Financial Accounting Homework: UGB105 Module Solution

VerifiedAdded on 2022/11/30

|14

|2685

|119

Homework Assignment

AI Summary

This document presents a comprehensive solution to a financial accounting homework assignment, likely for a university-level course. It addresses key concepts such as preparing trading and profit and loss accounts, analyzing financial statements, and calculating important financial ratios like gross profit margin, return on capital employed, and current ratio. The solution includes detailed calculations, explanations of accounting principles, and interpretations of financial data. Furthermore, it explores the importance of financial information for various stakeholders, including management, shareholders, lenders, employees, and the public, highlighting the significance of financial records and reports in business operations and decision-making. The assignment also includes the preparation of bank, business takings, drawings, and purchases accounts.

UGB105 Module Title Introduction to Financial

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Question 1a......................................................................................................................................4

1 b)...................................................................................................................................................4

Question 2a).....................................................................................................................................9

2 b).................................................................................................................................................11

2 c).................................................................................................................................................13

Question 1a......................................................................................................................................4

1 b)...................................................................................................................................................4

Question 2a).....................................................................................................................................9

2 b).................................................................................................................................................11

2 c).................................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

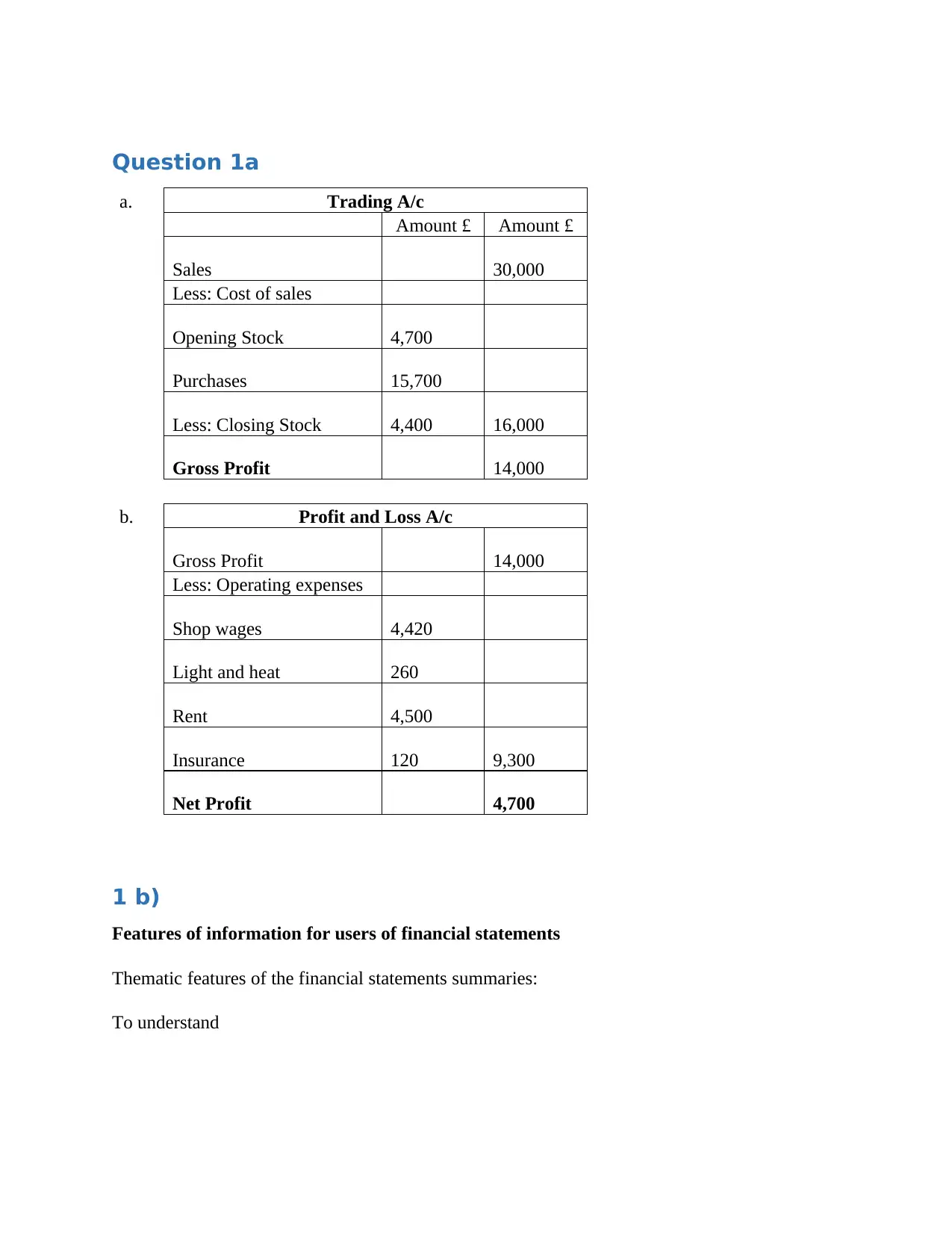

Question 1a

a. Trading A/c

Amount £ Amount £

Sales 30,000

Less: Cost of sales

Opening Stock 4,700

Purchases 15,700

Less: Closing Stock 4,400 16,000

Gross Profit 14,000

b. Profit and Loss A/c

Gross Profit 14,000

Less: Operating expenses

Shop wages 4,420

Light and heat 260

Rent 4,500

Insurance 120 9,300

Net Profit 4,700

1 b)

Features of information for users of financial statements

Thematic features of the financial statements summaries:

To understand

a. Trading A/c

Amount £ Amount £

Sales 30,000

Less: Cost of sales

Opening Stock 4,700

Purchases 15,700

Less: Closing Stock 4,400 16,000

Gross Profit 14,000

b. Profit and Loss A/c

Gross Profit 14,000

Less: Operating expenses

Shop wages 4,420

Light and heat 260

Rent 4,500

Insurance 120 9,300

Net Profit 4,700

1 b)

Features of information for users of financial statements

Thematic features of the financial statements summaries:

To understand

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

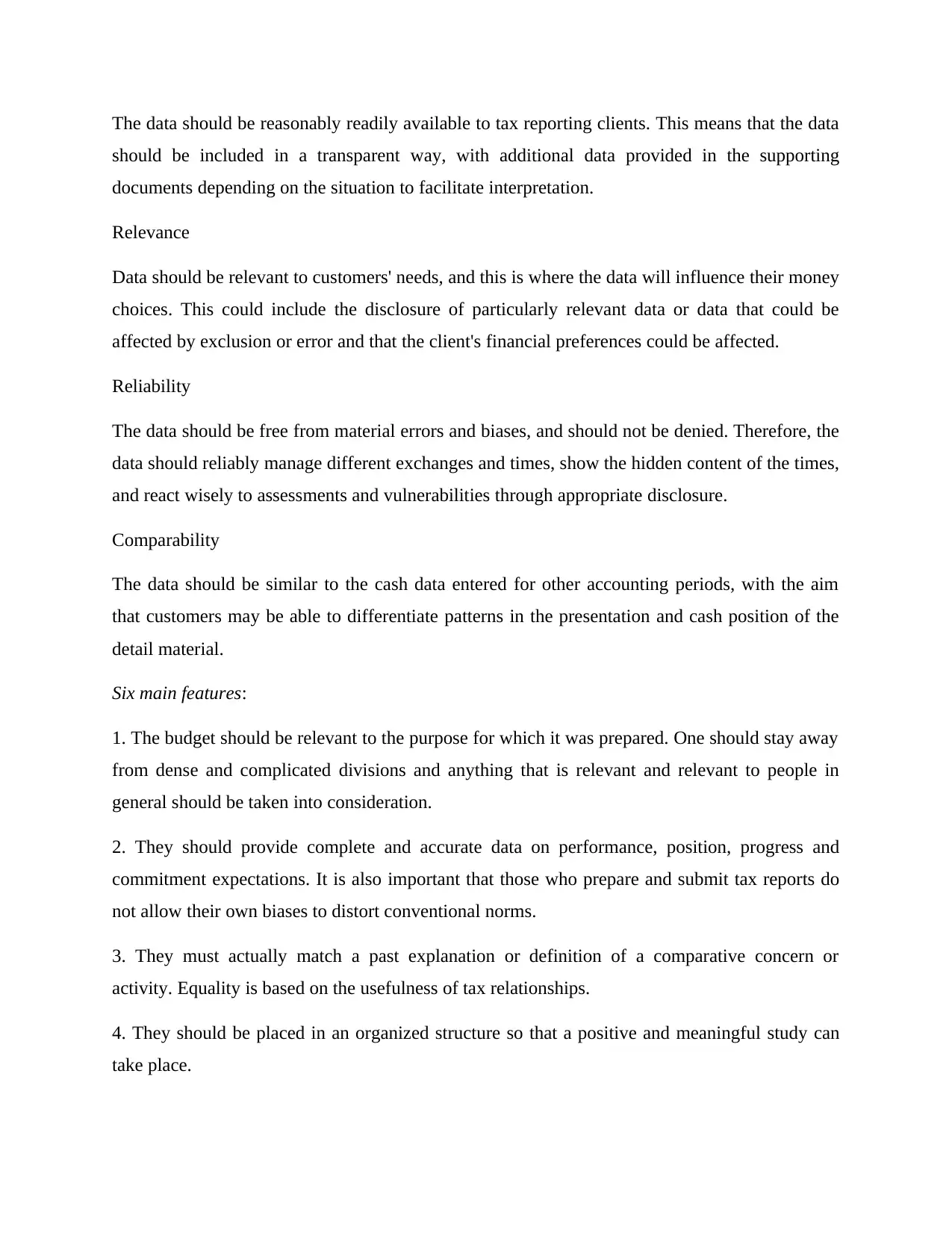

The data should be reasonably readily available to tax reporting clients. This means that the data

should be included in a transparent way, with additional data provided in the supporting

documents depending on the situation to facilitate interpretation.

Relevance

Data should be relevant to customers' needs, and this is where the data will influence their money

choices. This could include the disclosure of particularly relevant data or data that could be

affected by exclusion or error and that the client's financial preferences could be affected.

Reliability

The data should be free from material errors and biases, and should not be denied. Therefore, the

data should reliably manage different exchanges and times, show the hidden content of the times,

and react wisely to assessments and vulnerabilities through appropriate disclosure.

Comparability

The data should be similar to the cash data entered for other accounting periods, with the aim

that customers may be able to differentiate patterns in the presentation and cash position of the

detail material.

Six main features:

1. The budget should be relevant to the purpose for which it was prepared. One should stay away

from dense and complicated divisions and anything that is relevant and relevant to people in

general should be taken into consideration.

2. They should provide complete and accurate data on performance, position, progress and

commitment expectations. It is also important that those who prepare and submit tax reports do

not allow their own biases to distort conventional norms.

3. They must actually match a past explanation or definition of a comparative concern or

activity. Equality is based on the usefulness of tax relationships.

