Analysis of CSR Limited: Auditing, Risk, and Account Balances

VerifiedAdded on 2020/02/18

|16

|2953

|303

Report

AI Summary

This report provides an in-depth analysis of CSR Limited's auditing processes, encompassing a detailed examination of industry and regulatory factors impacting the company's operations. It identifies and assesses various business risks, including those stemming from competitive pressures, technological advancements, and changes in management or accounting practices. The report specifically highlights three account balances—assets and liabilities, equity interests, and transactions—that are deemed at significant risk of material misstatement, explaining the underlying reasons for this assessment. For each account balance, the report outlines the key assertions at risk, details relevant substantive audit procedures designed to address these risks, and suggests practical internal controls to mitigate them. The report emphasizes the importance of understanding the entity and its environment, and the application of both quantitative and qualitative disclosures to identify and mitigate risks in the audit process.

1 Auditing

Auditing

Auditing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2 Auditing

Contents

Introduction.................................................................................................................................................3

1. Report on the knowledge gained of CSR Limitedand its environment:...................................................3

2. Identify and assess its business risk:........................................................................................................4

3. From your risk identification identify three (3) specific account balances (not account classifications)

that you consider at significant risk of material misstatement. For each of the three account balances

you identify:................................................................................................................................................5

Conclusion.................................................................................................................................................14

References:................................................................................................................................................15

Contents

Introduction.................................................................................................................................................3

1. Report on the knowledge gained of CSR Limitedand its environment:...................................................3

2. Identify and assess its business risk:........................................................................................................4

3. From your risk identification identify three (3) specific account balances (not account classifications)

that you consider at significant risk of material misstatement. For each of the three account balances

you identify:................................................................................................................................................5

Conclusion.................................................................................................................................................14

References:................................................................................................................................................15

3 Auditing

Introduction

This study helps in developing an understanding of CSR Limitedand the different environments which

impact the organization. Industry factors, regulatory factors and various other external factors affect the

working of CSR Limited. To deal with these factors, the management of CSR Limiteddefine overall goals

and objectives of the organization in order to make the plans. This study also provides a detailed

understanding of various business risk of CSR Limited. The business risk also includes various internal

and external events which are relevant to the preparation of financial statements of the organization.

This study also provides details of business risk that may consider at significant risk of material

misstatement in the account balances of financial statements of CSR Limited.

1. Report on the knowledge gained of CSR Limited and its environment:

The Entity and its environment

Industry Factors

The industry factors which impact CSR Limitedare competitive environment, customer relationships,

organization relation with its suppliers and different technologies advancement. The other industry

factors which will impact CSR Limited are energy supply and cost, price competition and seasonal

activities. The industry in which CSR Limited is carrying out its operations may lead towards risks of

material misstatements in the financial statements (Australian Government, 2017). These material

misstatements arise from the degree of regulations and the nature and objective of the business of the

organization.

Regulatory Factors

The regulatory environment of CSR Limited is composed of applicable accounting policies and financial

framework and the political and legal environment. The other regulatory factors which affect the

organization are industry specific practices which are formed by government and the regulations which

may impact the operations of the organization. Foreign exchange policies, monetary policies, fiscal

policies and trade restriction policies are the regulatory factors which impact CSR Limited (Berg, 2010).

Other External factors

Introduction

This study helps in developing an understanding of CSR Limitedand the different environments which

impact the organization. Industry factors, regulatory factors and various other external factors affect the

working of CSR Limited. To deal with these factors, the management of CSR Limiteddefine overall goals

and objectives of the organization in order to make the plans. This study also provides a detailed

understanding of various business risk of CSR Limited. The business risk also includes various internal

and external events which are relevant to the preparation of financial statements of the organization.

This study also provides details of business risk that may consider at significant risk of material

misstatement in the account balances of financial statements of CSR Limited.

1. Report on the knowledge gained of CSR Limited and its environment:

The Entity and its environment

Industry Factors

The industry factors which impact CSR Limitedare competitive environment, customer relationships,

organization relation with its suppliers and different technologies advancement. The other industry

factors which will impact CSR Limited are energy supply and cost, price competition and seasonal

activities. The industry in which CSR Limited is carrying out its operations may lead towards risks of

material misstatements in the financial statements (Australian Government, 2017). These material

misstatements arise from the degree of regulations and the nature and objective of the business of the

organization.

