Accounting Fundamentals: Financial Statement Presentation Essay

VerifiedAdded on 2023/06/14

|14

|3198

|121

Essay

AI Summary

This essay provides a comprehensive overview of accounting fundamentals, beginning with the preparation of financial statements for General Supplies Ltd. for the year ended 31/12/2021, including an adjusted trial balance, an income statement, and a balance sheet. It then critically analyzes key accounting principles such as the consistency principle, materiality principle, monetary unit principle, and going concern principle, explaining their relevance in the presentation of final accounts. The essay highlights how these principles ensure reliability, completeness, and relevance in financial reporting, enabling stakeholders to make informed decisions. Desklib offers more resources for students.

Essay on Accounting

Fundamentals

Fundamentals

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................2

TASK...............................................................................................................................................2

1.Financial Statements of General Supplies Ltd for the Year ended 31/12/2021:......................2

A. Adjusted Trial Balance:..........................................................................................................3

B Statement Showing Financial Performance:............................................................................4

C Statement Showing Financial Position:...................................................................................5

2.Critically analysis the accounting principle with relevance to the presentation of the final

accounts:......................................................................................................................................7

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................2

TASK...............................................................................................................................................2

1.Financial Statements of General Supplies Ltd for the Year ended 31/12/2021:......................2

A. Adjusted Trial Balance:..........................................................................................................3

B Statement Showing Financial Performance:............................................................................4

C Statement Showing Financial Position:...................................................................................5

2.Critically analysis the accounting principle with relevance to the presentation of the final

accounts:......................................................................................................................................7

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION

Accounting fundamentals is the basic function of maintaining the standard which include

keeping of records of the monetary information. For this, every organisation has to use standard

forms to store the data so that it can be retrieved easily when needs (AGĂNENCEI, GHERMAN, and

Sîrbulescu, 2021). These transactions which recorded should be accurate because it helps to take

decisions for the growth of the business. Some of the basic principle are mandatory for every

business entity to follow as it helps in gaining the information about the costs and incomes that

the business incur by ensuring the statutory compliance report. In the below report, trial balance

is adjusted of the General Supplies Ltd. and further for this income statement and balance sheet

is made. In the second part the principle of accounting fundamentals is explained with respective

to the preparation and representation of the financial documents.

TASK

1.Financial Statements of General Supplies Ltd for the Year ended 31/12/2021:

Financial Statement highlight the financial performance of the organisation during the

accounting period. These statement are thee written records that explains the activity of business

and performance of the entity. It is necessary to obtain certificate from the accountants that these

statements are audited completely. Financial Statements are divided into following categories

such as: -

Income Statement: Income statements represents the profit earned by the entity during the

year. These statements reflect the operating performance of the entity in accounting

period (Bergmann, Fuchs, and Schuler, 2019).

Statement of financial Performance: This statement is also known as Balance Sheet.

Balance shows the position of Assets and liabilities as on the particular data. These are

the reports which shows the company assets, liabilities and shareholders equity. It is one

of the important aspects of financial statement and the users evaluate balance sheet

properly in order to determine that whether to make investments in company or not.

Statement of Changes in Equity: This statement includes total comprehensive income of

the entity, which includes annul profit, the effect of changes in equity, and correction of

any errors that the entity made during the accounting year

Accounting fundamentals is the basic function of maintaining the standard which include

keeping of records of the monetary information. For this, every organisation has to use standard

forms to store the data so that it can be retrieved easily when needs (AGĂNENCEI, GHERMAN, and

Sîrbulescu, 2021). These transactions which recorded should be accurate because it helps to take

decisions for the growth of the business. Some of the basic principle are mandatory for every

business entity to follow as it helps in gaining the information about the costs and incomes that

the business incur by ensuring the statutory compliance report. In the below report, trial balance

is adjusted of the General Supplies Ltd. and further for this income statement and balance sheet

is made. In the second part the principle of accounting fundamentals is explained with respective

to the preparation and representation of the financial documents.

TASK

1.Financial Statements of General Supplies Ltd for the Year ended 31/12/2021:

Financial Statement highlight the financial performance of the organisation during the

accounting period. These statement are thee written records that explains the activity of business

and performance of the entity. It is necessary to obtain certificate from the accountants that these

statements are audited completely. Financial Statements are divided into following categories

such as: -

Income Statement: Income statements represents the profit earned by the entity during the

year. These statements reflect the operating performance of the entity in accounting

period (Bergmann, Fuchs, and Schuler, 2019).

Statement of financial Performance: This statement is also known as Balance Sheet.

