Management Accounting Report: Financial and Non-Financial Information

VerifiedAdded on 2020/07/23

|20

|5688

|137

Report

AI Summary

This report on management accounting provides a comprehensive overview of the subject, focusing on its application within Tech (UK) Limited. It begins by differentiating between management and financial accounting, highlighting the importance of management accounting in strategic management, performance appraisal, and risk reduction. The report then delves into various management accounting systems, including cost accounting, inventory management, and job costing, explaining their roles in providing critical financial and non-financial information for decision-making. Furthermore, the report examines different types of managerial accounting reports, such as budget reports, accounts receivable reports, and job cost reports, and their significance in planning, control, and performance evaluation. The report also explores the calculation of costs using marginal costing and the preparation of income statements. Finally, it discusses the advantages and disadvantages of different types of budgets and their use as tools for planning and control, concluding with the application of management accounting in addressing financial problems. Overall, the report aims to provide a detailed understanding of management accounting principles and their practical applications in a business context.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1. Management accounting and essential requirements of management accounting systems..3

P2. Different types of managerial accounting reports and their importance..........................6

M1...........................................................................................................................................8

D1...........................................................................................................................................8

TASK 2............................................................................................................................................9

P3 Calculation of cost and preparation of income statement.................................................9

M2.........................................................................................................................................11

D2.........................................................................................................................................12

TASK 3..........................................................................................................................................12

P4 Different kind of budgets and their advantages and disadvantages................................12

M3.........................................................................................................................................14

D3.........................................................................................................................................14

TASK 4..........................................................................................................................................15

P5 Use of management accounting to respond financial problem.......................................15

M4.........................................................................................................................................16

CONCLUSION .............................................................................................................................16

REFERENCES..............................................................................................................................18

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1. Management accounting and essential requirements of management accounting systems..3

P2. Different types of managerial accounting reports and their importance..........................6

M1...........................................................................................................................................8

D1...........................................................................................................................................8

TASK 2............................................................................................................................................9

P3 Calculation of cost and preparation of income statement.................................................9

M2.........................................................................................................................................11

D2.........................................................................................................................................12

TASK 3..........................................................................................................................................12

P4 Different kind of budgets and their advantages and disadvantages................................12

M3.........................................................................................................................................14

D3.........................................................................................................................................14

TASK 4..........................................................................................................................................15

P5 Use of management accounting to respond financial problem.......................................15

M4.........................................................................................................................................16

CONCLUSION .............................................................................................................................16

REFERENCES..............................................................................................................................18

INTRODUCTION

Management accounting system includes job costing, cost accounting, inventory

management, etc. which helps the accountant of company to provide true information regarding

transaction.. These information are used by the management to make effective decisions

regarding various operations of company. This helps the manager of company to perform three

main functions like strategic management, performance appraisal and risk reduction. This

provides an opportunity to company to effectively guide their employees and achieve

organisational objectives. Tech (UK) Limited is producing special charger for mobile telephone

and other gadgets for the retail outlets in the UK (Baldvinsdottir, Mitchell and Nørreklit, 2010).

In the present report, difference between management accounting and financial

accounting, importance of management accounting in decision making, different management

accounting systems, different types of managerial reports and their importance in providing

relevant information will be discussed. Here, advantages and disadvantages of different kinds of

budgets with their importance as a tool for planning and control purposes will also be discussed.

TASK 1

P1. Management accounting and essential requirements of management accounting systems

Management Accounting

Management accounting includes the use of different accounts and reports to provide

information regarding different activities of business. This will have huge importance regarding

improvement of decision making power of their different stakeholders. These accounts and

reports and good planning and risk management tools which helps in removal of the risk and

accomplishment of their targets.

Management accounting system uses various provisions of accounting to prepare

different accounts which provide accurate information regarding different important functions of

Management accounting system includes job costing, cost accounting, inventory

management, etc. which helps the accountant of company to provide true information regarding

transaction.. These information are used by the management to make effective decisions

regarding various operations of company. This helps the manager of company to perform three

main functions like strategic management, performance appraisal and risk reduction. This

provides an opportunity to company to effectively guide their employees and achieve

organisational objectives. Tech (UK) Limited is producing special charger for mobile telephone

and other gadgets for the retail outlets in the UK (Baldvinsdottir, Mitchell and Nørreklit, 2010).

In the present report, difference between management accounting and financial

accounting, importance of management accounting in decision making, different management

accounting systems, different types of managerial reports and their importance in providing

relevant information will be discussed. Here, advantages and disadvantages of different kinds of

budgets with their importance as a tool for planning and control purposes will also be discussed.

TASK 1

P1. Management accounting and essential requirements of management accounting systems

Management Accounting

Management accounting includes the use of different accounts and reports to provide

information regarding different activities of business. This will have huge importance regarding

improvement of decision making power of their different stakeholders. These accounts and

reports and good planning and risk management tools which helps in removal of the risk and

accomplishment of their targets.

Management accounting system uses various provisions of accounting to prepare

different accounts which provide accurate information regarding different important functions of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company. This helps the manager of company to perform main three functions which are defined

as below:

Strategic management: This increases the role of accountant of company to effectively

organise the activities and operations.

Performance management: These accounting system provides informational base

which provides chances to appraise the performance of their employees with standards

and provide solution to improve their skills as well (Christ and Burritt, 2013).

Risk management: Various information regarding different departments of company

helps the manager to make effective decisions and policies. This provides opportunity to

reduce the risks among different functions of company.

