Managerial Accounting Report: Costing Methods and System Improvement

VerifiedAdded on 2021/02/21

|13

|4018

|249

Report

AI Summary

This managerial accounting report examines the core principles of managerial accounting, focusing on the application of absorption and marginal costing methods for Swipe 50 Limited, a laptop screen protector manufacturer. The report includes profit statements prepared using both costing methods, detailed calculations of closing inventory, and a reconciliation of the statements. It highlights the key differences between absorption and marginal costing, emphasizing their impact on profit measurement and decision-making. Furthermore, the report identifies three ways to improve accounting systems and underscores the importance of managerial accountants in manufacturing companies. The analysis covers the implications of each costing method, the advantages of marginal costing for decision-making, and the importance of both methods for financial reporting and internal management. The report concludes with a comprehensive overview of the benefits of each approach and its relevance in business.

Managerial

Accounting

Report

Accounting

Report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

A. Profit Statement......................................................................................................................1

B. Reconciliation of statements ..................................................................................................4

C. Difference between absorption costing and marginal costing ...............................................4

D. Three Ways to improve accounting system...........................................................................7

E. Importance of managerial accountant jobs for manufacturing company...............................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

A. Profit Statement......................................................................................................................1

B. Reconciliation of statements ..................................................................................................4

C. Difference between absorption costing and marginal costing ...............................................4

D. Three Ways to improve accounting system...........................................................................7

E. Importance of managerial accountant jobs for manufacturing company...............................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION

Managerial accounting is the procedure to recognizing, measuring, analysing, interpreting

and communicating information to managers for the pursuit of an organizational goals and

objectives (Achleitner and et.al., 2014) . On the basis of these information a manager take

appropriate decision and arrange all the company's operations. The management accountant of

the company need to determine several events and operational metrics in reference to interpret

the data for using as useful information that can be advantage by the management of company.

There are including some managerial topic like calculation of a producing products costs which

is important for the external financial statements which is essential to follow with US GAAP.

The purpose of the report to develop understanding of the managerial accounting processes and

learn several types of accounting methods. The report based on the Swipe 50 limited, which

manufactures unique screen protector for laptops computers. The presented report base on the

case study where produce profit statement for Swipe 50 Limited through using marginal and

absorption costing method. Define both methods in detail and how to different from each other.

Apart from the report, define different accounting system in three ways and importance of

managerial accountants jobs for manufacturing company.

MAIN BODY

A. Profit Statement

Absorption Costing – It is a costing method where consist of all expenses and costs are

connected with manufacturing a particular product. This method essential for generally accepted

accounting principles (GAAP) as external reporting. To calculate cost of finished products

through absorption costing method consist of different cost such as

Direct materials – These types of material are using to calculate of finish products cost.

Direct Labour – The factory labour cost important to construct a product.

Variable manufacturing overhead – It is operating to provide facility of manufacturing

company in effective manner. For example – supplies and electricity for production

equipment (Ahrens and Khalifa, 2015) .

Fixed manufacturing overhead – The particular cost to conduct a manufacturing facility

which do not vary with production volume. For instance – Rent and insurance.

1

Managerial accounting is the procedure to recognizing, measuring, analysing, interpreting

and communicating information to managers for the pursuit of an organizational goals and

objectives (Achleitner and et.al., 2014) . On the basis of these information a manager take

appropriate decision and arrange all the company's operations. The management accountant of

the company need to determine several events and operational metrics in reference to interpret

the data for using as useful information that can be advantage by the management of company.

There are including some managerial topic like calculation of a producing products costs which

is important for the external financial statements which is essential to follow with US GAAP.

The purpose of the report to develop understanding of the managerial accounting processes and

learn several types of accounting methods. The report based on the Swipe 50 limited, which

manufactures unique screen protector for laptops computers. The presented report base on the

case study where produce profit statement for Swipe 50 Limited through using marginal and

absorption costing method. Define both methods in detail and how to different from each other.

Apart from the report, define different accounting system in three ways and importance of

managerial accountants jobs for manufacturing company.

MAIN BODY

A. Profit Statement

Absorption Costing – It is a costing method where consist of all expenses and costs are

connected with manufacturing a particular product. This method essential for generally accepted

accounting principles (GAAP) as external reporting. To calculate cost of finished products

through absorption costing method consist of different cost such as

Direct materials – These types of material are using to calculate of finish products cost.

Direct Labour – The factory labour cost important to construct a product.

Variable manufacturing overhead – It is operating to provide facility of manufacturing

company in effective manner. For example – supplies and electricity for production

equipment (Ahrens and Khalifa, 2015) .

Fixed manufacturing overhead – The particular cost to conduct a manufacturing facility

which do not vary with production volume. For instance – Rent and insurance.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