Balance shows the position of Assets and liabilities as on the particular data. These are

the reports which shows the company assets, liabilities and shareholders equity. It is one

of the important aspects of financial statement and the users evaluate balance sheet

properly in order to determine that whether to make investments in company or not.

Statement of Changes in Equity: This statement includes total comprehensive income of

the entity, which includes annul profit, the effect of changes in equity, and correction of

any errors that the entity made during the accounting year

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Notes to Accounts: Notes to account are the supporting information which is annexed in

the bottom of financial statements which shows the details of adjustments made in the

balance sheet with respect to assets, liabilities, income and expenses (Blakey, 2021).

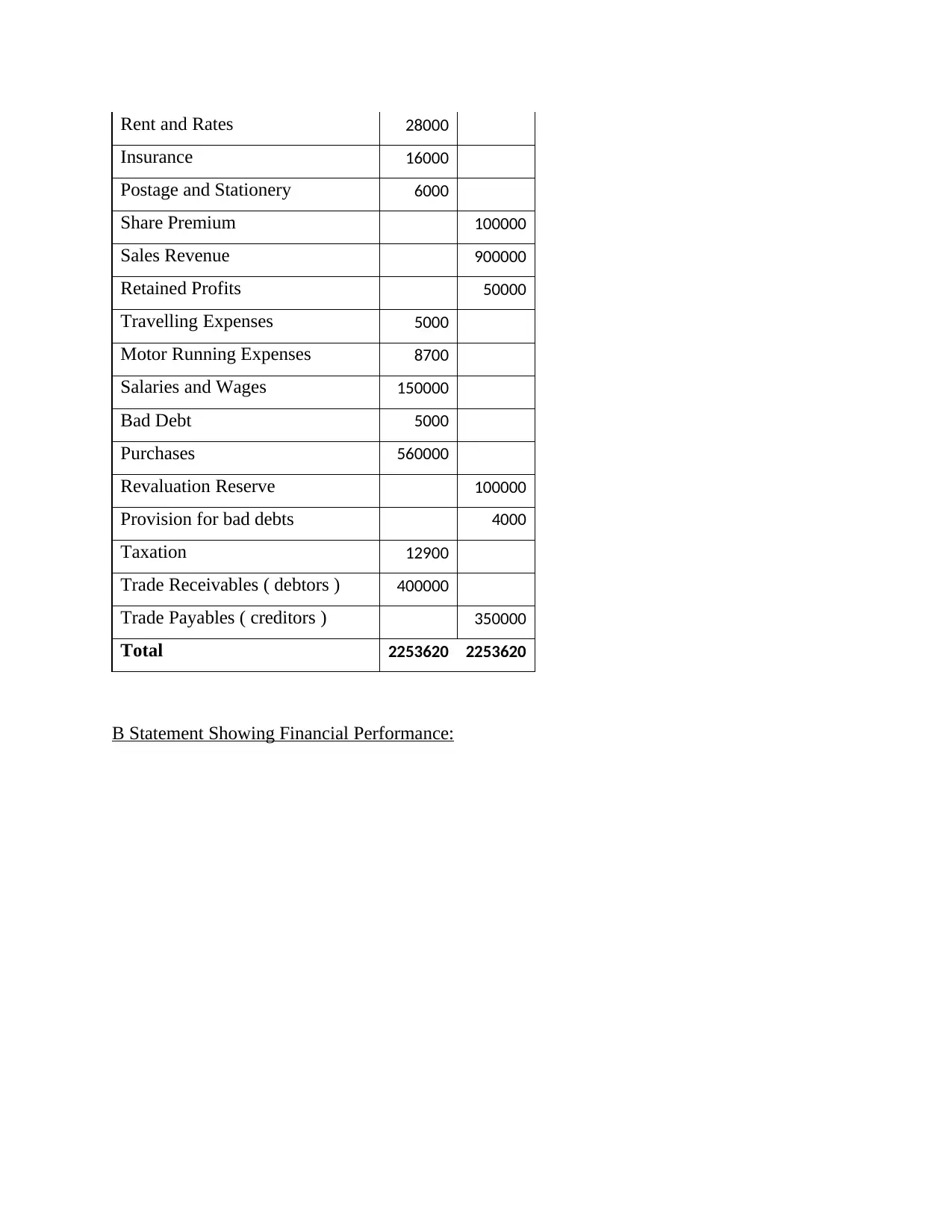

A. Adjusted Trial Balance:

Adjusted trial balance list the balance of various accounts after meeting all the adjustments

related to outstanding or prepaid expenses, unearned or accrued income etc. The total of adjusted

trial balance must be tallied before preparation of financial statements. The purpose of adjusted

trial balance is to ensure that all debits and credits in general ledger accounts are properly

transferred to financial statements (Breton, 2018.)

