Accounting and Finance Assignment: Gravepals, Cornpeace, Dane Jones

VerifiedAdded on 2021/01/02

|15

|3802

|248

Homework Assignment

AI Summary

This document presents a comprehensive solution to a finance assignment, addressing various aspects of accounting and financial management. Part A focuses on Gravepals Plc, providing an income statement and statement of financial position for 2017. Part B analyzes Cornpeace Ltd, including contribution per unit, break-even point (BEP) and margin of safety (MOS) calculations, profit estimations, and the effectiveness of marketing strategies. It also explores the assumptions of the break-even model. Part C delves into Dane Jones Ltd, calculating the payback period (PBP), accounting rate of return (ARR), and net present value (NPV). It includes a report analyzing the merits and limitations of investment appraisal techniques, along with an examination of the benefits and limitations of budgets as a strategic planning tool. The assignment covers financial statement preparation, cost-volume-profit analysis, investment appraisal, and budgeting, offering a complete overview of key finance concepts.

UGB 163 –

Introduction to Accounting and

Finance

Introduction to Accounting and

Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Part A – Gravepals Plc....................................................................................................................2

1.Preparation of the Income Statement for the year ended 2017 for Gravepals Plc....................3

2.Preparation of the Statement of Financial Position as at 31 December 2017 for Gravepals

Plc................................................................................................................................................4

Part B – Cornpeace Ltd....................................................................................................................5

a) Estimation of contribution per unit..........................................................................................5

b) calculation of BEP and MOS..................................................................................................5

c) Calculation of profit for the firm if it produces and sells 48,000 units..................................6

d) Effectiveness of Increase in marketing and advertising costs and raising of unit price by

9% and volume by 17%...............................................................................................................6

e) Identification and explanation of assumptions of Break-even model including analysing

whether the model can successfully be utilised by a range of differing businesses....................7

Part C – Dane Jones Ltd..................................................................................................................8

a) Calculation of the PBP, ARR and NPV..................................................................................8

b) Produce a report that explains and analyses the key merits and limitations of the differing

investment appraisal techniques................................................................................................10

c) identification and explanation of the key benefits and limitations of budgets as a strategic

planning tool..............................................................................................................................12

Budget as a tool of strategic Planning...................................................................................12

Key benefits of Budget as a tool for Strategic planning........................................................12

Limitations of Budget as a tool for strategic planning..........................................................13

Part A – Gravepals Plc....................................................................................................................2

1.Preparation of the Income Statement for the year ended 2017 for Gravepals Plc....................3

2.Preparation of the Statement of Financial Position as at 31 December 2017 for Gravepals

Plc................................................................................................................................................4

Part B – Cornpeace Ltd....................................................................................................................5

a) Estimation of contribution per unit..........................................................................................5

b) calculation of BEP and MOS..................................................................................................5

c) Calculation of profit for the firm if it produces and sells 48,000 units..................................6

d) Effectiveness of Increase in marketing and advertising costs and raising of unit price by

9% and volume by 17%...............................................................................................................6

e) Identification and explanation of assumptions of Break-even model including analysing

whether the model can successfully be utilised by a range of differing businesses....................7

Part C – Dane Jones Ltd..................................................................................................................8

a) Calculation of the PBP, ARR and NPV..................................................................................8

b) Produce a report that explains and analyses the key merits and limitations of the differing

investment appraisal techniques................................................................................................10

c) identification and explanation of the key benefits and limitations of budgets as a strategic

planning tool..............................................................................................................................12

Budget as a tool of strategic Planning...................................................................................12

Key benefits of Budget as a tool for Strategic planning........................................................12

Limitations of Budget as a tool for strategic planning..........................................................13

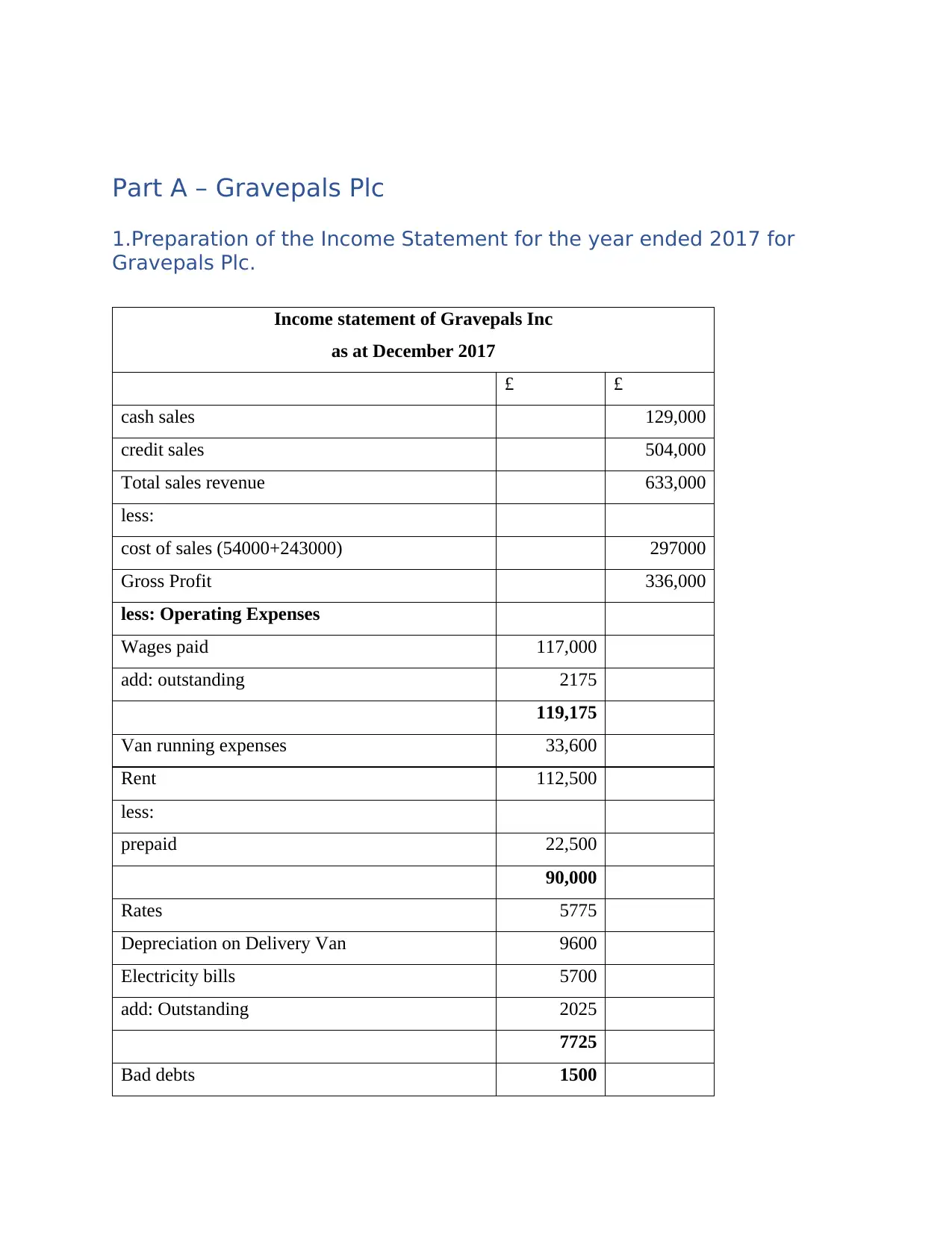

Part A – Gravepals Plc

1.Preparation of the Income Statement for the year ended 2017 for

Gravepals Plc.

