Management Accounting: Cost Elements, Costing and Overhead Allocation

VerifiedAdded on 2020/01/23

|12

|2012

|199

Report

AI Summary

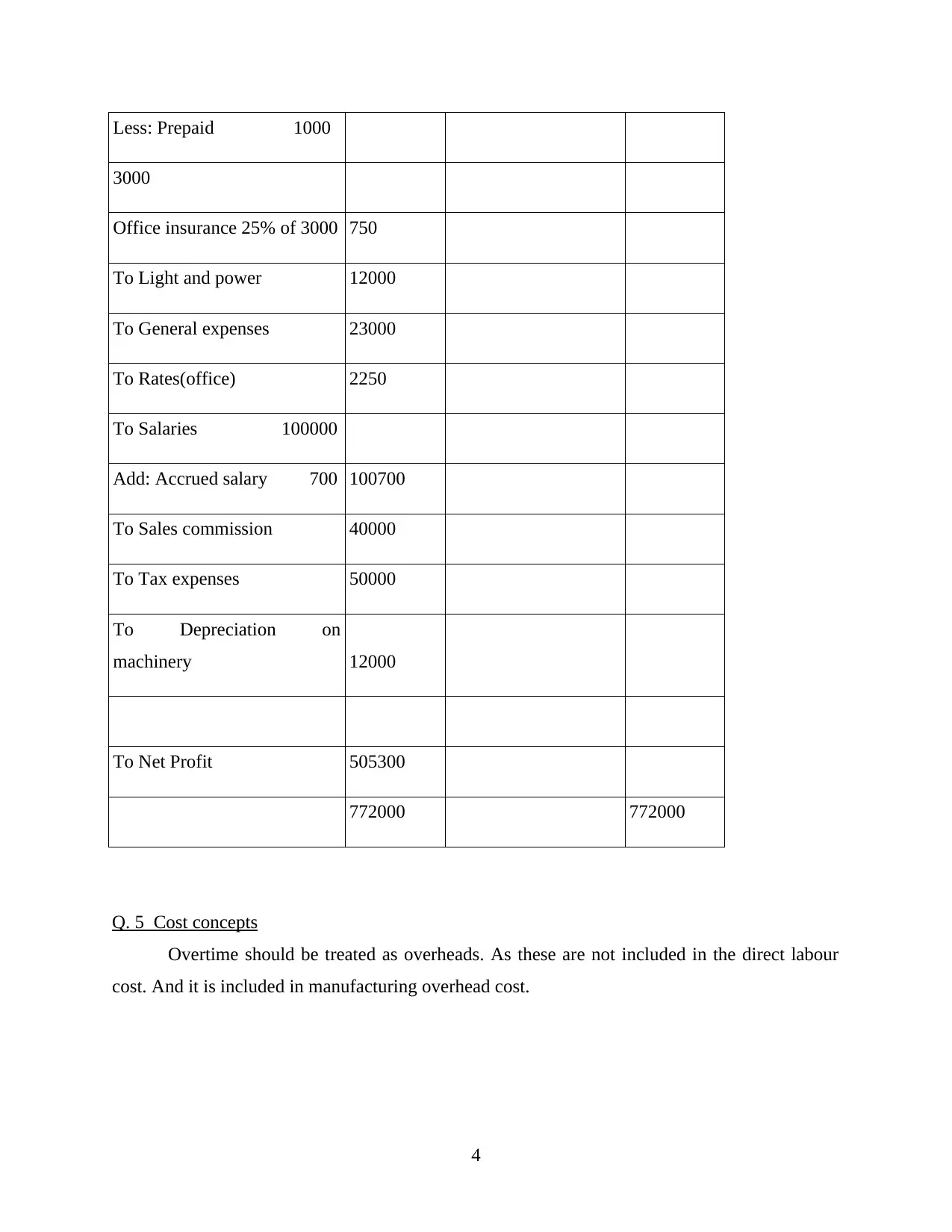

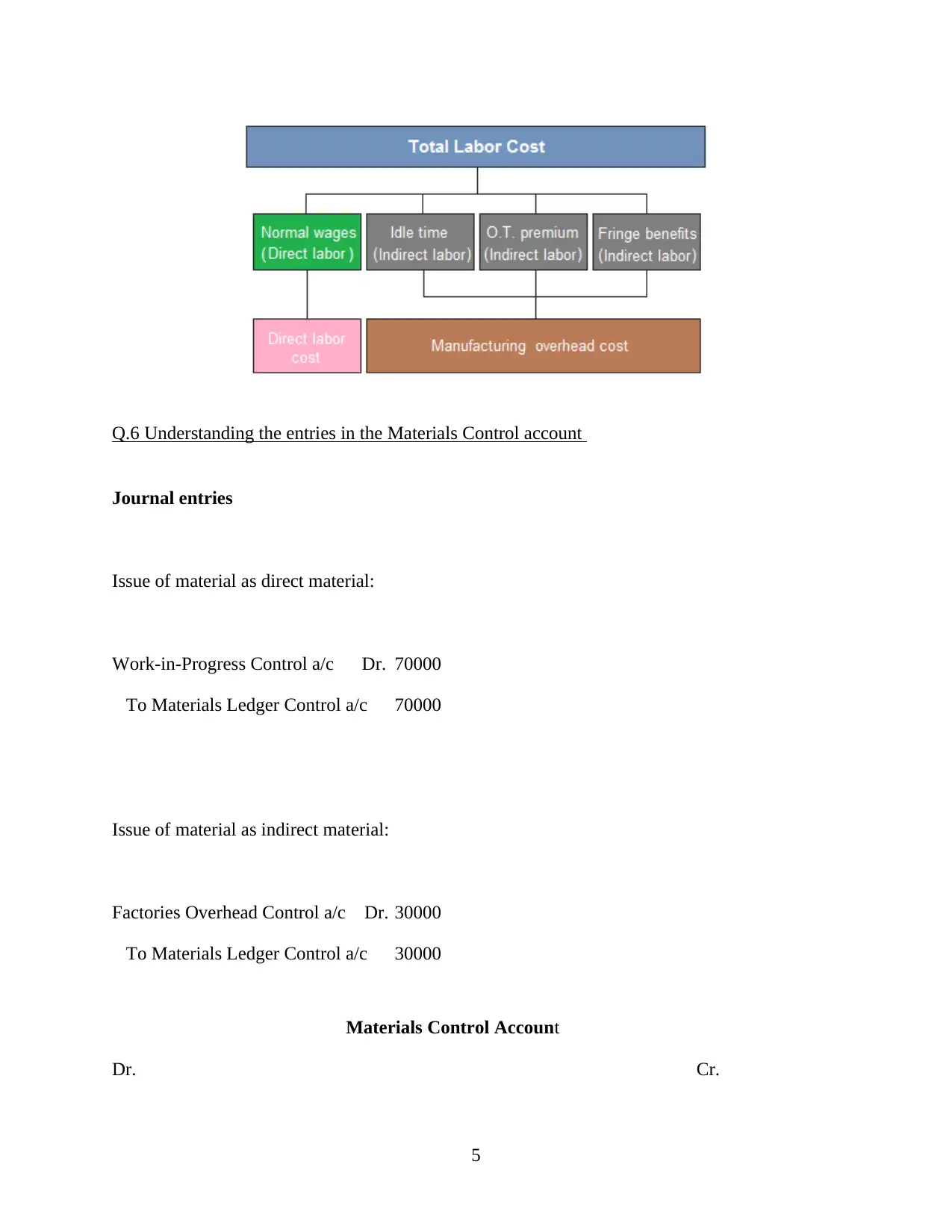

