Management Accounting Report: Analysis of Costing and Planning Methods

VerifiedAdded on 2020/02/03

|17

|6252

|164

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles, focusing on their application within the context of Agmet, a chemical product manufacturer. The report begins with an introduction to the core concepts of management accounting, emphasizing its role in providing financial data and advisory support to businesses. It then delves into various management accounting systems, including cost accounting, inventory management, and job creation systems, as well as different reporting methods such as budget reports and cash flow analysis. The report examines the calculation of costs using both absorption costing and marginal costing, and it explores the advantages and disadvantages of different planning tools. Finally, the report concludes with a comparative analysis of adapting management accounting systems, offering insights into the practical implications of these concepts for Agmet's operations and decision-making processes. The report also includes supporting evidence and analysis from various sources, ensuring a well-rounded understanding of the subject matter.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................4

P1 Concept of management accounting system..........................................................................4

P2 Different methods used for management accounting reporting.............................................5

M1 ..............................................................................................................................................6

D1................................................................................................................................................7

TASK 2............................................................................................................................................7

P3 Calculation of cost by using absorption costing and marginal costing..................................7

M2.............................................................................................................................................10

D2..............................................................................................................................................11

TASK 3..........................................................................................................................................11

P4 Advantages and disadvantages of different planning tools..................................................11

M3.............................................................................................................................................12

D3..............................................................................................................................................13

P5 Comparison on adapting management accounting system..................................................13

M4.............................................................................................................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................4

P1 Concept of management accounting system..........................................................................4

P2 Different methods used for management accounting reporting.............................................5

M1 ..............................................................................................................................................6

D1................................................................................................................................................7

TASK 2............................................................................................................................................7

P3 Calculation of cost by using absorption costing and marginal costing..................................7

M2.............................................................................................................................................10

D2..............................................................................................................................................11

TASK 3..........................................................................................................................................11

P4 Advantages and disadvantages of different planning tools..................................................11

M3.............................................................................................................................................12

D3..............................................................................................................................................13

P5 Comparison on adapting management accounting system..................................................13

M4.............................................................................................................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting having the provision of the financial data and also provide the

advice as well as suggestions to a company so that they can use in the business entity. Moreover,

it helps in developing its business. In the corporation, employees have to use management

accounting system which assist in collecting, analysing and reporting the information which are

related to the operational activities and the finances of the business (Baldvinsdottir, Mitchell and

Nørreklit, 2010). These reports are related with the managers rather than external entities like

shareholders as well as lenders. Management accounting provides the economic information

which is to be used by the companies in making the appropriate decisions. When staff members

of enterprise have to make correct and relevant decision then they have to devise plans which aid

in improving the performance in the market place. The present report is focused on Agmet which

is a manufacturer of chemical products. In the below mentioned study, concept of management

accounting system and different type of system which are related to management accounting

(marginal cost, 2017). Along with this different methods which can be used for management

accounting reporting has to be discussed. Moreover, advantages and disadvantages of the

planning tools which is used for budgetary control has to be discussed.

TASK 1

P1 Concept of management accounting system

Management accounting system is a profession which assist in involving the partnering in

the management which helps in making the correct decisions. Along with this they have to

devise the planning as well as performance management system so that experts can provide the

proper and appropriate report so that managers of Agmet can control the formulation of the plans

so that they can not face any problems as well as attain the goals and objectives. Management

accounting system helps in making the work flows along with the processes so that they become

more efficient and effective (Bennett, Schaltegger and Zvezdov, 2013). For providing the best

and qualitative services, the workers of Agmet have to use appropriate information and data and

according to that they can meet the standards and goals and objectives. When company using

management accounting system internally than they have to centralize lots of data. After that

they have to organise the information and data and then the staff members have to create the

structure which aid in providing best services. Along with this employees of Agmet have to use

Management accounting having the provision of the financial data and also provide the

advice as well as suggestions to a company so that they can use in the business entity. Moreover,

it helps in developing its business. In the corporation, employees have to use management

accounting system which assist in collecting, analysing and reporting the information which are

related to the operational activities and the finances of the business (Baldvinsdottir, Mitchell and

Nørreklit, 2010). These reports are related with the managers rather than external entities like

shareholders as well as lenders. Management accounting provides the economic information

which is to be used by the companies in making the appropriate decisions. When staff members

of enterprise have to make correct and relevant decision then they have to devise plans which aid

in improving the performance in the market place. The present report is focused on Agmet which

is a manufacturer of chemical products. In the below mentioned study, concept of management

accounting system and different type of system which are related to management accounting

(marginal cost, 2017). Along with this different methods which can be used for management

accounting reporting has to be discussed. Moreover, advantages and disadvantages of the

planning tools which is used for budgetary control has to be discussed.

