Taxation Assessment for Michael: Income, FBT, and Capital Gains 2019

VerifiedAdded on 2023/01/11

|7

|1223

|52

Homework Assignment

AI Summary

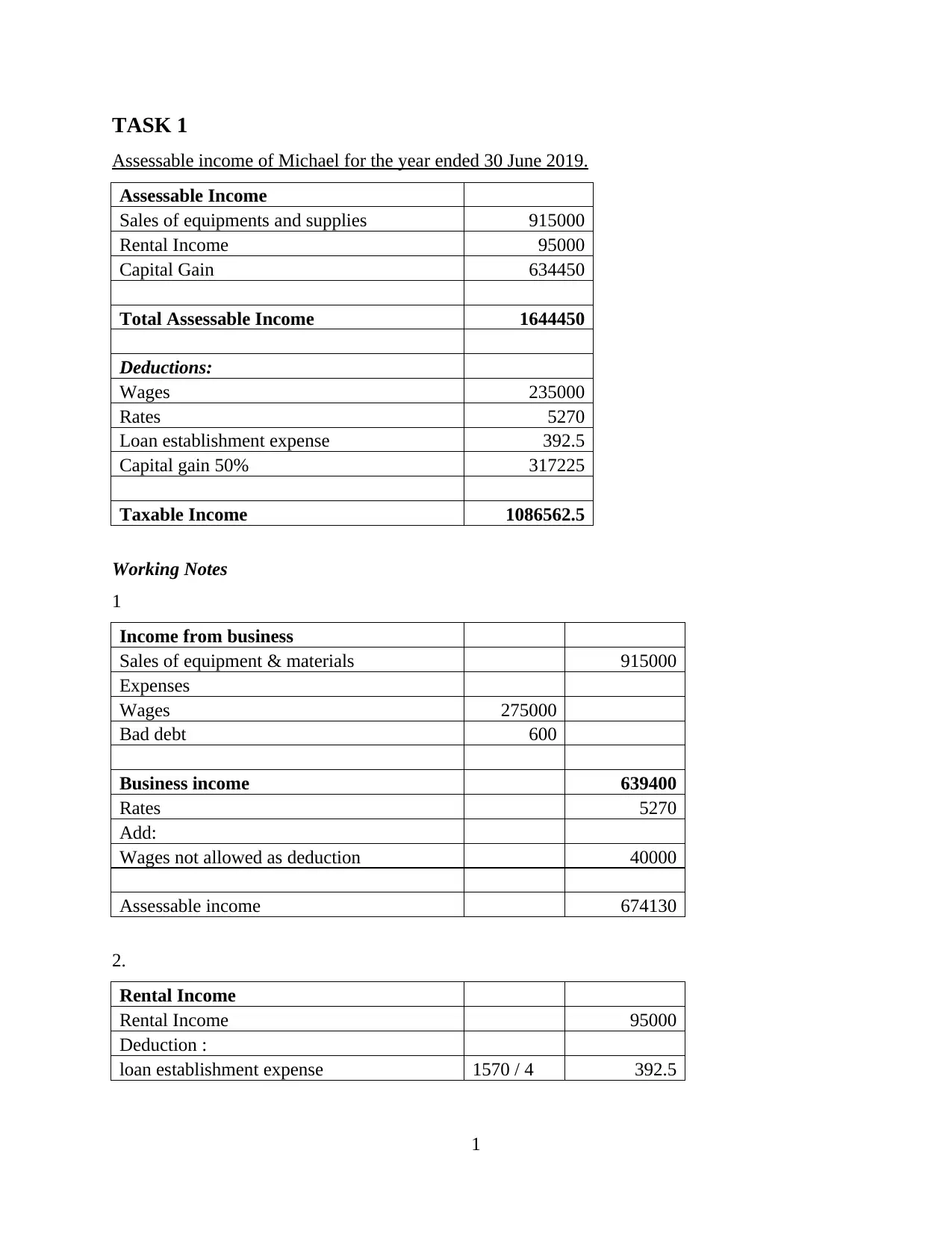

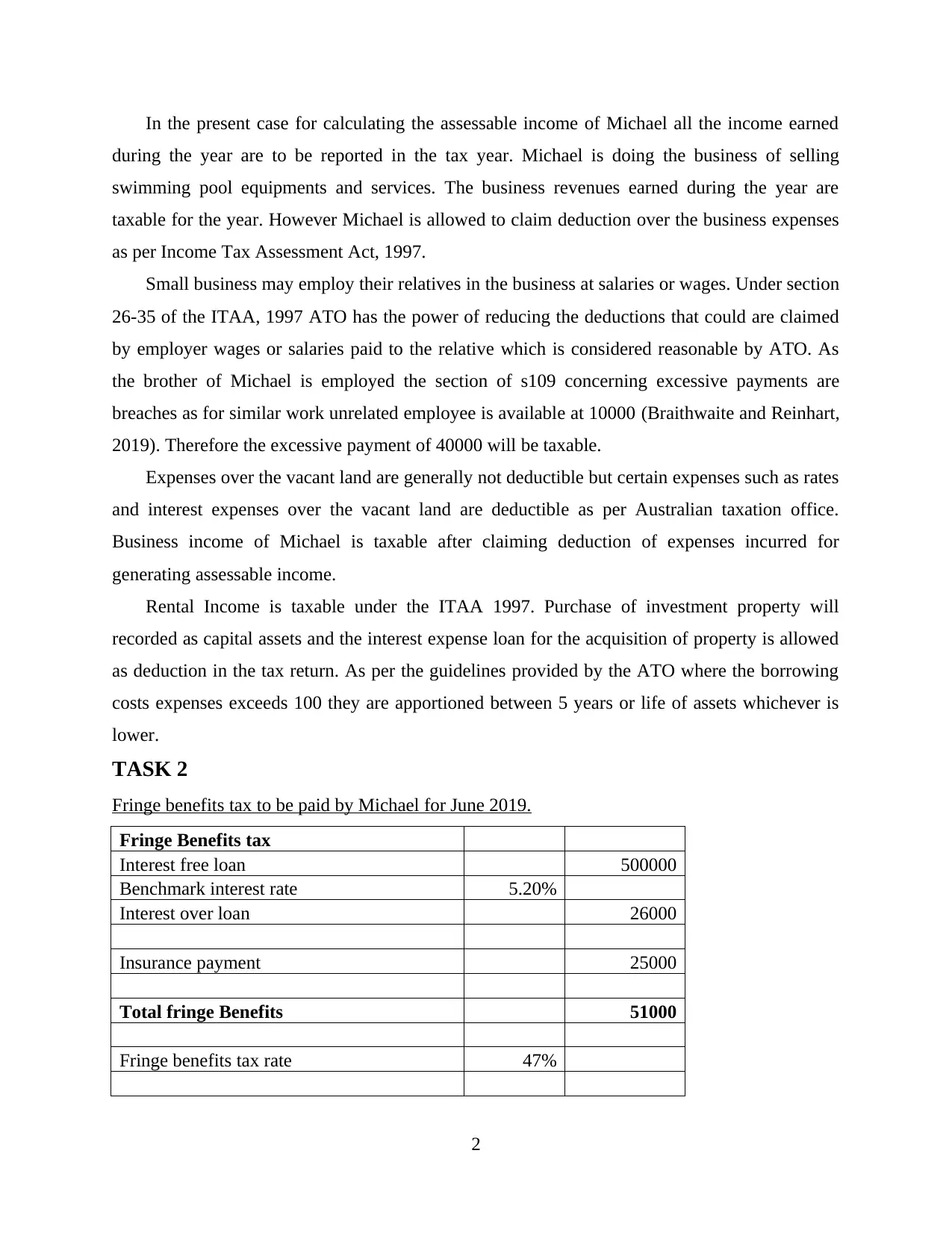

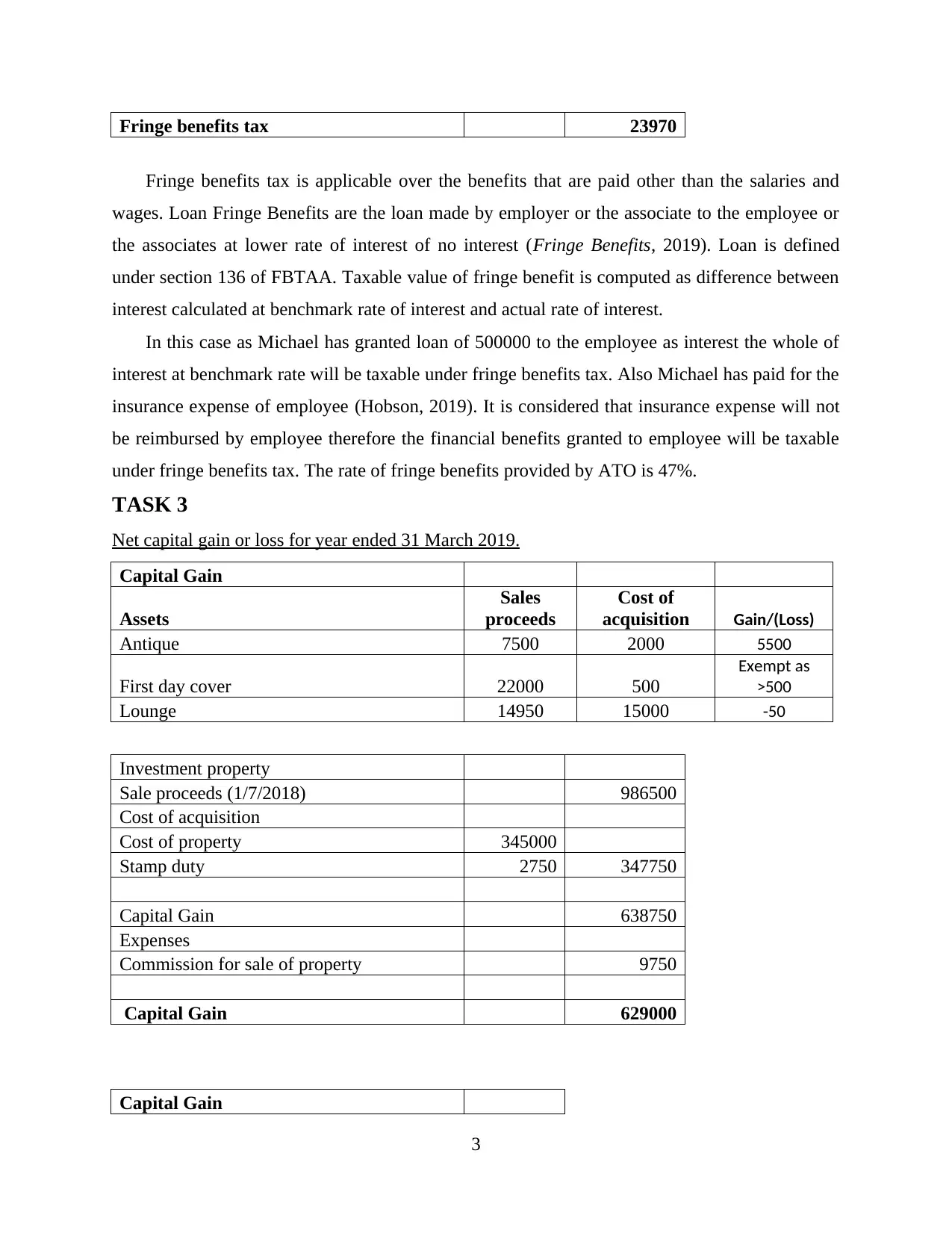

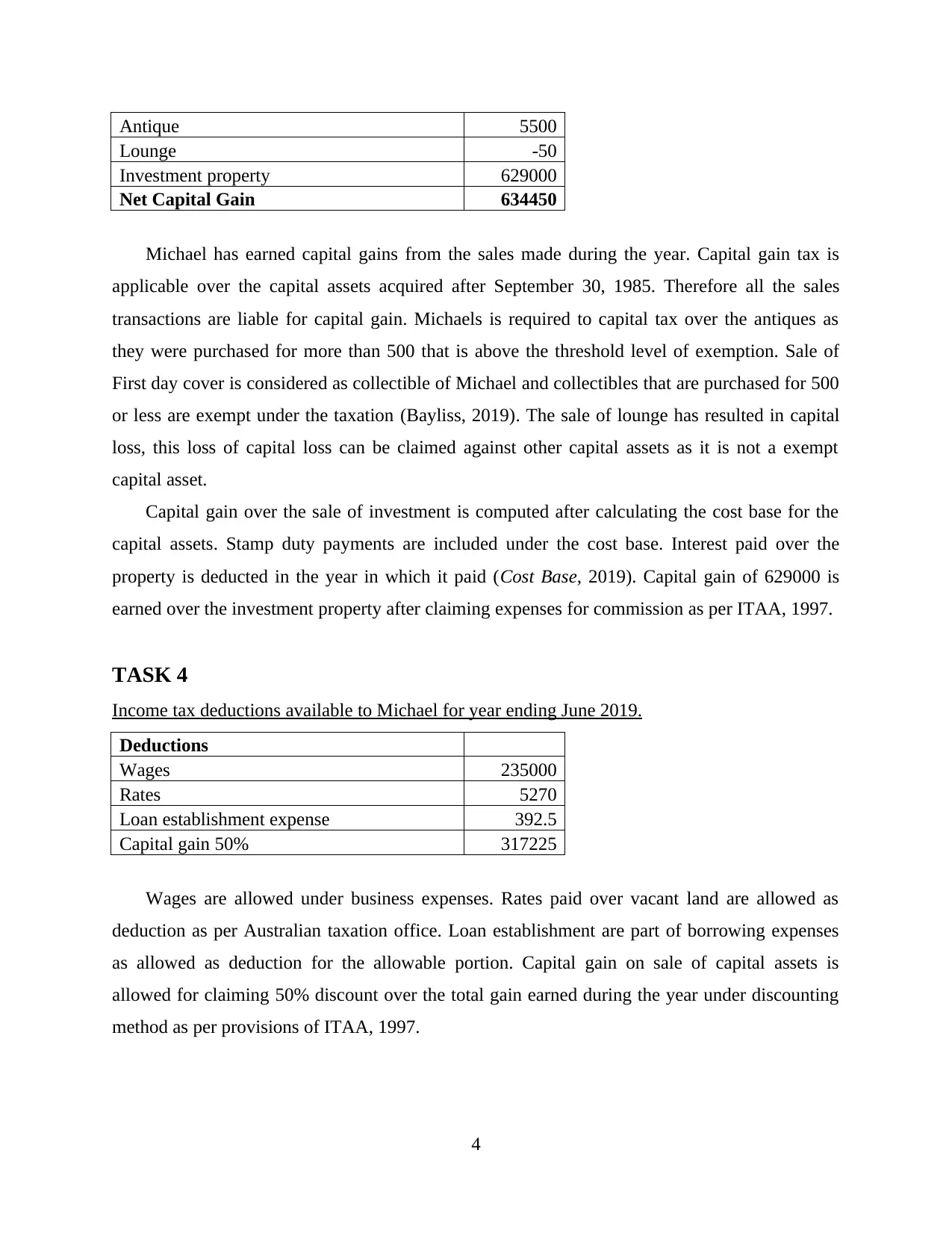

This assignment provides a comprehensive taxation assessment for Michael for the financial year ending June 2019. It begins by calculating Michael's assessable income, which includes revenue from equipment sales, rental income, and capital gains, along with applicable deductions such as wages, rates, and loan expenses. The assessment then calculates the fringe benefits tax (FBT) payable, focusing on an interest-free loan and insurance payments. Next, it determines Michael's net capital gain or loss, considering the sale of various assets like antiques, a lounge, and an investment property, with attention to cost bases and exemptions. Finally, the assignment identifies and details the income tax deductions available to Michael, including wages, rates on vacant land, loan establishment expenses, and the 50% capital gains discount. The analysis is supported by working notes and references to relevant tax legislation and resources.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.