Income statement of Gravepals Inc

as at December 2017

£ £

cash sales 129,000

credit sales 504,000

Total sales revenue 633,000

less:

cost of sales (54000+243000) 297000

Gross Profit 336,000

less: Operating Expenses

Wages paid 117,000

add: outstanding 2175

119,175

Van running expenses 33,600

Rent 112,500

less:

prepaid 22,500

90,000

Rates 5775

Depreciation on Delivery Van 9600

Electricity bills 5700

add: Outstanding 2025

7725

Bad debts 1500

1.Preparation of the Income Statement for the year ended 2017 for

Gravepals Plc.

Income statement of Gravepals Inc

as at December 2017

£ £

cash sales 129,000

credit sales 504,000

Total sales revenue 633,000

less:

cost of sales (54000+243000) 297000

Gross Profit 336,000

less: Operating Expenses

Wages paid 117,000

add: outstanding 2175

119,175

Van running expenses 33,600

Rent 112,500

less:

prepaid 22,500

90,000

Rates 5775

Depreciation on Delivery Van 9600

Electricity bills 5700

add: Outstanding 2025

7725

Bad debts 1500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total Expenses 267,375

Net income 68,625

2.Preparation of the Statement of Financial Position as at 31 December

2017 for Gravepals Plc.

Statement of financial position of Gravepal’s Inc

as at December 2017

£ £

Current Assets:

cash 0

Accounts Receivables 64,500

Inventory 228,000

Prepaid Rent 22,500

prepaid Rates 1,125

Total current Assets 317,625

Non-current Assets:

Delivery Van 60,000

less: depreciation -9,600 50,400

Total assets 366,525

Current Liability:

bank overdraft 20,700

Accrued wages 2,175

Outstanding Electricity bills 2,025

Accounts payable 93,000

Total CL 117,900

Common stock 180,000

add: Net income 68,625

Net income 68,625

2.Preparation of the Statement of Financial Position as at 31 December

2017 for Gravepals Plc.

Statement of financial position of Gravepal’s Inc

as at December 2017

£ £

Current Assets:

cash 0

Accounts Receivables 64,500

Inventory 228,000

Prepaid Rent 22,500

prepaid Rates 1,125

Total current Assets 317,625

Non-current Assets:

Delivery Van 60,000

less: depreciation -9,600 50,400

Total assets 366,525

Current Liability:

bank overdraft 20,700

Accrued wages 2,175

Outstanding Electricity bills 2,025

Accounts payable 93,000

Total CL 117,900

Common stock 180,000

add: Net income 68,625

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

less: Dividends paid 0

shareholders’ funds 248,625

Shareholders’ funds and total Liability 366,525

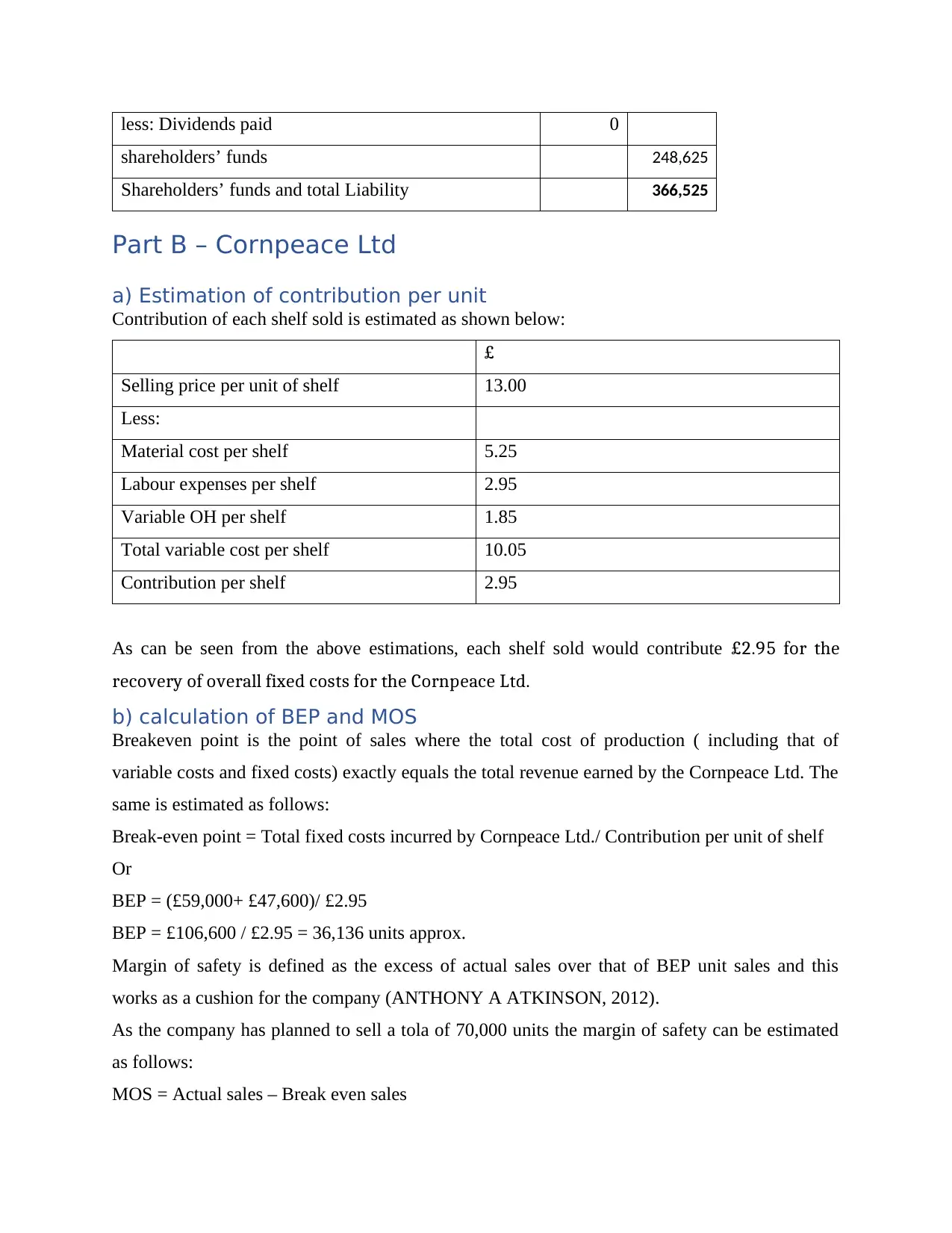

Part B – Cornpeace Ltd

a) Estimation of contribution per unit

Contribution of each shelf sold is estimated as shown below:

£

Selling price per unit of shelf 13.00

Less:

Material cost per shelf 5.25

Labour expenses per shelf 2.95

Variable OH per shelf 1.85

Total variable cost per shelf 10.05

Contribution per shelf 2.95

As can be seen from the above estimations, each shelf sold would contribute £2.95 for the

recovery of overall fixed costs for the Cornpeace Ltd.

b) calculation of BEP and MOS

Breakeven point is the point of sales where the total cost of production ( including that of

variable costs and fixed costs) exactly equals the total revenue earned by the Cornpeace Ltd. The

same is estimated as follows:

Break-even point = Total fixed costs incurred by Cornpeace Ltd./ Contribution per unit of shelf

Or

BEP = (£59,000+ £47,600)/ £2.95

BEP = £106,600 / £2.95 = 36,136 units approx.

Margin of safety is defined as the excess of actual sales over that of BEP unit sales and this

works as a cushion for the company (ANTHONY A ATKINSON, 2012).

As the company has planned to sell a tola of 70,000 units the margin of safety can be estimated

as follows:

MOS = Actual sales – Break even sales

shareholders’ funds 248,625

Shareholders’ funds and total Liability 366,525

Part B – Cornpeace Ltd

a) Estimation of contribution per unit

Contribution of each shelf sold is estimated as shown below:

£

Selling price per unit of shelf 13.00

Less:

Material cost per shelf 5.25

Labour expenses per shelf 2.95

Variable OH per shelf 1.85

Total variable cost per shelf 10.05

Contribution per shelf 2.95

As can be seen from the above estimations, each shelf sold would contribute £2.95 for the

recovery of overall fixed costs for the Cornpeace Ltd.

b) calculation of BEP and MOS

Breakeven point is the point of sales where the total cost of production ( including that of

variable costs and fixed costs) exactly equals the total revenue earned by the Cornpeace Ltd. The

same is estimated as follows:

Break-even point = Total fixed costs incurred by Cornpeace Ltd./ Contribution per unit of shelf

Or

BEP = (£59,000+ £47,600)/ £2.95

BEP = £106,600 / £2.95 = 36,136 units approx.

Margin of safety is defined as the excess of actual sales over that of BEP unit sales and this

works as a cushion for the company (ANTHONY A ATKINSON, 2012).

As the company has planned to sell a tola of 70,000 units the margin of safety can be estimated

as follows:

MOS = Actual sales – Break even sales

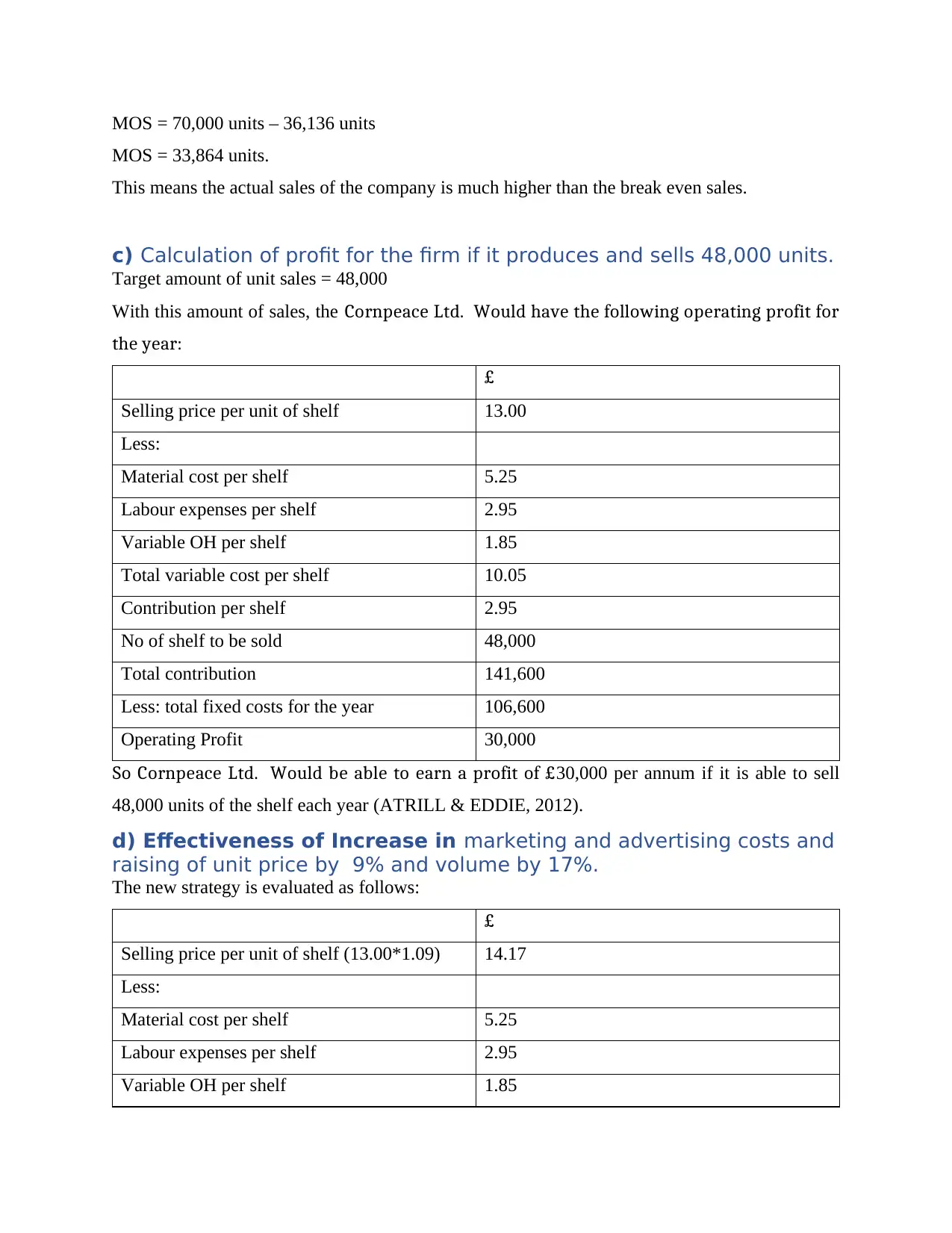

MOS = 70,000 units – 36,136 units

MOS = 33,864 units.

