Management Accounting Report: Financial Reporting and Decision Making

VerifiedAdded on 2020/10/05

|18

|4673

|51

Report

AI Summary

This report delves into the core principles of management accounting, emphasizing its role in decision-making, planning, and control within organizations. It distinguishes between management and financial accounting, highlighting the importance of management accounting as a decision-making tool. The report explores various management accounting systems, including inventory management and job costing, along with different types of managerial reports such as accounts receivable and cash flow reports, and their significance in improving organizational performance. It provides a detailed analysis of absorption and marginal costing methods for income statement preparation, as well as the advantages and disadvantages of different budgeting approaches and their impact on financial strategies. Furthermore, the report examines how management accounting systems can be applied to address and overcome financial issues, providing a comprehensive overview of the subject matter.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1 ...........................................................................................................................................1

P1 Concept of management accounting and its essential requirement.......................................1

P2 Different types of managerial reports and its importance......................................................3

M1...............................................................................................................................................5

D1................................................................................................................................................5

TASK 2............................................................................................................................................5

P3 Application of absorption and marginal costing method for preparation of income

statement.....................................................................................................................................5

M2...............................................................................................................................................8

D2................................................................................................................................................8

TASK 3............................................................................................................................................8

P4 Advantages and disadvantages of different kind of budgets and their importance..............8

M3.............................................................................................................................................10

D3..............................................................................................................................................11

TASK 4..........................................................................................................................................11

P5 Application of management accounting system to overcome from financial issues...........11

M4.............................................................................................................................................12

CONCLUSION..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1 ...........................................................................................................................................1

P1 Concept of management accounting and its essential requirement.......................................1

P2 Different types of managerial reports and its importance......................................................3

M1...............................................................................................................................................5

D1................................................................................................................................................5

TASK 2............................................................................................................................................5

P3 Application of absorption and marginal costing method for preparation of income

statement.....................................................................................................................................5

M2...............................................................................................................................................8

D2................................................................................................................................................8

TASK 3............................................................................................................................................8

P4 Advantages and disadvantages of different kind of budgets and their importance..............8

M3.............................................................................................................................................10

D3..............................................................................................................................................11

TASK 4..........................................................................................................................................11

P5 Application of management accounting system to overcome from financial issues...........11

M4.............................................................................................................................................12

CONCLUSION..............................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is important profession which contributes in decision making,

planning, monitoring, controlling of organisational functions. It is considered as process of

preparing reports and accounts which provides timely and reliable information to the managers

for operation of day to day functions. In comparison to financial accounting, management

accounting is broad concept which includes the provisions of costing also which helps to bring

coordination among the different departmental functions. It helps the management to attain

flexibility in their structure and build effective strategies which helps in achievement of

organisational objectives. Tech(UK)Ltd. Produces special charger for retailers (Arroyo, 2012).

In the present report explain about, difference between management and financial

accounting, importance of management accounting as decision making tool, different

management accounting systems, different types of managerial accounting reports and its

importance and use of absorption and marginal costing method for preparation of income

statement. Also, advantages and disadvantages of different kind of budgets, budget preparation

process, importance of budget and application of management accounting systems to respond

financial issues.

TASK 1

P1 Concept of management accounting and its essential requirement

Distinguish between management and financial accounting

Management Accounting Financial Accounting

Includes preparation of reports and accounts

for the benefit of internal parties to improve

their decision-making and effectively manage

day to day operations.

Includes the preparation of annual accounts of

organisation for the use of external

stakeholders to improve their decision making

regarding make investments

The information gathered from such reports

used for preparation of future strategies

The information collected from these accounts

used to for measurement of past performance

Such reports are based on specific areas These reports are based on the performance of

entire organisation

Helps in measurement of operation and Only helps in measurement of financial data

Management accounting is important profession which contributes in decision making,

planning, monitoring, controlling of organisational functions. It is considered as process of

preparing reports and accounts which provides timely and reliable information to the managers

for operation of day to day functions. In comparison to financial accounting, management

accounting is broad concept which includes the provisions of costing also which helps to bring

coordination among the different departmental functions. It helps the management to attain

flexibility in their structure and build effective strategies which helps in achievement of

organisational objectives. Tech(UK)Ltd. Produces special charger for retailers (Arroyo, 2012).

In the present report explain about, difference between management and financial

accounting, importance of management accounting as decision making tool, different

management accounting systems, different types of managerial accounting reports and its

importance and use of absorption and marginal costing method for preparation of income

statement. Also, advantages and disadvantages of different kind of budgets, budget preparation

process, importance of budget and application of management accounting systems to respond

financial issues.

TASK 1

P1 Concept of management accounting and its essential requirement

Distinguish between management and financial accounting

Management Accounting Financial Accounting

Includes preparation of reports and accounts

for the benefit of internal parties to improve

their decision-making and effectively manage

day to day operations.

