UGB 106 Introduction to Management Accounting

VerifiedAdded on 2023/06/18

|20

|4088

|226

AI Summary

This article discusses the estimation of contribution per unit, break-even sales revenue, profit, and pricing strategy for Plaistead Plc and Crawford Plc in UGB 106 Introduction to Management Accounting.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

UGB 106 Introduction to

management accounting

management accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

Contents................................................................................................................................................2

Part 1.....................................................................................................................................................3

Question 2: Plaistead Plc..................................................................................................................3

Part 2.....................................................................................................................................................8

Question 3: Crawford Plc.................................................................................................................8

Part 3.....................................................................................................................................................3

Question 4:........................................................................................................................................3

REFERENCES...................................................................................................................................10

Contents................................................................................................................................................2

Part 1.....................................................................................................................................................3

Question 2: Plaistead Plc..................................................................................................................3

Part 2.....................................................................................................................................................8

Question 3: Crawford Plc.................................................................................................................8

Part 3.....................................................................................................................................................3

Question 4:........................................................................................................................................3

REFERENCES...................................................................................................................................10

Part 1

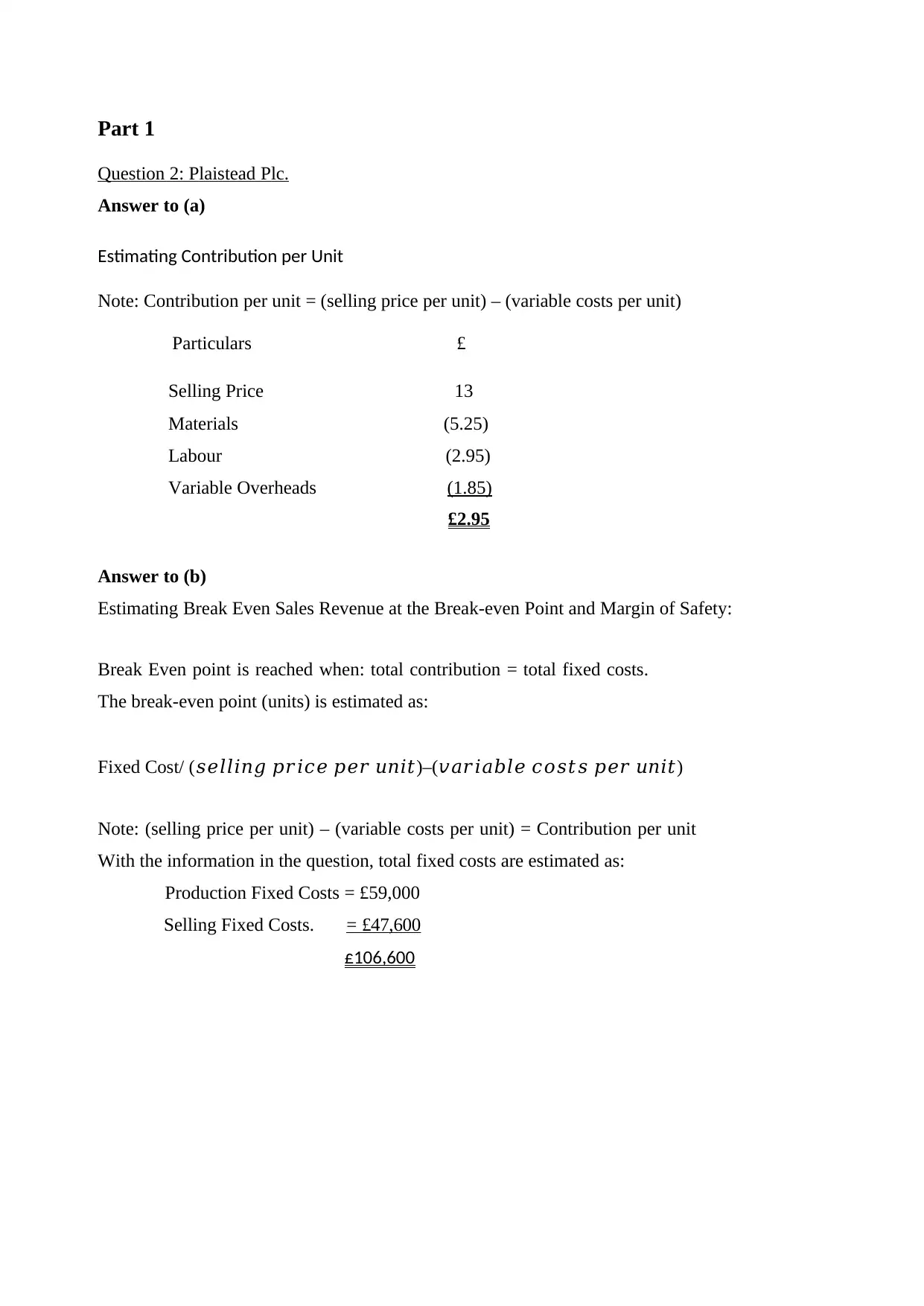

Question 2: Plaistead Plc.

Answer to (a)

Estimating Contribution per Unit

Note: Contribution per unit = (selling price per unit) – (variable costs per unit)

Particulars £

Selling Price 13

Materials (5.25)

Labour (2.95)

Variable Overheads (1.85)

£2.95

Answer to (b)

Estimating Break Even Sales Revenue at the Break-even Point and Margin of Safety:

Break Even point is reached when: total contribution = total fixed costs.

The break-even point (units) is estimated as:

Fixed Cost/ (𝑠𝑒𝑙𝑙𝑖𝑛𝑔 𝑝𝑟𝑖𝑐𝑒 𝑝𝑒𝑟 𝑢𝑛𝑖𝑡)–(𝑣𝑎𝑟𝑖𝑎𝑏𝑙𝑒 𝑐𝑜𝑠𝑡𝑠 𝑝𝑒𝑟 𝑢𝑛𝑖𝑡)

Note: (selling price per unit) – (variable costs per unit) = Contribution per unit

With the information in the question, total fixed costs are estimated as:

Production Fixed Costs = £59,000

Selling Fixed Costs. = £47,600

£106,600

Question 2: Plaistead Plc.

Answer to (a)

Estimating Contribution per Unit

Note: Contribution per unit = (selling price per unit) – (variable costs per unit)

Particulars £

Selling Price 13

Materials (5.25)

Labour (2.95)

Variable Overheads (1.85)

£2.95

Answer to (b)

Estimating Break Even Sales Revenue at the Break-even Point and Margin of Safety:

Break Even point is reached when: total contribution = total fixed costs.

The break-even point (units) is estimated as:

Fixed Cost/ (𝑠𝑒𝑙𝑙𝑖𝑛𝑔 𝑝𝑟𝑖𝑐𝑒 𝑝𝑒𝑟 𝑢𝑛𝑖𝑡)–(𝑣𝑎𝑟𝑖𝑎𝑏𝑙𝑒 𝑐𝑜𝑠𝑡𝑠 𝑝𝑒𝑟 𝑢𝑛𝑖𝑡)

Note: (selling price per unit) – (variable costs per unit) = Contribution per unit

With the information in the question, total fixed costs are estimated as:

Production Fixed Costs = £59,000

Selling Fixed Costs. = £47,600

£106,600

Applying the formula, the number of electric kettles at break-even (the break-even point

(sales): =£106,600

£2.95

= 36,136 electric kettles.

Therefore, Revenue at Break-even = 36,136 electric kettles x £13

= £469,768

Margin of Safety (Volumes/Units) = (Planned sales in unit) - (Breakeven sales in unit)

= (53, 000 electric kettles) – (36, 136 electric kettles)

= 16, 864 electric kettles

Margin of Safety (Revenue) = (Planned sales revenue) - (Breakeven revenue)

= £689,000 –£469,768

= £219, 232

OR

Margin of safety (revenue) = (Margin of safety (volume/unit)) x (Selling price)

= 16,864 electric kettles x £13

= £219, 232

Answer to (c)

Estimating profit at 53,000 electric kettles at selling price of £13per electric kettle:

Sales (from question) = 53,000 electric kettles

Break even number of electric kettles (from calculation). = 36,136 electric kettles

Therefore, sales are above break-even point by 16,864 electric kettles (53, 000 – 36,136)

Contribution per electric kettles = £2.95

Additional contribution = 16, 864 x £2.95 = £49, 749

Answer to (d)

Estimating units of electric kettles to produce and sell for a profit of £90,000

(sales): =£106,600

£2.95

= 36,136 electric kettles.

Therefore, Revenue at Break-even = 36,136 electric kettles x £13

= £469,768

Margin of Safety (Volumes/Units) = (Planned sales in unit) - (Breakeven sales in unit)

= (53, 000 electric kettles) – (36, 136 electric kettles)

= 16, 864 electric kettles

Margin of Safety (Revenue) = (Planned sales revenue) - (Breakeven revenue)

= £689,000 –£469,768

= £219, 232

OR

Margin of safety (revenue) = (Margin of safety (volume/unit)) x (Selling price)

= 16,864 electric kettles x £13

= £219, 232

Answer to (c)

Estimating profit at 53,000 electric kettles at selling price of £13per electric kettle:

Sales (from question) = 53,000 electric kettles

Break even number of electric kettles (from calculation). = 36,136 electric kettles

Therefore, sales are above break-even point by 16,864 electric kettles (53, 000 – 36,136)

Contribution per electric kettles = £2.95

Additional contribution = 16, 864 x £2.95 = £49, 749

Answer to (d)

Estimating units of electric kettles to produce and sell for a profit of £90,000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

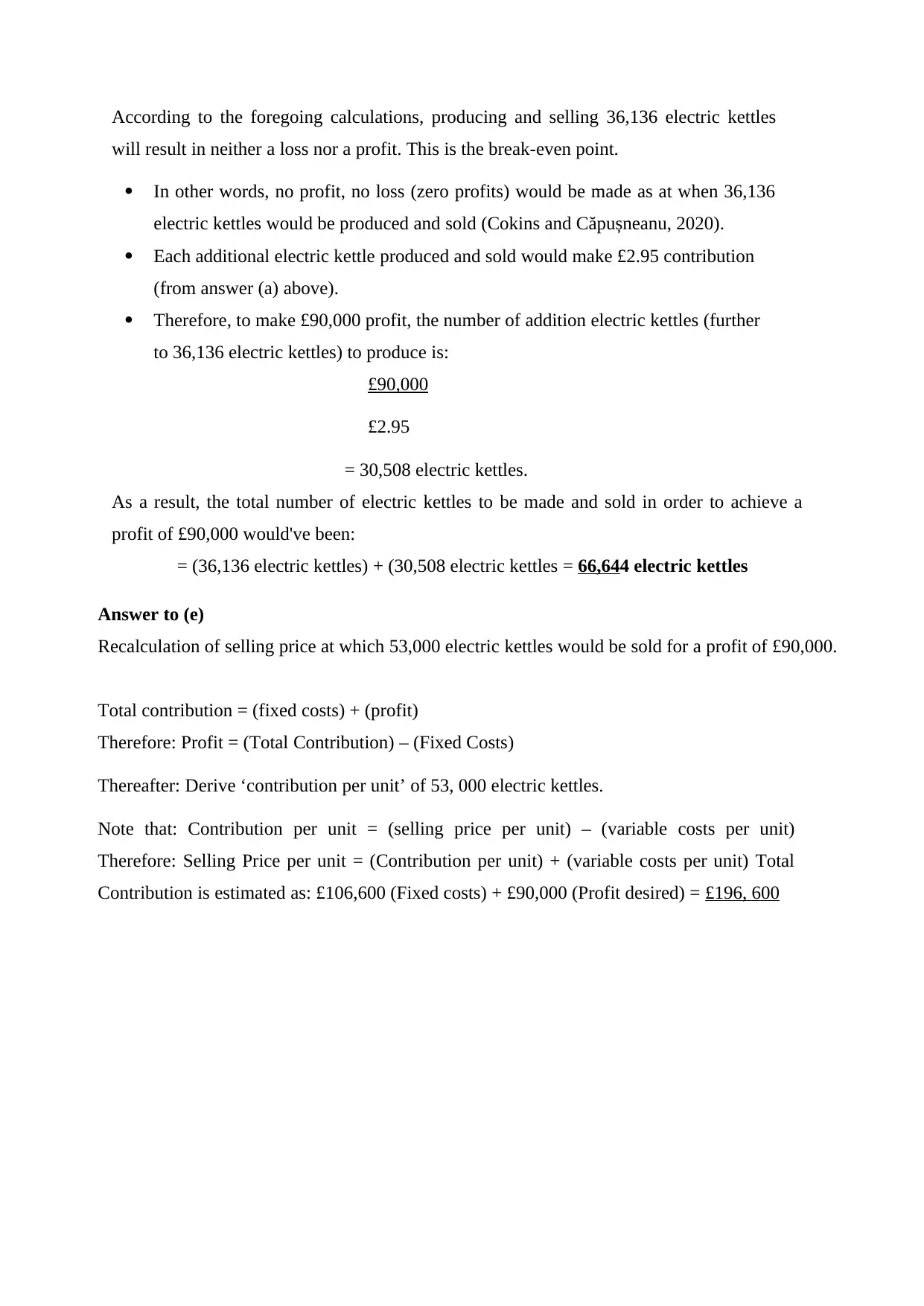

According to the foregoing calculations, producing and selling 36,136 electric kettles

will result in neither a loss nor a profit. This is the break-even point.