This means the actual sales of the company is much higher than the break even sales.

c) Calculation of profit for the firm if it produces and sells 48,000 units.

Target amount of unit sales = 48,000

With this amount of sales, the Cornpeace Ltd. Would have the following operating profit for

the year:

£

Selling price per unit of shelf 13.00

Less:

Material cost per shelf 5.25

Labour expenses per shelf 2.95

Variable OH per shelf 1.85

Total variable cost per shelf 10.05

Contribution per shelf 2.95

No of shelf to be sold 48,000

Total contribution 141,600

Less: total fixed costs for the year 106,600

Operating Profit 30,000

So Cornpeace Ltd. Would be able to earn a profit of £30,000 per annum if it is able to sell

48,000 units of the shelf each year (ATRILL & EDDIE, 2012).

d) Effectiveness of Increase in marketing and advertising costs and

raising of unit price by 9% and volume by 17%.

The new strategy is evaluated as follows:

£

Selling price per unit of shelf (13.00*1.09) 14.17

Less:

Material cost per shelf 5.25

Labour expenses per shelf 2.95

Variable OH per shelf 1.85

MOS = 33,864 units.

This means the actual sales of the company is much higher than the break even sales.

c) Calculation of profit for the firm if it produces and sells 48,000 units.

Target amount of unit sales = 48,000

With this amount of sales, the Cornpeace Ltd. Would have the following operating profit for

the year:

£

Selling price per unit of shelf 13.00

Less:

Material cost per shelf 5.25

Labour expenses per shelf 2.95

Variable OH per shelf 1.85

Total variable cost per shelf 10.05

Contribution per shelf 2.95

No of shelf to be sold 48,000

Total contribution 141,600

Less: total fixed costs for the year 106,600

Operating Profit 30,000

So Cornpeace Ltd. Would be able to earn a profit of £30,000 per annum if it is able to sell

48,000 units of the shelf each year (ATRILL & EDDIE, 2012).

d) Effectiveness of Increase in marketing and advertising costs and

raising of unit price by 9% and volume by 17%.

The new strategy is evaluated as follows:

£

Selling price per unit of shelf (13.00*1.09) 14.17

Less:

Material cost per shelf 5.25

Labour expenses per shelf 2.95

Variable OH per shelf 1.85

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

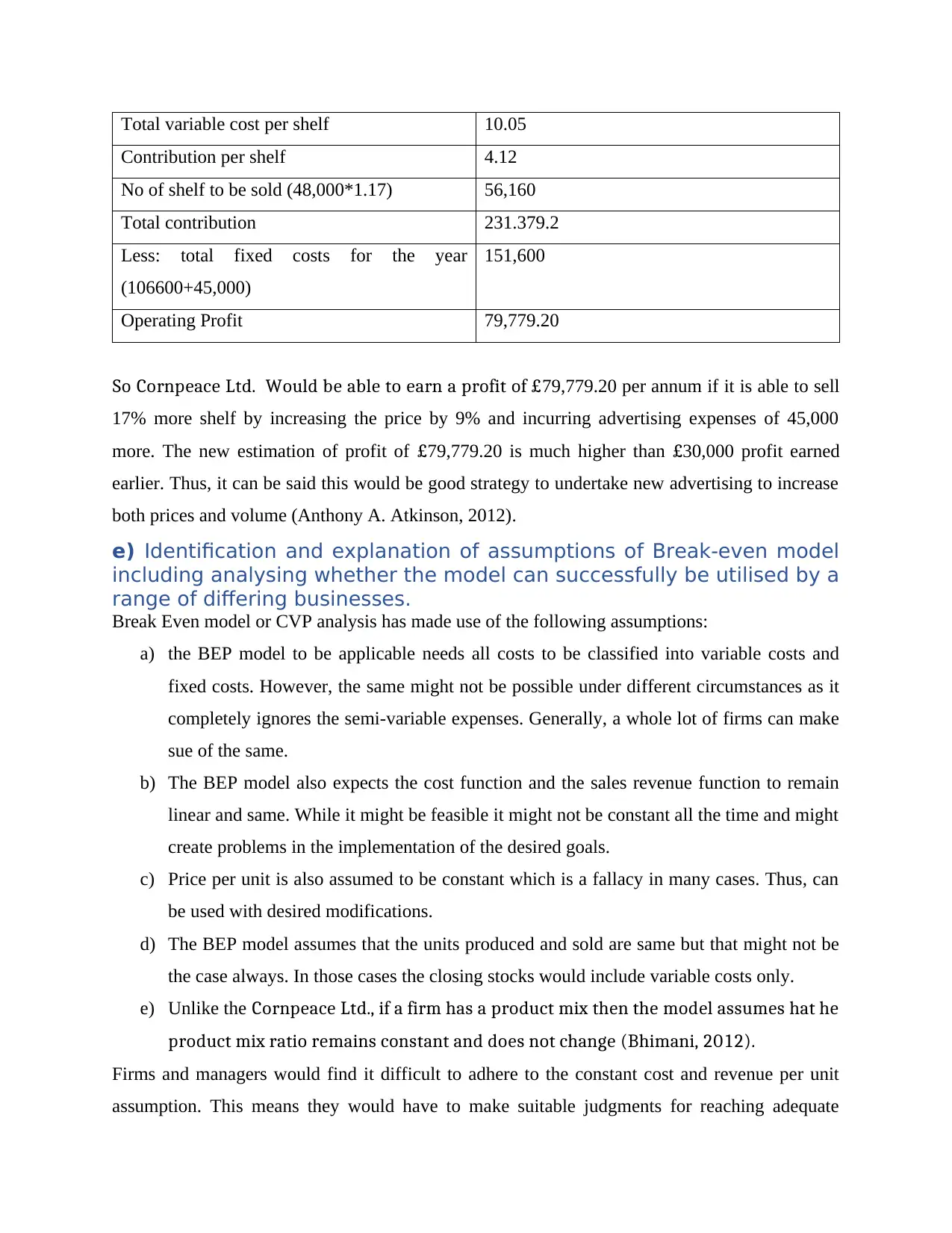

Total variable cost per shelf 10.05

Contribution per shelf 4.12

No of shelf to be sold (48,000*1.17) 56,160

Total contribution 231.379.2

Less: total fixed costs for the year

(106600+45,000)

151,600

Operating Profit 79,779.20

So Cornpeace Ltd. Would be able to earn a profit of £79,779.20 per annum if it is able to sell

17% more shelf by increasing the price by 9% and incurring advertising expenses of 45,000

more. The new estimation of profit of £79,779.20 is much higher than £30,000 profit earned

earlier. Thus, it can be said this would be good strategy to undertake new advertising to increase

both prices and volume (Anthony A. Atkinson, 2012).

e) Identification and explanation of assumptions of Break-even model

including analysing whether the model can successfully be utilised by a

range of differing businesses.

