Corporate Finance Information 2022

VerifiedAdded on 2022/09/28

|10

|2684

|23

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running Head: CORPORATE FINANCE 1

CORPORATE FINANCE

CORPORATE FINANCE

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Running Head: CORPORATE FINANCE

Table of Contents

1 Investment Decision.....................................................................................................................3

Shareholder’s net worth...............................................................................................................3

Reasoning.....................................................................................................................................3

2) Fundamental financial concepts..................................................................................................4

Concept of agency relationship....................................................................................................4

Concept of Market Efficiency......................................................................................................5

Concept of Assert pricing............................................................................................................6

3) Debt Financing............................................................................................................................6

4) Bond Valuations..........................................................................................................................6

A...................................................................................................................................................6

B...................................................................................................................................................6

C...................................................................................................................................................6

D...................................................................................................................................................6

E...................................................................................................................................................7

5) Bond Duration.............................................................................................................................7

A...................................................................................................................................................7

B...................................................................................................................................................7

C...................................................................................................................................................8

References......................................................................................................................................10

Table of Contents

1 Investment Decision.....................................................................................................................3

Shareholder’s net worth...............................................................................................................3

Reasoning.....................................................................................................................................3

2) Fundamental financial concepts..................................................................................................4

Concept of agency relationship....................................................................................................4

Concept of Market Efficiency......................................................................................................5

Concept of Assert pricing............................................................................................................6

3) Debt Financing............................................................................................................................6

4) Bond Valuations..........................................................................................................................6

A...................................................................................................................................................6

B...................................................................................................................................................6

C...................................................................................................................................................6

D...................................................................................................................................................6

E...................................................................................................................................................7

5) Bond Duration.............................................................................................................................7

A...................................................................................................................................................7

B...................................................................................................................................................7

C...................................................................................................................................................8

References......................................................................................................................................10