Includes the preparation of annual accounts of

organisation for the use of external

stakeholders to improve their decision making

regarding make investments

The information gathered from such reports

used for preparation of future strategies

The information collected from these accounts

used to for measurement of past performance

Such reports are based on specific areas These reports are based on the performance of

entire organisation

Helps in measurement of operation and Only helps in measurement of financial data

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

financial performance

Management Accounting: Every organisation whether small or large in nature requires

to adopt management accounting system for appraisal of the performance of each and every

department. It is the process of measuring, evaluating, interpreting the information with the help

of various tool to accomplish their goals. The different managerial and costing techniques

support the manager of Tech(UK)Ltd. To plan, control, monitor and enhance the performance of

overall organisation. The different kind of accounts which are prepared through use of this

system includes job costing, inventory management, price optimisation, cost accounting etc. It

assist the different departments in determination of their issues and improves their performance.

Importance of management accounting information as decision-making tool

There are large number of benefits are associated with application of the management

accounting systems within the organisation. It provides different type of management accounting

information which helps the manager of Tech(UK)Ltd. To use it as decision-making tools

regarding different aspects which defined below:

Measurement of performance: One of the basic function which is performed with the

help of these systems is to measure the actual performance of employees through

comparing with standards (Boyns and Edwards, 2013). It provides the opportunity is to

identify the issues and deviations in performance and apply appropriate techniques to

overcome from them.

Assessment of risk: One of the major importance of management accounting system

that it helps in assessing the future risk factors and mitigate them through application of

the effective management approaches.

Allocation of resources: The different kind of reports and accounts based of different

reports helps the manager to identify the requirement of resources by each and every

department. This will contributes in effective allocation of given resources to attain

maximum output from its optimum utilisation. It helps in achievement of organisational

objectives and further contributes the effort regarding maintenance of long term

sustainability in their operations.

Financial statement presentation: The provisions of management accounting helps in

collection of different information and data which represents the financial position of

Management Accounting: Every organisation whether small or large in nature requires

to adopt management accounting system for appraisal of the performance of each and every

department. It is the process of measuring, evaluating, interpreting the information with the help

of various tool to accomplish their goals. The different managerial and costing techniques

support the manager of Tech(UK)Ltd. To plan, control, monitor and enhance the performance of

overall organisation. The different kind of accounts which are prepared through use of this

system includes job costing, inventory management, price optimisation, cost accounting etc. It

assist the different departments in determination of their issues and improves their performance.

Importance of management accounting information as decision-making tool

There are large number of benefits are associated with application of the management

accounting systems within the organisation. It provides different type of management accounting

information which helps the manager of Tech(UK)Ltd. To use it as decision-making tools

regarding different aspects which defined below:

Measurement of performance: One of the basic function which is performed with the

help of these systems is to measure the actual performance of employees through

comparing with standards (Boyns and Edwards, 2013). It provides the opportunity is to

identify the issues and deviations in performance and apply appropriate techniques to

overcome from them.

Assessment of risk: One of the major importance of management accounting system

that it helps in assessing the future risk factors and mitigate them through application of

the effective management approaches.

Allocation of resources: The different kind of reports and accounts based of different

reports helps the manager to identify the requirement of resources by each and every

department. This will contributes in effective allocation of given resources to attain

maximum output from its optimum utilisation. It helps in achievement of organisational

objectives and further contributes the effort regarding maintenance of long term

sustainability in their operations.

Financial statement presentation: The provisions of management accounting helps in

collection of different information and data which represents the financial position of

organisation. Such different information and data regarding costs and finance helps in

preparation of precise financial reports which contributes in key decision-making.

Decision making: There is huge importance of management accounting systems in

improvement of the decision making power of internal parties to get higher results. For

ex., application of inventory management system helps to control stock in effective

manner.

Make or buy: Application of cost accounting system provides the opportunity to make

decisions regarding manufacturing or outsourcing which is the most beneficial for

organisation. It helps to improve profitability.

Keep or sale: Use of different management accounting system contributes in

identification of such assets or technology of organisation which obsolete and increase

their expenses. So, it helps to take the decision regarding keep and sale of them.

Different types of management accounting systems

Inventory management system: One of the important system which provides the

function regarding supervision and management of stock and assets of organisation. The main

aim behind the implementation of this system within the organisation is effective flow stock

within the organisation for its optimum utilisation. In this regard, three different tools are used

which are known as FIFO, LIFO, AVCO. The role of three different tools are mentioned below:

FIFO: This method is known as first in first out method where the inventory is tracked

on the basis of provisions of this tool. It helps in effective valuation of the closing

inventory at the end of the period.

LIFO: This method is known as last in first out method. It helps is value the valuation of

closing inventory

AVCO: It refers to as the average cost which helps to assess the inventory value in more

precise form which enhance decision-making.

