Analyzing Absorption and Marginal Costing for Financial Reporting

VerifiedAdded on 2023/01/07

|4

|615

|40

Homework Assignment

AI Summary

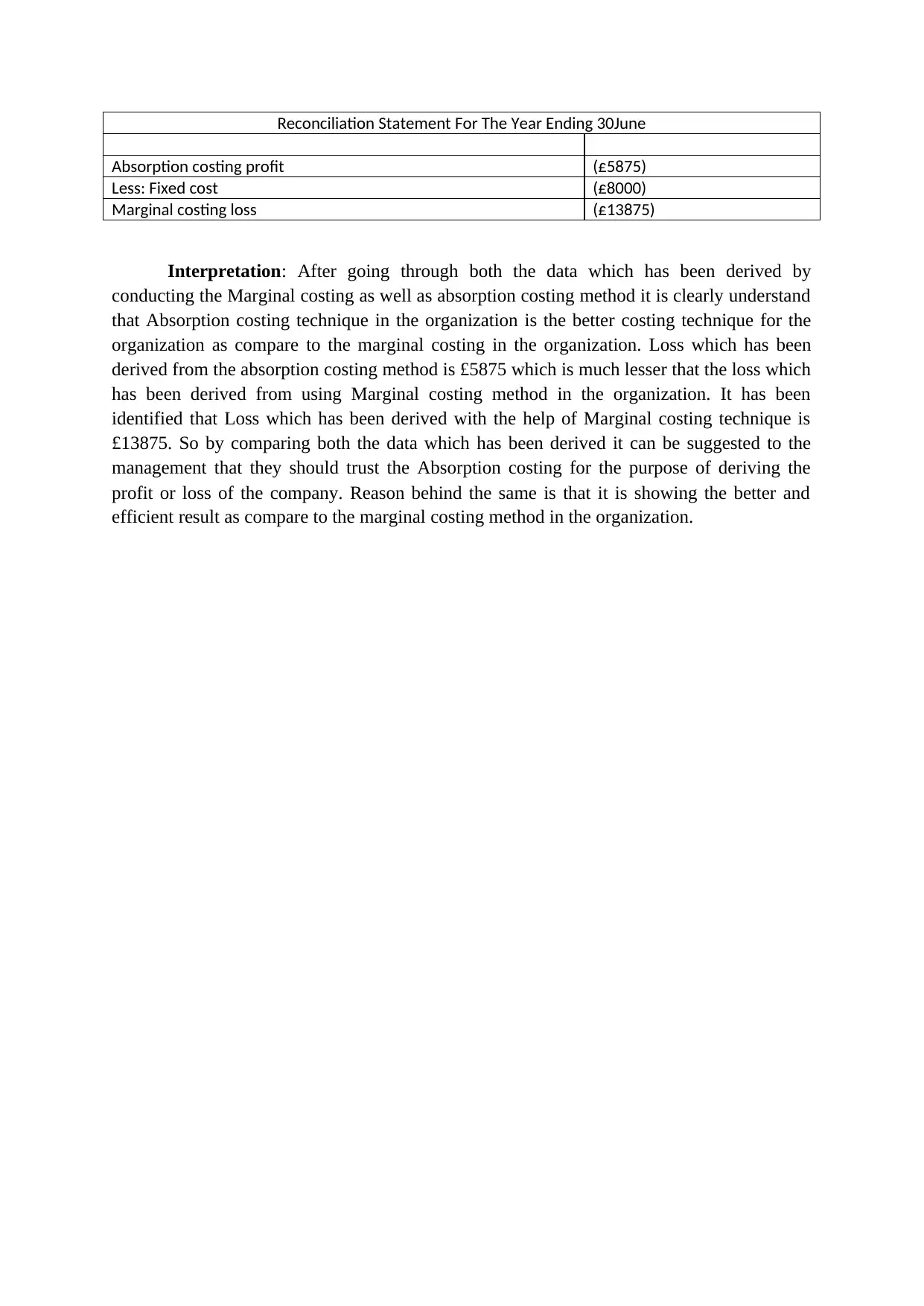

This assignment delves into the analysis of absorption and marginal costing methods, crucial for financial reporting and management accounting. The document includes detailed profit and loss statements for both methods, comparing their impacts on financial results. The student presents calculations, demonstrating the application of each costing technique. A reconciliation statement is provided to explain the differences in profit or loss derived from each method. The assignment concludes with an interpretation, suggesting the preferred costing method based on the analysis. The student recommends absorption costing as a more effective approach based on the calculated results, and also includes relevant references to support the analysis.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.