4. They should be placed in an organized structure so that a positive and meaningful study can

take place.

should be included in a transparent way, with additional data provided in the supporting

documents depending on the situation to facilitate interpretation.

Relevance

Data should be relevant to customers' needs, and this is where the data will influence their money

choices. This could include the disclosure of particularly relevant data or data that could be

affected by exclusion or error and that the client's financial preferences could be affected.

Reliability

The data should be free from material errors and biases, and should not be denied. Therefore, the

data should reliably manage different exchanges and times, show the hidden content of the times,

and react wisely to assessments and vulnerabilities through appropriate disclosure.

Comparability

The data should be similar to the cash data entered for other accounting periods, with the aim

that customers may be able to differentiate patterns in the presentation and cash position of the

detail material.

Six main features:

1. The budget should be relevant to the purpose for which it was prepared. One should stay away

from dense and complicated divisions and anything that is relevant and relevant to people in

general should be taken into consideration.

2. They should provide complete and accurate data on performance, position, progress and

commitment expectations. It is also important that those who prepare and submit tax reports do

not allow their own biases to distort conventional norms.

3. They must actually match a past explanation or definition of a comparative concern or

activity. Equality is based on the usefulness of tax relationships.

4. They should be placed in an organized structure so that a positive and meaningful study can

take place.

5. Budget reports should be prepared and presented at the right time. Too much delay in their

settlement would diminish the importance and usefulness of these claims.

6. Tax reports should have a common value and understanding. This can be achieved simply by

applying some "strict accounting guidelines" in their configuration.

The importance of the financial information:

The essence of tax summaries lies in their need to satisfy the movable interest of several types of

meetings such as administrative, tenants, public and so on.

1. Importance for governance:

The increase in the size and complexity of the elements that influence business activity requires a

logical and visionary approach in the management of current business activity.

The management team needs separate, accurate and systematic financial data for the purposes.

Tax summaries help the administration to understand the state, progress and prospects of the

business.

By giving management reasons for the industry's results, it empowers them to develop

appropriate strategies and approaches for the future. The administration disseminates in detail

through these budget reports, their presentation to various assemblies and legitimizes their

exercises and in this way the truth.

A close examination of the balance sheets reveals the pattern in the progress and position of large

corporations and allows the administration to implement appropriate improvements in ways to

avoid threatening situations.

2. Importance of shareholders:

The board is separate from the ownership owed to the organizations. Investors simply cannot

participate in the day-to-day running of the business. However, the impact of these exercises for

investors at the group's annual meeting should be reported as tax minutes.

These tests give investors the power to think about the capacity and adequacy of the

administration, as well as the supply chain and financial strength of the organization.

settlement would diminish the importance and usefulness of these claims.

6. Tax reports should have a common value and understanding. This can be achieved simply by

applying some "strict accounting guidelines" in their configuration.

The importance of the financial information:

The essence of tax summaries lies in their need to satisfy the movable interest of several types of

meetings such as administrative, tenants, public and so on.

1. Importance for governance:

The increase in the size and complexity of the elements that influence business activity requires a

logical and visionary approach in the management of current business activity.

The management team needs separate, accurate and systematic financial data for the purposes.

Tax summaries help the administration to understand the state, progress and prospects of the

business.

By giving management reasons for the industry's results, it empowers them to develop

appropriate strategies and approaches for the future. The administration disseminates in detail

through these budget reports, their presentation to various assemblies and legitimizes their

exercises and in this way the truth.

A close examination of the balance sheets reveals the pattern in the progress and position of large

corporations and allows the administration to implement appropriate improvements in ways to

avoid threatening situations.

2. Importance of shareholders:

The board is separate from the ownership owed to the organizations. Investors simply cannot

participate in the day-to-day running of the business. However, the impact of these exercises for

investors at the group's annual meeting should be reported as tax minutes.

These tests give investors the power to think about the capacity and adequacy of the

administration, as well as the supply chain and financial strength of the organization.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

By reviewing tax reports, prospective investors could determine the extent of receiving benefits,

the organization's current position and future opportunities, and choose to pursue their interests

in this group.

Distributed budget reports are the main source of data for future lenders.

3. Importance for lenders / creditors:

Budget reports provide valuable guidance for current and future providers and potential group

loan experts.

It is through a fundamental assessment of balance sheet reports that these collections form a

reflection on an organization's liquidity, profitability and long-term distribution position. This

will help them decide their future strategy.

4. Importance for the job:

Employees are granted a reward based on the amount of benefit as disclosed by a verified

benefits and incidents account. In this way, P and L a / c seem to be very necessary for experts.

Likewise, in compensation exchanges, the amount of benefits and benefits achieved is extremely

significant.

5. Public importance:

Industry is a social stuff. A number of company meetings, while not directly related to business,

want to learn about the position, progress and prospects of a business venture.

They are monetary examiners, legal advisors, exchange affiliations, worker's guilds, monetary

press, research researchers and instructors, and so forth It is just through these distributed budget

reports these individuals can dissect, judge and remark upon business undertaking.

6. Significance to National Economy:

The ascent and development of corporate area, by and large, impact the financial advancement of

a country. Deceitful and false corporate administrations break the certainty of the overall

population in business entities, which is fundamental for monetary advancement and retard the

financial development of the country.

the organization's current position and future opportunities, and choose to pursue their interests

in this group.

Distributed budget reports are the main source of data for future lenders.

3. Importance for lenders / creditors:

Budget reports provide valuable guidance for current and future providers and potential group

loan experts.

It is through a fundamental assessment of balance sheet reports that these collections form a

reflection on an organization's liquidity, profitability and long-term distribution position. This

will help them decide their future strategy.

