Management Accounting Report: HLW Club Cost and Revenue Analysis

VerifiedAdded on 2020/06/04

|12

|3066

|30

Report

AI Summary

This report delves into management accounting, focusing on Activity-Based Costing (ABC) and budgeting. Part A explains ABC, its factors, advantages, and disadvantages, followed by a cost analysis using activity drivers for various activities like invoices, purchase orders, and sales orders. A bill of activities and cost per unit for lamington is also provided. Part B examines budgeting, its influence on business decisions, and limitations. It further analyzes a new membership plan and fee structure for HLW club, estimating its impact on cash receipts and sales revenue. The report concludes with an assessment of the new plan's effectiveness in financial planning and management.

MANAGEMENT

ACCOUNTING

Contents

ACCOUNTING

Contents

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

A). Cost per unit of activity driver for listed activity:............................................................3

b). Bill of activities and cost per unit for lamington:.............................................................4

PART B............................................................................................................................................6

A). New membership plan and fee structure enhance its ability to plan its cash receipts:....7

B). Estimate the effect on sales revenue emerging from planned change in the fee structure:7

C). New membership plan and fee structure:.........................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

PART A...........................................................................................................................................1

A). Cost per unit of activity driver for listed activity:............................................................3

b). Bill of activities and cost per unit for lamington:.............................................................4

PART B............................................................................................................................................6

A). New membership plan and fee structure enhance its ability to plan its cash receipts:....7

B). Estimate the effect on sales revenue emerging from planned change in the fee structure:7

C). New membership plan and fee structure:.........................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

Management accounting is the tool which is used for accountable for handling activities of the

firm. they likewise accountable for handling the available finance for escaping liquid funds

deficiency. Under this, the budgetary process is defined in an effective manner, their advantages

and disadvantages are also defined. The second part of this report is related to the pricing

decisions.

PART A

ABC definition:

It is a methodology of assigning indirect costs to services and products involving finding cost of

products based on consumption of every activity. It is a refined approach of costing products

replacing traditional practices it can be also understood as adding indirect cost to direct cost

which results in increasing of indirect cost and unnecessary proliferate of losses (Zimmerman

and Yahya-Zadeh, 2011). This method helps in management for making flexible cost model to

ease out difficulty of differentiation and identification of indirect and direct cost.

objective

ABC estimate overall costing of element of all products, services and activities.

They try to identify and omit unprofitable and overpriced products

Also identify products which are involved in production process.

identify and classify products and place them on cost hierarchy i.e. unit-level, facility

level, production level.

Identifying cost driver for each activity

calculation of unit cost according to type of activity.

Activity rate calculation e.g. activity per unit in relevance to cross drivers

cost hierarchy

Factors of Activity Based Costing:

Estimating time- they mainly emphases on time driven costing activities which helps in

achieving budget in prescribed time and with minimal costing

Cost calculation- through this costing method several input variables can be taken which helps

in formulation easing out in solving complex outcomes.

1

Management accounting is the tool which is used for accountable for handling activities of the

firm. they likewise accountable for handling the available finance for escaping liquid funds

deficiency. Under this, the budgetary process is defined in an effective manner, their advantages

and disadvantages are also defined. The second part of this report is related to the pricing

decisions.

PART A

ABC definition:

It is a methodology of assigning indirect costs to services and products involving finding cost of

products based on consumption of every activity. It is a refined approach of costing products

replacing traditional practices it can be also understood as adding indirect cost to direct cost

which results in increasing of indirect cost and unnecessary proliferate of losses (Zimmerman

and Yahya-Zadeh, 2011). This method helps in management for making flexible cost model to

ease out difficulty of differentiation and identification of indirect and direct cost.

objective

ABC estimate overall costing of element of all products, services and activities.

They try to identify and omit unprofitable and overpriced products

Also identify products which are involved in production process.

identify and classify products and place them on cost hierarchy i.e. unit-level, facility

level, production level.

Identifying cost driver for each activity

calculation of unit cost according to type of activity.

Activity rate calculation e.g. activity per unit in relevance to cross drivers

cost hierarchy

Factors of Activity Based Costing:

Estimating time- they mainly emphases on time driven costing activities which helps in

achieving budget in prescribed time and with minimal costing

Cost calculation- through this costing method several input variables can be taken which helps

in formulation easing out in solving complex outcomes.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Identification of services, products and values- it identifies the value of the product and elements

those which are unprofitable and low in sales.

Financial institution- like effective implementation in manufacturing industry they can also be

implemented in analysing services related to financial sectors where they can be attributed

explicitly.

Lean accounting- it is a time driven activity which eases calculation and planning in accounting

activities

applications

applied in both costing and financing activities

they have practical analysis of surveys in accounting

helps in reducing costs in production and organisational level

neutralising unnecessary production cost

Advantages and disadvantages:

Advantages

they estimate accurate production cost by concentrating on effective relationship in

context of cost occurrence.

They inform about cost behaviour which identifies activities decreasing values of

product.

They trace overhead costs related to process, customers and department.

They enhance better decision making by having adequate analysis of product and fix their

selling prices.

They are helpful in service industry and financial sectors where overhear cost and

indirect cost are very high which hamper growth of organisation.

Limitations

the analysis is very expensive and cannot be afforded by small scale industries.

Input variables are large so it makes it a complex process which is not easy to understand

by everyone

it is very difficult to find the effectiveness of ABC analysis in public sectors like

budgeting practices hence it cannot be trusted to be implemented

it is a time consuming task as it need large sources of data.

2

those which are unprofitable and low in sales.

Financial institution- like effective implementation in manufacturing industry they can also be

implemented in analysing services related to financial sectors where they can be attributed

explicitly.