Regulatory Factors

The regulatory environment of CSR Limited is composed of applicable accounting policies and financial

framework and the political and legal environment. The other regulatory factors which affect the

organization are industry specific practices which are formed by government and the regulations which

may impact the operations of the organization. Foreign exchange policies, monetary policies, fiscal

policies and trade restriction policies are the regulatory factors which impact CSR Limited (Berg, 2010).

Other External factors

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4 Auditing

The other external factors which impact CSR Limited are general economic conditions of the

organization, interest rates, availability of loan in the country and revaluation of currency.

Nature of CSR Limited

CSR Limited is carrying out its business activities in according with the industry factors, regulatory factors

and other factors. To deal with these factors, the management of CSR Limited define overall goals and

objectives of the organization in order to make the plans. The management of the organization

formulates various strategies in order to achieve the goals and objectives and theses strategies by the

top management changes from time to time (De Martinis et. al., 2011).

For assessment of risk, the auditor should develop a proper understanding on the nature of CSR Limited.

The nature of CSR Limited primary consists of ownerships, governance and the other types of

investments. The Auditor should also identify the structure of CSR Limited and the availability of finance

for the organization. This understanding will help the auditor to properly make an understanding about

classes of transactions, disclosures and account balances in the financial reporting system (Keane et. al.,

2012). The auditor should also develop an understanding about the ownership and the key personnel of

CSR Limited and their relationship with each other in order to identify the related party transactions in

the organization.

The auditor should develop an understanding about the measurement of the financial performance of

CSR Limited. Financial performance measurement in the organization always creates inbuilt pressure to

take some reasonable steps in order to improve the performance of the organization. This will help the

auditor to identify whether the management actions can lead towards material misstatement or not.

The The auditor should obtain a particular understanding through carrying out various procedures

regarding risk assessment in order to identify the design of controls which can play an important role in

the audit of the financial statements of the organization (Asare and Wright,2012). This will also help the

auditor that these controls have been implemented in the organization or not.

2. Identify and assess its business risk:

There is various business risk of CSR Limited which is discussed here. The business risk can be regarding

to the preparation of the financial statements according to the applicable financial standards and

reporting system prevalent in the country. The business risk to the organization can be to make an

estimation of the importance and assessment of the occurrence of transactions in order to make a

The other external factors which impact CSR Limited are general economic conditions of the

organization, interest rates, availability of loan in the country and revaluation of currency.

Nature of CSR Limited

CSR Limited is carrying out its business activities in according with the industry factors, regulatory factors

and other factors. To deal with these factors, the management of CSR Limited define overall goals and

objectives of the organization in order to make the plans. The management of the organization

formulates various strategies in order to achieve the goals and objectives and theses strategies by the

top management changes from time to time (De Martinis et. al., 2011).

For assessment of risk, the auditor should develop a proper understanding on the nature of CSR Limited.

The nature of CSR Limited primary consists of ownerships, governance and the other types of

investments. The Auditor should also identify the structure of CSR Limited and the availability of finance

for the organization. This understanding will help the auditor to properly make an understanding about

classes of transactions, disclosures and account balances in the financial reporting system (Keane et. al.,

2012). The auditor should also develop an understanding about the ownership and the key personnel of

CSR Limited and their relationship with each other in order to identify the related party transactions in

the organization.

The auditor should develop an understanding about the measurement of the financial performance of

CSR Limited. Financial performance measurement in the organization always creates inbuilt pressure to

take some reasonable steps in order to improve the performance of the organization. This will help the

auditor to identify whether the management actions can lead towards material misstatement or not.

The The auditor should obtain a particular understanding through carrying out various procedures

regarding risk assessment in order to identify the design of controls which can play an important role in

the audit of the financial statements of the organization (Asare and Wright,2012). This will also help the

auditor that these controls have been implemented in the organization or not.

2. Identify and assess its business risk:

There is various business risk of CSR Limited which is discussed here. The business risk can be regarding

to the preparation of the financial statements according to the applicable financial standards and

reporting system prevalent in the country. The business risk to the organization can be to make an

estimation of the importance and assessment of the occurrence of transactions in order to make a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5 Auditing

decision regarding the results which have to be attained. The business risk also includes various internal

and external events which are relevant to the preparation of financial statements of the organization.

The internal and external events in the organization have the ability to affect the financial reporting and

the financial data consistently (Aldamen et. al., 2012). The management of the organization can make

plans and actions in order to mitigate the risks. The business risk in the organization can arise due to

some changes in the circumstances-

When there is a change in the operating environment of the organization then there arises a risk

of competitive pressure which can lead towards the risk in misstatements of account balances

regarding assets and liabilities and equity interest (Lary and Taylor,2012).

