Business Analysis and Interpretation Assignment Solution ACC10707

VerifiedAdded on 2022/11/01

|6

|517

|66

Homework Assignment

AI Summary

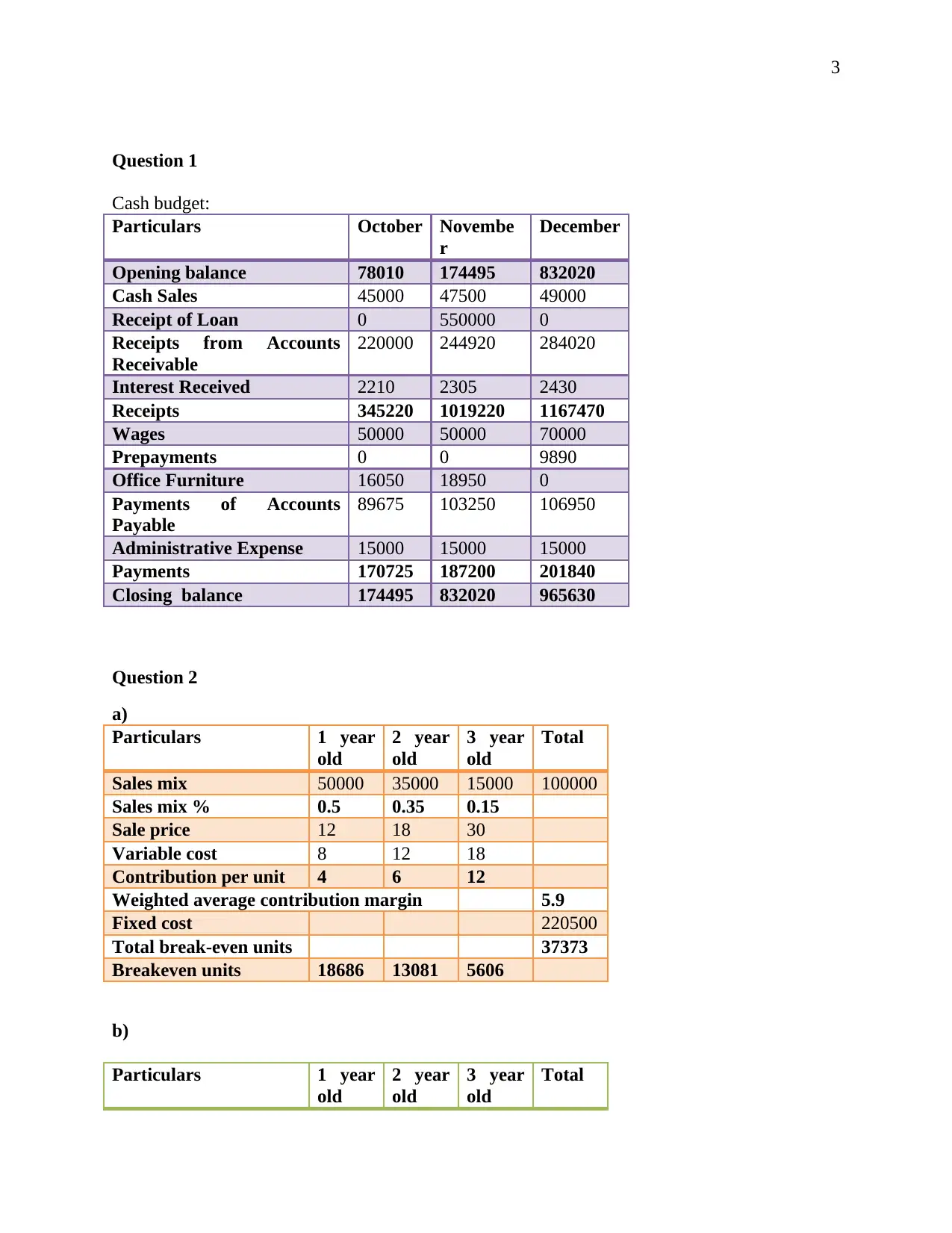

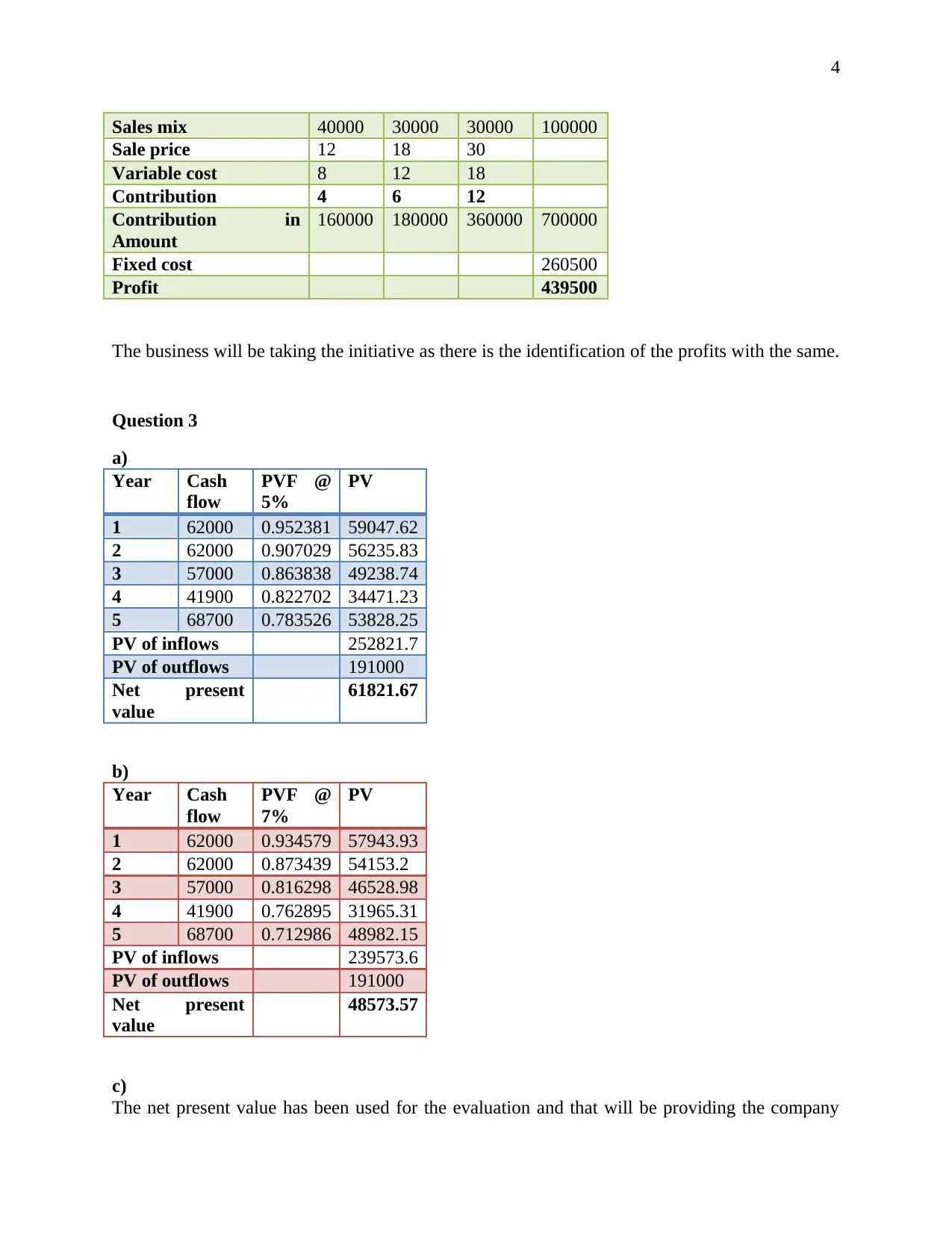

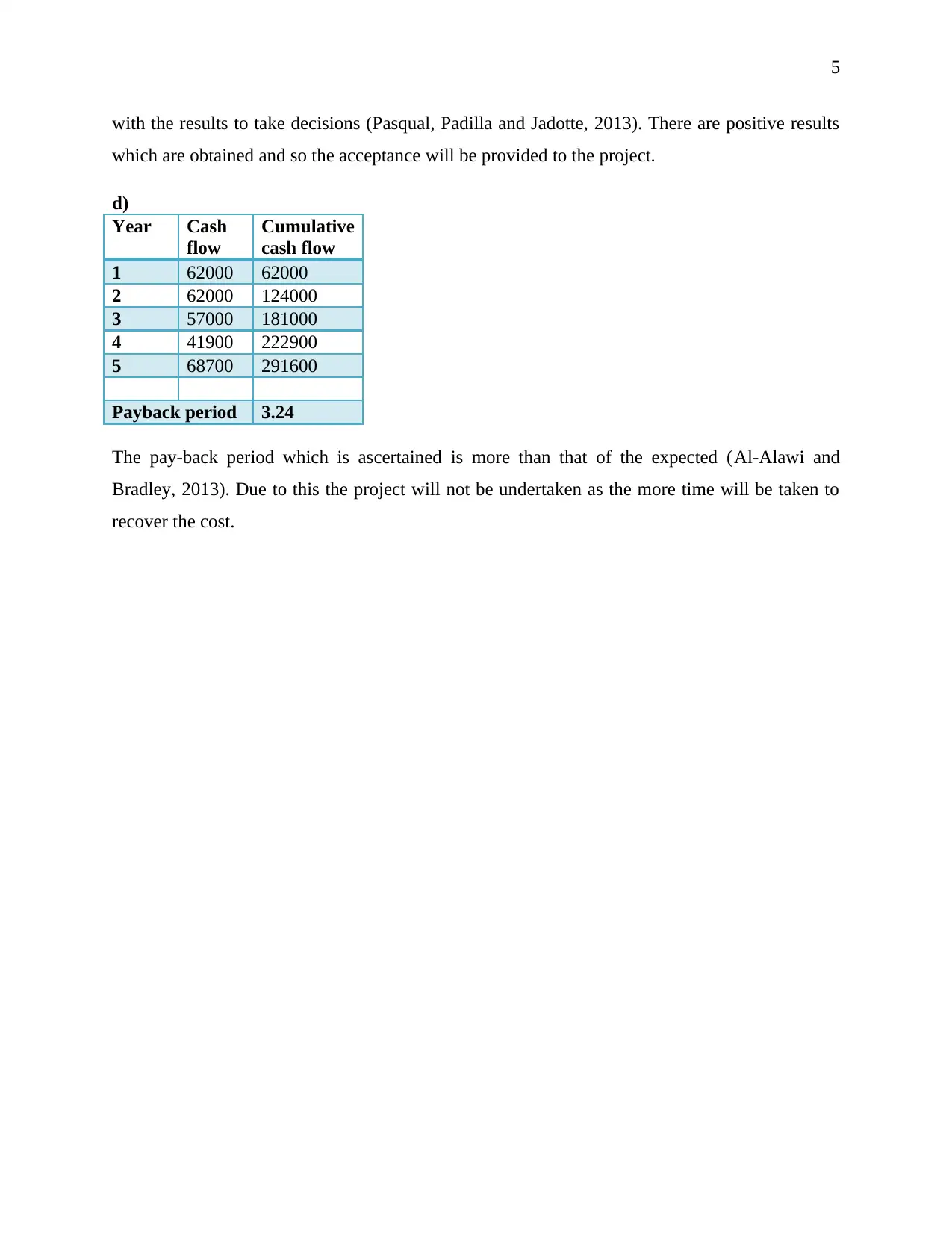

This document presents a comprehensive solution to a finance assignment, addressing key aspects of business analysis and interpretation. The assignment includes a detailed cash budget for Garden Enterprises, projecting cash inflows and outflows over a three-month period. It further analyzes the business's break-even point under different sales mix scenarios, calculating the weighted average contribution margin and break-even units. Additionally, the assignment delves into investment appraisal techniques, calculating the net present value (NPV) and payback period for a given project. The NPV is computed at both 5% and 7% discount rates to evaluate the project's profitability, and the payback period determines the time required to recover the initial investment. The document also references academic literature to support the methodologies used. The solution provides a complete analysis of the given financial data and offers insights into making sound financial decisions.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.