Lean accounting- it is a time driven activity which eases calculation and planning in accounting

activities

applications

applied in both costing and financing activities

they have practical analysis of surveys in accounting

helps in reducing costs in production and organisational level

neutralising unnecessary production cost

Advantages and disadvantages:

Advantages

they estimate accurate production cost by concentrating on effective relationship in

context of cost occurrence.

They inform about cost behaviour which identifies activities decreasing values of

product.

They trace overhead costs related to process, customers and department.

They enhance better decision making by having adequate analysis of product and fix their

selling prices.

They are helpful in service industry and financial sectors where overhear cost and

indirect cost are very high which hamper growth of organisation.

Limitations

the analysis is very expensive and cannot be afforded by small scale industries.

Input variables are large so it makes it a complex process which is not easy to understand

by everyone

it is very difficult to find the effectiveness of ABC analysis in public sectors like

budgeting practices hence it cannot be trusted to be implemented

it is a time consuming task as it need large sources of data.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

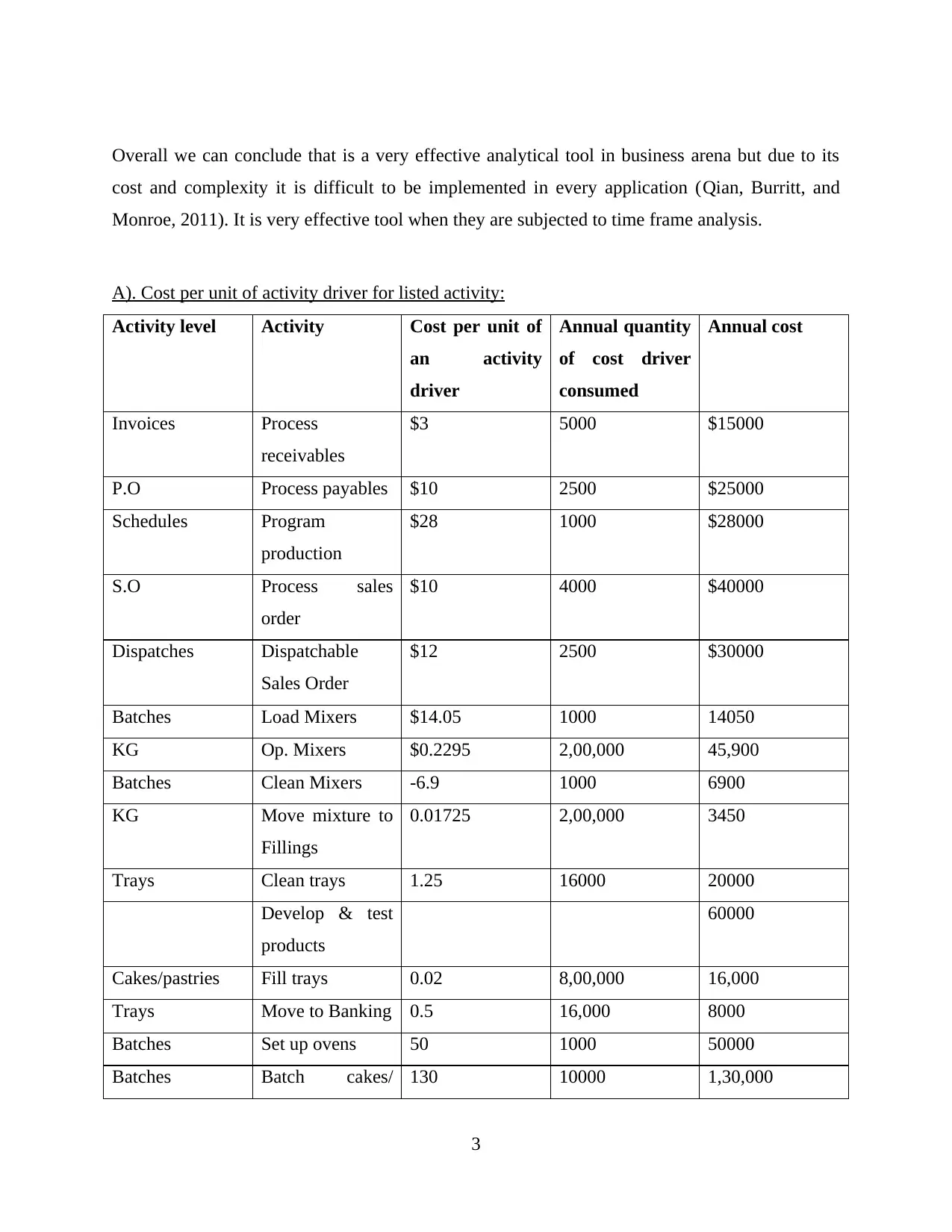

Overall we can conclude that is a very effective analytical tool in business arena but due to its

cost and complexity it is difficult to be implemented in every application (Qian, Burritt, and

Monroe, 2011). It is very effective tool when they are subjected to time frame analysis.

A). Cost per unit of activity driver for listed activity:

Activity level Activity Cost per unit of

an activity

driver

Annual quantity

of cost driver

consumed

Annual cost

Invoices Process

receivables

$3 5000 $15000

P.O Process payables $10 2500 $25000

Schedules Program

production

$28 1000 $28000

S.O Process sales

order

$10 4000 $40000

Dispatches Dispatchable

Sales Order

$12 2500 $30000

Batches Load Mixers $14.05 1000 14050

KG Op. Mixers $0.2295 2,00,000 45,900

Batches Clean Mixers -6.9 1000 6900

KG Move mixture to

Fillings

0.01725 2,00,000 3450

Trays Clean trays 1.25 16000 20000

Develop & test

products

60000

Cakes/pastries Fill trays 0.02 8,00,000 16,000

Trays Move to Banking 0.5 16,000 8000

Batches Set up ovens 50 1000 50000

Batches Batch cakes/ 130 10000 1,30,000

3

cost and complexity it is difficult to be implemented in every application (Qian, Burritt, and

Monroe, 2011). It is very effective tool when they are subjected to time frame analysis.