Job costing: The system is useful for manufacturing organisation which produces

multiple products. This helps in allocation of cost to to each and every product. It provides the

opportunity to track the actual expenses which are incurred on production of product. Here, the

costs are apportioned on the basis of Direct material, Fixed and variable overheads (Arroyo,

2012).

preparation of precise financial reports which contributes in key decision-making.

Decision making: There is huge importance of management accounting systems in

improvement of the decision making power of internal parties to get higher results. For

ex., application of inventory management system helps to control stock in effective

manner.

Make or buy: Application of cost accounting system provides the opportunity to make

decisions regarding manufacturing or outsourcing which is the most beneficial for

organisation. It helps to improve profitability.

Keep or sale: Use of different management accounting system contributes in

identification of such assets or technology of organisation which obsolete and increase

their expenses. So, it helps to take the decision regarding keep and sale of them.

Different types of management accounting systems

Inventory management system: One of the important system which provides the

function regarding supervision and management of stock and assets of organisation. The main

aim behind the implementation of this system within the organisation is effective flow stock

within the organisation for its optimum utilisation. In this regard, three different tools are used

which are known as FIFO, LIFO, AVCO. The role of three different tools are mentioned below:

FIFO: This method is known as first in first out method where the inventory is tracked

on the basis of provisions of this tool. It helps in effective valuation of the closing

inventory at the end of the period.

LIFO: This method is known as last in first out method. It helps is value the valuation of

closing inventory

AVCO: It refers to as the average cost which helps to assess the inventory value in more

precise form which enhance decision-making.

Job costing: The system is useful for manufacturing organisation which produces

multiple products. This helps in allocation of cost to to each and every product. It provides the

opportunity to track the actual expenses which are incurred on production of product. Here, the

costs are apportioned on the basis of Direct material, Fixed and variable overheads (Arroyo,