4. Importance for the job:

Employees are granted a reward based on the amount of benefit as disclosed by a verified

benefits and incidents account. In this way, P and L a / c seem to be very necessary for experts.

Likewise, in compensation exchanges, the amount of benefits and benefits achieved is extremely

significant.

5. Public importance:

Industry is a social stuff. A number of company meetings, while not directly related to business,

want to learn about the position, progress and prospects of a business venture.

They are monetary examiners, legal advisors, exchange affiliations, worker's guilds, monetary

press, research researchers and instructors, and so forth It is just through these distributed budget

reports these individuals can dissect, judge and remark upon business undertaking.

6. Significance to National Economy:

The ascent and development of corporate area, by and large, impact the financial advancement of

a country. Deceitful and false corporate administrations break the certainty of the overall

population in business entities, which is fundamental for monetary advancement and retard the

financial development of the country.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Budget summaries act the hero of overall population by giving data by which they can analyze

and evaluate the genuine worth of the organization and try not to be cheated by corrupt people.

The law tries to raise the degree of business profound quality by convincing the organizations to

plan budget summaries in an unmistakable and efficient frame and reveal material data.

This has expanded the certainty of people in general in organizations. Budget reports are

additionally fundamental for the different administrative bodies, for example, charge specialists,

Registrar of organizations, and so on They can decide whether the guidelines are as a rule

stringently followed and furthermore if the guidelines are delivering the ideal impact, by

assessing the fiscal reports.

Benefits:

Monetary records are important for the organization's bookkeeping framework. Organizations

frequently use bookkeeping as an approach to keep track of who's winning. Private ventures

frequently think that its essential to keep track of who's winning since precisely following

monetary data is the most ideal approach to decide the adequacy and effectiveness of their

activities. Neglecting to comprehend or follow monetary data can rapidly prompt hazardous

business circumstances, for example, low income or the chance of insolvency. Monetary records

can likewise give chronicled records to settling on future business choices.

Fiscal report Reviews

Monetary records permit organizations to foster budget summaries. Each record contains explicit

data that is gathered into a total accumulation of monetary data. Maybe than evaluating every

individual record for patterns and other examination, fiscal reports permit organizations to direct

a hierarchical audit of monetary data. Monetary record investigation with mechanized

bookkeeping frameworks can build the budget summary examination of individual records.

Automated explanation examination regularly permits organizations to "drill down" into singular

records and audit explicit monetary exchanges.

The pay explanation, asset report and articulation of incomes are the three most mainstream

budget summaries and business. Every one of these assertions contains diverse monetary records

and data identifying with business activities. Organizations may utilize monetary records to

and evaluate the genuine worth of the organization and try not to be cheated by corrupt people.

The law tries to raise the degree of business profound quality by convincing the organizations to

plan budget summaries in an unmistakable and efficient frame and reveal material data.

This has expanded the certainty of people in general in organizations. Budget reports are

additionally fundamental for the different administrative bodies, for example, charge specialists,

Registrar of organizations, and so on They can decide whether the guidelines are as a rule

stringently followed and furthermore if the guidelines are delivering the ideal impact, by

assessing the fiscal reports.

Benefits:

Monetary records are important for the organization's bookkeeping framework. Organizations

frequently use bookkeeping as an approach to keep track of who's winning. Private ventures

frequently think that its essential to keep track of who's winning since precisely following

monetary data is the most ideal approach to decide the adequacy and effectiveness of their

activities. Neglecting to comprehend or follow monetary data can rapidly prompt hazardous

business circumstances, for example, low income or the chance of insolvency. Monetary records

can likewise give chronicled records to settling on future business choices.

Fiscal report Reviews

Monetary records permit organizations to foster budget summaries. Each record contains explicit

data that is gathered into a total accumulation of monetary data. Maybe than evaluating every

individual record for patterns and other examination, fiscal reports permit organizations to direct

a hierarchical audit of monetary data. Monetary record investigation with mechanized

bookkeeping frameworks can build the budget summary examination of individual records.

Automated explanation examination regularly permits organizations to "drill down" into singular

records and audit explicit monetary exchanges.

The pay explanation, asset report and articulation of incomes are the three most mainstream

budget summaries and business. Every one of these assertions contains diverse monetary records

and data identifying with business activities. Organizations may utilize monetary records to

foster other explicit monetary reports. These reports are frequently industry explicit and furnish

entrepreneurs or chiefs with explicit data in regards to business tasks.

Foster Budgets

Numerous organizations foster working spending plans for their activities. These spending plans

contain recorded data dependent on an organization's monetary records. Spending plans are

typically made by exploring chronicled data from different monetary records and endeavoring to

gauge whether these numbers will diminish, stay something very similar or expansion in future

tasks. Spending plans make a monetary guide that organizations can utilize when settling on

business choices.

Track Cash Management

Monetary records permit organizations to buy financial assets, products or administrations on

account from different organizations. These buys address exchange credit the business climate.

Organizations use creditor liabilities and records receivable monetary records to monitor this

data. Records payable addresses all cash owed to different organizations for assets bought.

Records receivable incorporates all cash not gathered from customer buys.