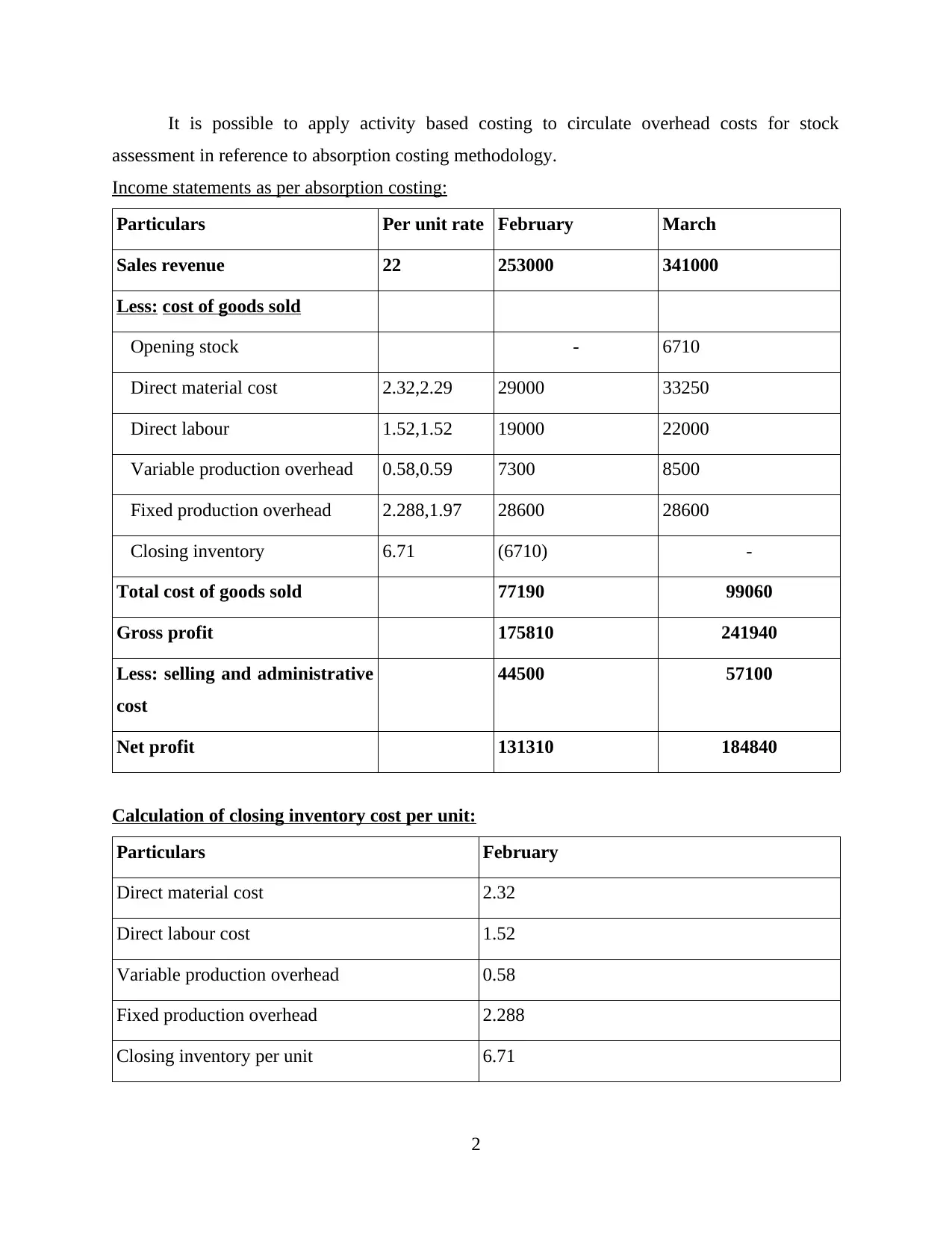

It is possible to apply activity based costing to circulate overhead costs for stock

assessment in reference to absorption costing methodology.

Income statements as per absorption costing:

Particulars Per unit rate February March

Sales revenue 22 253000 341000

Less: cost of goods sold

Opening stock - 6710

Direct material cost 2.32,2.29 29000 33250

Direct labour 1.52,1.52 19000 22000

Variable production overhead 0.58,0.59 7300 8500

Fixed production overhead 2.288,1.97 28600 28600

Closing inventory 6.71 (6710) -

Total cost of goods sold 77190 99060

Gross profit 175810 241940

Less: selling and administrative

cost

44500 57100

Net profit 131310 184840

Calculation of closing inventory cost per unit:

Particulars February

Direct material cost 2.32

Direct labour cost 1.52

Variable production overhead 0.58

Fixed production overhead 2.288

Closing inventory per unit 6.71

2

assessment in reference to absorption costing methodology.

Income statements as per absorption costing:

Particulars Per unit rate February March

Sales revenue 22 253000 341000

Less: cost of goods sold

Opening stock - 6710

Direct material cost 2.32,2.29 29000 33250

Direct labour 1.52,1.52 19000 22000

Variable production overhead 0.58,0.59 7300 8500

Fixed production overhead 2.288,1.97 28600 28600

Closing inventory 6.71 (6710) -

Total cost of goods sold 77190 99060

Gross profit 175810 241940

Less: selling and administrative

cost

44500 57100

Net profit 131310 184840

Calculation of closing inventory cost per unit:

Particulars February

Direct material cost 2.32

Direct labour cost 1.52

Variable production overhead 0.58

Fixed production overhead 2.288

Closing inventory per unit 6.71

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interpretation – As per the above table it has been analysed that there are calculating net

profit through absorption costing method in February and March. Through this method firstly

calculate cost of goods sold where includes opening stock, direct material cost, variable

production overhead, fixed production overhead and closing inventory. These amounts are less

into selling amount than get amount of gross profit. From the amount of gross profit less amount

of selling and administrative cost which is 44500 in February and 57100 in March. After these

all calculation get the amount of Net profit of Swipes 50 limited which is 131310 in February

and 184840 in March. There are calculating cost of closing stock and with the help of direct

material cost, direct labour cost, variable production overhead. In the end of calculation get

amount 6.71 of closing inventory per unit.

Marginal Costing – The managerial cost of manufacturing is the change in total cost that

comes from developing and producing one extra unit. The main purpose to determining the

marginal cost and what point a business accomplish through economic system of scale. To

calculate extra unit of calculation apply the formula by dividing the change in the total cost by

the change in the product result (Boyns, Anderson and Edwards, 2014). It defines that the rate at

which the total cost of a product changes as the manufacturing improve by one unit.

Furthermore, due to fixed costs do not change on the basis of number of products manufactured,

the variable cost is effected only by the alternations in the marginal cost.

Marginal costing cost categorised into variable cost as well as fixed cost and it is mainly

depend on the behaviour of costs with volume of results. As per the particular approach, it is

getting that to recognise the amount of contribution regarding to per product towards fixed

overhead and profits. The contribution departure among sales volume and the marginal cost of

sales.

Income statements as per marginal costing:

Particulars Per unit rate February March

Sales revenue 22 253000 341000

Less: Marginal cost of goods

sold

Opening stock - 4420

Direct material cost 2.32,2.29 29000 33250

3

profit through absorption costing method in February and March. Through this method firstly

calculate cost of goods sold where includes opening stock, direct material cost, variable

production overhead, fixed production overhead and closing inventory. These amounts are less

into selling amount than get amount of gross profit. From the amount of gross profit less amount

of selling and administrative cost which is 44500 in February and 57100 in March. After these

all calculation get the amount of Net profit of Swipes 50 limited which is 131310 in February

and 184840 in March. There are calculating cost of closing stock and with the help of direct

material cost, direct labour cost, variable production overhead. In the end of calculation get

amount 6.71 of closing inventory per unit.