2012).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

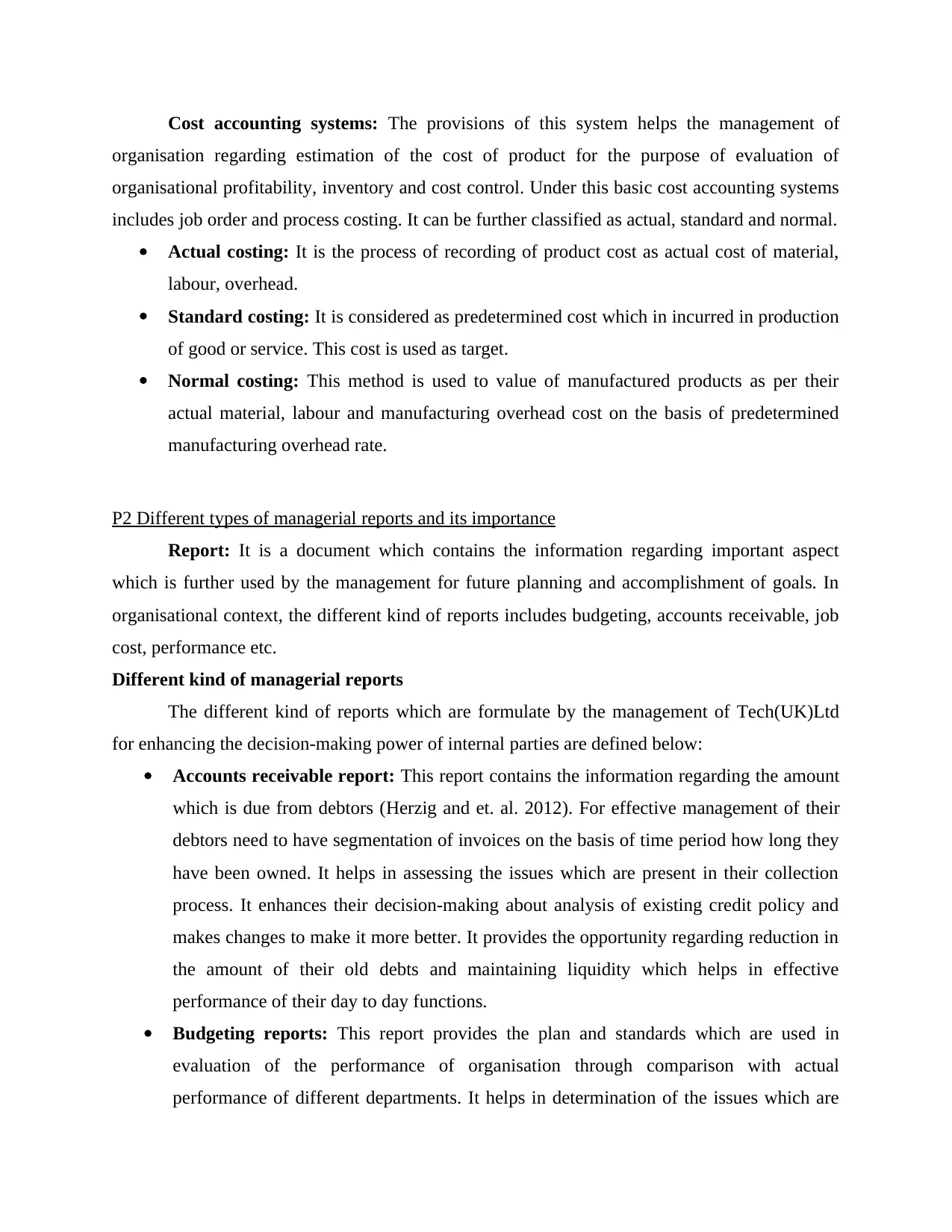

Cost accounting systems: The provisions of this system helps the management of

organisation regarding estimation of the cost of product for the purpose of evaluation of

organisational profitability, inventory and cost control. Under this basic cost accounting systems

includes job order and process costing. It can be further classified as actual, standard and normal.

Actual costing: It is the process of recording of product cost as actual cost of material,

labour, overhead.

Standard costing: It is considered as predetermined cost which in incurred in production

of good or service. This cost is used as target.

Normal costing: This method is used to value of manufactured products as per their

actual material, labour and manufacturing overhead cost on the basis of predetermined

manufacturing overhead rate.

P2 Different types of managerial reports and its importance

Report: It is a document which contains the information regarding important aspect

which is further used by the management for future planning and accomplishment of goals. In

organisational context, the different kind of reports includes budgeting, accounts receivable, job

cost, performance etc.

Different kind of managerial reports

The different kind of reports which are formulate by the management of Tech(UK)Ltd

for enhancing the decision-making power of internal parties are defined below:

Accounts receivable report: This report contains the information regarding the amount

which is due from debtors (Herzig and et. al. 2012). For effective management of their

debtors need to have segmentation of invoices on the basis of time period how long they

have been owned. It helps in assessing the issues which are present in their collection

process. It enhances their decision-making about analysis of existing credit policy and

makes changes to make it more better. It provides the opportunity regarding reduction in

the amount of their old debts and maintaining liquidity which helps in effective

performance of their day to day functions.

Budgeting reports: This report provides the plan and standards which are used in

evaluation of the performance of organisation through comparison with actual

performance of different departments. It helps in determination of the issues which are

organisation regarding estimation of the cost of product for the purpose of evaluation of

organisational profitability, inventory and cost control. Under this basic cost accounting systems

includes job order and process costing. It can be further classified as actual, standard and normal.

Actual costing: It is the process of recording of product cost as actual cost of material,

labour, overhead.

Standard costing: It is considered as predetermined cost which in incurred in production

of good or service. This cost is used as target.

Normal costing: This method is used to value of manufactured products as per their

actual material, labour and manufacturing overhead cost on the basis of predetermined

manufacturing overhead rate.

P2 Different types of managerial reports and its importance

Report: It is a document which contains the information regarding important aspect

which is further used by the management for future planning and accomplishment of goals. In

organisational context, the different kind of reports includes budgeting, accounts receivable, job

cost, performance etc.

Different kind of managerial reports

The different kind of reports which are formulate by the management of Tech(UK)Ltd

for enhancing the decision-making power of internal parties are defined below:

Accounts receivable report: This report contains the information regarding the amount

which is due from debtors (Herzig and et. al. 2012). For effective management of their

debtors need to have segmentation of invoices on the basis of time period how long they

have been owned. It helps in assessing the issues which are present in their collection

process. It enhances their decision-making about analysis of existing credit policy and

makes changes to make it more better. It provides the opportunity regarding reduction in

the amount of their old debts and maintaining liquidity which helps in effective

performance of their day to day functions.

Budgeting reports: This report provides the plan and standards which are used in

evaluation of the performance of organisation through comparison with actual

performance of different departments. It helps in determination of the issues which are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

associated with their functions and helps in controlling of costs. On the basis of such

comparison, incentive report is prepared by the management for every different

employee which contributes in improvement of their passion towards their work.

Job cost report: One of the important report which helps the management of

Tech(UK)Ltd. Is to assess the cost, expenses and profitability which is attached with the

production of each product. Such analysis helps in identification of the most earning

aspect of project which enhance decision making regarding more efforts are need to

provide on such aspects. It also helps in determination of the areas of waste on which

need to be taken care more and make the project more profitable.

Cash flow report: It is one of the important document which helps in effective

management of can within the organisation. It provides the information regarding inflow

and outflow of cash during specified period of time. It helps to maintain the liquidity

within the organisation.