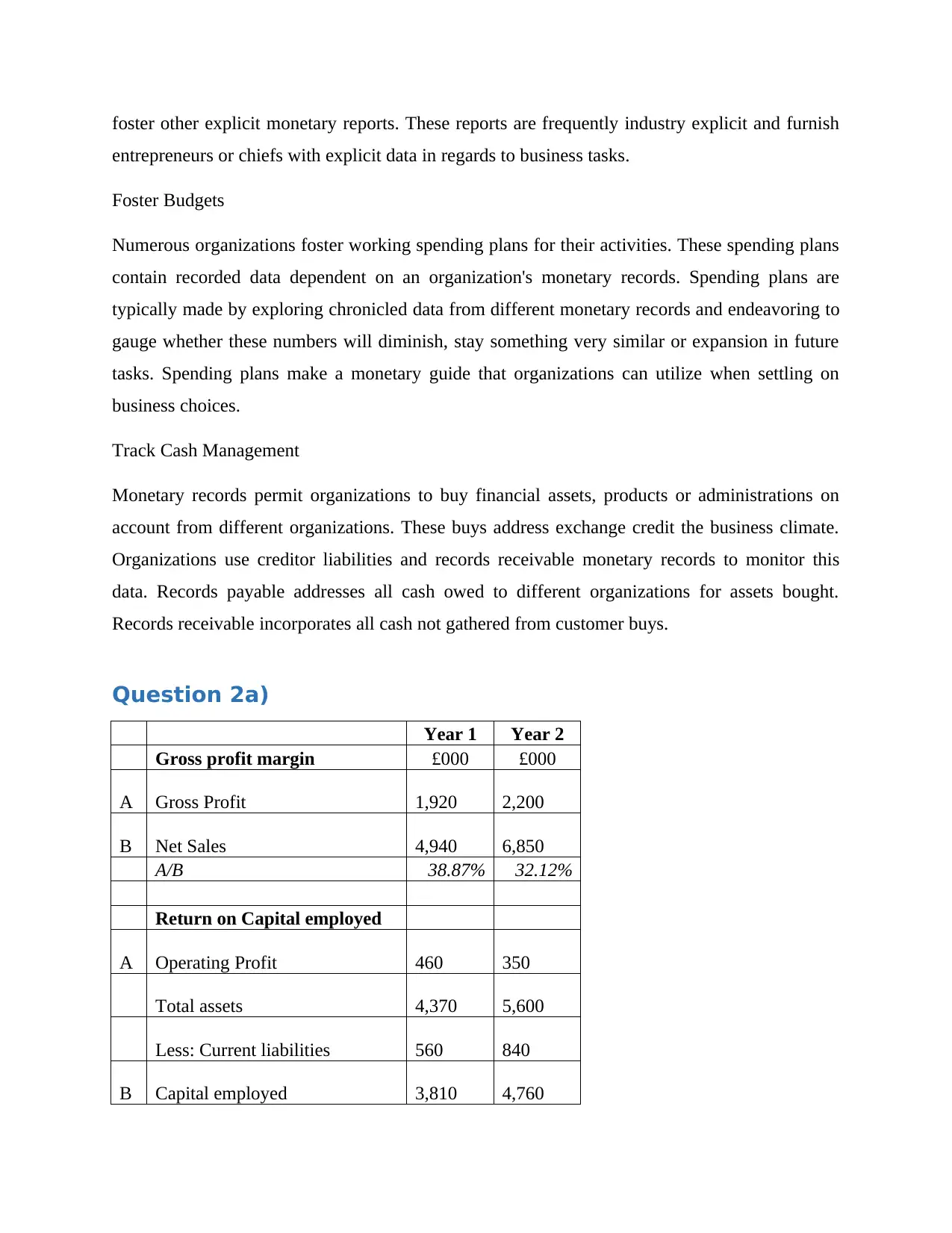

Question 2a)

Year 1 Year 2

Gross profit margin £000 £000

A Gross Profit 1,920 2,200

B Net Sales 4,940 6,850

A/B 38.87% 32.12%

Return on Capital employed

A Operating Profit 460 350

Total assets 4,370 5,600

Less: Current liabilities 560 840

B Capital employed 3,810 4,760

entrepreneurs or chiefs with explicit data in regards to business tasks.

Foster Budgets

Numerous organizations foster working spending plans for their activities. These spending plans

contain recorded data dependent on an organization's monetary records. Spending plans are

typically made by exploring chronicled data from different monetary records and endeavoring to

gauge whether these numbers will diminish, stay something very similar or expansion in future

tasks. Spending plans make a monetary guide that organizations can utilize when settling on

business choices.

Track Cash Management

Monetary records permit organizations to buy financial assets, products or administrations on

account from different organizations. These buys address exchange credit the business climate.

Organizations use creditor liabilities and records receivable monetary records to monitor this

data. Records payable addresses all cash owed to different organizations for assets bought.

Records receivable incorporates all cash not gathered from customer buys.

Question 2a)