In other words, no profit, no loss (zero profits) would be made as at when 36,136

electric kettles would be produced and sold (Cokins and Căpușneanu, 2020).

Each additional electric kettle produced and sold would make £2.95 contribution

(from answer (a) above).

Therefore, to make £90,000 profit, the number of addition electric kettles (further

to 36,136 electric kettles) to produce is:

£90,000

£2.95

= 30,508 electric kettles.

As a result, the total number of electric kettles to be made and sold in order to achieve a

profit of £90,000 would've been:

= (36,136 electric kettles) + (30,508 electric kettles = 66,644 electric kettles

Answer to (e)

Recalculation of selling price at which 53,000 electric kettles would be sold for a profit of £90,000.

Total contribution = (fixed costs) + (profit)

Therefore: Profit = (Total Contribution) – (Fixed Costs)

Thereafter: Derive ‘contribution per unit’ of 53, 000 electric kettles.

Note that: Contribution per unit = (selling price per unit) – (variable costs per unit)

Therefore: Selling Price per unit = (Contribution per unit) + (variable costs per unit) Total

Contribution is estimated as: £106,600 (Fixed costs) + £90,000 (Profit desired) = £196, 600

will result in neither a loss nor a profit. This is the break-even point.

In other words, no profit, no loss (zero profits) would be made as at when 36,136

electric kettles would be produced and sold (Cokins and Căpușneanu, 2020).

Each additional electric kettle produced and sold would make £2.95 contribution

(from answer (a) above).

Therefore, to make £90,000 profit, the number of addition electric kettles (further

to 36,136 electric kettles) to produce is:

£90,000

£2.95

= 30,508 electric kettles.

As a result, the total number of electric kettles to be made and sold in order to achieve a

profit of £90,000 would've been:

= (36,136 electric kettles) + (30,508 electric kettles = 66,644 electric kettles

Answer to (e)

Recalculation of selling price at which 53,000 electric kettles would be sold for a profit of £90,000.

Total contribution = (fixed costs) + (profit)

Therefore: Profit = (Total Contribution) – (Fixed Costs)

Thereafter: Derive ‘contribution per unit’ of 53, 000 electric kettles.

Note that: Contribution per unit = (selling price per unit) – (variable costs per unit)

Therefore: Selling Price per unit = (Contribution per unit) + (variable costs per unit) Total

Contribution is estimated as: £106,600 (Fixed costs) + £90,000 (Profit desired) = £196, 600

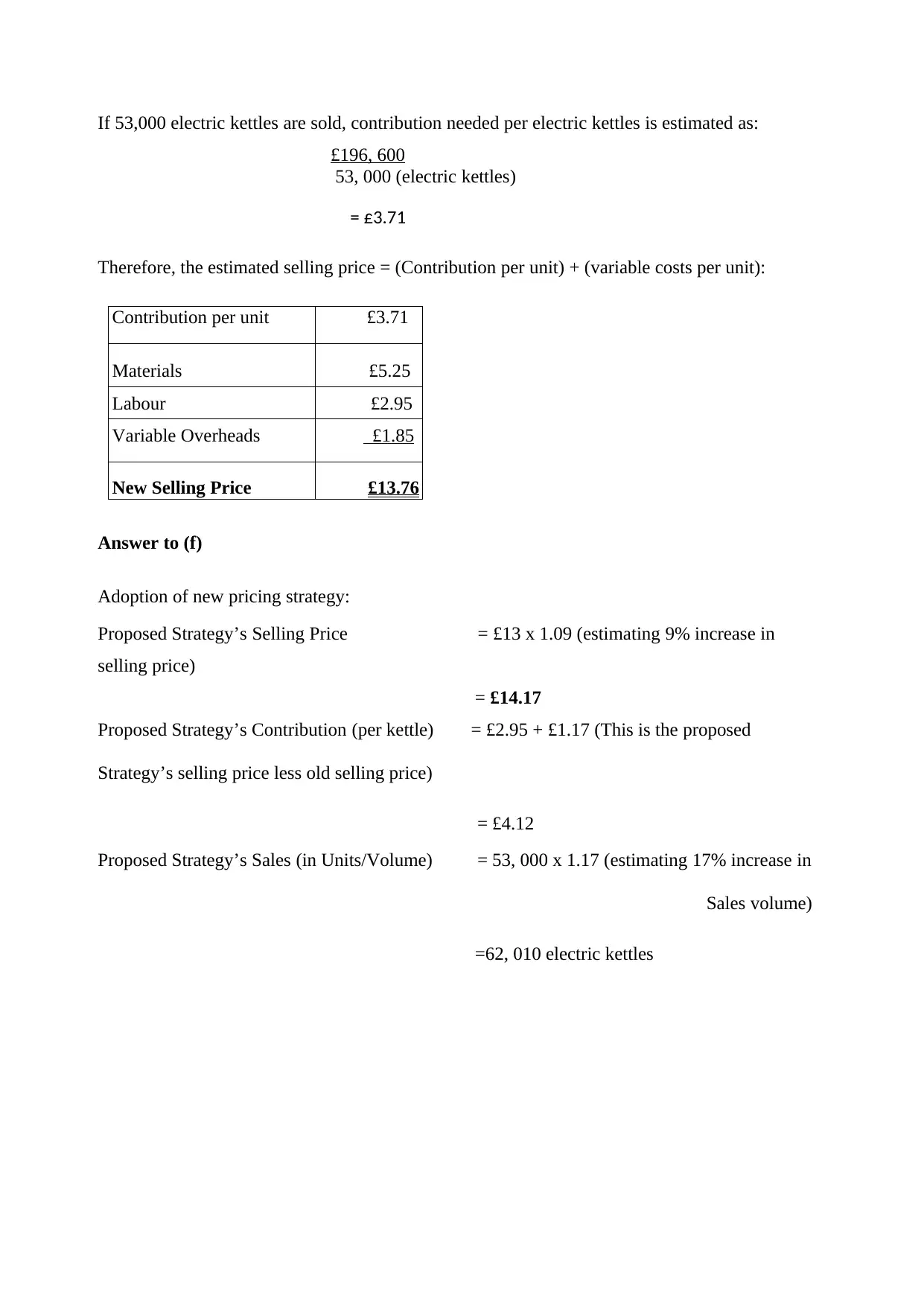

If 53,000 electric kettles are sold, contribution needed per electric kettles is estimated as:

£196, 600

53, 000 (electric kettles)

= £3.71

Therefore, the estimated selling price = (Contribution per unit) + (variable costs per unit):

Contribution per unit £3.71

Materials £5.25

Labour £2.95

Variable Overheads £1.85

New Selling Price £13.76

Answer to (f)

Adoption of new pricing strategy:

Proposed Strategy’s Selling Price = £13 x 1.09 (estimating 9% increase in

selling price)

= £14.17

Proposed Strategy’s Contribution (per kettle) = £2.95 + £1.17 (This is the proposed

Strategy’s selling price less old selling price)

= £4.12

Proposed Strategy’s Sales (in Units/Volume) = 53, 000 x 1.17 (estimating 17% increase in

Sales volume)

=62, 010 electric kettles

£196, 600

53, 000 (electric kettles)

= £3.71

Therefore, the estimated selling price = (Contribution per unit) + (variable costs per unit):

Contribution per unit £3.71

Materials £5.25

Labour £2.95

Variable Overheads £1.85

New Selling Price £13.76

Answer to (f)

Adoption of new pricing strategy:

Proposed Strategy’s Selling Price = £13 x 1.09 (estimating 9% increase in

selling price)

= £14.17

Proposed Strategy’s Contribution (per kettle) = £2.95 + £1.17 (This is the proposed

Strategy’s selling price less old selling price)

= £4.12

Proposed Strategy’s Sales (in Units/Volume) = 53, 000 x 1.17 (estimating 17% increase in

Sales volume)

=62, 010 electric kettles

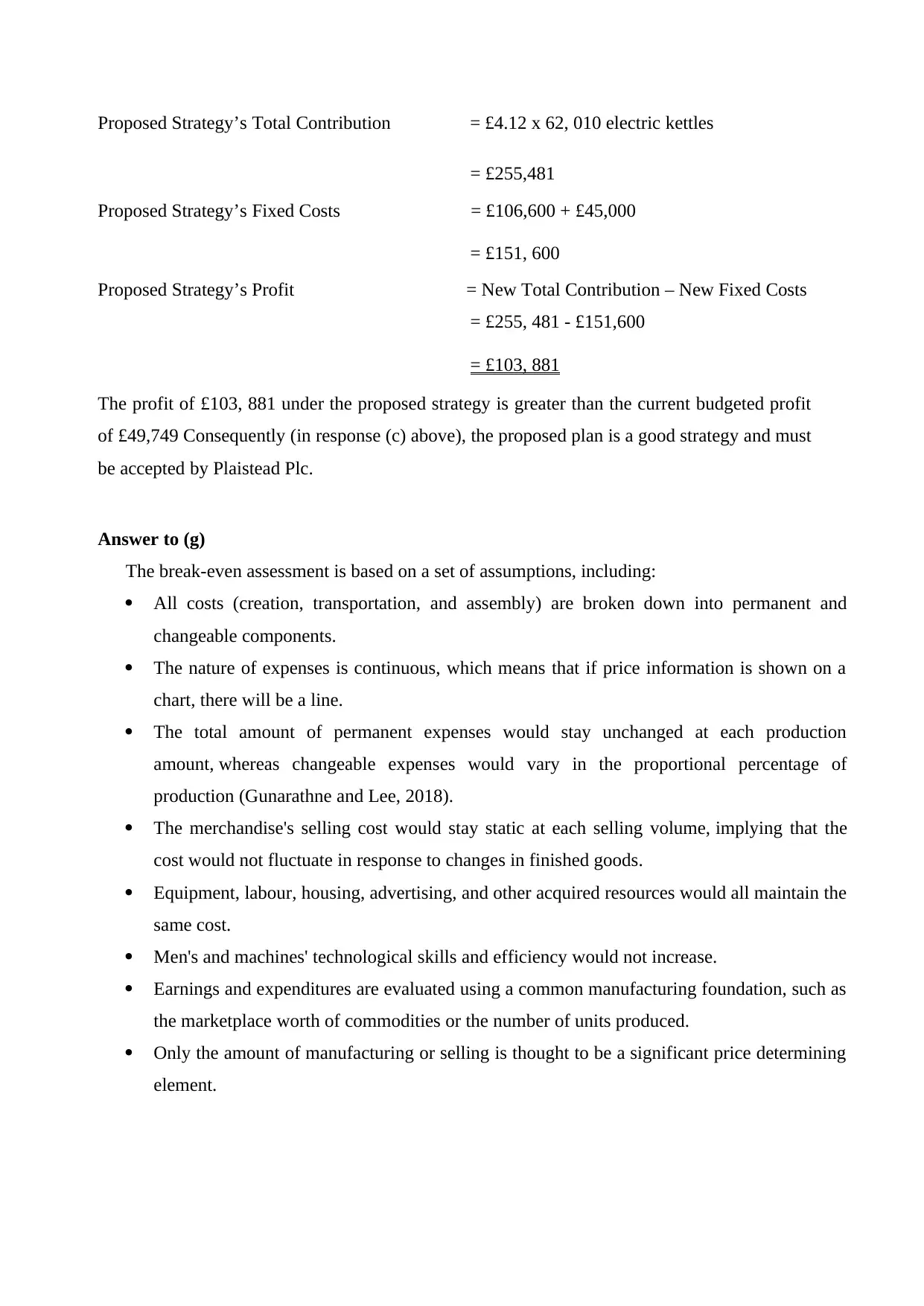

Proposed Strategy’s Total Contribution = £4.12 x 62, 010 electric kettles

= £255,481

Proposed Strategy’s Fixed Costs = £106,600 + £45,000

= £151, 600

Proposed Strategy’s Profit = New Total Contribution – New Fixed Costs

= £255, 481 - £151,600

= £103, 881

The profit of £103, 881 under the proposed strategy is greater than the current budgeted profit

of £49,749 Consequently (in response (c) above), the proposed plan is a good strategy and must

be accepted by Plaistead Plc.