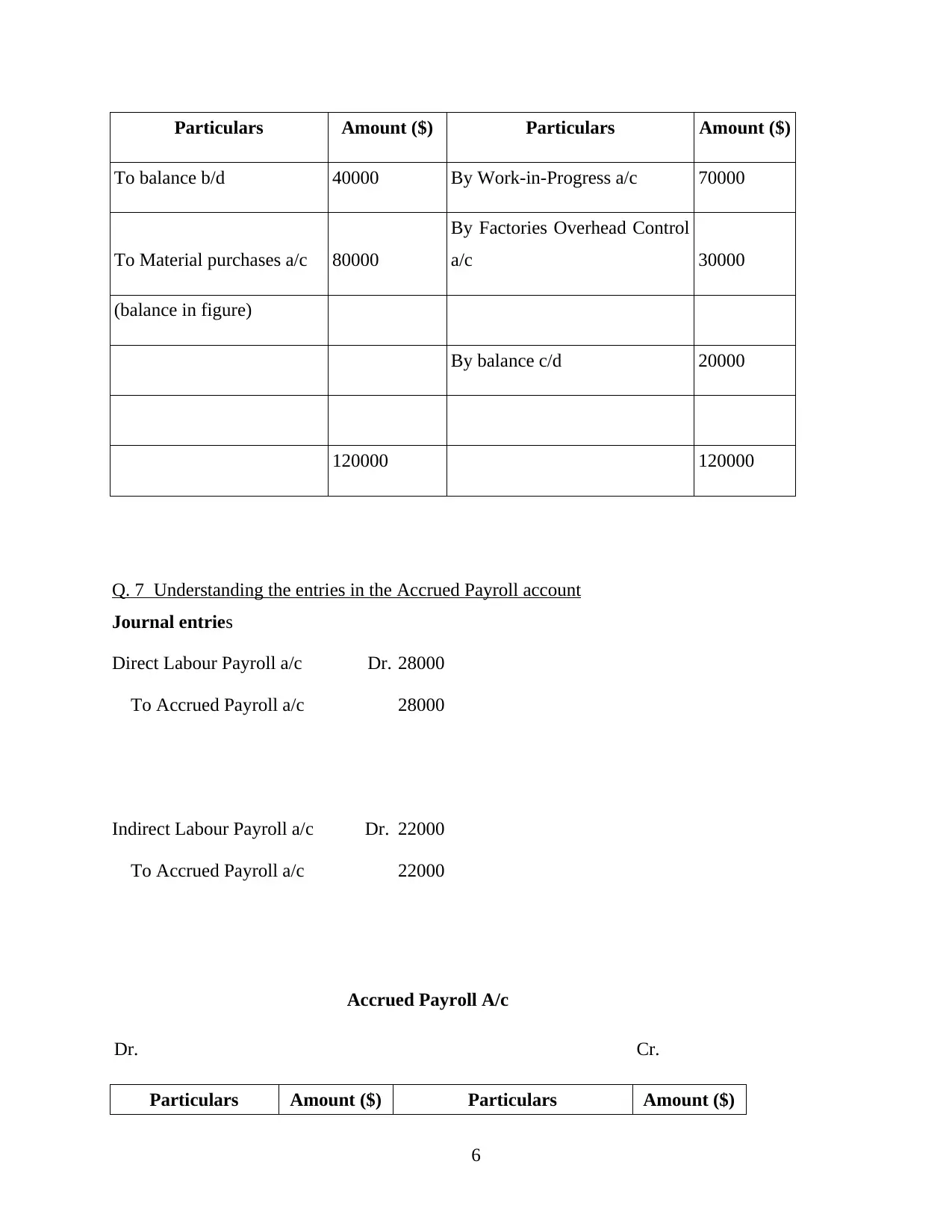

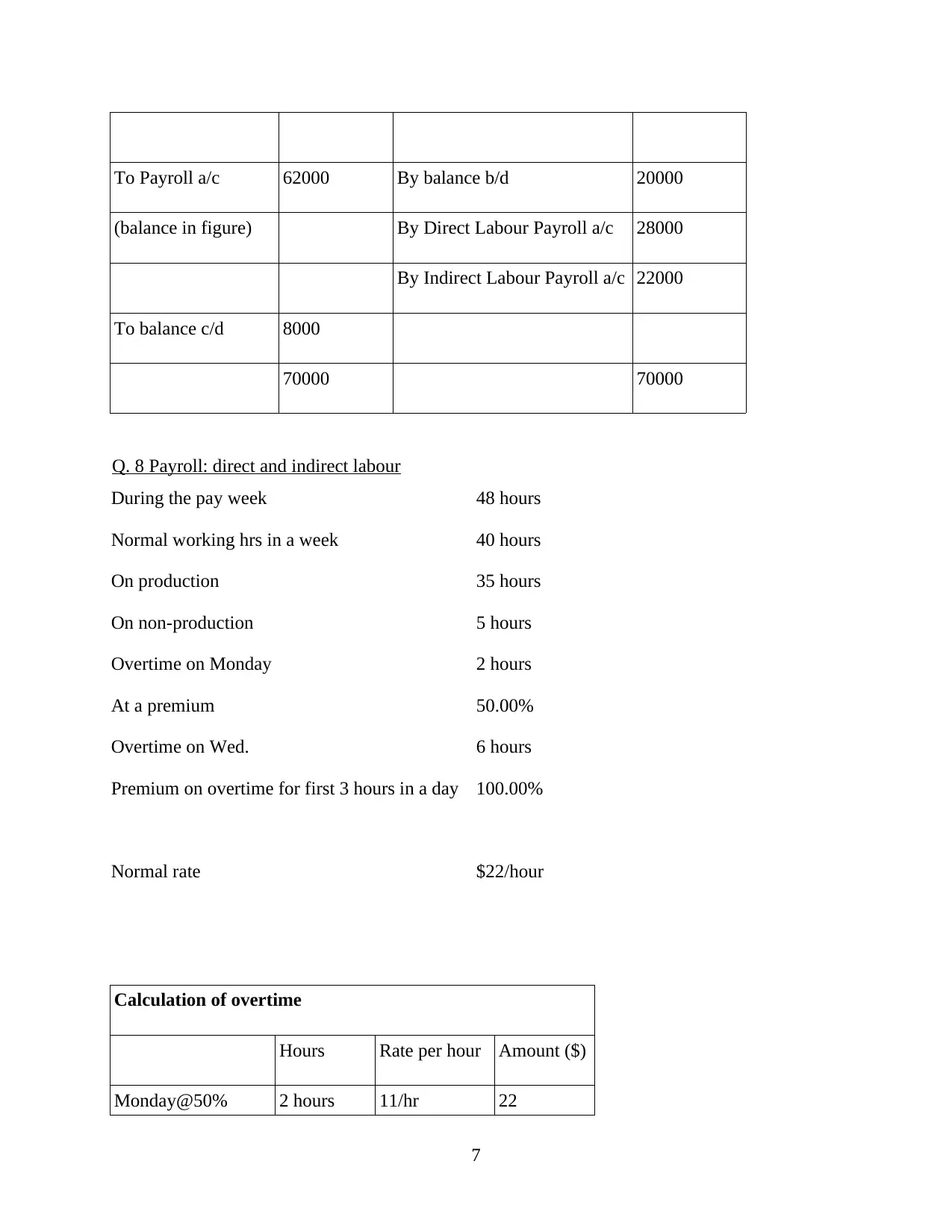

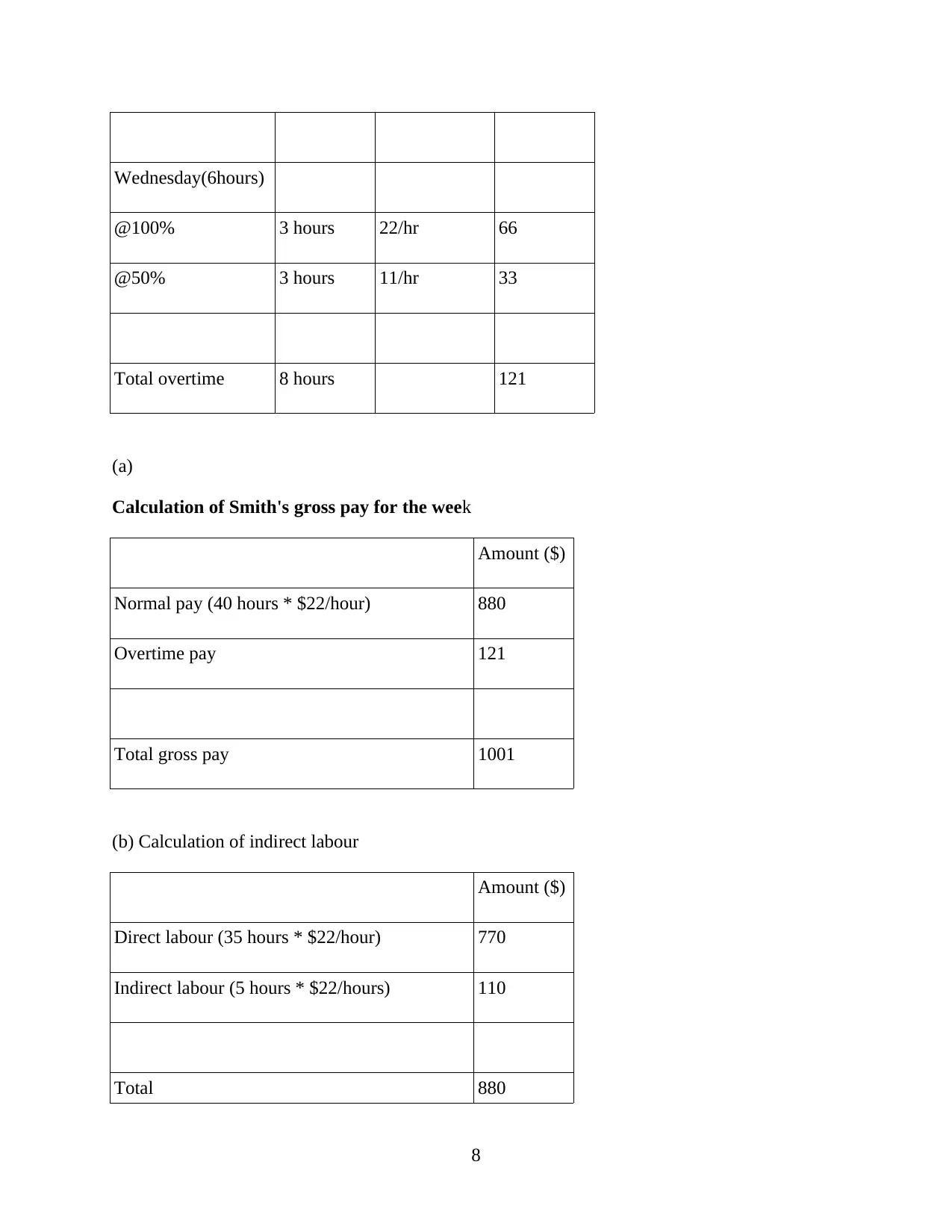

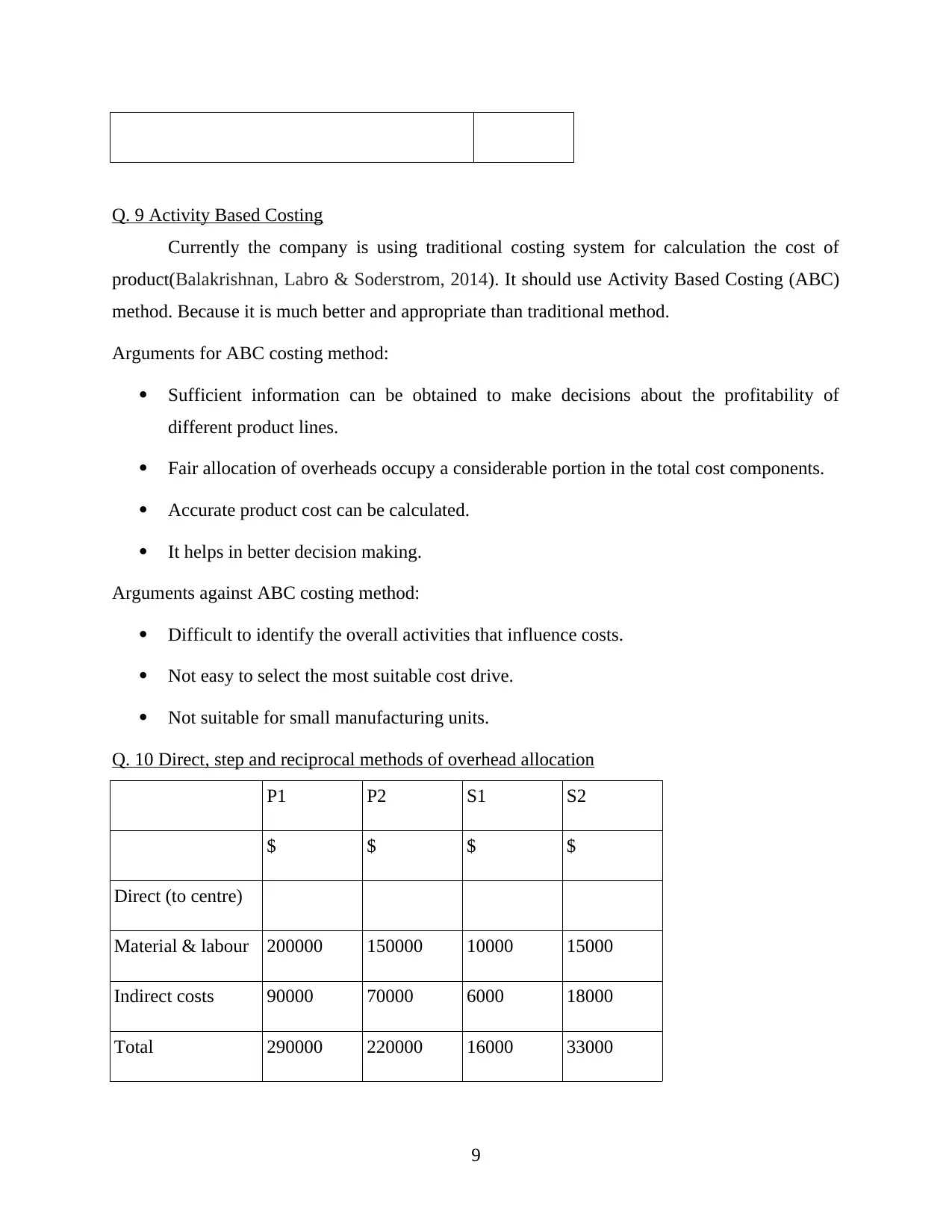

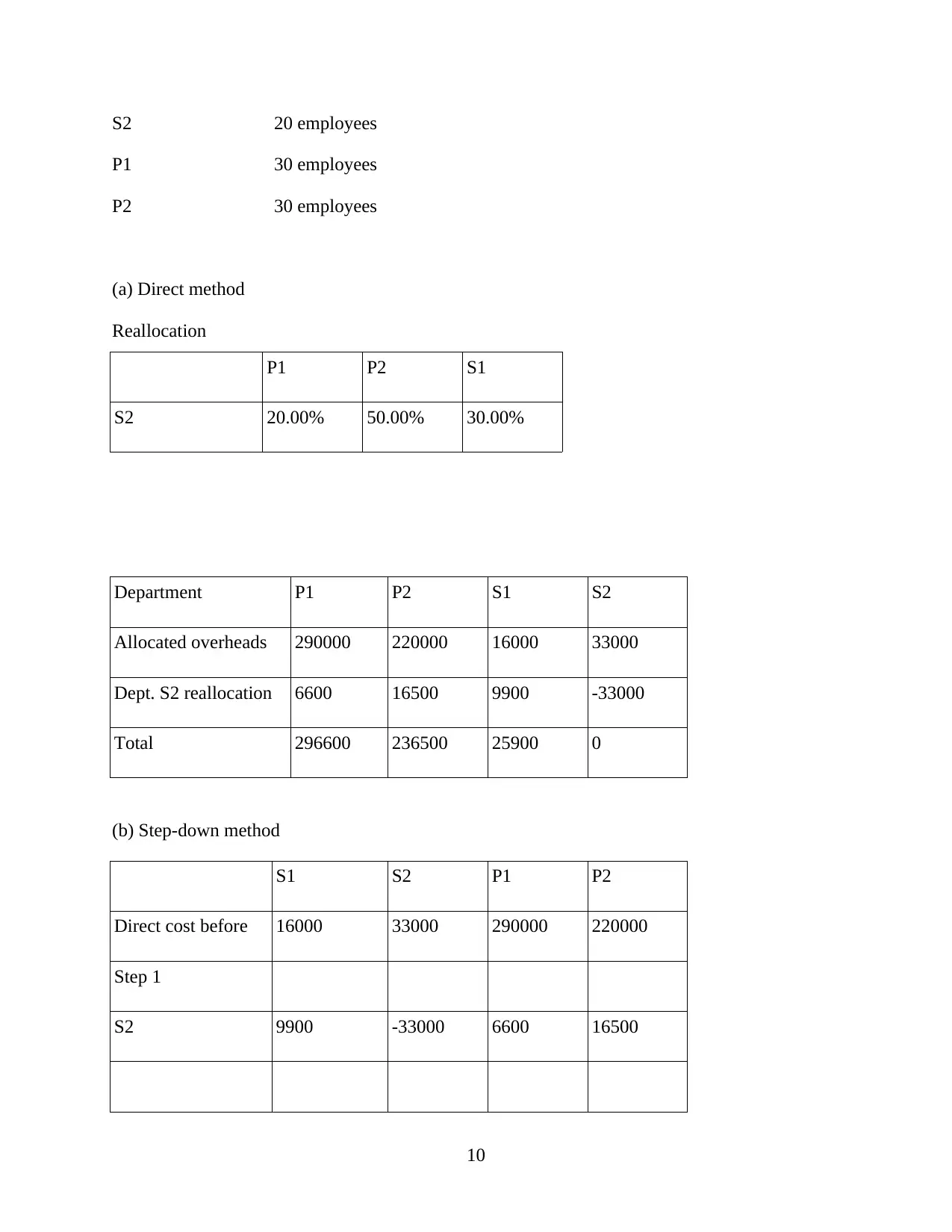

This report delves into the core elements of cost accounting, encompassing materials, labor, and overhead. It explores various costing methods applicable to different product scenarios, including manufacturing and averaging techniques. The report explains key cost concepts like prime cost, product cost, and period cost. It also provides a detailed analysis of manufacturing and income statements, including calculations of inventories. Furthermore, it clarifies the treatment of overtime costs and provides journal entries for material control and accrued payroll accounts. The report analyzes payroll calculations for direct and indirect labor, and evaluates the effectiveness of Activity Based Costing (ABC) compared to traditional costing systems. Finally, it examines different methods of overhead allocation, including direct, step-down, and reciprocal methods, providing a comparative analysis of each approach. The report aims to provide a comprehensive understanding of cost accounting principles and their practical applications.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.