Marginal Costing – The managerial cost of manufacturing is the change in total cost that

comes from developing and producing one extra unit. The main purpose to determining the

marginal cost and what point a business accomplish through economic system of scale. To

calculate extra unit of calculation apply the formula by dividing the change in the total cost by

the change in the product result (Boyns, Anderson and Edwards, 2014). It defines that the rate at

which the total cost of a product changes as the manufacturing improve by one unit.

Furthermore, due to fixed costs do not change on the basis of number of products manufactured,

the variable cost is effected only by the alternations in the marginal cost.

Marginal costing cost categorised into variable cost as well as fixed cost and it is mainly

depend on the behaviour of costs with volume of results. As per the particular approach, it is

getting that to recognise the amount of contribution regarding to per product towards fixed

overhead and profits. The contribution departure among sales volume and the marginal cost of

sales.

Income statements as per marginal costing:

Particulars Per unit rate February March

Sales revenue 22 253000 341000

Less: Marginal cost of goods

sold

Opening stock - 4420

Direct material cost 2.32,2.29 29000 33250

3

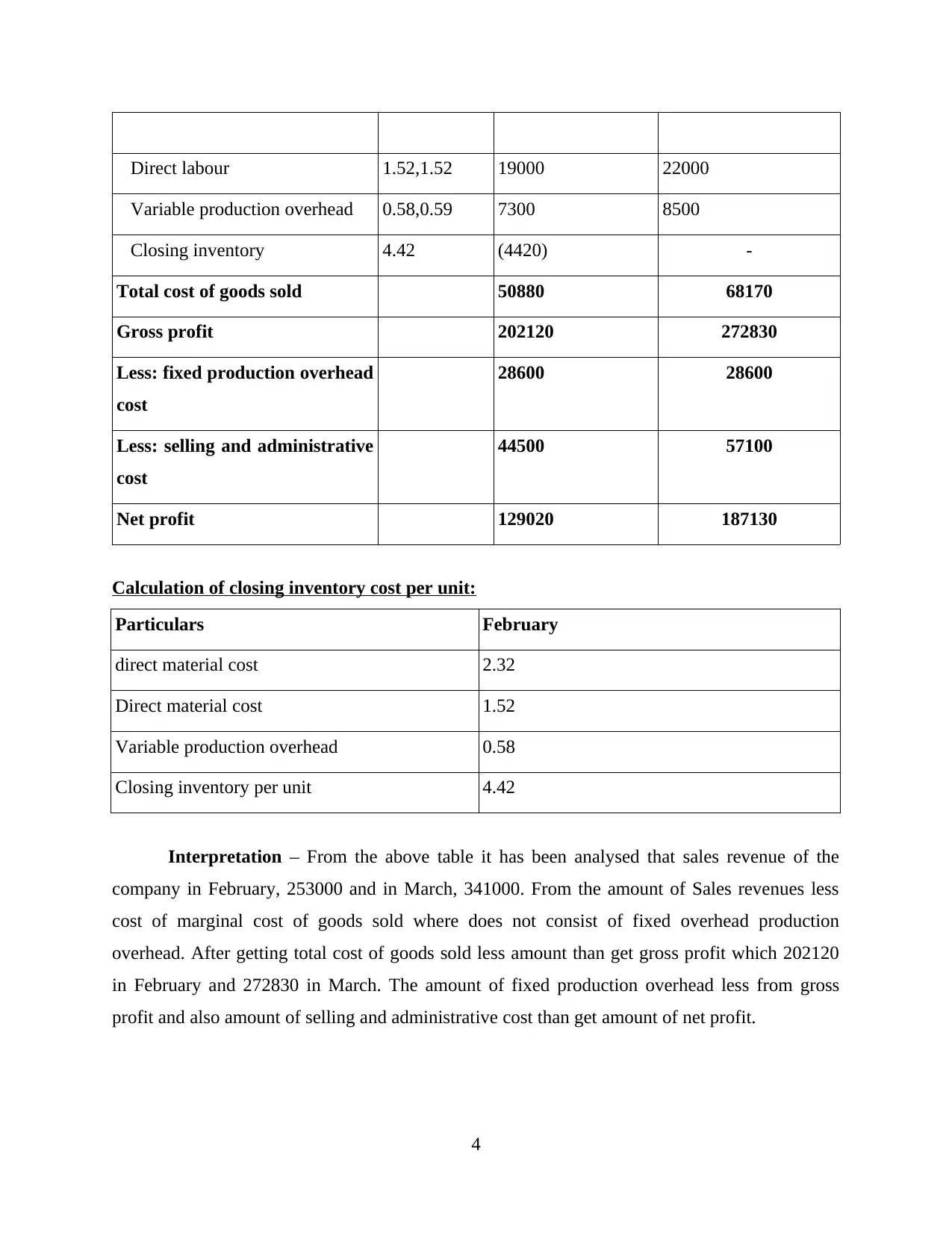

Direct labour 1.52,1.52 19000 22000

Variable production overhead 0.58,0.59 7300 8500

Closing inventory 4.42 (4420) -

Total cost of goods sold 50880 68170

Gross profit 202120 272830

Less: fixed production overhead

cost

28600 28600

Less: selling and administrative

cost

44500 57100

Net profit 129020 187130

Calculation of closing inventory cost per unit:

Particulars February

direct material cost 2.32

Direct material cost 1.52

Variable production overhead 0.58

Closing inventory per unit 4.42

Interpretation – From the above table it has been analysed that sales revenue of the

company in February, 253000 and in March, 341000. From the amount of Sales revenues less

cost of marginal cost of goods sold where does not consist of fixed overhead production

overhead. After getting total cost of goods sold less amount than get gross profit which 202120

in February and 272830 in March. The amount of fixed production overhead less from gross

profit and also amount of selling and administrative cost than get amount of net profit.

