Financial Accounting Report: Stakeholders, Final Accounts, Tasks

VerifiedAdded on 2023/01/06

|22

|3838

|29

Report

AI Summary

This report delves into the core concepts of financial accounting, emphasizing its role in tracking and interpreting an organization's financial transactions. It explores the purpose of financial accounting, including the preparation of financial statements like profit and loss accounts and balance sheets. The report is divided into two main tasks. The first task defines financial accounting, outlines its characteristics, and examines the roles of various stakeholders, both internal (owners, management) and external (investors, government, creditors, society). The second task focuses on practical application, demonstrating the double-entry accounting system, the preparation of final accounts, and the understanding of bank reconciliation statements and suspense accounts. The report provides detailed examples and practical applications to enhance the understanding of financial accounting principles.

Financial Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1. Financial accounting...............................................................................................................3

2. Stakeholder..............................................................................................................................6

TASK 2............................................................................................................................................8

Client 1........................................................................................................................................8

Client 2......................................................................................................................................12

Client 2......................................................................................................................................16

Client 4......................................................................................................................................17

Client 5......................................................................................................................................18

2

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1. Financial accounting...............................................................................................................3

2. Stakeholder..............................................................................................................................6

TASK 2............................................................................................................................................8

Client 1........................................................................................................................................8

Client 2......................................................................................................................................12

Client 2......................................................................................................................................16

Client 4......................................................................................................................................17

Client 5......................................................................................................................................18

2

INTRODUCTION

Financial accounting is a specialized branch of accounting whose focal point is on

tracking organization's financial transactions. Financial accounting is a routine schedule of every

organisation. It is a very important branch of accounting as mere doing business is not enough

for an organisation, to see, whether, the efforts are directed into right direction or not is also

essential (Baker and Burlaud, 2015). This check on the efforts of organisation and its employees

is done by the application of financial accounting. This involves preparation of financial

statements like profit and loss account for determining profits earned by company in current year

and it also includes balance sheet, which is a detailed statement of company's financial position.

This report is divided into two tasks. First task explains about concept of financial accounting

and its purpose. It also shows light upon stakeholders of a large organisation. Second part is

focused upon the practical part to develop an understanding of double entry accounting system

and preparation of final accounts. Further understanding of bank reconciliation statement and

suspense account is developed in this report.

TASK 1

1. Financial accounting

It is defined as the process of recording, classifying, summarizing, interpreting and

reporting of financial data of a business. This process utilizes different accounting principles

which are established by regulating authorities. Use of financial accounting makes accounting of

every organisation world wide common. The data used in financial accounting is categorized

under five different heads that are incomes, expenditures, assets, liabilities and capital (or

equity). There is different accounting treatment for every item which is in accordance of

established accounting principles and policies followed in organisation. The basic purpose of

financial accounting is to ascertain profits or losses of a specified period, to ascertain financial

position of business (Barker, 2015). From above explanation, following characteristics of

financial accounting can be drawn:

Recording: This refers to the process of recording of transactions that can be measured

in monetary terms, soon after they are occurred in books of accounts. Transactions are

recorded in journal.

3

Financial accounting is a specialized branch of accounting whose focal point is on

tracking organization's financial transactions. Financial accounting is a routine schedule of every

organisation. It is a very important branch of accounting as mere doing business is not enough

for an organisation, to see, whether, the efforts are directed into right direction or not is also

essential (Baker and Burlaud, 2015). This check on the efforts of organisation and its employees

is done by the application of financial accounting. This involves preparation of financial

statements like profit and loss account for determining profits earned by company in current year

and it also includes balance sheet, which is a detailed statement of company's financial position.

This report is divided into two tasks. First task explains about concept of financial accounting

and its purpose. It also shows light upon stakeholders of a large organisation. Second part is

focused upon the practical part to develop an understanding of double entry accounting system

and preparation of final accounts. Further understanding of bank reconciliation statement and

suspense account is developed in this report.

TASK 1

1. Financial accounting

It is defined as the process of recording, classifying, summarizing, interpreting and

reporting of financial data of a business. This process utilizes different accounting principles

which are established by regulating authorities. Use of financial accounting makes accounting of

every organisation world wide common. The data used in financial accounting is categorized

under five different heads that are incomes, expenditures, assets, liabilities and capital (or

equity). There is different accounting treatment for every item which is in accordance of

established accounting principles and policies followed in organisation. The basic purpose of

financial accounting is to ascertain profits or losses of a specified period, to ascertain financial

position of business (Barker, 2015). From above explanation, following characteristics of

financial accounting can be drawn:

Recording: This refers to the process of recording of transactions that can be measured

in monetary terms, soon after they are occurred in books of accounts. Transactions are

recorded in journal.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Classifying: It is concerned with the classification of the recorded data in a way that

similar nature of transactions are grouped under common head (Cooper, 2017).

