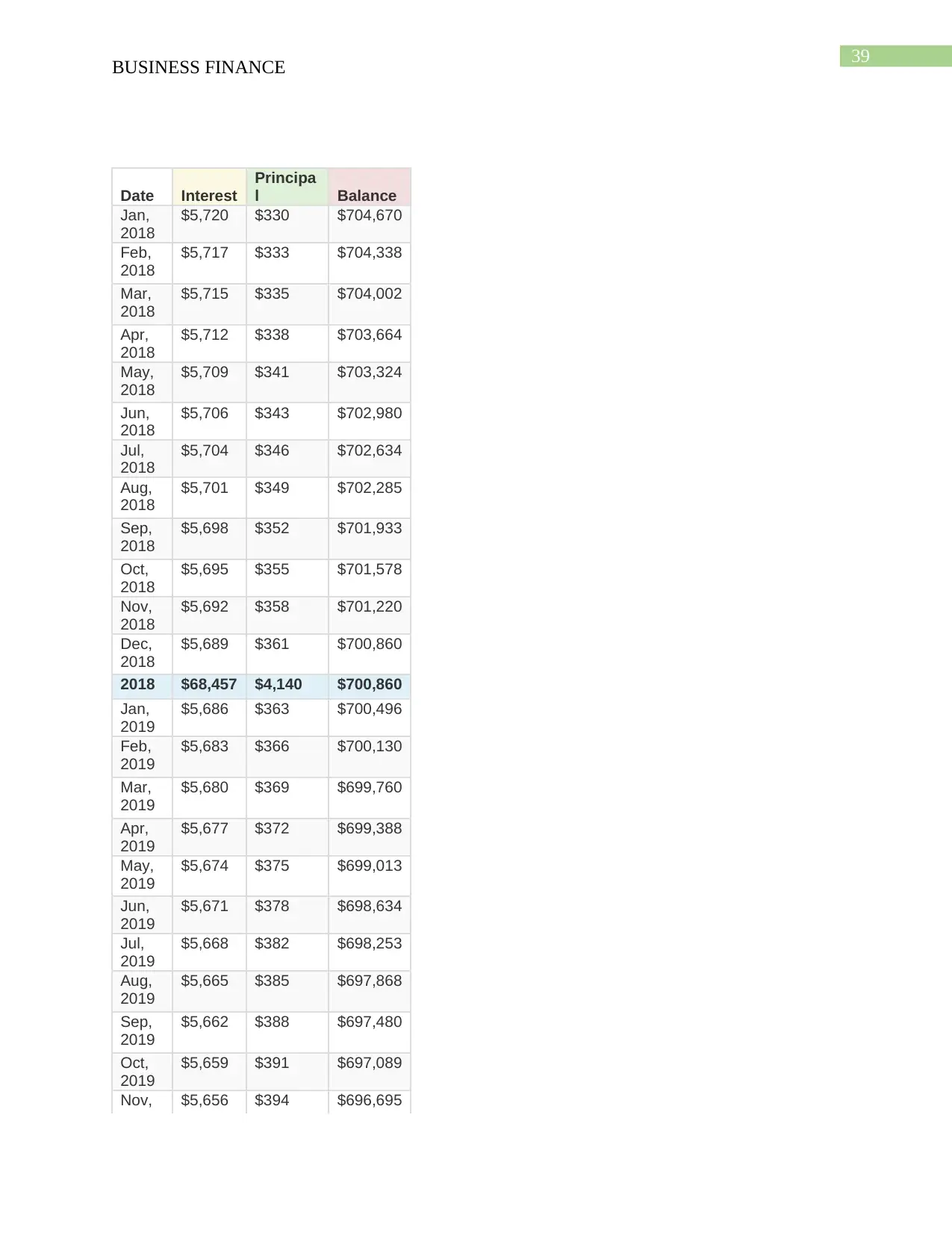

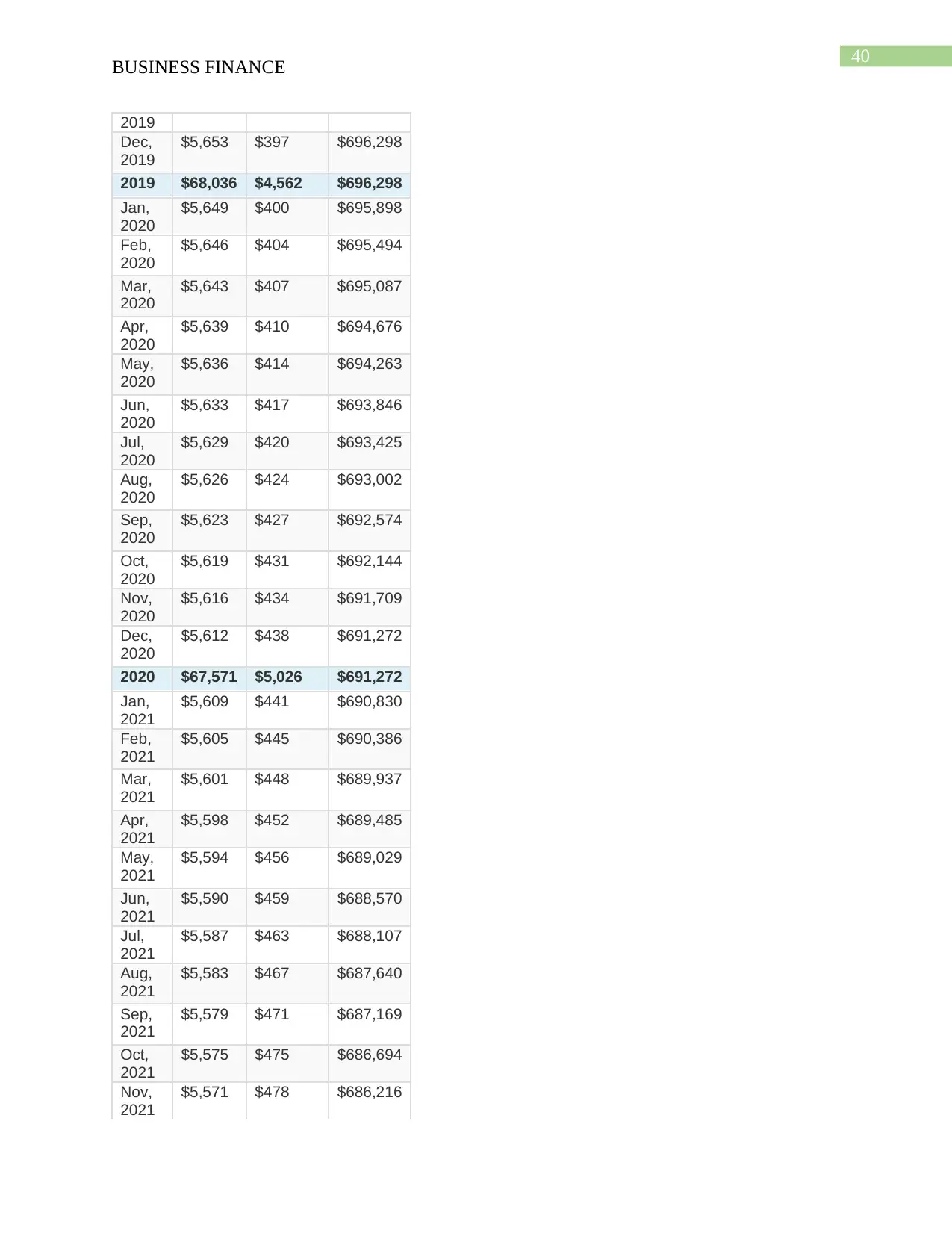

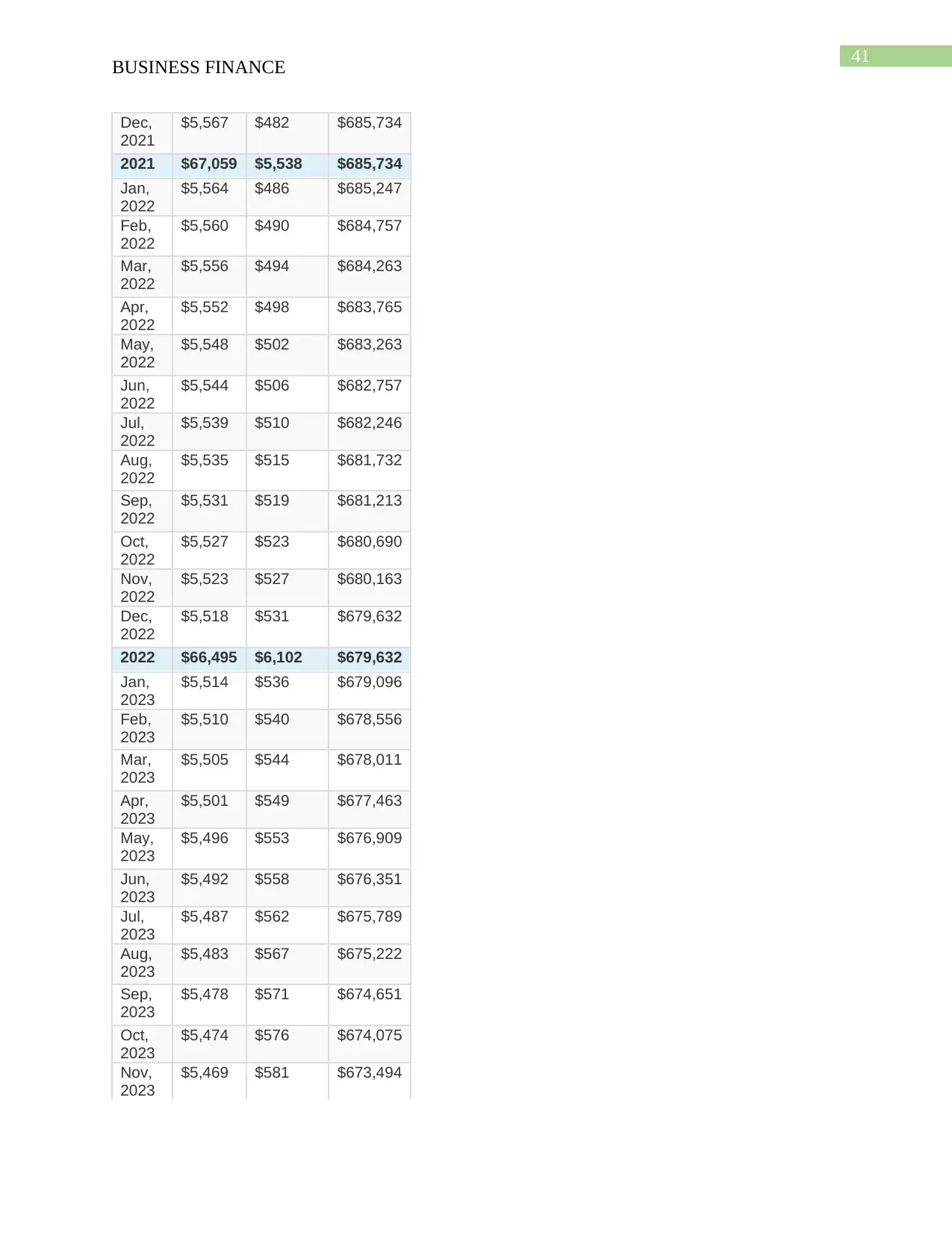

Question 4

In this case, 9 percent mortgage has been taken to find out the loan balance for year 19 and