When new personnel is hired in the organization than this raises the risk of misstatement in the

transactions of the financial statements because the individual may have different focus towards

development on understanding of accounting policies and practices adopted by CSR Limited.

If the new information technology system is implemented in the organization than this arises

the business risk of misstatements in the financial statements because rapid changes in

technology can made the personnel of CSR Limited incapable of development of an

understanding of how the calculations has to be done with these new systems of the

organization (Azim, 2012).

If CSR limited wants to do corporate restructuring than it arises the risk of misstatement of

assets and liabilities because the professionals will face difficulties in segregation of the liabilities

and assets.

Adoption of new accounting practices and policies by CSR limited can lead the business risk of

misstatement in the financial statement because changes in accounting principles always have

affect on financial reporting (Stanley and Marsden, 2013).

CSR Limited is thinking of entering into new business areas and wants to expand its business

which may lead towards business risks as it will lead towards misstatement in the transactions

of the various account balances of the organization (Mazza and Azzali, 2015).

3. Three (3) specific account balances (not account classifications) at significant risk of material

misstatement

Specific account balance

decision regarding the results which have to be attained. The business risk also includes various internal

and external events which are relevant to the preparation of financial statements of the organization.

The internal and external events in the organization have the ability to affect the financial reporting and

the financial data consistently (Aldamen et. al., 2012). The management of the organization can make

plans and actions in order to mitigate the risks. The business risk in the organization can arise due to

some changes in the circumstances-

When there is a change in the operating environment of the organization then there arises a risk

of competitive pressure which can lead towards the risk in misstatements of account balances

regarding assets and liabilities and equity interest (Lary and Taylor,2012).

When new personnel is hired in the organization than this raises the risk of misstatement in the

transactions of the financial statements because the individual may have different focus towards

development on understanding of accounting policies and practices adopted by CSR Limited.

If the new information technology system is implemented in the organization than this arises

the business risk of misstatements in the financial statements because rapid changes in

technology can made the personnel of CSR Limited incapable of development of an

understanding of how the calculations has to be done with these new systems of the

organization (Azim, 2012).

If CSR limited wants to do corporate restructuring than it arises the risk of misstatement of

assets and liabilities because the professionals will face difficulties in segregation of the liabilities

and assets.

Adoption of new accounting practices and policies by CSR limited can lead the business risk of

misstatement in the financial statement because changes in accounting principles always have

affect on financial reporting (Stanley and Marsden, 2013).

CSR Limited is thinking of entering into new business areas and wants to expand its business

which may lead towards business risks as it will lead towards misstatement in the transactions

of the various account balances of the organization (Mazza and Azzali, 2015).