Summarising: It is focused on presentation of classified data in a manner that is useful

for users. This step of financial accounting involves preparation of financial statements

such as profit and loss account, balance sheet, cash flow statement, etc.

Interpreting: After all above mentioned functions are performed, interpreting comes in

role, it means communication of results derived to managers after interpreting them.

This interpretation includes questions like (a) why it happened (b) what can happen in

coming time.

Financial accounting is an art and science as well: Accounting is an art as some of

the decisions are based on the personal judgement of accountant and it is a science as,

universally, books of accounts are prepared in similar nature based on accounting

principles that are followed by every accountant.

There are various branches under accounting, but they all differ in their functions and roles. In

order to explain above statement, difference between financial accounting and management

accounting is given below (Drew and Dollery, 2015):

Basis Financial accounting Management accounting

Meaning It refers to the mathematical

operations carried on raw monetary

data, in order to present them in a

systematic and meaningful manner.

It refers to the steps and analysis

conducted on results of operation of

financial accounting. This is done with

the purpose of obtaining assisting

source for strategy formulation.

Users Both internal and external users have

access to financial accounting. This

is given in annual reports of

company.

This is done only for the use of

internal users, as, it assists them to

plan for future course of actions.

Purpose of financial accounting: To keep systematic records- Financial accounting is performed with basic purpose of

maintaining systematic records. If accounting is not performed, than it will create a huge

4

similar nature of transactions are grouped under common head (Cooper, 2017).

Summarising: It is focused on presentation of classified data in a manner that is useful

for users. This step of financial accounting involves preparation of financial statements

such as profit and loss account, balance sheet, cash flow statement, etc.

Interpreting: After all above mentioned functions are performed, interpreting comes in

role, it means communication of results derived to managers after interpreting them.

This interpretation includes questions like (a) why it happened (b) what can happen in

coming time.

Financial accounting is an art and science as well: Accounting is an art as some of

the decisions are based on the personal judgement of accountant and it is a science as,

universally, books of accounts are prepared in similar nature based on accounting

principles that are followed by every accountant.

There are various branches under accounting, but they all differ in their functions and roles. In

order to explain above statement, difference between financial accounting and management

accounting is given below (Drew and Dollery, 2015):

Basis Financial accounting Management accounting

Meaning It refers to the mathematical

operations carried on raw monetary

data, in order to present them in a

systematic and meaningful manner.

It refers to the steps and analysis

conducted on results of operation of

financial accounting. This is done with

the purpose of obtaining assisting

source for strategy formulation.

Users Both internal and external users have

access to financial accounting. This

is given in annual reports of

company.

This is done only for the use of

internal users, as, it assists them to

plan for future course of actions.

Purpose of financial accounting: To keep systematic records- Financial accounting is performed with basic purpose of

maintaining systematic records. If accounting is not performed, than it will create a huge

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

burden on administration mind and in most cases it will lead to failure of business

operations. To protect business properties- Financial accounting provides safety to business

properties from unjustified use. This is possible because managers keeps a check in

particulars like amount of funds invested in business, amount of debt and credit on

organisation, various information like amount of fixed assets, cash in hand, WIP, amount

of finished goods, stock of raw material, activities that generate greater profits, etc. these

all information helps manager to assure that funds are not kept idle or underutilised (Fall

and Fournier, 2015). To determine amount of profit or losses- Main purpose of financial accounting is to

ascertain profits and losses of business. This function is performed by keeping a proper

record of incomes and expenditures relating to a specific period of time. If income

exceeds expenditures than it is profit on account of business and in the opposite case, it is

loss. This function is performed by preparing profit and loss account and this account

help managers, investors and every stakeholder to know about the profitability of

business. In case, there are losses for consecutive periods, than managers can take

required investigating steps in order to ascertain reasons for these losses. To ascertain financial position: Financial position refers to where the business actually

stands, what it owns and owes? This objective is served by Balance sheet. It is a detailed

statement of assets and liabilities of business on a particular date, generally, the last date

of specific period of time. It acts as barometer of financial health of organisation. Various

analysis tests are conducted on this statement only, which further leads to generation of

information which are useful for the task of strategy formulation. This is an important

task to perform as mere calculation of profit is not enough, as it can produce a vague

picture, and it can become clear only on preparation of Balance sheet (Flower and