20. In this case, the 1 st year or the base year has been assumed as 2018. It has been evaluated

that at the end of 20 th year, the amount will be zero, while at the end of 19 th Year, the amount

will be $474,265 and balance after 20th year will be $447,804.

21

BUSINESS FINANCE

Date Interest Principal Balance

Jan, 2018 $5,288 $385 $704,615

Feb, 2018 $5,285 $388 $704,227

Mar, 2018 $5,282 $391 $703,836

Apr, 2018 $5,279 $394 $703,442

May, 2018 $5,276 $397 $703,045

Jun, 2018 $5,273 $400 $702,646

Jul, 2018 $5,270 $403 $702,243

Aug, 2018 $5,267 $406 $701,837

Sep, 2018 $5,264 $409 $701,428

Oct, 2018 $5,261 $412 $701,017

Nov, 2018 $5,258 $415 $700,602

Dec, 2018 $5,255 $418 $700,183

2018 $63,255 $4,817 $700,183

Jan, 2019 $5,251 $421 $699,762

Feb, 2019 $5,248 $424 $699,338

Mar, 2019 $5,245 $428 $698,910

Apr, 2019 $5,242 $431 $698,480

May, 2019 $5,239 $434 $698,046

Jun, 2019 $5,235 $437 $697,608

Jul, 2019 $5,232 $441 $697,168

Aug, 2019 $5,229 $444 $696,724

Sep, 2019 $5,225 $447 $696,277

Oct, 2019 $5,222 $451 $695,826

Nov, 2019 $5,219 $454 $695,372

Dec, 2019 $5,215 $457 $694,915

2019 $62,803 $5,268 $694,915

Jan, 2020 $5,212 $461 $694,454

Feb, 2020 $5,208 $464 $693,990

Mar, 2020 $5,205 $468 $693,523

Apr, 2020 $5,201 $471 $693,051

May, 2020 $5,198 $475 $692,577

BUSINESS FINANCE

Date Interest Principal Balance

Jan, 2018 $5,288 $385 $704,615

Feb, 2018 $5,285 $388 $704,227

Mar, 2018 $5,282 $391 $703,836

Apr, 2018 $5,279 $394 $703,442

May, 2018 $5,276 $397 $703,045

Jun, 2018 $5,273 $400 $702,646

Jul, 2018 $5,270 $403 $702,243

Aug, 2018 $5,267 $406 $701,837

Sep, 2018 $5,264 $409 $701,428

Oct, 2018 $5,261 $412 $701,017

Nov, 2018 $5,258 $415 $700,602

Dec, 2018 $5,255 $418 $700,183

2018 $63,255 $4,817 $700,183

Jan, 2019 $5,251 $421 $699,762

Feb, 2019 $5,248 $424 $699,338

Mar, 2019 $5,245 $428 $698,910

Apr, 2019 $5,242 $431 $698,480

May, 2019 $5,239 $434 $698,046

Jun, 2019 $5,235 $437 $697,608

Jul, 2019 $5,232 $441 $697,168

Aug, 2019 $5,229 $444 $696,724

Sep, 2019 $5,225 $447 $696,277

Oct, 2019 $5,222 $451 $695,826

Nov, 2019 $5,219 $454 $695,372

Dec, 2019 $5,215 $457 $694,915

2019 $62,803 $5,268 $694,915

Jan, 2020 $5,212 $461 $694,454

Feb, 2020 $5,208 $464 $693,990

Mar, 2020 $5,205 $468 $693,523

Apr, 2020 $5,201 $471 $693,051

May, 2020 $5,198 $475 $692,577

22

BUSINESS FINANCE

Date Interest Principal Balance

Jun, 2020 $5,194 $478 $692,098

Jul, 2020 $5,191 $482 $691,617

Aug, 2020 $5,187 $485 $691,131

Sep, 2020 $5,183 $489 $690,642

Oct, 2020 $5,180 $493 $690,149

Nov, 2020 $5,176 $496 $689,653

Dec, 2020 $5,172 $500 $689,153

2020 $62,309 $5,763 $689,153

Jan, 2021 $5,169 $504 $688,649

Feb, 2021 $5,165 $508 $688,141

Mar, 2021 $5,161 $512 $687,629

Apr, 2021 $5,157 $515 $687,114

May, 2021 $5,153 $519 $686,595

Jun, 2021 $5,149 $523 $686,072

Jul, 2021 $5,146 $527 $685,545

Aug, 2021 $5,142 $531 $685,014

Sep, 2021 $5,138 $535 $684,479

Oct, 2021 $5,134 $539 $683,940

Nov, 2021 $5,130 $543 $683,396

Dec, 2021 $5,125 $547 $682,849

2021 $61,768 $6,303 $682,849

Jan, 2022 $5,121 $551 $682,298

Feb, 2022 $5,117 $555 $681,743

Mar, 2022 $5,113 $560 $681,183

Apr, 2022 $5,109 $564 $680,620

May, 2022 $5,105 $568 $680,052

Jun, 2022 $5,100 $572 $679,479

Jul, 2022 $5,096 $576 $678,903

Aug, 2022 $5,092 $581 $678,322

Sep, 2022 $5,087 $585 $677,737

Oct, 2022 $5,083 $590 $677,147

BUSINESS FINANCE

Date Interest Principal Balance

Jun, 2020 $5,194 $478 $692,098

Jul, 2020 $5,191 $482 $691,617

Aug, 2020 $5,187 $485 $691,131

Sep, 2020 $5,183 $489 $690,642

Oct, 2020 $5,180 $493 $690,149

Nov, 2020 $5,176 $496 $689,653

Dec, 2020 $5,172 $500 $689,153

2020 $62,309 $5,763 $689,153

Jan, 2021 $5,169 $504 $688,649

Feb, 2021 $5,165 $508 $688,141

Mar, 2021 $5,161 $512 $687,629

Apr, 2021 $5,157 $515 $687,114

May, 2021 $5,153 $519 $686,595

Jun, 2021 $5,149 $523 $686,072

Jul, 2021 $5,146 $527 $685,545

Aug, 2021 $5,142 $531 $685,014

Sep, 2021 $5,138 $535 $684,479

Oct, 2021 $5,134 $539 $683,940

Nov, 2021 $5,130 $543 $683,396

Dec, 2021 $5,125 $547 $682,849

2021 $61,768 $6,303 $682,849

Jan, 2022 $5,121 $551 $682,298

Feb, 2022 $5,117 $555 $681,743

Mar, 2022 $5,113 $560 $681,183

Apr, 2022 $5,109 $564 $680,620

May, 2022 $5,105 $568 $680,052

Jun, 2022 $5,100 $572 $679,479

Jul, 2022 $5,096 $576 $678,903

Aug, 2022 $5,092 $581 $678,322

Sep, 2022 $5,087 $585 $677,737

Oct, 2022 $5,083 $590 $677,147

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

23

BUSINESS FINANCE

Date Interest Principal Balance

Nov, 2022 $5,079 $594 $676,553

Dec, 2022 $5,074 $598 $675,955

2022 $61,177 $6,894 $675,955

Jan, 2023 $5,070 $603 $675,352

Feb, 2023 $5,065 $607 $674,745