Answer to (g)

The break-even assessment is based on a set of assumptions, including:

All costs (creation, transportation, and assembly) are broken down into permanent and

changeable components.

The nature of expenses is continuous, which means that if price information is shown on a

chart, there will be a line.

The total amount of permanent expenses would stay unchanged at each production

amount, whereas changeable expenses would vary in the proportional percentage of

production (Gunarathne and Lee, 2018).

The merchandise's selling cost would stay static at each selling volume, implying that the

cost would not fluctuate in response to changes in finished goods.

Equipment, labour, housing, advertising, and other acquired resources would all maintain the

same cost.

Men's and machines' technological skills and efficiency would not increase.

Earnings and expenditures are evaluated using a common manufacturing foundation, such as

the marketplace worth of commodities or the number of units produced.

Only the amount of manufacturing or selling is thought to be a significant price determining

element.

= £255,481

Proposed Strategy’s Fixed Costs = £106,600 + £45,000

= £151, 600

Proposed Strategy’s Profit = New Total Contribution – New Fixed Costs

= £255, 481 - £151,600

= £103, 881

The profit of £103, 881 under the proposed strategy is greater than the current budgeted profit

of £49,749 Consequently (in response (c) above), the proposed plan is a good strategy and must

be accepted by Plaistead Plc.

Answer to (g)

The break-even assessment is based on a set of assumptions, including:

All costs (creation, transportation, and assembly) are broken down into permanent and

changeable components.

The nature of expenses is continuous, which means that if price information is shown on a

chart, there will be a line.

The total amount of permanent expenses would stay unchanged at each production

amount, whereas changeable expenses would vary in the proportional percentage of

production (Gunarathne and Lee, 2018).

The merchandise's selling cost would stay static at each selling volume, implying that the

cost would not fluctuate in response to changes in finished goods.

Equipment, labour, housing, advertising, and other acquired resources would all maintain the

same cost.

Men's and machines' technological skills and efficiency would not increase.

Earnings and expenditures are evaluated using a common manufacturing foundation, such as

the marketplace worth of commodities or the number of units produced.

Only the amount of manufacturing or selling is thought to be a significant price determining

element.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Part 2

Question 3: Crawford Plc

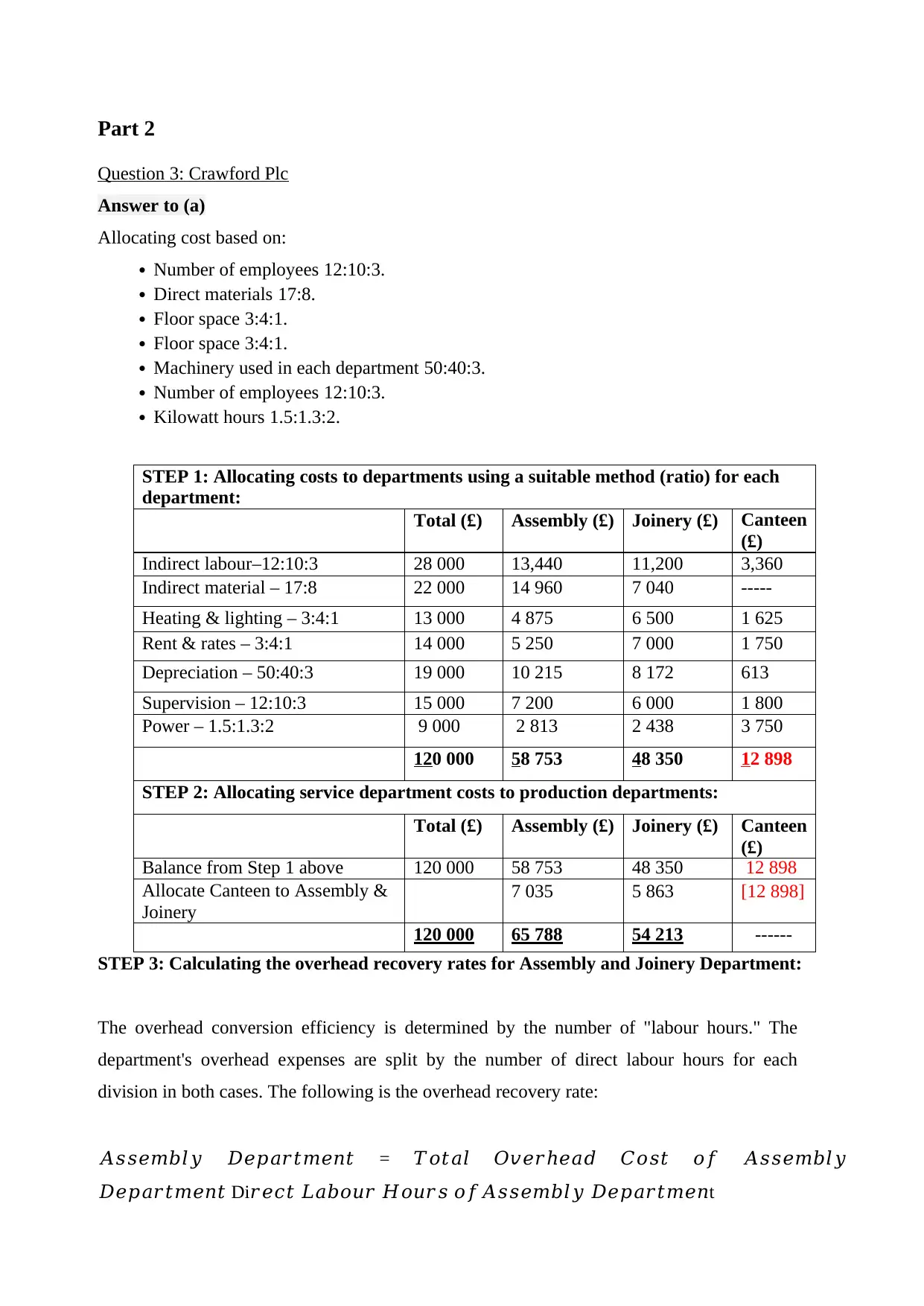

Answer to (a)

Allocating cost based on:

Number of employees 12:10:3.

Direct materials 17:8.

Floor space 3:4:1.

Floor space 3:4:1.

Machinery used in each department 50:40:3.

Number of employees 12:10:3.

Kilowatt hours 1.5:1.3:2.

STEP 1: Allocating costs to departments using a suitable method (ratio) for each

department:

Total (£) Assembly (£) Joinery (£) Canteen

(£)

Indirect labour–12:10:3 28 000 13,440 11,200 3,360

Indirect material – 17:8 22 000 14 960 7 040 -----

Heating & lighting – 3:4:1 13 000 4 875 6 500 1 625

Rent & rates – 3:4:1 14 000 5 250 7 000 1 750

Depreciation – 50:40:3 19 000 10 215 8 172 613

Supervision – 12:10:3 15 000 7 200 6 000 1 800

Power – 1.5:1.3:2 9 000 2 813 2 438 3 750

120 000 58 753 48 350 12 898

STEP 2: Allocating service department costs to production departments:

Total (£) Assembly (£) Joinery (£) Canteen

(£)

Balance from Step 1 above 120 000 58 753 48 350 12 898

Allocate Canteen to Assembly &

Joinery

7 035 5 863 [12 898]

120 000 65 788 54 213 ------

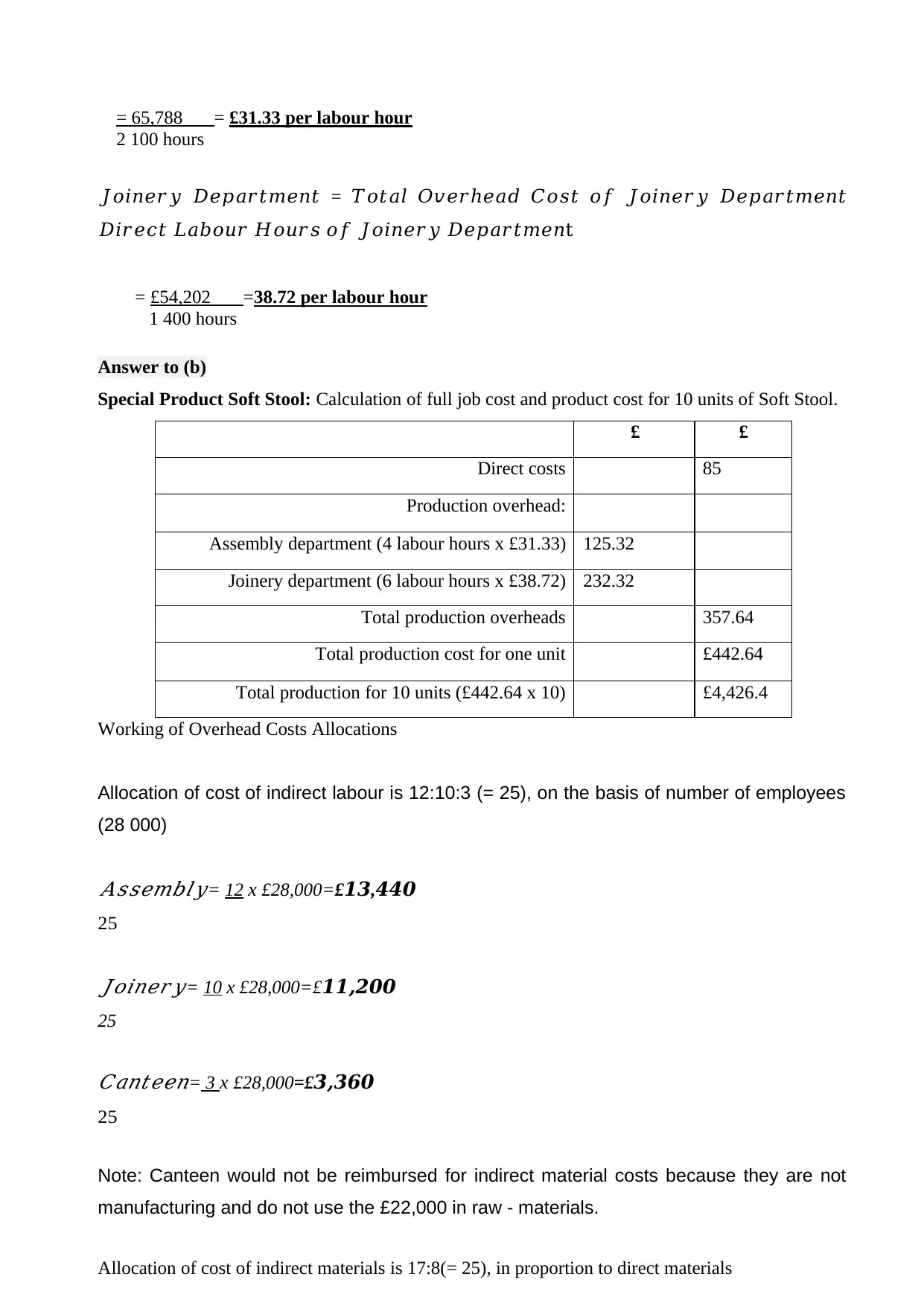

STEP 3: Calculating the overhead recovery rates for Assembly and Joinery Department:

The overhead conversion efficiency is determined by the number of "labour hours." The

department's overhead expenses are split by the number of direct labour hours for each

division in both cases. The following is the overhead recovery rate:

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦 𝐷𝑒𝑝𝑎𝑟𝑡𝑚𝑒𝑛𝑡 = 𝑇𝑜𝑡𝑎𝑙 𝑂𝑣𝑒𝑟ℎ𝑒𝑎𝑑 𝐶𝑜𝑠𝑡 𝑜𝑓 𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦

𝐷𝑒𝑝𝑎𝑟𝑡𝑚𝑒𝑛𝑡 Di𝑟𝑒𝑐𝑡 𝐿𝑎𝑏𝑜𝑢𝑟 𝐻𝑜𝑢𝑟𝑠 𝑜𝑓𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦 𝐷𝑒𝑝𝑎𝑟𝑡𝑚𝑒𝑛t

Question 3: Crawford Plc

Answer to (a)

Allocating cost based on:

Number of employees 12:10:3.