Break Even model or CVP analysis has made use of the following assumptions:

a) the BEP model to be applicable needs all costs to be classified into variable costs and

fixed costs. However, the same might not be possible under different circumstances as it

completely ignores the semi-variable expenses. Generally, a whole lot of firms can make

sue of the same.

b) The BEP model also expects the cost function and the sales revenue function to remain

linear and same. While it might be feasible it might not be constant all the time and might

create problems in the implementation of the desired goals.

c) Price per unit is also assumed to be constant which is a fallacy in many cases. Thus, can

be used with desired modifications.

d) The BEP model assumes that the units produced and sold are same but that might not be

the case always. In those cases the closing stocks would include variable costs only.

e) Unlike the Cornpeace Ltd., if a firm has a product mix then the model assumes hat he

product mix ratio remains constant and does not change (Bhimani, 2012).

Firms and managers would find it difficult to adhere to the constant cost and revenue per unit

assumption. This means they would have to make suitable judgments for reaching adequate

Contribution per shelf 4.12

No of shelf to be sold (48,000*1.17) 56,160

Total contribution 231.379.2

Less: total fixed costs for the year

(106600+45,000)

151,600

Operating Profit 79,779.20

So Cornpeace Ltd. Would be able to earn a profit of £79,779.20 per annum if it is able to sell

17% more shelf by increasing the price by 9% and incurring advertising expenses of 45,000

more. The new estimation of profit of £79,779.20 is much higher than £30,000 profit earned

earlier. Thus, it can be said this would be good strategy to undertake new advertising to increase

both prices and volume (Anthony A. Atkinson, 2012).

e) Identification and explanation of assumptions of Break-even model

including analysing whether the model can successfully be utilised by a

range of differing businesses.

Break Even model or CVP analysis has made use of the following assumptions:

a) the BEP model to be applicable needs all costs to be classified into variable costs and

fixed costs. However, the same might not be possible under different circumstances as it

completely ignores the semi-variable expenses. Generally, a whole lot of firms can make

sue of the same.

b) The BEP model also expects the cost function and the sales revenue function to remain

linear and same. While it might be feasible it might not be constant all the time and might

create problems in the implementation of the desired goals.

c) Price per unit is also assumed to be constant which is a fallacy in many cases. Thus, can

be used with desired modifications.

d) The BEP model assumes that the units produced and sold are same but that might not be

the case always. In those cases the closing stocks would include variable costs only.

e) Unlike the Cornpeace Ltd., if a firm has a product mix then the model assumes hat he

product mix ratio remains constant and does not change (Bhimani, 2012).

Firms and managers would find it difficult to adhere to the constant cost and revenue per unit

assumption. This means they would have to make suitable judgments for reaching adequate

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

results. Also, costs would not remain linear in the long run and most probably it would decline

with higher production in the long run. So managers would be needed to keep a watch on the

cost functions and make necessary changes to the model. Because the BEP model is based on a

number of restrictive assumptions the same only can act as approximation tools and not as a pure

and real tool for making long range decisions. It would only act true in the short run when cost

and revenue functions are more or less expected to remain linear (Brearly, 2012).

