ACC202 Management Accounting: Transfer Pricing Analysis

VerifiedAdded on 2022/11/29

|4

|615

|391

Practical Assignment

AI Summary

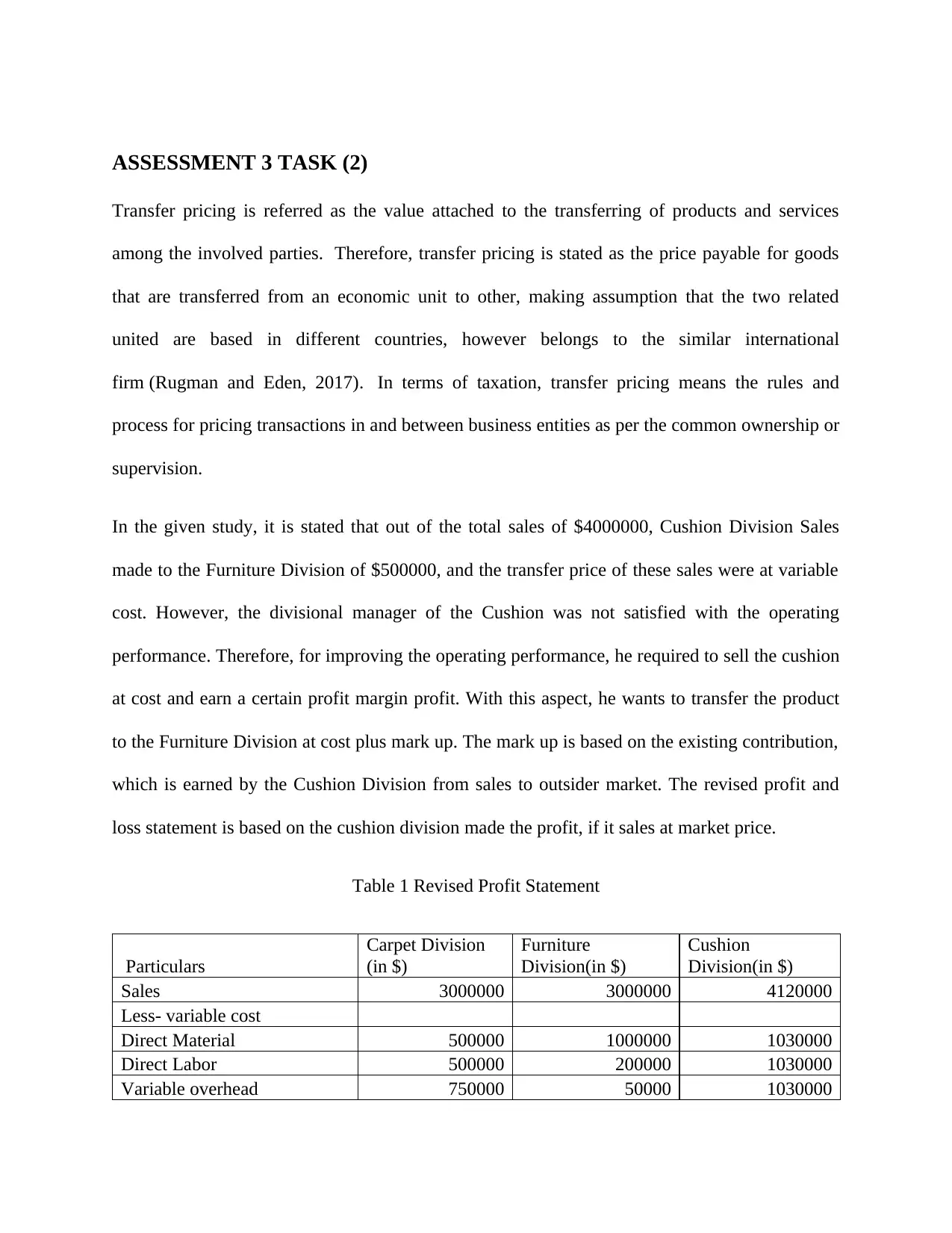

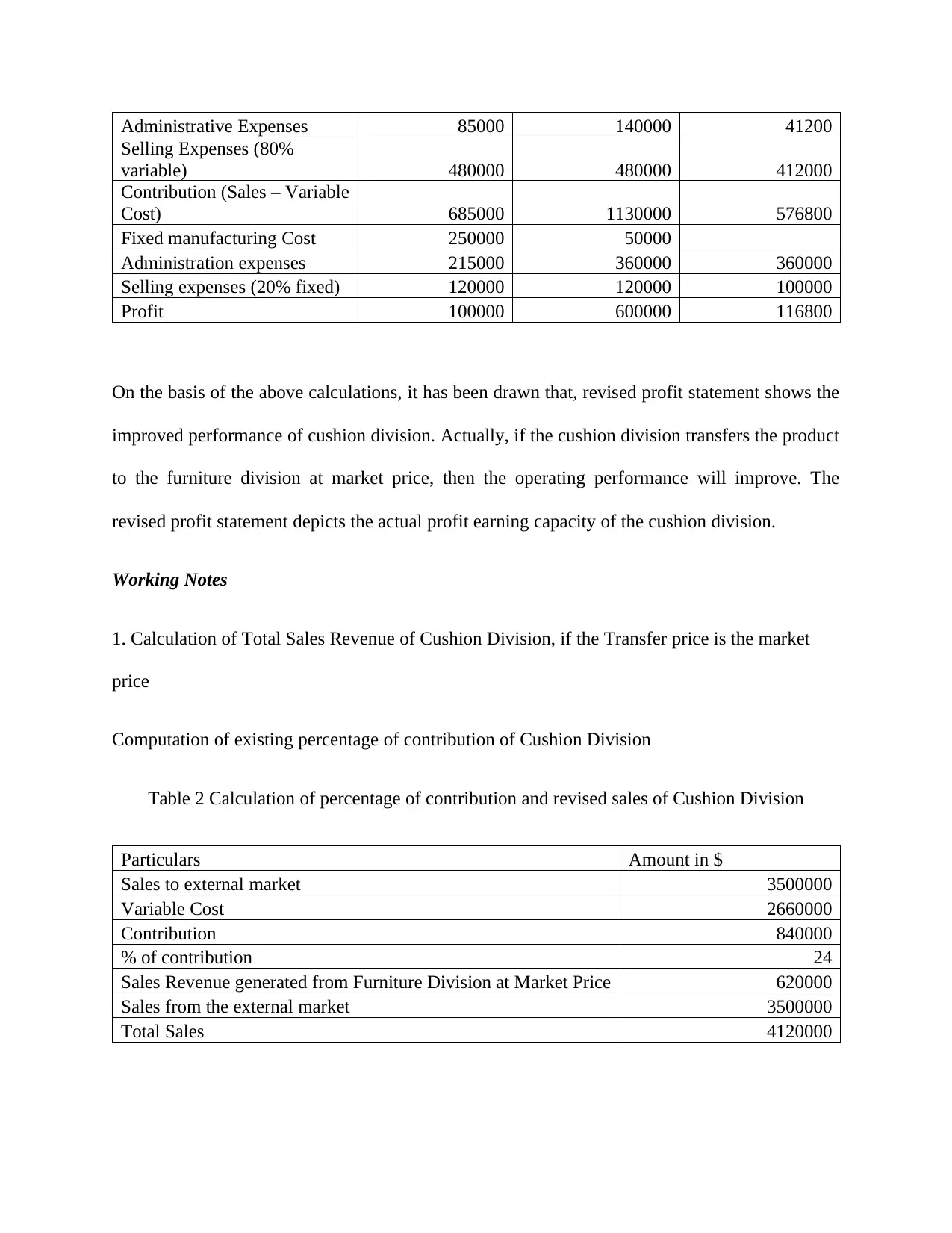

This assignment explores the concept of transfer pricing within a management accounting context, specifically focusing on how different transfer pricing methods affect divisional performance and profitability. The scenario involves two divisions, Cushion and Furniture, within a company, and examines the impact of transferring goods between them at variable cost versus market price. The solution includes a revised profit statement demonstrating the improved performance of the Cushion Division when transferring products at market price. The analysis incorporates calculations of contribution margin, variable costs, and total sales revenue to support the conclusions. The assignment also highlights the importance of considering the percentage of contribution and the impact of variable selling expenses on overall profitability. The provided solution showcases a practical application of transfer pricing principles in decision-making and performance evaluation within a business setting.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.