AcF 311 Coursework: Accounting Analysis of Agrico plc

VerifiedAdded on 2023/01/12

|8

|1254

|69

Case Study

AI Summary

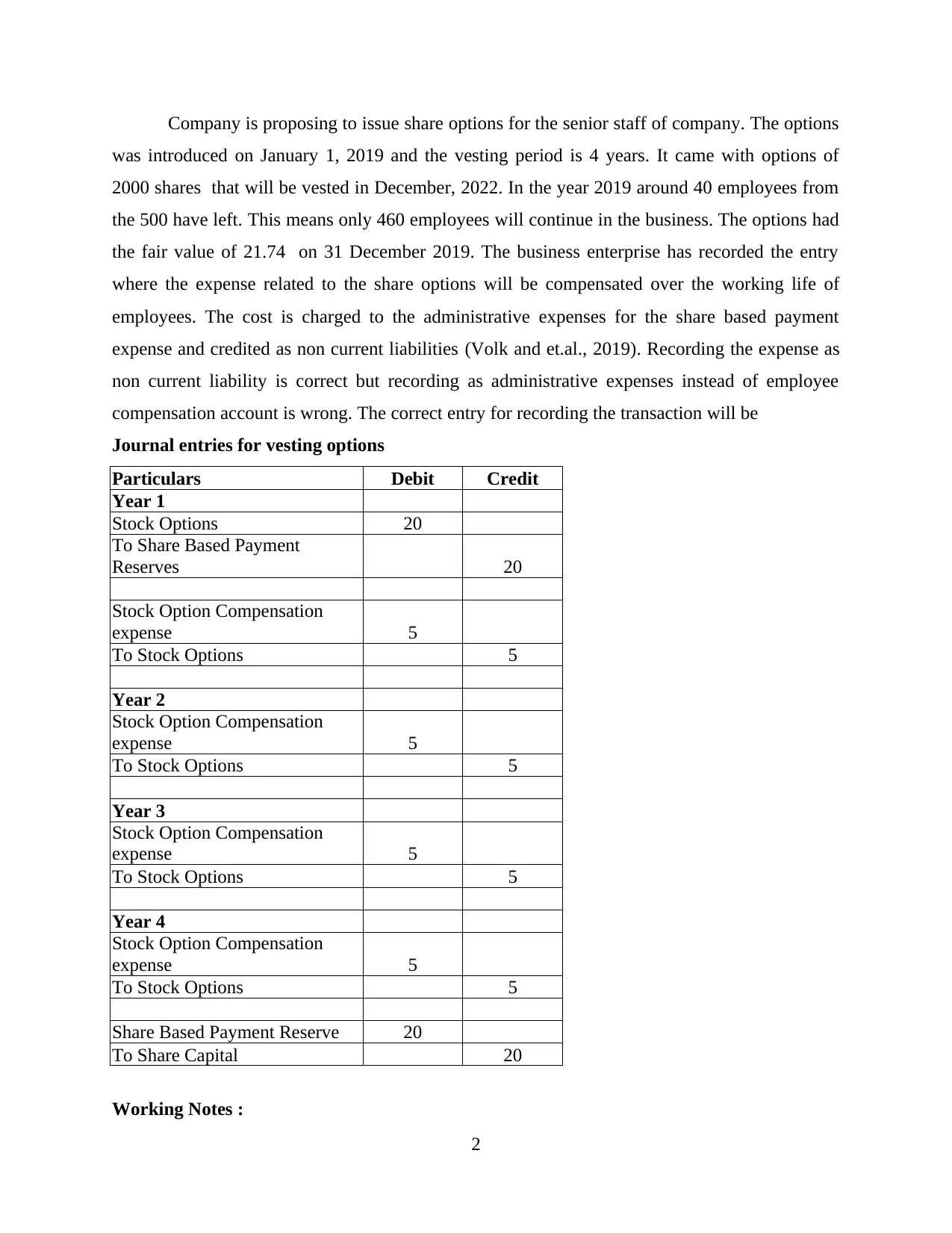

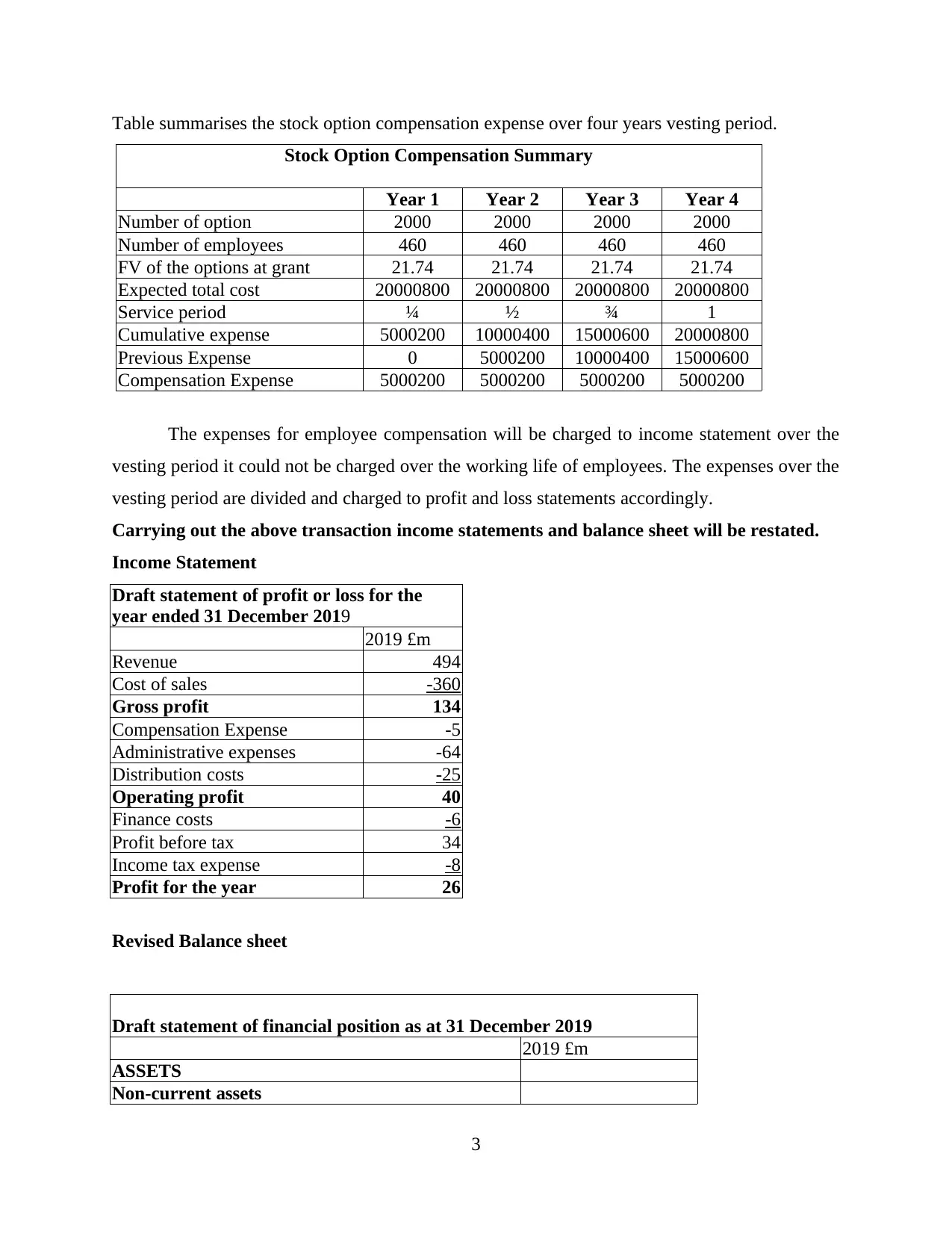

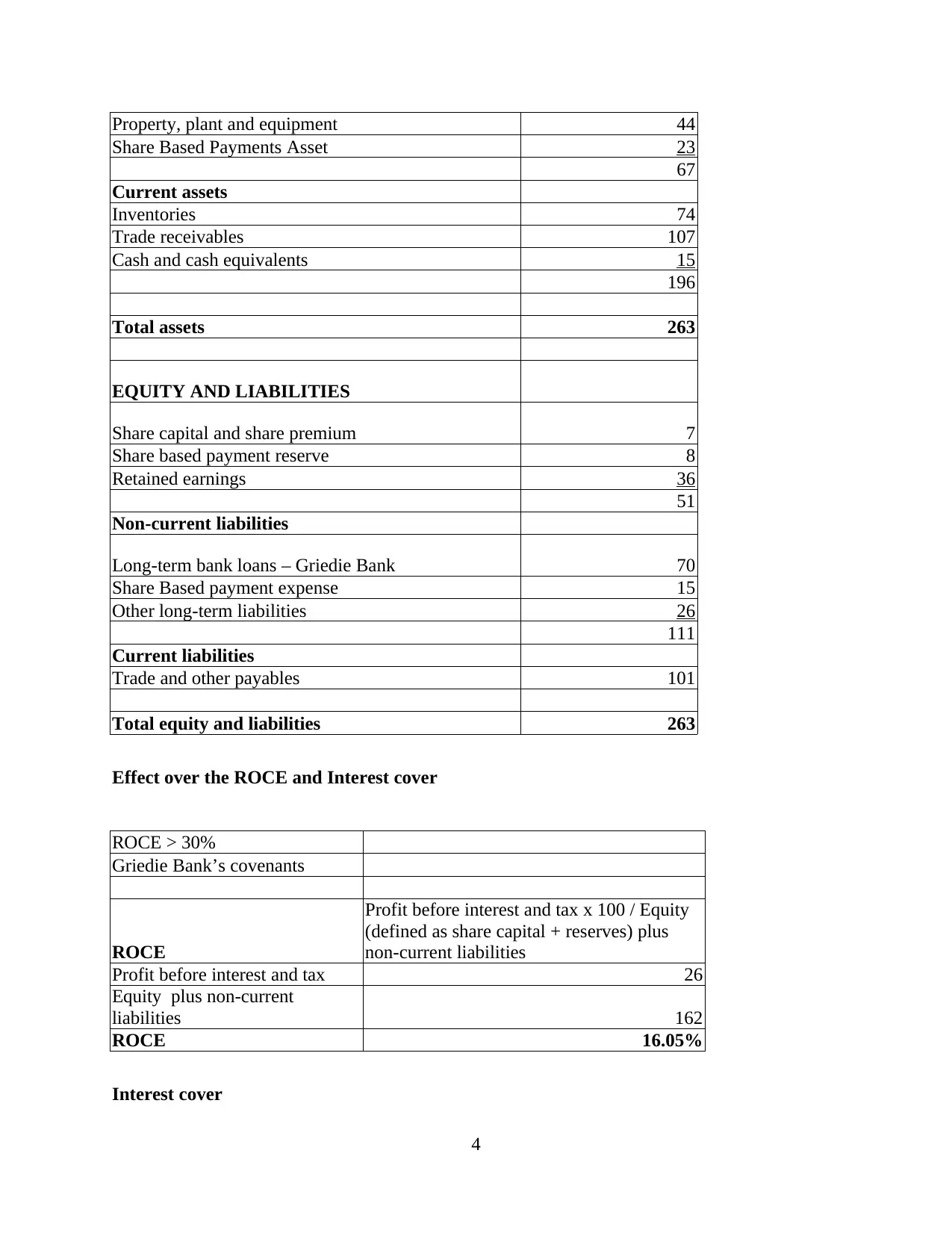

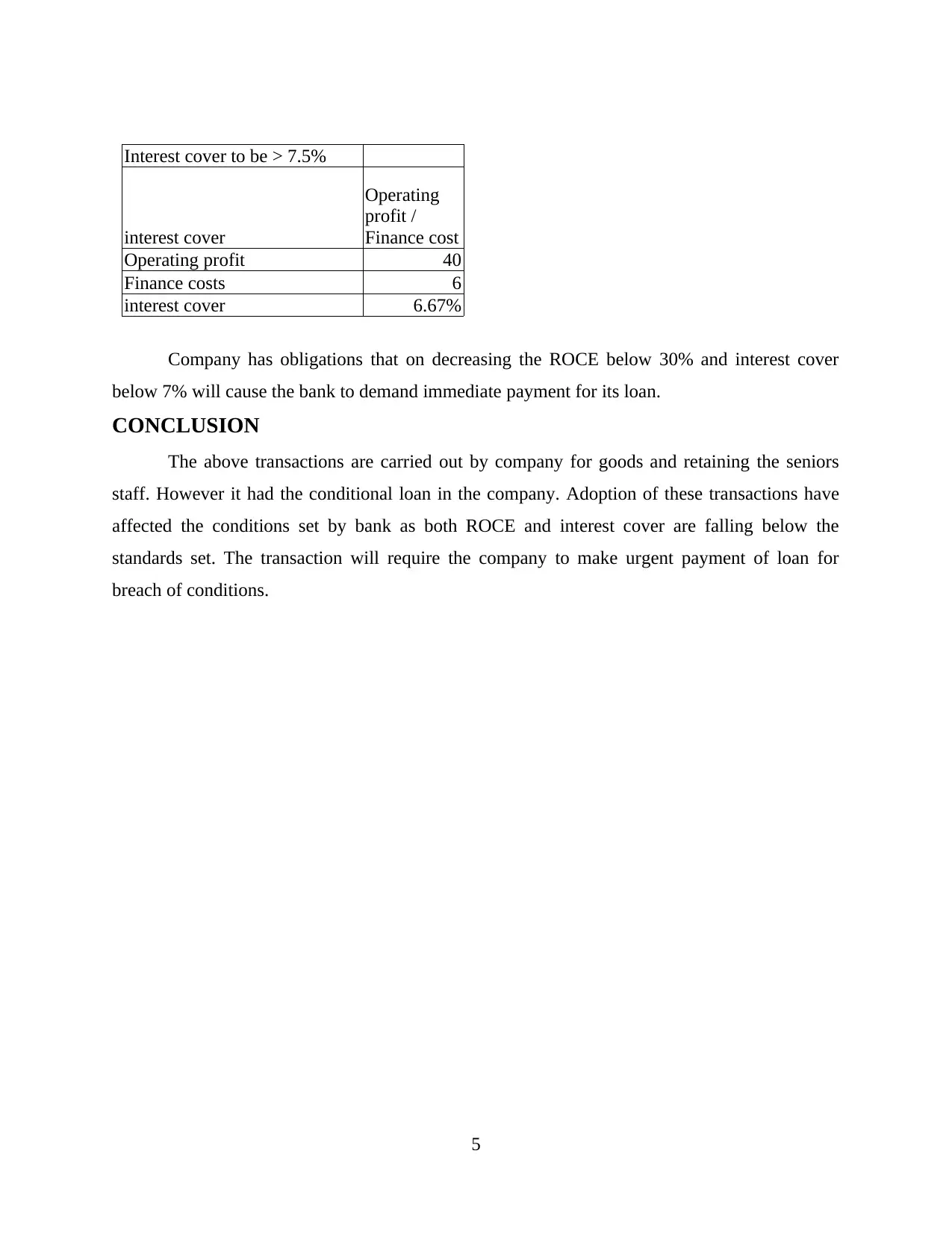

This case study analyzes the financial accounting practices of Agrico plc, focusing on two significant transactions: share-based payments to suppliers for goods and share options issued to senior staff. The analysis includes detailed journal entries for recording these transactions, along with the creation of reserve accounts and the allocation of expenses over vesting periods. The study further examines the impact of these transactions on Agrico plc's financial statements, including the income statement and balance sheet, and calculates the effects on Return on Capital Employed (ROCE) and interest cover, highlighting potential breaches of bank covenants. The conclusion emphasizes the implications of these financial decisions on the company's financial health and obligations.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.