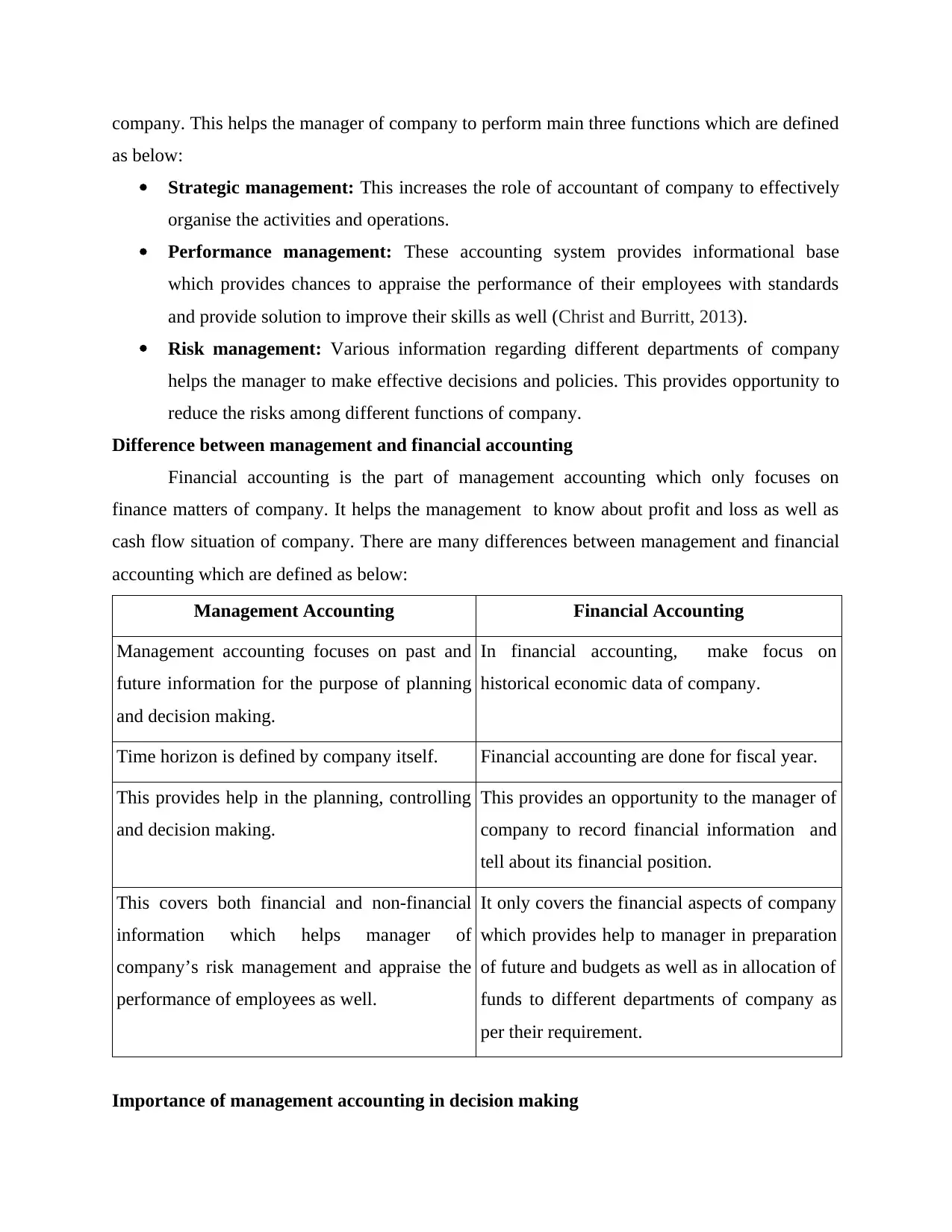

Difference between management and financial accounting

Financial accounting is the part of management accounting which only focuses on

finance matters of company. It helps the management to know about profit and loss as well as

cash flow situation of company. There are many differences between management and financial

accounting which are defined as below:

Management Accounting Financial Accounting

Management accounting focuses on past and

future information for the purpose of planning

and decision making.

In financial accounting, make focus on

historical economic data of company.

Time horizon is defined by company itself. Financial accounting are done for fiscal year.

This provides help in the planning, controlling

and decision making.

This provides an opportunity to the manager of

company to record financial information and

tell about its financial position.

This covers both financial and non-financial

information which helps manager of

company’s risk management and appraise the

performance of employees as well.

It only covers the financial aspects of company

which provides help to manager in preparation

of future and budgets as well as in allocation of

funds to different departments of company as

per their requirement.

Importance of management accounting in decision making

as below:

Strategic management: This increases the role of accountant of company to effectively

organise the activities and operations.

Performance management: These accounting system provides informational base

which provides chances to appraise the performance of their employees with standards

and provide solution to improve their skills as well (Christ and Burritt, 2013).

Risk management: Various information regarding different departments of company

helps the manager to make effective decisions and policies. This provides opportunity to

reduce the risks among different functions of company.

Difference between management and financial accounting

Financial accounting is the part of management accounting which only focuses on

finance matters of company. It helps the management to know about profit and loss as well as

cash flow situation of company. There are many differences between management and financial

accounting which are defined as below:

Management Accounting Financial Accounting

Management accounting focuses on past and

future information for the purpose of planning

and decision making.

In financial accounting, make focus on

historical economic data of company.

Time horizon is defined by company itself. Financial accounting are done for fiscal year.

This provides help in the planning, controlling

and decision making.

This provides an opportunity to the manager of

company to record financial information and

tell about its financial position.