Mar, 2023 $5,061 $612 $674,133

Apr, 2023 $5,056 $617 $673,516

May, 2023 $5,051 $621 $672,895

Jun, 2023 $5,047 $626 $672,269

Jul, 2023 $5,042 $631 $671,638

Aug, 2023 $5,037 $635 $671,003

Sep, 2023 $5,033 $640 $670,363

Oct, 2023 $5,028 $645 $669,718

Nov, 2023 $5,023 $650 $669,068

Dec, 2023 $5,018 $655 $668,414

2023 $60,530 $7,541 $668,414

Jan, 2024 $5,013 $659 $667,754

Feb, 2024 $5,008 $664 $667,090

Mar, 2024 $5,003 $669 $666,420

Apr, 2024 $4,998 $674 $665,746

May, 2024 $4,993 $679 $665,067

Jun, 2024 $4,988 $685 $664,382

Jul, 2024 $4,983 $690 $663,692

Aug, 2024 $4,978 $695 $662,997

Sep, 2024 $4,972 $700 $662,297

Oct, 2024 $4,967 $705 $661,592

Nov, 2024 $4,962 $711 $660,881

Dec, 2024 $4,957 $716 $660,165

2024 $59,822 $8,249 $660,165

Jan, 2025 $4,951 $721 $659,444

Feb, 2025 $4,946 $727 $658,717

BUSINESS FINANCE

Date Interest Principal Balance

Nov, 2022 $5,079 $594 $676,553

Dec, 2022 $5,074 $598 $675,955

2022 $61,177 $6,894 $675,955

Jan, 2023 $5,070 $603 $675,352

Feb, 2023 $5,065 $607 $674,745

Mar, 2023 $5,061 $612 $674,133

Apr, 2023 $5,056 $617 $673,516

May, 2023 $5,051 $621 $672,895

Jun, 2023 $5,047 $626 $672,269

Jul, 2023 $5,042 $631 $671,638

Aug, 2023 $5,037 $635 $671,003

Sep, 2023 $5,033 $640 $670,363

Oct, 2023 $5,028 $645 $669,718

Nov, 2023 $5,023 $650 $669,068

Dec, 2023 $5,018 $655 $668,414

2023 $60,530 $7,541 $668,414

Jan, 2024 $5,013 $659 $667,754

Feb, 2024 $5,008 $664 $667,090

Mar, 2024 $5,003 $669 $666,420

Apr, 2024 $4,998 $674 $665,746

May, 2024 $4,993 $679 $665,067

Jun, 2024 $4,988 $685 $664,382

Jul, 2024 $4,983 $690 $663,692

Aug, 2024 $4,978 $695 $662,997

Sep, 2024 $4,972 $700 $662,297

Oct, 2024 $4,967 $705 $661,592

Nov, 2024 $4,962 $711 $660,881

Dec, 2024 $4,957 $716 $660,165

2024 $59,822 $8,249 $660,165

Jan, 2025 $4,951 $721 $659,444

Feb, 2025 $4,946 $727 $658,717

24

BUSINESS FINANCE

Date Interest Principal Balance

Mar, 2025 $4,940 $732 $657,985

Apr, 2025 $4,935 $738 $657,247

May, 2025 $4,929 $743 $656,504

Jun, 2025 $4,924 $749 $655,755

Jul, 2025 $4,918 $754 $655,001

Aug, 2025 $4,913 $760 $654,241

Sep, 2025 $4,907 $766 $653,475

Oct, 2025 $4,901 $772 $652,703

Nov, 2025 $4,895 $777 $651,926

Dec, 2025 $4,889 $783 $651,143

2025 $59,049 $9,022 $651,143

Jan, 2026 $4,884 $789 $650,354

Feb, 2026 $4,878 $795 $649,559

Mar, 2026 $4,872 $801 $648,758

Apr, 2026 $4,866 $807 $647,951

May, 2026 $4,860 $813 $647,138

Jun, 2026 $4,854 $819 $646,319

Jul, 2026 $4,847 $825 $645,494

Aug, 2026 $4,841 $831 $644,663

Sep, 2026 $4,835 $838 $643,825

Oct, 2026 $4,829 $844 $642,981

Nov, 2026 $4,822 $850 $642,131

Dec, 2026 $4,816 $857 $641,274

2026 $58,202 $9,869 $641,274

Jan, 2027 $4,810 $863 $640,411

Feb, 2027 $4,803 $870 $639,542

Mar, 2027 $4,797 $876 $638,666

Apr, 2027 $4,790 $883 $637,783

May, 2027 $4,783 $889 $636,894

Jun, 2027 $4,777 $896 $635,998

Jul, 2027 $4,770 $903 $635,095

BUSINESS FINANCE

Date Interest Principal Balance

Mar, 2025 $4,940 $732 $657,985

Apr, 2025 $4,935 $738 $657,247

May, 2025 $4,929 $743 $656,504

Jun, 2025 $4,924 $749 $655,755

Jul, 2025 $4,918 $754 $655,001

Aug, 2025 $4,913 $760 $654,241

Sep, 2025 $4,907 $766 $653,475

Oct, 2025 $4,901 $772 $652,703

Nov, 2025 $4,895 $777 $651,926

Dec, 2025 $4,889 $783 $651,143

2025 $59,049 $9,022 $651,143

Jan, 2026 $4,884 $789 $650,354

Feb, 2026 $4,878 $795 $649,559

Mar, 2026 $4,872 $801 $648,758

Apr, 2026 $4,866 $807 $647,951

May, 2026 $4,860 $813 $647,138

Jun, 2026 $4,854 $819 $646,319

Jul, 2026 $4,847 $825 $645,494

Aug, 2026 $4,841 $831 $644,663

Sep, 2026 $4,835 $838 $643,825

Oct, 2026 $4,829 $844 $642,981

Nov, 2026 $4,822 $850 $642,131

Dec, 2026 $4,816 $857 $641,274

2026 $58,202 $9,869 $641,274

Jan, 2027 $4,810 $863 $640,411

Feb, 2027 $4,803 $870 $639,542

Mar, 2027 $4,797 $876 $638,666

Apr, 2027 $4,790 $883 $637,783

May, 2027 $4,783 $889 $636,894

Jun, 2027 $4,777 $896 $635,998

Jul, 2027 $4,770 $903 $635,095

25

BUSINESS FINANCE

Date Interest Principal Balance

Aug, 2027 $4,763 $909 $634,186

Sep, 2027 $4,756 $916 $633,270

Oct, 2027 $4,750 $923 $632,347

Nov, 2027 $4,743 $930 $631,417

Dec, 2027 $4,736 $937 $630,480

2027 $57,277 $10,794 $630,480

Jan, 2028 $4,729 $944 $629,536

Feb, 2028 $4,722 $951 $628,585

Mar, 2028 $4,714 $958 $627,626

Apr, 2028 $4,707 $965 $626,661

May, 2028 $4,700 $973 $625,688

Jun, 2028 $4,693 $980 $624,708

Jul, 2028 $4,685 $987 $623,721

Aug, 2028 $4,678 $995 $622,727

Sep, 2028 $4,670 $1,002 $621,724

Oct, 2028 $4,663 $1,010 $620,715

Nov, 2028 $4,655 $1,017 $619,697

Dec, 2028 $4,648 $1,025 $618,673

2028 $56,264 $11,807 $618,673

Jan, 2029 $4,640 $1,033 $617,640

Feb, 2029 $4,632 $1,040 $616,600

Mar, 2029 $4,624 $1,048 $615,552