A). Cost per unit of activity driver for listed activity:

Activity level Activity Cost per unit of

an activity

driver

Annual quantity

of cost driver

consumed

Annual cost

Invoices Process

receivables

$3 5000 $15000

P.O Process payables $10 2500 $25000

Schedules Program

production

$28 1000 $28000

S.O Process sales

order

$10 4000 $40000

Dispatches Dispatchable

Sales Order

$12 2500 $30000

Batches Load Mixers $14.05 1000 14050

KG Op. Mixers $0.2295 2,00,000 45,900

Batches Clean Mixers -6.9 1000 6900

KG Move mixture to

Fillings

0.01725 2,00,000 3450

Trays Clean trays 1.25 16000 20000

Develop & test

products

60000

Cakes/pastries Fill trays 0.02 8,00,000 16,000

Trays Move to Banking 0.5 16,000 8000

Batches Set up ovens 50 1000 50000

Batches Batch cakes/ 130 10000 1,30,000

3

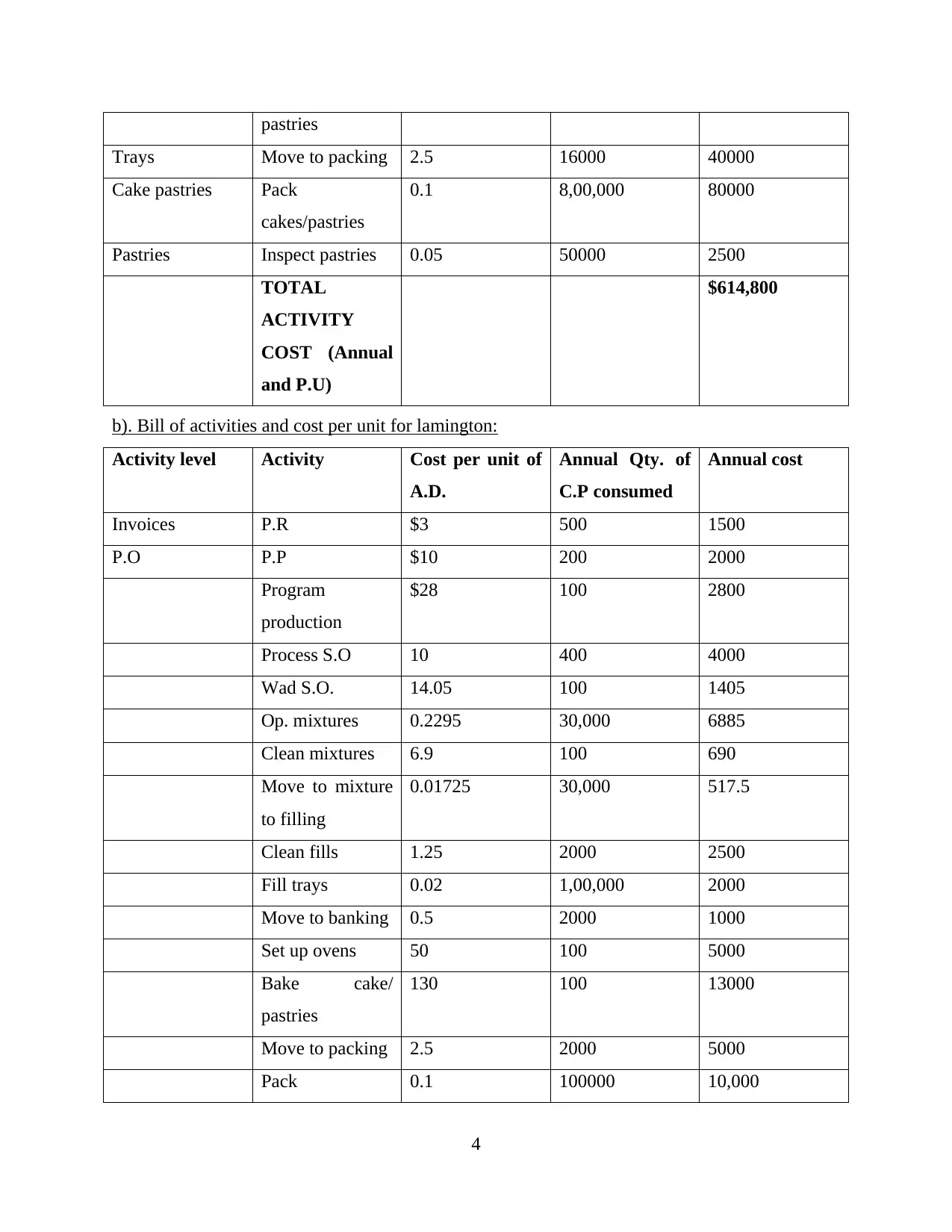

pastries

Trays Move to packing 2.5 16000 40000

Cake pastries Pack

cakes/pastries

0.1 8,00,000 80000

Pastries Inspect pastries 0.05 50000 2500

TOTAL

ACTIVITY

COST (Annual

and P.U)

$614,800

b). Bill of activities and cost per unit for lamington:

Activity level Activity Cost per unit of

A.D.

Annual Qty. of

C.P consumed

Annual cost

Invoices P.R $3 500 1500

P.O P.P $10 200 2000

Program

production

$28 100 2800

Process S.O 10 400 4000

Wad S.O. 14.05 100 1405

Op. mixtures 0.2295 30,000 6885

Clean mixtures 6.9 100 690

Move to mixture

to filling

0.01725 30,000 517.5

Clean fills 1.25 2000 2500

Fill trays 0.02 1,00,000 2000

Move to banking 0.5 2000 1000

Set up ovens 50 100 5000

Bake cake/

pastries

130 100 13000

Move to packing 2.5 2000 5000

Pack 0.1 100000 10,000

4

Trays Move to packing 2.5 16000 40000

Cake pastries Pack

cakes/pastries

0.1 8,00,000 80000

Pastries Inspect pastries 0.05 50000 2500

TOTAL

ACTIVITY

COST (Annual

and P.U)

$614,800

b). Bill of activities and cost per unit for lamington:

Activity level Activity Cost per unit of

A.D.