This covers both financial and non-financial

information which helps manager of

company’s risk management and appraise the

performance of employees as well.

It only covers the financial aspects of company

which provides help to manager in preparation

of future and budgets as well as in allocation of

funds to different departments of company as

per their requirement.

Importance of management accounting in decision making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

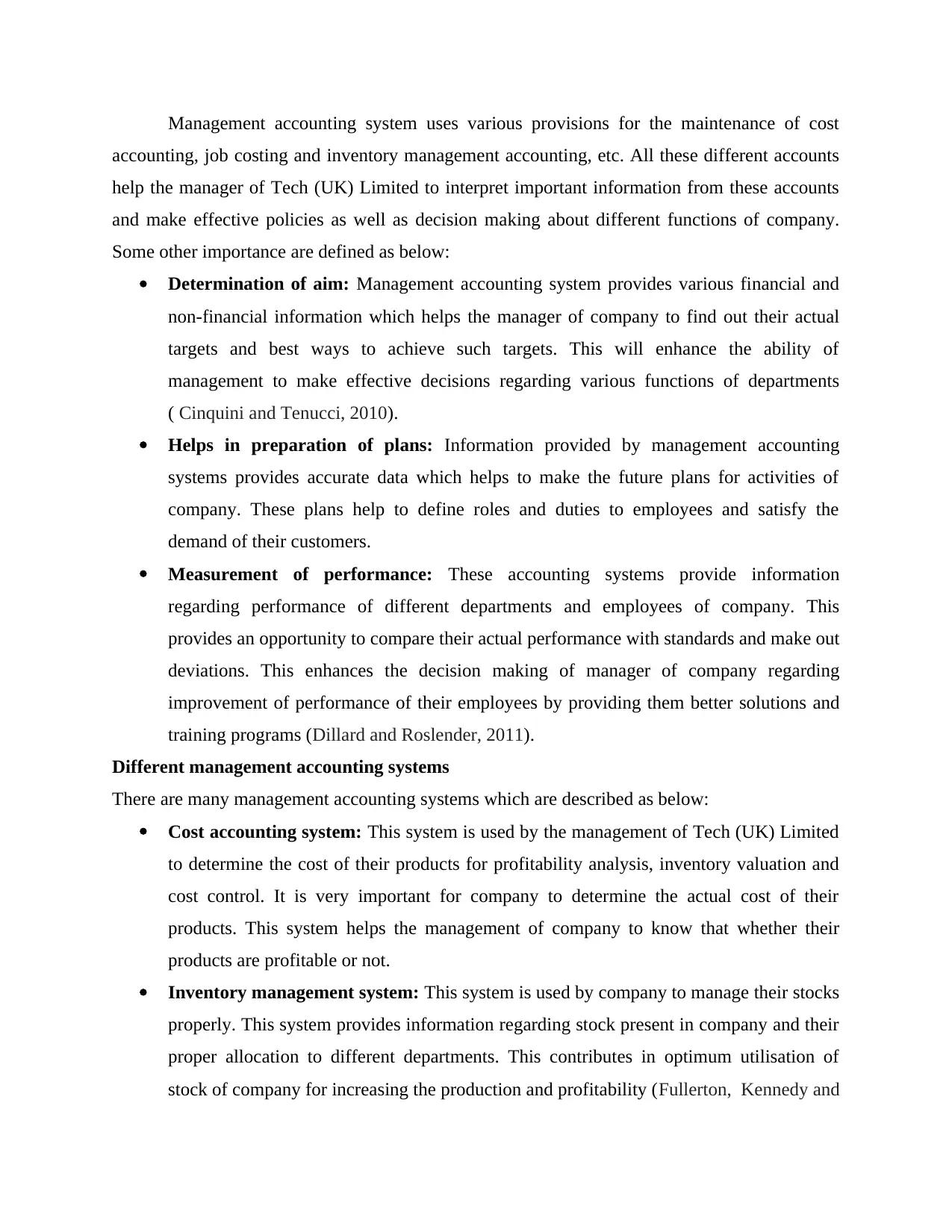

Management accounting system uses various provisions for the maintenance of cost

accounting, job costing and inventory management accounting, etc. All these different accounts

help the manager of Tech (UK) Limited to interpret important information from these accounts

and make effective policies as well as decision making about different functions of company.

Some other importance are defined as below:

Determination of aim: Management accounting system provides various financial and

non-financial information which helps the manager of company to find out their actual

targets and best ways to achieve such targets. This will enhance the ability of

management to make effective decisions regarding various functions of departments

( Cinquini and Tenucci, 2010).

Helps in preparation of plans: Information provided by management accounting

systems provides accurate data which helps to make the future plans for activities of

company. These plans help to define roles and duties to employees and satisfy the

demand of their customers.

Measurement of performance: These accounting systems provide information

regarding performance of different departments and employees of company. This

provides an opportunity to compare their actual performance with standards and make out

deviations. This enhances the decision making of manager of company regarding

improvement of performance of their employees by providing them better solutions and

training programs (Dillard and Roslender, 2011).

Different management accounting systems

There are many management accounting systems which are described as below:

Cost accounting system: This system is used by the management of Tech (UK) Limited

to determine the cost of their products for profitability analysis, inventory valuation and

cost control. It is very important for company to determine the actual cost of their

products. This system helps the management of company to know that whether their

products are profitable or not.

Inventory management system: This system is used by company to manage their stocks

properly. This system provides information regarding stock present in company and their

proper allocation to different departments. This contributes in optimum utilisation of

stock of company for increasing the production and profitability (Fullerton, Kennedy and

accounting, job costing and inventory management accounting, etc. All these different accounts

help the manager of Tech (UK) Limited to interpret important information from these accounts

and make effective policies as well as decision making about different functions of company.