Direct materials 17:8.

Floor space 3:4:1.

Floor space 3:4:1.

Machinery used in each department 50:40:3.

Number of employees 12:10:3.

Kilowatt hours 1.5:1.3:2.

STEP 1: Allocating costs to departments using a suitable method (ratio) for each

department:

Total (£) Assembly (£) Joinery (£) Canteen

(£)

Indirect labour–12:10:3 28 000 13,440 11,200 3,360

Indirect material – 17:8 22 000 14 960 7 040 -----

Heating & lighting – 3:4:1 13 000 4 875 6 500 1 625

Rent & rates – 3:4:1 14 000 5 250 7 000 1 750

Depreciation – 50:40:3 19 000 10 215 8 172 613

Supervision – 12:10:3 15 000 7 200 6 000 1 800

Power – 1.5:1.3:2 9 000 2 813 2 438 3 750

120 000 58 753 48 350 12 898

STEP 2: Allocating service department costs to production departments:

Total (£) Assembly (£) Joinery (£) Canteen

(£)

Balance from Step 1 above 120 000 58 753 48 350 12 898

Allocate Canteen to Assembly &

Joinery

7 035 5 863 [12 898]

120 000 65 788 54 213 ------

STEP 3: Calculating the overhead recovery rates for Assembly and Joinery Department:

The overhead conversion efficiency is determined by the number of "labour hours." The

department's overhead expenses are split by the number of direct labour hours for each

division in both cases. The following is the overhead recovery rate:

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦 𝐷𝑒𝑝𝑎𝑟𝑡𝑚𝑒𝑛𝑡 = 𝑇𝑜𝑡𝑎𝑙 𝑂𝑣𝑒𝑟ℎ𝑒𝑎𝑑 𝐶𝑜𝑠𝑡 𝑜𝑓 𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦

𝐷𝑒𝑝𝑎𝑟𝑡𝑚𝑒𝑛𝑡 Di𝑟𝑒𝑐𝑡 𝐿𝑎𝑏𝑜𝑢𝑟 𝐻𝑜𝑢𝑟𝑠 𝑜𝑓𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦 𝐷𝑒𝑝𝑎𝑟𝑡𝑚𝑒𝑛t

= 65,788 = £31.33 per labour hour

2 100 hours

𝐽𝑜𝑖𝑛𝑒𝑟𝑦 𝐷𝑒𝑝𝑎𝑟𝑡𝑚𝑒𝑛𝑡 = 𝑇𝑜𝑡𝑎𝑙 𝑂𝑣𝑒𝑟ℎ𝑒𝑎𝑑 𝐶𝑜𝑠𝑡 𝑜𝑓 𝐽𝑜𝑖𝑛𝑒𝑟𝑦 𝐷𝑒𝑝𝑎𝑟𝑡𝑚𝑒𝑛𝑡

𝐷𝑖𝑟𝑒𝑐𝑡 𝐿𝑎𝑏𝑜𝑢𝑟 𝐻𝑜𝑢𝑟𝑠 𝑜𝑓 𝐽𝑜𝑖𝑛𝑒𝑟𝑦 𝐷𝑒𝑝𝑎𝑟𝑡𝑚𝑒𝑛t

= £54,202 =38.72 per labour hour

1 400 hours

Answer to (b)

Special Product Soft Stool: Calculation of full job cost and product cost for 10 units of Soft Stool.

£ £

Direct costs 85

Production overhead:

Assembly department (4 labour hours x £31.33) 125.32

Joinery department (6 labour hours x £38.72) 232.32

Total production overheads 357.64

Total production cost for one unit £442.64

Total production for 10 units (£442.64 x 10) £4,426.4

Working of Overhead Costs Allocations

Allocation of cost of indirect labour is 12:10:3 (= 25), on the basis of number of employees

(28 000)

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦= 12 x £28,000=£13,440

25

𝐽𝑜𝑖𝑛𝑒𝑟𝑦= 10 x £28,000=£11,200

25

𝐶𝑎𝑛𝑡𝑒𝑒𝑛= 3 x £28,000=£3,360

25

Note: Canteen would not be reimbursed for indirect material costs because they are not

manufacturing and do not use the £22,000 in raw - materials.

Allocation of cost of indirect materials is 17:8(= 25), in proportion to direct materials

2 100 hours

𝐽𝑜𝑖𝑛𝑒𝑟𝑦 𝐷𝑒𝑝𝑎𝑟𝑡𝑚𝑒𝑛𝑡 = 𝑇𝑜𝑡𝑎𝑙 𝑂𝑣𝑒𝑟ℎ𝑒𝑎𝑑 𝐶𝑜𝑠𝑡 𝑜𝑓 𝐽𝑜𝑖𝑛𝑒𝑟𝑦 𝐷𝑒𝑝𝑎𝑟𝑡𝑚𝑒𝑛𝑡

𝐷𝑖𝑟𝑒𝑐𝑡 𝐿𝑎𝑏𝑜𝑢𝑟 𝐻𝑜𝑢𝑟𝑠 𝑜𝑓 𝐽𝑜𝑖𝑛𝑒𝑟𝑦 𝐷𝑒𝑝𝑎𝑟𝑡𝑚𝑒𝑛t

= £54,202 =38.72 per labour hour

1 400 hours

Answer to (b)

Special Product Soft Stool: Calculation of full job cost and product cost for 10 units of Soft Stool.

£ £

Direct costs 85

Production overhead:

Assembly department (4 labour hours x £31.33) 125.32

Joinery department (6 labour hours x £38.72) 232.32

Total production overheads 357.64

Total production cost for one unit £442.64

Total production for 10 units (£442.64 x 10) £4,426.4

Working of Overhead Costs Allocations

Allocation of cost of indirect labour is 12:10:3 (= 25), on the basis of number of employees

(28 000)

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦= 12 x £28,000=£13,440

25

𝐽𝑜𝑖𝑛𝑒𝑟𝑦= 10 x £28,000=£11,200

25

𝐶𝑎𝑛𝑡𝑒𝑒𝑛= 3 x £28,000=£3,360

25

Note: Canteen would not be reimbursed for indirect material costs because they are not

manufacturing and do not use the £22,000 in raw - materials.

Allocation of cost of indirect materials is 17:8(= 25), in proportion to direct materials

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦= 17x £22,000=£1

𝟒,960

25

𝐽𝑜𝑖𝑛𝑒𝑟𝑦= 8 x£22,000=£7,4

𝟎

25

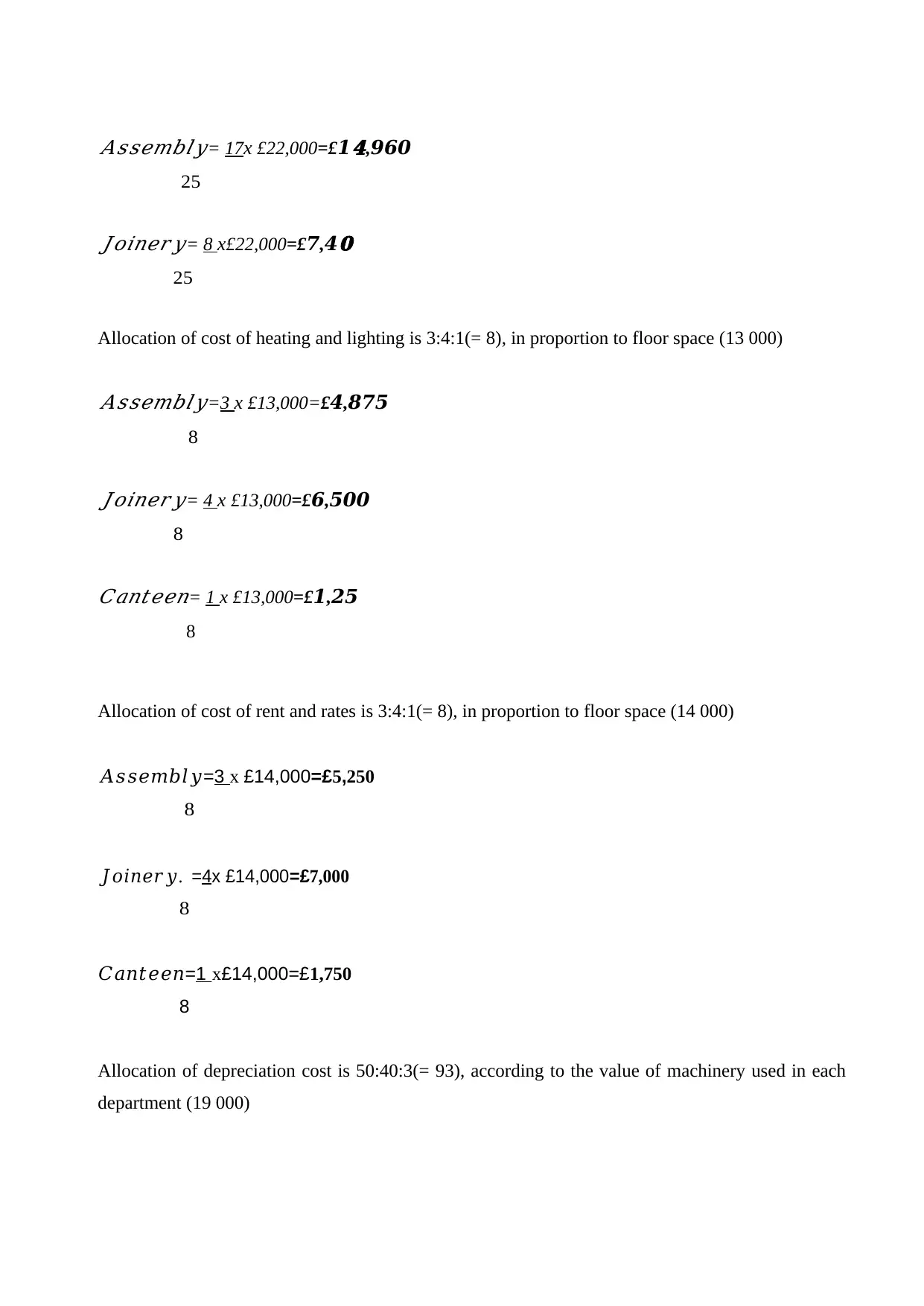

Allocation of cost of heating and lighting is 3:4:1(= 8), in proportion to floor space (13 000)

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦=3 x £13,000=£4,875

8

𝐽𝑜𝑖𝑛𝑒𝑟𝑦= 4 x £13,000=£6,500

8𝐶𝑎𝑛𝑡𝑒𝑒𝑛= 1 x £13,000=£1,25

8

Allocation of cost of rent and rates is 3:4:1(= 8), in proportion to floor space (14 000)

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦=3 x £14,000=£5,250

8

𝐽𝑜𝑖𝑛𝑒𝑟𝑦. =4x £14,000=£7,000

8

𝐶𝑎𝑛𝑡𝑒𝑒𝑛=1 x£14,000=£1,750

8

Allocation of depreciation cost is 50:40:3(= 93), according to the value of machinery used in each

department (19 000)

𝟒,960

25

𝐽𝑜𝑖𝑛𝑒𝑟𝑦= 8 x£22,000=£7,4

𝟎

25

Allocation of cost of heating and lighting is 3:4:1(= 8), in proportion to floor space (13 000)

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦=3 x £13,000=£4,875

8

𝐽𝑜𝑖𝑛𝑒𝑟𝑦= 4 x £13,000=£6,500

8𝐶𝑎𝑛𝑡𝑒𝑒𝑛= 1 x £13,000=£1,25

8

Allocation of cost of rent and rates is 3:4:1(= 8), in proportion to floor space (14 000)