Annual Qty. of

C.P consumed

Annual cost

Invoices P.R $3 500 1500

P.O P.P $10 200 2000

Program

production

$28 100 2800

Process S.O 10 400 4000

Wad S.O. 14.05 100 1405

Op. mixtures 0.2295 30,000 6885

Clean mixtures 6.9 100 690

Move to mixture

to filling

0.01725 30,000 517.5

Clean fills 1.25 2000 2500

Fill trays 0.02 1,00,000 2000

Move to banking 0.5 2000 1000

Set up ovens 50 100 5000

Bake cake/

pastries

130 100 13000

Move to packing 2.5 2000 5000

Pack 0.1 100000 10,000

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

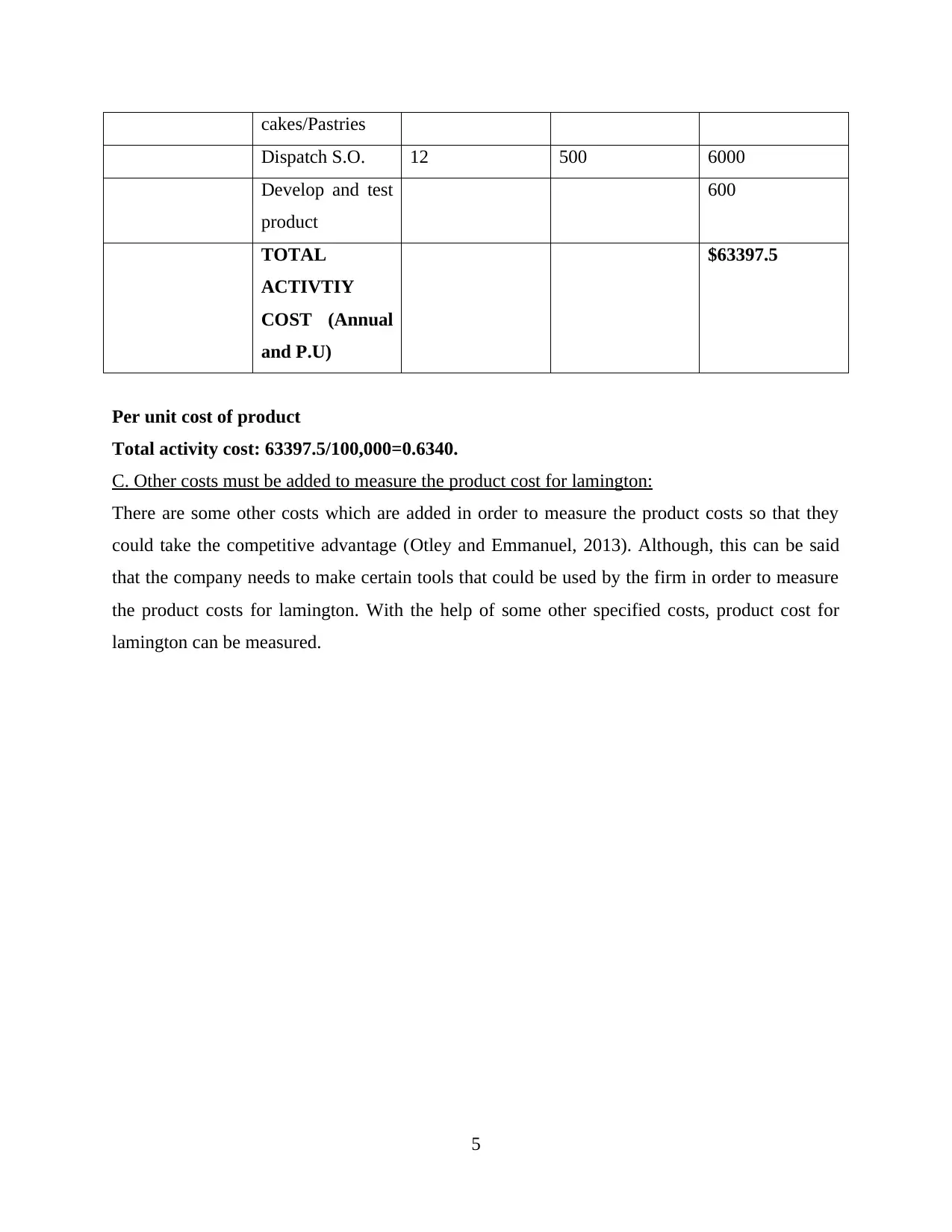

cakes/Pastries

Dispatch S.O. 12 500 6000

Develop and test

product

600

TOTAL

ACTIVTIY

COST (Annual

and P.U)

$63397.5

Per unit cost of product

Total activity cost: 63397.5/100,000=0.6340.

C. Other costs must be added to measure the product cost for lamington:

There are some other costs which are added in order to measure the product costs so that they

could take the competitive advantage (Otley and Emmanuel, 2013). Although, this can be said

that the company needs to make certain tools that could be used by the firm in order to measure

the product costs for lamington. With the help of some other specified costs, product cost for

lamington can be measured.

5

Dispatch S.O. 12 500 6000

Develop and test

product

600

TOTAL

ACTIVTIY

COST (Annual

and P.U)

$63397.5

Per unit cost of product

Total activity cost: 63397.5/100,000=0.6340.