Some other importance are defined as below:

Determination of aim: Management accounting system provides various financial and

non-financial information which helps the manager of company to find out their actual

targets and best ways to achieve such targets. This will enhance the ability of

management to make effective decisions regarding various functions of departments

( Cinquini and Tenucci, 2010).

Helps in preparation of plans: Information provided by management accounting

systems provides accurate data which helps to make the future plans for activities of

company. These plans help to define roles and duties to employees and satisfy the

demand of their customers.

Measurement of performance: These accounting systems provide information

regarding performance of different departments and employees of company. This

provides an opportunity to compare their actual performance with standards and make out

deviations. This enhances the decision making of manager of company regarding

improvement of performance of their employees by providing them better solutions and

training programs (Dillard and Roslender, 2011).

Different management accounting systems

There are many management accounting systems which are described as below:

Cost accounting system: This system is used by the management of Tech (UK) Limited

to determine the cost of their products for profitability analysis, inventory valuation and

cost control. It is very important for company to determine the actual cost of their

products. This system helps the management of company to know that whether their

products are profitable or not.

Inventory management system: This system is used by company to manage their stocks

properly. This system provides information regarding stock present in company and their

proper allocation to different departments. This contributes in optimum utilisation of

stock of company for increasing the production and profitability (Fullerton, Kennedy and

Widener, 2014). It is effective system which helps in determination of the stocks which

are used and remains in organisation. It also contributes in planning activities regarding

the inventories and stocks and helps in their proper allocation to different departments.

This provides the opportunity to different departments achieve their individuals targets

effectively.

Job costing system: This system provides information regarding cost and revenue

generated by job in company. To support this system, job numbers are assigned to

individual items of expenses and revenues. To apply job costing in manufacturing

company, there is the need to track various types of direct expenses such as direct labour

and direct materials which are involved in completion of particular job. This method has

huge importance regarding determination of the profitable process and areas which helps

regarding improvement of overall profitability. This process have large importance

regarding reduction of cost and become cost efficient.

P2. Different types of managerial accounting reports and their importance

There are many accounts formed to record various operations of company. Management

of Tech (UK) Limited prepares different accounts like job costing, cost accounting, inventory

management system, etc. To provide important information from all such accounts, the manager

of company provides different managerial accounting reports. These reports contain important

information regarding functions of company. This enables the management of company to make

effective decision making, planning, performance appraisal, risk reduction etc. These reports also

provide an important information to external stakeholders which attract a large number of

investors towards the activities of company (Garrison And et. al., 2010). Different managerial

reports which are prepared by the management of company are defined as below:

Budget report: These reports are used by the management of company to analyse

performance of different departments and control costs. The estimated budget made by

the manager of cited company is based on the actual expenses from prior years. These

budgets helps the company to compare the actual performance of employees with such

standards are make improvements. These budgets are used by management of company

to provide benefits to the employees which are performing good. Financial budgets which

are made by manager contributes in effective distribution of financial resources to

different departments as per their requirements.

are used and remains in organisation. It also contributes in planning activities regarding

the inventories and stocks and helps in their proper allocation to different departments.

This provides the opportunity to different departments achieve their individuals targets

effectively.

Job costing system: This system provides information regarding cost and revenue

generated by job in company. To support this system, job numbers are assigned to

individual items of expenses and revenues. To apply job costing in manufacturing

company, there is the need to track various types of direct expenses such as direct labour

and direct materials which are involved in completion of particular job. This method has

huge importance regarding determination of the profitable process and areas which helps

regarding improvement of overall profitability. This process have large importance

regarding reduction of cost and become cost efficient.

P2. Different types of managerial accounting reports and their importance

There are many accounts formed to record various operations of company. Management

of Tech (UK) Limited prepares different accounts like job costing, cost accounting, inventory

management system, etc. To provide important information from all such accounts, the manager

of company provides different managerial accounting reports. These reports contain important

information regarding functions of company. This enables the management of company to make

effective decision making, planning, performance appraisal, risk reduction etc. These reports also

provide an important information to external stakeholders which attract a large number of

investors towards the activities of company (Garrison And et. al., 2010). Different managerial

reports which are prepared by the management of company are defined as below:

Budget report: These reports are used by the management of company to analyse

performance of different departments and control costs. The estimated budget made by

the manager of cited company is based on the actual expenses from prior years. These

budgets helps the company to compare the actual performance of employees with such

standards are make improvements. These budgets are used by management of company

to provide benefits to the employees which are performing good. Financial budgets which

are made by manager contributes in effective distribution of financial resources to

different departments as per their requirements.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounts Receivable report: This report provides the information to the management of

cited company about amount outstanding from debtors. This provides the opportunity to

effectively manage the cash flow and credit period given to their customers. This helps

the manager to understand about what are their existing credit polices and need to

improve them regarding fast recover of dues form customers (Macintosh and Quattrone,

2010).

Job cost reports: This report shows the cost incurred on starting of specific project. This

report provides the information regarding cost and revenue which are going to incurred

on specific project for evaluation of jobs profitability. This contributes in identification

of such areas of job which are high earning and have to give more emphasis on them.

This saves the time and cost of company on wasting low profit margin jobs. This helps

the management of company to increase the overall profitability.

Inventory and manufacturing: These reports provides the information regarding actual

position of inventory in company. By using this information the management of cited

company effectively allocate the resources to different departments and increase their

efficiency (Nandan, 2010).