TASK 1

P1 Concept of management accounting system

Management accounting system is a profession which assist in involving the partnering in

the management which helps in making the correct decisions. Along with this they have to

devise the planning as well as performance management system so that experts can provide the

proper and appropriate report so that managers of Agmet can control the formulation of the plans

so that they can not face any problems as well as attain the goals and objectives. Management

accounting system helps in making the work flows along with the processes so that they become

more efficient and effective (Bennett, Schaltegger and Zvezdov, 2013). For providing the best

and qualitative services, the workers of Agmet have to use appropriate information and data and

according to that they can meet the standards and goals and objectives. When company using

management accounting system internally than they have to centralize lots of data. After that

they have to organise the information and data and then the staff members have to create the

structure which aid in providing best services. Along with this employees of Agmet have to use

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

appropriate business models so that all the work and operational activities can managed.

Different type of management accounting system are:

Cost accounting system: This system helps in analysing the profit so that employees of

Agmet can do the valuation of inventory so that manager of the company can control the cost of

their products. It assist in recording, summarizing, clarifying the course of action and also

provide the detailed information so that they can make proper operational planning so that they

can success in future (Busco and Scapens, 2011).

Inventory management system: This system is very much important and necessary for

the company as it helps in managing the inventory of Agmet. In this they have to use the

different software which includes barcode scanner, mobile device etc. which assist in managing

the stock which is provided by suppliers. Along with this it provides support in making the

decisions related to inventory.

There are several type and they have their own benefits along with the functions of these

system and they involve the distinctive things that is to create purchase order, workflow of the

business entity to be improved as well as accuracy in calculating the inventory of Agmet (Christ

and Burritt, 2013).

Job creation system: This system helps in attaining the actual information related to the

cost of the product. In this system different factors which are included that is direct material,

labour as well as overhead cost and these factors aid in improving the cost creation system.

Pricing optimizing: This system helps Agmet in analysing or evaluating the information

programs which are in mathematical or practical form which succour in calculating the different

price level of the product so that they can increase the profit of the company. Along with this it

also aid in assessing the value of merchandise in which Agmet doing the transactions as well as

manage all the profitability which having a influence to measuring pricing strategies (Cinquini

and Tenucci, 2010).

P2 Different methods used for management accounting reporting

Management accounting reports are to be prepared by every entrepreneur in every

enterprise as it helps in evaluating the performance of Agmet in the market. These reports can be

made quarterly, monthly, yearly as well as daily basis. There are different type of management

accounting reports which can be used by Agmet:

Different type of management accounting system are:

Cost accounting system: This system helps in analysing the profit so that employees of

Agmet can do the valuation of inventory so that manager of the company can control the cost of

their products. It assist in recording, summarizing, clarifying the course of action and also

provide the detailed information so that they can make proper operational planning so that they

can success in future (Busco and Scapens, 2011).

Inventory management system: This system is very much important and necessary for

the company as it helps in managing the inventory of Agmet. In this they have to use the

different software which includes barcode scanner, mobile device etc. which assist in managing

the stock which is provided by suppliers. Along with this it provides support in making the

decisions related to inventory.

There are several type and they have their own benefits along with the functions of these

system and they involve the distinctive things that is to create purchase order, workflow of the

business entity to be improved as well as accuracy in calculating the inventory of Agmet (Christ

and Burritt, 2013).

Job creation system: This system helps in attaining the actual information related to the

cost of the product. In this system different factors which are included that is direct material,

labour as well as overhead cost and these factors aid in improving the cost creation system.

Pricing optimizing: This system helps Agmet in analysing or evaluating the information

programs which are in mathematical or practical form which succour in calculating the different

price level of the product so that they can increase the profit of the company. Along with this it

also aid in assessing the value of merchandise in which Agmet doing the transactions as well as

manage all the profitability which having a influence to measuring pricing strategies (Cinquini

and Tenucci, 2010).

P2 Different methods used for management accounting reporting

Management accounting reports are to be prepared by every entrepreneur in every

enterprise as it helps in evaluating the performance of Agmet in the market. These reports can be

made quarterly, monthly, yearly as well as daily basis. There are different type of management

accounting reports which can be used by Agmet:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Budget report: In every business, budgets has to be prepared whether it is small business or large

company as it assist in evaluating the performance of business entity in the market. The owner of

Agmet have to analyse or evaluate the budget so that they can minimise the cost of the products

and services. If budget is large then the manager of the firm have to divide that into different

departments which helps in reducing or managing the cost (Contrafatto and Burns, 2013). Along

with this, in the budget some incentives are to be added which is given by the higher authorities

of Agmet to employees. Budget includes all the incomes as well as expenses and by that workers

can find that where they have to spend and also how much amount spent in the distinctive

activities.

Cash flow analysis: This analysis helps in analysing the the cash inflow as well as outflow of the

business entity during a specified period of time. This analysing begins with a starting balance of

cash and generate or earn the ending balance after doing the accounting for all cash receipts as

well as paid expenses during the given period of time (What is Budgetary control?, 2017). It is

used for the reporting purposes. Cash is important for the company to do different business

activities as they have to make the payments for the distinctive purchases to run the business

which includes the expenses like stock or raw material, employees as well as other operating

expenses. When company make positive cash flow means that the business of Agmet is running

smoothly. For example, account receivable helps in managing the cash flow activity from its

debtors so that they can not face any problem and attain the goals and objectives (Dillard and

Roslender, 2011).