3. Three (3) specific account balances (not account classifications) at significant risk of material

misstatement

Specific account balance

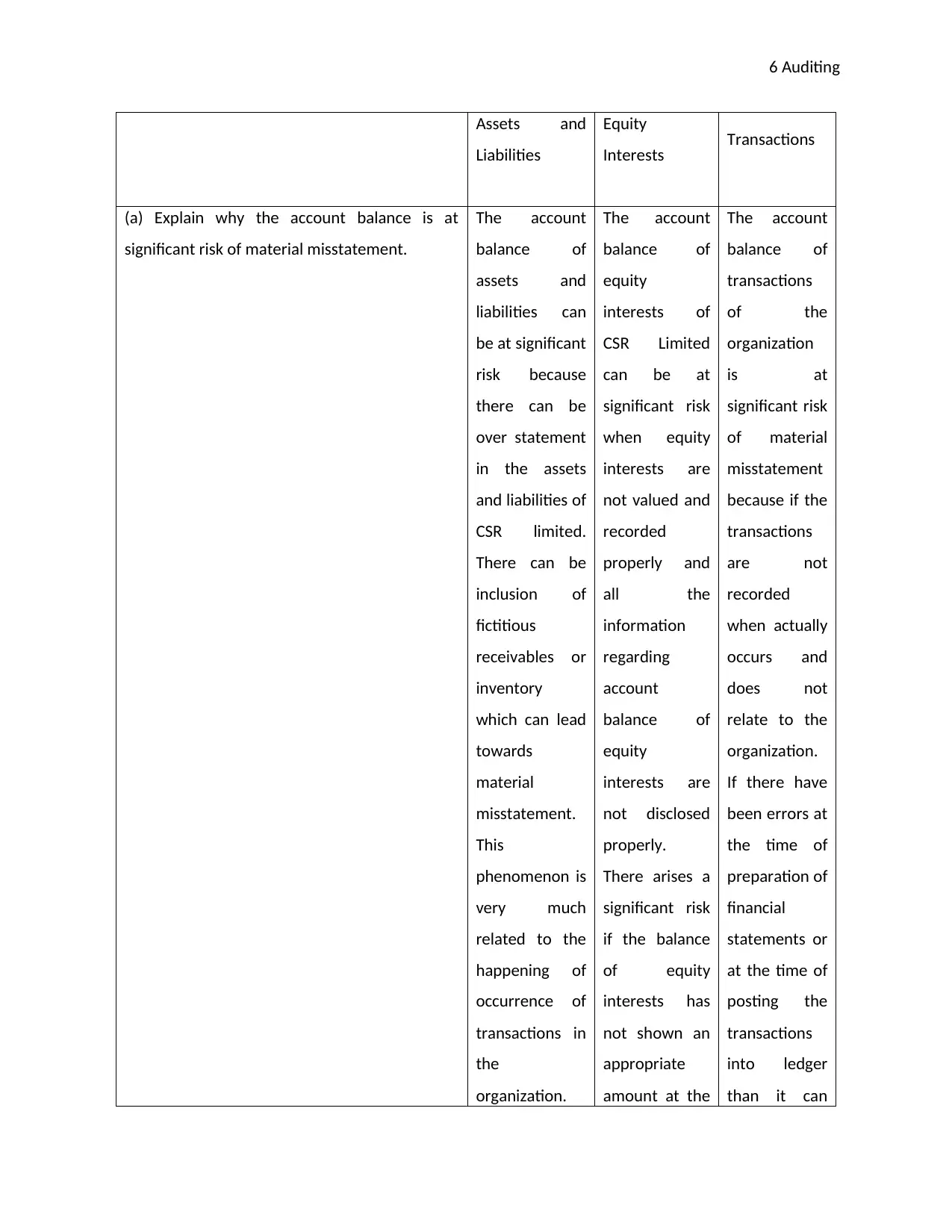

6 Auditing

Assets and

Liabilities

Equity

Interests Transactions

(a) Explain why the account balance is at

significant risk of material misstatement.

The account

balance of

assets and

liabilities can

be at significant

risk because

there can be

over statement

in the assets

and liabilities of

CSR limited.

There can be

inclusion of

fictitious

receivables or

inventory

which can lead

towards

material

misstatement.

This

phenomenon is

very much

related to the

happening of

occurrence of

transactions in

the

organization.

The account

balance of

equity

interests of

CSR Limited

can be at

significant risk

when equity

interests are

not valued and

recorded

properly and

all the

information

regarding

account

balance of

equity

interests are

not disclosed

properly.

There arises a

significant risk

if the balance

of equity

interests has

not shown an

appropriate

amount at the

The account

balance of

transactions

of the

organization

is at

significant risk

of material

misstatement

because if the

transactions

are not

recorded

when actually

occurs and

does not

relate to the

organization.

If there have

been errors at

the time of

preparation of

financial

statements or

at the time of

posting the

transactions

into ledger

than it can

Assets and

Liabilities

Equity

Interests Transactions

(a) Explain why the account balance is at

significant risk of material misstatement.

The account

balance of

assets and

liabilities can

be at significant

risk because

there can be

over statement

in the assets

and liabilities of

CSR limited.

There can be

inclusion of

fictitious

receivables or

inventory

which can lead

towards

material

misstatement.

This

phenomenon is

very much

related to the

happening of

occurrence of

transactions in

the

organization.

The account

balance of

equity

interests of

CSR Limited

can be at

significant risk

when equity

interests are

not valued and

recorded

properly and

all the

information

regarding

account

balance of

equity

interests are

not disclosed

properly.

There arises a

significant risk

if the balance

of equity

interests has

not shown an

appropriate

amount at the

The account

balance of

transactions

of the

organization

is at

significant risk

of material

misstatement

because if the

transactions

are not

recorded

when actually

occurs and

does not

relate to the

organization.