Importance of managerial accounting reports

There are many importance management accounting reports which are defined below:

Decision making: These reports provides various financial and non financial information

which enhance the ability of the manager of company to make effective decisions

regarding important aspects. This helps in future planning, performance management and

risk management which increases the profitability. These systems and reports plays huge

role regarding enhancement of the power of management to improve their decision

making power. The information provide by such system are used by manages as planning

and risk management tool which improve their power to make effective budgets and

provisions which are used further in future.

Reduces loss: These informations helps the management of company to anticipate the

future problems and make provisions regarding that. This enables the company to

effectively tackle the problems and reduces the chance of future losses. For ex, use of Job

costing method helps determination of such area which wasteful and having less

cited company about amount outstanding from debtors. This provides the opportunity to

effectively manage the cash flow and credit period given to their customers. This helps

the manager to understand about what are their existing credit polices and need to

improve them regarding fast recover of dues form customers (Macintosh and Quattrone,

2010).

Job cost reports: This report shows the cost incurred on starting of specific project. This

report provides the information regarding cost and revenue which are going to incurred

on specific project for evaluation of jobs profitability. This contributes in identification

of such areas of job which are high earning and have to give more emphasis on them.

This saves the time and cost of company on wasting low profit margin jobs. This helps

the management of company to increase the overall profitability.

Inventory and manufacturing: These reports provides the information regarding actual

position of inventory in company. By using this information the management of cited

company effectively allocate the resources to different departments and increase their

efficiency (Nandan, 2010).

Importance of managerial accounting reports

There are many importance management accounting reports which are defined below:

Decision making: These reports provides various financial and non financial information

which enhance the ability of the manager of company to make effective decisions

regarding important aspects. This helps in future planning, performance management and

risk management which increases the profitability. These systems and reports plays huge

role regarding enhancement of the power of management to improve their decision

making power. The information provide by such system are used by manages as planning

and risk management tool which improve their power to make effective budgets and

provisions which are used further in future.

Reduces loss: These informations helps the management of company to anticipate the

future problems and make provisions regarding that. This enables the company to

effectively tackle the problems and reduces the chance of future losses. For ex, use of Job

costing method helps determination of such area which wasteful and having less

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

profitability. This provides chance regarding focus on profitable areas and saves their

cost and increase their profit margin.

Increase financial returns: Such important information helps the manager to make

better policies and plans for futures which enhance the ability of departments to perform

their functions effectively. Development of new skills and training to employees

increases the financial returns for company.

M1

Benefits of different management accounting systems are mentioned below:

Job costing systems

Advantages

It helps estimation of all types of cost which are incurred during overall manufacturing

process

It helps in analysis of the quality of work which is performed by different departments

Inventory management systems

Advantages

It provides the opportunity regarding saving time and cost

It helps in effective management of inventory

D1

Type of reporting Integration with organisational process

Accounts receivable report Its integration with organisational functions

helps in collection of due amounts from

debtors.

Job cost report Its integration helps in improvement of the

efficiency of manger regarding ascertainment

of the most profitable project.

cost and increase their profit margin.

Increase financial returns: Such important information helps the manager to make

better policies and plans for futures which enhance the ability of departments to perform

their functions effectively. Development of new skills and training to employees

increases the financial returns for company.

M1

Benefits of different management accounting systems are mentioned below:

Job costing systems

Advantages

It helps estimation of all types of cost which are incurred during overall manufacturing

process

It helps in analysis of the quality of work which is performed by different departments

Inventory management systems

Advantages

It provides the opportunity regarding saving time and cost

It helps in effective management of inventory

D1

Type of reporting Integration with organisational process

Accounts receivable report Its integration with organisational functions

helps in collection of due amounts from

debtors.

Job cost report Its integration helps in improvement of the

efficiency of manger regarding ascertainment

of the most profitable project.