C. Other costs must be added to measure the product cost for lamington:

There are some other costs which are added in order to measure the product costs so that they

could take the competitive advantage (Otley and Emmanuel, 2013). Although, this can be said

that the company needs to make certain tools that could be used by the firm in order to measure

the product costs for lamington. With the help of some other specified costs, product cost for

lamington can be measured.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PART B

Budget: Budget is procedure of planning the finance for a determined time period, often a year.

This is also known microeconomics concepts which present the trade-off made while one

product is exchanged for another. This is an anticipated surplus budget or plan in which expenses

and revenues are expected for managing the functions of business in effective and efficient

manner. The process undertakes proper process in which determination of sales trends, cost

trends and outlook of sector in trade or sector industry (Hoque, 2011). This is the process which

helps in managing entire business expenses in effective way while developing the designed plan.

There are two types of budget i.e. flexible that contain relational values to the determined

variables and other is static budget which remain unaltered or unchanged includes all figures,

accounts and periods which also remain same. Thus, budget is very crucial process which an

organisation requires to undertake while making, developing and implementing a strategy in

order to save the overcasting of the plan and control the optimised activities. This is essential for

an organisation to evaluate the limitation and benefits of this procedure, the company can meet

unexpected outcome (Østergren and Stensaker, 2011).

Budget influence on business decision-making: The quality of the undertaken decision decided

the failure and success of small business. Thus, this is required for a business organisation to

undertake the process of budgeting while making judgements and decision for business. Budget

assist in making rational decision while considering the spending of money in best ways. This

help in developing and adjusting the strategy according to the financial situation of enterprise. It

also guides the company in making balanced decision making to an organisation. For example, if

an organisation’s income renders them the investment of 25, 000$ in marketing, the process of

budgeting aid in removing over-spending from an organisation (Granlund, 2011). This consists

of expansion of plan and purchases the instruments that render growth to a company as well.

Budget- Limitation: As there is always a loophole in a system, so as the process of

budgeting. As the process of budget is highly used in the business weather it is small or large

organisation, there are various limitation and restriction. This is essential to analyse and evaluate

entire limitation of budgeting before making a budget of organisation. This can lead an

organisation in decision-making inflexibility to company and require alternation according to

different circumstances. Also the procedure is very time consuming in especially large

6

Budget: Budget is procedure of planning the finance for a determined time period, often a year.

This is also known microeconomics concepts which present the trade-off made while one

product is exchanged for another. This is an anticipated surplus budget or plan in which expenses

and revenues are expected for managing the functions of business in effective and efficient

manner. The process undertakes proper process in which determination of sales trends, cost

trends and outlook of sector in trade or sector industry (Hoque, 2011). This is the process which

helps in managing entire business expenses in effective way while developing the designed plan.

There are two types of budget i.e. flexible that contain relational values to the determined

variables and other is static budget which remain unaltered or unchanged includes all figures,

accounts and periods which also remain same. Thus, budget is very crucial process which an

organisation requires to undertake while making, developing and implementing a strategy in

order to save the overcasting of the plan and control the optimised activities. This is essential for

an organisation to evaluate the limitation and benefits of this procedure, the company can meet

unexpected outcome (Østergren and Stensaker, 2011).

Budget influence on business decision-making: The quality of the undertaken decision decided

the failure and success of small business. Thus, this is required for a business organisation to

undertake the process of budgeting while making judgements and decision for business. Budget

assist in making rational decision while considering the spending of money in best ways. This

help in developing and adjusting the strategy according to the financial situation of enterprise. It

also guides the company in making balanced decision making to an organisation. For example, if

an organisation’s income renders them the investment of 25, 000$ in marketing, the process of

budgeting aid in removing over-spending from an organisation (Granlund, 2011). This consists

of expansion of plan and purchases the instruments that render growth to a company as well.

Budget- Limitation: As there is always a loophole in a system, so as the process of

budgeting. As the process of budget is highly used in the business weather it is small or large

organisation, there are various limitation and restriction. This is essential to analyse and evaluate

entire limitation of budgeting before making a budget of organisation. This can lead an

organisation in decision-making inflexibility to company and require alternation according to

different circumstances. Also the procedure is very time consuming in especially large

6

businesses that sometimes the entire departments need to be dedicated to budget control and

setting process.

This is a short term judgement process which is not more effective in term of long term

objectives and decision making. Also sometimes, unreasonable and inaccurate assumption can

lead to unrealistic budget and goals which lead to failure and unrealistic goals in the company.

This can lead to behavioural changes to business which requires to proper evaluation of external

and internal environment. Through accurate analysis and reviewing of organisational strengths

and weakness, company can meet the unexpected and effective outcome in the organisation.