Running Head: CORPORATE FINANCE

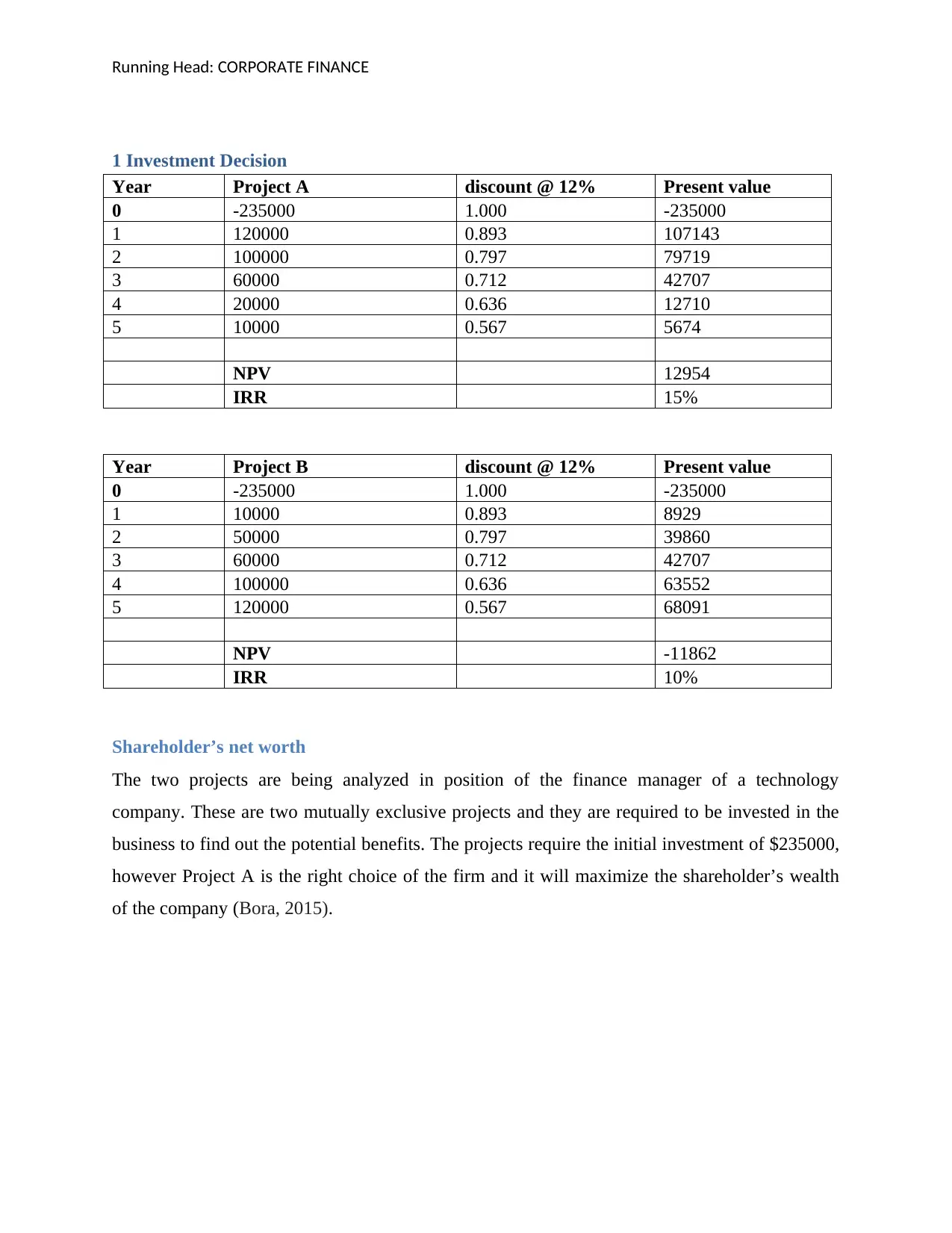

1 Investment Decision

Year Project A discount @ 12% Present value

0 -235000 1.000 -235000

1 120000 0.893 107143

2 100000 0.797 79719

3 60000 0.712 42707

4 20000 0.636 12710

5 10000 0.567 5674

NPV 12954

IRR 15%

Year Project B discount @ 12% Present value

0 -235000 1.000 -235000

1 10000 0.893 8929

2 50000 0.797 39860

3 60000 0.712 42707

4 100000 0.636 63552

5 120000 0.567 68091

NPV -11862

IRR 10%

Shareholder’s net worth

The two projects are being analyzed in position of the finance manager of a technology

company. These are two mutually exclusive projects and they are required to be invested in the

business to find out the potential benefits. The projects require the initial investment of $235000,

however Project A is the right choice of the firm and it will maximize the shareholder’s wealth

of the company (Bora, 2015).

1 Investment Decision

Year Project A discount @ 12% Present value

0 -235000 1.000 -235000

1 120000 0.893 107143

2 100000 0.797 79719

3 60000 0.712 42707

4 20000 0.636 12710

5 10000 0.567 5674

NPV 12954

IRR 15%

Year Project B discount @ 12% Present value

0 -235000 1.000 -235000

1 10000 0.893 8929

2 50000 0.797 39860

3 60000 0.712 42707

4 100000 0.636 63552

5 120000 0.567 68091

NPV -11862

IRR 10%

Shareholder’s net worth

The two projects are being analyzed in position of the finance manager of a technology

company. These are two mutually exclusive projects and they are required to be invested in the

business to find out the potential benefits. The projects require the initial investment of $235000,

however Project A is the right choice of the firm and it will maximize the shareholder’s wealth

of the company (Bora, 2015).

Running Head: CORPORATE FINANCE

Reasoning

The relevant advantage while using the net present worth strategy is that it considers the

fundamental thought that a future dollar is worth not exactly a dollar today. In each period, the

money streams are limited by another time of capital expense. The NPV technique likewise

reveals to us whether a speculation will make an incentive for the organization or the financial

specialist, and by how much regarding dollars.

The NPV which is also termed as NPV states the difference between the present value of the

cash inflows and the present value of the cash outflows. The NPV of the company is calculated

with the help of the discounting factor. Here in this scenario the discounting factor @12%.

Generally the positive NPV is entertained as it is assumed that the present value of the company

is worthy more than the future dollars. In terms of the project A the NPV is $12954 and in case

of the proposal B the NPV tends to be negative at ($11862).

The IRR is the rate of the measurement of the investment which excludes the factors such as risk

free rate of return, cost of capital and various other financial. It is callused as discounted cash

flow rate of return as well. At this rate the NPV of all the cash flows will be equivalent to zero.

In case of the project A the IRR is 15% and it is greater than the cost of capital at 12% whereas

in case of the IRR for the project B, the rate is 10%. Clearly it states that the future possibilities

and the greater returns are present in the project A. Hence, the project A is the useful choice from

the point of view of the company and for its growth (Patrick and French, 2016).

2) Fundamental financial concepts

Concept of agency relationship

An agency relationship is a relationship is a relation between a principal and the agent where the

principal gives legal consent to the agent to act on the behalf of the principal. Hence it can also

be said that the relationship created between bot h the principal and the agent can be termed as

agency where the agent works on behalf of the principal. Thus the agency defines a clear

relationship between the principal and the agent where the agent has to perform several duties

and responsibilities no matter what the tasks are, the agent is given specified responsibilities

which he or she needs to be performing within the given framework.

Reasoning

The relevant advantage while using the net present worth strategy is that it considers the

fundamental thought that a future dollar is worth not exactly a dollar today. In each period, the

money streams are limited by another time of capital expense. The NPV technique likewise

reveals to us whether a speculation will make an incentive for the organization or the financial

specialist, and by how much regarding dollars.

The NPV which is also termed as NPV states the difference between the present value of the

cash inflows and the present value of the cash outflows. The NPV of the company is calculated

with the help of the discounting factor. Here in this scenario the discounting factor @12%.

Generally the positive NPV is entertained as it is assumed that the present value of the company

is worthy more than the future dollars. In terms of the project A the NPV is $12954 and in case

of the proposal B the NPV tends to be negative at ($11862).

The IRR is the rate of the measurement of the investment which excludes the factors such as risk

free rate of return, cost of capital and various other financial. It is callused as discounted cash

flow rate of return as well. At this rate the NPV of all the cash flows will be equivalent to zero.

