Detailed Analysis of Management Accounting Costing Methods Assignment

VerifiedAdded on 2019/11/25

|6

|868

|143

Homework Assignment

AI Summary

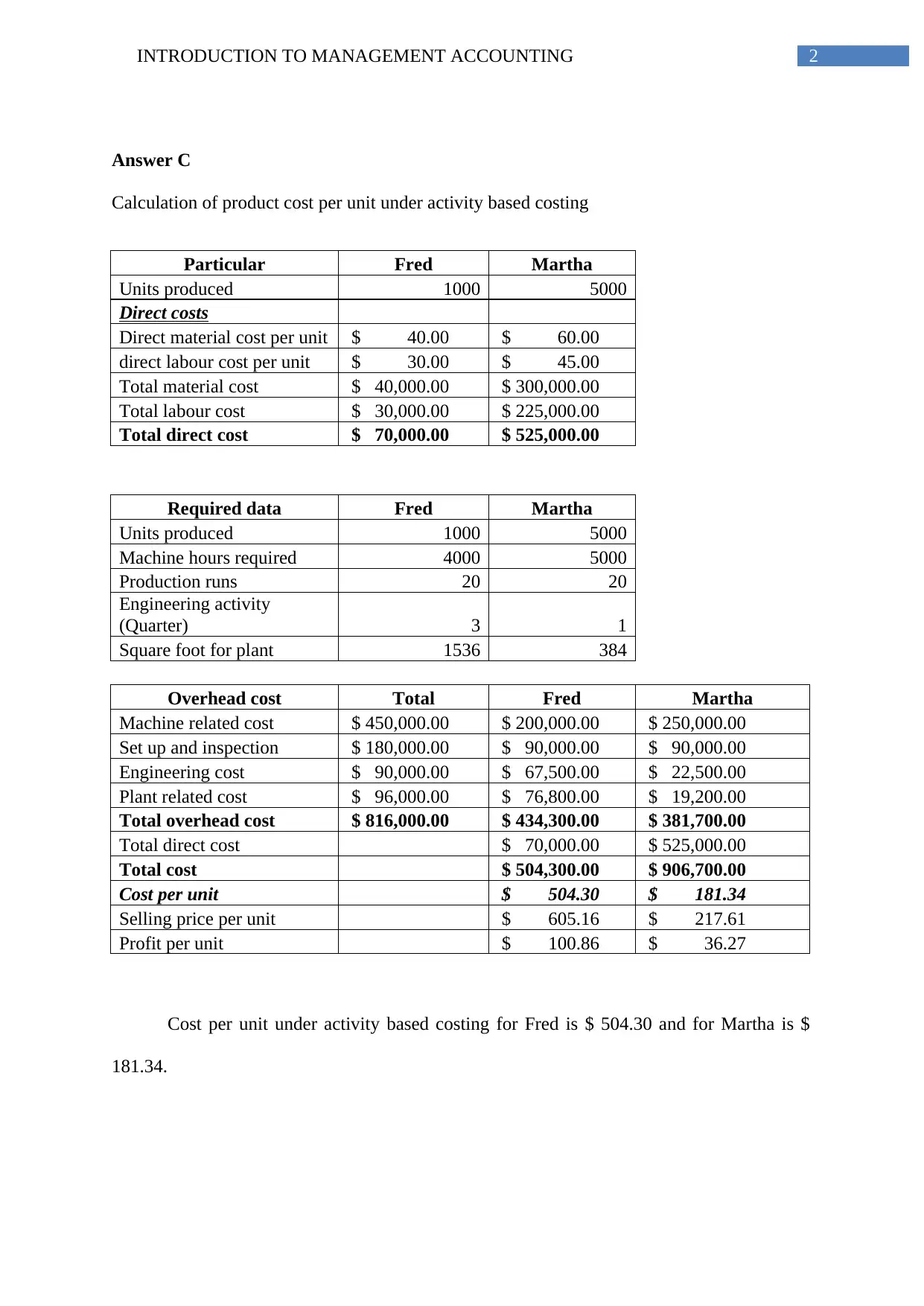

This assignment delves into management accounting, specifically comparing and contrasting activity-based costing (ABC) with traditional costing methods. It includes a detailed calculation of product cost per unit for two products, Fred and Martha, under ABC, demonstrating the allocation of overhead costs based on various activities like machine hours, setup, and engineering. The assignment highlights the mispricing issues that can arise from conventional overhead allocation, which relies on a single cost driver, and presents the advantages of ABC, such as improved business processes, identification of wasteful products, and enhanced cost management. It emphasizes how ABC helps in resource allocation, pricing strategies, and continuous business procedure improvement. The document references academic sources to support its analysis.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.