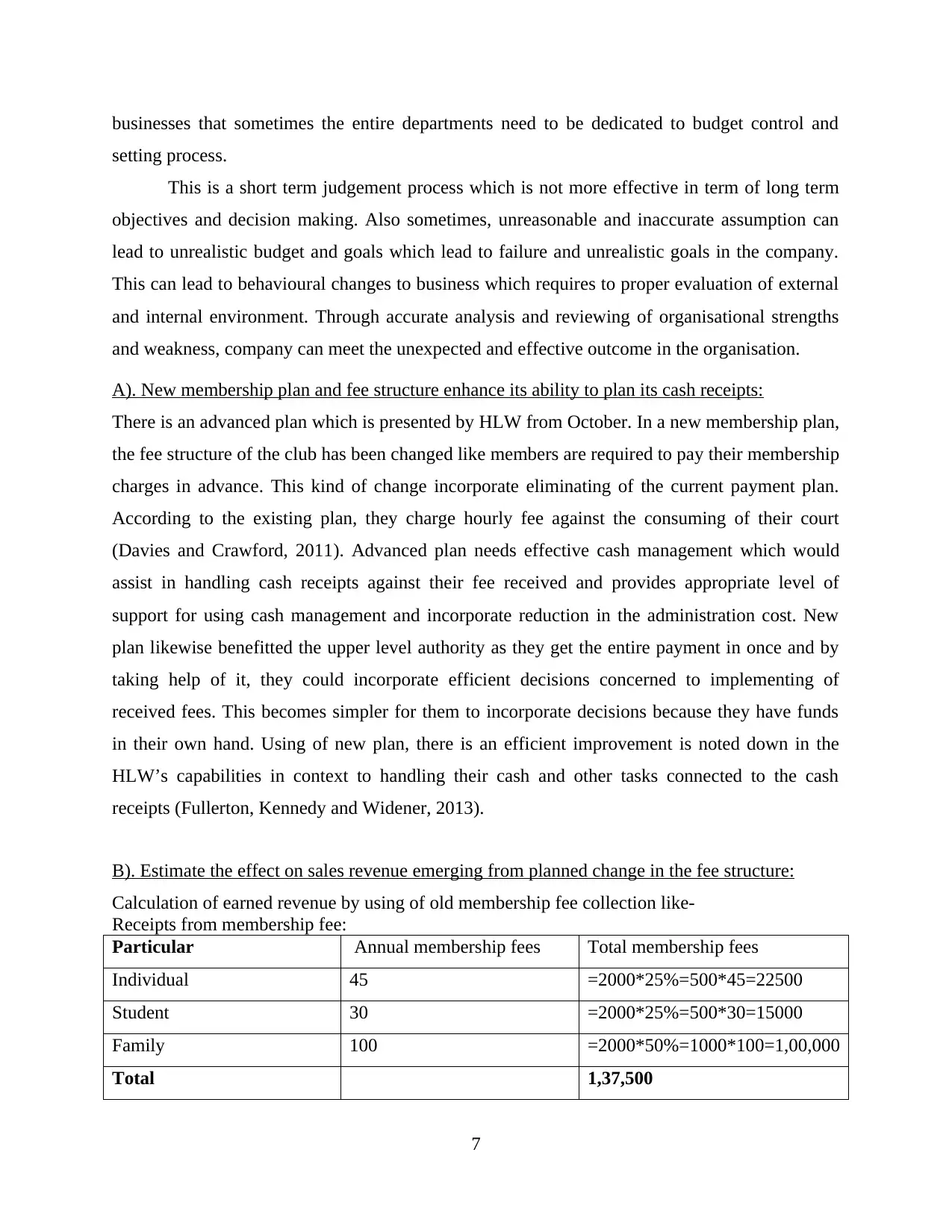

A). New membership plan and fee structure enhance its ability to plan its cash receipts:

There is an advanced plan which is presented by HLW from October. In a new membership plan,

the fee structure of the club has been changed like members are required to pay their membership

charges in advance. This kind of change incorporate eliminating of the current payment plan.

According to the existing plan, they charge hourly fee against the consuming of their court

(Davies and Crawford, 2011). Advanced plan needs effective cash management which would

assist in handling cash receipts against their fee received and provides appropriate level of

support for using cash management and incorporate reduction in the administration cost. New

plan likewise benefitted the upper level authority as they get the entire payment in once and by

taking help of it, they could incorporate efficient decisions concerned to implementing of

received fees. This becomes simpler for them to incorporate decisions because they have funds

in their own hand. Using of new plan, there is an efficient improvement is noted down in the

HLW’s capabilities in context to handling their cash and other tasks connected to the cash

receipts (Fullerton, Kennedy and Widener, 2013).

B). Estimate the effect on sales revenue emerging from planned change in the fee structure:

Calculation of earned revenue by using of old membership fee collection like-

Receipts from membership fee:

Particular Annual membership fees Total membership fees

Individual 45 =2000*25%=500*45=22500

Student 30 =2000*25%=500*30=15000

Family 100 =2000*50%=1000*100=1,00,000

Total 1,37,500

7

setting process.

This is a short term judgement process which is not more effective in term of long term

objectives and decision making. Also sometimes, unreasonable and inaccurate assumption can

lead to unrealistic budget and goals which lead to failure and unrealistic goals in the company.

This can lead to behavioural changes to business which requires to proper evaluation of external

and internal environment. Through accurate analysis and reviewing of organisational strengths

and weakness, company can meet the unexpected and effective outcome in the organisation.

A). New membership plan and fee structure enhance its ability to plan its cash receipts:

There is an advanced plan which is presented by HLW from October. In a new membership plan,

the fee structure of the club has been changed like members are required to pay their membership

charges in advance. This kind of change incorporate eliminating of the current payment plan.

According to the existing plan, they charge hourly fee against the consuming of their court

(Davies and Crawford, 2011). Advanced plan needs effective cash management which would

assist in handling cash receipts against their fee received and provides appropriate level of

support for using cash management and incorporate reduction in the administration cost. New

plan likewise benefitted the upper level authority as they get the entire payment in once and by

taking help of it, they could incorporate efficient decisions concerned to implementing of

received fees. This becomes simpler for them to incorporate decisions because they have funds

in their own hand. Using of new plan, there is an efficient improvement is noted down in the

HLW’s capabilities in context to handling their cash and other tasks connected to the cash

receipts (Fullerton, Kennedy and Widener, 2013).