In case of the project A the IRR is 15% and it is greater than the cost of capital at 12% whereas

in case of the IRR for the project B, the rate is 10%. Clearly it states that the future possibilities

and the greater returns are present in the project A. Hence, the project A is the useful choice from

the point of view of the company and for its growth (Patrick and French, 2016).

2) Fundamental financial concepts

Concept of agency relationship

An agency relationship is a relationship is a relation between a principal and the agent where the

principal gives legal consent to the agent to act on the behalf of the principal. Hence it can also

be said that the relationship created between bot h the principal and the agent can be termed as

agency where the agent works on behalf of the principal. Thus the agency defines a clear

relationship between the principal and the agent where the agent has to perform several duties

and responsibilities no matter what the tasks are, the agent is given specified responsibilities

which he or she needs to be performing within the given framework.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Running Head: CORPORATE FINANCE

The agency relationship may be of certain kinds such as authorization of the agent by the

principal to purchase or sell property, merchandise or to hire or fire certain individuals for the

organization. However, it shall be noted that in order to perform the agency functions between

the principal and the agent the principal should appoint such agent who are capable of

performing the legal undertaking given by the principal (Fenichel, et al 2016). The principal

agent relationship is also an explicit relationship between the agent and the principle where the

agent and the principal performs a written contract between each other which defines the

principal agent relationship as well as the duties and responsibilities of the principal as well as

the agent are also defines. There are two types of authority given by the principal to the agent

that is express and implied authority. Express authority is the authority given by the principal to

the agent that is the authority which is directed by the principal to the agent, in other words it is

an express order by the principal to the agent where the principal directs the agent how and

where the task can be completed in a given way. Implied authority is the authority which needs

to be completed by the agent to complete the express authority given by the principal. It can also

be said that the implied authority is the authority, where the agent takes all the necessary steps

with an intention to fulfill the purpose of agency given by the principal. However, in the agency

relationship there is also an obligation of allegiance between the principal and the agent, it states

that the principal and the agent both should avoid such a situation which harms the interest of

both the parties (Romaioli and Contarello, 2017.

Concept of Market Efficiency

Market efficiency projects a series of information regarding the price and all the other relevant

information of the investment. However there is no compulsion of equalization of the market

price of the investment and the true value of the investment, the errors in the market can be

treated as unbiased as such deviations can be treated as random where the market price can be

greater and lower than the actual true value and the price of the investment (Lipton, 2015).

The basic function of the market efficiency is that it helps in providing the maximum

opportunities to the purchaser of the investment and the sellers of the securities by restricting the

transaction costs. There are three degrees of the efficiency of the market that is the weak form,

the semi strong form and the strong form. The weak form of the efficiency basically assumes that

the last price has no effect on the upcoming rates. The semi strong form has the ability to adjust

The agency relationship may be of certain kinds such as authorization of the agent by the

principal to purchase or sell property, merchandise or to hire or fire certain individuals for the

organization. However, it shall be noted that in order to perform the agency functions between

the principal and the agent the principal should appoint such agent who are capable of

performing the legal undertaking given by the principal (Fenichel, et al 2016). The principal

agent relationship is also an explicit relationship between the agent and the principle where the

agent and the principal performs a written contract between each other which defines the

principal agent relationship as well as the duties and responsibilities of the principal as well as

the agent are also defines. There are two types of authority given by the principal to the agent

that is express and implied authority. Express authority is the authority given by the principal to

the agent that is the authority which is directed by the principal to the agent, in other words it is

an express order by the principal to the agent where the principal directs the agent how and

where the task can be completed in a given way. Implied authority is the authority which needs

to be completed by the agent to complete the express authority given by the principal. It can also

be said that the implied authority is the authority, where the agent takes all the necessary steps

with an intention to fulfill the purpose of agency given by the principal. However, in the agency

relationship there is also an obligation of allegiance between the principal and the agent, it states

that the principal and the agent both should avoid such a situation which harms the interest of

both the parties (Romaioli and Contarello, 2017.

Concept of Market Efficiency

Market efficiency projects a series of information regarding the price and all the other relevant

information of the investment. However there is no compulsion of equalization of the market

price of the investment and the true value of the investment, the errors in the market can be

treated as unbiased as such deviations can be treated as random where the market price can be

greater and lower than the actual true value and the price of the investment (Lipton, 2015).

The basic function of the market efficiency is that it helps in providing the maximum

opportunities to the purchaser of the investment and the sellers of the securities by restricting the

transaction costs. There are three degrees of the efficiency of the market that is the weak form,

the semi strong form and the strong form. The weak form of the efficiency basically assumes that

the last price has no effect on the upcoming rates. The semi strong form has the ability to adjust

Running Head: CORPORATE FINANCE

with the information available in the market hence there are lesser possibility of the investor to

get benefitted on the basis of such information. The strong form of efficiency reflect all forms of

facts and figures whether public or private where no investor even also the insider would able to

gain any profit (Hökkä, et al 2017).

Market productivity does not necessitate that the market cost be equivalent to genuine incentive

at every point of time. It is majorly concerned with the fair market cost which is more prominent

and not worthy enough until and unless the deviations are arbitrary.