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦=3 x £14,000=£5,250

8

𝐽𝑜𝑖𝑛𝑒𝑟𝑦. =4x £14,000=£7,000

8

𝐶𝑎𝑛𝑡𝑒𝑒𝑛=1 x£14,000=£1,750

8

Allocation of depreciation cost is 50:40:3(= 93), according to the value of machinery used in each

department (19 000)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

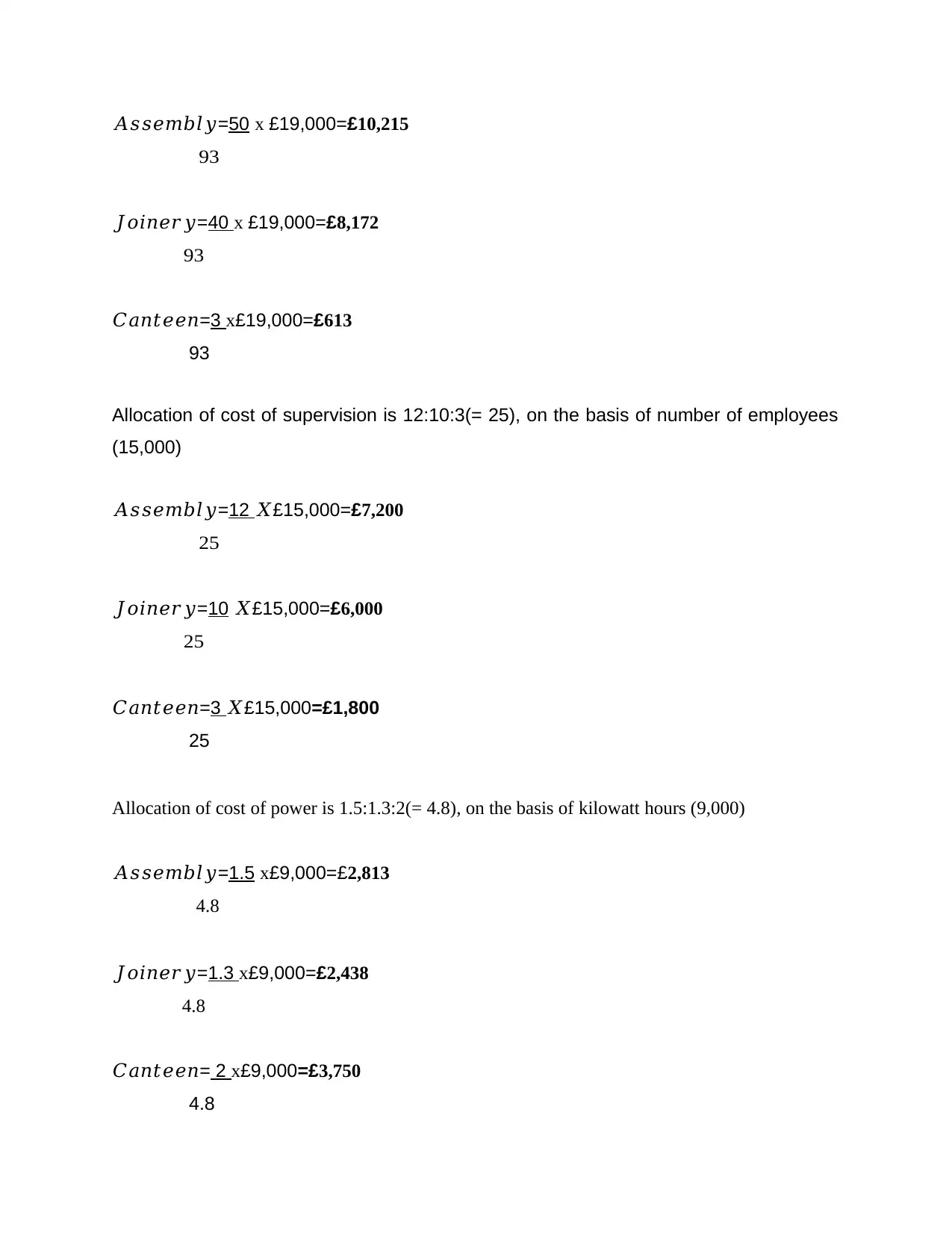

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦=50 x £19,000=£10,215

93

𝐽𝑜𝑖𝑛𝑒𝑟𝑦=40 x £19,000=£8,172

93

𝐶𝑎𝑛𝑡𝑒𝑒𝑛=3 x£19,000=£613

93

Allocation of cost of supervision is 12:10:3(= 25), on the basis of number of employees

(15,000)

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦=12 𝑋£15,000=£7,200

25

𝐽𝑜𝑖𝑛𝑒𝑟𝑦=10 𝑋£15,000=£6,000

25

𝐶𝑎𝑛𝑡𝑒𝑒𝑛=3 𝑋£15,000=£1,800

25

Allocation of cost of power is 1.5:1.3:2(= 4.8), on the basis of kilowatt hours (9,000)

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦=1.5 x£9,000=£2,813

4.8

𝐽𝑜𝑖𝑛𝑒𝑟𝑦=1.3 x£9,000=£2,438

4.8

𝐶𝑎𝑛𝑡𝑒𝑒𝑛= 2 x£9,000=£3,750

4.8

93

𝐽𝑜𝑖𝑛𝑒𝑟𝑦=40 x £19,000=£8,172

93

𝐶𝑎𝑛𝑡𝑒𝑒𝑛=3 x£19,000=£613

93

Allocation of cost of supervision is 12:10:3(= 25), on the basis of number of employees

(15,000)

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦=12 𝑋£15,000=£7,200

25

𝐽𝑜𝑖𝑛𝑒𝑟𝑦=10 𝑋£15,000=£6,000

25

𝐶𝑎𝑛𝑡𝑒𝑒𝑛=3 𝑋£15,000=£1,800

25

Allocation of cost of power is 1.5:1.3:2(= 4.8), on the basis of kilowatt hours (9,000)

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦=1.5 x£9,000=£2,813

4.8

𝐽𝑜𝑖𝑛𝑒𝑟𝑦=1.3 x£9,000=£2,438

4.8

𝐶𝑎𝑛𝑡𝑒𝑒𝑛= 2 x£9,000=£3,750

4.8

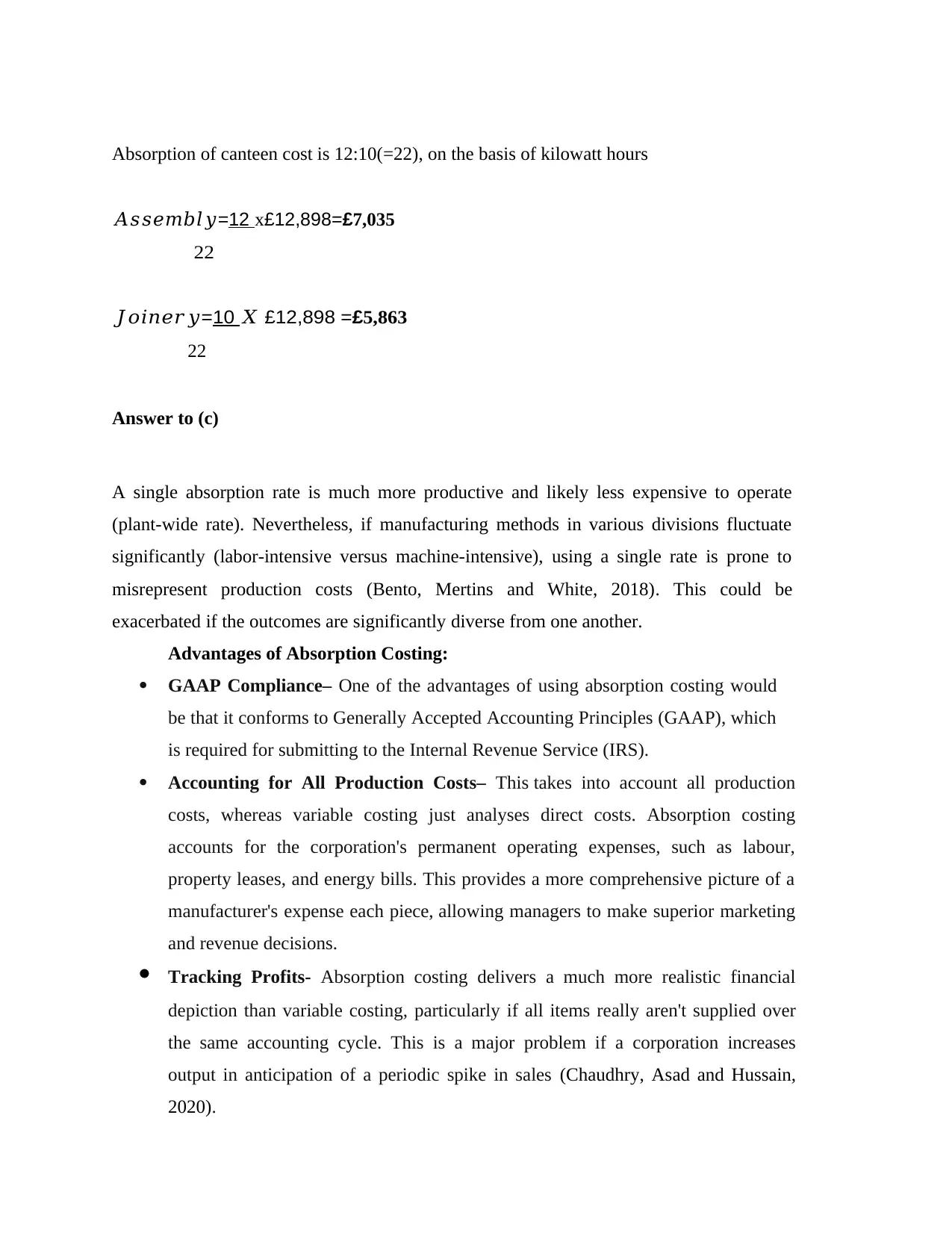

Absorption of canteen cost is 12:10(=22), on the basis of kilowatt hours

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦=12 x£12,898=£7,035

22

𝐽𝑜𝑖𝑛𝑒𝑟𝑦=10 𝑋 £12,898 =£5,863

22

Answer to (c)

A single absorption rate is much more productive and likely less expensive to operate

(plant-wide rate). Nevertheless, if manufacturing methods in various divisions fluctuate

significantly (labor-intensive versus machine-intensive), using a single rate is prone to

misrepresent production costs (Bento, Mertins and White, 2018). This could be

exacerbated if the outcomes are significantly diverse from one another.

Advantages of Absorption Costing:

GAAP Compliance– One of the advantages of using absorption costing would

be that it conforms to Generally Accepted Accounting Principles (GAAP), which

is required for submitting to the Internal Revenue Service (IRS).

Accounting for All Production Costs– This takes into account all production

costs, whereas variable costing just analyses direct costs. Absorption costing

accounts for the corporation's permanent operating expenses, such as labour,

property leases, and energy bills. This provides a more comprehensive picture of a

manufacturer's expense each piece, allowing managers to make superior marketing

and revenue decisions.

Tracking Profits- Absorption costing delivers a much more realistic financial

depiction than variable costing, particularly if all items really aren't supplied over

the same accounting cycle. This is a major problem if a corporation increases

output in anticipation of a periodic spike in sales (Chaudhry, Asad and Hussain,

2020).

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦=12 x£12,898=£7,035

22

𝐽𝑜𝑖𝑛𝑒𝑟𝑦=10 𝑋 £12,898 =£5,863

22

Answer to (c)

A single absorption rate is much more productive and likely less expensive to operate

(plant-wide rate). Nevertheless, if manufacturing methods in various divisions fluctuate

significantly (labor-intensive versus machine-intensive), using a single rate is prone to

misrepresent production costs (Bento, Mertins and White, 2018). This could be

exacerbated if the outcomes are significantly diverse from one another.

Advantages of Absorption Costing:

GAAP Compliance– One of the advantages of using absorption costing would

be that it conforms to Generally Accepted Accounting Principles (GAAP), which

is required for submitting to the Internal Revenue Service (IRS).

Accounting for All Production Costs– This takes into account all production

costs, whereas variable costing just analyses direct costs. Absorption costing

accounts for the corporation's permanent operating expenses, such as labour,

property leases, and energy bills. This provides a more comprehensive picture of a

manufacturer's expense each piece, allowing managers to make superior marketing

and revenue decisions.

Tracking Profits- Absorption costing delivers a much more realistic financial

depiction than variable costing, particularly if all items really aren't supplied over

the same accounting cycle. This is a major problem if a corporation increases

output in anticipation of a periodic spike in sales (Chaudhry, Asad and Hussain,

2020).

Disadvantages of Absorption Costing:

Skewed Profit and Loss- Absorption costing could give the impression that a

company is making more money than it actually is throughout any given accounting

period. This is due to the fact that all permanent expenditures are not subtracted

from the firm's revenue unless all of the corporation's manufactured products are

supplied. As a result, the management could be deceived.

No influence on operational efficiency- Absorption costing lacks to provide quite a

comprehensive a cost assessment as variable costing; hence it has no impact on

operating effectiveness. When fixed expenses account for a large portion of total

expenses, it's tough to figure out expense variances at various sales volumes, making

it harder for managers to take the optimal operating judgments.