If there have

been errors at

the time of

preparation of

financial

statements or

at the time of

posting the

transactions

into ledger

than it can

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7 Auditing

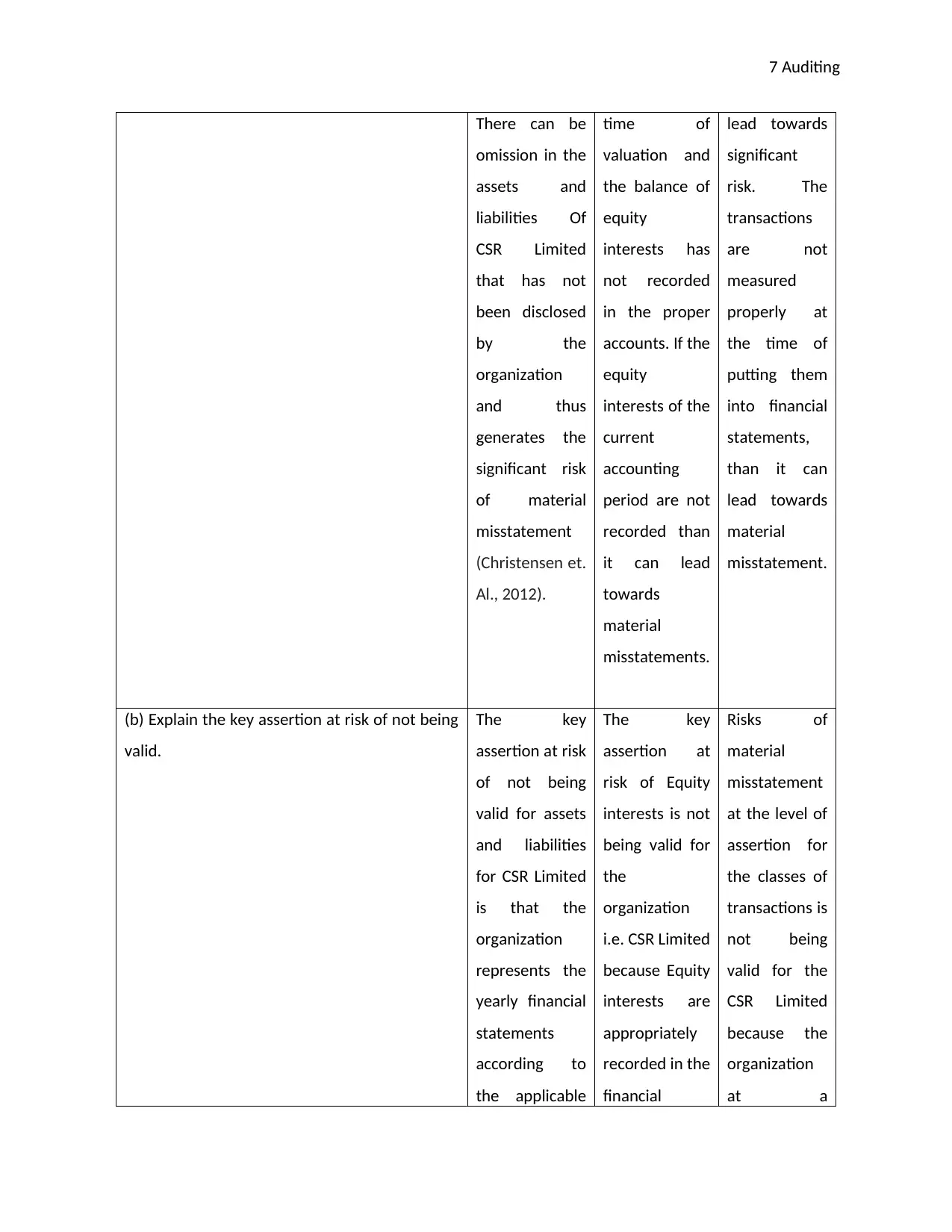

There can be

omission in the

assets and

liabilities Of

CSR Limited

that has not

been disclosed

by the

organization

and thus

generates the

significant risk

of material

misstatement

(Christensen et.

Al., 2012).

time of

valuation and

the balance of

equity

interests has

not recorded

in the proper

accounts. If the

equity

interests of the

current

accounting

period are not

recorded than

it can lead

towards

material

misstatements.

lead towards

significant

risk. The

transactions

are not

measured

properly at

the time of

putting them

into financial

statements,

than it can

lead towards

material

misstatement.

(b) Explain the key assertion at risk of not being

valid.

The key

assertion at risk

of not being

valid for assets

and liabilities

for CSR Limited

is that the

organization

represents the

yearly financial

statements

according to

the applicable

The key

assertion at

risk of Equity

interests is not

being valid for

the

organization

i.e. CSR Limited

because Equity

interests are

appropriately

recorded in the

financial

Risks of

material

misstatement

at the level of

assertion for

the classes of

transactions is

not being

valid for the

CSR Limited

because the

organization

at a

There can be

omission in the

assets and

liabilities Of

CSR Limited

that has not

been disclosed

by the

organization

and thus

generates the

significant risk

of material

misstatement

(Christensen et.