Job cost reports: This report is prepared by the staff members of Agmet so that they can

evaluate or analyse the profitability as well as how much profit they are generating by this job. It

aid in focusing on the jobs rather than the time which is wasting on this job and by that they are

generating low profit. Along with this it succour the business organisation in identifying the

areas in which they can earn high and also have to assess the expenses before the project of the

company started and by this manager can reduce the wastage of the projects or the different

activities of Agmet (Fullerton, Kennedy and Widener, 2014). Further, it assists in analysing the

performance of the company in the market place when they are facing high competition.

Inventory and manufacturing: The employees of the business entity have to use inventory

and manufacturing accounting reports so that they can reduce the cost which is related to the

storage of stock such as wastage of inventory, overhead cost as well as labour cost as these are

company as it assist in evaluating the performance of business entity in the market. The owner of

Agmet have to analyse or evaluate the budget so that they can minimise the cost of the products

and services. If budget is large then the manager of the firm have to divide that into different

departments which helps in reducing or managing the cost (Contrafatto and Burns, 2013). Along

with this, in the budget some incentives are to be added which is given by the higher authorities

of Agmet to employees. Budget includes all the incomes as well as expenses and by that workers

can find that where they have to spend and also how much amount spent in the distinctive

activities.

Cash flow analysis: This analysis helps in analysing the the cash inflow as well as outflow of the

business entity during a specified period of time. This analysing begins with a starting balance of

cash and generate or earn the ending balance after doing the accounting for all cash receipts as

well as paid expenses during the given period of time (What is Budgetary control?, 2017). It is

used for the reporting purposes. Cash is important for the company to do different business

activities as they have to make the payments for the distinctive purchases to run the business

which includes the expenses like stock or raw material, employees as well as other operating

expenses. When company make positive cash flow means that the business of Agmet is running

smoothly. For example, account receivable helps in managing the cash flow activity from its

debtors so that they can not face any problem and attain the goals and objectives (Dillard and

Roslender, 2011).

Job cost reports: This report is prepared by the staff members of Agmet so that they can

evaluate or analyse the profitability as well as how much profit they are generating by this job. It

aid in focusing on the jobs rather than the time which is wasting on this job and by that they are

generating low profit. Along with this it succour the business organisation in identifying the

areas in which they can earn high and also have to assess the expenses before the project of the

company started and by this manager can reduce the wastage of the projects or the different

activities of Agmet (Fullerton, Kennedy and Widener, 2014). Further, it assists in analysing the

performance of the company in the market place when they are facing high competition.

Inventory and manufacturing: The employees of the business entity have to use inventory

and manufacturing accounting reports so that they can reduce the cost which is related to the

storage of stock such as wastage of inventory, overhead cost as well as labour cost as these are

related to that. This aid the managers of Agmet in reducing the cost of the merchandise

(Håkansson, Kraus and Lind, 2010).

M1

The employees of Agmet can use the different methods for the management accounting

system which assist in managing all the business activities and reduce the cost of the products

which are providing to the service users. Different methods includes the financial planning, fund

flow analysis, decision making accounting. Along with this they can use management reporting

as it helps in preparing the specific accounting report of the distinct contents that is balance sheet

as well as profit and loss statement (Herbert and Seal, 2012). The staff members can use ratio

analysis, cost accounting as well as marginal costing which helps them in attaining the goals and

objectives. Different type of management accounting system that can be used by Agmet and they

are discussed above as it aid in reaping the benefits of the competitive advantage and by that

staff members can improve the process which is related to the cost allocation by using the

distinctive management functions. The use of management accounting system aid in making the

correct decisions and these decisions which are taken by the managers with the involvement of

the employees they are for the betterment of Agmet and they can accomplish their targets.

Inventory management is a part of management accounting system and it helps to the

organisation to manage their stock in an appropriate manner. As they are working in

manufacturing so it is essential for them to keep a stock level according to their orders which can

reduce their inventory managing cost. Excess inventory increase their inventory operating cost

which is a cause of deficit. So implementation of inventory management system helping them to

maintain their profits.

D1

As per the views of Hiebl, (2014), it has been analysed that they can use they have to use

proper management accounting system so that they can not face any issues or problems. They

can use appropriate tools and techniques which includes the ratio analysis, marginal costing

method as it assist in finding out the net profit of the company. Along with this they have to fix

the price for selling the products and also have to use appropriate mix strategies so that they

become successful in selecting the sources of raw material for the product which they are making

for their end users. They have to make correct and relevant decision which is based on the cost of

variable along with the contribution. According to Jansen, (2011), it has been depicted that if

(Håkansson, Kraus and Lind, 2010).

M1

The employees of Agmet can use the different methods for the management accounting

system which assist in managing all the business activities and reduce the cost of the products

which are providing to the service users. Different methods includes the financial planning, fund

flow analysis, decision making accounting. Along with this they can use management reporting

as it helps in preparing the specific accounting report of the distinct contents that is balance sheet

as well as profit and loss statement (Herbert and Seal, 2012). The staff members can use ratio

analysis, cost accounting as well as marginal costing which helps them in attaining the goals and

objectives. Different type of management accounting system that can be used by Agmet and they

are discussed above as it aid in reaping the benefits of the competitive advantage and by that

staff members can improve the process which is related to the cost allocation by using the

distinctive management functions. The use of management accounting system aid in making the

correct decisions and these decisions which are taken by the managers with the involvement of

the employees they are for the betterment of Agmet and they can accomplish their targets.