TASK 2

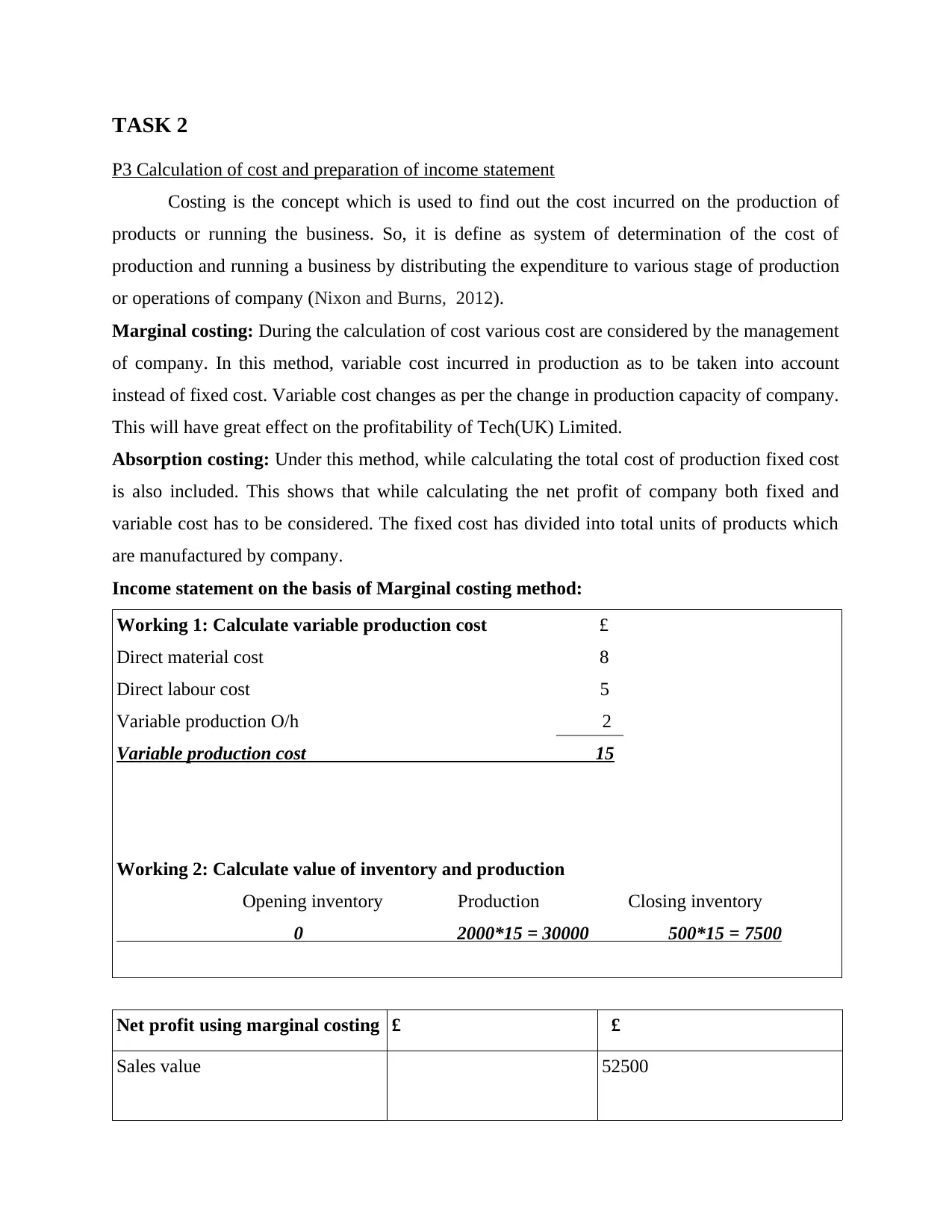

P3 Calculation of cost and preparation of income statement

Costing is the concept which is used to find out the cost incurred on the production of

products or running the business. So, it is define as system of determination of the cost of

production and running a business by distributing the expenditure to various stage of production

or operations of company (Nixon and Burns, 2012).

Marginal costing: During the calculation of cost various cost are considered by the management

of company. In this method, variable cost incurred in production as to be taken into account

instead of fixed cost. Variable cost changes as per the change in production capacity of company.

This will have great effect on the profitability of Tech(UK) Limited.

Absorption costing: Under this method, while calculating the total cost of production fixed cost

is also included. This shows that while calculating the net profit of company both fixed and

variable cost has to be considered. The fixed cost has divided into total units of products which

are manufactured by company.