Apr, 2029 $4,617 $1,056 $614,496

May, 2029 $4,609 $1,064 $613,432

Jun, 2029 $4,601 $1,072 $612,360

Jul, 2029 $4,593 $1,080 $611,280

Aug, 2029 $4,585 $1,088 $610,192

Sep, 2029 $4,576 $1,096 $609,096

Oct, 2029 $4,568 $1,104 $607,992

Nov, 2029 $4,560 $1,113 $606,879

Dec, 2029 $4,552 $1,121 $605,758

BUSINESS FINANCE

Date Interest Principal Balance

Aug, 2027 $4,763 $909 $634,186

Sep, 2027 $4,756 $916 $633,270

Oct, 2027 $4,750 $923 $632,347

Nov, 2027 $4,743 $930 $631,417

Dec, 2027 $4,736 $937 $630,480

2027 $57,277 $10,794 $630,480

Jan, 2028 $4,729 $944 $629,536

Feb, 2028 $4,722 $951 $628,585

Mar, 2028 $4,714 $958 $627,626

Apr, 2028 $4,707 $965 $626,661

May, 2028 $4,700 $973 $625,688

Jun, 2028 $4,693 $980 $624,708

Jul, 2028 $4,685 $987 $623,721

Aug, 2028 $4,678 $995 $622,727

Sep, 2028 $4,670 $1,002 $621,724

Oct, 2028 $4,663 $1,010 $620,715

Nov, 2028 $4,655 $1,017 $619,697

Dec, 2028 $4,648 $1,025 $618,673

2028 $56,264 $11,807 $618,673

Jan, 2029 $4,640 $1,033 $617,640

Feb, 2029 $4,632 $1,040 $616,600

Mar, 2029 $4,624 $1,048 $615,552

Apr, 2029 $4,617 $1,056 $614,496

May, 2029 $4,609 $1,064 $613,432

Jun, 2029 $4,601 $1,072 $612,360

Jul, 2029 $4,593 $1,080 $611,280

Aug, 2029 $4,585 $1,088 $610,192

Sep, 2029 $4,576 $1,096 $609,096

Oct, 2029 $4,568 $1,104 $607,992

Nov, 2029 $4,560 $1,113 $606,879

Dec, 2029 $4,552 $1,121 $605,758

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

26

BUSINESS FINANCE

Date Interest Principal Balance

2029 $55,156 $12,915 $605,758

Jan, 2030 $4,543 $1,129 $604,629

Feb, 2030 $4,535 $1,138 $603,491

Mar, 2030 $4,526 $1,146 $602,344

Apr, 2030 $4,518 $1,155 $601,189

May, 2030 $4,509 $1,164 $600,026

Jun, 2030 $4,500 $1,172 $598,853

Jul, 2030 $4,491 $1,181 $597,672

Aug, 2030 $4,483 $1,190 $596,482

Sep, 2030 $4,474 $1,199 $595,283

Oct, 2030 $4,465 $1,208 $594,075

Nov, 2030 $4,456 $1,217 $592,858

Dec, 2030 $4,446 $1,226 $591,632

2030 $53,945 $14,126 $591,632

Jan, 2031 $4,437 $1,235 $590,397

Feb, 2031 $4,428 $1,245 $589,152

Mar, 2031 $4,419 $1,254 $587,898

Apr, 2031 $4,409 $1,263 $586,635

May, 2031 $4,400 $1,273 $585,362

Jun, 2031 $4,390 $1,282 $584,079

Jul, 2031 $4,381 $1,292 $582,787

Aug, 2031 $4,371 $1,302 $581,486

Sep, 2031 $4,361 $1,311 $580,174

Oct, 2031 $4,351 $1,321 $578,853

Nov, 2031 $4,341 $1,331 $577,522

Dec, 2031 $4,331 $1,341 $576,181

2031 $52,620 $15,451 $576,181

Jan, 2032 $4,321 $1,351 $574,829

Feb, 2032 $4,311 $1,361 $573,468

Mar, 2032 $4,301 $1,372 $572,096

Apr, 2032 $4,291 $1,382 $570,715

BUSINESS FINANCE

Date Interest Principal Balance

2029 $55,156 $12,915 $605,758

Jan, 2030 $4,543 $1,129 $604,629

Feb, 2030 $4,535 $1,138 $603,491

Mar, 2030 $4,526 $1,146 $602,344

Apr, 2030 $4,518 $1,155 $601,189

May, 2030 $4,509 $1,164 $600,026

Jun, 2030 $4,500 $1,172 $598,853

Jul, 2030 $4,491 $1,181 $597,672

Aug, 2030 $4,483 $1,190 $596,482

Sep, 2030 $4,474 $1,199 $595,283

Oct, 2030 $4,465 $1,208 $594,075

Nov, 2030 $4,456 $1,217 $592,858

Dec, 2030 $4,446 $1,226 $591,632

2030 $53,945 $14,126 $591,632

Jan, 2031 $4,437 $1,235 $590,397

Feb, 2031 $4,428 $1,245 $589,152

Mar, 2031 $4,419 $1,254 $587,898

Apr, 2031 $4,409 $1,263 $586,635

May, 2031 $4,400 $1,273 $585,362

Jun, 2031 $4,390 $1,282 $584,079

Jul, 2031 $4,381 $1,292 $582,787

Aug, 2031 $4,371 $1,302 $581,486

Sep, 2031 $4,361 $1,311 $580,174

Oct, 2031 $4,351 $1,321 $578,853

Nov, 2031 $4,341 $1,331 $577,522

Dec, 2031 $4,331 $1,341 $576,181

2031 $52,620 $15,451 $576,181

Jan, 2032 $4,321 $1,351 $574,829

Feb, 2032 $4,311 $1,361 $573,468

Mar, 2032 $4,301 $1,372 $572,096

Apr, 2032 $4,291 $1,382 $570,715

27

BUSINESS FINANCE

Date Interest Principal Balance

May, 2032 $4,280 $1,392 $569,322

Jun, 2032 $4,270 $1,403 $567,920

Jul, 2032 $4,259 $1,413 $566,506

Aug, 2032 $4,249 $1,424 $565,083

Sep, 2032 $4,238 $1,434 $563,648

Oct, 2032 $4,227 $1,445 $562,203

Nov, 2032 $4,217 $1,456 $560,747

Dec, 2032 $4,206 $1,467 $559,280

2032 $51,170 $16,901 $559,280

Jan, 2033 $4,195 $1,478 $557,802

Feb, 2033 $4,184 $1,489 $556,313

Mar, 2033 $4,172 $1,500 $554,813

Apr, 2033 $4,161 $1,511 $553,301

May, 2033 $4,150 $1,523 $551,778

Jun, 2033 $4,138 $1,534 $550,244

Jul, 2033 $4,127 $1,546 $548,698

Aug, 2033 $4,115 $1,557 $547,141

Sep, 2033 $4,104 $1,569 $545,572

Oct, 2033 $4,092 $1,581 $543,991

Nov, 2033 $4,080 $1,593 $542,398

Dec, 2033 $4,068 $1,605 $540,794

2033 $49,585 $18,486 $540,794

Jan, 2034 $4,056 $1,617 $539,177

Feb, 2034 $4,044 $1,629 $537,548

Mar, 2034 $4,032 $1,641 $535,907

Apr, 2034 $4,019 $1,653 $534,254

May, 2034 $4,007 $1,666 $532,589

Jun, 2034 $3,994 $1,678 $530,910

Jul, 2034 $3,982 $1,691 $529,220

Aug, 2034 $3,969 $1,703 $527,516