B). Estimate the effect on sales revenue emerging from planned change in the fee structure:

Calculation of earned revenue by using of old membership fee collection like-

Receipts from membership fee:

Particular Annual membership fees Total membership fees

Individual 45 =2000*25%=500*45=22500

Student 30 =2000*25%=500*30=15000

Family 100 =2000*50%=1000*100=1,00,000

Total 1,37,500

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

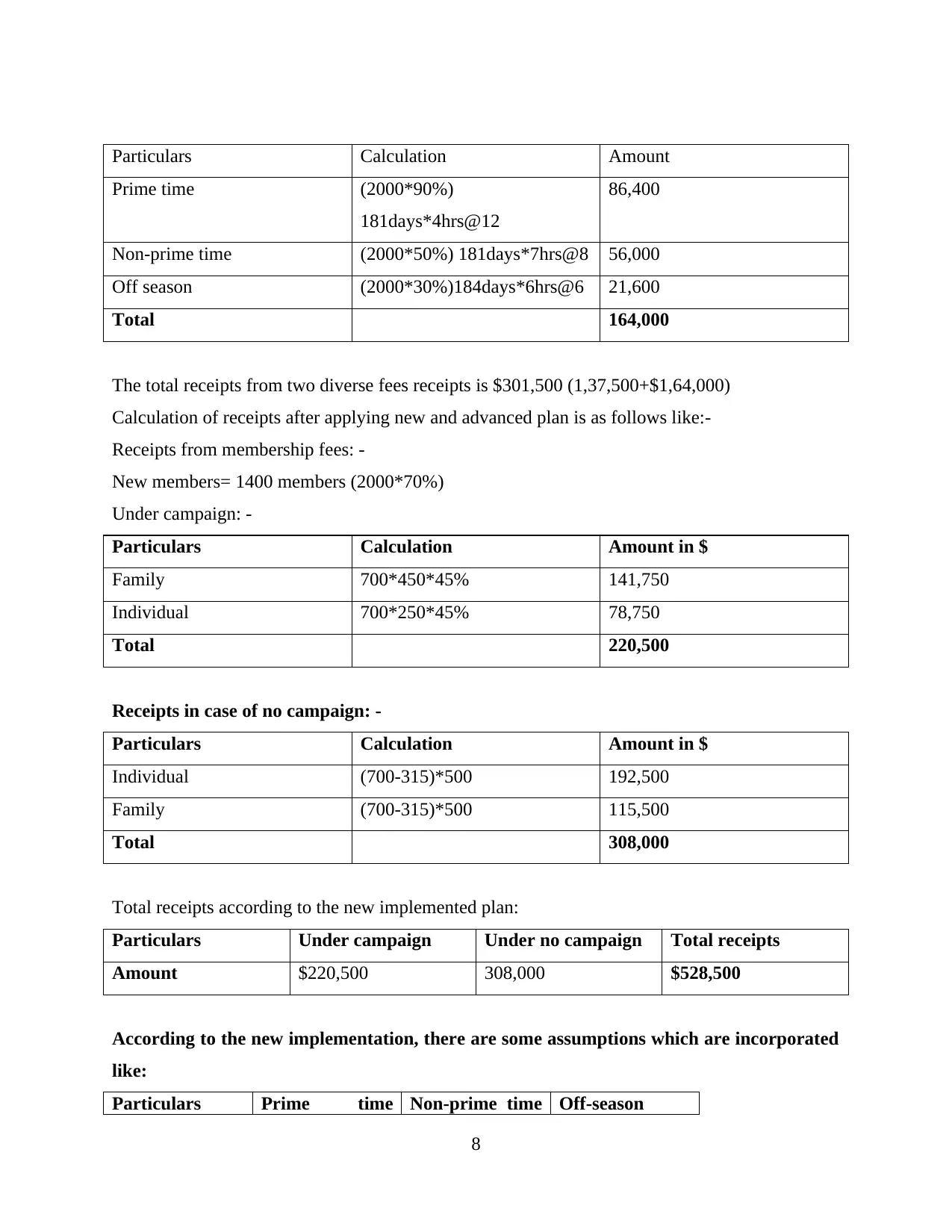

Particulars Calculation Amount

Prime time (2000*90%)

181days*4hrs@12

86,400

Non-prime time (2000*50%) 181days*7hrs@8 56,000

Off season (2000*30%)184days*6hrs@6 21,600

Total 164,000

The total receipts from two diverse fees receipts is $301,500 (1,37,500+$1,64,000)

Calculation of receipts after applying new and advanced plan is as follows like:-

Receipts from membership fees: -

New members= 1400 members (2000*70%)

Under campaign: -

Particulars Calculation Amount in $

Family 700*450*45% 141,750

Individual 700*250*45% 78,750

Total 220,500

Receipts in case of no campaign: -

Particulars Calculation Amount in $

Individual (700-315)*500 192,500

Family (700-315)*500 115,500

Total 308,000

Total receipts according to the new implemented plan:

Particulars Under campaign Under no campaign Total receipts

Amount $220,500 308,000 $528,500

According to the new implementation, there are some assumptions which are incorporated

like:

Particulars Prime time Non-prime time Off-season

8

Prime time (2000*90%)

181days*4hrs@12

86,400

Non-prime time (2000*50%) 181days*7hrs@8 56,000

Off season (2000*30%)184days*6hrs@6 21,600

Total 164,000

The total receipts from two diverse fees receipts is $301,500 (1,37,500+$1,64,000)

Calculation of receipts after applying new and advanced plan is as follows like:-

Receipts from membership fees: -

New members= 1400 members (2000*70%)

Under campaign: -

Particulars Calculation Amount in $

Family 700*450*45% 141,750

Individual 700*250*45% 78,750

Total 220,500

Receipts in case of no campaign: -

Particulars Calculation Amount in $

Individual (700-315)*500 192,500

Family (700-315)*500 115,500

Total 308,000

Total receipts according to the new implemented plan:

Particulars Under campaign Under no campaign Total receipts

Amount $220,500 308,000 $528,500

According to the new implementation, there are some assumptions which are incorporated

like:

Particulars Prime time Non-prime time Off-season

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

occupancy occupancy occupancy

Percentage 90% 50% 30%

Changes in the new membership plan or advanced fee collection plan put efficient impact over

their processing as this emergence into enhance in the revenue as this reflects incremental value

as $227,000.