Adjusted Trial Balance For the

year ended 31/12/2021

Particular Debit Credit

Finance Income 4000

Finance Expense 16000

Share Capital 347900

Outstanding Rent and Rates 3220

Bank 2000

Opening Inventory 90000

Machinery at cost 120000

Buildings at cost 750000

Provision for Depreciation –

Buildings 137500

Depreciation on Building 37500

Prepaid Insurance 1520

Provision for Depreciation on

Machinery 55000

Depreciation on Machine 30000

Legal expenses 7000

Heating and Lighting 10000

Long Term Loans 200000

the bottom of financial statements which shows the details of adjustments made in the

balance sheet with respect to assets, liabilities, income and expenses (Blakey, 2021).

A. Adjusted Trial Balance:

Adjusted trial balance list the balance of various accounts after meeting all the adjustments

related to outstanding or prepaid expenses, unearned or accrued income etc. The total of adjusted

trial balance must be tallied before preparation of financial statements. The purpose of adjusted

trial balance is to ensure that all debits and credits in general ledger accounts are properly

transferred to financial statements (Breton, 2018.)

Adjusted Trial Balance For the

year ended 31/12/2021

Particular Debit Credit

Finance Income 4000

Finance Expense 16000

Share Capital 347900

Outstanding Rent and Rates 3220

Bank 2000

Opening Inventory 90000

Machinery at cost 120000

Buildings at cost 750000

Provision for Depreciation –

Buildings 137500

Depreciation on Building 37500

Prepaid Insurance 1520

Provision for Depreciation on

Machinery 55000

Depreciation on Machine 30000

Legal expenses 7000

Heating and Lighting 10000

Long Term Loans 200000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Rent and Rates 28000