Sales report: This report provides the information regarding the amount of sales which

is required to attain from providence of their business functions. It is used for the

guidance of employees to provides their functions according to such requirements.

Production report: This report provides the information regarding amount of good

which are required to produce for satisfaction of the different requirements of customers.

This report assist the production department is to achieve their targets.

Importance of management accounting reports

Reduction of loss: Different kind of reports contains different information from which

issues are analysed for reduction of their future losses. For ex., Accounts receivable

report helps in identification of the amount of outstanding debts. Correction in policies

helps in maintenance of liquidity within the organisation.

Increased financial returns: Use of job costing reports helps in identification of the

most profitable aspect of project. It helps the management to put more efforts of those

areas to improve their earnings. Subsequently, different reports provides the opportunity

to improve the understanding between different departments to improve their

performance.

Formulation of budgets: Different kind of reports provides various information through

which budgets are prepared for guidance of employees. These budgets are work as

comparison, incentive report is prepared by the management for every different

employee which contributes in improvement of their passion towards their work.

Job cost report: One of the important report which helps the management of

Tech(UK)Ltd. Is to assess the cost, expenses and profitability which is attached with the

production of each product. Such analysis helps in identification of the most earning

aspect of project which enhance decision making regarding more efforts are need to

provide on such aspects. It also helps in determination of the areas of waste on which

need to be taken care more and make the project more profitable.

Cash flow report: It is one of the important document which helps in effective

management of can within the organisation. It provides the information regarding inflow

and outflow of cash during specified period of time. It helps to maintain the liquidity

within the organisation.

Sales report: This report provides the information regarding the amount of sales which

is required to attain from providence of their business functions. It is used for the

guidance of employees to provides their functions according to such requirements.

Production report: This report provides the information regarding amount of good

which are required to produce for satisfaction of the different requirements of customers.

This report assist the production department is to achieve their targets.

Importance of management accounting reports

Reduction of loss: Different kind of reports contains different information from which

issues are analysed for reduction of their future losses. For ex., Accounts receivable

report helps in identification of the amount of outstanding debts. Correction in policies

helps in maintenance of liquidity within the organisation.

Increased financial returns: Use of job costing reports helps in identification of the

most profitable aspect of project. It helps the management to put more efforts of those

areas to improve their earnings. Subsequently, different reports provides the opportunity

to improve the understanding between different departments to improve their

performance.

Formulation of budgets: Different kind of reports provides various information through

which budgets are prepared for guidance of employees. These budgets are work as

standards which provides the opportunity to improve overall performance and accomplish

targets.

Improvement of understanding: There is huge importance of these different kind of

reports behind the improvement of the understand between different department

activities. It helps to attain their support in achievement of common objective.

M1

Advantages of management accounting system:

Cost accounting system

This system helps in measurement of the efficiency in processes and contributes in

making of improvements (Otley and Emmanuel, 2013).

Helps in effective planning

Job costing system

It helps to assess the quality of work

Prevention from duplication of efforts

D1

Type of reporting Integration with organisational process

Accounts receivable report Use of these reports in organisation for the

purpose of timely collection of their

outstanding amount.

Job cost report Integration of these reports with organisational

process helps in achievement of cost objectives

and fixing up of their pricing strategies

TASK 2

P3 Application of absorption and marginal costing method for preparation of income statement

Cost: It refers to the amount spend on the production of products. The amount which is

incurred upon resources is included in total cost of product. For ex., material, labour, time, risk

etc.

targets.

Improvement of understanding: There is huge importance of these different kind of

reports behind the improvement of the understand between different department

activities. It helps to attain their support in achievement of common objective.

M1

Advantages of management accounting system:

Cost accounting system

This system helps in measurement of the efficiency in processes and contributes in

making of improvements (Otley and Emmanuel, 2013).

Helps in effective planning

Job costing system

It helps to assess the quality of work

Prevention from duplication of efforts

D1

Type of reporting Integration with organisational process

Accounts receivable report Use of these reports in organisation for the

purpose of timely collection of their

outstanding amount.

Job cost report Integration of these reports with organisational

process helps in achievement of cost objectives

and fixing up of their pricing strategies

TASK 2

P3 Application of absorption and marginal costing method for preparation of income statement

