Business Decision Making Assignment - Financial Analysis and Methods

VerifiedAdded on 2023/01/04

|13

|2510

|45

Homework Assignment

AI Summary

This assignment solution addresses various aspects of business decision-making. It begins with a statistical analysis of data, including frequency distributions, mean, median, mode, range, variance, and standard deviation calculations. The solution then delves into project management, specifically the identification of a critical path. Further analysis includes financial evaluations such as payback period calculations for machine purchase decisions. The assignment also explores non-discounted and discounted cash flow methods, comparing and contrasting payback period and accounting rate of return (ARR), and net present value (NPV) and internal rate of return (IRR). The solution provides detailed explanations, formulas, and examples to illustrate these financial concepts, offering a comprehensive overview of financial decision-making techniques used in business.

BUSINESS DECISION

MAKING

MAKING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

TASK..................................................................................................................................3

Question 1.................................................................................................................3

Question 2.................................................................................................................3

Question 3.................................................................................................................5

Question 4.................................................................................................................5

Question 5...............................................................................................................................5

Question 6...............................................................................................................................7

TASK..................................................................................................................................3

Question 1.................................................................................................................3

Question 2.................................................................................................................3

Question 3.................................................................................................................5

Question 4.................................................................................................................5

Question 5...............................................................................................................................5

Question 6...............................................................................................................................7

TASK

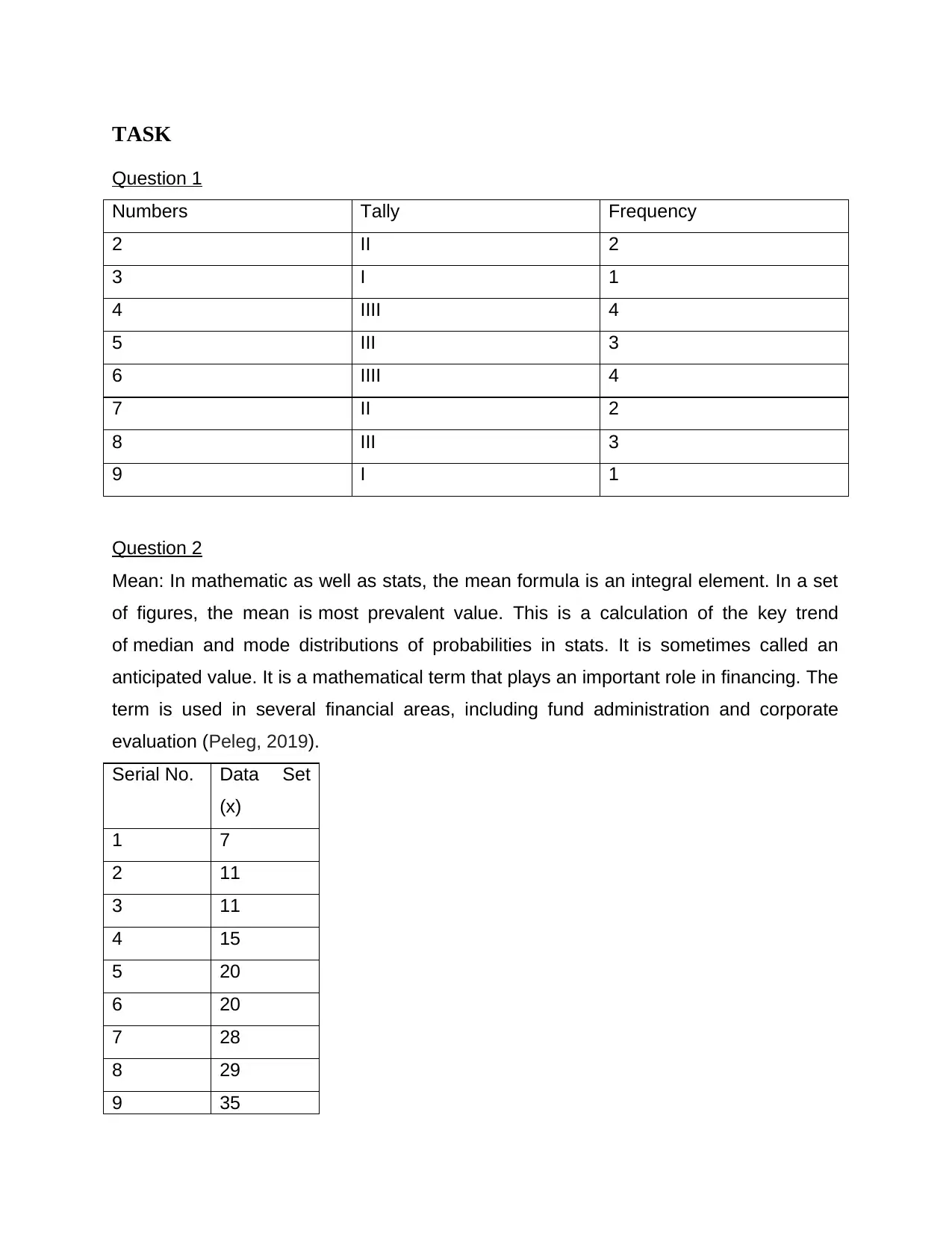

Question 1

Numbers Tally Frequency

2 II 2

3 I 1

4 IIII 4

5 III 3

6 IIII 4

7 II 2

8 III 3

9 I 1

Question 2

Mean: In mathematic as well as stats, the mean formula is an integral element. In a set

of figures, the mean is most prevalent value. This is a calculation of the key trend

of median and mode distributions of probabilities in stats. It is sometimes called an

anticipated value. It is a mathematical term that plays an important role in financing. The

term is used in several financial areas, including fund administration and corporate

evaluation (Peleg, 2019).

Serial No. Data Set

(x)

1 7

2 11

3 11

4 15

5 20

6 20

7 28

8 29

9 35

Question 1

Numbers Tally Frequency

2 II 2

3 I 1

4 IIII 4

5 III 3

6 IIII 4

7 II 2

8 III 3

9 I 1

Question 2

Mean: In mathematic as well as stats, the mean formula is an integral element. In a set

of figures, the mean is most prevalent value. This is a calculation of the key trend

of median and mode distributions of probabilities in stats. It is sometimes called an

anticipated value. It is a mathematical term that plays an important role in financing. The

term is used in several financial areas, including fund administration and corporate

evaluation (Peleg, 2019).