The deviation or the variance from the true value implies that stocks can be overvalued or

undervalued at the same time and they are not correlated with chances observable variable. For

example, stocks with lower PE proportions ought to be no pretty much prone to underestimated

than stocks with high PE proportions (Caspar, Cleeremans and Haggard, 2015).

If the variations in the market are really worthy, it defines that even if the experts gather for the

particular understanding, they are not liable to have an option to figure out whether the stocks are

undervalued or overvalued by using any small venture.

Concept of Asset pricing

In financial economics the term asset pricing is termed as the formal treatment that is governed

by the two major principles. These two theories stems from general equilibrium asset pricing and

rational asset pricing. It is a concept which helps in the evaluation of the assets in the form of

return on investment of the assets, it generally describes the systematic risks and analyses the

expected returns of the assets. In other words it helps in the decision making process of the

investor whether to invest in such assert or not. It helps in studying how the financial price of the

asserts are being calculated which help the investors to share the risks between the other

investors as well as it also helps in moving capital to such individuals or to such persons who can

use such more productively (Fernando and Gunasekara, 2018).

The asset pricing is determines on the basis of the various models such as capital asset pricing

model which is generally used in taking the capital budgeting decisions. The Capital Asset

Pricing Model (CAPM) is a model that depicts the connection between the normal return and

danger of putting resources into a security. It demonstrates that the normal profit for a security is

with the information available in the market hence there are lesser possibility of the investor to

get benefitted on the basis of such information. The strong form of efficiency reflect all forms of

facts and figures whether public or private where no investor even also the insider would able to

gain any profit (Hökkä, et al 2017).

Market productivity does not necessitate that the market cost be equivalent to genuine incentive

at every point of time. It is majorly concerned with the fair market cost which is more prominent

and not worthy enough until and unless the deviations are arbitrary.

The deviation or the variance from the true value implies that stocks can be overvalued or

undervalued at the same time and they are not correlated with chances observable variable. For

example, stocks with lower PE proportions ought to be no pretty much prone to underestimated

than stocks with high PE proportions (Caspar, Cleeremans and Haggard, 2015).

If the variations in the market are really worthy, it defines that even if the experts gather for the

particular understanding, they are not liable to have an option to figure out whether the stocks are

undervalued or overvalued by using any small venture.

Concept of Asset pricing

In financial economics the term asset pricing is termed as the formal treatment that is governed

by the two major principles. These two theories stems from general equilibrium asset pricing and

rational asset pricing. It is a concept which helps in the evaluation of the assets in the form of

return on investment of the assets, it generally describes the systematic risks and analyses the

expected returns of the assets. In other words it helps in the decision making process of the

investor whether to invest in such assert or not. It helps in studying how the financial price of the

asserts are being calculated which help the investors to share the risks between the other

investors as well as it also helps in moving capital to such individuals or to such persons who can

use such more productively (Fernando and Gunasekara, 2018).

The asset pricing is determines on the basis of the various models such as capital asset pricing

model which is generally used in taking the capital budgeting decisions. The Capital Asset

Pricing Model (CAPM) is a model that depicts the connection between the normal return and

danger of putting resources into a security. It demonstrates that the normal profit for a security is