4

Variable production overhead 0.58,0.59 7300 8500

Closing inventory 4.42 (4420) -

Total cost of goods sold 50880 68170

Gross profit 202120 272830

Less: fixed production overhead

cost

28600 28600

Less: selling and administrative

cost

44500 57100

Net profit 129020 187130

Calculation of closing inventory cost per unit:

Particulars February

direct material cost 2.32

Direct material cost 1.52

Variable production overhead 0.58

Closing inventory per unit 4.42

Interpretation – From the above table it has been analysed that sales revenue of the

company in February, 253000 and in March, 341000. From the amount of Sales revenues less

cost of marginal cost of goods sold where does not consist of fixed overhead production

overhead. After getting total cost of goods sold less amount than get gross profit which 202120

in February and 272830 in March. The amount of fixed production overhead less from gross

profit and also amount of selling and administrative cost than get amount of net profit.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

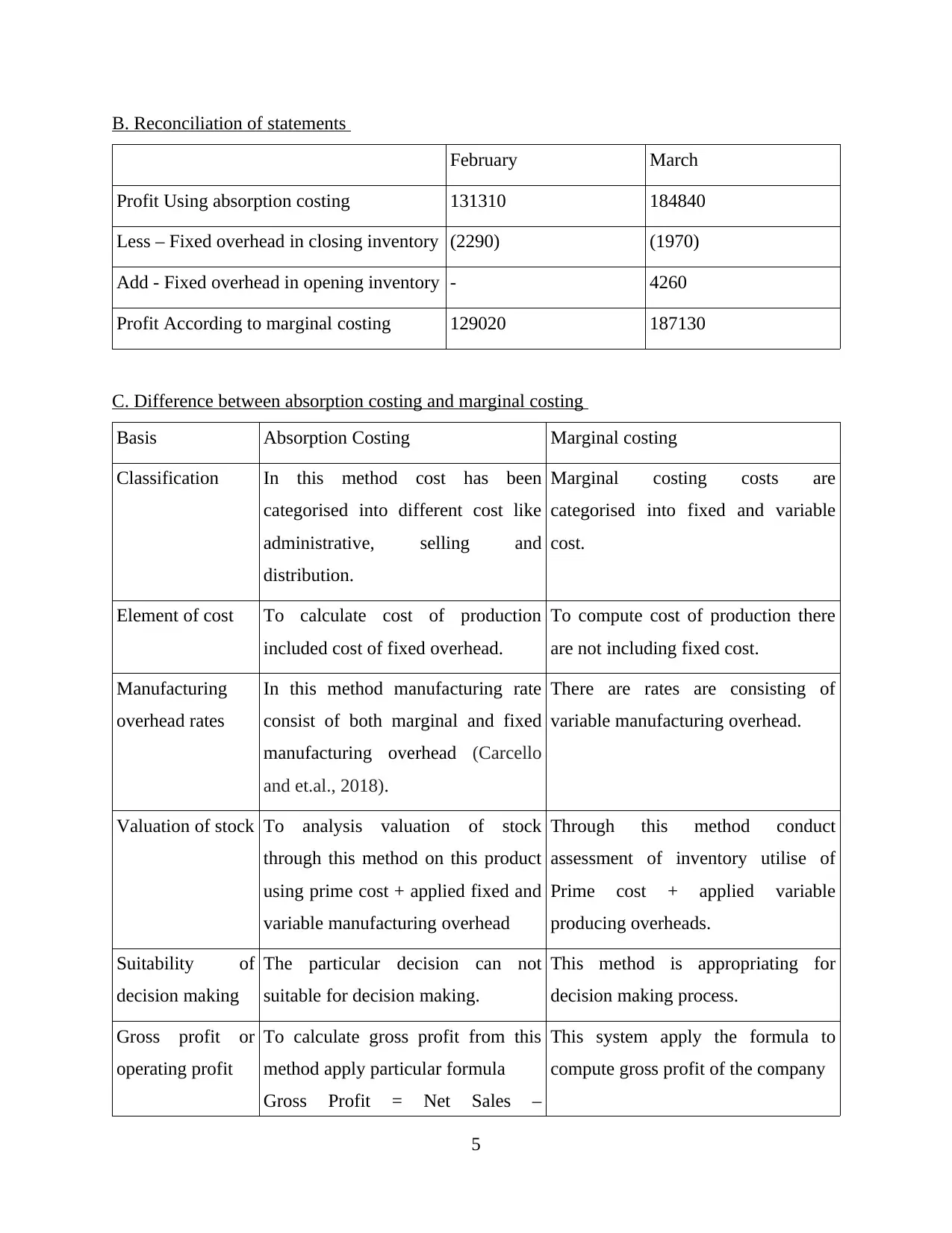

B. Reconciliation of statements

February March

Profit Using absorption costing 131310 184840

Less – Fixed overhead in closing inventory (2290) (1970)

Add - Fixed overhead in opening inventory - 4260

Profit According to marginal costing 129020 187130

C. Difference between absorption costing and marginal costing

Basis Absorption Costing Marginal costing

Classification In this method cost has been

categorised into different cost like

administrative, selling and

distribution.

Marginal costing costs are

categorised into fixed and variable

cost.

Element of cost To calculate cost of production

included cost of fixed overhead.

To compute cost of production there

are not including fixed cost.

Manufacturing

overhead rates

In this method manufacturing rate

consist of both marginal and fixed

manufacturing overhead (Carcello

and et.al., 2018).

There are rates are consisting of

variable manufacturing overhead.

Valuation of stock To analysis valuation of stock

through this method on this product

using prime cost + applied fixed and

variable manufacturing overhead

Through this method conduct

assessment of inventory utilise of

Prime cost + applied variable

producing overheads.

Suitability of

decision making

The particular decision can not

suitable for decision making.

This method is appropriating for

decision making process.

Gross profit or

operating profit

To calculate gross profit from this

method apply particular formula

Gross Profit = Net Sales –

This system apply the formula to

compute gross profit of the company

5

February March

Profit Using absorption costing 131310 184840

Less – Fixed overhead in closing inventory (2290) (1970)

Add - Fixed overhead in opening inventory - 4260

Profit According to marginal costing 129020 187130

C. Difference between absorption costing and marginal costing

Basis Absorption Costing Marginal costing

Classification In this method cost has been

categorised into different cost like

administrative, selling and

distribution.