Ebbers, 2018) . Facilitate rational decision making- Financial accounting serves as assistance tool for

managers in decision making, as, the results generated by final accounts are used as data

for comparing performance of firm with other firms in the industry. This comparison

makes it easy for managers to take decisions about future course of actions. If the

evaluation is not made proper, than results obtained will be vague, hence, decisions will

5

operations. To protect business properties- Financial accounting provides safety to business

properties from unjustified use. This is possible because managers keeps a check in

particulars like amount of funds invested in business, amount of debt and credit on

organisation, various information like amount of fixed assets, cash in hand, WIP, amount

of finished goods, stock of raw material, activities that generate greater profits, etc. these

all information helps manager to assure that funds are not kept idle or underutilised (Fall

and Fournier, 2015). To determine amount of profit or losses- Main purpose of financial accounting is to

ascertain profits and losses of business. This function is performed by keeping a proper

record of incomes and expenditures relating to a specific period of time. If income

exceeds expenditures than it is profit on account of business and in the opposite case, it is

loss. This function is performed by preparing profit and loss account and this account

help managers, investors and every stakeholder to know about the profitability of

business. In case, there are losses for consecutive periods, than managers can take

required investigating steps in order to ascertain reasons for these losses. To ascertain financial position: Financial position refers to where the business actually

stands, what it owns and owes? This objective is served by Balance sheet. It is a detailed

statement of assets and liabilities of business on a particular date, generally, the last date

of specific period of time. It acts as barometer of financial health of organisation. Various

analysis tests are conducted on this statement only, which further leads to generation of

information which are useful for the task of strategy formulation. This is an important

task to perform as mere calculation of profit is not enough, as it can produce a vague

picture, and it can become clear only on preparation of Balance sheet (Flower and

Ebbers, 2018) . Facilitate rational decision making- Financial accounting serves as assistance tool for

managers in decision making, as, the results generated by final accounts are used as data

for comparing performance of firm with other firms in the industry. This comparison

makes it easy for managers to take decisions about future course of actions. If the

evaluation is not made proper, than results obtained will be vague, hence, decisions will

5

not be taken in correct manner. These decisions relates to matters like, depreciation

policy, disposal of some obsolete asset, etc.

Information system: Financial accounting play role of information system as well having

role of collecting and communicating information about organisation. This collected

information helps administration to take suitable and required decisions (García‐Sánchez

and Noguera‐Gámez, 2017).

2. Stakeholder

The main objective of financial accounting is to furnish users (inside and outside of

organisation) with information relating to financial transactions and position of business. Users

of this information can be classified into two categories i.e. internal and external users. These

users are often termed as stakeholders.

Internal stakeholders: These are persons or groups who are present within the

organisation. They are using this information for separate reasons, some of them are explained

below: Owners: They are prime users of accounting data, as they only provide funds for

operations of organisation, therefore, they need to know whether their money is being

properly utilised or not. They are interested in knowing about profitability and financial

position of business. As already discusses, it is main focus of financial accounting to

prepare final accounts of organisation, which generate related results (Keil, 2016).

Management: Main task of management is to getting work done through others, and to

ensure that its sub ordinates are working properly or not. Financial accounting provides

an aid in this matter by providing them with monitoring performance of employees.

Actual performance is compared with desired performance that management was

expecting out of them. Important roles of management includes planning and controlling.

Planning is done with the help of preparation of various budgets. Controlling is

performed with assistance of calculation of variances between actual figures and

budgeted figures. Accounting information is useful in fixing appropriate selling prices.

Over/ under fixation of prices may lead to failure of product as, over fixation will not

attract customers and under fixation will lead to losses due to price not covering the cost

also. Thus, appropriate fixation of price is necessary.

6

policy, disposal of some obsolete asset, etc.

Information system: Financial accounting play role of information system as well having

role of collecting and communicating information about organisation. This collected

information helps administration to take suitable and required decisions (García‐Sánchez

and Noguera‐Gámez, 2017).

2. Stakeholder

The main objective of financial accounting is to furnish users (inside and outside of

organisation) with information relating to financial transactions and position of business. Users

of this information can be classified into two categories i.e. internal and external users. These

users are often termed as stakeholders.

Internal stakeholders: These are persons or groups who are present within the

organisation. They are using this information for separate reasons, some of them are explained

below: Owners: They are prime users of accounting data, as they only provide funds for

operations of organisation, therefore, they need to know whether their money is being

properly utilised or not. They are interested in knowing about profitability and financial

position of business. As already discusses, it is main focus of financial accounting to

prepare final accounts of organisation, which generate related results (Keil, 2016).