Serial No. Data Set

(x)

1 7

2 11

3 11

4 15

5 20

6 20

7 28

8 29

9 35

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

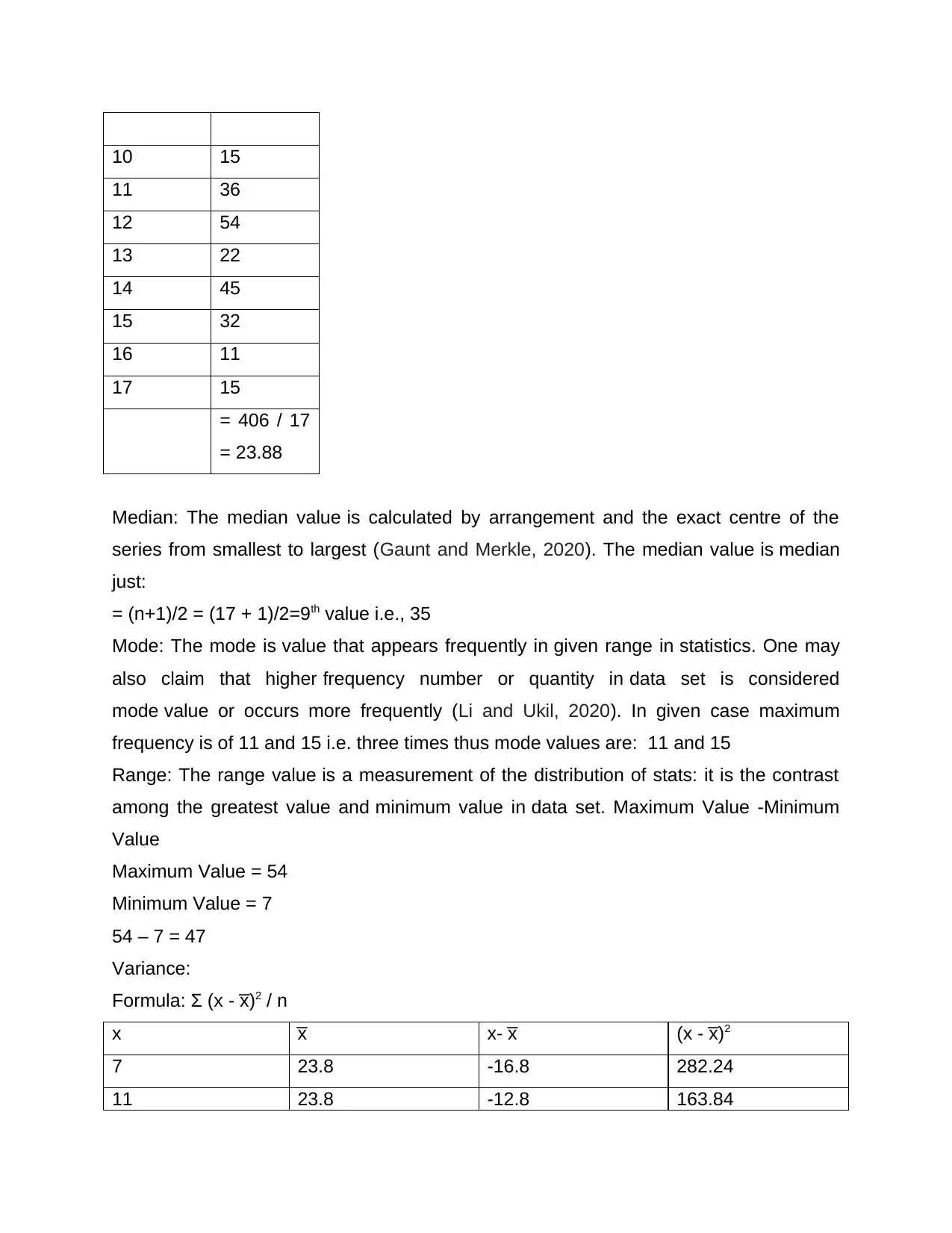

10 15

11 36

12 54

13 22

14 45

15 32

16 11

17 15

= 406 / 17

= 23.88

Median: The median value is calculated by arrangement and the exact centre of the

series from smallest to largest (Gaunt and Merkle, 2020). The median value is median

just:

= (n+1)/2 = (17 + 1)/2=9th value i.e., 35

Mode: The mode is value that appears frequently in given range in statistics. One may

also claim that higher frequency number or quantity in data set is considered

mode value or occurs more frequently (Li and Ukil, 2020). In given case maximum

frequency is of 11 and 15 i.e. three times thus mode values are: 11 and 15

Range: The range value is a measurement of the distribution of stats: it is the contrast

among the greatest value and minimum value in data set. Maximum Value -Minimum

Value

Maximum Value = 54

Minimum Value = 7

54 – 7 = 47

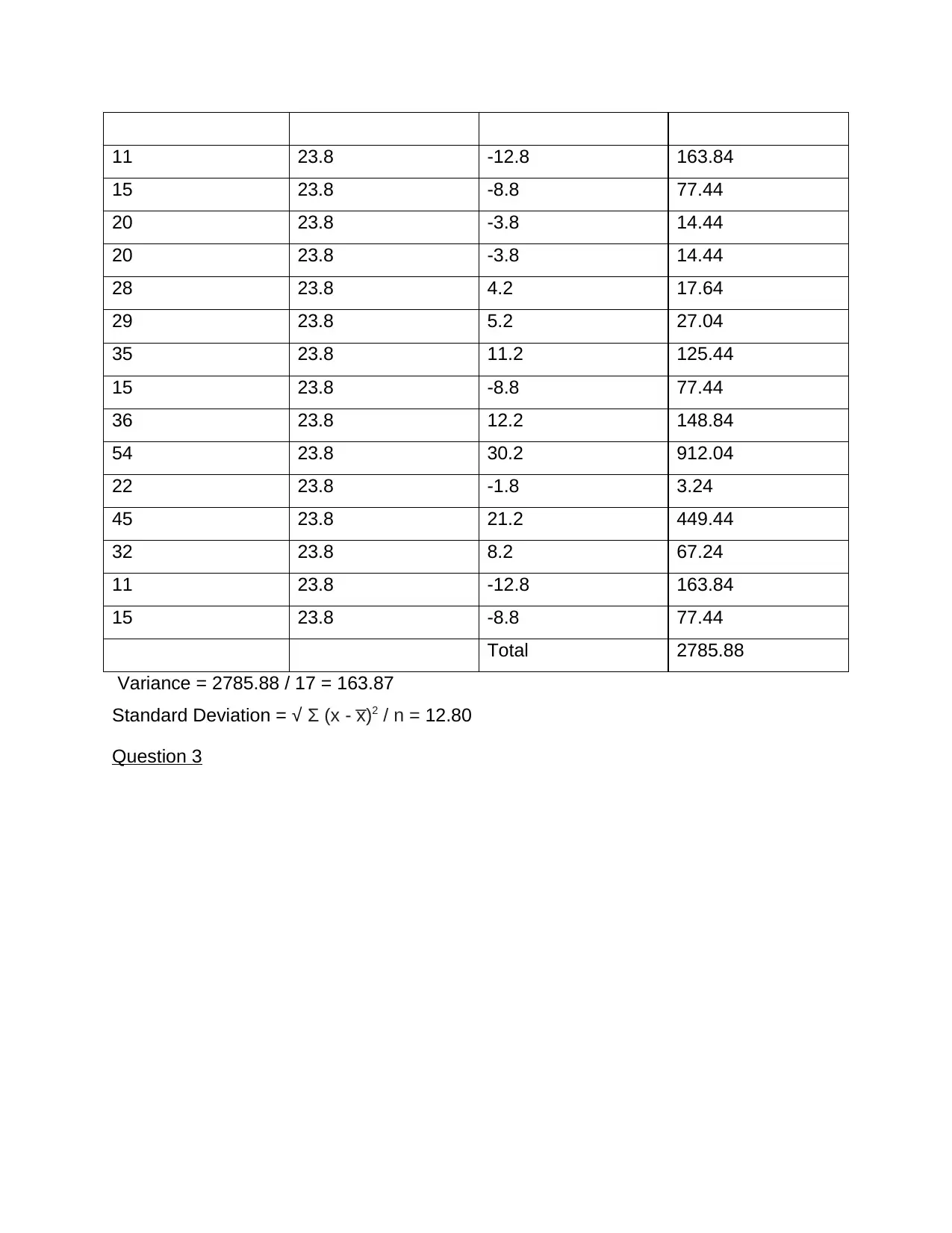

Variance:

Formula: Σ (x - x̅)2 / n

x x̅ x- x̅ (x - x̅)2

7 23.8 -16.8 282.24

11 23.8 -12.8 163.84

11 36

12 54

13 22

14 45

15 32

16 11

17 15

= 406 / 17

= 23.88

Median: The median value is calculated by arrangement and the exact centre of the

series from smallest to largest (Gaunt and Merkle, 2020). The median value is median

just:

= (n+1)/2 = (17 + 1)/2=9th value i.e., 35

Mode: The mode is value that appears frequently in given range in statistics. One may

also claim that higher frequency number or quantity in data set is considered

mode value or occurs more frequently (Li and Ukil, 2020). In given case maximum

frequency is of 11 and 15 i.e. three times thus mode values are: 11 and 15

Range: The range value is a measurement of the distribution of stats: it is the contrast

among the greatest value and minimum value in data set. Maximum Value -Minimum

Value

Maximum Value = 54

Minimum Value = 7

54 – 7 = 47

Variance:

Formula: Σ (x - x̅)2 / n

x x̅ x- x̅ (x - x̅)2

7 23.8 -16.8 282.24

11 23.8 -12.8 163.84

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11 23.8 -12.8 163.84

15 23.8 -8.8 77.44

20 23.8 -3.8 14.44

20 23.8 -3.8 14.44

28 23.8 4.2 17.64

29 23.8 5.2 27.04

35 23.8 11.2 125.44

15 23.8 -8.8 77.44

36 23.8 12.2 148.84

54 23.8 30.2 912.04

22 23.8 -1.8 3.24

45 23.8 21.2 449.44

32 23.8 8.2 67.24

11 23.8 -12.8 163.84

15 23.8 -8.8 77.44

Total 2785.88

Variance = 2785.88 / 17 = 163.87

Standard Deviation = √ Σ (x - x̅)2 / n = 12.80

Question 3

15 23.8 -8.8 77.44

20 23.8 -3.8 14.44

20 23.8 -3.8 14.44

28 23.8 4.2 17.64

29 23.8 5.2 27.04

35 23.8 11.2 125.44

15 23.8 -8.8 77.44

36 23.8 12.2 148.84

54 23.8 30.2 912.04

22 23.8 -1.8 3.24

45 23.8 21.2 449.44

32 23.8 8.2 67.24

11 23.8 -12.8 163.84

15 23.8 -8.8 77.44

Total 2785.88

Variance = 2785.88 / 17 = 163.87

Standard Deviation = √ Σ (x - x̅)2 / n = 12.80

Question 3

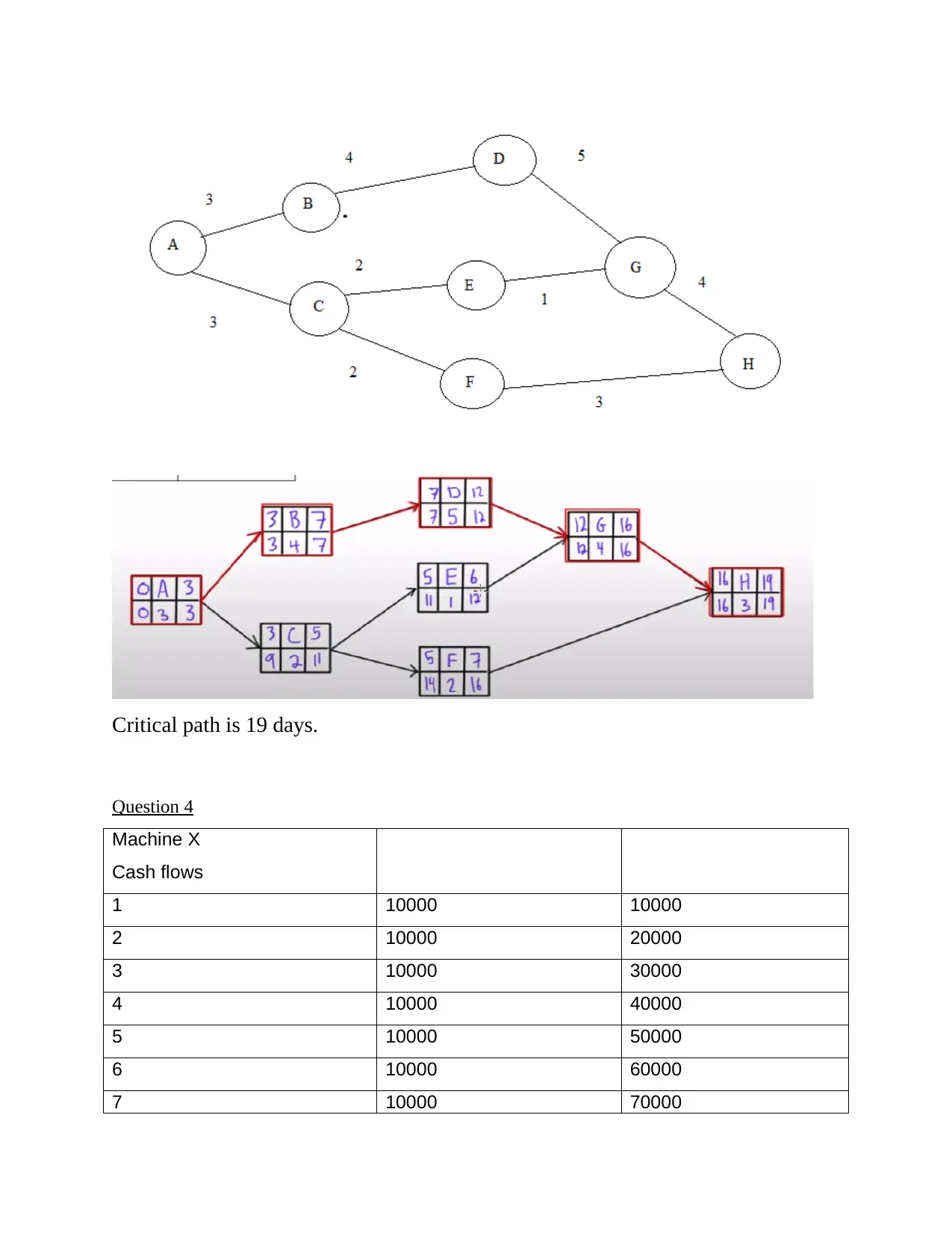

Critical path is 19 days.