Not suited to product line comparison– Variable costing, instead of absorption

costing, would've been significantly more effective and beneficial in situations when

an organisation desires to synchronize the unique revenue of a commodity. This is

because it is easier to determine the cost difference between one item and another by

properly observing the variable costs of each commodity.

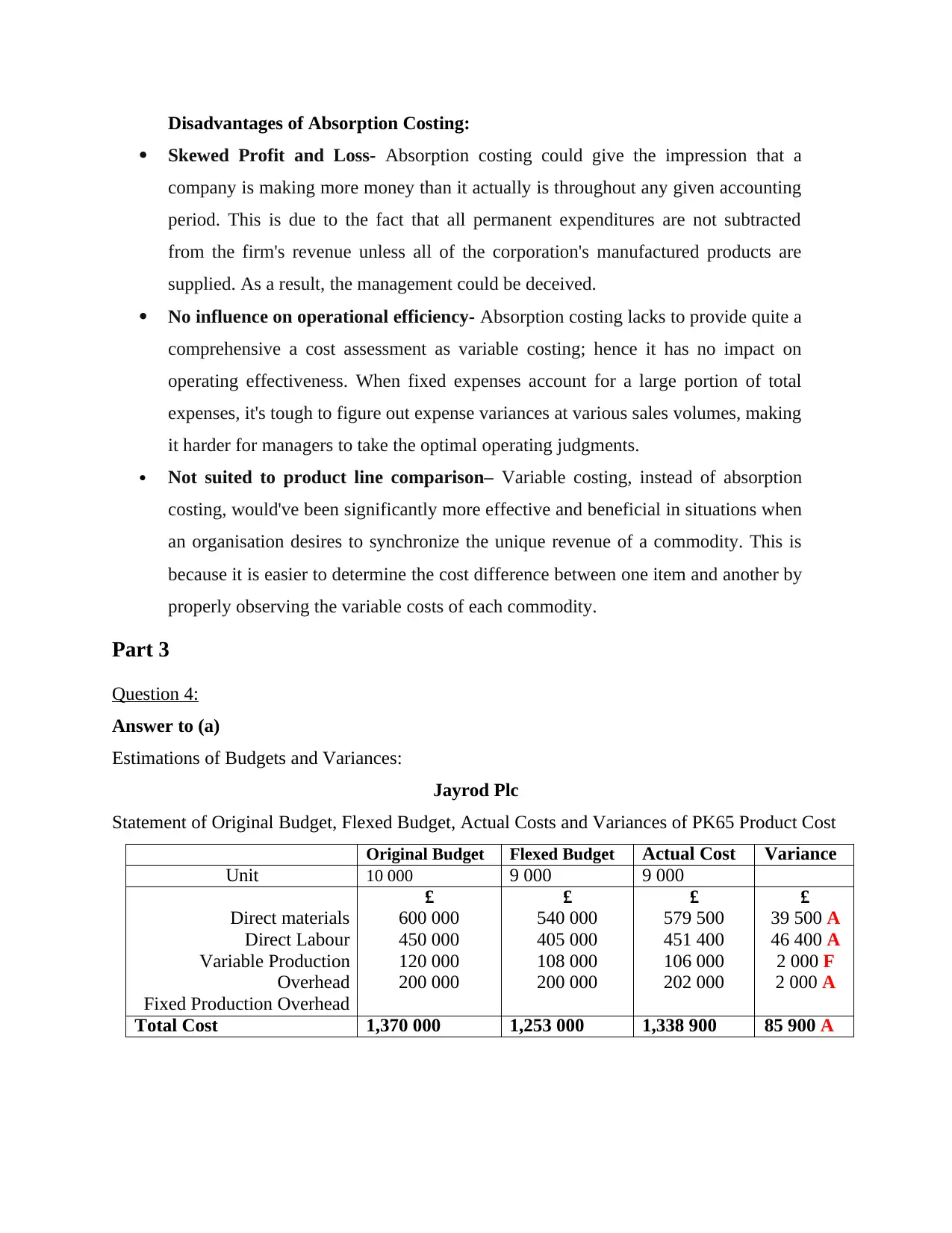

Part 3

Question 4:

Answer to (a)

Estimations of Budgets and Variances:

Jayrod Plc

Statement of Original Budget, Flexed Budget, Actual Costs and Variances of PK65 Product Cost

Original Budget Flexed Budget Actual Cost Variance

Unit 10 000 9 000 9 000

£ £ £ £

Direct materials 600 000 540 000 579 500 39 500 A

Direct Labour 450 000 405 000 451 400 46 400 A

Variable Production 120 000 108 000 106 000 2 000 F

Overhead 200 000 200 000 202 000 2 000 A

Fixed Production Overhead

Total Cost 1,370 000 1,253 000 1,338 900 85 900 A

Skewed Profit and Loss- Absorption costing could give the impression that a

company is making more money than it actually is throughout any given accounting

period. This is due to the fact that all permanent expenditures are not subtracted

from the firm's revenue unless all of the corporation's manufactured products are

supplied. As a result, the management could be deceived.

No influence on operational efficiency- Absorption costing lacks to provide quite a

comprehensive a cost assessment as variable costing; hence it has no impact on

operating effectiveness. When fixed expenses account for a large portion of total

expenses, it's tough to figure out expense variances at various sales volumes, making

it harder for managers to take the optimal operating judgments.

Not suited to product line comparison– Variable costing, instead of absorption

costing, would've been significantly more effective and beneficial in situations when

an organisation desires to synchronize the unique revenue of a commodity. This is

because it is easier to determine the cost difference between one item and another by

properly observing the variable costs of each commodity.

Part 3

Question 4:

Answer to (a)

Estimations of Budgets and Variances:

Jayrod Plc

Statement of Original Budget, Flexed Budget, Actual Costs and Variances of PK65 Product Cost

Original Budget Flexed Budget Actual Cost Variance

Unit 10 000 9 000 9 000

£ £ £ £

Direct materials 600 000 540 000 579 500 39 500 A

Direct Labour 450 000 405 000 451 400 46 400 A

Variable Production 120 000 108 000 106 000 2 000 F

Overhead 200 000 200 000 202 000 2 000 A

Fixed Production Overhead

Total Cost 1,370 000 1,253 000 1,338 900 85 900 A

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

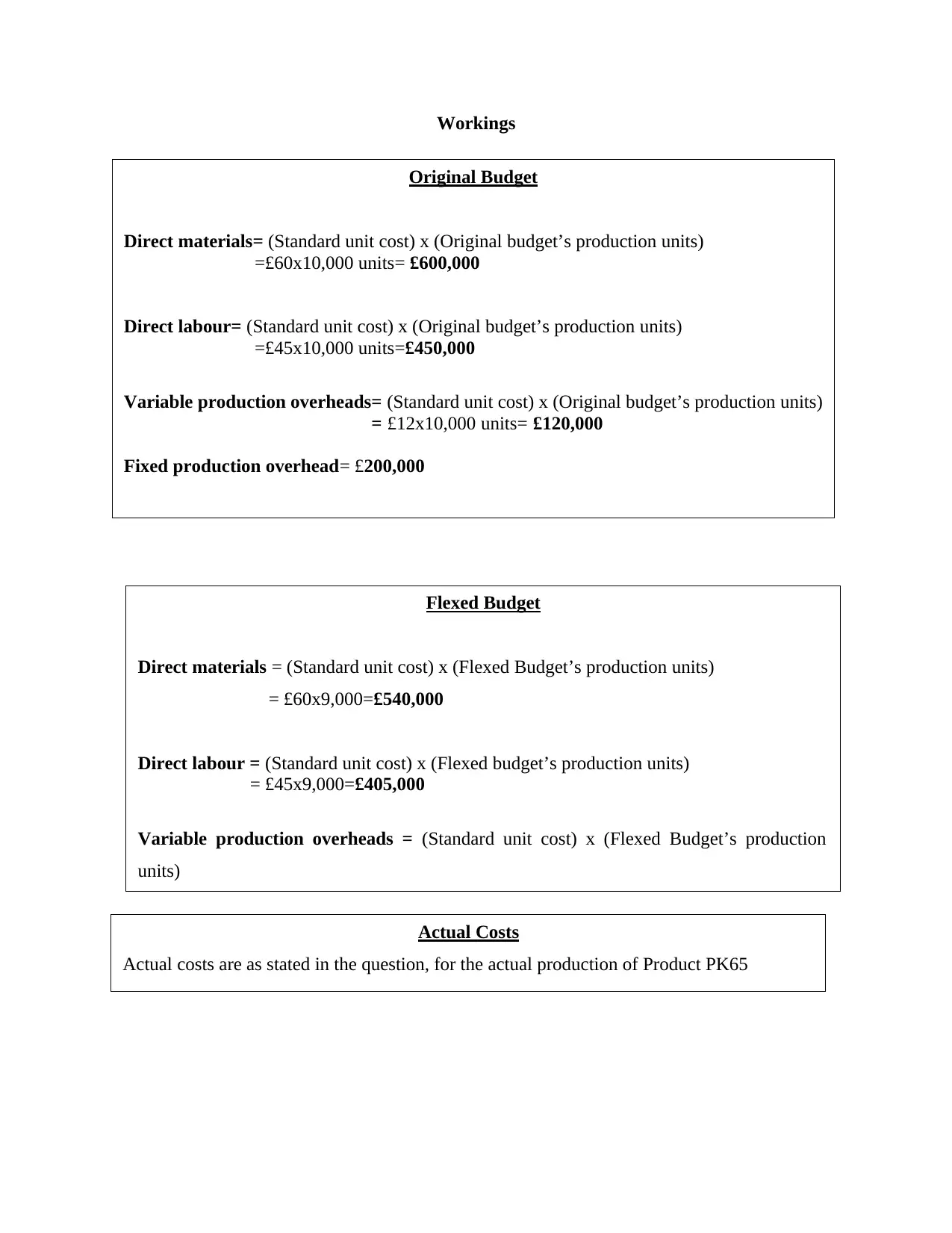

Original Budget

Direct materials= (Standard unit cost) x (Original budget’s production units)

=£60x10,000 units= £600,000

Direct labour= (Standard unit cost) x (Original budget’s production units)

=£45x10,000 units=£450,000

Variable production overheads= (Standard unit cost) x (Original budget’s production units)

= £12x10,000 units= £120,000

Fixed production overhead= £200,000

Actual Costs

Actual costs are as stated in the question, for the actual production of Product PK65

Workings

Flexed Budget

Direct materials = (Standard unit cost) x (Flexed Budget’s production units)

= £60x9,000=£540,000

Direct labour = (Standard unit cost) x (Flexed budget’s production units)

= £45x9,000=£405,000

Variable production overheads = (Standard unit cost) x (Flexed Budget’s production

units)

Direct materials= (Standard unit cost) x (Original budget’s production units)

=£60x10,000 units= £600,000

Direct labour= (Standard unit cost) x (Original budget’s production units)

=£45x10,000 units=£450,000

Variable production overheads= (Standard unit cost) x (Original budget’s production units)

= £12x10,000 units= £120,000

Fixed production overhead= £200,000

Actual Costs

Actual costs are as stated in the question, for the actual production of Product PK65

Workings

Flexed Budget

Direct materials = (Standard unit cost) x (Flexed Budget’s production units)

= £60x9,000=£540,000

Direct labour = (Standard unit cost) x (Flexed budget’s production units)

= £45x9,000=£405,000

Variable production overheads = (Standard unit cost) x (Flexed Budget’s production

units)