Marginal costing costs are

categorised into fixed and variable

cost.

Element of cost To calculate cost of production

included cost of fixed overhead.

To compute cost of production there

are not including fixed cost.

Manufacturing

overhead rates

In this method manufacturing rate

consist of both marginal and fixed

manufacturing overhead (Carcello

and et.al., 2018).

There are rates are consisting of

variable manufacturing overhead.

Valuation of stock To analysis valuation of stock

through this method on this product

using prime cost + applied fixed and

variable manufacturing overhead

Through this method conduct

assessment of inventory utilise of

Prime cost + applied variable

producing overheads.

Suitability of

decision making

The particular decision can not

suitable for decision making.

This method is appropriating for

decision making process.

Gross profit or

operating profit

To calculate gross profit from this

method apply particular formula

Gross Profit = Net Sales –

This system apply the formula to

compute gross profit of the company

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

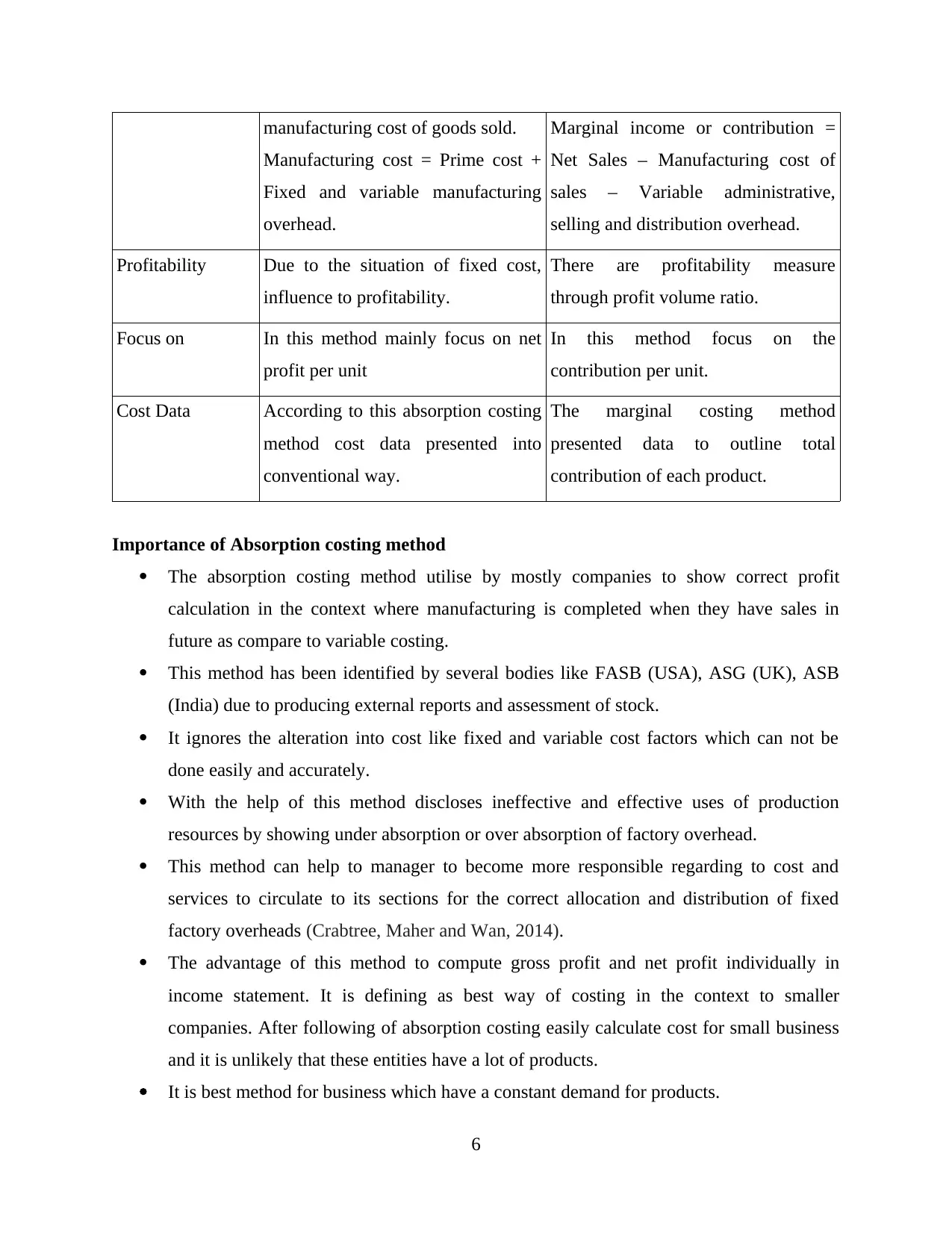

manufacturing cost of goods sold.

Manufacturing cost = Prime cost +

Fixed and variable manufacturing

overhead.

Marginal income or contribution =

Net Sales – Manufacturing cost of

sales – Variable administrative,

selling and distribution overhead.

Profitability Due to the situation of fixed cost,

influence to profitability.

There are profitability measure

through profit volume ratio.

Focus on In this method mainly focus on net

profit per unit

In this method focus on the

contribution per unit.

Cost Data According to this absorption costing

method cost data presented into

conventional way.

The marginal costing method

presented data to outline total

contribution of each product.

Importance of Absorption costing method

The absorption costing method utilise by mostly companies to show correct profit

calculation in the context where manufacturing is completed when they have sales in

future as compare to variable costing.

This method has been identified by several bodies like FASB (USA), ASG (UK), ASB

(India) due to producing external reports and assessment of stock.

It ignores the alteration into cost like fixed and variable cost factors which can not be

done easily and accurately.

With the help of this method discloses ineffective and effective uses of production

resources by showing under absorption or over absorption of factory overhead.

This method can help to manager to become more responsible regarding to cost and

services to circulate to its sections for the correct allocation and distribution of fixed

factory overheads (Crabtree, Maher and Wan, 2014).

The advantage of this method to compute gross profit and net profit individually in

income statement. It is defining as best way of costing in the context to smaller

companies. After following of absorption costing easily calculate cost for small business

and it is unlikely that these entities have a lot of products.