Al., 2012).

time of

valuation and

the balance of

equity

interests has

not recorded

in the proper

accounts. If the

equity

interests of the

current

accounting

period are not

recorded than

it can lead

towards

material

misstatements.

lead towards

significant

risk. The

transactions

are not

measured

properly at

the time of

putting them

into financial

statements,

than it can

lead towards

material

misstatement.

(b) Explain the key assertion at risk of not being

valid.

The key

assertion at risk

of not being

valid for assets

and liabilities

for CSR Limited

is that the

organization

represents the

yearly financial

statements

according to

the applicable

The key

assertion at

risk of Equity

interests is not

being valid for

the

organization

i.e. CSR Limited

because Equity

interests are

appropriately

recorded in the

financial

Risks of

material

misstatement

at the level of

assertion for

the classes of

transactions is

not being

valid for the

CSR Limited

because the

organization

at a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8 Auditing

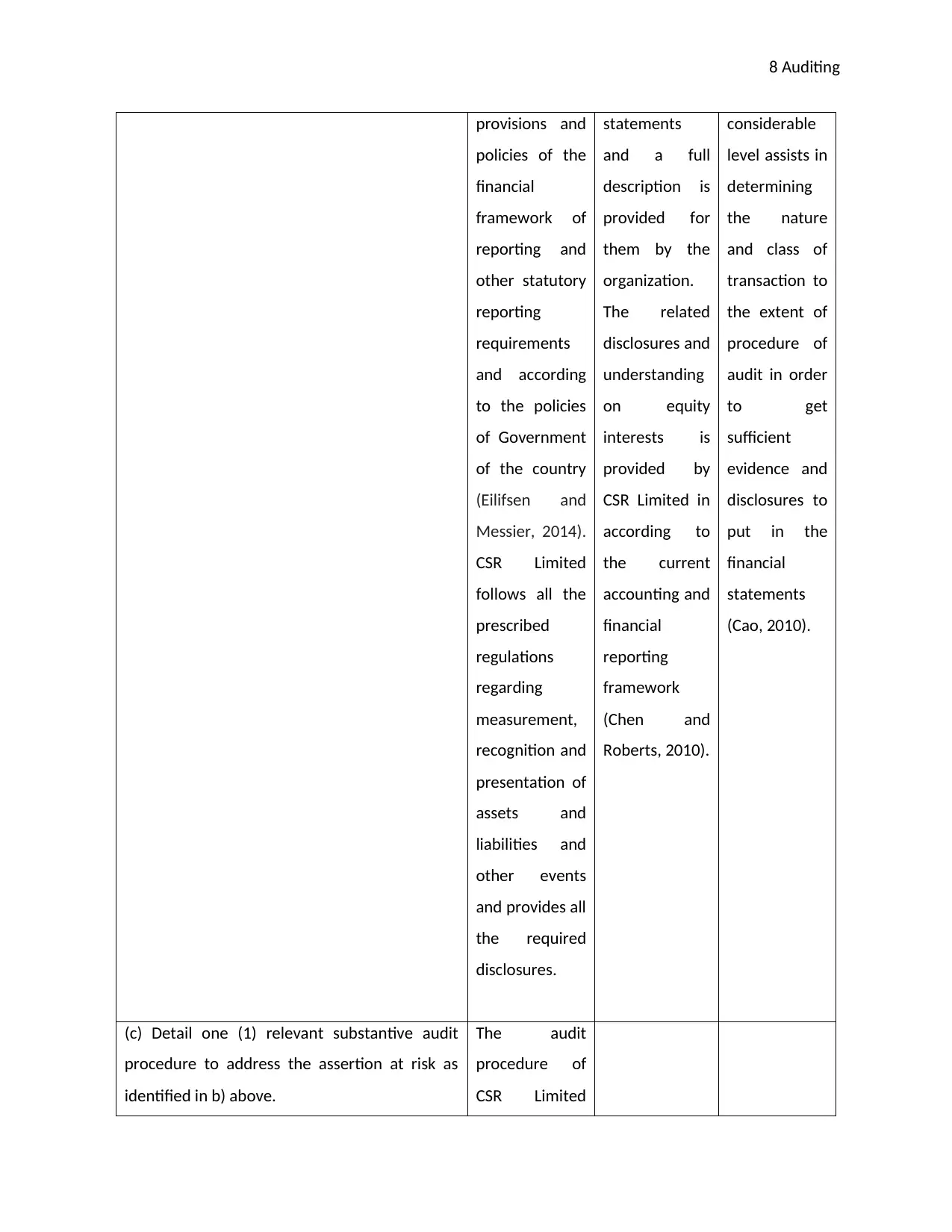

provisions and

policies of the

financial

framework of

reporting and

other statutory

reporting

requirements

and according

to the policies

of Government

of the country

(Eilifsen and

Messier, 2014).