Year 1 Year 2

Gross profit margin £000 £000

A Gross Profit 1,920 2,200

B Net Sales 4,940 6,850

A/B 38.87% 32.12%

Return on Capital employed

A Operating Profit 460 350

Total assets 4,370 5,600

Less: Current liabilities 560 840

B Capital employed 3,810 4,760

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

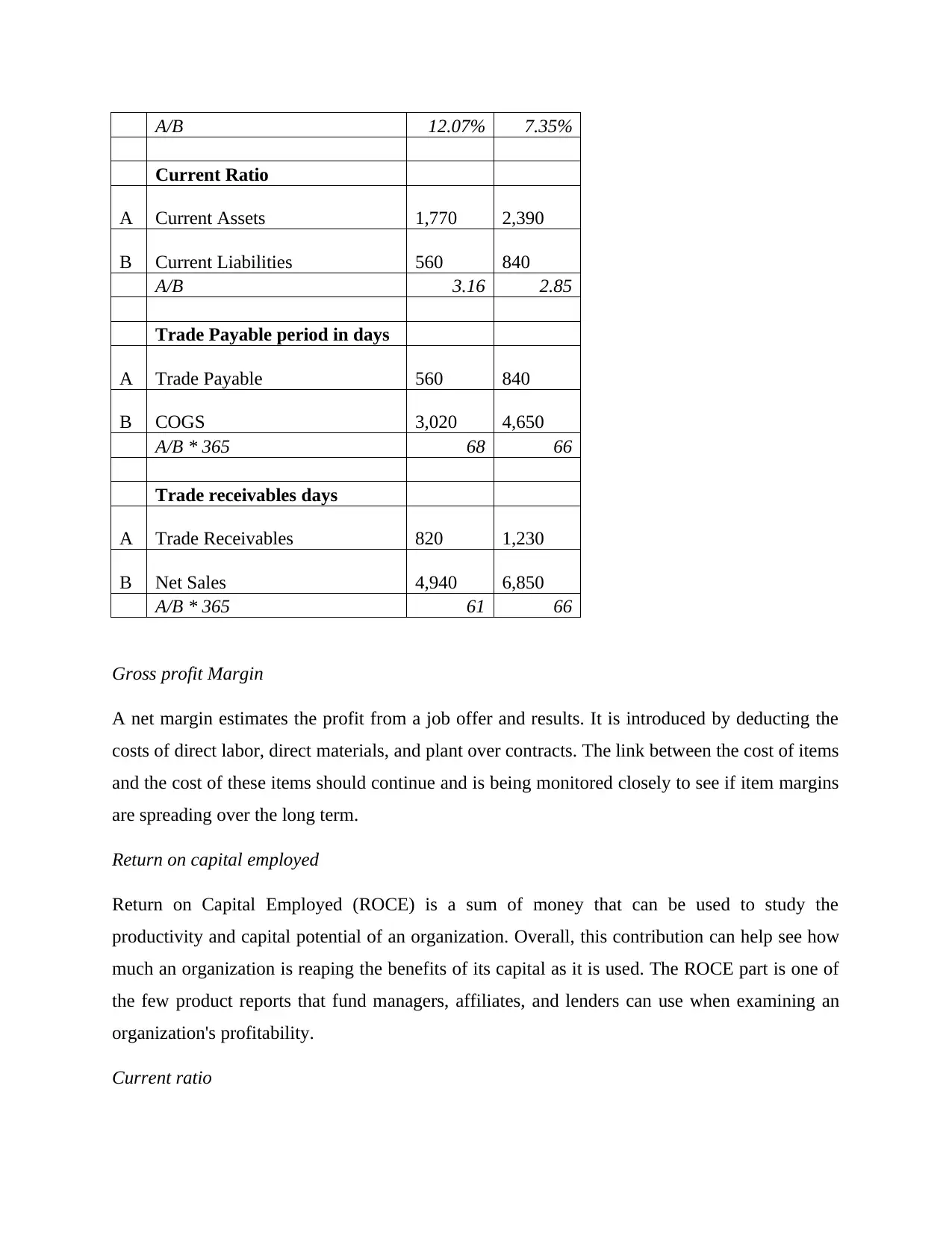

A/B 12.07% 7.35%

Current Ratio

A Current Assets 1,770 2,390

B Current Liabilities 560 840

A/B 3.16 2.85

Trade Payable period in days

A Trade Payable 560 840

B COGS 3,020 4,650

A/B * 365 68 66

Trade receivables days

A Trade Receivables 820 1,230

B Net Sales 4,940 6,850

A/B * 365 61 66

Gross profit Margin

A net margin estimates the profit from a job offer and results. It is introduced by deducting the

costs of direct labor, direct materials, and plant over contracts. The link between the cost of items

and the cost of these items should continue and is being monitored closely to see if item margins

are spreading over the long term.

Return on capital employed

Return on Capital Employed (ROCE) is a sum of money that can be used to study the

productivity and capital potential of an organization. Overall, this contribution can help see how

much an organization is reaping the benefits of its capital as it is used. The ROCE part is one of

the few product reports that fund managers, affiliates, and lenders can use when examining an

organization's profitability.

Current ratio

Current Ratio

A Current Assets 1,770 2,390

B Current Liabilities 560 840

A/B 3.16 2.85

Trade Payable period in days

A Trade Payable 560 840

B COGS 3,020 4,650

A/B * 365 68 66

Trade receivables days

A Trade Receivables 820 1,230

B Net Sales 4,940 6,850

A/B * 365 61 66

Gross profit Margin

A net margin estimates the profit from a job offer and results. It is introduced by deducting the

costs of direct labor, direct materials, and plant over contracts. The link between the cost of items

and the cost of these items should continue and is being monitored closely to see if item margins

are spreading over the long term.

Return on capital employed

Return on Capital Employed (ROCE) is a sum of money that can be used to study the

productivity and capital potential of an organization. Overall, this contribution can help see how

much an organization is reaping the benefits of its capital as it is used. The ROCE part is one of

the few product reports that fund managers, affiliates, and lenders can use when examining an

organization's profitability.

Current ratio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The current allowance is used to assess an organization's ability to meet its outstanding

commitments, for example, credit liabilities and salary. It is justified by the division of current

resources into current responsibilities. Entrepreneurs should pay attention to this allowance for

their organization, and lenders may find it helpful to review the available allowances of the

groups as they consider which shares to buy.