Running Head: CORPORATE FINANCE

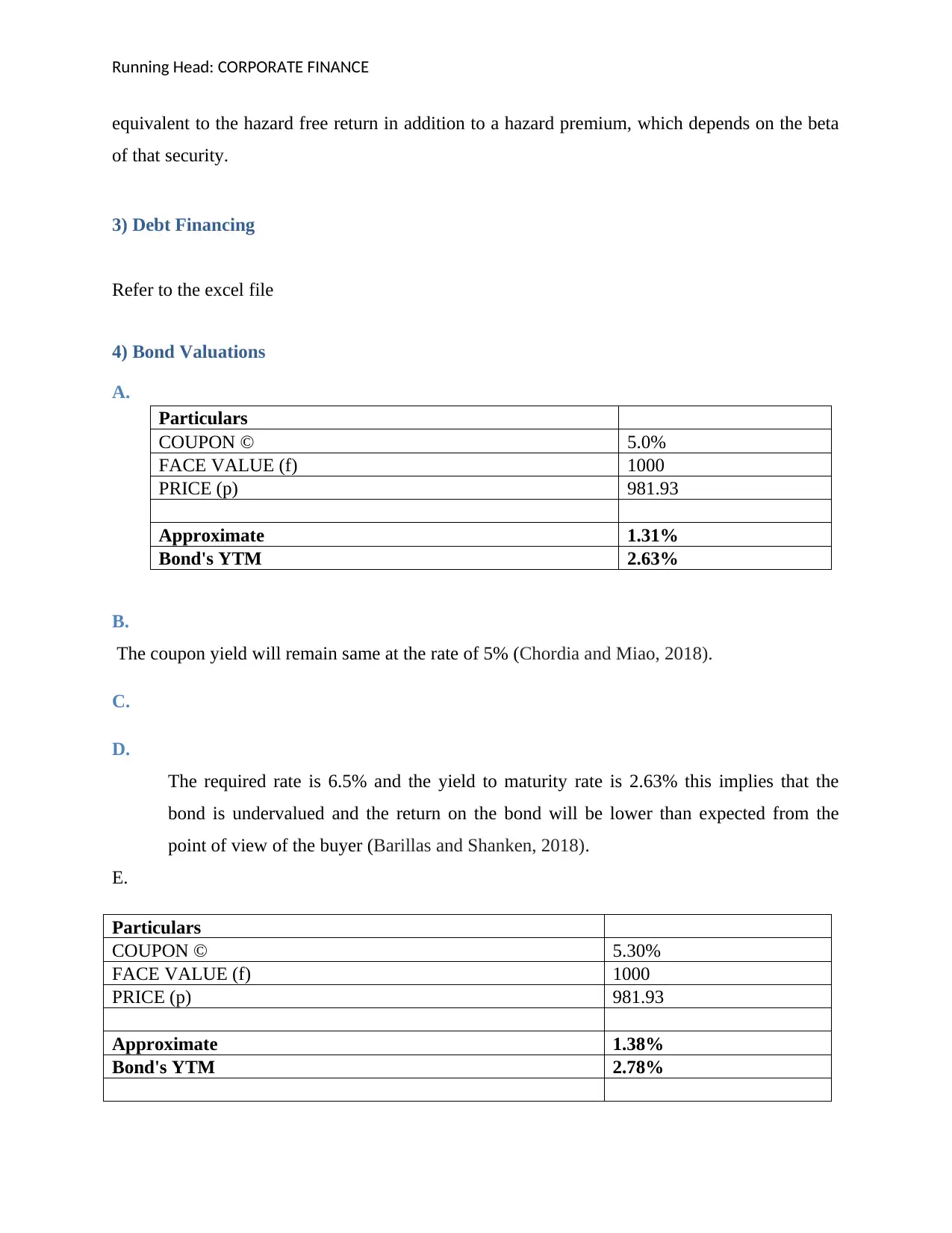

equivalent to the hazard free return in addition to a hazard premium, which depends on the beta

of that security.

3) Debt Financing

Refer to the excel file

4) Bond Valuations

A.

Particulars

COUPON © 5.0%

FACE VALUE (f) 1000

PRICE (p) 981.93

Approximate 1.31%

Bond's YTM 2.63%

B.

The coupon yield will remain same at the rate of 5% (Chordia and Miao, 2018).

C.

D.

The required rate is 6.5% and the yield to maturity rate is 2.63% this implies that the

bond is undervalued and the return on the bond will be lower than expected from the

point of view of the buyer (Barillas and Shanken, 2018).

E.

Particulars

COUPON © 5.30%

FACE VALUE (f) 1000

PRICE (p) 981.93

Approximate 1.38%

Bond's YTM 2.78%

equivalent to the hazard free return in addition to a hazard premium, which depends on the beta

of that security.

3) Debt Financing

Refer to the excel file

4) Bond Valuations

A.

Particulars

COUPON © 5.0%

FACE VALUE (f) 1000

PRICE (p) 981.93

Approximate 1.31%

Bond's YTM 2.63%

B.

The coupon yield will remain same at the rate of 5% (Chordia and Miao, 2018).

C.

D.

The required rate is 6.5% and the yield to maturity rate is 2.63% this implies that the

bond is undervalued and the return on the bond will be lower than expected from the

point of view of the buyer (Barillas and Shanken, 2018).

E.

Particulars

COUPON © 5.30%

FACE VALUE (f) 1000

PRICE (p) 981.93

Approximate 1.38%

Bond's YTM 2.78%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: CORPORATE FINANCE

