Accounting and Finance for Business: Pizza Franchise Project Analysis

VerifiedAdded on 2021/06/14

|10

|1980

|12

Homework Assignment

AI Summary

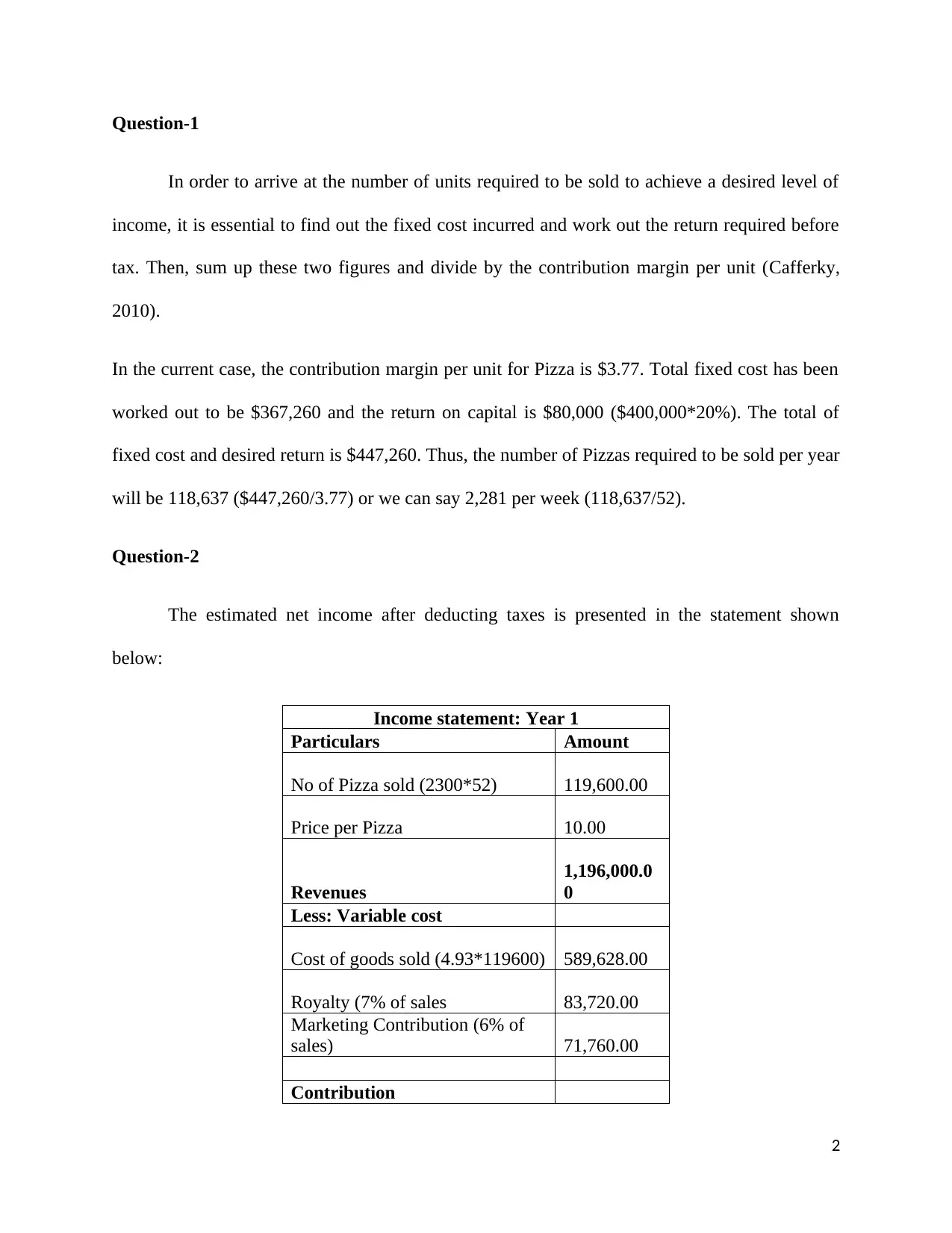

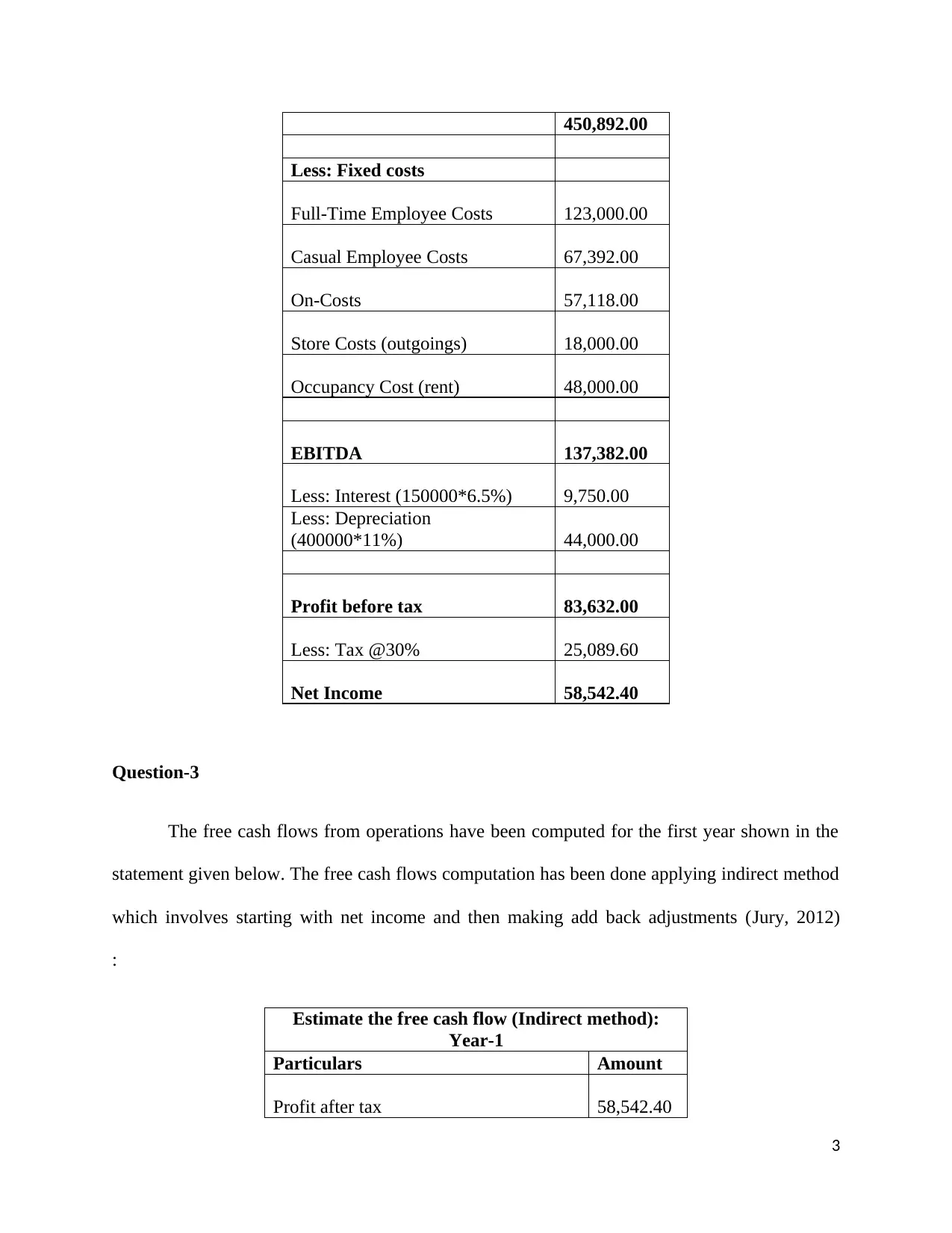