Inventory management is a part of management accounting system and it helps to the

organisation to manage their stock in an appropriate manner. As they are working in

manufacturing so it is essential for them to keep a stock level according to their orders which can

reduce their inventory managing cost. Excess inventory increase their inventory operating cost

which is a cause of deficit. So implementation of inventory management system helping them to

maintain their profits.

D1

As per the views of Hiebl, (2014), it has been analysed that they can use they have to use

proper management accounting system so that they can not face any issues or problems. They

can use appropriate tools and techniques which includes the ratio analysis, marginal costing

method as it assist in finding out the net profit of the company. Along with this they have to fix

the price for selling the products and also have to use appropriate mix strategies so that they

become successful in selecting the sources of raw material for the product which they are making

for their end users. They have to make correct and relevant decision which is based on the cost of

variable along with the contribution. According to Jansen, (2011), it has been depicted that if

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

they are using the cost accounting then this method assist in representing the current data of the

products and services. Moreover, they have to use the appropriate process of the department so

that employees of Agmet can make the management decisions for the different reasons which are

responsible for various costs.

TASK 2

P3 Calculation of cost by using absorption costing and marginal costing

Absorption costing: It is a instrument which assist in calculating the cost of a product and

this cost is included in the indirect expenses along with the direct costs. It is a tool which aid in

accumulating the cost of the product and it is associated with the production process so that

inventory valuation can be done properly. This method includes the different factors that is direct

material, direct labour, variable overhead of manufacturing as well as fixed overhead which is

also related to manufacturing (Kaplan and Atkinson, 2015). Moreover, it helps in allocating the

overhead cost for the valuation purpose of stock. It is a cost effective technique only when all the

resources distributed properly and in this all the things to be done by the GAAP.

Marginal costing: It is a accounting system in which variable costs are charged to the

cost units as well as fixed cost of the unit so that they can make appropriate contribution.

Marginal cost helps in defining the fixed and variable cost. Marginal cost of the product is its

variable cost. Sometimes, marginal cost refers to the marginal cost per unit but sometimes they

are related to the marginal cost of a department or operations. By using marginal costing

technique, staff members of Agmet can manage all the work so that they can accomplish the

goals and objectives (Lee, 2011Luft and Shields, 2010). It helps in making the appropriate

decisions so that they can improve performance and productivity.

Selling price £35

Unit costs

Direct materials £6

Direct Labour £5

Variable Production overhead £2

Variable sales overhead £1

Budgeted production for the period is 600 units

Fixed costs for the month are given below

products and services. Moreover, they have to use the appropriate process of the department so

that employees of Agmet can make the management decisions for the different reasons which are

responsible for various costs.

TASK 2

P3 Calculation of cost by using absorption costing and marginal costing

Absorption costing: It is a instrument which assist in calculating the cost of a product and

this cost is included in the indirect expenses along with the direct costs. It is a tool which aid in

accumulating the cost of the product and it is associated with the production process so that

inventory valuation can be done properly. This method includes the different factors that is direct

material, direct labour, variable overhead of manufacturing as well as fixed overhead which is

also related to manufacturing (Kaplan and Atkinson, 2015). Moreover, it helps in allocating the

overhead cost for the valuation purpose of stock. It is a cost effective technique only when all the

resources distributed properly and in this all the things to be done by the GAAP.

Marginal costing: It is a accounting system in which variable costs are charged to the

cost units as well as fixed cost of the unit so that they can make appropriate contribution.

Marginal cost helps in defining the fixed and variable cost. Marginal cost of the product is its

variable cost. Sometimes, marginal cost refers to the marginal cost per unit but sometimes they

are related to the marginal cost of a department or operations. By using marginal costing

technique, staff members of Agmet can manage all the work so that they can accomplish the

goals and objectives (Lee, 2011Luft and Shields, 2010). It helps in making the appropriate

decisions so that they can improve performance and productivity.