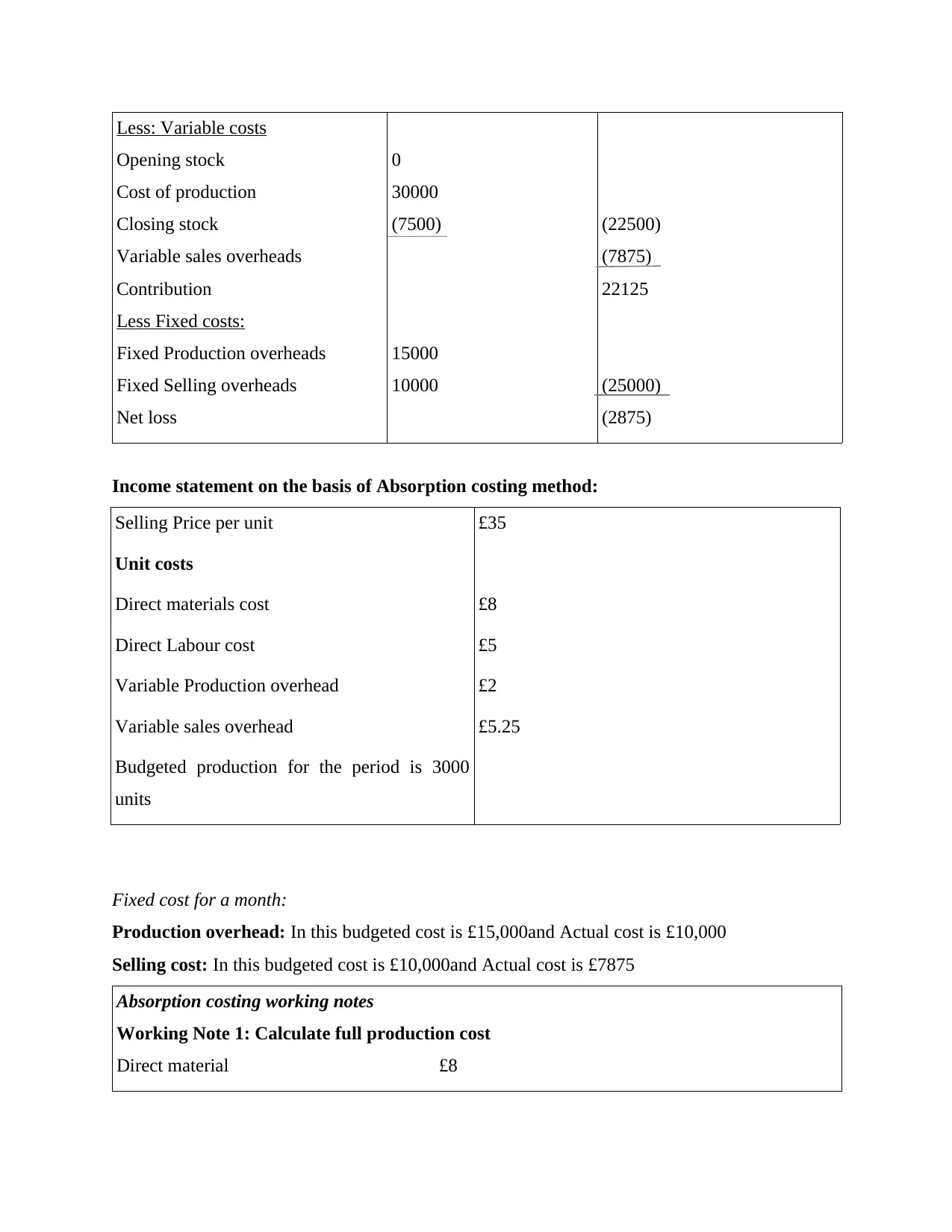

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material cost 8

Direct labour cost 5

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £ £

Sales value 52500

P3 Calculation of cost and preparation of income statement

Costing is the concept which is used to find out the cost incurred on the production of

products or running the business. So, it is define as system of determination of the cost of

production and running a business by distributing the expenditure to various stage of production

or operations of company (Nixon and Burns, 2012).

Marginal costing: During the calculation of cost various cost are considered by the management

of company. In this method, variable cost incurred in production as to be taken into account

instead of fixed cost. Variable cost changes as per the change in production capacity of company.

This will have great effect on the profitability of Tech(UK) Limited.

Absorption costing: Under this method, while calculating the total cost of production fixed cost

is also included. This shows that while calculating the net profit of company both fixed and

variable cost has to be considered. The fixed cost has divided into total units of products which

are manufactured by company.

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material cost 8

Direct labour cost 5

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £ £

Sales value 52500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Less: Variable costs

Opening stock

Cost of production

Closing stock

Variable sales overheads

Contribution

Less Fixed costs:

Fixed Production overheads

Fixed Selling overheads

Net loss

0

30000

(7500)

15000

10000

(22500)

(7875)

22125

(25000)

(2875)

Income statement on the basis of Absorption costing method:

Selling Price per unit £35

Unit costs

Direct materials cost £8

Direct Labour cost £5

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted production for the period is 3000

units

Fixed cost for a month:

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: In this budgeted cost is £10,000and Actual cost is £7875

Absorption costing working notes

Working Note 1: Calculate full production cost

Direct material £8

Opening stock

Cost of production

Closing stock

Variable sales overheads

Contribution

Less Fixed costs:

Fixed Production overheads

Fixed Selling overheads

Net loss

0

30000

(7500)

15000

10000

(22500)

(7875)

22125

(25000)

(2875)

Income statement on the basis of Absorption costing method:

Selling Price per unit £35

Unit costs

Direct materials cost £8

Direct Labour cost £5

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted production for the period is 3000

units

Fixed cost for a month:

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: In this budgeted cost is £10,000and Actual cost is £7875

