ACC211 Task 2: Financial Viability and Sensitivity Analysis of Project

VerifiedAdded on 2023/06/12

|25

|2866

|486

Report

AI Summary

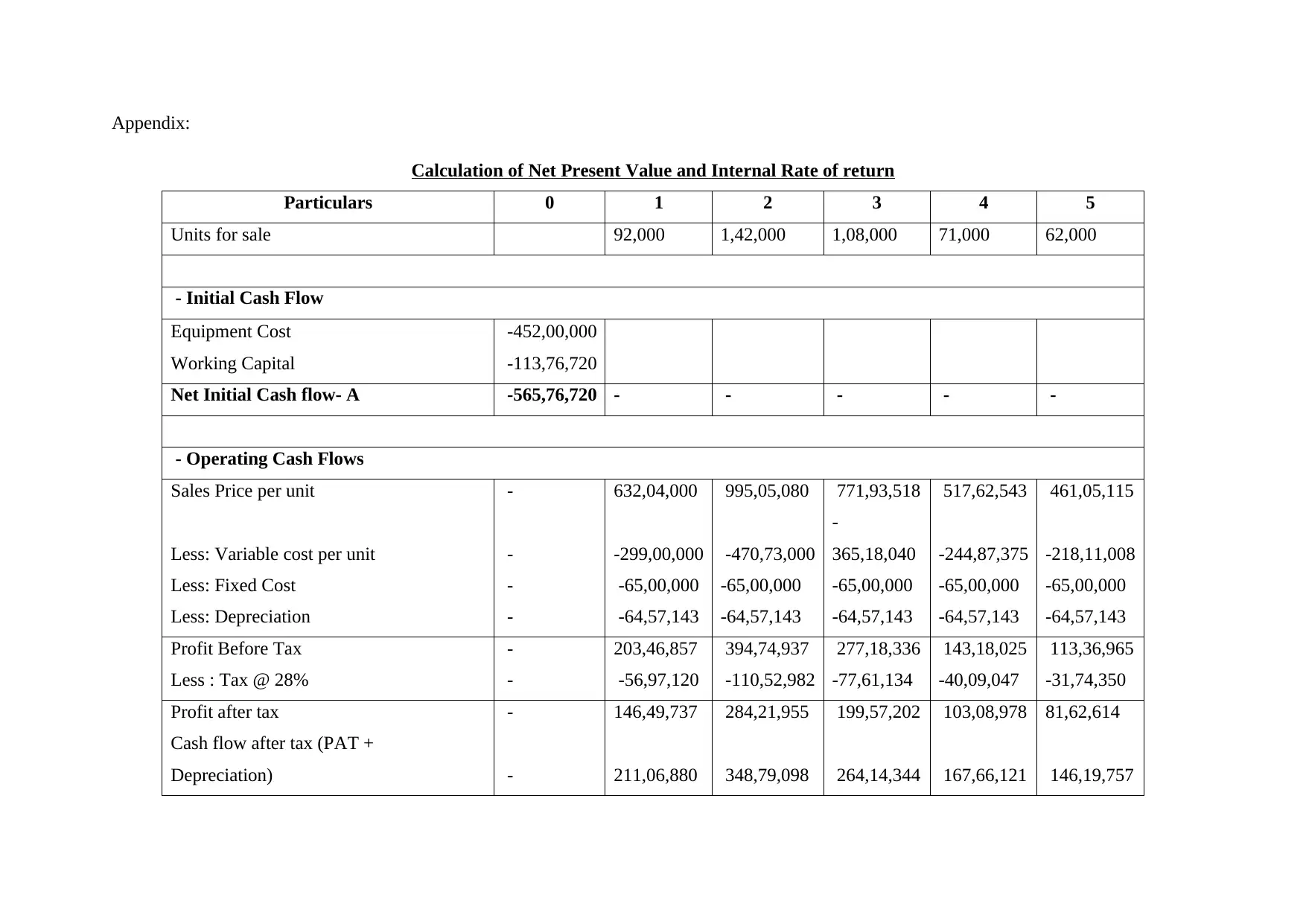

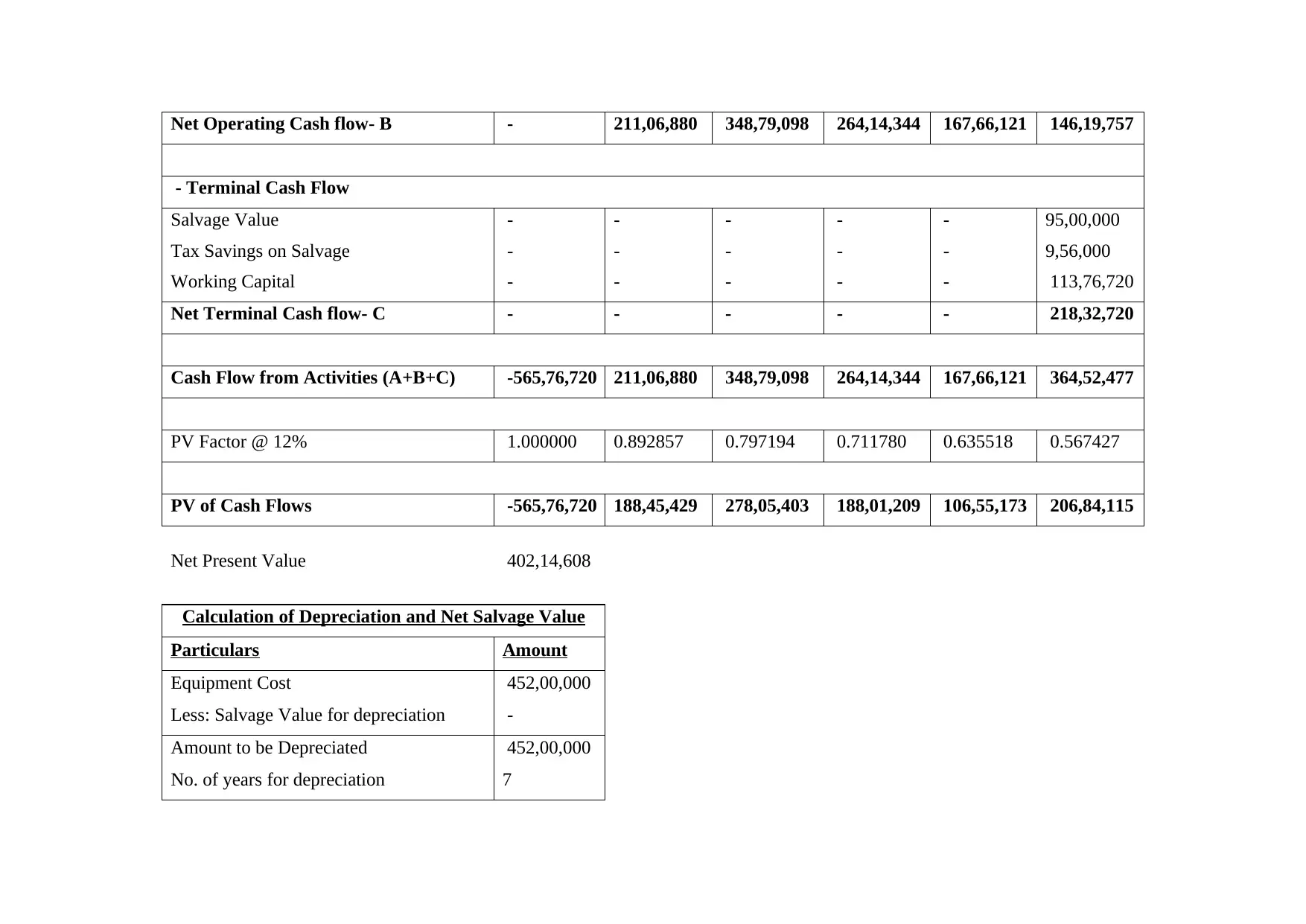

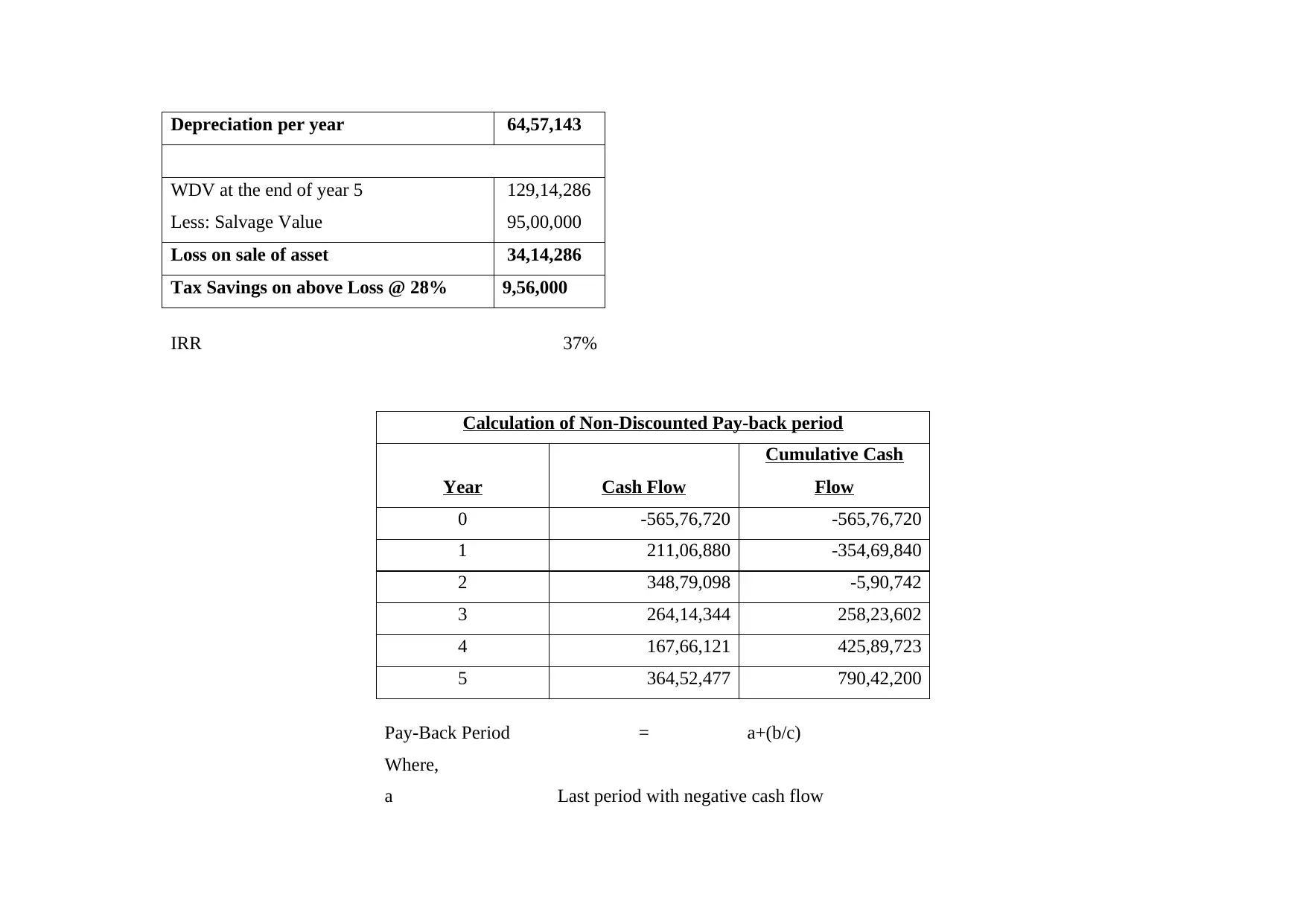

This report assesses the financial viability of a new project using capital budgeting techniques such as Net Present Value (NPV), Internal Rate of Return (IRR), payback period, and profitability index. The analysis indicates a positive NPV and an IRR exceeding the required rate of return, suggesting the project's financial feasibility. Sensitivity analysis is performed to evaluate the impact of changes in sales price and quantity on the project's NPV, revealing the project's sensitivity to these factors. The report also addresses the effect of potential loss of sales from other models due to the new project and concludes with a recommendation to accept the project based on its projected high returns. The calculations and analysis are based on provided financial data and standard capital budgeting principles.

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.