Management: Main task of management is to getting work done through others, and to

ensure that its sub ordinates are working properly or not. Financial accounting provides

an aid in this matter by providing them with monitoring performance of employees.

Actual performance is compared with desired performance that management was

expecting out of them. Important roles of management includes planning and controlling.

Planning is done with the help of preparation of various budgets. Controlling is

performed with assistance of calculation of variances between actual figures and

budgeted figures. Accounting information is useful in fixing appropriate selling prices.

Over/ under fixation of prices may lead to failure of product as, over fixation will not

attract customers and under fixation will lead to losses due to price not covering the cost

also. Thus, appropriate fixation of price is necessary.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

External stakeholders: These are group or persons who are outside the company but are

indirectly interested in its accounting information. Following are some examples of external

stakeholders. Investors: These are persons who invests in organisation and are interested in knowing

financial position of organisation to know that their money is in safe hands or not. They

are interested to know that whether the returns are in accordance of what they expected

or not. Future investment decisions are dependent upon accounting results of financial

statements like EPS, net profit, etc. Government: Central and state governments both are interested in accounting

information of organisation due to their own reasons. Some of the reason of interest are

taxation records. They also need accounting information due to compiling statistics

related to business which are needed for compiling national accounts. Creditors: Company owes some money to certain parties (eg.- supplier of raw material,

bankers, or other lenders of money). They are interested in accounting information due

to reason as they want to be ensured about creditworthiness of organisation. If prior

calculations and investigation is not done by creditors, than it may lead to their bad debts

as company does not hold that position in which it will be capable of returning debts. Society: Society as a whole wants to review accounting information of company, for

wanting to know whether that company is fulfilling its responsibility towards society or

not (Eg.- CSR). This will be an important tool in establishing good position among

society and targeted customers (Küpper and Pedell, 2016).

7

indirectly interested in its accounting information. Following are some examples of external

stakeholders. Investors: These are persons who invests in organisation and are interested in knowing

financial position of organisation to know that their money is in safe hands or not. They

are interested to know that whether the returns are in accordance of what they expected

or not. Future investment decisions are dependent upon accounting results of financial

statements like EPS, net profit, etc. Government: Central and state governments both are interested in accounting

information of organisation due to their own reasons. Some of the reason of interest are

taxation records. They also need accounting information due to compiling statistics

related to business which are needed for compiling national accounts. Creditors: Company owes some money to certain parties (eg.- supplier of raw material,

bankers, or other lenders of money). They are interested in accounting information due

to reason as they want to be ensured about creditworthiness of organisation. If prior

calculations and investigation is not done by creditors, than it may lead to their bad debts

as company does not hold that position in which it will be capable of returning debts. Society: Society as a whole wants to review accounting information of company, for

wanting to know whether that company is fulfilling its responsibility towards society or

not (Eg.- CSR). This will be an important tool in establishing good position among

society and targeted customers (Küpper and Pedell, 2016).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