Insurance 16000

Postage and Stationery 6000

Share Premium 100000

Sales Revenue 900000

Retained Profits 50000

Travelling Expenses 5000

Motor Running Expenses 8700

Salaries and Wages 150000

Bad Debt 5000

Purchases 560000

Revaluation Reserve 100000

Provision for bad debts 4000

Taxation 12900

Trade Receivables ( debtors ) 400000

Trade Payables ( creditors ) 350000

Total 2253620 2253620

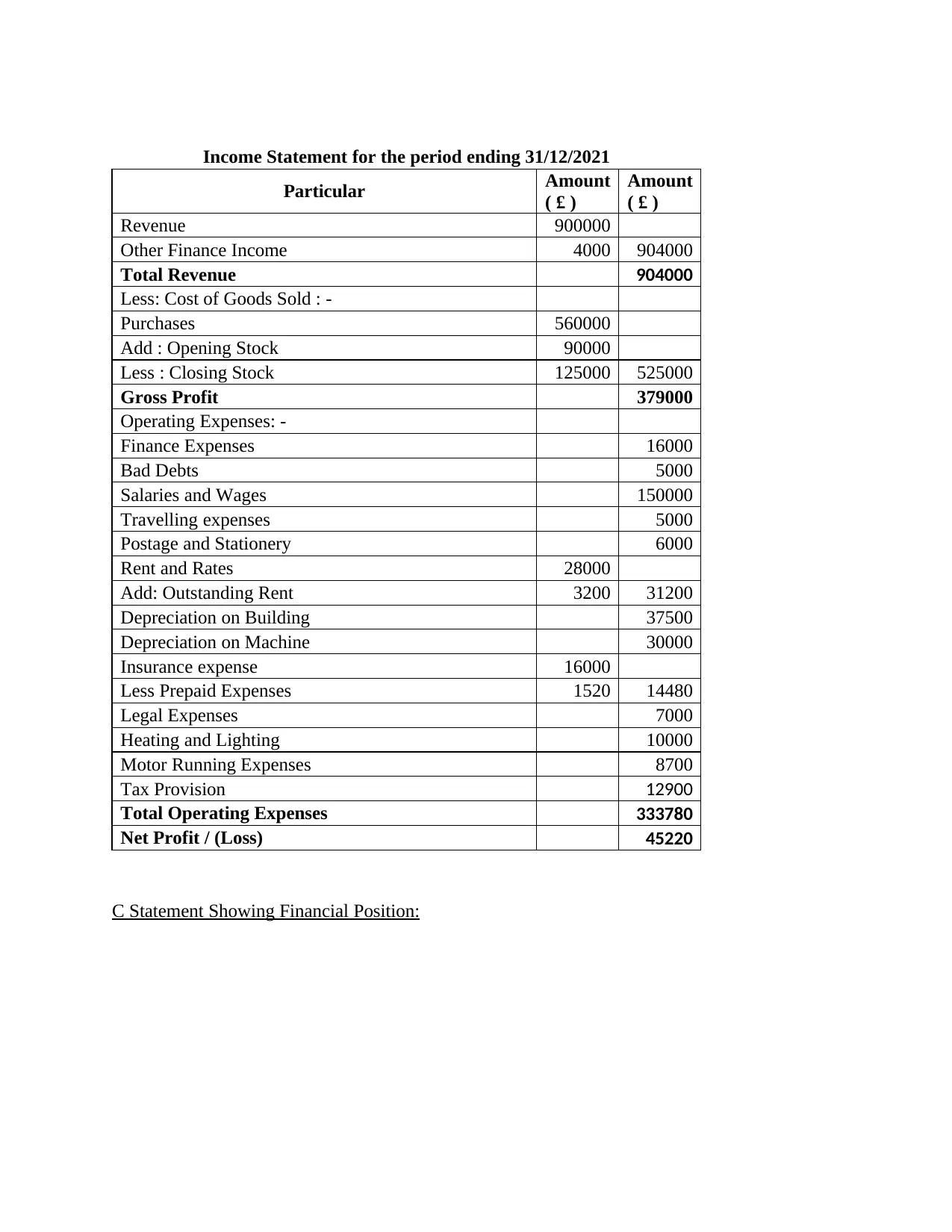

B Statement Showing Financial Performance:

Insurance 16000

Postage and Stationery 6000

Share Premium 100000

Sales Revenue 900000

Retained Profits 50000

Travelling Expenses 5000

Motor Running Expenses 8700

Salaries and Wages 150000

Bad Debt 5000

Purchases 560000

Revaluation Reserve 100000

Provision for bad debts 4000

Taxation 12900

Trade Receivables ( debtors ) 400000

Trade Payables ( creditors ) 350000

Total 2253620 2253620

B Statement Showing Financial Performance:

Income Statement for the period ending 31/12/2021

Particular Amount

( £ )

Amount

( £ )