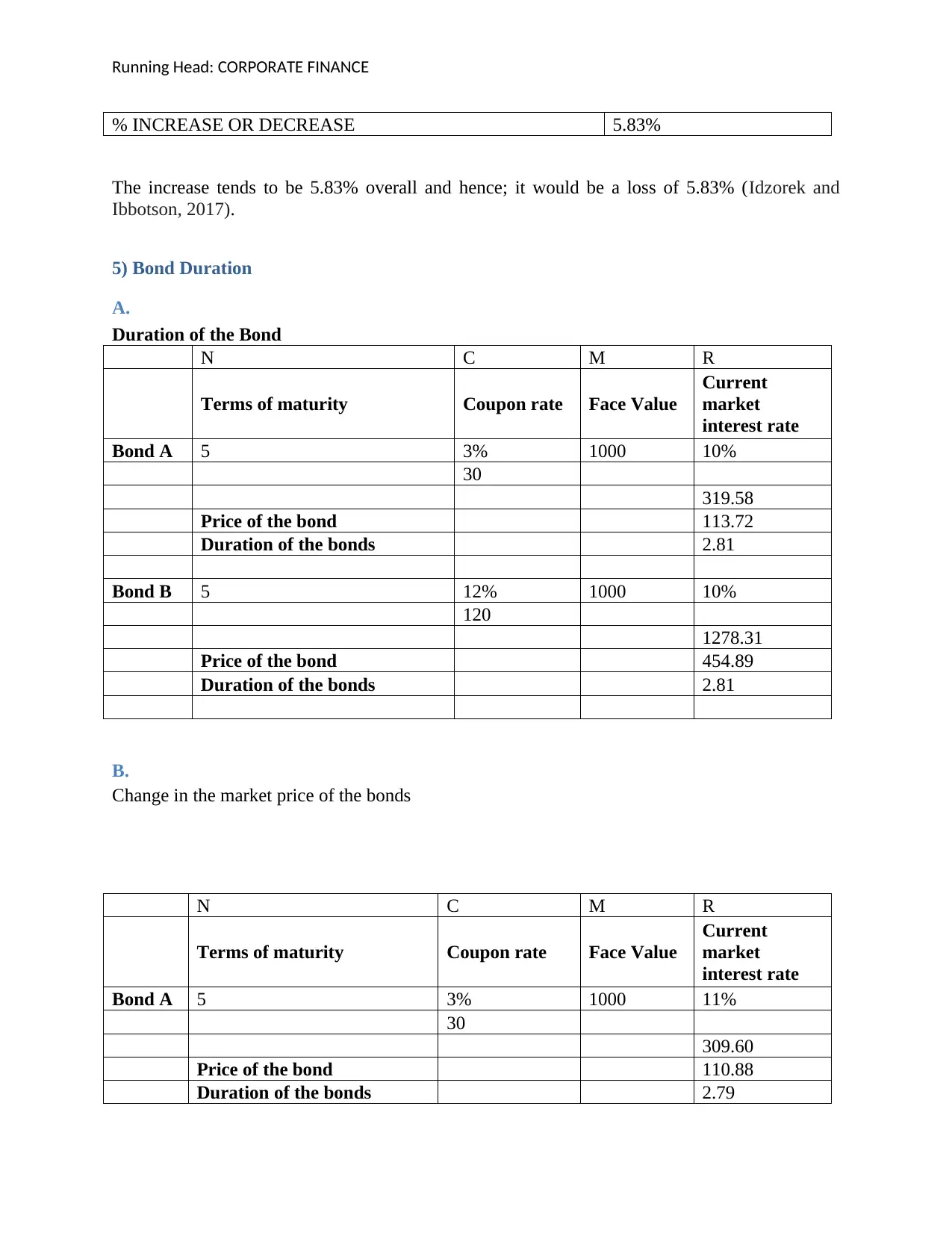

% INCREASE OR DECREASE 5.83%

The increase tends to be 5.83% overall and hence; it would be a loss of 5.83% (Idzorek and

Ibbotson, 2017).

5) Bond Duration

A.

Duration of the Bond

N C M R

Terms of maturity Coupon rate Face Value

Current

market

interest rate

Bond A 5 3% 1000 10%

30

319.58

Price of the bond 113.72

Duration of the bonds 2.81

Bond B 5 12% 1000 10%

120

1278.31

Price of the bond 454.89

Duration of the bonds 2.81

B.

Change in the market price of the bonds

N C M R

Terms of maturity Coupon rate Face Value

Current

market

interest rate

Bond A 5 3% 1000 11%

30

309.60

Price of the bond 110.88

Duration of the bonds 2.79

% INCREASE OR DECREASE 5.83%

The increase tends to be 5.83% overall and hence; it would be a loss of 5.83% (Idzorek and

Ibbotson, 2017).

5) Bond Duration

A.

Duration of the Bond

N C M R

Terms of maturity Coupon rate Face Value

Current

market

interest rate

Bond A 5 3% 1000 10%

30

319.58

Price of the bond 113.72

Duration of the bonds 2.81

Bond B 5 12% 1000 10%

120

1278.31

Price of the bond 454.89

Duration of the bonds 2.81

B.