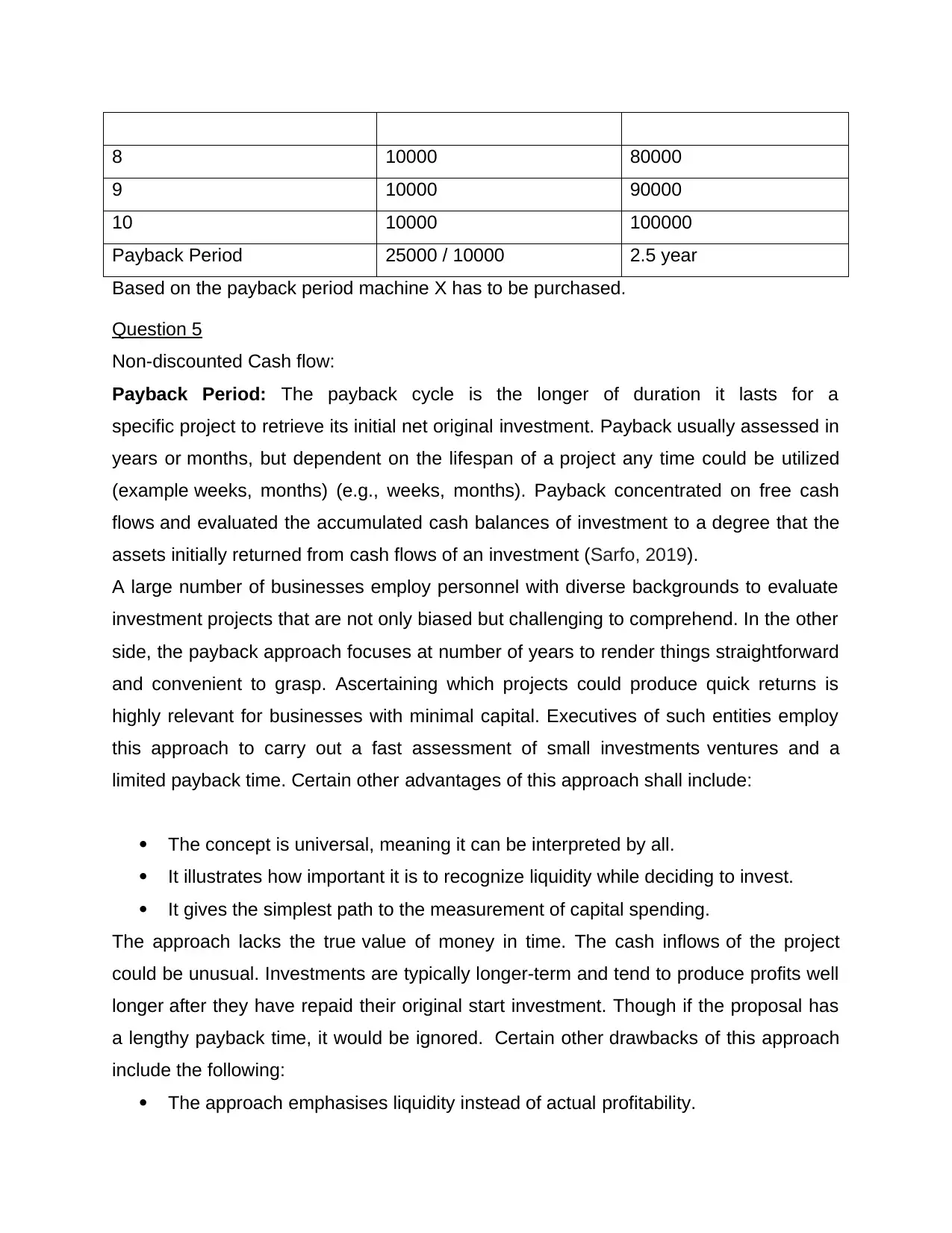

Question 4

Machine X

Cash flows

1 10000 10000

2 10000 20000

3 10000 30000

4 10000 40000

5 10000 50000

6 10000 60000

7 10000 70000

Question 4

Machine X

Cash flows

1 10000 10000

2 10000 20000

3 10000 30000

4 10000 40000

5 10000 50000

6 10000 60000

7 10000 70000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

8 10000 80000

9 10000 90000

10 10000 100000

Payback Period 25000 / 10000 2.5 year

Based on the payback period machine X has to be purchased.

Question 5

Non-discounted Cash flow:

Payback Period: The payback cycle is the longer of duration it lasts for a

specific project to retrieve its initial net original investment. Payback usually assessed in

years or months, but dependent on the lifespan of a project any time could be utilized

(example weeks, months) (e.g., weeks, months). Payback concentrated on free cash

flows and evaluated the accumulated cash balances of investment to a degree that the

assets initially returned from cash flows of an investment (Sarfo, 2019).

A large number of businesses employ personnel with diverse backgrounds to evaluate

investment projects that are not only biased but challenging to comprehend. In the other

side, the payback approach focuses at number of years to render things straightforward

and convenient to grasp. Ascertaining which projects could produce quick returns is

highly relevant for businesses with minimal capital. Executives of such entities employ

this approach to carry out a fast assessment of small investments ventures and a

limited payback time. Certain other advantages of this approach shall include:

The concept is universal, meaning it can be interpreted by all.

It illustrates how important it is to recognize liquidity while deciding to invest.

It gives the simplest path to the measurement of capital spending.

The approach lacks the true value of money in time. The cash inflows of the project

could be unusual. Investments are typically longer-term and tend to produce profits well

longer after they have repaid their original start investment. Though if the proposal has

a lengthy payback time, it would be ignored. Certain other drawbacks of this approach

include the following:

The approach emphasises liquidity instead of actual profitability.

9 10000 90000

10 10000 100000

Payback Period 25000 / 10000 2.5 year

Based on the payback period machine X has to be purchased.

Question 5

Non-discounted Cash flow:

Payback Period: The payback cycle is the longer of duration it lasts for a

specific project to retrieve its initial net original investment. Payback usually assessed in

years or months, but dependent on the lifespan of a project any time could be utilized

(example weeks, months) (e.g., weeks, months). Payback concentrated on free cash

flows and evaluated the accumulated cash balances of investment to a degree that the

assets initially returned from cash flows of an investment (Sarfo, 2019).

A large number of businesses employ personnel with diverse backgrounds to evaluate

investment projects that are not only biased but challenging to comprehend. In the other

side, the payback approach focuses at number of years to render things straightforward

and convenient to grasp. Ascertaining which projects could produce quick returns is

highly relevant for businesses with minimal capital. Executives of such entities employ

this approach to carry out a fast assessment of small investments ventures and a

limited payback time. Certain other advantages of this approach shall include:

The concept is universal, meaning it can be interpreted by all.