Trade payable period in days

The portion of the trade conversion payable, also known as the percentage of debt conversion or

tenant conversion allowance, is a proportion of working liquidity that is the normal number of

times an organization pays its banks over accounting periods. A portion is a percentage of cash

per minute, with a higher pay conversion percentage more appropriate.

Trade receivables days

The proportion of the lender's days (or credits as a trade) is related to liquidity.

The allowance focuses on how long it takes for borrowers to settle their bills. The allowance

shows whether people in debt are given unnecessary credit. A high figure (higher than normal

business) can cause common problems with bond mix or the position of important client money.

The effective and unique combination of customer responsibilities is a key component of

executives ’revenue, so this is a percentage that is strongly viewed in a number of organizations.

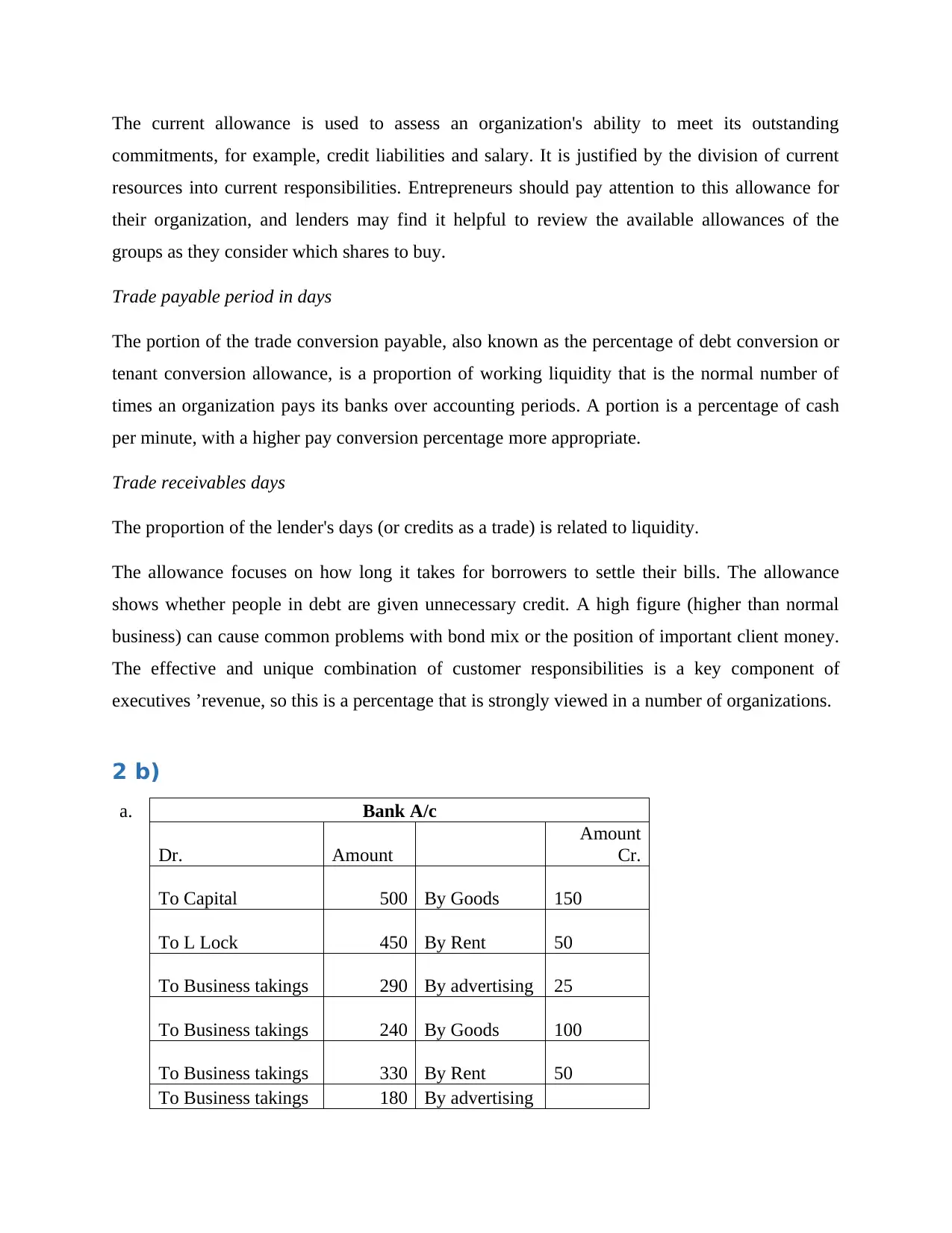

2 b)

a. Bank A/c

Dr. Amount

Amount

Cr.

To Capital 500 By Goods 150

To L Lock 450 By Rent 50

To Business takings 290 By advertising 25

To Business takings 240 By Goods 100

To Business takings 330 By Rent 50

To Business takings 180 By advertising

commitments, for example, credit liabilities and salary. It is justified by the division of current

resources into current responsibilities. Entrepreneurs should pay attention to this allowance for

their organization, and lenders may find it helpful to review the available allowances of the

groups as they consider which shares to buy.

Trade payable period in days

The portion of the trade conversion payable, also known as the percentage of debt conversion or

tenant conversion allowance, is a proportion of working liquidity that is the normal number of

times an organization pays its banks over accounting periods. A portion is a percentage of cash

per minute, with a higher pay conversion percentage more appropriate.

Trade receivables days

The proportion of the lender's days (or credits as a trade) is related to liquidity.

The allowance focuses on how long it takes for borrowers to settle their bills. The allowance

shows whether people in debt are given unnecessary credit. A high figure (higher than normal

business) can cause common problems with bond mix or the position of important client money.