Selling price £35

Unit costs

Direct materials £6

Direct Labour £5

Variable Production overhead £2

Variable sales overhead £1

Budgeted production for the period is 600 units

Fixed costs for the month are given below

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

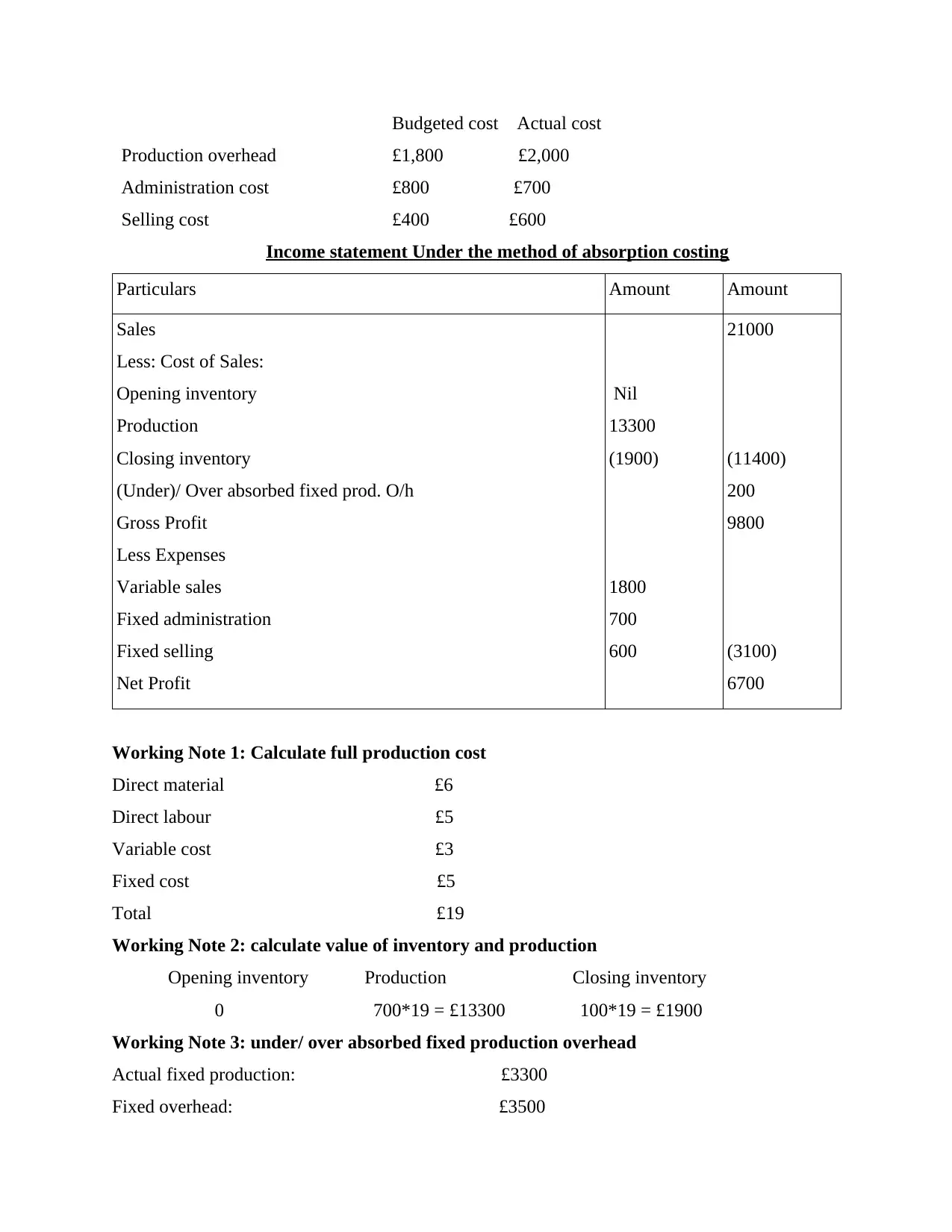

Budgeted cost Actual cost

Production overhead £1,800 £2,000

Administration cost £800 £700

Selling cost £400 £600

Income statement Under the method of absorption costing

Particulars Amount Amount

Sales

Less: Cost of Sales:

Opening inventory

Production

Closing inventory

(Under)/ Over absorbed fixed prod. O/h

Gross Profit

Less Expenses

Variable sales

Fixed administration

Fixed selling

Net Profit

Nil

13300

(1900)

1800

700

600

21000

(11400)

200

9800

(3100)

6700

Working Note 1: Calculate full production cost

Direct material £6

Direct labour £5

Variable cost £3

Fixed cost £5

Total £19

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*19 = £13300 100*19 = £1900

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £3300

Fixed overhead: £3500

Production overhead £1,800 £2,000

Administration cost £800 £700

Selling cost £400 £600

Income statement Under the method of absorption costing

Particulars Amount Amount

Sales

Less: Cost of Sales:

Opening inventory

Production

Closing inventory

(Under)/ Over absorbed fixed prod. O/h

Gross Profit

Less Expenses

Variable sales

Fixed administration

Fixed selling

Net Profit

Nil

13300

(1900)

1800

700

600

21000

(11400)

200

9800

(3100)