It is best method for business which have a constant demand for products.

6

Manufacturing cost = Prime cost +

Fixed and variable manufacturing

overhead.

Marginal income or contribution =

Net Sales – Manufacturing cost of

sales – Variable administrative,

selling and distribution overhead.

Profitability Due to the situation of fixed cost,

influence to profitability.

There are profitability measure

through profit volume ratio.

Focus on In this method mainly focus on net

profit per unit

In this method focus on the

contribution per unit.

Cost Data According to this absorption costing

method cost data presented into

conventional way.

The marginal costing method

presented data to outline total

contribution of each product.

Importance of Absorption costing method

The absorption costing method utilise by mostly companies to show correct profit

calculation in the context where manufacturing is completed when they have sales in

future as compare to variable costing.

This method has been identified by several bodies like FASB (USA), ASG (UK), ASB

(India) due to producing external reports and assessment of stock.

It ignores the alteration into cost like fixed and variable cost factors which can not be

done easily and accurately.

With the help of this method discloses ineffective and effective uses of production

resources by showing under absorption or over absorption of factory overhead.

This method can help to manager to become more responsible regarding to cost and

services to circulate to its sections for the correct allocation and distribution of fixed

factory overheads (Crabtree, Maher and Wan, 2014).

The advantage of this method to compute gross profit and net profit individually in

income statement. It is defining as best way of costing in the context to smaller

companies. After following of absorption costing easily calculate cost for small business

and it is unlikely that these entities have a lot of products.

It is best method for business which have a constant demand for products.

6

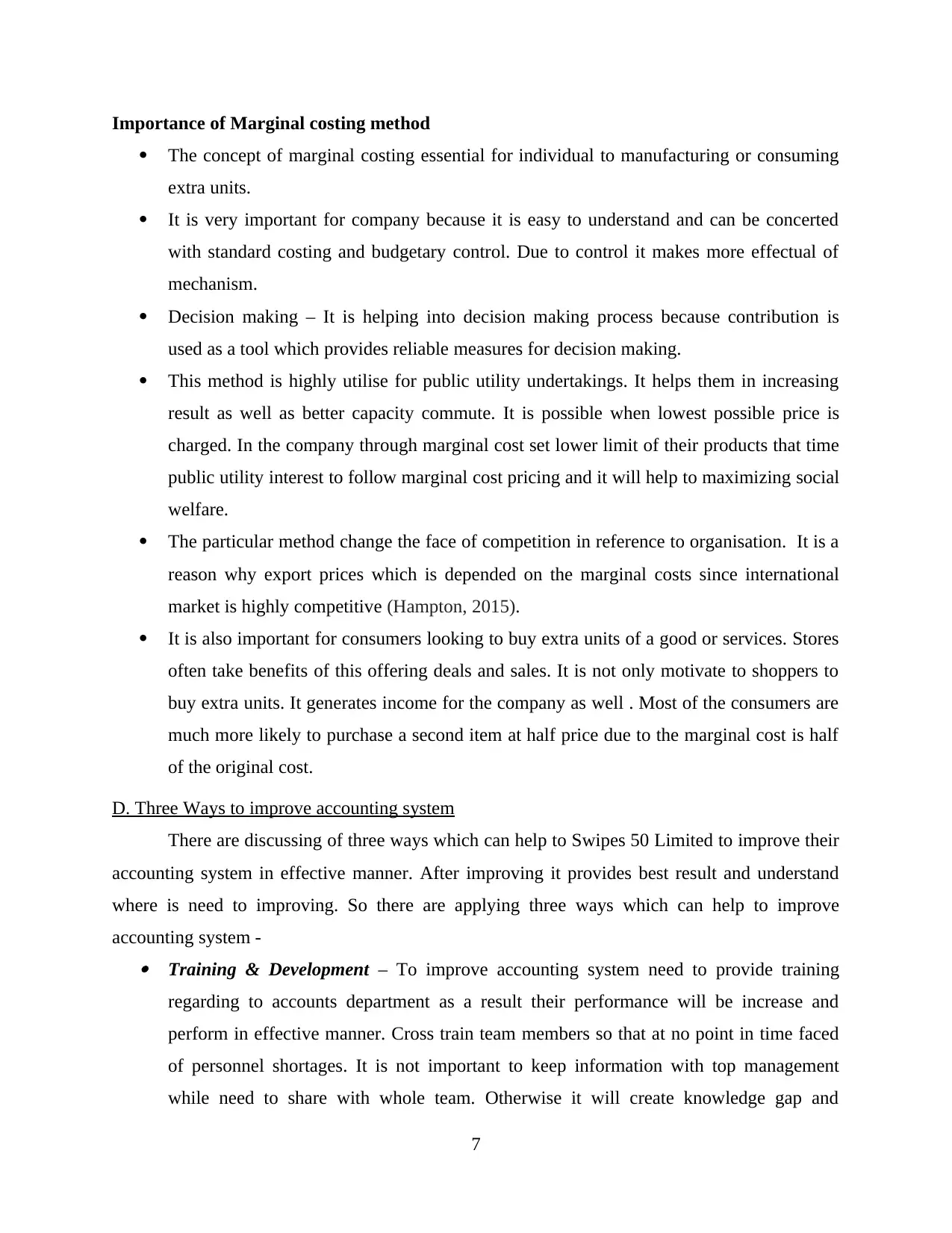

Importance of Marginal costing method

The concept of marginal costing essential for individual to manufacturing or consuming

extra units.

It is very important for company because it is easy to understand and can be concerted

with standard costing and budgetary control. Due to control it makes more effectual of

mechanism.

Decision making – It is helping into decision making process because contribution is

used as a tool which provides reliable measures for decision making.

This method is highly utilise for public utility undertakings. It helps them in increasing

result as well as better capacity commute. It is possible when lowest possible price is

charged. In the company through marginal cost set lower limit of their products that time

public utility interest to follow marginal cost pricing and it will help to maximizing social

welfare.

The particular method change the face of competition in reference to organisation. It is a

reason why export prices which is depended on the marginal costs since international

market is highly competitive (Hampton, 2015).