It illustrates how important it is to recognize liquidity while deciding to invest.

It gives the simplest path to the measurement of capital spending.

The approach lacks the true value of money in time. The cash inflows of the project

could be unusual. Investments are typically longer-term and tend to produce profits well

longer after they have repaid their original start investment. Though if the proposal has

a lengthy payback time, it would be ignored. Certain other drawbacks of this approach

include the following:

The approach emphasises liquidity instead of actual profitability.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Just cash returns flow within the timeframe are considered under this method.

Accounting Rate of Return: This is the cumulative rate of returns expected through

a project or asset compared with the initial investment cost. Commonly, ARR is tasked

to make the decision. For e.g., if the corporation needs to decide whether to pursue with

a specified investment, the ARR calculation can assist to determine whether to go

through an investment or project is correct decision (Wambua and Koori, 2018).

ARR has goal of being profitable when investments are rendered. Businesses

may employ accounting rate of return metric to calculate the profitability status of

financial project effectiveness and financial cost. It would allow businesses to develop

alternatives and plans that are adequately related to the use of resources. Moreover, it

is an important and less taxing approach to computing and seeing by the use of the

ARR tactic; a speedy evaluation can be made of the identification that will enable

businesses to penetrate opportunities faster. Appraisal may be utilized for longer-haul

activities and ventures would be useful for using net present quality methodology since

it accounts for the approximate length of cash taking into account the potential method

of money source and the volume of money sources measured. This will then recognize

future revenue stream challenges and risks, as well as general net money source. In

comparison, the net current value tends to enhance the value of the alliance.

The downside of ARR approach is that this embraces continuous adaptation to

maintain same capital investment. This occurs once in while when the cash inflows

adjust adaptation over the time. A business will have to keep same outfit on a daily

basis. It is impossible to do this because of logistical problems and spending. It is also

not straightforward to measure cost of resources used to map down money sources. At

money sources by using the lowest targeted rate of return. In turn, Net present factors

have disadvantaged the end of the day the ARR method is not all helpful to the point at

which the organisation handles capital allocation by itself. In addition to ARR, gain file

will be used to evaluate the priorities in capital allocation scenario (Ndanyenbah and

Zakaria, 2019).

The goal of ARR capital allocation system is to resolve the component of payback

shortfall and rate of return on accounts. Net presents value of all capital sources and

outpourings over life of the project. This makes a pay-out for the time number of cash-

Accounting Rate of Return: This is the cumulative rate of returns expected through

a project or asset compared with the initial investment cost. Commonly, ARR is tasked

to make the decision. For e.g., if the corporation needs to decide whether to pursue with

a specified investment, the ARR calculation can assist to determine whether to go

through an investment or project is correct decision (Wambua and Koori, 2018).

ARR has goal of being profitable when investments are rendered. Businesses

may employ accounting rate of return metric to calculate the profitability status of

financial project effectiveness and financial cost. It would allow businesses to develop

alternatives and plans that are adequately related to the use of resources. Moreover, it

is an important and less taxing approach to computing and seeing by the use of the

ARR tactic; a speedy evaluation can be made of the identification that will enable

businesses to penetrate opportunities faster. Appraisal may be utilized for longer-haul

activities and ventures would be useful for using net present quality methodology since

it accounts for the approximate length of cash taking into account the potential method

of money source and the volume of money sources measured. This will then recognize

future revenue stream challenges and risks, as well as general net money source. In

comparison, the net current value tends to enhance the value of the alliance.

The downside of ARR approach is that this embraces continuous adaptation to

maintain same capital investment. This occurs once in while when the cash inflows

adjust adaptation over the time. A business will have to keep same outfit on a daily

basis. It is impossible to do this because of logistical problems and spending. It is also

not straightforward to measure cost of resources used to map down money sources. At

money sources by using the lowest targeted rate of return. In turn, Net present factors

have disadvantaged the end of the day the ARR method is not all helpful to the point at

which the organisation handles capital allocation by itself. In addition to ARR, gain file

will be used to evaluate the priorities in capital allocation scenario (Ndanyenbah and

Zakaria, 2019).

The goal of ARR capital allocation system is to resolve the component of payback

shortfall and rate of return on accounts. Net presents value of all capital sources and

outpourings over life of the project. This makes a pay-out for the time number of cash-

funds as well as measures the latest forecast of all daily possible when ARR cannot

specifically settle on a choice if the metric of decision is not same for entirely unrelated

activities.