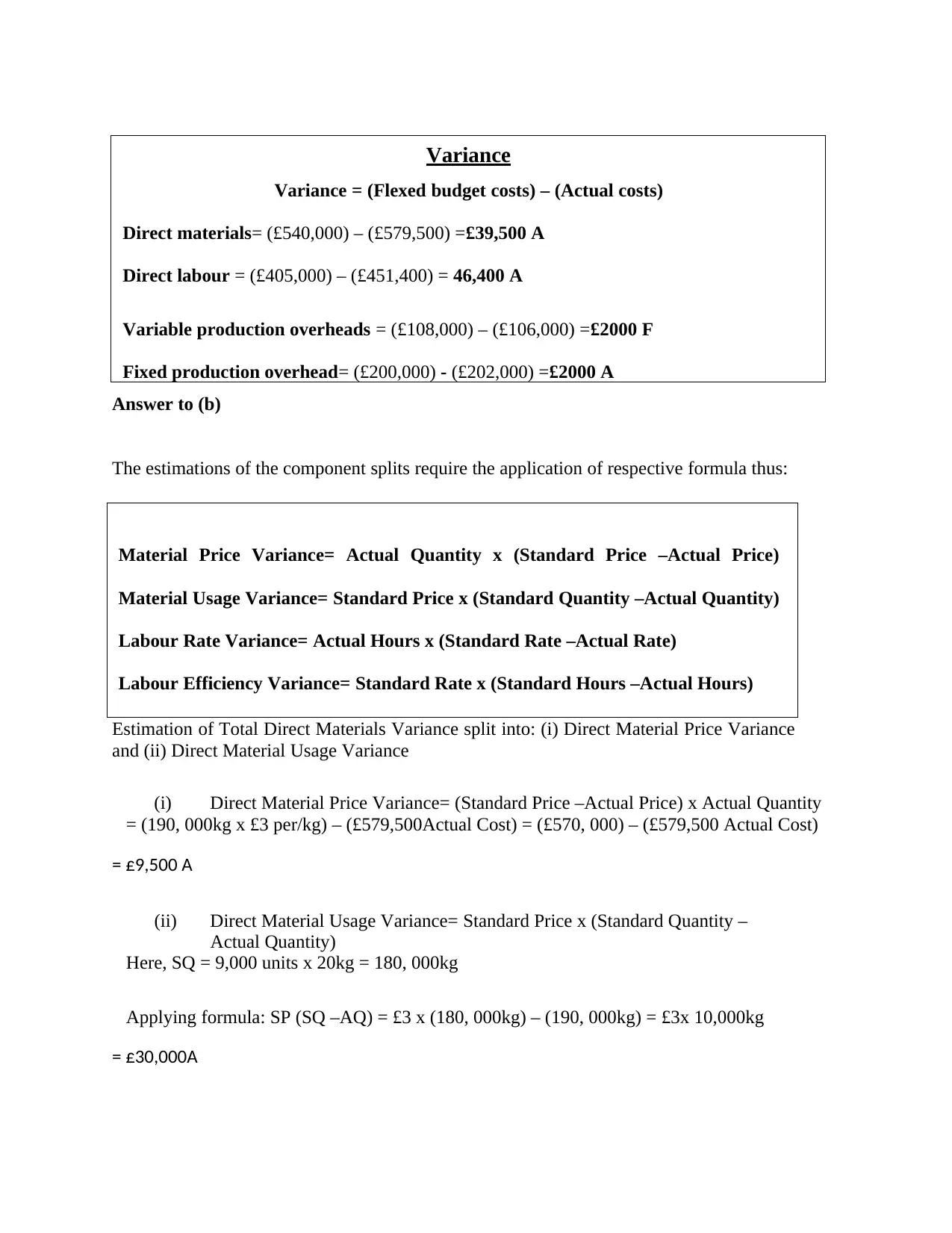

Variance

Variance = (Flexed budget costs) – (Actual costs)

Direct materials= (£540,000) – (£579,500) =£39,500 A

Direct labour = (£405,000) – (£451,400) = 46,400 A

Variable production overheads = (£108,000) – (£106,000) =£2000 F

Fixed production overhead= (£200,000) - (£202,000) =£2000 A

Material Price Variance= Actual Quantity x (Standard Price –Actual Price)

Material Usage Variance= Standard Price x (Standard Quantity –Actual Quantity)

Labour Rate Variance= Actual Hours x (Standard Rate –Actual Rate)

Labour Efficiency Variance= Standard Rate x (Standard Hours –Actual Hours)

Answer to (b)

The estimations of the component splits require the application of respective formula thus:

Estimation of Total Direct Materials Variance split into: (i) Direct Material Price Variance

and (ii) Direct Material Usage Variance

(i) Direct Material Price Variance= (Standard Price –Actual Price) x Actual Quantity

= (190, 000kg x £3 per/kg) – (£579,500Actual Cost) = (£570, 000) – (£579,500 Actual Cost)

= £9,500 A

(ii) Direct Material Usage Variance= Standard Price x (Standard Quantity –

Actual Quantity)

Here, SQ = 9,000 units x 20kg = 180, 000kg

Applying formula: SP (SQ –AQ) = £3 x (180, 000kg) – (190, 000kg) = £3x 10,000kg

= £30,000A

Variance = (Flexed budget costs) – (Actual costs)

Direct materials= (£540,000) – (£579,500) =£39,500 A

Direct labour = (£405,000) – (£451,400) = 46,400 A

Variable production overheads = (£108,000) – (£106,000) =£2000 F

Fixed production overhead= (£200,000) - (£202,000) =£2000 A

Material Price Variance= Actual Quantity x (Standard Price –Actual Price)

Material Usage Variance= Standard Price x (Standard Quantity –Actual Quantity)

Labour Rate Variance= Actual Hours x (Standard Rate –Actual Rate)

Labour Efficiency Variance= Standard Rate x (Standard Hours –Actual Hours)

Answer to (b)

The estimations of the component splits require the application of respective formula thus:

Estimation of Total Direct Materials Variance split into: (i) Direct Material Price Variance

and (ii) Direct Material Usage Variance

(i) Direct Material Price Variance= (Standard Price –Actual Price) x Actual Quantity

= (190, 000kg x £3 per/kg) – (£579,500Actual Cost) = (£570, 000) – (£579,500 Actual Cost)

= £9,500 A

(ii) Direct Material Usage Variance= Standard Price x (Standard Quantity –

Actual Quantity)

Here, SQ = 9,000 units x 20kg = 180, 000kg

Applying formula: SP (SQ –AQ) = £3 x (180, 000kg) – (190, 000kg) = £3x 10,000kg

= £30,000A

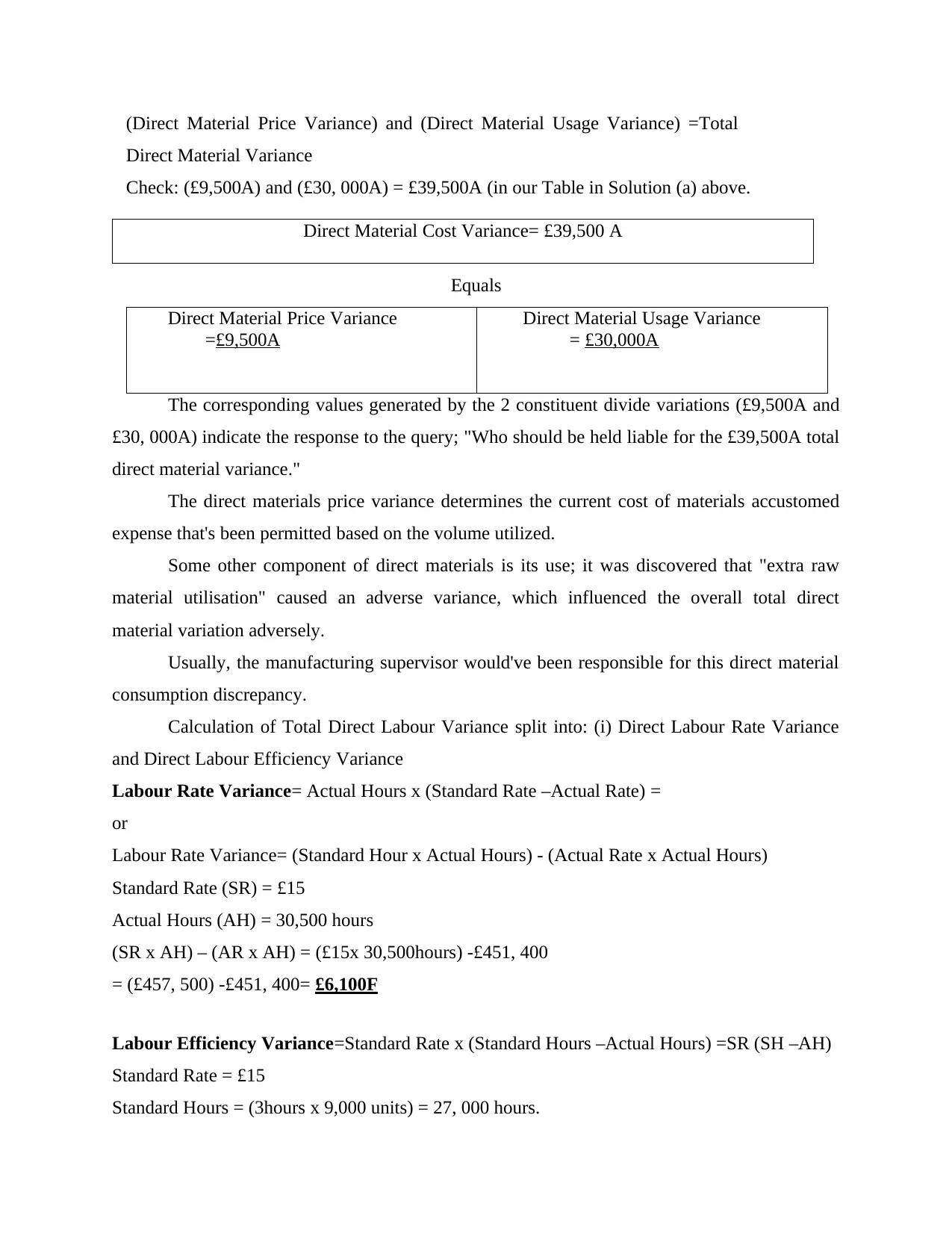

Direct Material Cost Variance= £39,500 A

(Direct Material Price Variance) and (Direct Material Usage Variance) =Total

Direct Material Variance

Check: (£9,500A) and (£30, 000A) = £39,500A (in our Table in Solution (a) above.

Equals

Direct Material Price Variance

=£9,500A

Direct Material Usage Variance

= £30,000A

The corresponding values generated by the 2 constituent divide variations (£9,500A and

£30, 000A) indicate the response to the query; "Who should be held liable for the £39,500A total

direct material variance."

The direct materials price variance determines the current cost of materials accustomed

expense that's been permitted based on the volume utilized.

Some other component of direct materials is its use; it was discovered that "extra raw

material utilisation" caused an adverse variance, which influenced the overall total direct

material variation adversely.

Usually, the manufacturing supervisor would've been responsible for this direct material

consumption discrepancy.

Calculation of Total Direct Labour Variance split into: (i) Direct Labour Rate Variance

and Direct Labour Efficiency Variance

Labour Rate Variance= Actual Hours x (Standard Rate –Actual Rate) =

or

Labour Rate Variance= (Standard Hour x Actual Hours) - (Actual Rate x Actual Hours)

Standard Rate (SR) = £15

Actual Hours (AH) = 30,500 hours

(SR x AH) – (AR x AH) = (£15x 30,500hours) -£451, 400

= (£457, 500) -£451, 400= £6,100F

Labour Efficiency Variance=Standard Rate x (Standard Hours –Actual Hours) =SR (SH –AH)

Standard Rate = £15

Standard Hours = (3hours x 9,000 units) = 27, 000 hours.

(Direct Material Price Variance) and (Direct Material Usage Variance) =Total

Direct Material Variance

Check: (£9,500A) and (£30, 000A) = £39,500A (in our Table in Solution (a) above.

Equals

Direct Material Price Variance

=£9,500A

Direct Material Usage Variance

= £30,000A

The corresponding values generated by the 2 constituent divide variations (£9,500A and

£30, 000A) indicate the response to the query; "Who should be held liable for the £39,500A total

direct material variance."

The direct materials price variance determines the current cost of materials accustomed

expense that's been permitted based on the volume utilized.

Some other component of direct materials is its use; it was discovered that "extra raw

material utilisation" caused an adverse variance, which influenced the overall total direct

material variation adversely.

Usually, the manufacturing supervisor would've been responsible for this direct material

consumption discrepancy.