Absorption costing working notes

Working Note 1: Calculate full production cost

Direct material £8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

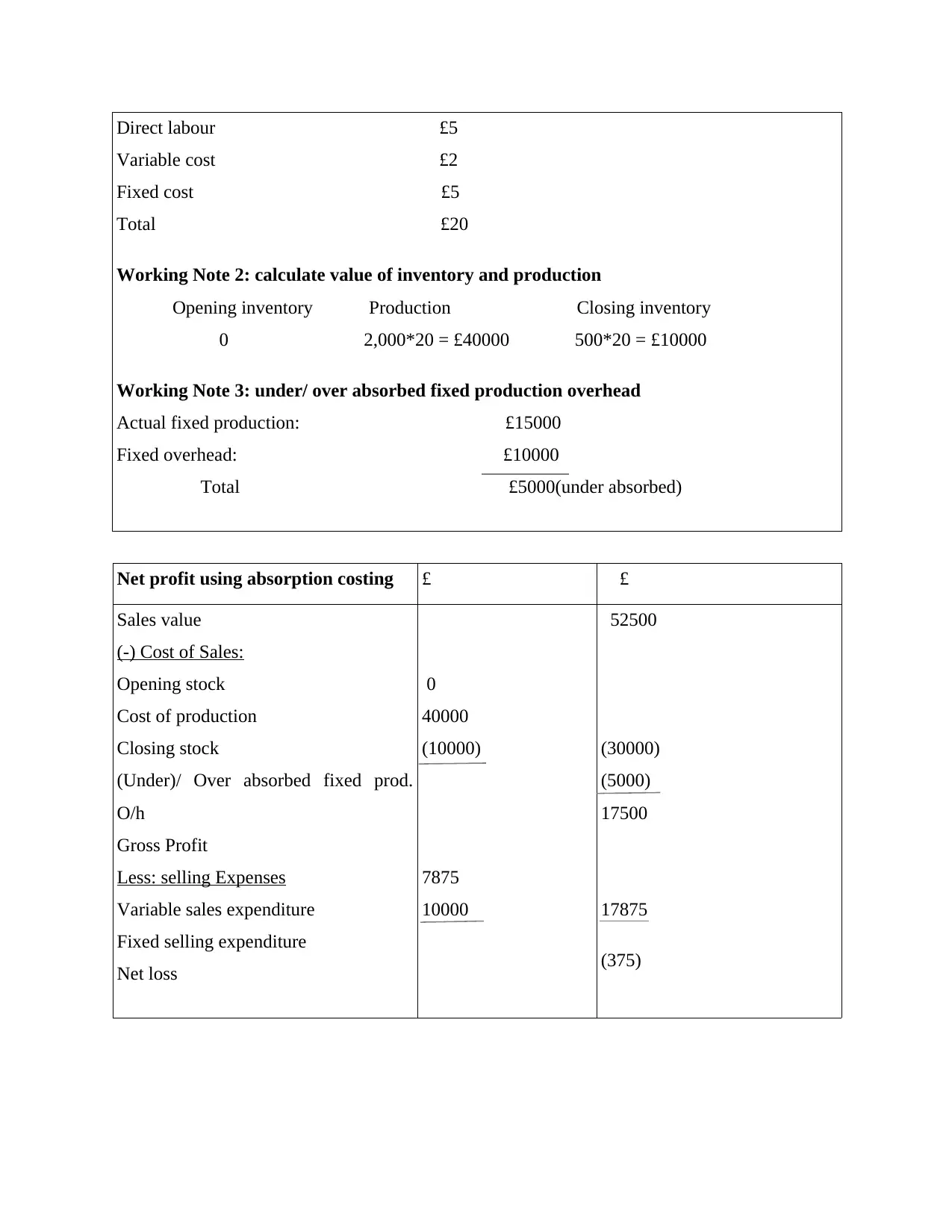

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40000 500*20 = £10000

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000(under absorbed)

Net profit using absorption costing £ £

Sales value

(-) Cost of Sales:

Opening stock

Cost of production

Closing stock

(Under)/ Over absorbed fixed prod.

O/h

Gross Profit

Less: selling Expenses

Variable sales expenditure

Fixed selling expenditure

Net loss

0

40000

(10000)

7875

10000

52500

(30000)

(5000)

17500

17875

(375)

Variable cost £2

Fixed cost £5

Total £20

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40000 500*20 = £10000

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000(under absorbed)

Net profit using absorption costing £ £

Sales value

(-) Cost of Sales:

Opening stock

Cost of production

Closing stock

(Under)/ Over absorbed fixed prod.

O/h

Gross Profit

Less: selling Expenses

Variable sales expenditure

Fixed selling expenditure

Net loss

0

40000

(10000)

7875

10000

52500

(30000)

(5000)

17500

17875

(375)

M2

To interpret the financial position different accounting tools are used. Such information

enhance the decision making power and improve the organisational profitability. It is analysed

from the above financial statements that organisation working in loss. It means they don't have

the sufficient amount of funds for future growth of their business functions. Keeping the record

of all data improves their internal strength and forecasting power.

D2

It is observed that two costing techniques are used regarding calculation of profit which

are marginal and absorption. Through the use of Absorption costing method loss is obtained by

the organisation of 375. On other hand, by the use of Marginal costing loss of 2875 is attained by

the organisation. This different between the loss is arses due to the amount of fixed assets

because it is considered under absorption costing method.

TASK 3

P4 Different kind of budgets and their advantages and disadvantages

There are many kind of budgets are prepared by the management of Tech(UK) Limited to

effectively the manage the functions of company. It includes master budget, operational budget,

cash flow budget etc. These budgets are includes principles which are required to follow by the

employees of company to accomplish their tasks. These budgets are described below:

Master budget: This budgets includes about the projection of different functions of

company during fiscal year. Master budget of company includes the cash budget which

provides the information regarding estimated income statement and balance sheet. Master

budget of company is interrelated to the many budgets of various departments of

company. These budgets are used by the manager of company to plan and set

performance objectives (Otley and Emmanuel, 2013).

Operational budgets: This budget covers the revenue and expenses incurred by

company on day to day core business activities. This budget shows the cost incurred on

production of good and overhead and administrative cost which are directly related to

production of products. This also shows about the revenue generated by company by

sales of their products in markets. All these information helps the company to effectively

plan their operations in such way that increases their profits and reduces operational cost.

To interpret the financial position different accounting tools are used. Such information

enhance the decision making power and improve the organisational profitability. It is analysed

from the above financial statements that organisation working in loss. It means they don't have

the sufficient amount of funds for future growth of their business functions. Keeping the record

of all data improves their internal strength and forecasting power.

D2

It is observed that two costing techniques are used regarding calculation of profit which

are marginal and absorption. Through the use of Absorption costing method loss is obtained by

the organisation of 375. On other hand, by the use of Marginal costing loss of 2875 is attained by

the organisation. This different between the loss is arses due to the amount of fixed assets

because it is considered under absorption costing method.

TASK 3

P4 Different kind of budgets and their advantages and disadvantages

There are many kind of budgets are prepared by the management of Tech(UK) Limited to

effectively the manage the functions of company. It includes master budget, operational budget,

cash flow budget etc. These budgets are includes principles which are required to follow by the

employees of company to accomplish their tasks. These budgets are described below:

Master budget: This budgets includes about the projection of different functions of

company during fiscal year. Master budget of company includes the cash budget which

provides the information regarding estimated income statement and balance sheet. Master

budget of company is interrelated to the many budgets of various departments of

company. These budgets are used by the manager of company to plan and set

performance objectives (Otley and Emmanuel, 2013).

Operational budgets: This budget covers the revenue and expenses incurred by

company on day to day core business activities. This budget shows the cost incurred on

production of good and overhead and administrative cost which are directly related to

production of products. This also shows about the revenue generated by company by

sales of their products in markets. All these information helps the company to effectively

plan their operations in such way that increases their profits and reduces operational cost.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.