Sep, 2034 $3,956 $1,716 $525,800

BUSINESS FINANCE

Date Interest Principal Balance

May, 2032 $4,280 $1,392 $569,322

Jun, 2032 $4,270 $1,403 $567,920

Jul, 2032 $4,259 $1,413 $566,506

Aug, 2032 $4,249 $1,424 $565,083

Sep, 2032 $4,238 $1,434 $563,648

Oct, 2032 $4,227 $1,445 $562,203

Nov, 2032 $4,217 $1,456 $560,747

Dec, 2032 $4,206 $1,467 $559,280

2032 $51,170 $16,901 $559,280

Jan, 2033 $4,195 $1,478 $557,802

Feb, 2033 $4,184 $1,489 $556,313

Mar, 2033 $4,172 $1,500 $554,813

Apr, 2033 $4,161 $1,511 $553,301

May, 2033 $4,150 $1,523 $551,778

Jun, 2033 $4,138 $1,534 $550,244

Jul, 2033 $4,127 $1,546 $548,698

Aug, 2033 $4,115 $1,557 $547,141

Sep, 2033 $4,104 $1,569 $545,572

Oct, 2033 $4,092 $1,581 $543,991

Nov, 2033 $4,080 $1,593 $542,398

Dec, 2033 $4,068 $1,605 $540,794

2033 $49,585 $18,486 $540,794

Jan, 2034 $4,056 $1,617 $539,177

Feb, 2034 $4,044 $1,629 $537,548

Mar, 2034 $4,032 $1,641 $535,907

Apr, 2034 $4,019 $1,653 $534,254

May, 2034 $4,007 $1,666 $532,589

Jun, 2034 $3,994 $1,678 $530,910

Jul, 2034 $3,982 $1,691 $529,220

Aug, 2034 $3,969 $1,703 $527,516

Sep, 2034 $3,956 $1,716 $525,800

28

BUSINESS FINANCE

Date Interest Principal Balance

Oct, 2034 $3,943 $1,729 $524,071

Nov, 2034 $3,931 $1,742 $522,329

Dec, 2034 $3,917 $1,755 $520,574

2034 $47,851 $20,220 $520,574

Jan, 2035 $3,904 $1,768 $518,805

Feb, 2035 $3,891 $1,782 $517,024

Mar, 2035 $3,878 $1,795 $515,229

Apr, 2035 $3,864 $1,808 $513,421

May, 2035 $3,851 $1,822 $511,599

Jun, 2035 $3,837 $1,836 $509,763

Jul, 2035 $3,823 $1,849 $507,914

Aug, 2035 $3,809 $1,863 $506,050

Sep, 2035 $3,795 $1,877 $504,173

Oct, 2035 $3,781 $1,891 $502,282

Nov, 2035 $3,767 $1,905 $500,376

Dec, 2035 $3,753 $1,920 $498,457

2035 $45,954 $22,117 $498,457

Jan, 2036 $3,738 $1,934 $496,522

Feb, 2036 $3,724 $1,949 $494,574

Mar, 2036 $3,709 $1,963 $492,611

Apr, 2036 $3,695 $1,978 $490,632

May, 2036 $3,680 $1,993 $488,640

Jun, 2036 $3,665 $2,008 $486,632

Jul, 2036 $3,650 $2,023 $484,609

Aug, 2036 $3,635 $2,038 $482,571

Sep, 2036 $3,619 $2,053 $480,518

Oct, 2036 $3,604 $2,069 $478,449

Nov, 2036 $3,588 $2,084 $476,365

Dec, 2036 $3,573 $2,100 $474,265

2036 $43,879 $24,192 $474,265

Jan, 2037 $3,557 $2,116 $472,149

BUSINESS FINANCE

Date Interest Principal Balance

Oct, 2034 $3,943 $1,729 $524,071

Nov, 2034 $3,931 $1,742 $522,329

Dec, 2034 $3,917 $1,755 $520,574

2034 $47,851 $20,220 $520,574

Jan, 2035 $3,904 $1,768 $518,805

Feb, 2035 $3,891 $1,782 $517,024

Mar, 2035 $3,878 $1,795 $515,229

Apr, 2035 $3,864 $1,808 $513,421

May, 2035 $3,851 $1,822 $511,599

Jun, 2035 $3,837 $1,836 $509,763

Jul, 2035 $3,823 $1,849 $507,914

Aug, 2035 $3,809 $1,863 $506,050

Sep, 2035 $3,795 $1,877 $504,173

Oct, 2035 $3,781 $1,891 $502,282

Nov, 2035 $3,767 $1,905 $500,376

Dec, 2035 $3,753 $1,920 $498,457

2035 $45,954 $22,117 $498,457

Jan, 2036 $3,738 $1,934 $496,522

Feb, 2036 $3,724 $1,949 $494,574

Mar, 2036 $3,709 $1,963 $492,611

Apr, 2036 $3,695 $1,978 $490,632

May, 2036 $3,680 $1,993 $488,640

Jun, 2036 $3,665 $2,008 $486,632

Jul, 2036 $3,650 $2,023 $484,609

Aug, 2036 $3,635 $2,038 $482,571

Sep, 2036 $3,619 $2,053 $480,518

Oct, 2036 $3,604 $2,069 $478,449

Nov, 2036 $3,588 $2,084 $476,365

Dec, 2036 $3,573 $2,100 $474,265

2036 $43,879 $24,192 $474,265

Jan, 2037 $3,557 $2,116 $472,149

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

29

BUSINESS FINANCE

Date Interest Principal Balance

Feb, 2037 $3,541 $2,131 $470,018

Mar, 2037 $3,525 $2,147 $467,870

Apr, 2037 $3,509 $2,164 $465,707

May, 2037 $3,493 $2,180 $463,527

Jun, 2037 $3,476 $2,196 $461,331

Jul, 2037 $3,460 $2,213 $459,118

Aug, 2037 $3,443 $2,229 $456,889

Sep, 2037 $3,427 $2,246 $454,643

Oct, 2037 $3,410 $2,263 $452,380

Nov, 2037 $3,393 $2,280 $450,101

Dec, 2037 $3,376 $2,297 $447,804

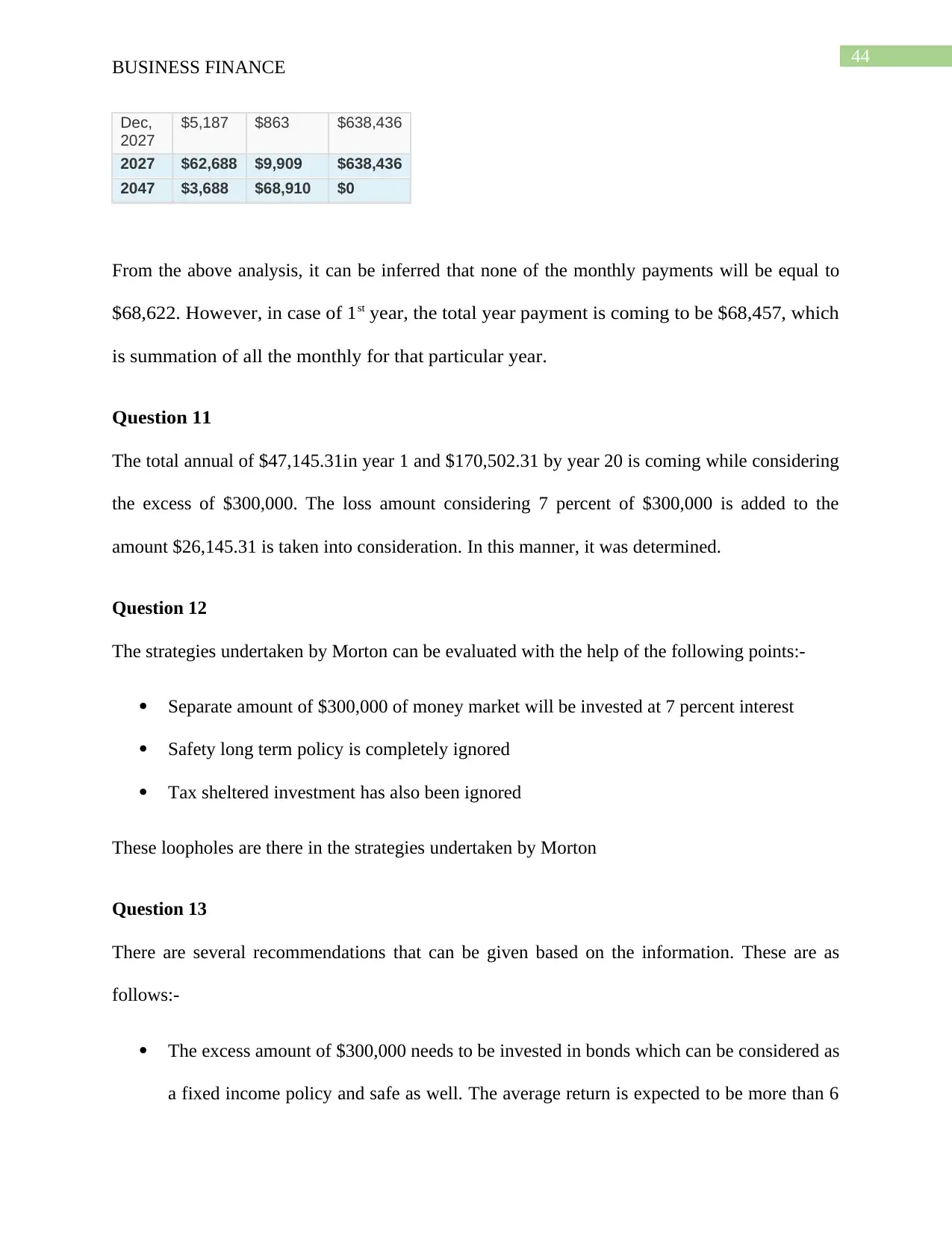

2037 $41,610 $26,461 $447,804

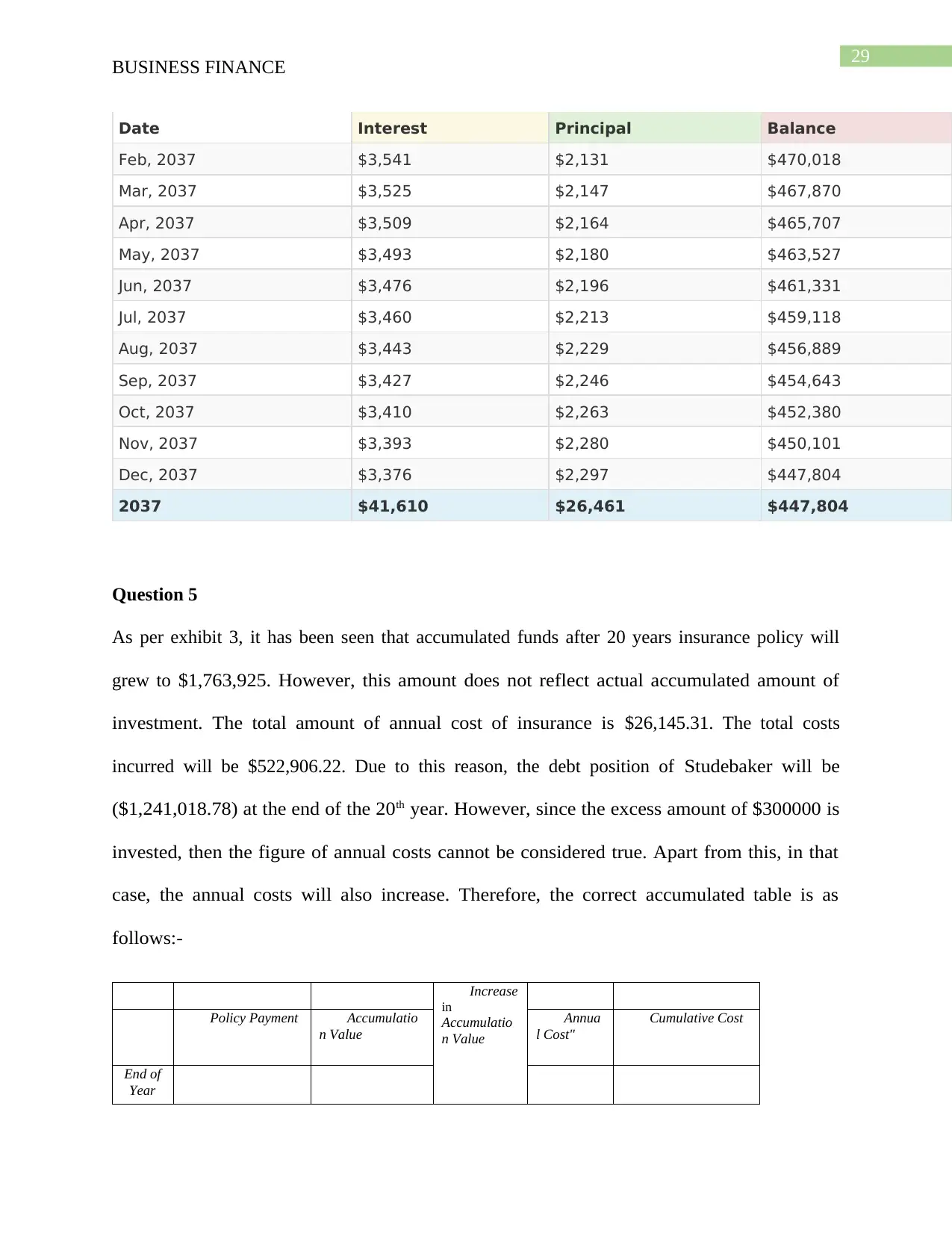

Question 5

As per exhibit 3, it has been seen that accumulated funds after 20 years insurance policy will

grew to $1,763,925. However, this amount does not reflect actual accumulated amount of

investment. The total amount of annual cost of insurance is $26,145.31. The total costs

incurred will be $522,906.22. Due to this reason, the debt position of Studebaker will be

($1,241,018.78) at the end of the 20 th year. However, since the excess amount of $300000 is

invested, then the figure of annual costs cannot be considered true. Apart from this, in that

case, the annual costs will also increase. Therefore, the correct accumulated table is as

follows:-

Increase

in

Accumulatio

n Value

Policy Payment Accumulatio

n Value

Annua

l Cost"