Change in the market price of the bonds

N C M R

Terms of maturity Coupon rate Face Value

Current

market

interest rate

Bond A 5 3% 1000 11%

30

309.60

Price of the bond 110.88

Duration of the bonds 2.79

Running Head: CORPORATE FINANCE

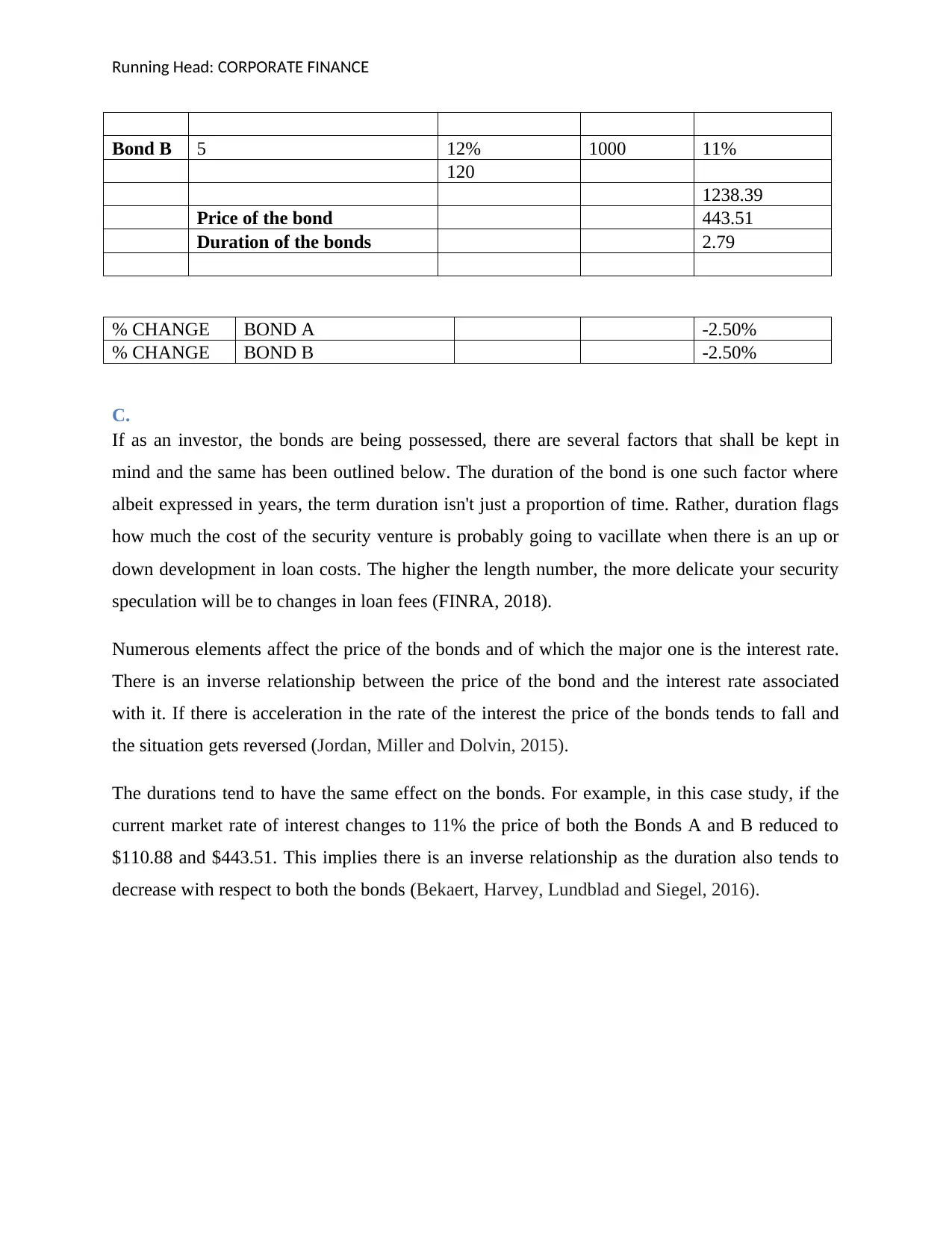

Bond B 5 12% 1000 11%

120

1238.39

Price of the bond 443.51

Duration of the bonds 2.79

% CHANGE BOND A -2.50%

% CHANGE BOND B -2.50%

C.

If as an investor, the bonds are being possessed, there are several factors that shall be kept in

mind and the same has been outlined below. The duration of the bond is one such factor where

albeit expressed in years, the term duration isn't just a proportion of time. Rather, duration flags

how much the cost of the security venture is probably going to vacillate when there is an up or

down development in loan costs. The higher the length number, the more delicate your security

speculation will be to changes in loan fees (FINRA, 2018).

Numerous elements affect the price of the bonds and of which the major one is the interest rate.

There is an inverse relationship between the price of the bond and the interest rate associated

with it. If there is acceleration in the rate of the interest the price of the bonds tends to fall and

the situation gets reversed (Jordan, Miller and Dolvin, 2015).

The durations tend to have the same effect on the bonds. For example, in this case study, if the

current market rate of interest changes to 11% the price of both the Bonds A and B reduced to

$110.88 and $443.51. This implies there is an inverse relationship as the duration also tends to

decrease with respect to both the bonds (Bekaert, Harvey, Lundblad and Siegel, 2016).

Bond B 5 12% 1000 11%

120

1238.39

Price of the bond 443.51

Duration of the bonds 2.79

% CHANGE BOND A -2.50%

% CHANGE BOND B -2.50%

C.

If as an investor, the bonds are being possessed, there are several factors that shall be kept in

mind and the same has been outlined below. The duration of the bond is one such factor where

albeit expressed in years, the term duration isn't just a proportion of time. Rather, duration flags

how much the cost of the security venture is probably going to vacillate when there is an up or

down development in loan costs. The higher the length number, the more delicate your security

speculation will be to changes in loan fees (FINRA, 2018).

Numerous elements affect the price of the bonds and of which the major one is the interest rate.

There is an inverse relationship between the price of the bond and the interest rate associated

with it. If there is acceleration in the rate of the interest the price of the bonds tends to fall and

the situation gets reversed (Jordan, Miller and Dolvin, 2015).

The durations tend to have the same effect on the bonds. For example, in this case study, if the

current market rate of interest changes to 11% the price of both the Bonds A and B reduced to

$110.88 and $443.51. This implies there is an inverse relationship as the duration also tends to

decrease with respect to both the bonds (Bekaert, Harvey, Lundblad and Siegel, 2016).