The effective and unique combination of customer responsibilities is a key component of

executives ’revenue, so this is a percentage that is strongly viewed in a number of organizations.

2 b)

a. Bank A/c

Dr. Amount

Amount

Cr.

To Capital 500 By Goods 150

To L Lock 450 By Rent 50

To Business takings 290 By advertising 25

To Business takings 240 By Goods 100

To Business takings 330 By Rent 50

To Business takings 180 By advertising

30

By Drawings 100

By Drawings 75

By Bal c/d 1,410

1,990 1,990

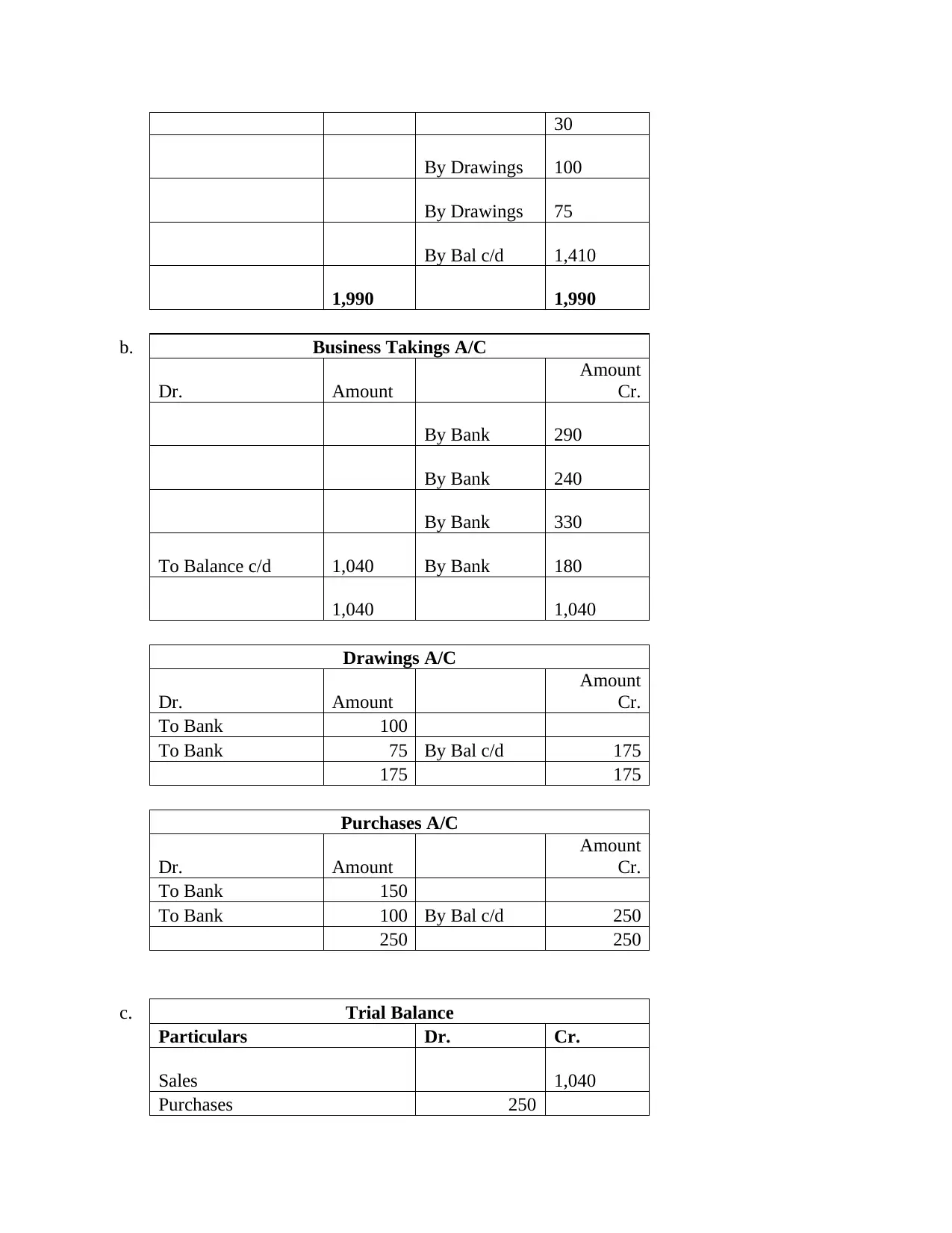

b. Business Takings A/C

Dr. Amount

Amount

Cr.

By Bank 290

By Bank 240

By Bank 330

To Balance c/d 1,040 By Bank 180

1,040 1,040

Drawings A/C

Dr. Amount

Amount

Cr.

To Bank 100

To Bank 75 By Bal c/d 175

175 175

Purchases A/C

Dr. Amount

Amount

Cr.

To Bank 150

To Bank 100 By Bal c/d 250

250 250

c. Trial Balance

Particulars Dr. Cr.

Sales 1,040

Purchases 250

By Drawings 100

By Drawings 75

By Bal c/d 1,410

1,990 1,990

b. Business Takings A/C

Dr. Amount

Amount

Cr.

By Bank 290

By Bank 240

By Bank 330

To Balance c/d 1,040 By Bank 180

1,040 1,040

Drawings A/C

Dr. Amount

Amount

Cr.

To Bank 100

To Bank 75 By Bal c/d 175

175 175

Purchases A/C

Dr. Amount

Amount

Cr.

To Bank 150

To Bank 100 By Bal c/d 250

250 250

c. Trial Balance

Particulars Dr. Cr.

Sales 1,040

Purchases 250

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.