Revenue 900000

Other Finance Income 4000 904000

Total Revenue 904000

Less: Cost of Goods Sold : -

Purchases 560000

Add : Opening Stock 90000

Less : Closing Stock 125000 525000

Gross Profit 379000

Operating Expenses: -

Finance Expenses 16000

Bad Debts 5000

Salaries and Wages 150000

Travelling expenses 5000

Postage and Stationery 6000

Rent and Rates 28000

Add: Outstanding Rent 3200 31200

Depreciation on Building 37500

Depreciation on Machine 30000

Insurance expense 16000

Less Prepaid Expenses 1520 14480

Legal Expenses 7000

Heating and Lighting 10000

Motor Running Expenses 8700

Tax Provision 12900

Total Operating Expenses 333780

Net Profit / (Loss) 45220

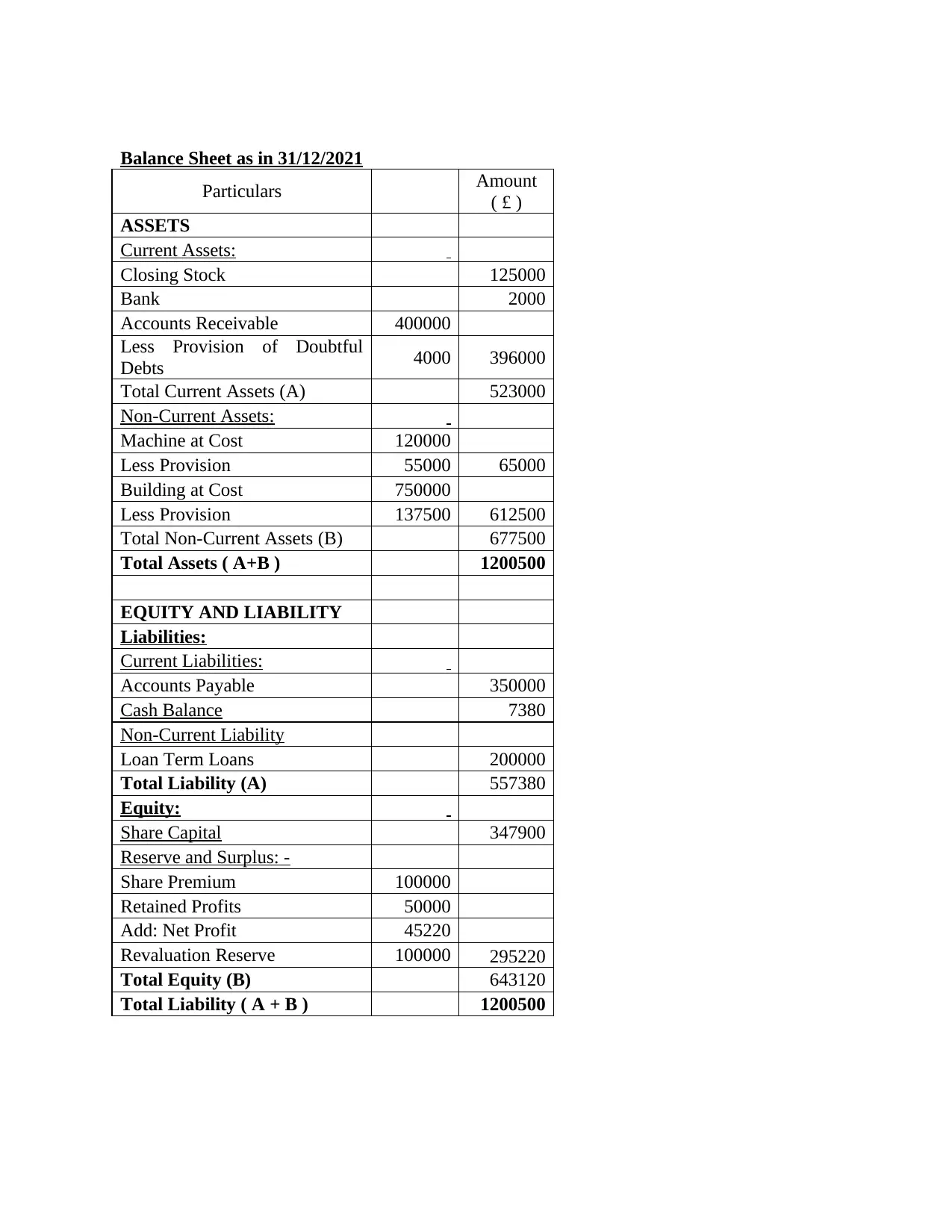

C Statement Showing Financial Position:

Particular Amount

( £ )

Amount

( £ )

Revenue 900000

Other Finance Income 4000 904000

Total Revenue 904000

Less: Cost of Goods Sold : -

Purchases 560000

Add : Opening Stock 90000

Less : Closing Stock 125000 525000

Gross Profit 379000

Operating Expenses: -

Finance Expenses 16000

Bad Debts 5000

Salaries and Wages 150000

Travelling expenses 5000

Postage and Stationery 6000

Rent and Rates 28000

Add: Outstanding Rent 3200 31200

Depreciation on Building 37500

Depreciation on Machine 30000

Insurance expense 16000

Less Prepaid Expenses 1520 14480

Legal Expenses 7000

Heating and Lighting 10000

Motor Running Expenses 8700

Tax Provision 12900

Total Operating Expenses 333780

Net Profit / (Loss) 45220

C Statement Showing Financial Position:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Balance Sheet as in 31/12/2021

Particulars Amount

( £ )

ASSETS

Current Assets:

Closing Stock 125000

Bank 2000

Accounts Receivable 400000

Less Provision of Doubtful

Debts 4000 396000

Total Current Assets (A) 523000

Non-Current Assets:

Machine at Cost 120000

Less Provision 55000 65000

Building at Cost 750000

Less Provision 137500 612500

Total Non-Current Assets (B) 677500

Total Assets ( A+B ) 1200500

EQUITY AND LIABILITY

Liabilities:

Current Liabilities:

Accounts Payable 350000

Cash Balance 7380

Non-Current Liability

Loan Term Loans 200000

Total Liability (A) 557380

Equity:

Share Capital 347900

Reserve and Surplus: -

Share Premium 100000

Retained Profits 50000

Add: Net Profit 45220

Revaluation Reserve 100000 295220

Total Equity (B) 643120

Total Liability ( A + B ) 1200500

Particulars Amount

( £ )

ASSETS

Current Assets:

Closing Stock 125000

Bank 2000

Accounts Receivable 400000

Less Provision of Doubtful

Debts 4000 396000

Total Current Assets (A) 523000

Non-Current Assets:

Machine at Cost 120000

Less Provision 55000 65000

Building at Cost 750000

Less Provision 137500 612500

Total Non-Current Assets (B) 677500

Total Assets ( A+B ) 1200500

EQUITY AND LIABILITY

Liabilities:

Current Liabilities:

Accounts Payable 350000

Cash Balance 7380

Non-Current Liability

Loan Term Loans 200000

Total Liability (A) 557380

Equity:

Share Capital 347900

Reserve and Surplus: -

Share Premium 100000

Retained Profits 50000

Add: Net Profit 45220

Revaluation Reserve 100000 295220

Total Equity (B) 643120

Total Liability ( A + B ) 1200500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.Critically analysis the accounting principle with relevance to the presentation of the final

accounts:

Consistency Principle: The basic accounting principle of consistency states that the its should

remain the same the accounting methods are applied in the financial period of time. It is helpful

is measuring the trends. It is a significant for a business both according to bookkeeping and

reviewing perspective as having a reliable arrangement of bookkeeping standards, systems helps

bookkeepers in recording deals in a deliberate way (Callejas and Ocampo-Salazar, 2021). While on

account of reviewers, it helps looking at business information a lot more straightforward as

similar bookkeeping strategies are followed reliably. It additionally furnishes the partners and

investors with a feeling of fulfilment that the exhibition of the business can be followed utilizing

an attempted and tried bookkeeping philosophy which gives predictable outcomes. The exactness

of the gave data can be guaranteed as there is no change while following consistency standard,

which empowers investors and the board in settling on better business choices.

Comparable fiscal information: By utilizing a steady bookkeeping strategy starting with one

bookkeeping period then onto the next, the monetary reports will all hold a comparable

construction. This makes it more straightforward for investors, supervisors, banks, and different

partners to think about the presentation of the business over various monetary years (Emilina,

Hisam, and Norsuriati, 2018).

Familiarisation: A steady bookkeeping strategy can be both expense and time effective.

Bookkeepers and supervisors will get comfortable with the bookkeeping strategy, and by being

predictable, you will just require the underlying preparation for this technique.

Auditors: Examiners are outside people who are prepared to ensure the bookkeeping

information given by an organization compares to the exercises of that organization. Following

the consistency guideline, examiners will request purposes behind any progressions that could

influence the translation of the fiscal reports of a business.

It likewise furnishes the partners and investors with a feeling of fulfilment that the presentation

of the business can be followed utilizing an attempted and tried bookkeeping strategy which

gives steady outcomes.

accounts:

Consistency Principle: The basic accounting principle of consistency states that the its should

remain the same the accounting methods are applied in the financial period of time. It is helpful

is measuring the trends. It is a significant for a business both according to bookkeeping and

reviewing perspective as having a reliable arrangement of bookkeeping standards, systems helps

bookkeepers in recording deals in a deliberate way (Callejas and Ocampo-Salazar, 2021). While on

account of reviewers, it helps looking at business information a lot more straightforward as

similar bookkeeping strategies are followed reliably. It additionally furnishes the partners and

investors with a feeling of fulfilment that the exhibition of the business can be followed utilizing

an attempted and tried bookkeeping philosophy which gives predictable outcomes. The exactness

of the gave data can be guaranteed as there is no change while following consistency standard,

which empowers investors and the board in settling on better business choices.

Comparable fiscal information: By utilizing a steady bookkeeping strategy starting with one

bookkeeping period then onto the next, the monetary reports will all hold a comparable

construction. This makes it more straightforward for investors, supervisors, banks, and different

partners to think about the presentation of the business over various monetary years (Emilina,

Hisam, and Norsuriati, 2018).

Familiarisation: A steady bookkeeping strategy can be both expense and time effective.

Bookkeepers and supervisors will get comfortable with the bookkeeping strategy, and by being

predictable, you will just require the underlying preparation for this technique.

Auditors: Examiners are outside people who are prepared to ensure the bookkeeping

information given by an organization compares to the exercises of that organization. Following

the consistency guideline, examiners will request purposes behind any progressions that could

influence the translation of the fiscal reports of a business.

It likewise furnishes the partners and investors with a feeling of fulfilment that the presentation

of the business can be followed utilizing an attempted and tried bookkeeping strategy which

gives steady outcomes.

Principle of Materiality: It is a bookkeeping guideline which expresses that all things that are

sensibly prone to affect the investors are very dynamic and should be recorded or announced

thoroughly in the entities fiscal reports utilizing GAAP principles.

Basically, materiality is connected with the meaning of data inside an organization's budget

reports. Assuming an exchange or business choice is sufficiently huge to warrant answering to

investors or different clients of the fiscal reports, that data is "material" to the business and can't

be excluded (Jassem and Razzak, 2021). The materiality standard is particularly significant while

concluding whether an exchange ought to be recorded as a feature of the end interaction, since

dispensing with certain exchanges can altogether diminish how much time expected to give

budget reports. It is valuable to talk about with the organization inspectors comprises a material

thing, so there will be no issues with these things when the budget summaries are evaluated.

It also states the business concern does not need to accumulate all the petty information which

will not have a crucial impact on the accounting performance of the business. It also measures a

significance of the user of the financial statement which is relevant in nature for the organisation.