Cumulative Cost

End of

Year

BUSINESS FINANCE

Date Interest Principal Balance

Feb, 2037 $3,541 $2,131 $470,018

Mar, 2037 $3,525 $2,147 $467,870

Apr, 2037 $3,509 $2,164 $465,707

May, 2037 $3,493 $2,180 $463,527

Jun, 2037 $3,476 $2,196 $461,331

Jul, 2037 $3,460 $2,213 $459,118

Aug, 2037 $3,443 $2,229 $456,889

Sep, 2037 $3,427 $2,246 $454,643

Oct, 2037 $3,410 $2,263 $452,380

Nov, 2037 $3,393 $2,280 $450,101

Dec, 2037 $3,376 $2,297 $447,804

2037 $41,610 $26,461 $447,804

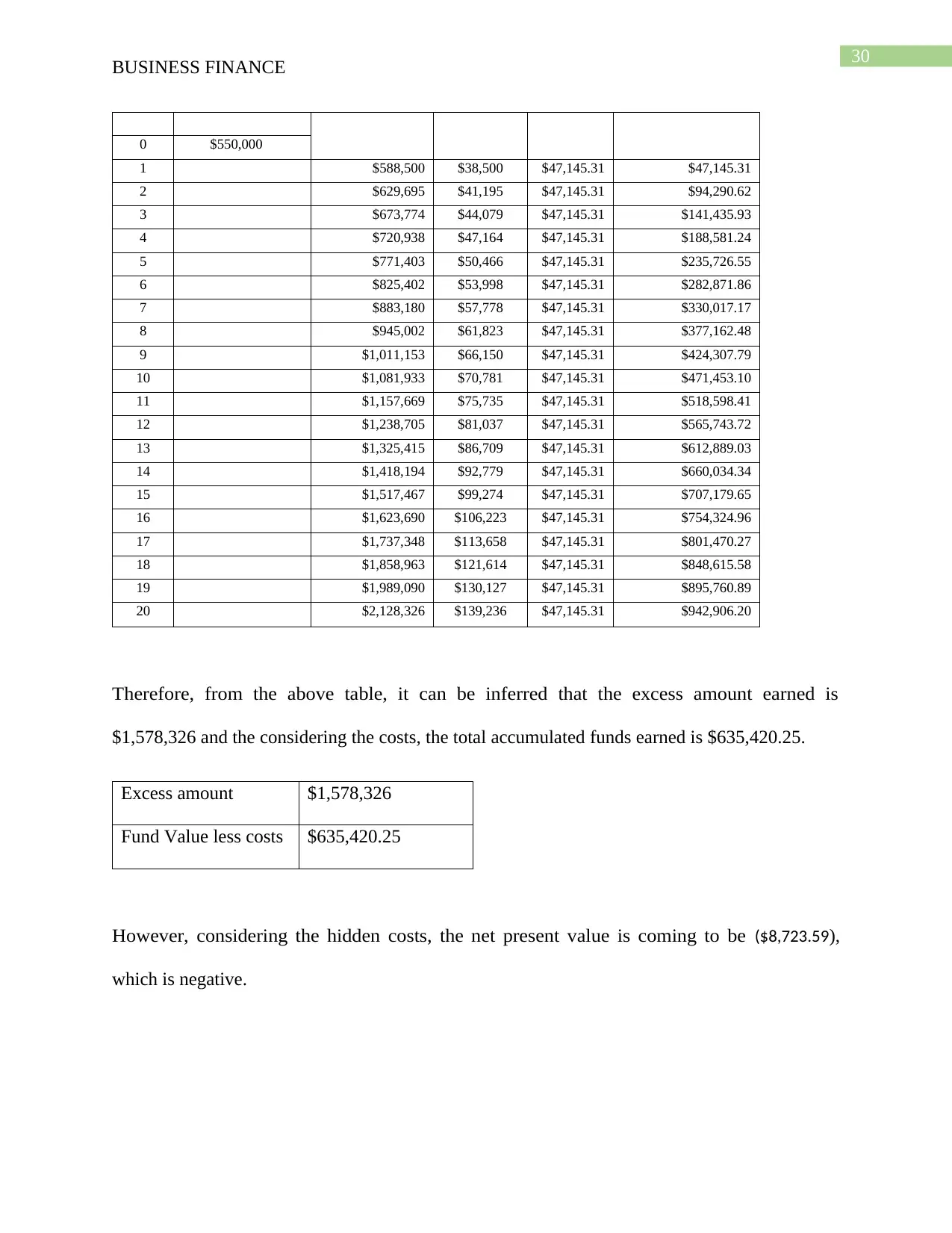

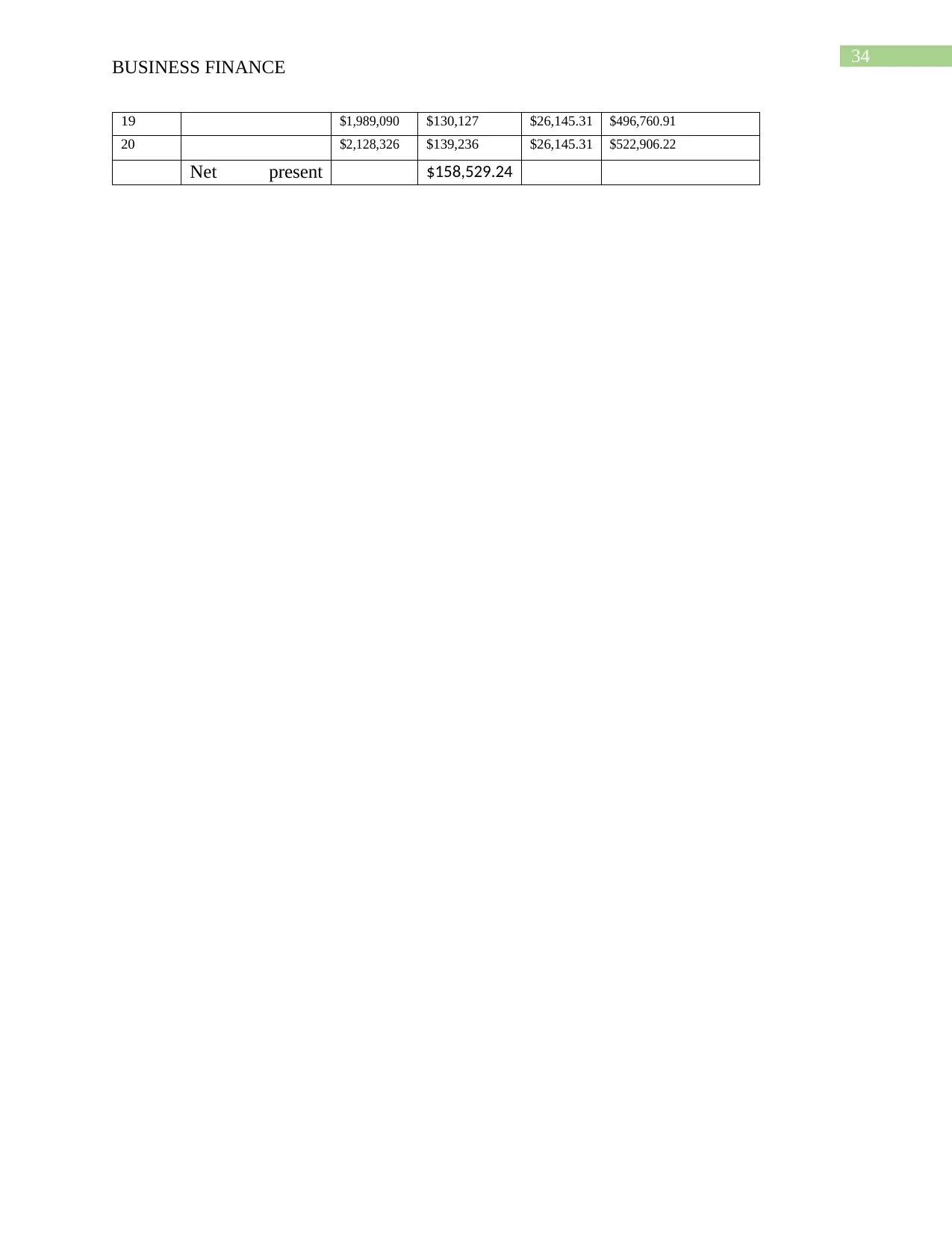

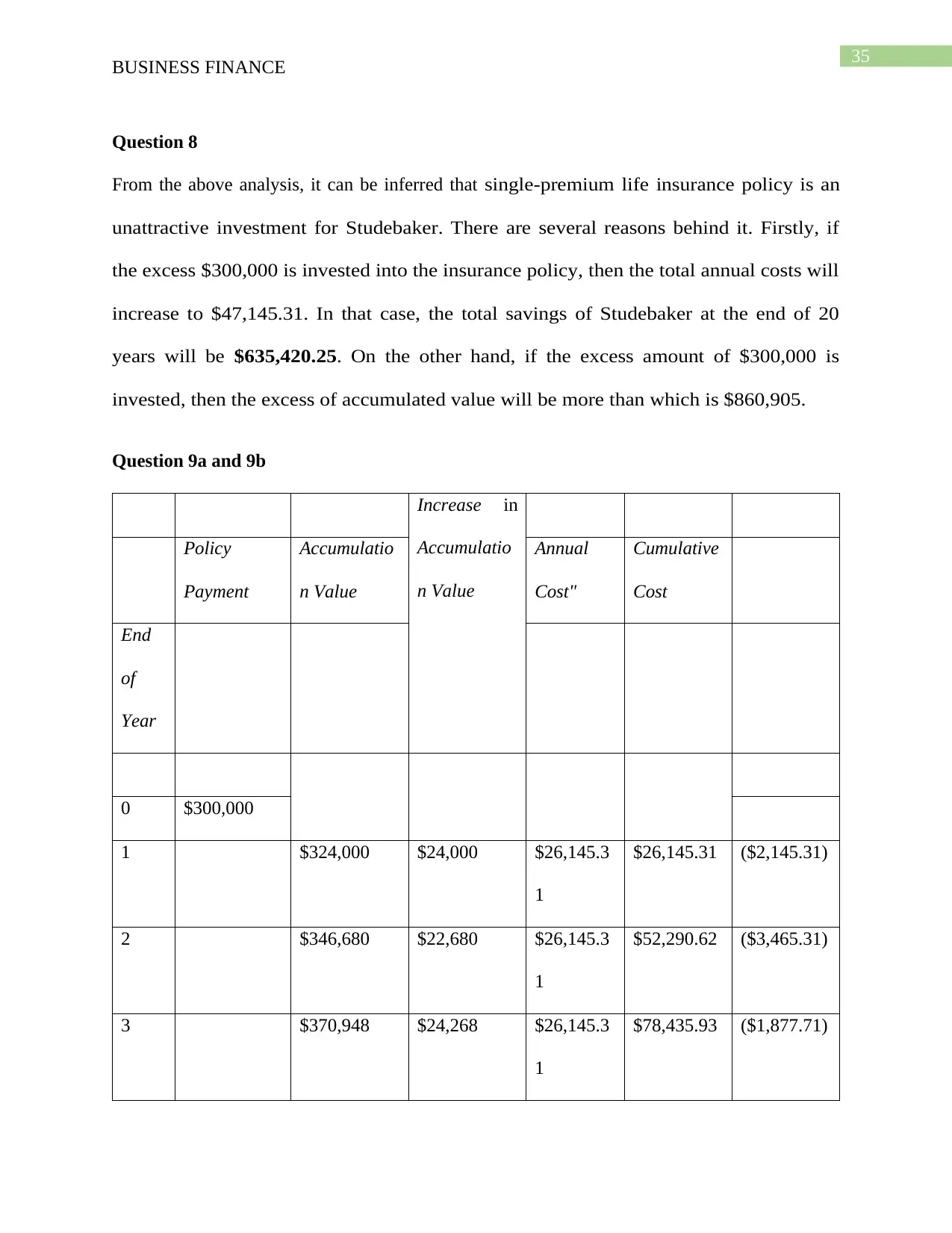

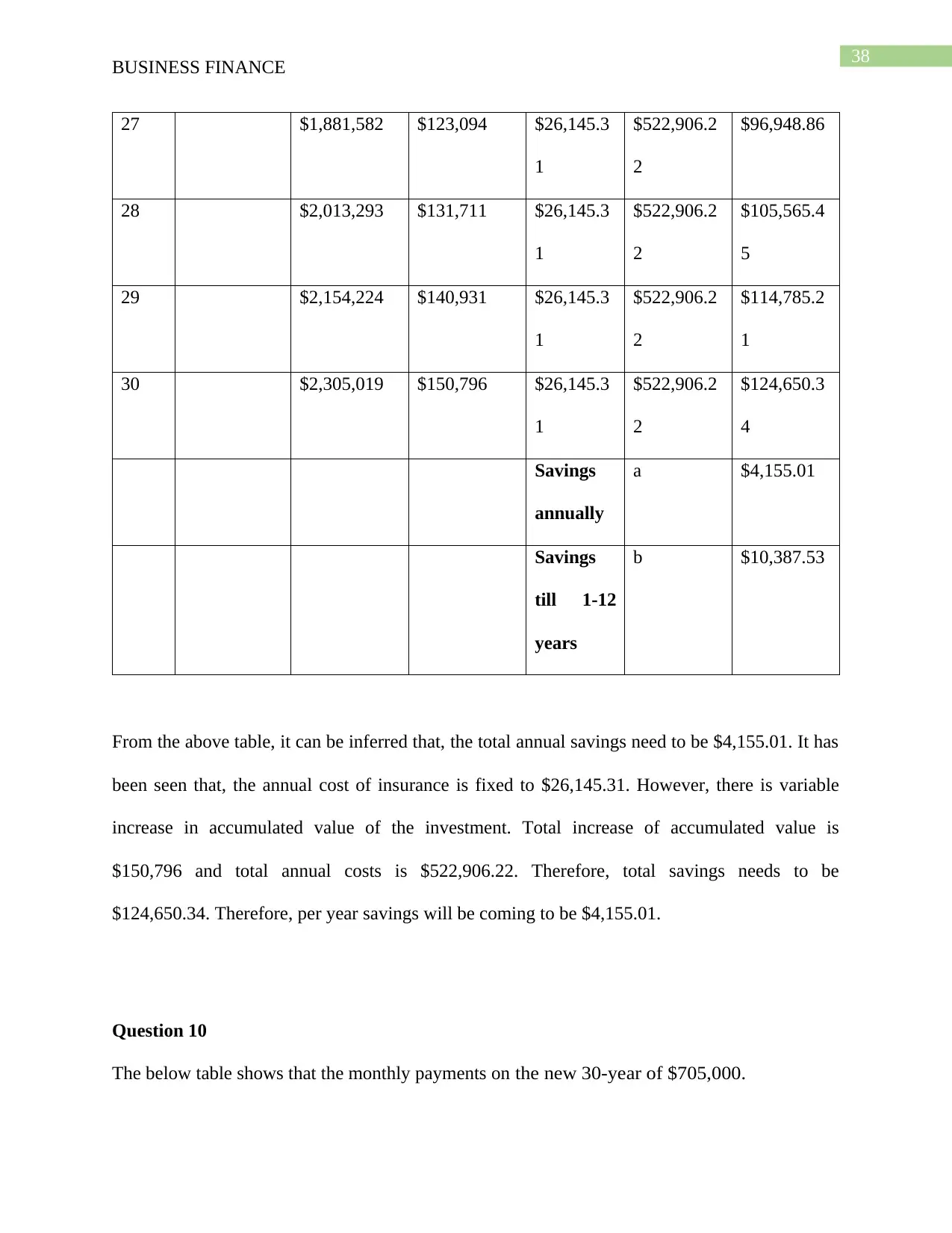

Question 5

As per exhibit 3, it has been seen that accumulated funds after 20 years insurance policy will

grew to $1,763,925. However, this amount does not reflect actual accumulated amount of

investment. The total amount of annual cost of insurance is $26,145.31. The total costs

incurred will be $522,906.22. Due to this reason, the debt position of Studebaker will be

($1,241,018.78) at the end of the 20 th year. However, since the excess amount of $300000 is

invested, then the figure of annual costs cannot be considered true. Apart from this, in that

case, the annual costs will also increase. Therefore, the correct accumulated table is as

follows:-

Increase

in

Accumulatio

n Value

Policy Payment Accumulatio

n Value

Annua

l Cost"

Cumulative Cost

End of

Year

30

BUSINESS FINANCE

0 $550,000

1 $588,500 $38,500 $47,145.31 $47,145.31

2 $629,695 $41,195 $47,145.31 $94,290.62

3 $673,774 $44,079 $47,145.31 $141,435.93

4 $720,938 $47,164 $47,145.31 $188,581.24

5 $771,403 $50,466 $47,145.31 $235,726.55

6 $825,402 $53,998 $47,145.31 $282,871.86

7 $883,180 $57,778 $47,145.31 $330,017.17

8 $945,002 $61,823 $47,145.31 $377,162.48

9 $1,011,153 $66,150 $47,145.31 $424,307.79

10 $1,081,933 $70,781 $47,145.31 $471,453.10

11 $1,157,669 $75,735 $47,145.31 $518,598.41

12 $1,238,705 $81,037 $47,145.31 $565,743.72