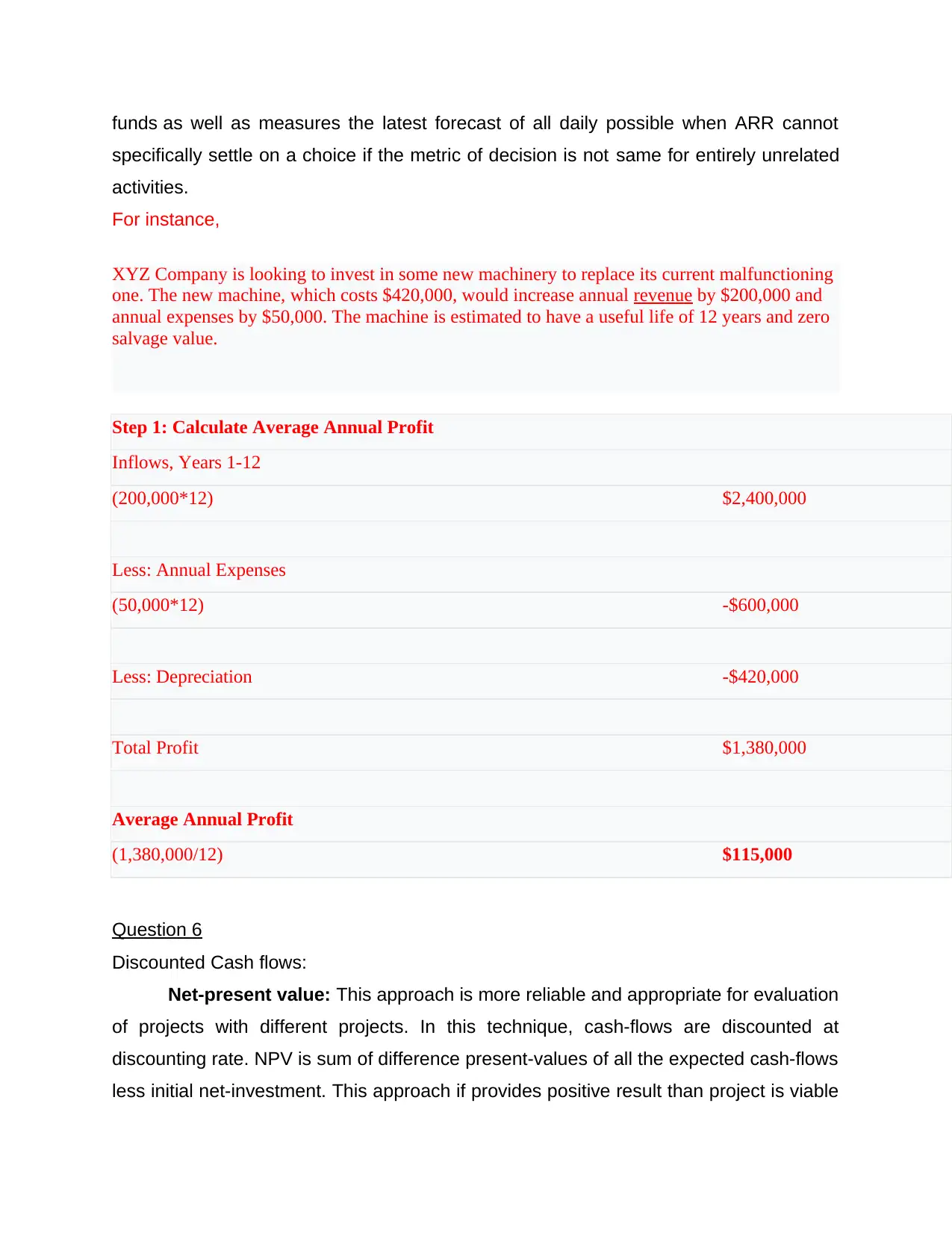

For instance,

XYZ Company is looking to invest in some new machinery to replace its current malfunctioning

one. The new machine, which costs $420,000, would increase annual revenue by $200,000 and

annual expenses by $50,000. The machine is estimated to have a useful life of 12 years and zero

salvage value.

Step 1: Calculate Average Annual Profit

Inflows, Years 1-12

(200,000*12) $2,400,000

Less: Annual Expenses

(50,000*12) -$600,000

Less: Depreciation -$420,000

Total Profit $1,380,000

Average Annual Profit

(1,380,000/12) $115,000

Question 6

Discounted Cash flows:

Net-present value: This approach is more reliable and appropriate for evaluation

of projects with different projects. In this technique, cash-flows are discounted at

discounting rate. NPV is sum of difference present-values of all the expected cash-flows

less initial net-investment. This approach if provides positive result than project is viable

specifically settle on a choice if the metric of decision is not same for entirely unrelated

activities.

For instance,

XYZ Company is looking to invest in some new machinery to replace its current malfunctioning

one. The new machine, which costs $420,000, would increase annual revenue by $200,000 and

annual expenses by $50,000. The machine is estimated to have a useful life of 12 years and zero

salvage value.

Step 1: Calculate Average Annual Profit

Inflows, Years 1-12

(200,000*12) $2,400,000

Less: Annual Expenses

(50,000*12) -$600,000

Less: Depreciation -$420,000

Total Profit $1,380,000

Average Annual Profit

(1,380,000/12) $115,000

Question 6

Discounted Cash flows:

Net-present value: This approach is more reliable and appropriate for evaluation

of projects with different projects. In this technique, cash-flows are discounted at

discounting rate. NPV is sum of difference present-values of all the expected cash-flows

less initial net-investment. This approach if provides positive result than project is viable

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and when NPV of project is negative value than project is not considered as viable. This

approach is most suitable for comparing two projects with different useful life.

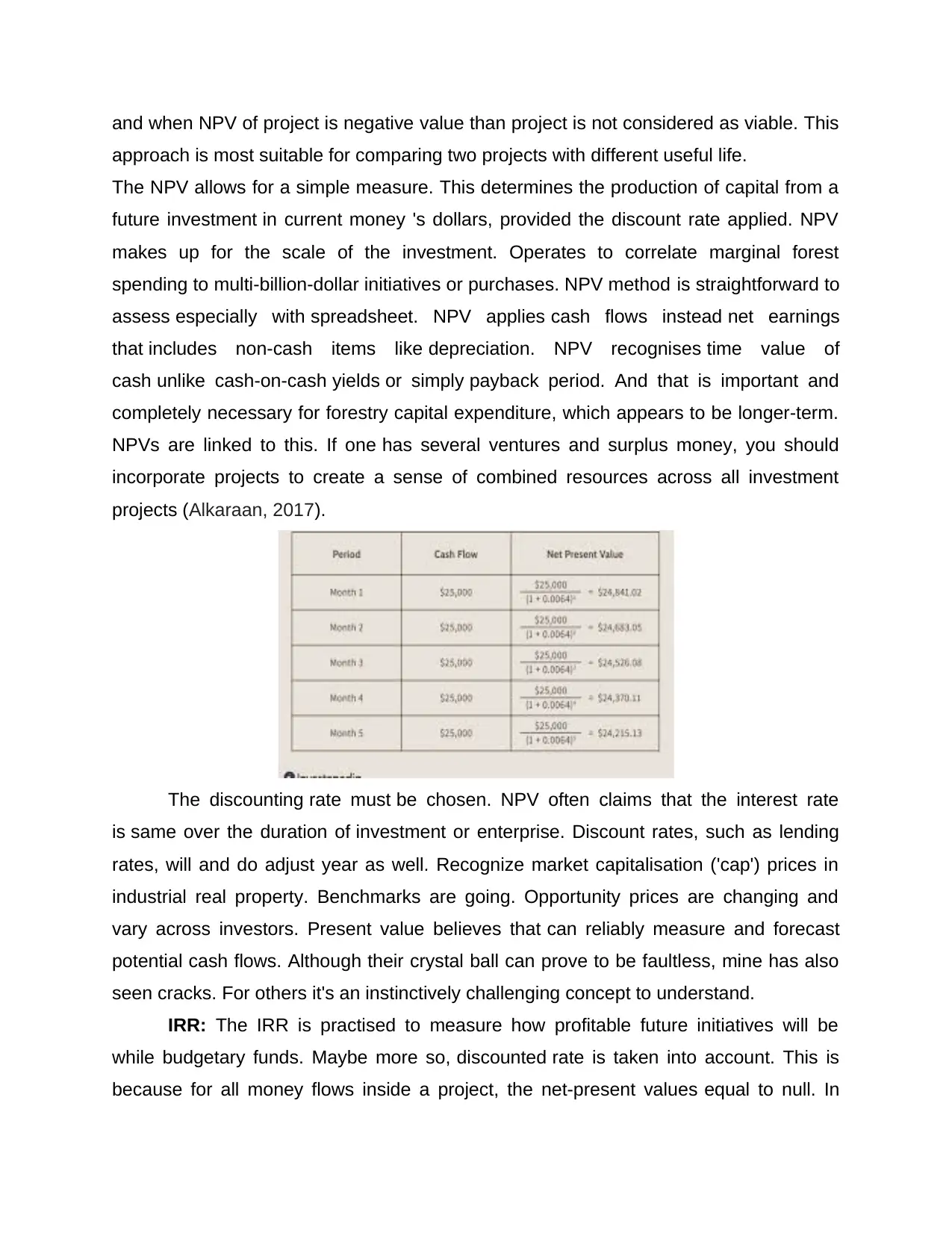

The NPV allows for a simple measure. This determines the production of capital from a

future investment in current money 's dollars, provided the discount rate applied. NPV

makes up for the scale of the investment. Operates to correlate marginal forest

spending to multi-billion-dollar initiatives or purchases. NPV method is straightforward to

assess especially with spreadsheet. NPV applies cash flows instead net earnings

that includes non-cash items like depreciation. NPV recognises time value of

cash unlike cash-on-cash yields or simply payback period. And that is important and

completely necessary for forestry capital expenditure, which appears to be longer-term.