CSR Limited

follows all the

prescribed

regulations

regarding

measurement,

recognition and

presentation of

assets and

liabilities and

other events

and provides all

the required

disclosures.

statements

and a full

description is

provided for

them by the

organization.

The related

disclosures and

understanding

on equity

interests is

provided by

CSR Limited in

according to

the current

accounting and

financial

reporting

framework

(Chen and

Roberts, 2010).

considerable

level assists in

determining

the nature

and class of

transaction to

the extent of

procedure of

audit in order

to get

sufficient

evidence and

disclosures to

put in the

financial

statements

(Cao, 2010).

(c) Detail one (1) relevant substantive audit

procedure to address the assertion at risk as

identified in b) above.

The audit

procedure of

CSR Limited

provisions and

policies of the

financial

framework of

reporting and

other statutory

reporting

requirements

and according

to the policies

of Government

of the country

(Eilifsen and

Messier, 2014).

CSR Limited

follows all the

prescribed

regulations

regarding

measurement,

recognition and

presentation of

assets and

liabilities and

other events

and provides all

the required

disclosures.

statements

and a full

description is

provided for

them by the

organization.

The related

disclosures and

understanding

on equity

interests is

provided by

CSR Limited in

according to

the current

accounting and

financial

reporting

framework

(Chen and

Roberts, 2010).

considerable

level assists in

determining

the nature

and class of

transaction to

the extent of

procedure of

audit in order

to get

sufficient

evidence and

disclosures to

put in the

financial

statements

(Cao, 2010).

(c) Detail one (1) relevant substantive audit

procedure to address the assertion at risk as

identified in b) above.