Significance:

Reliability: The oversight of a material or significant truth from the fiscal summaries might

think twice about client's capacity to take right choices. This is on the grounds that the greater

part of the financial backers chooses whether to put resources into an organization or not in light

of their investigation of that organization's fiscal reports. Along these lines, assuming the fiscal

reports of an organization discard specific data, the unwavering quality of the budget summaries

will turn out to be low (Jourdain, 2021).

Completeness: As per GAAP, the fiscal reports of an organization should address 'valid and fair'

perspective on the business. To have the option to do this, the data contained in its budget reports

should be 'finished' in all material viewpoints. Thus, on the off chance that a material piece of

data is absent in an organization's budget reports, the assertions cannot be thought of as

sensibly prone to affect the investors are very dynamic and should be recorded or announced

thoroughly in the entities fiscal reports utilizing GAAP principles.

Basically, materiality is connected with the meaning of data inside an organization's budget

reports. Assuming an exchange or business choice is sufficiently huge to warrant answering to

investors or different clients of the fiscal reports, that data is "material" to the business and can't

be excluded (Jassem and Razzak, 2021). The materiality standard is particularly significant while

concluding whether an exchange ought to be recorded as a feature of the end interaction, since

dispensing with certain exchanges can altogether diminish how much time expected to give

budget reports. It is valuable to talk about with the organization inspectors comprises a material

thing, so there will be no issues with these things when the budget summaries are evaluated.

It also states the business concern does not need to accumulate all the petty information which

will not have a crucial impact on the accounting performance of the business. It also measures a

significance of the user of the financial statement which is relevant in nature for the organisation.

Significance:

Reliability: The oversight of a material or significant truth from the fiscal summaries might

think twice about client's capacity to take right choices. This is on the grounds that the greater

part of the financial backers chooses whether to put resources into an organization or not in light

of their investigation of that organization's fiscal reports. Along these lines, assuming the fiscal

reports of an organization discard specific data, the unwavering quality of the budget summaries

will turn out to be low (Jourdain, 2021).

Completeness: As per GAAP, the fiscal reports of an organization should address 'valid and fair'

perspective on the business. To have the option to do this, the data contained in its budget reports

should be 'finished' in all material viewpoints. Thus, on the off chance that a material piece of

data is absent in an organization's budget reports, the assertions cannot be thought of as

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

complete. Furthermore, in this manner, they are unequipped for giving a valid and fair

perspective on the business.

Relevance: Just the material data is applicable to the necessities of clients. Thus, in the event

that the Income Statement of an organization is loaded down with such countless classes of costs,

with a little pay from a wide range of sources, etc., which don't at all mainly affect the choices of

clients, a significant piece of the pay explanation becomes immaterial for the. Subsequently, the

materiality idea additionally impacts the importance of the data introduced in the fiscal reports of

a business (Madsen, 2020).

Principle of monetary unit: According to this principle the entity can record those transaction

only which are expressed in terms of currency only. It means that who transaction’s which are

not in monetary terms such as the employees skill test in terms of unskilled or skilled, the service

quality that a concern serves to their customer, the technical performance of engineering

personnel etc are not to be adjusted in final accounts of entity. It can be explained with help of

example such as when an organisation purchase plant and machine worth Rs 100000 of its office

use and such asset useful life is 35 years. The monetary value of Rs 100000 is recorded as

purchases in the books however is non-monetary life of 35 years cannot be recorded (Moerman

and van der Laan, 2021).

This principle is again one of the generally accepted accounting principle that must be complied

by all the business enterprise. Over the period of time, money has been adopted as a unit for

measurement principle. According to this principle when any transaction occurs between party’s

then firstly it is converted into money and recoded in books of accounts of both parties involved

in transaction. This principle considers one assumption that the value of currency is stable over

the period of time. It means that in day-to-day use, monetary unit allows accounts executive to

consider financial statements of company which are recorded from multiple financial periods

assuming they were same during those periods.

Principle of going concern: According to this principle the organisation will run forever in the

foreseeable future. It assumes that the business will not be liquidate its operation and ran

continuously in future but the only difference is its management and board of directors’ changes

perspective on the business.

Relevance: Just the material data is applicable to the necessities of clients. Thus, in the event

that the Income Statement of an organization is loaded down with such countless classes of costs,

with a little pay from a wide range of sources, etc., which don't at all mainly affect the choices of

clients, a significant piece of the pay explanation becomes immaterial for the. Subsequently, the

materiality idea additionally impacts the importance of the data introduced in the fiscal reports of

a business (Madsen, 2020).