It is also important for consumers looking to buy extra units of a good or services. Stores

often take benefits of this offering deals and sales. It is not only motivate to shoppers to

buy extra units. It generates income for the company as well . Most of the consumers are

much more likely to purchase a second item at half price due to the marginal cost is half

of the original cost.

D. Three Ways to improve accounting system

There are discussing of three ways which can help to Swipes 50 Limited to improve their

accounting system in effective manner. After improving it provides best result and understand

where is need to improving. So there are applying three ways which can help to improve

accounting system - Training & Development – To improve accounting system need to provide training

regarding to accounts department as a result their performance will be increase and

perform in effective manner. Cross train team members so that at no point in time faced

of personnel shortages. It is not important to keep information with top management

while need to share with whole team. Otherwise it will create knowledge gap and

7

The concept of marginal costing essential for individual to manufacturing or consuming

extra units.

It is very important for company because it is easy to understand and can be concerted

with standard costing and budgetary control. Due to control it makes more effectual of

mechanism.

Decision making – It is helping into decision making process because contribution is

used as a tool which provides reliable measures for decision making.

This method is highly utilise for public utility undertakings. It helps them in increasing

result as well as better capacity commute. It is possible when lowest possible price is

charged. In the company through marginal cost set lower limit of their products that time

public utility interest to follow marginal cost pricing and it will help to maximizing social

welfare.

The particular method change the face of competition in reference to organisation. It is a

reason why export prices which is depended on the marginal costs since international

market is highly competitive (Hampton, 2015).

It is also important for consumers looking to buy extra units of a good or services. Stores

often take benefits of this offering deals and sales. It is not only motivate to shoppers to

buy extra units. It generates income for the company as well . Most of the consumers are

much more likely to purchase a second item at half price due to the marginal cost is half

of the original cost.

D. Three Ways to improve accounting system

There are discussing of three ways which can help to Swipes 50 Limited to improve their

accounting system in effective manner. After improving it provides best result and understand

where is need to improving. So there are applying three ways which can help to improve

accounting system - Training & Development – To improve accounting system need to provide training

regarding to accounts department as a result their performance will be increase and

perform in effective manner. Cross train team members so that at no point in time faced

of personnel shortages. It is not important to keep information with top management

while need to share with whole team. Otherwise it will create knowledge gap and

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

employees of Swipes 50 Limited can not understand of all terms easily (Ionescu, 2017).

To ignore these types of situation by directing continuous process training. Assuring back

ups for all roles and assuring for all important functions are well documented. The

accounting system apply by different members who is working into accounting

department and they are Streamline preparation of financial statements – To improve accounting system there is

required to time creation of financial statements change the areas of concern before they

intensify. When company effectively focus on every transaction and effectively apply all

accounting system that time get optimal results. It can help to analysis the performance of

the company. To improve accounting system for Swipes 50 Limited need to developed

financial statements in proper way. Record every transactions as per the guideline of

GAAP. It can help to remove errors and effectively prepare all financial statements. Increase collaboration with other departments – The accountants and finance

department focus on other departments and maintain relation in effective manner. The

function of accounting department in separation and they often depend on their division

for relating data (Murthy and Rooney 2018) . There are finding several ways in which the

data can be submitted on certain period of time. If in Swipes 50 Limited find an friction

among several sections and the team finance. Fine structure to sort out the issue of

improper accounting system. The manager of company define concerns to the other

managers and let them explain theirs. The company assure about the flow of data in

smoothly manner in several division.

Recognised failure system – In every organisation each system can not working properly

as per the requirement so they are required to identify those systems. Many companies

does not realise that their accounting system which is not running in correct manner.

There are need to continue to direct these imperfect systems. In the context to Swipes 50

limited identify those systems which are not working in perfect manner (Lam, 2014).

As per the above ways it is understand that every organisation apply different accounting

system as per the requirement. So there is need to understand of those systems and effectively

apply in swipes 50 limited.

8

To ignore these types of situation by directing continuous process training. Assuring back

ups for all roles and assuring for all important functions are well documented. The

accounting system apply by different members who is working into accounting

department and they are Streamline preparation of financial statements – To improve accounting system there is

required to time creation of financial statements change the areas of concern before they

intensify. When company effectively focus on every transaction and effectively apply all

accounting system that time get optimal results. It can help to analysis the performance of

the company. To improve accounting system for Swipes 50 Limited need to developed

financial statements in proper way. Record every transactions as per the guideline of

GAAP. It can help to remove errors and effectively prepare all financial statements. Increase collaboration with other departments – The accountants and finance

department focus on other departments and maintain relation in effective manner. The

function of accounting department in separation and they often depend on their division

for relating data (Murthy and Rooney 2018) . There are finding several ways in which the

data can be submitted on certain period of time. If in Swipes 50 Limited find an friction

among several sections and the team finance. Fine structure to sort out the issue of

improper accounting system. The manager of company define concerns to the other

managers and let them explain theirs. The company assure about the flow of data in

smoothly manner in several division.

Recognised failure system – In every organisation each system can not working properly

as per the requirement so they are required to identify those systems. Many companies

does not realise that their accounting system which is not running in correct manner.

There are need to continue to direct these imperfect systems. In the context to Swipes 50

limited identify those systems which are not working in perfect manner (Lam, 2014).

As per the above ways it is understand that every organisation apply different accounting

system as per the requirement. So there is need to understand of those systems and effectively

apply in swipes 50 limited.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

E. Importance of managerial accountant jobs for manufacturing company

Role of managerial accountant in a manufacturing company: The role of a

management accountant is to track internal cost for any business process that can help an

organisation to achieve its desired goals & objectives. Major part of the managerial accountant is

to analyse the records prepared, analyse non-financial information, preparing budgets and

comparing standard & actual data by identifying any improvements that can be made in the

process. Swipes 50 Limited has hired a well efficient management accountant whose roles &

responsibilities include preparing forecasts for the upcoming year which will include a brief idea

of all the income as well as expenditure relating to the period. Some of them are explained

below:

Manage records: In a manufacturing company, major role of a management accountant

is to determine costs associated with different products & services. Further this can comprise of

estimation cost of raw materials, labour, sales, advertising, social media networking etc. In order

to ensure Swipes 50 Limited's financial security as well as strategy implied by mangers, it is

necessary for a managerial accountant to maintain reports & follow various accounting systems.