NPVs are linked to this. If one has several ventures and surplus money, you should

incorporate projects to create a sense of combined resources across all investment

projects (Alkaraan, 2017).

The discounting rate must be chosen. NPV often claims that the interest rate

is same over the duration of investment or enterprise. Discount rates, such as lending

rates, will and do adjust year as well. Recognize market capitalisation ('cap') prices in

industrial real property. Benchmarks are going. Opportunity prices are changing and

vary across investors. Present value believes that can reliably measure and forecast

potential cash flows. Although their crystal ball can prove to be faultless, mine has also

seen cracks. For others it's an instinctively challenging concept to understand.

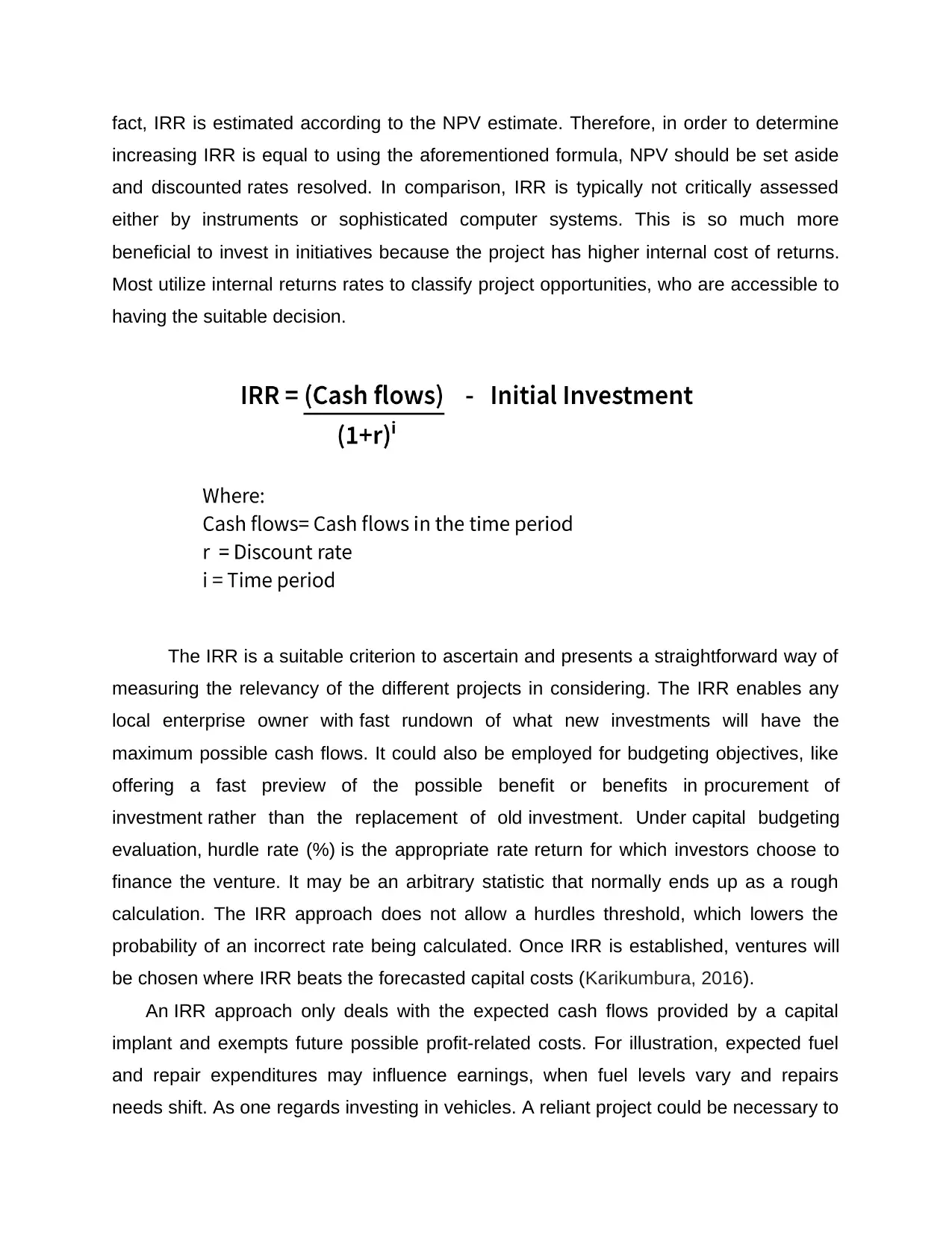

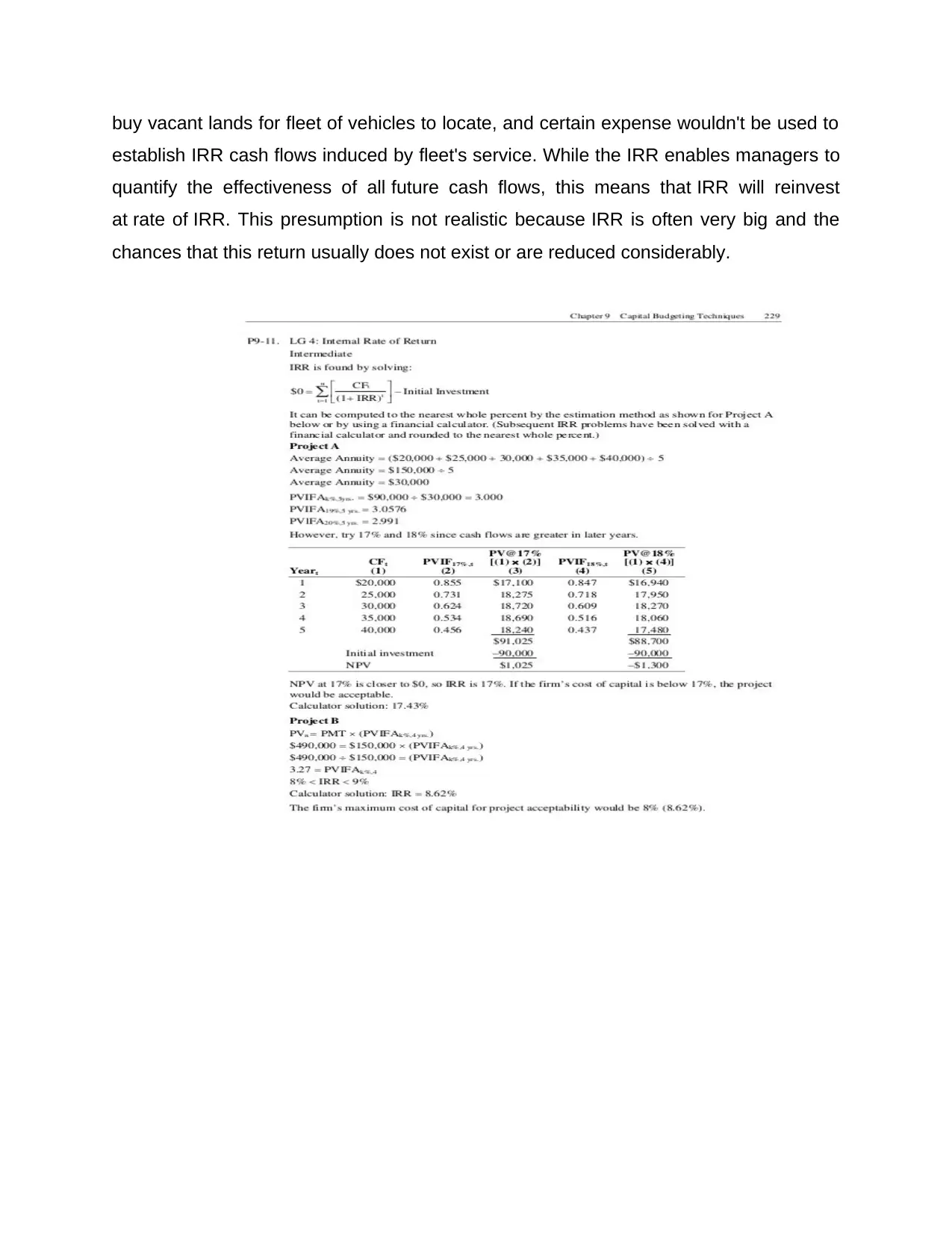

IRR: The IRR is practised to measure how profitable future initiatives will be

while budgetary funds. Maybe more so, discounted rate is taken into account. This is

because for all money flows inside a project, the net-present values equal to null. In

approach is most suitable for comparing two projects with different useful life.

The NPV allows for a simple measure. This determines the production of capital from a

future investment in current money 's dollars, provided the discount rate applied. NPV

makes up for the scale of the investment. Operates to correlate marginal forest

spending to multi-billion-dollar initiatives or purchases. NPV method is straightforward to

assess especially with spreadsheet. NPV applies cash flows instead net earnings

that includes non-cash items like depreciation. NPV recognises time value of

cash unlike cash-on-cash yields or simply payback period. And that is important and

completely necessary for forestry capital expenditure, which appears to be longer-term.

NPVs are linked to this. If one has several ventures and surplus money, you should

incorporate projects to create a sense of combined resources across all investment

projects (Alkaraan, 2017).

The discounting rate must be chosen. NPV often claims that the interest rate

is same over the duration of investment or enterprise. Discount rates, such as lending

rates, will and do adjust year as well. Recognize market capitalisation ('cap') prices in

industrial real property. Benchmarks are going. Opportunity prices are changing and

vary across investors. Present value believes that can reliably measure and forecast

potential cash flows. Although their crystal ball can prove to be faultless, mine has also

seen cracks. For others it's an instinctively challenging concept to understand.

IRR: The IRR is practised to measure how profitable future initiatives will be

while budgetary funds. Maybe more so, discounted rate is taken into account. This is

because for all money flows inside a project, the net-present values equal to null. In

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

fact, IRR is estimated according to the NPV estimate. Therefore, in order to determine

increasing IRR is equal to using the aforementioned formula, NPV should be set aside

and discounted rates resolved. In comparison, IRR is typically not critically assessed

either by instruments or sophisticated computer systems. This is so much more

beneficial to invest in initiatives because the project has higher internal cost of returns.

Most utilize internal returns rates to classify project opportunities, who are accessible to

having the suitable decision.

The IRR is a suitable criterion to ascertain and presents a straightforward way of

measuring the relevancy of the different projects in considering. The IRR enables any