13 $1,325,415 $86,709 $47,145.31 $612,889.03

14 $1,418,194 $92,779 $47,145.31 $660,034.34

15 $1,517,467 $99,274 $47,145.31 $707,179.65

16 $1,623,690 $106,223 $47,145.31 $754,324.96

17 $1,737,348 $113,658 $47,145.31 $801,470.27

18 $1,858,963 $121,614 $47,145.31 $848,615.58

19 $1,989,090 $130,127 $47,145.31 $895,760.89

20 $2,128,326 $139,236 $47,145.31 $942,906.20

Therefore, from the above table, it can be inferred that the excess amount earned is

$1,578,326 and the considering the costs, the total accumulated funds earned is $635,420.25.

Excess amount $1,578,326

Fund Value less costs $635,420.25

However, considering the hidden costs, the net present value is coming to be ($8,723.59),

which is negative.

BUSINESS FINANCE

0 $550,000

1 $588,500 $38,500 $47,145.31 $47,145.31

2 $629,695 $41,195 $47,145.31 $94,290.62

3 $673,774 $44,079 $47,145.31 $141,435.93

4 $720,938 $47,164 $47,145.31 $188,581.24

5 $771,403 $50,466 $47,145.31 $235,726.55

6 $825,402 $53,998 $47,145.31 $282,871.86

7 $883,180 $57,778 $47,145.31 $330,017.17

8 $945,002 $61,823 $47,145.31 $377,162.48

9 $1,011,153 $66,150 $47,145.31 $424,307.79

10 $1,081,933 $70,781 $47,145.31 $471,453.10

11 $1,157,669 $75,735 $47,145.31 $518,598.41

12 $1,238,705 $81,037 $47,145.31 $565,743.72

13 $1,325,415 $86,709 $47,145.31 $612,889.03

14 $1,418,194 $92,779 $47,145.31 $660,034.34

15 $1,517,467 $99,274 $47,145.31 $707,179.65

16 $1,623,690 $106,223 $47,145.31 $754,324.96

17 $1,737,348 $113,658 $47,145.31 $801,470.27

18 $1,858,963 $121,614 $47,145.31 $848,615.58

19 $1,989,090 $130,127 $47,145.31 $895,760.89

20 $2,128,326 $139,236 $47,145.31 $942,906.20

Therefore, from the above table, it can be inferred that the excess amount earned is

$1,578,326 and the considering the costs, the total accumulated funds earned is $635,420.25.

Excess amount $1,578,326

Fund Value less costs $635,420.25

However, considering the hidden costs, the net present value is coming to be ($8,723.59),

which is negative.