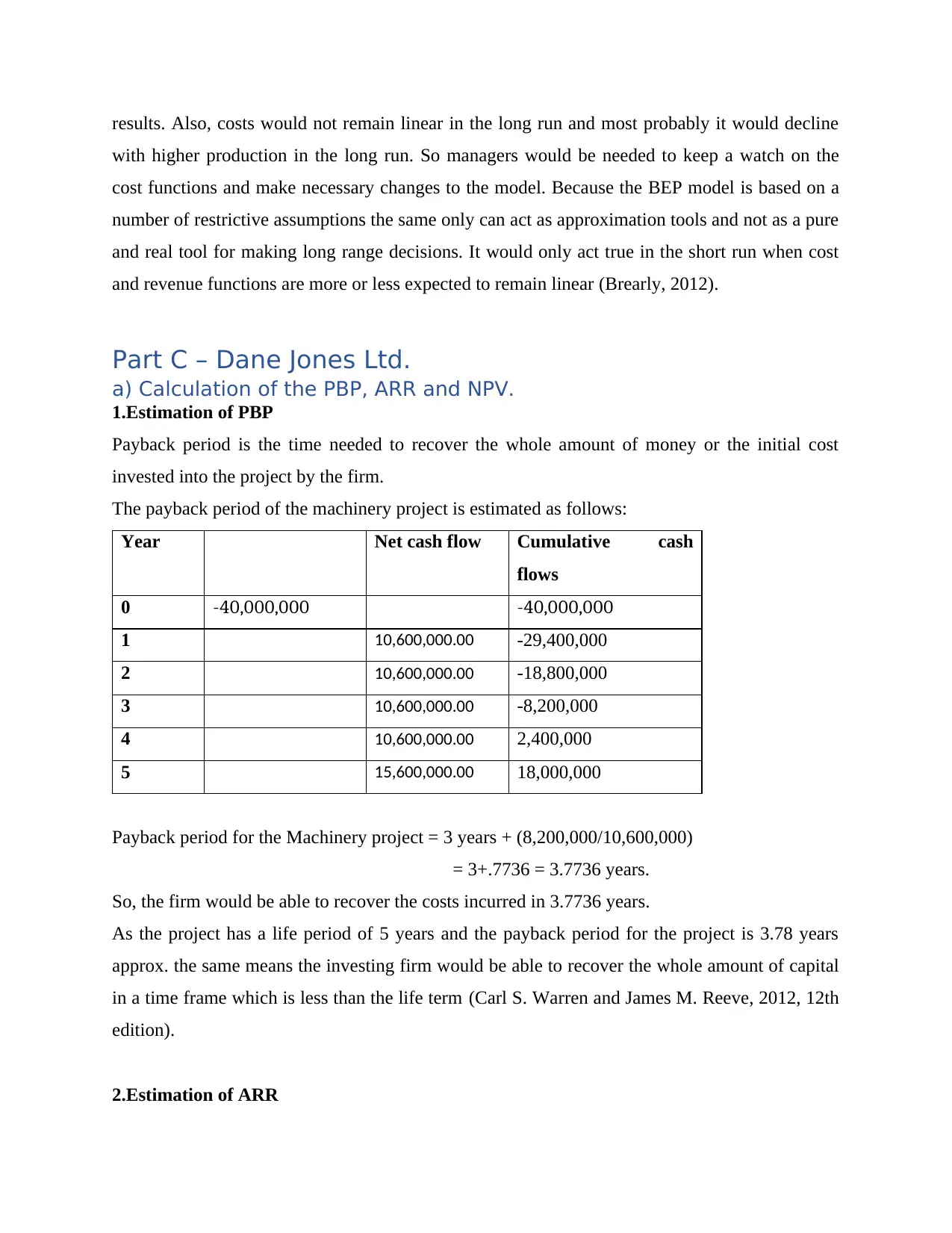

Part C – Dane Jones Ltd.

a) Calculation of the PBP, ARR and NPV.

1.Estimation of PBP

Payback period is the time needed to recover the whole amount of money or the initial cost

invested into the project by the firm.

The payback period of the machinery project is estimated as follows:

Year Net cash flow Cumulative cash

flows

0 -40,000,000 -40,000,000

1 10,600,000.00 -29,400,000

2 10,600,000.00 -18,800,000

3 10,600,000.00 -8,200,000

4 10,600,000.00 2,400,000

5 15,600,000.00 18,000,000

Payback period for the Machinery project = 3 years + (8,200,000/10,600,000)

= 3+.7736 = 3.7736 years.

So, the firm would be able to recover the costs incurred in 3.7736 years.

As the project has a life period of 5 years and the payback period for the project is 3.78 years

approx. the same means the investing firm would be able to recover the whole amount of capital

in a time frame which is less than the life term (Carl S. Warren and James M. Reeve, 2012, 12th

edition).

2.Estimation of ARR

with higher production in the long run. So managers would be needed to keep a watch on the

cost functions and make necessary changes to the model. Because the BEP model is based on a

number of restrictive assumptions the same only can act as approximation tools and not as a pure

and real tool for making long range decisions. It would only act true in the short run when cost

and revenue functions are more or less expected to remain linear (Brearly, 2012).

Part C – Dane Jones Ltd.

a) Calculation of the PBP, ARR and NPV.

1.Estimation of PBP

Payback period is the time needed to recover the whole amount of money or the initial cost

invested into the project by the firm.

The payback period of the machinery project is estimated as follows:

Year Net cash flow Cumulative cash

flows

0 -40,000,000 -40,000,000

1 10,600,000.00 -29,400,000

2 10,600,000.00 -18,800,000

3 10,600,000.00 -8,200,000

4 10,600,000.00 2,400,000

5 15,600,000.00 18,000,000

Payback period for the Machinery project = 3 years + (8,200,000/10,600,000)

= 3+.7736 = 3.7736 years.

So, the firm would be able to recover the costs incurred in 3.7736 years.

As the project has a life period of 5 years and the payback period for the project is 3.78 years

approx. the same means the investing firm would be able to recover the whole amount of capital

in a time frame which is less than the life term (Carl S. Warren and James M. Reeve, 2012, 12th

edition).

2.Estimation of ARR

ARR is estimated as :

0 1 2 3 4 5

initial

investment -40,000,000

Cash inflow

17,000,000.0

0

17,000,000.0

0

17,000,000.0

0

17,000,000.0

0 17,000,000

less:

cash outflow 6,400,000.00 6,400,000.00 6,400,000.00 6,400,000.00 6,400,000

Operating

profit 10,600,000.00 10,600,000.00 10,600,000.00 10,600,000.00 10,600,000

less:

Depreciation 7,000,000.00 7,000,000.00 7,000,000.00 7,000,000.00 7,000,000

PBT 3,600,000.00 3,600,000.00 3,600,000.00 3,600,000.00 3,600,000

Average profit is 3,600,000 as the profit of the company is the same in each of the 5 years of

operations.

ARR = Average Profit / Average Investments made

ARR = 3,600,000 / [(40,000,000+5,000,000)/2]

ARR = 3,600,000 / 22,500,000 = 16%

As the ARR is 16% for the machinery project, the same means the managers of the company

would be able to generate an ROI of 16% on the average amount of investment made in the

project (Damodaran, 2012).

3.Estimation of NPV

NPV of the project is estimated as shown in the following table:

0 1 2 3 4 5

initial

investment -40,000,000

Cash inflow

17,000,000.0

0

17,000,000.0

0

17,000,000.0

0

17,000,000.0

0 17,000,000

less:

cash outflow 6,400,000.00 6,400,000.00 6,400,000.00 6,400,000.00 6,400,000

Operating

profit 10,600,000.00 10,600,000.00 10,600,000.00 10,600,000.00 10,600,000

less:

Depreciation 7,000,000.00 7,000,000.00 7,000,000.00 7,000,000.00 7,000,000

PBT 3,600,000.00 3,600,000.00 3,600,000.00 3,600,000.00 3,600,000

tax 0.00 0.00 0.00 0.00 0.00

Add:

Depreciation 7,000,000.00 7,000,000.00 7,000,000.00 7,000,000.00 7,000,000

0 1 2 3 4 5

initial

investment -40,000,000

Cash inflow

17,000,000.0

0

17,000,000.0

0

17,000,000.0

0

17,000,000.0

0 17,000,000

less:

cash outflow 6,400,000.00 6,400,000.00 6,400,000.00 6,400,000.00 6,400,000

Operating

profit 10,600,000.00 10,600,000.00 10,600,000.00 10,600,000.00 10,600,000

less:

Depreciation 7,000,000.00 7,000,000.00 7,000,000.00 7,000,000.00 7,000,000

PBT 3,600,000.00 3,600,000.00 3,600,000.00 3,600,000.00 3,600,000

Average profit is 3,600,000 as the profit of the company is the same in each of the 5 years of

operations.

ARR = Average Profit / Average Investments made

ARR = 3,600,000 / [(40,000,000+5,000,000)/2]

ARR = 3,600,000 / 22,500,000 = 16%

As the ARR is 16% for the machinery project, the same means the managers of the company

would be able to generate an ROI of 16% on the average amount of investment made in the

project (Damodaran, 2012).