Principle of monetary unit: According to this principle the entity can record those transaction

only which are expressed in terms of currency only. It means that who transaction’s which are

not in monetary terms such as the employees skill test in terms of unskilled or skilled, the service

quality that a concern serves to their customer, the technical performance of engineering

personnel etc are not to be adjusted in final accounts of entity. It can be explained with help of

example such as when an organisation purchase plant and machine worth Rs 100000 of its office

use and such asset useful life is 35 years. The monetary value of Rs 100000 is recorded as

purchases in the books however is non-monetary life of 35 years cannot be recorded (Moerman

and van der Laan, 2021).

This principle is again one of the generally accepted accounting principle that must be complied

by all the business enterprise. Over the period of time, money has been adopted as a unit for

measurement principle. According to this principle when any transaction occurs between party’s

then firstly it is converted into money and recoded in books of accounts of both parties involved

in transaction. This principle considers one assumption that the value of currency is stable over

the period of time. It means that in day-to-day use, monetary unit allows accounts executive to

consider financial statements of company which are recorded from multiple financial periods

assuming they were same during those periods.

Principle of going concern: According to this principle the organisation will run forever in the

foreseeable future. It assumes that the business will not be liquidate its operation and ran

continuously in future but the only difference is its management and board of directors’ changes

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

in the upcoming period. Considering this assumption, the management of enterprise defers

certain expensed to be debited in profit and loss account over certain period. It is a predefined

assumption in any sort of business that it will run but however when the management notices that

they are unable to meet the obligation raised by creditors and debt holders in future then they

have to mentioned the fact in report that their going concern is affected so that users of business

concern can understand the actual picture of organisation (Predeus, Mashentseva, and Predeus,

2021).

In order to judge the going concern assumption the company auditor evaluated organisation’s

ability to continue for one year period following the date for financial statements being audited.

The auditor considers following items which raises doubt in their mind about entity’s ability to

continue as going concern. They are as follows: -

There is negative operating cash flows which includes series of losses the organisation

faces.

The entity is making default in repayment of loan on due dates.

The supplier of entity is denying credit to entity.

There are extravagant commitments for long period which bound the entity (Prosekov,

2020).

There is legal proceeding initiated against the company by various customer for quality

issues or other matters etc.

This are certain issues which must be addressed by the auditor in his audit report by

qualifying the same so that investors get the true working picture of entity.

CONCLUSION

Financial Statements are essential part of business organisation as they define the performance of

the organisation over the accounting period. These statements are prepared by the accountant of

the entity for 12 months and then these statements are audited by auditors of business concern. In

this report financial statements are prepared which includes adjusted trial balance, income

statement and balance sheet. Further accounting principle such as concept of materiality,

monetary unit principle, going concern assumptions are briefly explained along with live

examples. These principles are essential part of account process which directly work around

these principles and must be duly complied with by management of enterprise otherwise the

statements prepared does not reflect true picture of corporation. These accounting principle built

certain expensed to be debited in profit and loss account over certain period. It is a predefined

assumption in any sort of business that it will run but however when the management notices that

they are unable to meet the obligation raised by creditors and debt holders in future then they

have to mentioned the fact in report that their going concern is affected so that users of business

concern can understand the actual picture of organisation (Predeus, Mashentseva, and Predeus,

2021).

In order to judge the going concern assumption the company auditor evaluated organisation’s

ability to continue for one year period following the date for financial statements being audited.

The auditor considers following items which raises doubt in their mind about entity’s ability to

continue as going concern. They are as follows: -

There is negative operating cash flows which includes series of losses the organisation

faces.

The entity is making default in repayment of loan on due dates.

The supplier of entity is denying credit to entity.

There are extravagant commitments for long period which bound the entity (Prosekov,

2020).

There is legal proceeding initiated against the company by various customer for quality

issues or other matters etc.

This are certain issues which must be addressed by the auditor in his audit report by

qualifying the same so that investors get the true working picture of entity.

CONCLUSION

Financial Statements are essential part of business organisation as they define the performance of

the organisation over the accounting period. These statements are prepared by the accountant of

the entity for 12 months and then these statements are audited by auditors of business concern. In

this report financial statements are prepared which includes adjusted trial balance, income

statement and balance sheet. Further accounting principle such as concept of materiality,

monetary unit principle, going concern assumptions are briefly explained along with live

examples. These principles are essential part of account process which directly work around

these principles and must be duly complied with by management of enterprise otherwise the

statements prepared does not reflect true picture of corporation. These accounting principle built

a strong foundation for an enterprise for the longer period and investors are ready to invest their

funds in those enterprise whose books of accounts are clear with respect to compliance of these

principles.

funds in those enterprise whose books of accounts are clear with respect to compliance of these

principles.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.