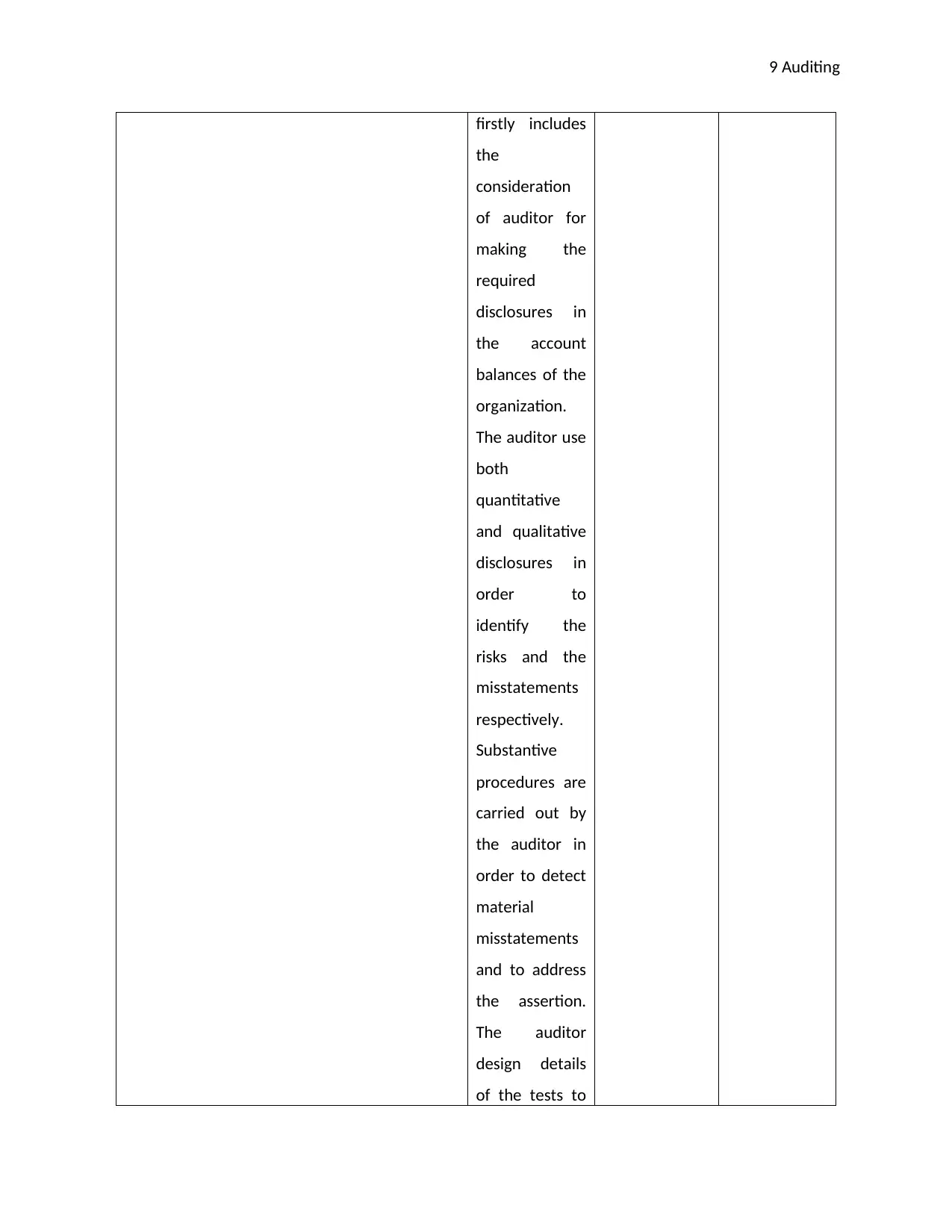

The audit

procedure of

CSR Limited

9 Auditing

firstly includes

the

consideration

of auditor for

making the

required

disclosures in

the account

balances of the

organization.

The auditor use

both

quantitative

and qualitative

disclosures in

order to

identify the

risks and the

misstatements

respectively.

Substantive

procedures are

carried out by

the auditor in

order to detect

material

misstatements

and to address

the assertion.

The auditor

design details

of the tests to

firstly includes

the

consideration

of auditor for

making the

required

disclosures in

the account

balances of the

organization.

The auditor use

both

quantitative

and qualitative

disclosures in

order to

identify the

risks and the

misstatements

respectively.

Substantive

procedures are

carried out by

the auditor in

order to detect

material

misstatements

and to address

the assertion.

The auditor

design details

of the tests to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10 Auditing

be undertaken

in order to

assess the risk

with the major

objective of

getting relevant

evidence for

the audit

procedure. This

will help the

auditor to

achieve

planned level

of assurance at

the assertion

level. In

designing the

substantive

procedure

regarding

existence of

assertion, the

auditor selects

various items

and

transactions

from the

financials of the

organization

and thus

obtains the

audit which can

be undertaken

in order to

assess the risk

with the major

objective of

getting relevant

evidence for

the audit

procedure. This

will help the

auditor to

achieve

planned level

of assurance at

the assertion

level. In

designing the

substantive

procedure

regarding

existence of

assertion, the

auditor selects

various items

and

transactions

from the

financials of the

organization

and thus

obtains the

audit which can

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11 Auditing

be considered

relevant. In

designing an

audit

procedure and

to get a

complete

assertion at risk

of

misstatement,

the auditor

investigates

different items

of the financial

items and their

reasonability

on inclusion in

the financial

statements

(Margret and

Hoque, 2016)

The nature and

extent of the

substantive

audit

procedure

depends on the

financial

reporting

complications

of the

organization

be considered

relevant. In

designing an

audit

procedure and

to get a

complete

assertion at risk

of

misstatement,

the auditor

investigates

different items

of the financial

items and their

reasonability

on inclusion in

the financial

statements

(Margret and

Hoque, 2016)

The nature and

extent of the

substantive

audit

procedure

depends on the

financial

reporting

complications

of the

organization

12 Auditing

and the risk

associated with

material

misstatement.

(d) Detail one (1) relevant practical internal

control that would mitigate the risk in relation

to the assertion at risk as identified in b) above.

Communication

and

enforcement of

integrity and

ethical values is

one of the

practical

internal

controls that

would help in

mitigation of

the risk in

relation to the

assertion at

risk. Integrity

and ethical

behaviour of

the individuals

in the

organization

brings the

effectiveness in

the control

system will

help the

organization.

The

and the risk

associated with

material

misstatement.

(d) Detail one (1) relevant practical internal

control that would mitigate the risk in relation

to the assertion at risk as identified in b) above.

Communication

and

enforcement of

integrity and

ethical values is

one of the

practical

internal

controls that

would help in

mitigation of

the risk in

relation to the

assertion at

risk. Integrity

and ethical

behaviour of

the individuals

in the

organization

brings the

effectiveness in

the control

system will

help the

organization.

The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.