6700

Working Note 1: Calculate full production cost

Direct material £6

Direct labour £5

Variable cost £3

Fixed cost £5

Total £19

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*19 = £13300 100*19 = £1900

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £3300

Fixed overhead: £3500

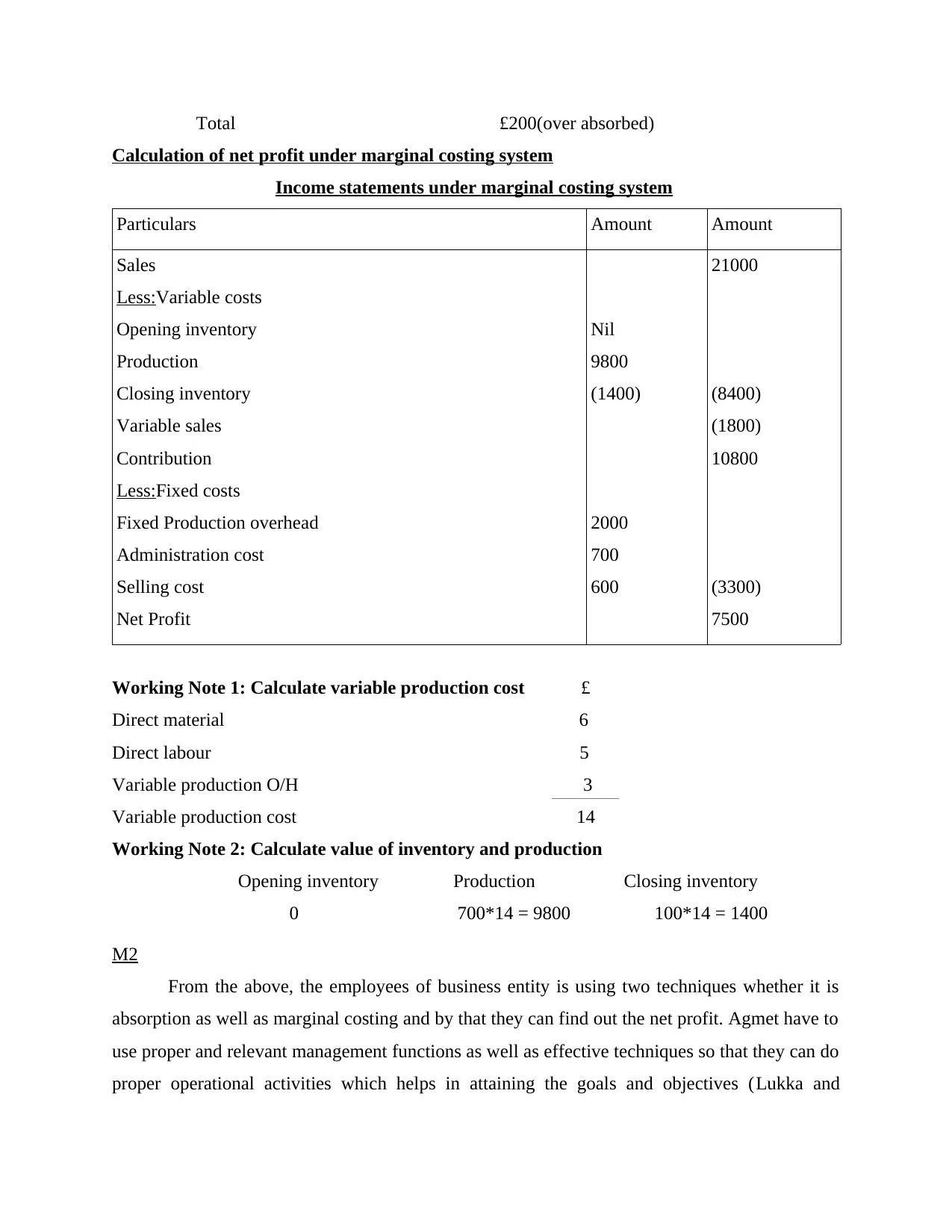

Total £200(over absorbed)

Calculation of net profit under marginal costing system

Income statements under marginal costing system

Particulars Amount Amount

Sales

Less:Variable costs

Opening inventory

Production

Closing inventory

Variable sales

Contribution

Less:Fixed costs

Fixed Production overhead

Administration cost

Selling cost

Net Profit

Nil

9800

(1400)

2000

700

600

21000

(8400)

(1800)

10800

(3300)

7500

Working Note 1: Calculate variable production cost £

Direct material 6

Direct labour 5

Variable production O/H 3

Variable production cost 14

Working Note 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*14 = 9800 100*14 = 1400

M2

From the above, the employees of business entity is using two techniques whether it is

absorption as well as marginal costing and by that they can find out the net profit. Agmet have to

use proper and relevant management functions as well as effective techniques so that they can do

proper operational activities which helps in attaining the goals and objectives (Lukka and

Calculation of net profit under marginal costing system

Income statements under marginal costing system

Particulars Amount Amount

Sales

Less:Variable costs

Opening inventory

Production

Closing inventory

Variable sales

Contribution

Less:Fixed costs

Fixed Production overhead

Administration cost

Selling cost

Net Profit

Nil

9800

(1400)

2000

700

600

21000

(8400)

(1800)

10800

(3300)

7500

Working Note 1: Calculate variable production cost £

Direct material 6

Direct labour 5

Variable production O/H 3

Variable production cost 14

Working Note 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*14 = 9800 100*14 = 1400

M2

From the above, the employees of business entity is using two techniques whether it is

absorption as well as marginal costing and by that they can find out the net profit. Agmet have to

use proper and relevant management functions as well as effective techniques so that they can do

proper operational activities which helps in attaining the goals and objectives (Lukka and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Modell, 2010). Agmet having 50 employees and also having turnover less than £500,000. There

are distinctive tools and techniques which the manager along with the leaders can use that is:

Cost volume analysis which is related to profit: This tool is used by the employees of

Agmet which assist in determining the changes in the cost along with the volume and they are

affected by the operating as well as new income. This can be find out the PV ratio by using the

formula which includes the total contribution which is divided by sales that is:

= contribution /sales x 100

= 10800/21000 x 100

= 51.42%

Absorption costing technique: The managers of cited organisation can use this tool also

which assist in interpreting that the employees of the company having a over absorption of the

spendings and these spendings are related to the fixed production is 200 as well as gross profit is

9800. moreover, gross profit of the company have to identified and affected by the over

absorption of fixed expenses (Macintosh and Quattrone, 2010).