C). New membership plan and fee structure:

HLW management determines cost reduction in the administration after using advanced

membership plan as after it they are required to form regular record connected to the revenue

gathering against the implementing of the court, etc. by their members. At the time of applying

new plan, management faces problems in getting advanced fee payments from their members

against their membership. The onetime advance payment affects harmfully as there is a fall down

in the total number of members. There are so many advantages which are likewise provided by

new membership plan because this present free services for their members.

For making the entire evaluation of their new membership plan, they are required to form

financial analysis like:

For analysing the liquid funds management, there is a strong need to calculate the liquidity ratio

because, assists in forming optimum using of liquid funds (Ahmad-Zaluki, Campbell and

Goodacre, 2011). They likewise form cash flow statement which assist in handling and

controlling their available liquid funds. They require an adequate balance between their cash

flows. They likewise form cash budgets for forecasting cash flows.

HLW management likewise form flexible budget which assist in achieving set desired

outcomes and by following these budgets operational level gets efficient support.

CONCLUSION

From the above mentioned report, this can be observed that the activity based costing is used

in order to calculated the per unit cost and the total cost in an effective manner. Apart from this,

budget is also defined under this project and made certain conclusion on the basis of such

conclusion.

9

Percentage 90% 50% 30%

Changes in the new membership plan or advanced fee collection plan put efficient impact over

their processing as this emergence into enhance in the revenue as this reflects incremental value

as $227,000.

C). New membership plan and fee structure:

HLW management determines cost reduction in the administration after using advanced

membership plan as after it they are required to form regular record connected to the revenue

gathering against the implementing of the court, etc. by their members. At the time of applying

new plan, management faces problems in getting advanced fee payments from their members

against their membership. The onetime advance payment affects harmfully as there is a fall down

in the total number of members. There are so many advantages which are likewise provided by

new membership plan because this present free services for their members.

For making the entire evaluation of their new membership plan, they are required to form

financial analysis like:

For analysing the liquid funds management, there is a strong need to calculate the liquidity ratio

because, assists in forming optimum using of liquid funds (Ahmad-Zaluki, Campbell and

Goodacre, 2011). They likewise form cash flow statement which assist in handling and

controlling their available liquid funds. They require an adequate balance between their cash

flows. They likewise form cash budgets for forecasting cash flows.

HLW management likewise form flexible budget which assist in achieving set desired

outcomes and by following these budgets operational level gets efficient support.

CONCLUSION

From the above mentioned report, this can be observed that the activity based costing is used

in order to calculated the per unit cost and the total cost in an effective manner. Apart from this,

budget is also defined under this project and made certain conclusion on the basis of such

conclusion.

9

REFERENCES

Books and Journals:

Ahmad-Zaluki, N.A., Campbell, K. and Goodacre, A., 2011. Earnings management in Malaysian

IPOs: The East Asian crisis, ownership control, and post-IPO performance. The

International Journal of Accounting. 46(2). pp.111-137.

Davies, T. and Crawford, I., 2011. Business accounting and finance. Pearson.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2013. Management accounting and control

practices in a lean manufacturing environment. Accounting, Organizations and Society.

38(1). pp.50-71.

Granlund, M., 2011. Extending AIS research to management accounting and control issues: A

research note. International Journal of Accounting Information Systems. 12(1). pp.3-19.

Hoque, Z., 2011. The relations among competition, delegation, management accounting systems

change and performance: A path model. Advances in Accounting. 27(2). pp.266-277.

Østergren, K. and Stensaker, I., 2011. Management control without budgets: a field study of

‘beyond budgeting’in practice. European Accounting Review. 20(1). pp.149-181.

Otley, D. and Emmanuel, K.M.C., 2013. Readings in accounting for management control.

Springer.

Qian, W., Burritt, R. and Monroe, G., 2011. Environmental management accounting in local

government: A case of waste management. Accounting, Auditing & Accountability

Journal. 24(1). pp.93-128.

Zimmerman, J.L. and Yahya-Zadeh, M., 2011. Accounting for decision making and control.

Issues in Accounting Education. 26(1). pp.258-259.

Online

Management Accounting 2017 [Online]. Available Through: <https://www.imanet.org/insights-

and-trends/management-accounting-quarterly?ssopc=1>.

10

Books and Journals:

Ahmad-Zaluki, N.A., Campbell, K. and Goodacre, A., 2011. Earnings management in Malaysian

IPOs: The East Asian crisis, ownership control, and post-IPO performance. The

International Journal of Accounting. 46(2). pp.111-137.

Davies, T. and Crawford, I., 2011. Business accounting and finance. Pearson.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2013. Management accounting and control

practices in a lean manufacturing environment. Accounting, Organizations and Society.

38(1). pp.50-71.

Granlund, M., 2011. Extending AIS research to management accounting and control issues: A

research note. International Journal of Accounting Information Systems. 12(1). pp.3-19.

Hoque, Z., 2011. The relations among competition, delegation, management accounting systems

change and performance: A path model. Advances in Accounting. 27(2). pp.266-277.

Østergren, K. and Stensaker, I., 2011. Management control without budgets: a field study of

‘beyond budgeting’in practice. European Accounting Review. 20(1). pp.149-181.

Otley, D. and Emmanuel, K.M.C., 2013. Readings in accounting for management control.

Springer.

Qian, W., Burritt, R. and Monroe, G., 2011. Environmental management accounting in local

government: A case of waste management. Accounting, Auditing & Accountability

Journal. 24(1). pp.93-128.

Zimmerman, J.L. and Yahya-Zadeh, M., 2011. Accounting for decision making and control.

Issues in Accounting Education. 26(1). pp.258-259.

Online

Management Accounting 2017 [Online]. Available Through: <https://www.imanet.org/insights-

and-trends/management-accounting-quarterly?ssopc=1>.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.