Cost: It refers to the amount spend on the production of products. The amount which is

incurred upon resources is included in total cost of product. For ex., material, labour, time, risk

etc.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

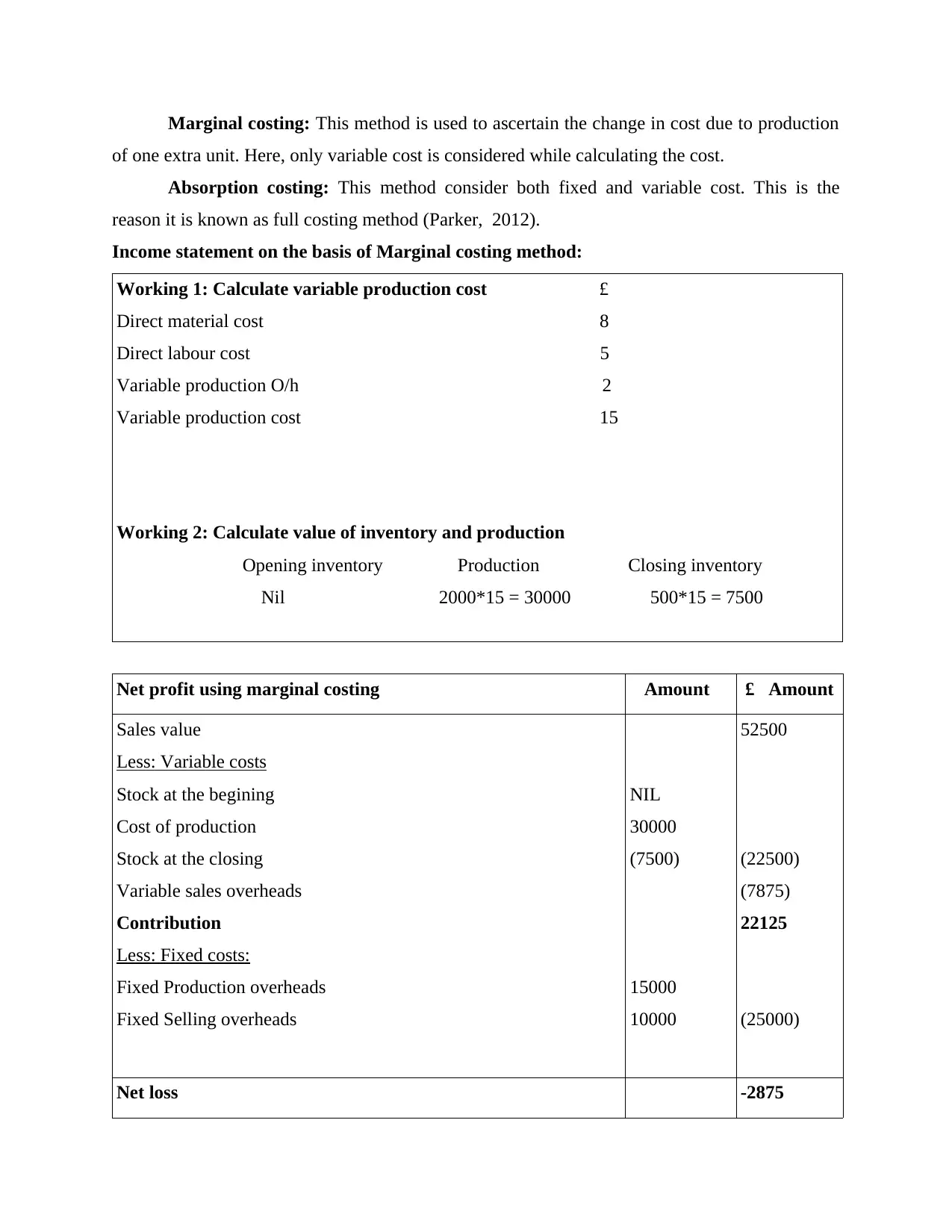

Marginal costing: This method is used to ascertain the change in cost due to production

of one extra unit. Here, only variable cost is considered while calculating the cost.

Absorption costing: This method consider both fixed and variable cost. This is the

reason it is known as full costing method (Parker, 2012).

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material cost 8

Direct labour cost 5

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

Nil 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £Amount £ Amount

Sales value

Less: Variable costs

Stock at the begining

Cost of production

Stock at the closing

Variable sales overheads

Contribution

Less: Fixed costs:

Fixed Production overheads

Fixed Selling overheads

NIL

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

Net loss -2875

of one extra unit. Here, only variable cost is considered while calculating the cost.

Absorption costing: This method consider both fixed and variable cost. This is the

reason it is known as full costing method (Parker, 2012).

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material cost 8

Direct labour cost 5

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

Nil 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £Amount £ Amount

Sales value

Less: Variable costs

Stock at the begining

Cost of production

Stock at the closing

Variable sales overheads

Contribution

Less: Fixed costs:

Fixed Production overheads

Fixed Selling overheads

NIL

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

Net loss -2875

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

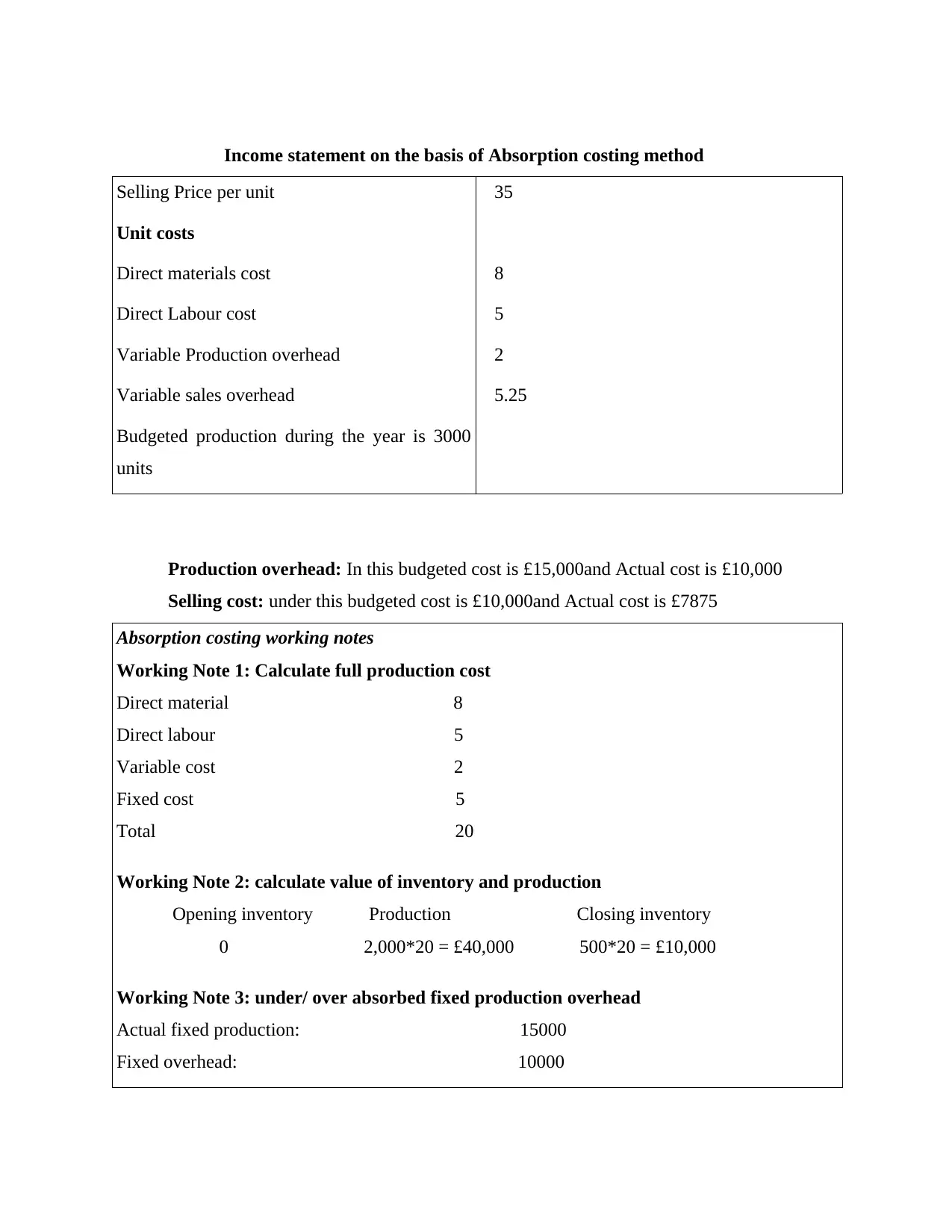

Income statement on the basis of Absorption costing method

Selling Price per unit £35

Unit costs

Direct materials cost £8

Direct Labour cost £5

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted production during the year is 3000

units

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: under this budgeted cost is £10,000and Actual cost is £7875

Absorption costing working notes

Working Note 1: Calculate full production cost

Direct material £8

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40,000 500*20 = £10,000

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Selling Price per unit £35

Unit costs

Direct materials cost £8

Direct Labour cost £5

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted production during the year is 3000

units

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: under this budgeted cost is £10,000and Actual cost is £7875