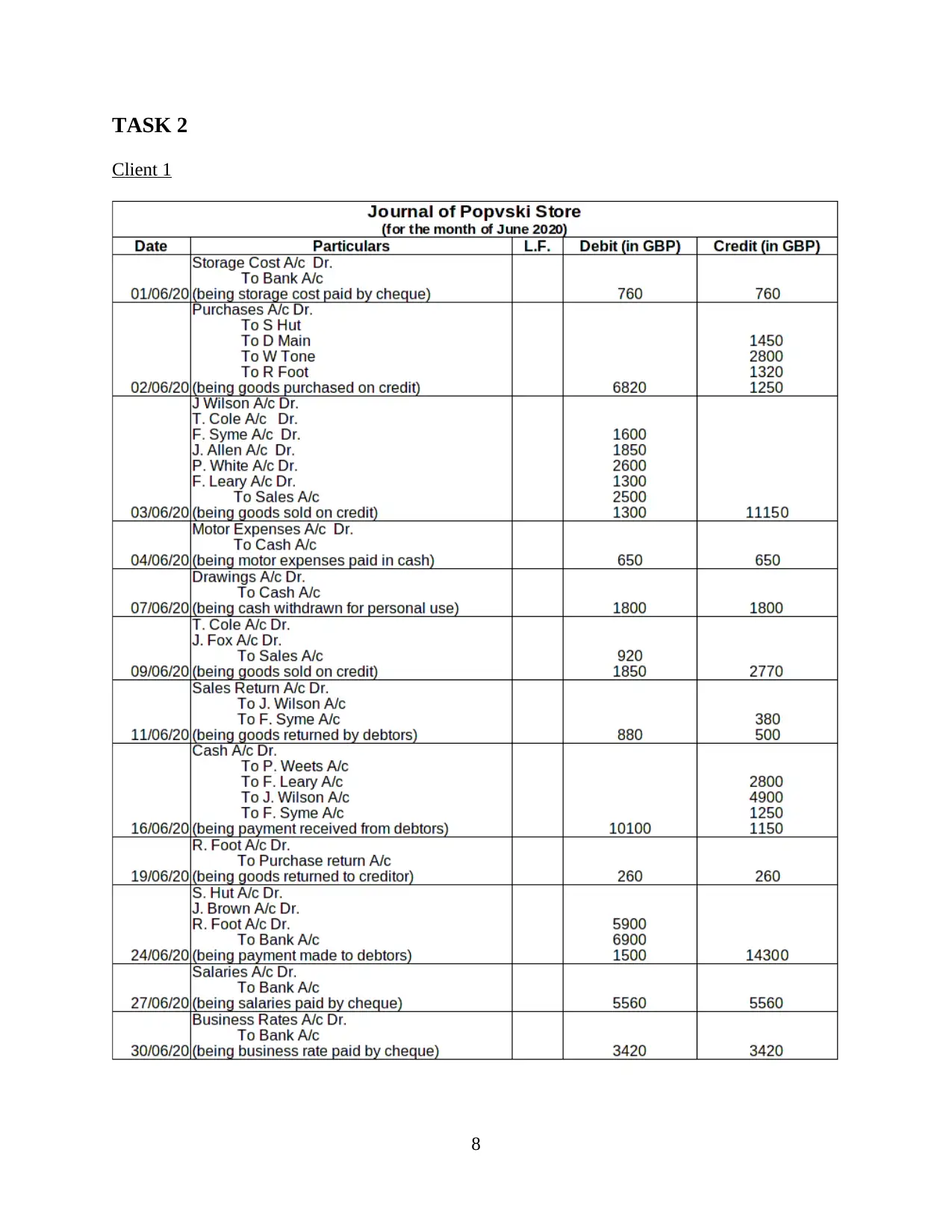

TASK 2

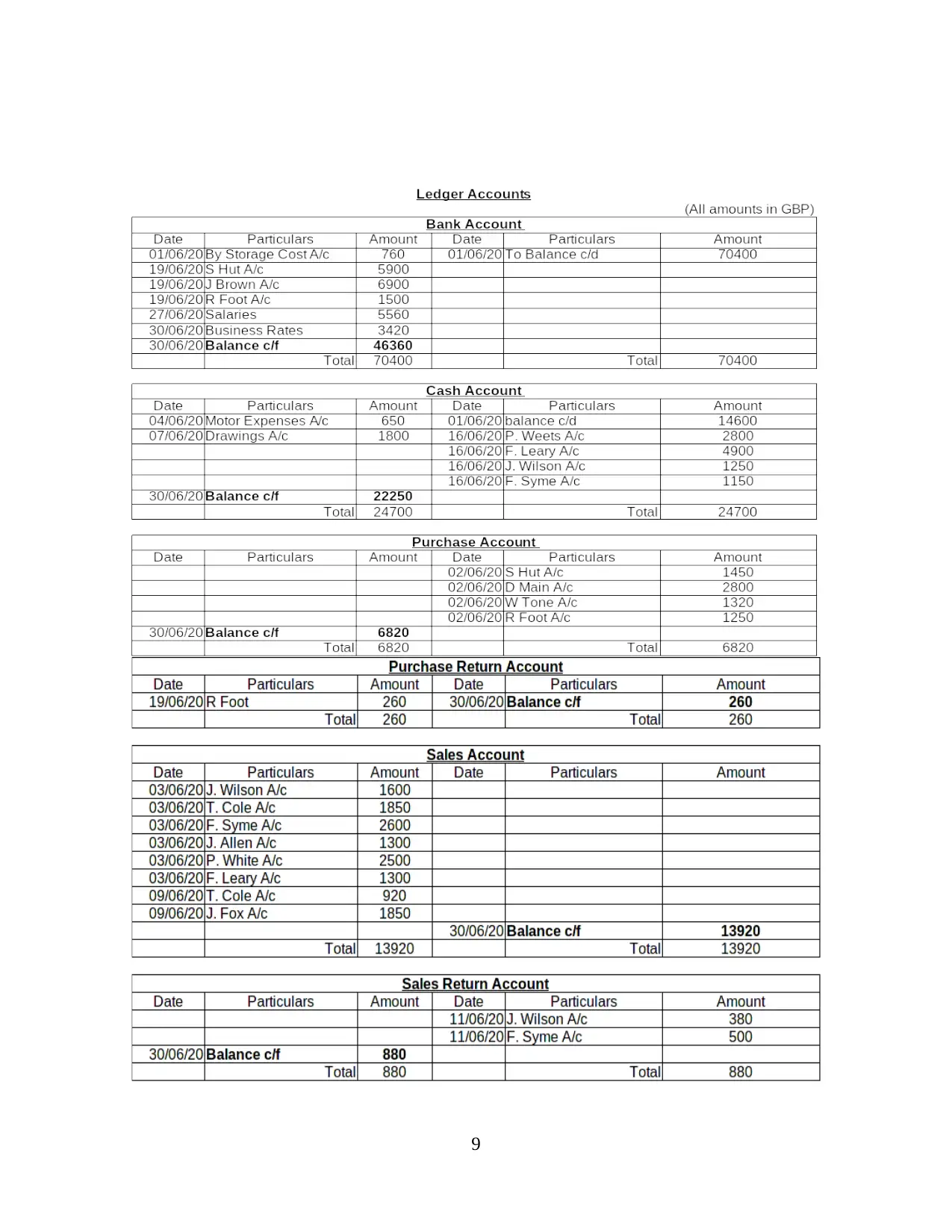

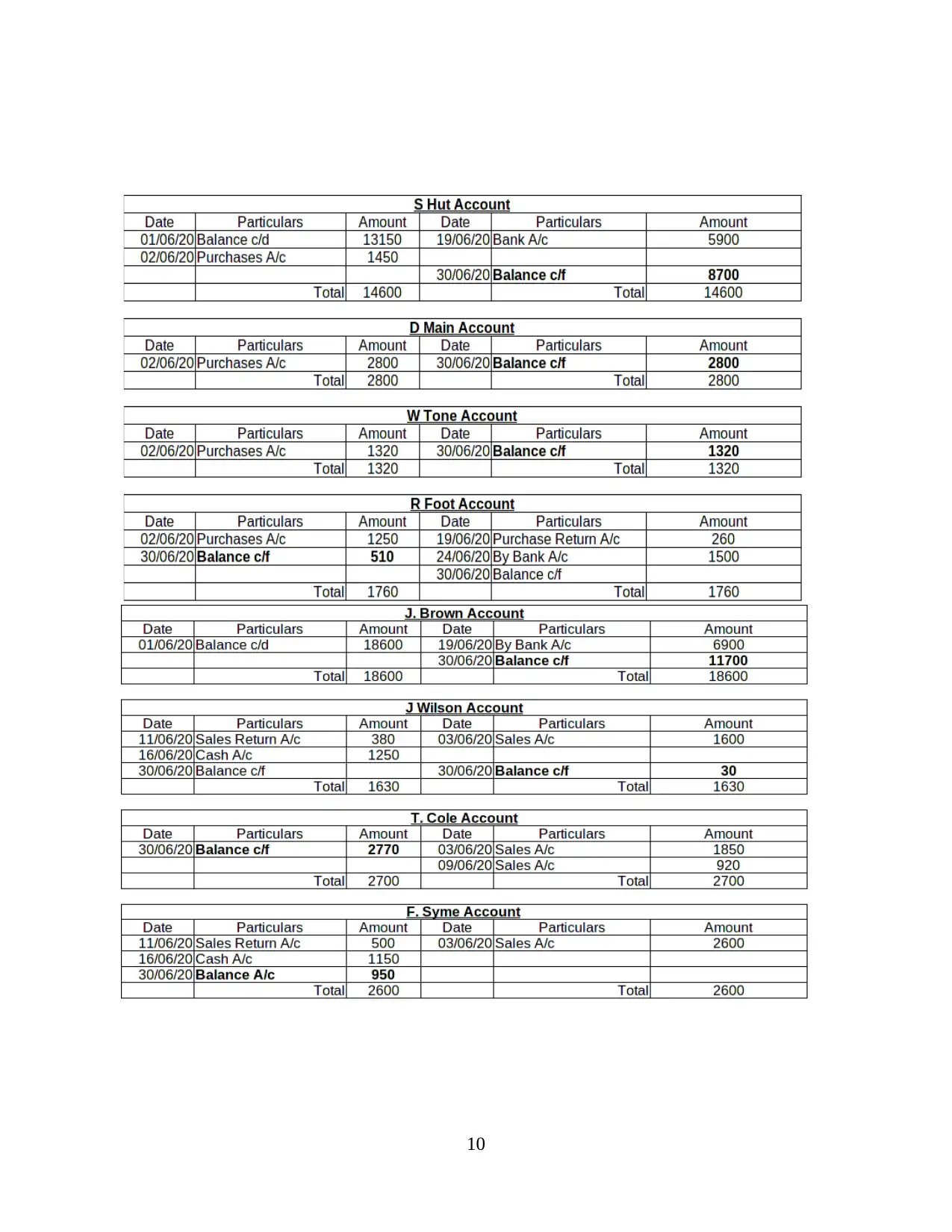

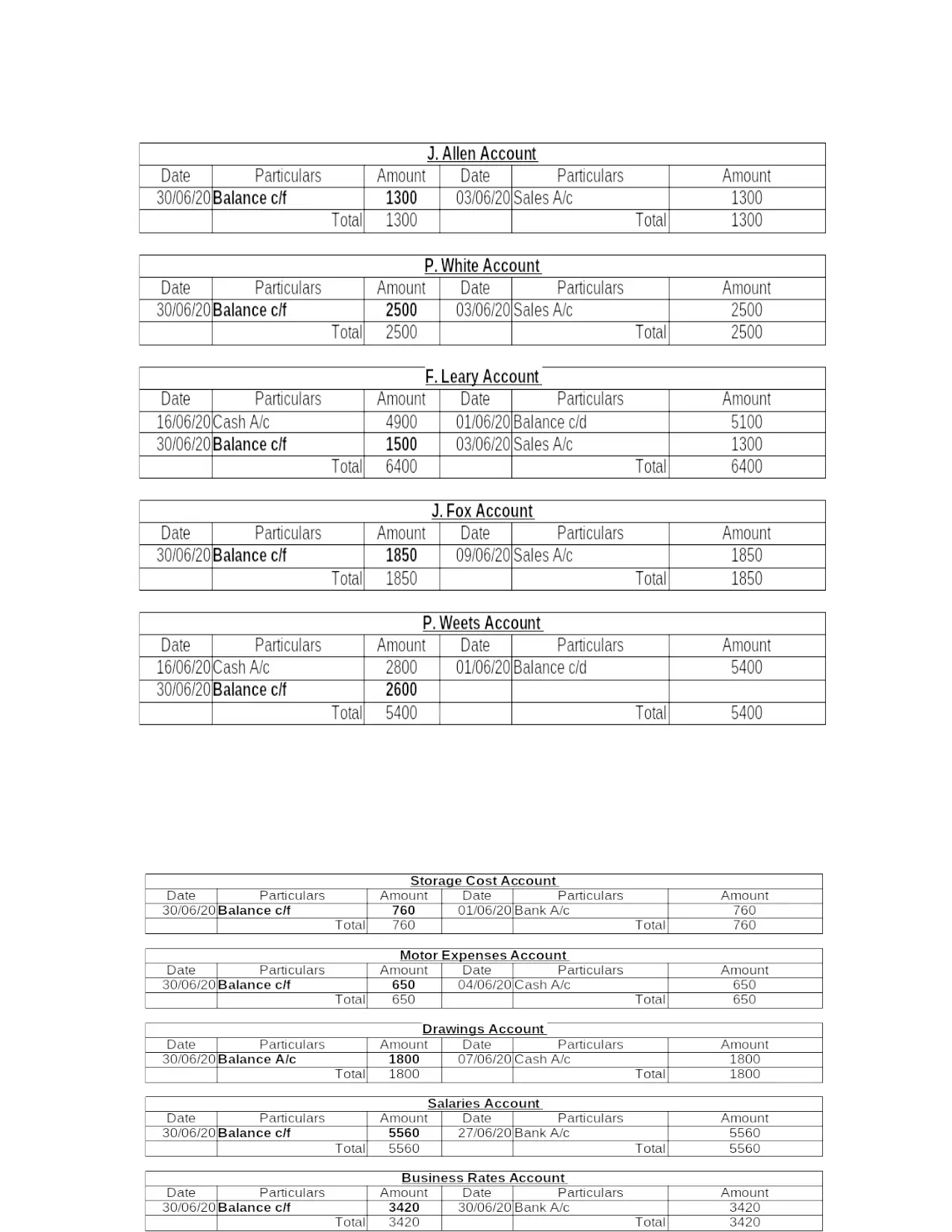

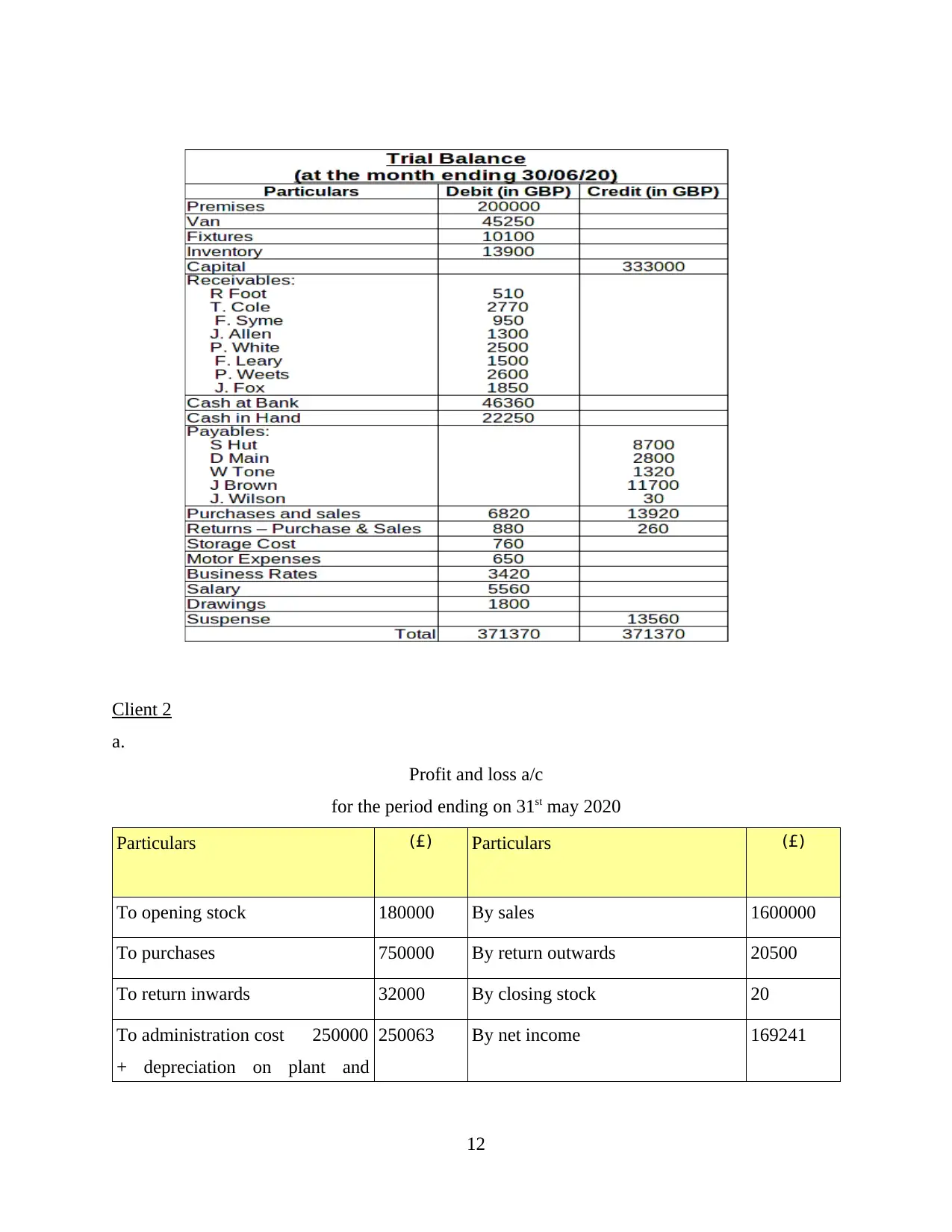

Client 1

8

Client 1

8

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

Client 2

a.

Profit and loss a/c

for the period ending on 31st may 2020

Particulars (£) Particulars (£)

To opening stock 180000 By sales 1600000

To purchases 750000 By return outwards 20500

To return inwards 32000 By closing stock 20

To administration cost 250000

+ depreciation on plant and

250063 By net income 169241

12

a.

Profit and loss a/c

for the period ending on 31st may 2020

Particulars (£) Particulars (£)

To opening stock 180000 By sales 1600000

To purchases 750000 By return outwards 20500

To return inwards 32000 By closing stock 20

To administration cost 250000

+ depreciation on plant and

250063 By net income 169241

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.