3.Estimation of NPV

NPV of the project is estimated as shown in the following table:

0 1 2 3 4 5

initial

investment -40,000,000

Cash inflow

17,000,000.0

0

17,000,000.0

0

17,000,000.0

0

17,000,000.0

0 17,000,000

less:

cash outflow 6,400,000.00 6,400,000.00 6,400,000.00 6,400,000.00 6,400,000

Operating

profit 10,600,000.00 10,600,000.00 10,600,000.00 10,600,000.00 10,600,000

less:

Depreciation 7,000,000.00 7,000,000.00 7,000,000.00 7,000,000.00 7,000,000

PBT 3,600,000.00 3,600,000.00 3,600,000.00 3,600,000.00 3,600,000

tax 0.00 0.00 0.00 0.00 0.00

Add:

Depreciation 7,000,000.00 7,000,000.00 7,000,000.00 7,000,000.00 7,000,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

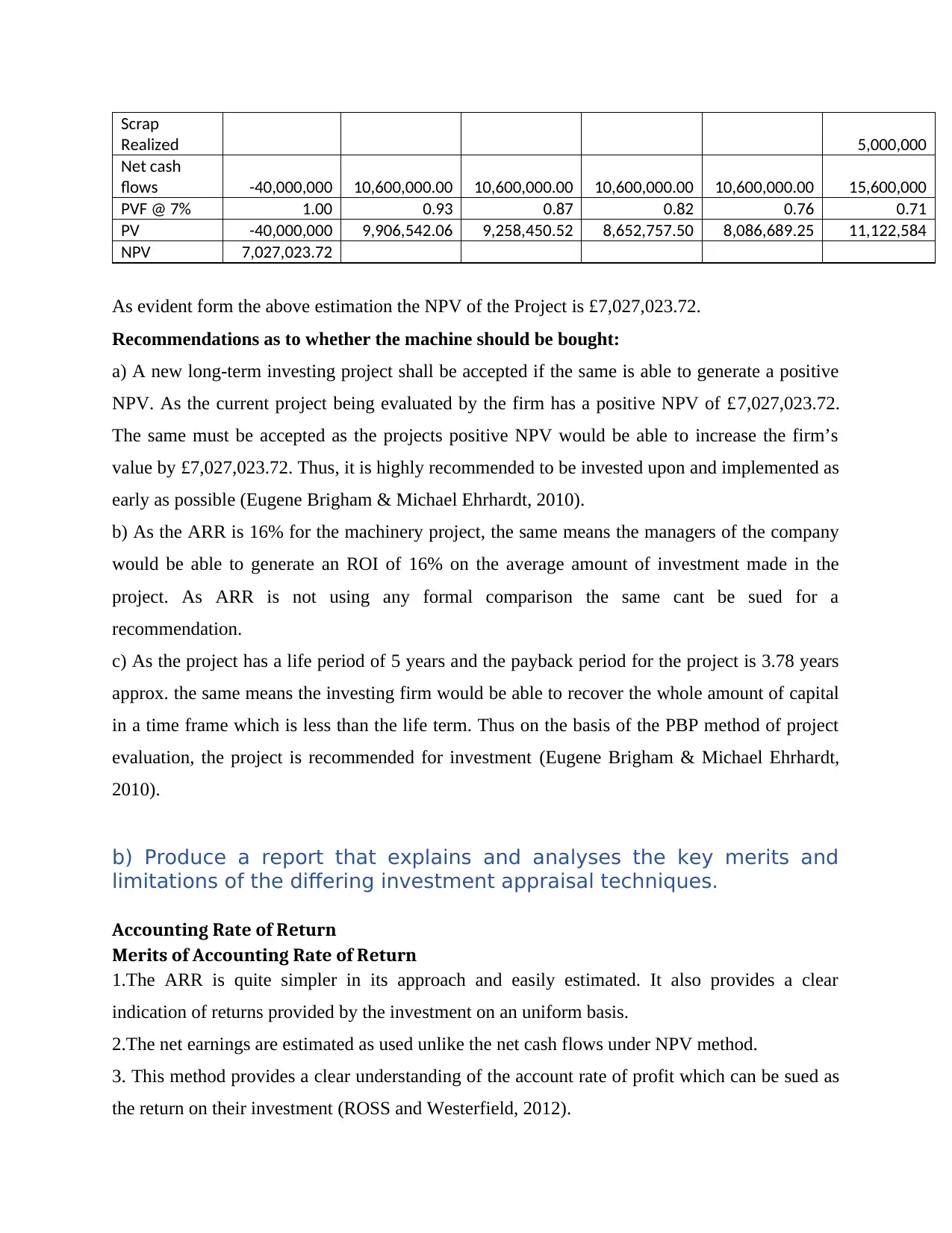

Scrap

Realized 5,000,000

Net cash

flows -40,000,000 10,600,000.00 10,600,000.00 10,600,000.00 10,600,000.00 15,600,000

PVF @ 7% 1.00 0.93 0.87 0.82 0.76 0.71

PV -40,000,000 9,906,542.06 9,258,450.52 8,652,757.50 8,086,689.25 11,122,584

NPV 7,027,023.72

As evident form the above estimation the NPV of the Project is £7,027,023.72.

Recommendations as to whether the machine should be bought:

a) A new long-term investing project shall be accepted if the same is able to generate a positive

NPV. As the current project being evaluated by the firm has a positive NPV of £7,027,023.72.

The same must be accepted as the projects positive NPV would be able to increase the firm’s

value by £7,027,023.72. Thus, it is highly recommended to be invested upon and implemented as

early as possible (Eugene Brigham & Michael Ehrhardt, 2010).

b) As the ARR is 16% for the machinery project, the same means the managers of the company

would be able to generate an ROI of 16% on the average amount of investment made in the

project. As ARR is not using any formal comparison the same cant be sued for a

recommendation.

c) As the project has a life period of 5 years and the payback period for the project is 3.78 years

approx. the same means the investing firm would be able to recover the whole amount of capital

in a time frame which is less than the life term. Thus on the basis of the PBP method of project

evaluation, the project is recommended for investment (Eugene Brigham & Michael Ehrhardt,

2010).

b) Produce a report that explains and analyses the key merits and

limitations of the differing investment appraisal techniques.

Accounting Rate of Return

Merits of Accounting Rate of Return

1.The ARR is quite simpler in its approach and easily estimated. It also provides a clear

indication of returns provided by the investment on an uniform basis.

2.The net earnings are estimated as used unlike the net cash flows under NPV method.

3. This method provides a clear understanding of the account rate of profit which can be sued as

the return on their investment (ROSS and Westerfield, 2012).

Realized 5,000,000

Net cash

flows -40,000,000 10,600,000.00 10,600,000.00 10,600,000.00 10,600,000.00 15,600,000

PVF @ 7% 1.00 0.93 0.87 0.82 0.76 0.71

PV -40,000,000 9,906,542.06 9,258,450.52 8,652,757.50 8,086,689.25 11,122,584

NPV 7,027,023.72

As evident form the above estimation the NPV of the Project is £7,027,023.72.