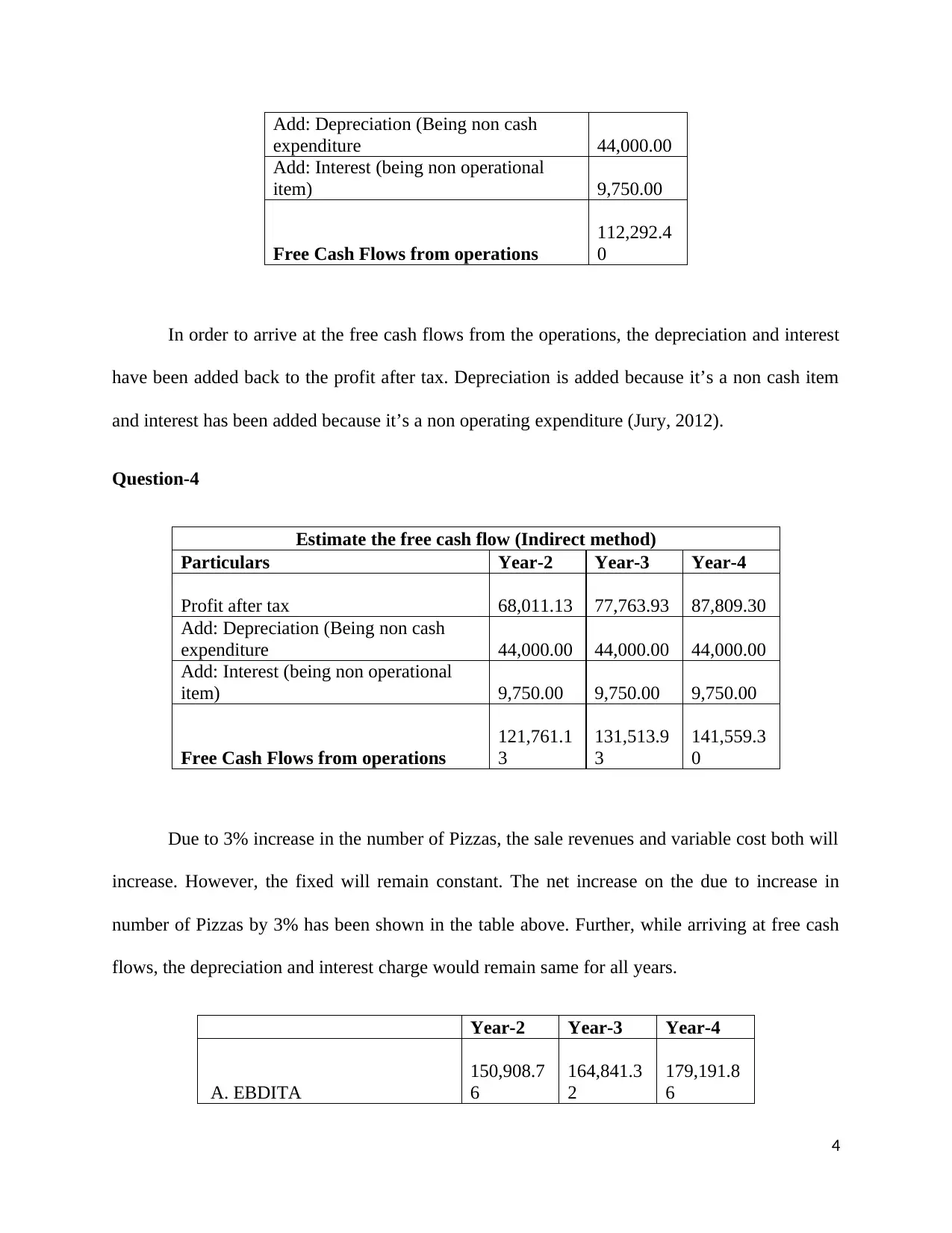

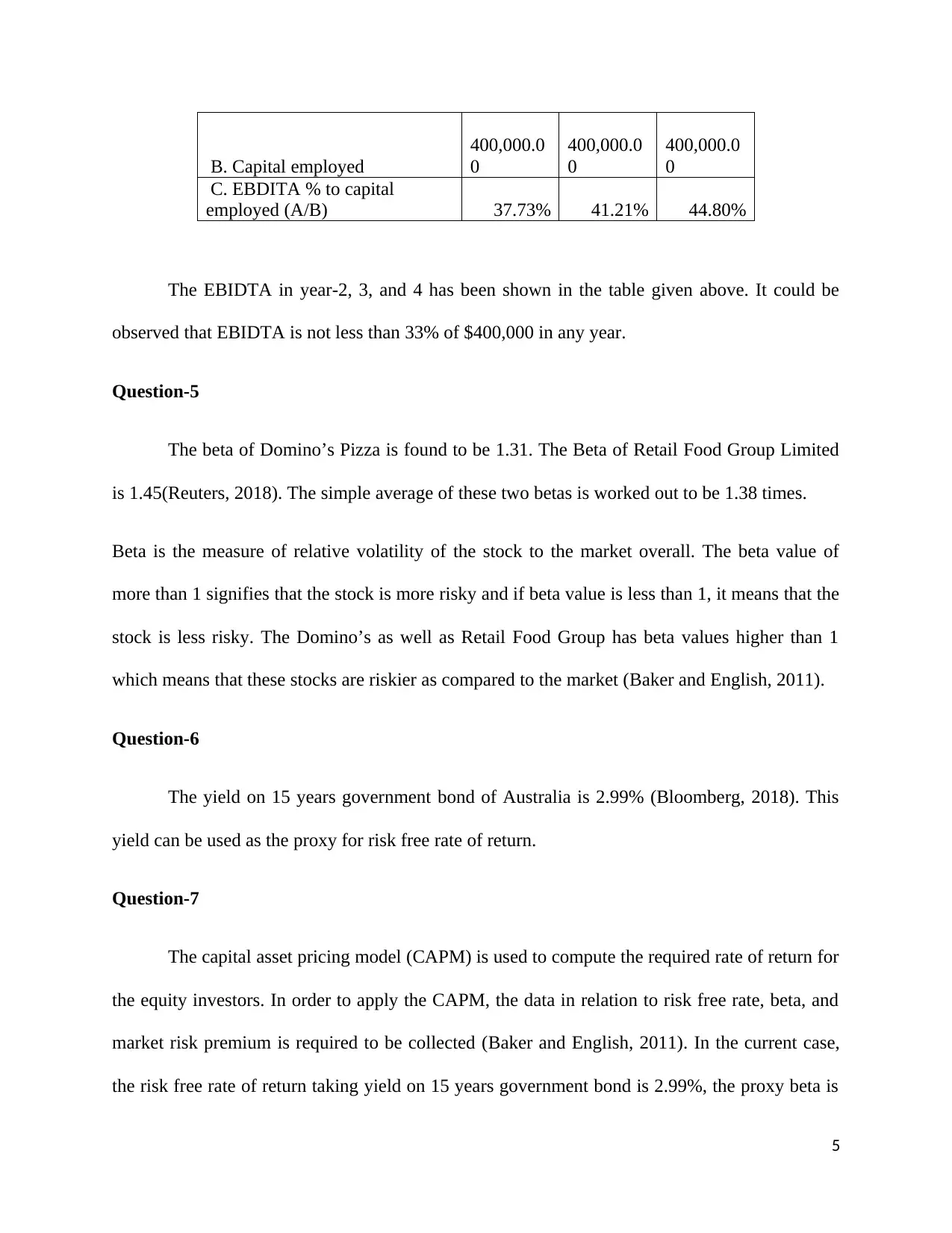

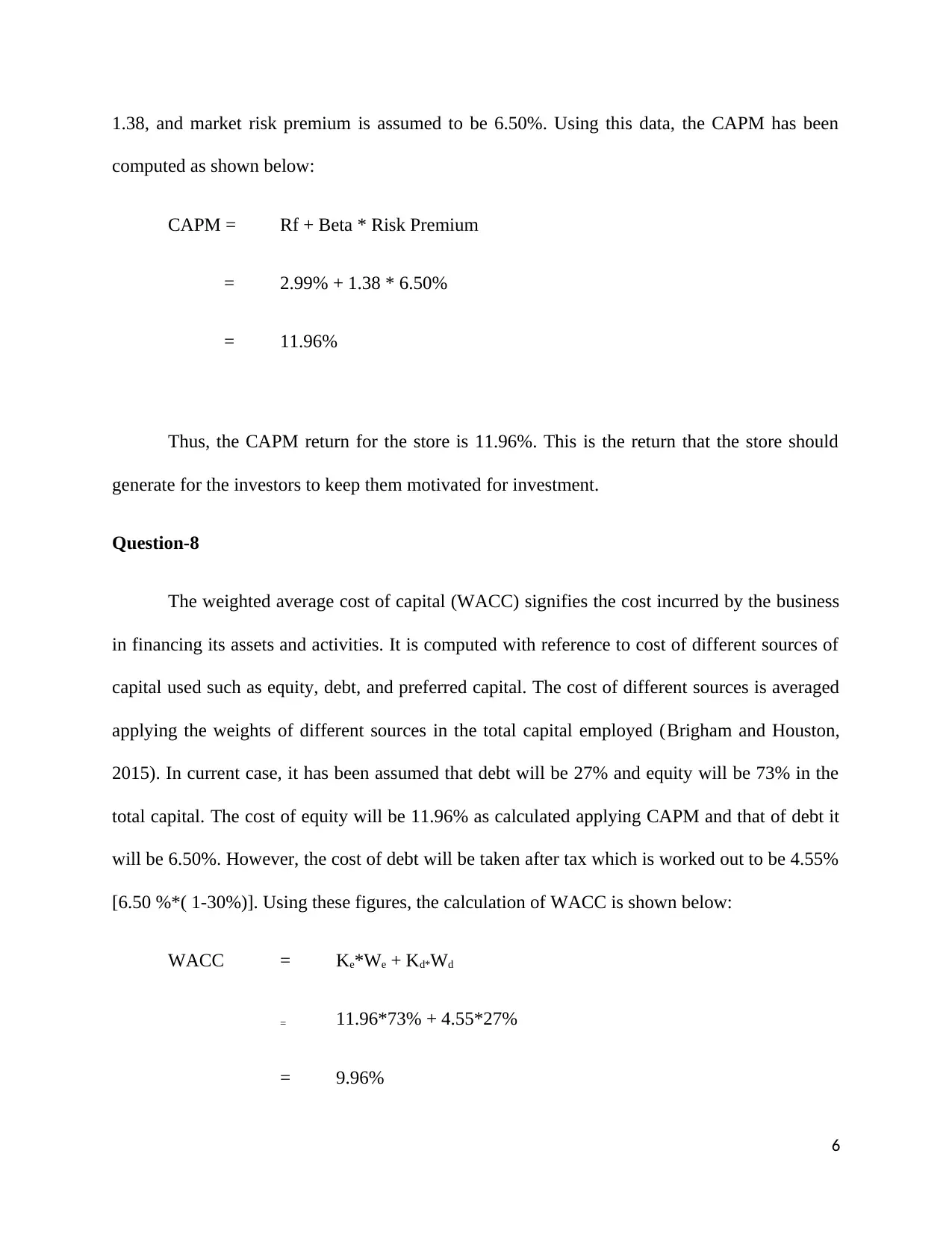

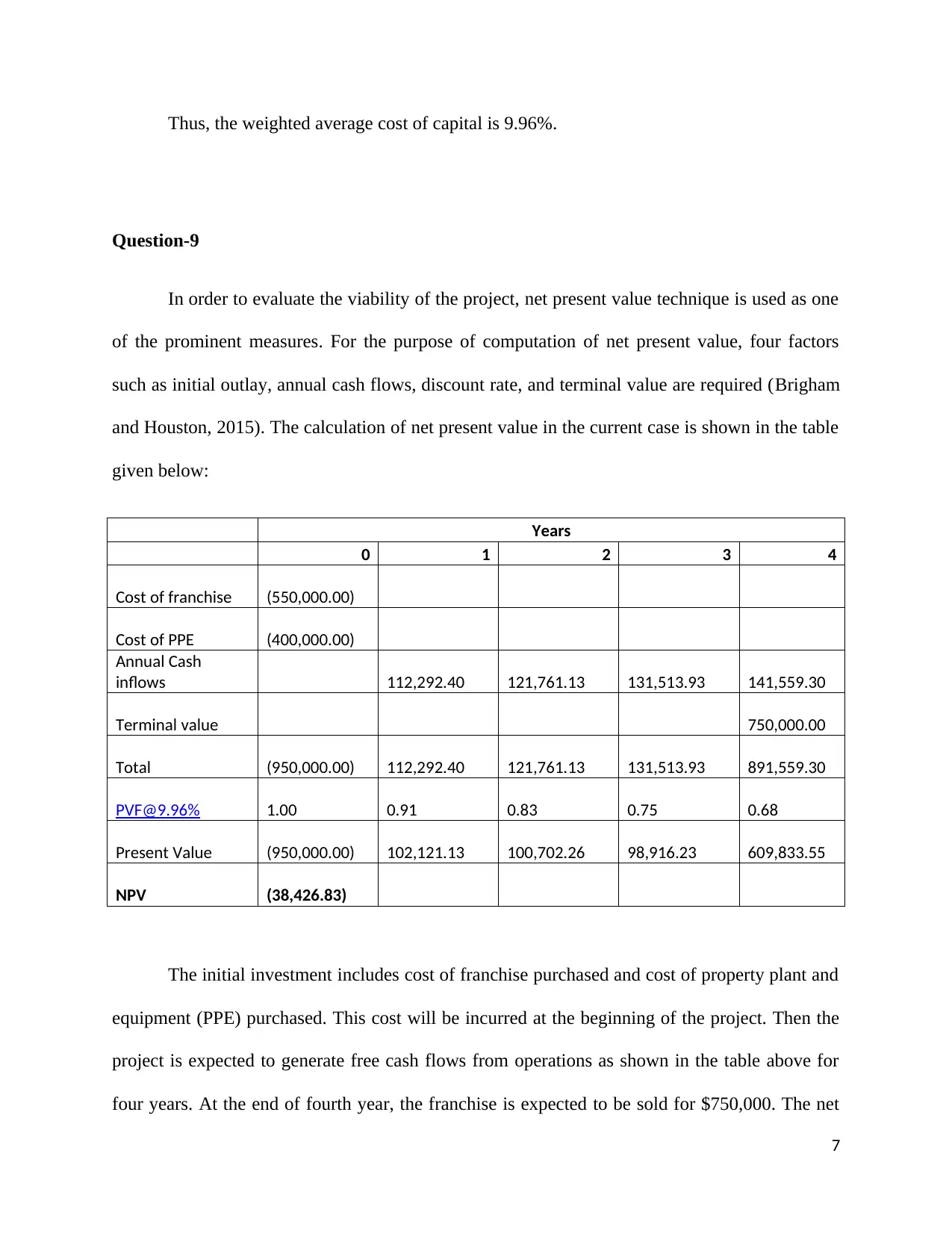

This assignment provides a comprehensive financial analysis of a proposed pizza franchise. It begins by calculating the number of pizzas required to break even, considering fixed and variable costs, and desired return on capital. An income statement is constructed to estimate net income, followed by a free cash flow analysis using the indirect method. The assignment then computes the Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) and assesses the franchise's beta and the risk-free rate to calculate the Capital Asset Pricing Model (CAPM) return and Weighted Average Cost of Capital (WACC). Finally, the Net Present Value (NPV) of the project is determined, leading to a recommendation to reject the project due to a negative NPV. The analysis also considers the risks associated with the project, such as market competition and regulatory changes, and references relevant financial literature.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.