Marginal costing method: As compare to both methods absorption costing system and

marginal costing system, marginal system is profitable for them, bys using this they can make a

more profits in their business operations. Project decision making is a concept which is based on

the management accounting techniques so Agmet has to take decisions as per their marginal

costing system.

D2

Every business entity have to make their financial reports which assist in providing the

information for the investors so that they can make the investment in the company which helps in

meeting the goals and objectives (Nandan, 2010). The managers or the members of the finance

department who make the financial reports have to make the reports in a attractive way which aid

in attracting and making the relevant decisions for the investment purpose. It helps in providing

the some descriptive as well as overview of the financial position of the corporation. Along with

this investors find the capabilities of the company that they can make investments or not. As per

the calculation of marginal cost, net profit is 7500 as well as contribution is 10800. Along with

this, net profit by using the absorption costing methods and by using both techniques net profit is

different from each other (Pipan and Czarniawska, 2010).

are distinctive tools and techniques which the manager along with the leaders can use that is:

Cost volume analysis which is related to profit: This tool is used by the employees of

Agmet which assist in determining the changes in the cost along with the volume and they are

affected by the operating as well as new income. This can be find out the PV ratio by using the

formula which includes the total contribution which is divided by sales that is:

= contribution /sales x 100

= 10800/21000 x 100

= 51.42%

Absorption costing technique: The managers of cited organisation can use this tool also

which assist in interpreting that the employees of the company having a over absorption of the

spendings and these spendings are related to the fixed production is 200 as well as gross profit is

9800. moreover, gross profit of the company have to identified and affected by the over

absorption of fixed expenses (Macintosh and Quattrone, 2010).

Marginal costing method: As compare to both methods absorption costing system and

marginal costing system, marginal system is profitable for them, bys using this they can make a

more profits in their business operations. Project decision making is a concept which is based on

the management accounting techniques so Agmet has to take decisions as per their marginal

costing system.

D2

Every business entity have to make their financial reports which assist in providing the

information for the investors so that they can make the investment in the company which helps in

meeting the goals and objectives (Nandan, 2010). The managers or the members of the finance

department who make the financial reports have to make the reports in a attractive way which aid

in attracting and making the relevant decisions for the investment purpose. It helps in providing

the some descriptive as well as overview of the financial position of the corporation. Along with

this investors find the capabilities of the company that they can make investments or not. As per

the calculation of marginal cost, net profit is 7500 as well as contribution is 10800. Along with

this, net profit by using the absorption costing methods and by using both techniques net profit is

different from each other (Pipan and Czarniawska, 2010).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 3

P4 Advantages and disadvantages of different planning tools

Budgetary control is a tool or instrument which helps managers to utilise the budgets.

Along with this they have to monitor and control the costs as well as operations in a specific time

period. Budgetary control is a process which aid the managers so that they can set the financial

as well as performance goals with the budgets as well as they have to compare the actual results

along with the adjusting performance as it is needed (Quinn, 2011). There are many advantages

of the budgetary control are:

Budgetary control helps in defining the goals of the business entity. Along with this they

have to use the appropriate policies along with the procedures within the organisation. The

company having the definite aim so that they can attain the goals. They have to do all the

activities with the better coordination between the distinctive departments of Agmet (Renz,

2016).

Master budget is a planning tool in budgetary control in which is master budget produce

by the higher management which can help to the management to continue their activities. All the

details of the master budget is known by each and every employee of the organisation which

helps to reduce confusion and conflicts in between managers.

If performance of the employees in the company is below than the expected level so that

they can find out the responsibility so that they can reduce the cost of the products and services

by that they can eliminate the waste products. Budgetary is the effective and essential methods

for Agmet so that they can achieve the objectives. The manager of the business entity have to set

the targets for their leaders and by doing qualitative work they have to achieve that in the

effective and efficient manner (Sánchez-Rodríguez and Spraakman, 2012).

Cash is the back bone of the business so it is essential for the management to manage a

cash flow in the organisation which can help them to make payments on right time of their

suppliers. Cash flow budgeting is planning tool of budgetary control and this helps them to

manage cash in flow and cash out flow to manage a balance in both.

Moreover, it helps in bringing the efficiency in the economy which aid in promoting the

cost consequences among the different employees of Agmet. They have to do proper planning so

that they can do all the operational activities in the efficient manner. By doing the proper

P4 Advantages and disadvantages of different planning tools

Budgetary control is a tool or instrument which helps managers to utilise the budgets.