Absorption costing working notes

Working Note 1: Calculate full production cost

Direct material £8

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40,000 500*20 = £10,000

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

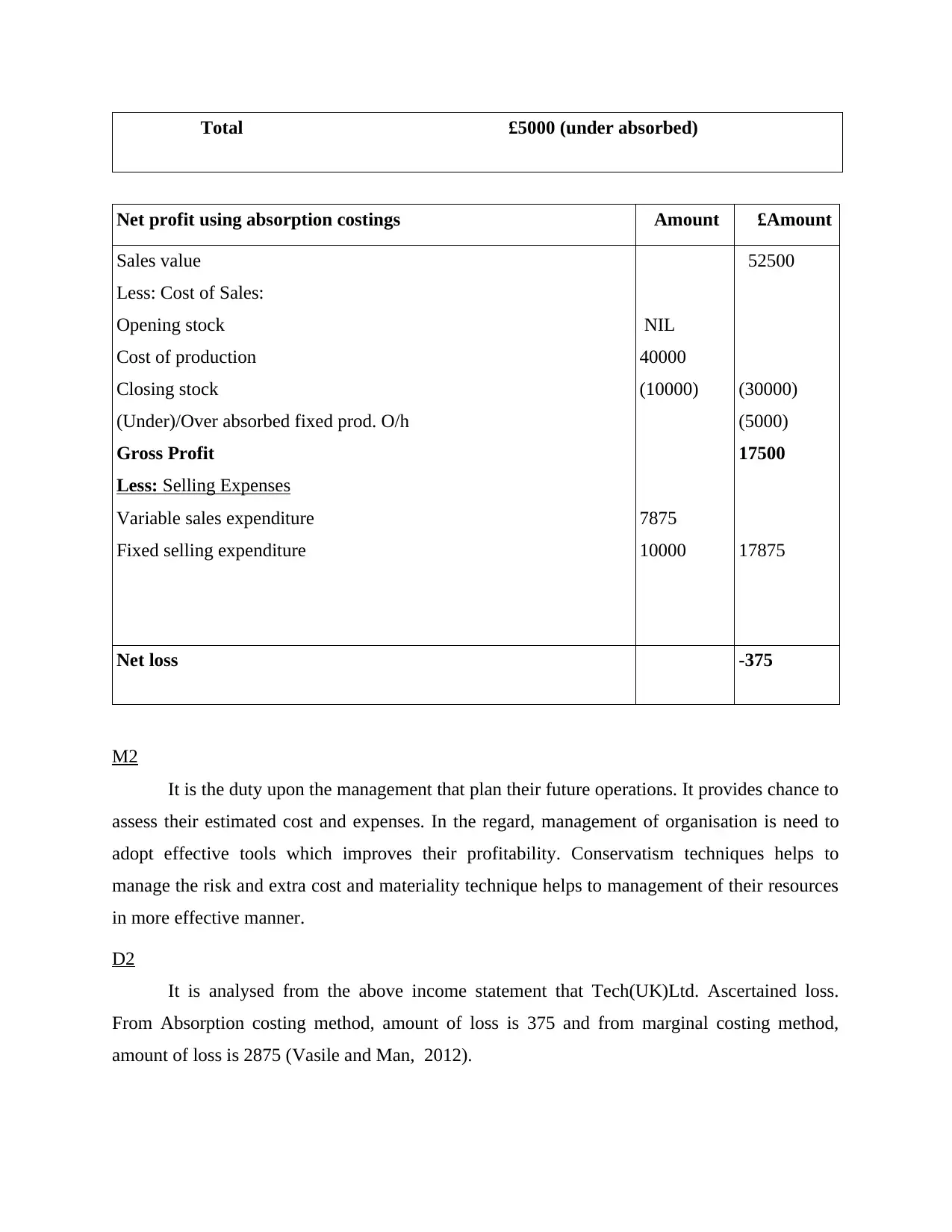

Total £5000 (under absorbed)

Net profit using absorption costings £Amount £Amount

Sales value

Less: Cost of Sales:

Opening stock

Cost of production

Closing stock

(Under)/Over absorbed fixed prod. O/h

Gross Profit

Less: Selling Expenses

Variable sales expenditure

Fixed selling expenditure

NIL

40000

(10000)

7875

10000

52500

(30000)

(5000)

17500

17875

Net loss -375

M2

It is the duty upon the management that plan their future operations. It provides chance to

assess their estimated cost and expenses. In the regard, management of organisation is need to

adopt effective tools which improves their profitability. Conservatism techniques helps to

manage the risk and extra cost and materiality technique helps to management of their resources

in more effective manner.

D2

It is analysed from the above income statement that Tech(UK)Ltd. Ascertained loss.

From Absorption costing method, amount of loss is 375 and from marginal costing method,

amount of loss is 2875 (Vasile and Man, 2012).

Net profit using absorption costings £Amount £Amount

Sales value

Less: Cost of Sales:

Opening stock

Cost of production

Closing stock

(Under)/Over absorbed fixed prod. O/h

Gross Profit

Less: Selling Expenses

Variable sales expenditure

Fixed selling expenditure

NIL

40000

(10000)

7875

10000

52500

(30000)

(5000)

17500

17875

Net loss -375

M2

It is the duty upon the management that plan their future operations. It provides chance to

assess their estimated cost and expenses. In the regard, management of organisation is need to

adopt effective tools which improves their profitability. Conservatism techniques helps to

manage the risk and extra cost and materiality technique helps to management of their resources

in more effective manner.

D2

It is analysed from the above income statement that Tech(UK)Ltd. Ascertained loss.

From Absorption costing method, amount of loss is 375 and from marginal costing method,

amount of loss is 2875 (Vasile and Man, 2012).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.