local enterprise owner with fast rundown of what new investments will have the

maximum possible cash flows. It could also be employed for budgeting objectives, like

offering a fast preview of the possible benefit or benefits in procurement of

investment rather than the replacement of old investment. Under capital budgeting

evaluation, hurdle rate (%) is the appropriate rate return for which investors choose to

finance the venture. It may be an arbitrary statistic that normally ends up as a rough

calculation. The IRR approach does not allow a hurdles threshold, which lowers the

probability of an incorrect rate being calculated. Once IRR is established, ventures will

be chosen where IRR beats the forecasted capital costs (Karikumbura, 2016).

An IRR approach only deals with the expected cash flows provided by a capital

implant and exempts future possible profit-related costs. For illustration, expected fuel

and repair expenditures may influence earnings, when fuel levels vary and repairs

needs shift. As one regards investing in vehicles. A reliant project could be necessary to

increasing IRR is equal to using the aforementioned formula, NPV should be set aside

and discounted rates resolved. In comparison, IRR is typically not critically assessed

either by instruments or sophisticated computer systems. This is so much more

beneficial to invest in initiatives because the project has higher internal cost of returns.

Most utilize internal returns rates to classify project opportunities, who are accessible to

having the suitable decision.

The IRR is a suitable criterion to ascertain and presents a straightforward way of

measuring the relevancy of the different projects in considering. The IRR enables any

local enterprise owner with fast rundown of what new investments will have the

maximum possible cash flows. It could also be employed for budgeting objectives, like

offering a fast preview of the possible benefit or benefits in procurement of

investment rather than the replacement of old investment. Under capital budgeting

evaluation, hurdle rate (%) is the appropriate rate return for which investors choose to

finance the venture. It may be an arbitrary statistic that normally ends up as a rough

calculation. The IRR approach does not allow a hurdles threshold, which lowers the

probability of an incorrect rate being calculated. Once IRR is established, ventures will

be chosen where IRR beats the forecasted capital costs (Karikumbura, 2016).

An IRR approach only deals with the expected cash flows provided by a capital

implant and exempts future possible profit-related costs. For illustration, expected fuel

and repair expenditures may influence earnings, when fuel levels vary and repairs

needs shift. As one regards investing in vehicles. A reliant project could be necessary to

buy vacant lands for fleet of vehicles to locate, and certain expense wouldn't be used to

establish IRR cash flows induced by fleet's service. While the IRR enables managers to

quantify the effectiveness of all future cash flows, this means that IRR will reinvest

at rate of IRR. This presumption is not realistic because IRR is often very big and the

chances that this return usually does not exist or are reduced considerably.

establish IRR cash flows induced by fleet's service. While the IRR enables managers to

quantify the effectiveness of all future cash flows, this means that IRR will reinvest

at rate of IRR. This presumption is not realistic because IRR is often very big and the

chances that this return usually does not exist or are reduced considerably.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.