Along with this they have to monitor and control the costs as well as operations in a specific time

period. Budgetary control is a process which aid the managers so that they can set the financial

as well as performance goals with the budgets as well as they have to compare the actual results

along with the adjusting performance as it is needed (Quinn, 2011). There are many advantages

of the budgetary control are:

Budgetary control helps in defining the goals of the business entity. Along with this they

have to use the appropriate policies along with the procedures within the organisation. The

company having the definite aim so that they can attain the goals. They have to do all the

activities with the better coordination between the distinctive departments of Agmet (Renz,

2016).

Master budget is a planning tool in budgetary control in which is master budget produce

by the higher management which can help to the management to continue their activities. All the

details of the master budget is known by each and every employee of the organisation which

helps to reduce confusion and conflicts in between managers.

If performance of the employees in the company is below than the expected level so that

they can find out the responsibility so that they can reduce the cost of the products and services

by that they can eliminate the waste products. Budgetary is the effective and essential methods

for Agmet so that they can achieve the objectives. The manager of the business entity have to set

the targets for their leaders and by doing qualitative work they have to achieve that in the

effective and efficient manner (Sánchez-Rodríguez and Spraakman, 2012).

Cash is the back bone of the business so it is essential for the management to manage a

cash flow in the organisation which can help them to make payments on right time of their

suppliers. Cash flow budgeting is planning tool of budgetary control and this helps them to

manage cash in flow and cash out flow to manage a balance in both.

Moreover, it helps in bringing the efficiency in the economy which aid in promoting the

cost consequences among the different employees of Agmet. They have to do proper planning so

that they can do all the operational activities in the efficient manner. By doing the proper

management they have to identify the problem and find out the effective way by which they can

resolve the problem in a effective manner.

There are some disadvantages of the budgetary control which helps in doing planning:

When economy is facing inflation then the managers or the person who are making the

budgets they can face lots of difficulties. Budget always requires the heavy and high expenditure

to prepare the budgets and these can not be afford by the small companies (Setthasakko, 2010).

Master budget involves a large scope of the organisation so it consumes a lot of time,

human efforts and costs. It has a need of huge experience which can help to manage all aspects

of the budget which can help to manage all things in the budgetary control.

Budgets are always prepared for the future so that they can make the changes in the

economic conditions and on the basis of that they can brings ups and downs in the budget.

Cash flow budgeting tool is not acceptable in the reality because accounts managers can

not assume a total cash inflow for a particular day. Another thing is that company has to make

payments on due date so they can not based on the cash inflow to make payments of their

employees, suppliers and investors.

Budgetary control is a tool which assist in doing the management and it can not be

replace the management by using the effective decision making process as it is a substitute.

The employees of Agmet can make the budgets by keeping the current organisational

structure in mind (Shah, Malik and Malik, 2011). The organisational structure which company is

following it may not be appropriate for the current conditions. As this is a cost control technique

so it can not be used by small organisation. The staff members have to do coordination and

correlation of the distinctive budgets is expensive.

M3

The staff members of Agmet can use different planning tools as well as application for

preparing the budgets which includes the future forecasting so that they can make future

estimation of the budgets but these budgets have to be prepare in advance (Talha, Raja and

Seetharaman, 2010). They can use cost aggregation in which they can minimise the cost by using

the different activities in the work breakdown structure as well as increase the productivity in the

organisation. They can use reserve analysis as it is a technique so that they can review the project

so that they can manage the plan which assist in identifying the risk factor. It will helps in

attaining the expert judgement so that they are responsible for monitoring as well as controlling

resolve the problem in a effective manner.

There are some disadvantages of the budgetary control which helps in doing planning:

When economy is facing inflation then the managers or the person who are making the

budgets they can face lots of difficulties. Budget always requires the heavy and high expenditure

to prepare the budgets and these can not be afford by the small companies (Setthasakko, 2010).

Master budget involves a large scope of the organisation so it consumes a lot of time,

human efforts and costs. It has a need of huge experience which can help to manage all aspects

of the budget which can help to manage all things in the budgetary control.

Budgets are always prepared for the future so that they can make the changes in the

economic conditions and on the basis of that they can brings ups and downs in the budget.

Cash flow budgeting tool is not acceptable in the reality because accounts managers can

not assume a total cash inflow for a particular day. Another thing is that company has to make

payments on due date so they can not based on the cash inflow to make payments of their

employees, suppliers and investors.

Budgetary control is a tool which assist in doing the management and it can not be

replace the management by using the effective decision making process as it is a substitute.

The employees of Agmet can make the budgets by keeping the current organisational

structure in mind (Shah, Malik and Malik, 2011). The organisational structure which company is

following it may not be appropriate for the current conditions. As this is a cost control technique

so it can not be used by small organisation. The staff members have to do coordination and

correlation of the distinctive budgets is expensive.

M3

The staff members of Agmet can use different planning tools as well as application for

preparing the budgets which includes the future forecasting so that they can make future

estimation of the budgets but these budgets have to be prepare in advance (Talha, Raja and

Seetharaman, 2010). They can use cost aggregation in which they can minimise the cost by using

the different activities in the work breakdown structure as well as increase the productivity in the

organisation. They can use reserve analysis as it is a technique so that they can review the project

so that they can manage the plan which assist in identifying the risk factor. It will helps in

attaining the expert judgement so that they are responsible for monitoring as well as controlling

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.