Calculation of Total Direct Labour Variance split into: (i) Direct Labour Rate Variance

and Direct Labour Efficiency Variance

Labour Rate Variance= Actual Hours x (Standard Rate –Actual Rate) =

or

Labour Rate Variance= (Standard Hour x Actual Hours) - (Actual Rate x Actual Hours)

Standard Rate (SR) = £15

Actual Hours (AH) = 30,500 hours

(SR x AH) – (AR x AH) = (£15x 30,500hours) -£451, 400

= (£457, 500) -£451, 400= £6,100F

Labour Efficiency Variance=Standard Rate x (Standard Hours –Actual Hours) =SR (SH –AH)

Standard Rate = £15

Standard Hours = (3hours x 9,000 units) = 27, 000 hours.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

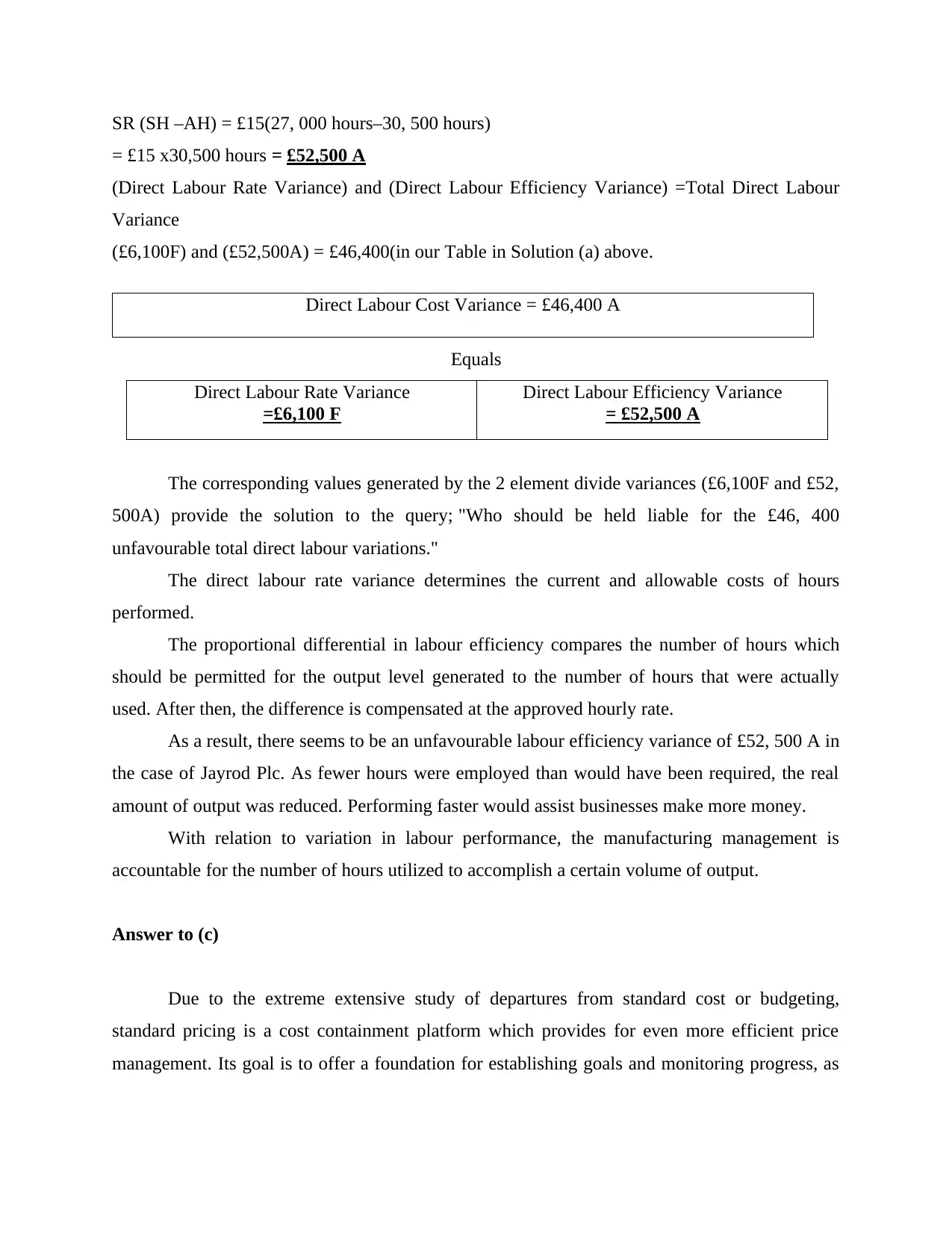

Direct Labour Cost Variance = £46,400 A

SR (SH –AH) = £15(27, 000 hours–30, 500 hours)

= £15 x30,500 hours = £52,500 A

(Direct Labour Rate Variance) and (Direct Labour Efficiency Variance) =Total Direct Labour

Variance

(£6,100F) and (£52,500A) = £46,400(in our Table in Solution (a) above.

Equals

Direct Labour Rate Variance

=£6,100 F

Direct Labour Efficiency Variance

= £52,500 A

The corresponding values generated by the 2 element divide variances (£6,100F and £52,

500A) provide the solution to the query; "Who should be held liable for the £46, 400

unfavourable total direct labour variations."

The direct labour rate variance determines the current and allowable costs of hours

performed.

The proportional differential in labour efficiency compares the number of hours which

should be permitted for the output level generated to the number of hours that were actually

used. After then, the difference is compensated at the approved hourly rate.

As a result, there seems to be an unfavourable labour efficiency variance of £52, 500 A in

the case of Jayrod Plc. As fewer hours were employed than would have been required, the real

amount of output was reduced. Performing faster would assist businesses make more money.

With relation to variation in labour performance, the manufacturing management is

accountable for the number of hours utilized to accomplish a certain volume of output.

Answer to (c)

Due to the extreme extensive study of departures from standard cost or budgeting,

standard pricing is a cost containment platform which provides for even more efficient price

management. Its goal is to offer a foundation for establishing goals and monitoring progress, as

SR (SH –AH) = £15(27, 000 hours–30, 500 hours)

= £15 x30,500 hours = £52,500 A

(Direct Labour Rate Variance) and (Direct Labour Efficiency Variance) =Total Direct Labour

Variance

(£6,100F) and (£52,500A) = £46,400(in our Table in Solution (a) above.

Equals

Direct Labour Rate Variance

=£6,100 F

Direct Labour Efficiency Variance

= £52,500 A

The corresponding values generated by the 2 element divide variances (£6,100F and £52,

500A) provide the solution to the query; "Who should be held liable for the £46, 400

unfavourable total direct labour variations."

The direct labour rate variance determines the current and allowable costs of hours

performed.

The proportional differential in labour efficiency compares the number of hours which

should be permitted for the output level generated to the number of hours that were actually

used. After then, the difference is compensated at the approved hourly rate.

As a result, there seems to be an unfavourable labour efficiency variance of £52, 500 A in

the case of Jayrod Plc. As fewer hours were employed than would have been required, the real

amount of output was reduced. Performing faster would assist businesses make more money.

With relation to variation in labour performance, the manufacturing management is

accountable for the number of hours utilized to accomplish a certain volume of output.

Answer to (c)

Due to the extreme extensive study of departures from standard cost or budgeting,

standard pricing is a cost containment platform which provides for even more efficient price

management. Its goal is to offer a foundation for establishing goals and monitoring progress, as

well as helpful data for management decision-making and a method for determining the sale

value of things.

The standard cost allows:

Control: This could be contrasted to real expenses and any discrepancies looked into.

Performance measurement: Any disparities among the benchmark and real expense

could be utilised to evaluate expense unit executives' effectiveness.

Variances: Standard expenses are used to prepare financial reports, but they're also

necessary for computing and evaluating deviations, which give administration 'input' on

how well the business has been doing (Abdel-Maksoud, Cheffi and Ghoudi, 2016).

To value inventories: Standard cost is an option to LIFO and FIFO methodologies for

valuing stocks.

Accounting simplification: The standard seems to be the only expense.

The significance of variance analysis and the need for it: Administration aims to have

lesser variations from projected expenditures, that results to precise and forward-looking policy

making, and that is why assessment of variance promotes efficient budgeted operations.

The assessment of variation is a control method. The analysis of variations on major goods

permits the company to identify the reasons and seek for possible solutions to avoid variations.

It allows for the assignment of responsibilities and, when suitable, incorporates agency

organisational framework. For example, if labour productivity variation is deemed negative, or

if raw material expense variation acquisition is deemed detrimental, administration would tighten

supervision over such divisions in order to boost productivity.

Limitations of variance analysis- Companies benefit greatly from variance

assessment; although it does have constraints:

Marking the termination of quarterly, fiscal information and outcomes are used to do

variance evaluation. There could be a laxity in collecting this data that could affect the

essential corrective steps. Furthermore, not all causes of variation would've been

available for data collection that could cause problems with actionable variation analysis

(Chung and Chen, 2016).

If the planning process is not finished, the budgetary activity must be performed

haphazardly, taking into consideration the detailed investigation of each aspect, which

value of things.

The standard cost allows:

Control: This could be contrasted to real expenses and any discrepancies looked into.

Performance measurement: Any disparities among the benchmark and real expense

could be utilised to evaluate expense unit executives' effectiveness.

Variances: Standard expenses are used to prepare financial reports, but they're also

necessary for computing and evaluating deviations, which give administration 'input' on

how well the business has been doing (Abdel-Maksoud, Cheffi and Ghoudi, 2016).

To value inventories: Standard cost is an option to LIFO and FIFO methodologies for

valuing stocks.

Accounting simplification: The standard seems to be the only expense.

The significance of variance analysis and the need for it: Administration aims to have

lesser variations from projected expenditures, that results to precise and forward-looking policy

making, and that is why assessment of variance promotes efficient budgeted operations.

The assessment of variation is a control method. The analysis of variations on major goods

permits the company to identify the reasons and seek for possible solutions to avoid variations.

It allows for the assignment of responsibilities and, when suitable, incorporates agency

organisational framework. For example, if labour productivity variation is deemed negative, or

if raw material expense variation acquisition is deemed detrimental, administration would tighten

supervision over such divisions in order to boost productivity.

Limitations of variance analysis- Companies benefit greatly from variance

assessment; although it does have constraints:

Marking the termination of quarterly, fiscal information and outcomes are used to do

variance evaluation. There could be a laxity in collecting this data that could affect the

essential corrective steps. Furthermore, not all causes of variation would've been

available for data collection that could cause problems with actionable variation analysis

(Chung and Chen, 2016).

If the planning process is not finished, the budgetary activity must be performed

haphazardly, taking into consideration the detailed investigation of each aspect, which

would be likely to diverge from the real data, perhaps leading to ineffective variance

assessment.

assessment.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals

Cokins, G. and Căpușneanu, S., 2020. Management accounting: The sustainable strategy map

and its associated sustainability balanced scorecard. In Management accounting

standards for sustainable business practices (pp. 1-26). IGI Global.

Gunarathne, A.N. and Lee, K.H., 2018. Environmental Management Maturity Stages and

Environmental Management Accounting.

Bento, R.F., Mertins, L. and White, L.F., 2018. Risk management and internal control: A study

of management accounting practice. In Advances in Management Accounting. Emerald

Publishing Limited.

Chaudhry, N.I., Asad, H. and Hussain, R.I., 2020. Environmental innovation and financial

performance: Mediating role of environmental management accounting and firm's

environmental strategy. Pakistan Journal of Commerce and Social Sciences

(PJCSS), 14(3), pp.715-737.

Abdel-Maksoud, A., Cheffi, W. and Ghoudi, K., 2016. The mediating effect of shop-floor

involvement on relations between advanced management accounting practices and

operational non-financial performance indicators. the british accounting review, 48(2),

pp.169-184.

Chung, S.H. and Chen, K.C., 2016, July. The relationships among personality, management

accounting information systems, and customer relationship quality. In 2016 5th IIAI

International Congress on Advanced Applied Informatics (IIAI-AAI) (pp. 759-763).

IEEE.

Books and journals

Cokins, G. and Căpușneanu, S., 2020. Management accounting: The sustainable strategy map

and its associated sustainability balanced scorecard. In Management accounting

standards for sustainable business practices (pp. 1-26). IGI Global.

Gunarathne, A.N. and Lee, K.H., 2018. Environmental Management Maturity Stages and

Environmental Management Accounting.

Bento, R.F., Mertins, L. and White, L.F., 2018. Risk management and internal control: A study

of management accounting practice. In Advances in Management Accounting. Emerald

Publishing Limited.

Chaudhry, N.I., Asad, H. and Hussain, R.I., 2020. Environmental innovation and financial

performance: Mediating role of environmental management accounting and firm's

environmental strategy. Pakistan Journal of Commerce and Social Sciences

(PJCSS), 14(3), pp.715-737.

Abdel-Maksoud, A., Cheffi, W. and Ghoudi, K., 2016. The mediating effect of shop-floor

involvement on relations between advanced management accounting practices and

operational non-financial performance indicators. the british accounting review, 48(2),

pp.169-184.

Chung, S.H. and Chen, K.C., 2016, July. The relationships among personality, management

accounting information systems, and customer relationship quality. In 2016 5th IIAI

International Congress on Advanced Applied Informatics (IIAI-AAI) (pp. 759-763).

IEEE.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.