Recommendations as to whether the machine should be bought:

a) A new long-term investing project shall be accepted if the same is able to generate a positive

NPV. As the current project being evaluated by the firm has a positive NPV of £7,027,023.72.

The same must be accepted as the projects positive NPV would be able to increase the firm’s

value by £7,027,023.72. Thus, it is highly recommended to be invested upon and implemented as

early as possible (Eugene Brigham & Michael Ehrhardt, 2010).

b) As the ARR is 16% for the machinery project, the same means the managers of the company

would be able to generate an ROI of 16% on the average amount of investment made in the

project. As ARR is not using any formal comparison the same cant be sued for a

recommendation.

c) As the project has a life period of 5 years and the payback period for the project is 3.78 years

approx. the same means the investing firm would be able to recover the whole amount of capital

in a time frame which is less than the life term. Thus on the basis of the PBP method of project

evaluation, the project is recommended for investment (Eugene Brigham & Michael Ehrhardt,

2010).

b) Produce a report that explains and analyses the key merits and

limitations of the differing investment appraisal techniques.

Accounting Rate of Return

Merits of Accounting Rate of Return

1.The ARR is quite simpler in its approach and easily estimated. It also provides a clear

indication of returns provided by the investment on an uniform basis.

2.The net earnings are estimated as used unlike the net cash flows under NPV method.

3. This method provides a clear understanding of the account rate of profit which can be sued as

the return on their investment (ROSS and Westerfield, 2012).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4. Current performance is easily estimated and compared.

Limitations of Accounting Rate of Return

Despite being a simple method ARR has many shortcomings which makes it harder to use to

evaluate projects on a financial analysis:

a) it does not use financial concept and is a purely accounting measure and thus ignored.

b) This method like PBP does not use TVM.

c) This method fails to find a fair return against which the ROI can be compared.

d) External factors like risks are ignored making it impossible to adjust the real profitability

(Brearly, 2012).

Payback Period

Merits of payback period

a) It is one of the simplest methods of project cost evaluation and also easier to

understand.

b) This method is extremely useful to determine the liquidity associated with a project.

c) When there is uncertainty surrounding a project managers prefer the PBP to be

used to find if the project shall be pursued for further estimations or not.

Limitations of Payback period

a) The most visible limitations pertaining to this method is that it ignores the

discounting method and also does not use the time value of cash flows involved.

b) This method ignores the cash flows which occurs after the payback period is

determined.

c) Under this method there is no baas which can be rationally apply to all projects

universally and thus decisions are likely to be under the subjective bias of managers

in charge (Fabozz & Drake, 2009. ).

Net Present Value (NPV)

Merits of Net Present value method

Limitations of Accounting Rate of Return

Despite being a simple method ARR has many shortcomings which makes it harder to use to

evaluate projects on a financial analysis:

a) it does not use financial concept and is a purely accounting measure and thus ignored.

b) This method like PBP does not use TVM.

c) This method fails to find a fair return against which the ROI can be compared.

d) External factors like risks are ignored making it impossible to adjust the real profitability

(Brearly, 2012).

Payback Period

Merits of payback period

a) It is one of the simplest methods of project cost evaluation and also easier to

understand.

b) This method is extremely useful to determine the liquidity associated with a project.

c) When there is uncertainty surrounding a project managers prefer the PBP to be

used to find if the project shall be pursued for further estimations or not.

Limitations of Payback period

a) The most visible limitations pertaining to this method is that it ignores the

discounting method and also does not use the time value of cash flows involved.

b) This method ignores the cash flows which occurs after the payback period is

determined.

c) Under this method there is no baas which can be rationally apply to all projects

universally and thus decisions are likely to be under the subjective bias of managers

in charge (Fabozz & Drake, 2009. ).

Net Present Value (NPV)

Merits of Net Present value method

a) The most obvious benefit of the NPV method is that it considers the time value of money

and discounts the cash flows with an appropriate level of capital cost known as the

discount rate.

b) NPV is able to provide a single value in dollar to demonstrate the benefit that would be

derived form the implementation of the project.

c) The cost of capital and the relevant risk is inserted into the discount rates and hence the

cash flows discounted with the same demonstrates the value that can be added to the firm.

Limitations of Net Present value method

Despite a no of benefits of the NPV method the method also has a number of drawbacks which is

listed as follows:

a) One of the biggest drawbacks of NPV is the estimation of the cost of capital that can be

sued to discount the cash flows. If the discount rate is wrongly estimated, then the NPV

would be wrongly estimated as well. If the cost of capital is higher than many good

investing options might be rejected.

b) NPV method despite being widley used is incapable of being used fairly for estimating

the true worth of projects of different sizes (Bhimani, 2012).

c) NPV method would not be successful in providing a definitive idea of project worth

when the size of the projects differs too much and also when the projects life period are

not equal.

c) identification and explanation of the key benefits and limitations of

budgets as a strategic planning tool.

As per the desire of the management of the company the following report has bene prepared to

showcase the utility of the budgeting tool in the development of the company’s business and to

understand the key benefits of the process and limitations of the same. The report would make

sure management is aware of possible benefits and at the same are able to avoid harmful side

effects.

Budget as a tool of strategic Planning

and discounts the cash flows with an appropriate level of capital cost known as the

discount rate.

b) NPV is able to provide a single value in dollar to demonstrate the benefit that would be

derived form the implementation of the project.

c) The cost of capital and the relevant risk is inserted into the discount rates and hence the

cash flows discounted with the same demonstrates the value that can be added to the firm.

Limitations of Net Present value method

Despite a no of benefits of the NPV method the method also has a number of drawbacks which is

listed as follows:

a) One of the biggest drawbacks of NPV is the estimation of the cost of capital that can be

sued to discount the cash flows. If the discount rate is wrongly estimated, then the NPV

would be wrongly estimated as well. If the cost of capital is higher than many good

investing options might be rejected.

b) NPV method despite being widley used is incapable of being used fairly for estimating

the true worth of projects of different sizes (Bhimani, 2012).

c) NPV method would not be successful in providing a definitive idea of project worth

when the size of the projects differs too much and also when the projects life period are

not equal.

c) identification and explanation of the key benefits and limitations of

budgets as a strategic planning tool.

As per the desire of the management of the company the following report has bene prepared to

showcase the utility of the budgeting tool in the development of the company’s business and to

understand the key benefits of the process and limitations of the same. The report would make

sure management is aware of possible benefits and at the same are able to avoid harmful side

effects.

Budget as a tool of strategic Planning

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.