This can consist of preparing different types of managerial accounting reports that relate to

producing budgets, keeping a track of inventory count. It can further include identifying the

defaulters in Swipes 50 Limited by calculating debtor collection period which states the number

of days a supplier or customer has to repay the due amount (Lee, Bishop and Parker, 2014).

Analysing non-financial information: The crucial role of a management accountant in

Swipes 50 Limited is to analyse and measure the non-financial information. It can be

improvement in decision making process by the members, better stakeholder relationships, lower

risk of problems, increased credibility, greater access to capital etc. In order to achieve growth &

success, a manufacturing company should produce such goods or services that caters to the needs

& requirements of a customer (Mio,Venturelli and Leopizzi, 2015). Since, these will be offered

to the market participants so it is important to attain customer satisfaction by making high quality

products. The managerial accountant is also responsible for getting best efforts out of employees

working in an organisation by providing them with additional incentives like bonus,

performance-based appraisal etc. that will help the company in attaining efficient & effective

results

9

Role of managerial accountant in a manufacturing company: The role of a

management accountant is to track internal cost for any business process that can help an

organisation to achieve its desired goals & objectives. Major part of the managerial accountant is

to analyse the records prepared, analyse non-financial information, preparing budgets and

comparing standard & actual data by identifying any improvements that can be made in the

process. Swipes 50 Limited has hired a well efficient management accountant whose roles &

responsibilities include preparing forecasts for the upcoming year which will include a brief idea

of all the income as well as expenditure relating to the period. Some of them are explained

below:

Manage records: In a manufacturing company, major role of a management accountant

is to determine costs associated with different products & services. Further this can comprise of

estimation cost of raw materials, labour, sales, advertising, social media networking etc. In order

to ensure Swipes 50 Limited's financial security as well as strategy implied by mangers, it is

necessary for a managerial accountant to maintain reports & follow various accounting systems.

This can consist of preparing different types of managerial accounting reports that relate to

producing budgets, keeping a track of inventory count. It can further include identifying the

defaulters in Swipes 50 Limited by calculating debtor collection period which states the number

of days a supplier or customer has to repay the due amount (Lee, Bishop and Parker, 2014).

Analysing non-financial information: The crucial role of a management accountant in

Swipes 50 Limited is to analyse and measure the non-financial information. It can be

improvement in decision making process by the members, better stakeholder relationships, lower

risk of problems, increased credibility, greater access to capital etc. In order to achieve growth &

success, a manufacturing company should produce such goods or services that caters to the needs

& requirements of a customer (Mio,Venturelli and Leopizzi, 2015). Since, these will be offered

to the market participants so it is important to attain customer satisfaction by making high quality

products. The managerial accountant is also responsible for getting best efforts out of employees

working in an organisation by providing them with additional incentives like bonus,

performance-based appraisal etc. that will help the company in attaining efficient & effective

results

9

Preparation of budgets: The main role of a management accountant in Swipes 50

Limited is to prepare budgets. Since these record all the details about the income & expenses

during an accounting year so it is very important to analyse previous statements before preparing

a budget. A review of historical data is also required in order to produce a forecast for the future.

Proper allocation of funds and resources should be done by the managerial accountant in Swipes

50 Limited as any misappropriation can lead to a downfall in profitability situation of the

company (Machado and Alves, 2017).

Comparison of standard and actual budget & identifying improvements: The major

role of a management accountant in Swipes 50 Limited is of forecasting. In relation to that,

comparison of standard and actual budget is essential in order to get an idea about the industry

average for a specific product or service. In a manufacturing company, examination of different

raw material used in production of goods, allocating expenses to separate departments within a

company etc. plays a crucial role when defining organisational goals & objectives. If any

improvements are required in the process so in that case the managerial accountant identifies the

issue and resolves it with the use of various techniques. It can include various measures to

evaluate performance of Swipes 50 Limited like key performance indicator, benchmarking,

balanced scorecard, financial governance etc.

CONCLUSION

As per the above report it has been concluded that managerial accounting essential to

conduct different types of business activities in effective manner. It is used for various activities

and help to get optimal result in the context of an organisation. There are calculate net profit

through absorption costing and marginal costing and get different results from both method.

Both methods are different from each other because it is applying in different styles and

important for organisation. They have their own value which is helping to achieve results of a

company. To improve accounting system apply ways on the basis of company such as training &

development, prepare financial statement in effective manner respectively. The job of managerial

accountant important for manufacturing company because they are aware for their roles and

responsibilities.

10

Limited is to prepare budgets. Since these record all the details about the income & expenses

during an accounting year so it is very important to analyse previous statements before preparing

a budget. A review of historical data is also required in order to produce a forecast for the future.

Proper allocation of funds and resources should be done by the managerial accountant in Swipes

50 Limited as any misappropriation can lead to a downfall in profitability situation of the

company (Machado and Alves, 2017).

Comparison of standard and actual budget & identifying improvements: The major

role of a management accountant in Swipes 50 Limited is of forecasting. In relation to that,

comparison of standard and actual budget is essential in order to get an idea about the industry

average for a specific product or service. In a manufacturing company, examination of different

raw material used in production of goods, allocating expenses to separate departments within a

company etc. plays a crucial role when defining organisational goals & objectives. If any

improvements are required in the process so in that case the managerial accountant identifies the

issue and resolves it with the use of various techniques. It can include various measures to

evaluate performance of Swipes 50 Limited like key performance indicator, benchmarking,

balanced scorecard, financial governance etc.

CONCLUSION

As per the above report it has been concluded that managerial accounting essential to

conduct different types of business activities in effective manner. It is used for various activities

and help to get optimal result in the context of an organisation. There are calculate net profit

through absorption costing and marginal costing and get different results from both method.

Both methods are different from each other because it is applying in different styles and

important for organisation. They have their own value which is helping to achieve results of a

company. To improve accounting system apply ways on the basis of company such as training &

development, prepare financial statement in effective manner respectively. The job of managerial

accountant important for manufacturing company because they are aware for their roles and

responsibilities.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.