Running Head: CORPORATE FINANCE

References

Barillas, F. and Shanken, J., 2018. Comparing asset pricing models. The Journal of

Finance, 73(2), pp.715-754.

Bekaert, G., Harvey, C.R., Lundblad, C.T. and Siegel, S., 2016. Political risk and international

valuation. Journal of Corporate Finance, 37, pp.1-23.

Bora, B., 2015. Comparison between NPV and IRR. International journal of research in finance

and marketing, 5(12), pp.61-71.

Caspar, E.A., Cleeremans, A. and Haggard, P., 2015. The relationship between human agency

and embodiment. Consciousness and cognition, 33, pp.226-236.

Chordia, T. and Miao, B., 2018. Market Efficiency in Real Time: Evidence from Low Latency

Activity around Earnings Announcements.

Fenichel, E.P., Abbott, J.K., Bayham, J., Boone, W., Haacker, E.M. and Pfeiffer, L., 2016.

Measuring the value of groundwater and other forms of natural capital. Proceedings of the

National Academy of Sciences, 113(9), pp.2382-2387.

Fernando, P.N.D. and Gunasekara, A.L., 2018. Is the Market Efficiency Static or Dynamic–

Evidence from Colombo Stock Exchange (CSE). Kelaniya Journal of Management, 7(1).

FINRA, (2018) Duration—What an Interest Rate Hike Could Do to Your Bond Portfolio

[Online] Available from https://www.finra.org/investors/alerts/duration-what-interest-rate-hike-

could-do-your-bond-portfolio [Accessed on 17th August 2019].

Hökkä, P.K., Vähäsantanen, K., Paloniemi, S. and Eteläpelto, A., 2017. The reciprocal

relationship between emotions and agency in the workplace. In Agency at Work (pp. 161-181).

Springer, Cham.

Idzorek, T.M. and Ibbotson, R.G., 2017. Popularity and Asset Pricing. The Journal of

Investing, 26(1), pp.46-56.

Jordan, B.D., Miller, T.W. and Dolvin, S.D., 2015. Fundamentals of investments: valuation and

management. McGraw-Hill Education.

Lipton, A.M., 2015. Searching for Market Efficiency. Ariz. L. Rev., 57, p.71.

Patrick, M. and French, N., 2016. The IRR (IRR): projections, benchmarks and pitfalls. Journal

of Property Investment & Finance, 34(6), pp.664-669.

Romaioli, D. and Contarello, A., 2017. Redefining agency in late life: the concept of

‘disponibility’. Ageing & Society, pp.1-23.

References

Barillas, F. and Shanken, J., 2018. Comparing asset pricing models. The Journal of

Finance, 73(2), pp.715-754.

Bekaert, G., Harvey, C.R., Lundblad, C.T. and Siegel, S., 2016. Political risk and international

valuation. Journal of Corporate Finance, 37, pp.1-23.

Bora, B., 2015. Comparison between NPV and IRR. International journal of research in finance

and marketing, 5(12), pp.61-71.

Caspar, E.A., Cleeremans, A. and Haggard, P., 2015. The relationship between human agency

and embodiment. Consciousness and cognition, 33, pp.226-236.

Chordia, T. and Miao, B., 2018. Market Efficiency in Real Time: Evidence from Low Latency

Activity around Earnings Announcements.

Fenichel, E.P., Abbott, J.K., Bayham, J., Boone, W., Haacker, E.M. and Pfeiffer, L., 2016.

Measuring the value of groundwater and other forms of natural capital. Proceedings of the

National Academy of Sciences, 113(9), pp.2382-2387.

Fernando, P.N.D. and Gunasekara, A.L., 2018. Is the Market Efficiency Static or Dynamic–

Evidence from Colombo Stock Exchange (CSE). Kelaniya Journal of Management, 7(1).

FINRA, (2018) Duration—What an Interest Rate Hike Could Do to Your Bond Portfolio

[Online] Available from https://www.finra.org/investors/alerts/duration-what-interest-rate-hike-

could-do-your-bond-portfolio [Accessed on 17th August 2019].

Hökkä, P.K., Vähäsantanen, K., Paloniemi, S. and Eteläpelto, A., 2017. The reciprocal

relationship between emotions and agency in the workplace. In Agency at Work (pp. 161-181).

Springer, Cham.

Idzorek, T.M. and Ibbotson, R.G., 2017. Popularity and Asset Pricing. The Journal of

Investing, 26(1), pp.46-56.

Jordan, B.D., Miller, T.W. and Dolvin, S.D., 2015. Fundamentals of investments: valuation and

management. McGraw-Hill Education.

Lipton, A.M., 2015. Searching for Market Efficiency. Ariz. L. Rev., 57, p.71.

Patrick, M. and French, N., 2016. The IRR (IRR): projections, benchmarks and pitfalls. Journal

of Property Investment & Finance, 34(6), pp.664-669.

Romaioli, D. and Contarello, A., 2017. Redefining agency in late life: the concept of

‘disponibility’. Ageing & Society, pp.1-23.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.