31

BUSINESS FINANCE

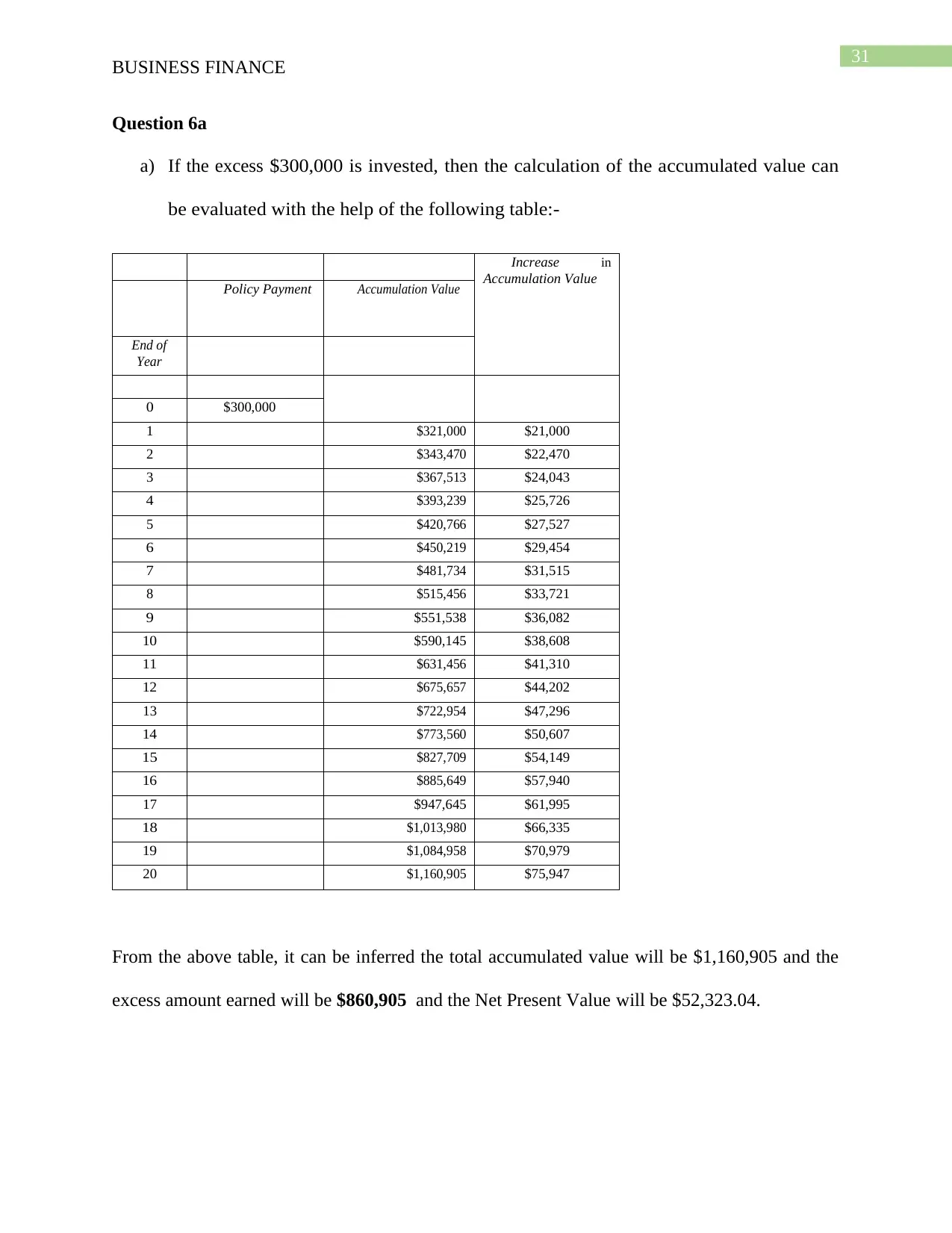

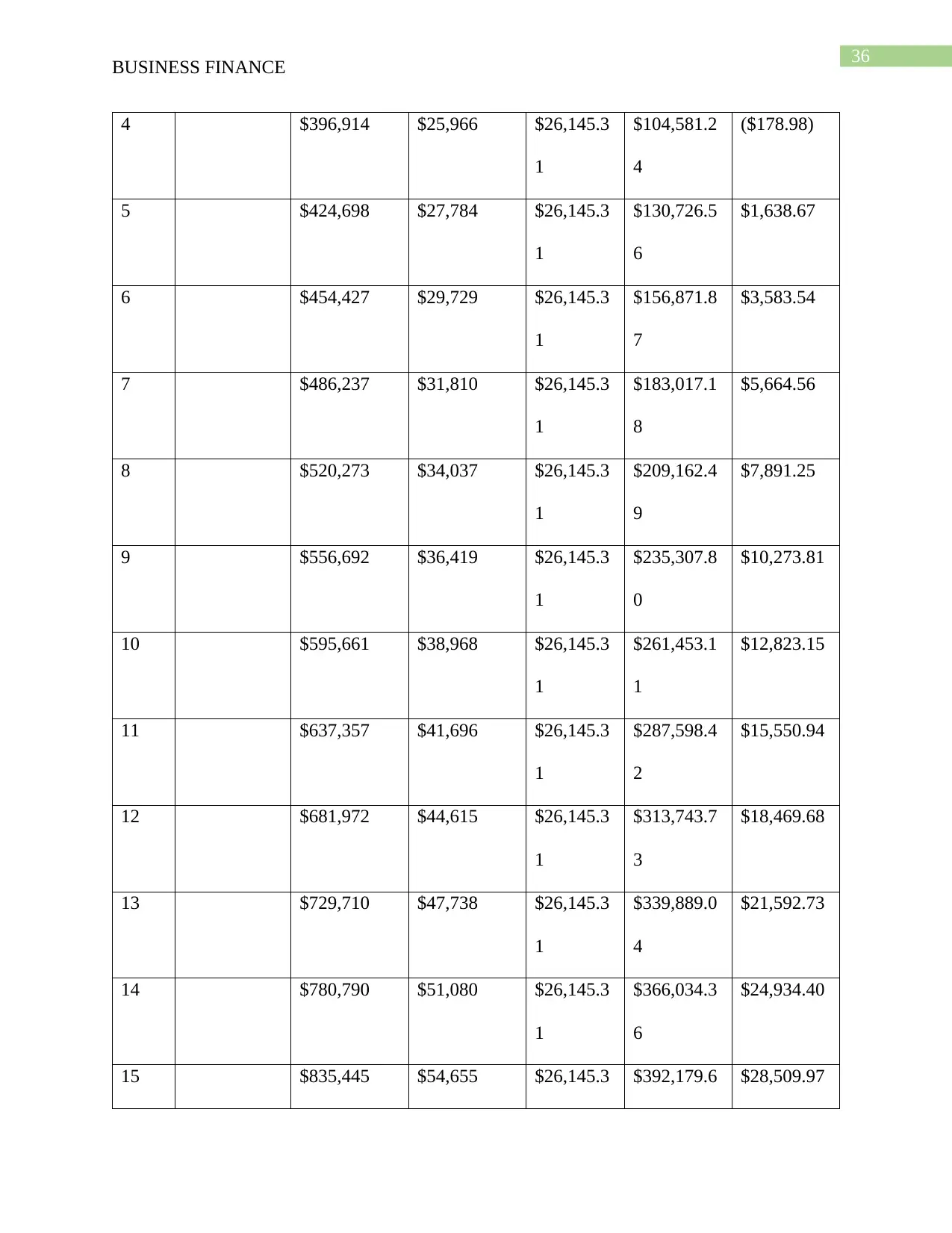

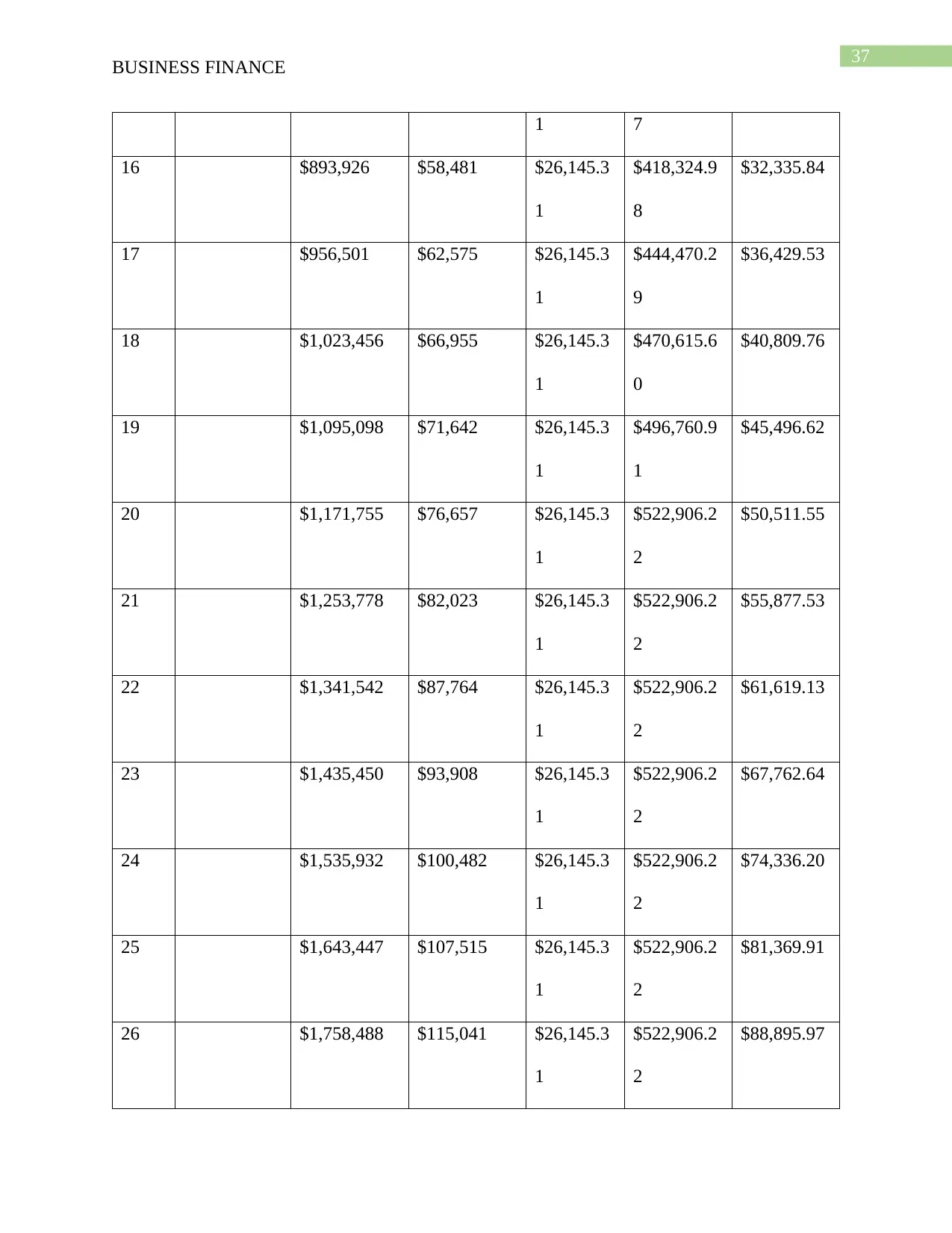

Question 6a

a) If the excess $300,000 is invested, then the calculation of the accumulated value can

be evaluated with the help of the following table:-

Increase in

Accumulation Value

Policy Payment Accumulation Value

End of

Year

0 $300,000

1 $321,000 $21,000

2 $343,470 $22,470

3 $367,513 $24,043

4 $393,239 $25,726

5 $420,766 $27,527

6 $450,219 $29,454

7 $481,734 $31,515

8 $515,456 $33,721

9 $551,538 $36,082

10 $590,145 $38,608

11 $631,456 $41,310

12 $675,657 $44,202

13 $722,954 $47,296

14 $773,560 $50,607

15 $827,709 $54,149

16 $885,649 $57,940

17 $947,645 $61,995

18 $1,013,980 $66,335

19 $1,084,958 $70,979

20 $1,160,905 $75,947

From the above table, it can be inferred the total accumulated value will be $1,160,905 and the

excess amount earned will be $860,905 and the Net Present Value will be $52,323.04.

BUSINESS FINANCE

Question 6a

a) If the excess $300,000 is invested, then the calculation of the accumulated value can

be evaluated with the help of the following table:-

Increase in

Accumulation Value

Policy Payment Accumulation Value

End of

Year

0 $300,000

1 $321,000 $21,000

2 $343,470 $22,470

3 $367,513 $24,043

4 $393,239 $25,726

5 $420,766 $27,527

6 $450,219 $29,454

7 $481,734 $31,515

8 $515,456 $33,721

9 $551,538 $36,082

10 $590,145 $38,608

11 $631,456 $41,310

12 $675,657 $44,202

13 $722,954 $47,296

14 $773,560 $50,607

15 $827,709 $54,149

16 $885,649 $57,940

17 $947,645 $61,995

18 $1,013,980 $66,335

19 $1,084,958 $70,979

20 $1,160,905 $75,947

From the above table, it can be inferred the total accumulated value will be $1,160,905 and the