Purchase of Soletta Ltd: Consolidated Financial Statement Preparation

VerifiedAdded on 2023/06/06

|11

|1273

|88

Homework Assignment

AI Summary

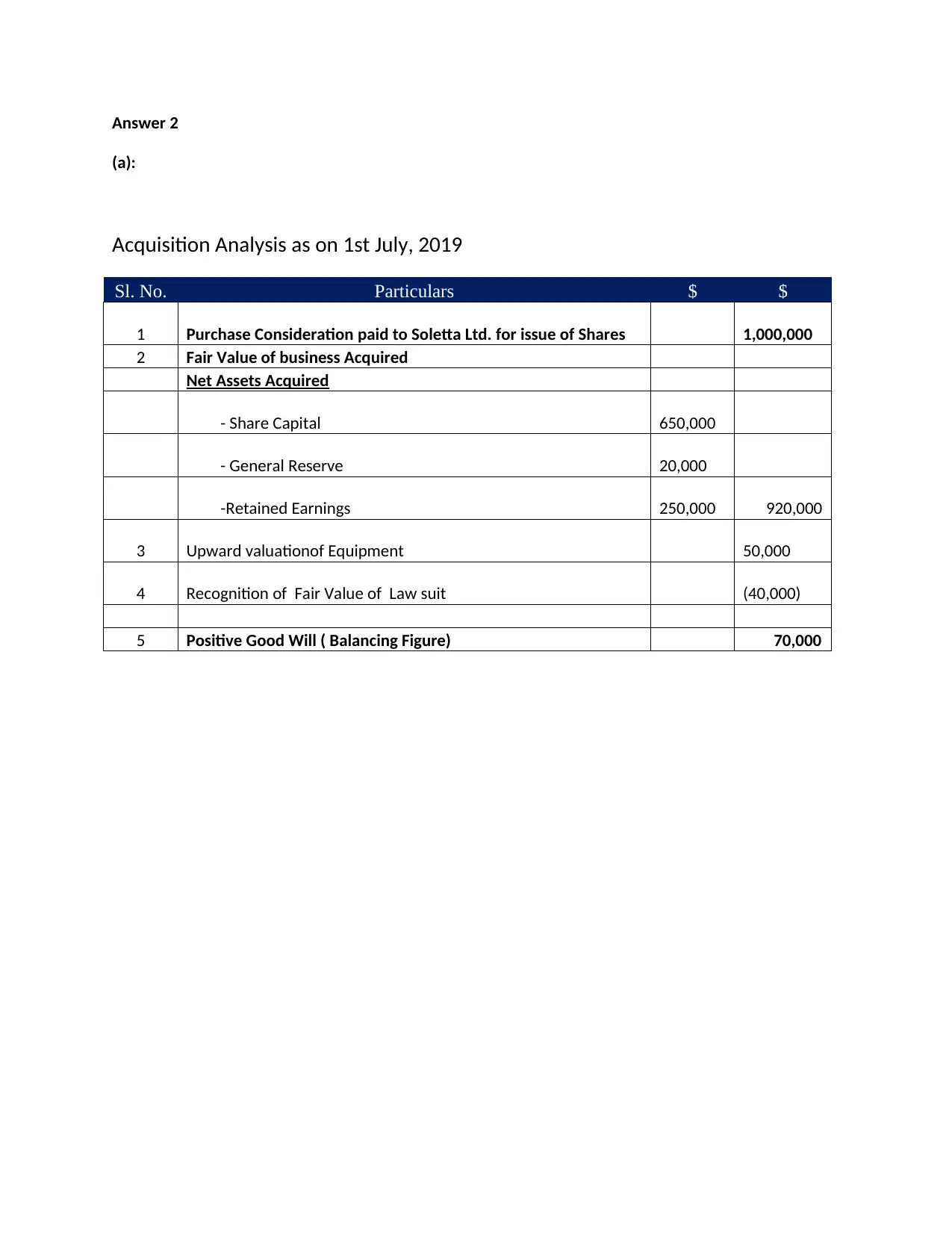

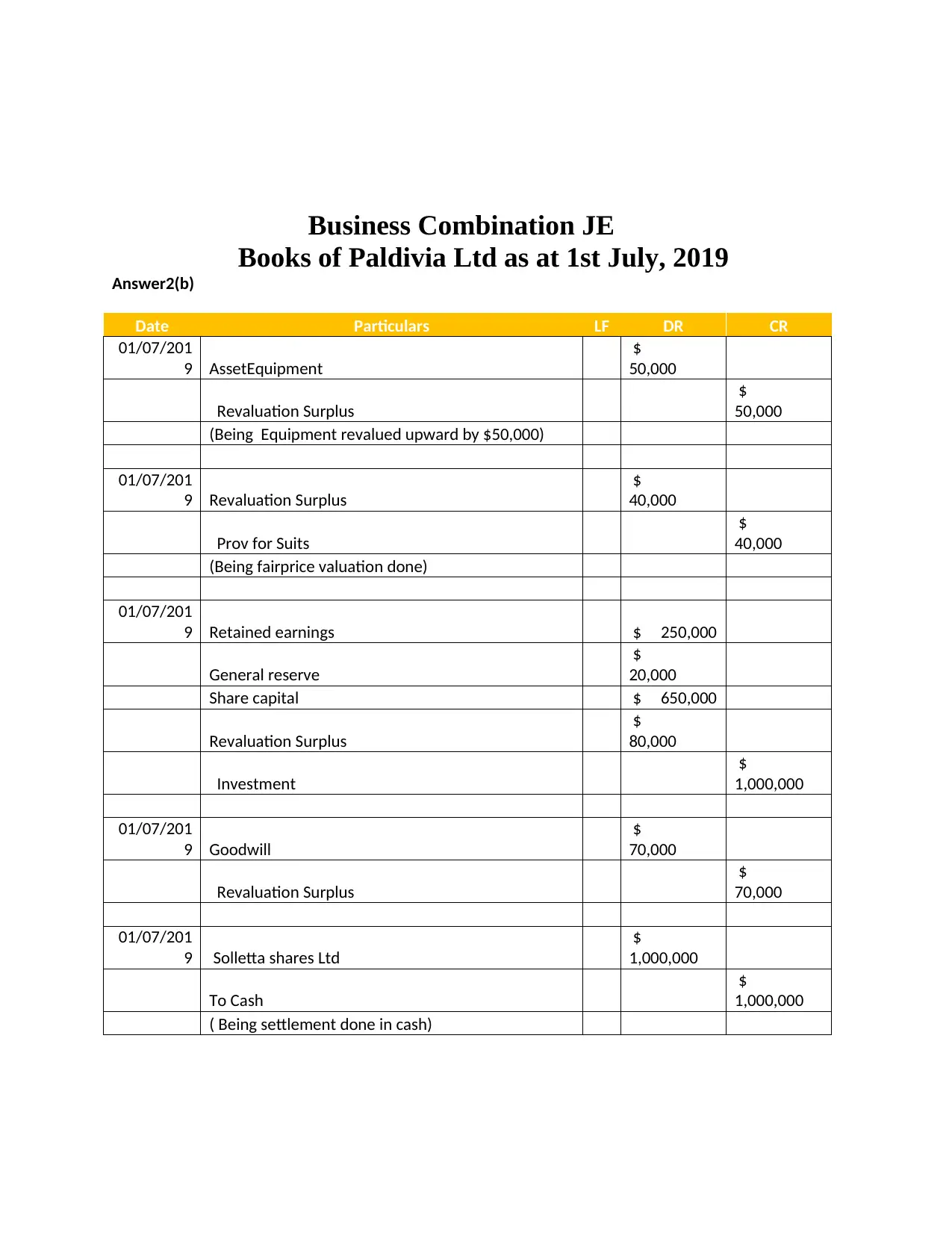

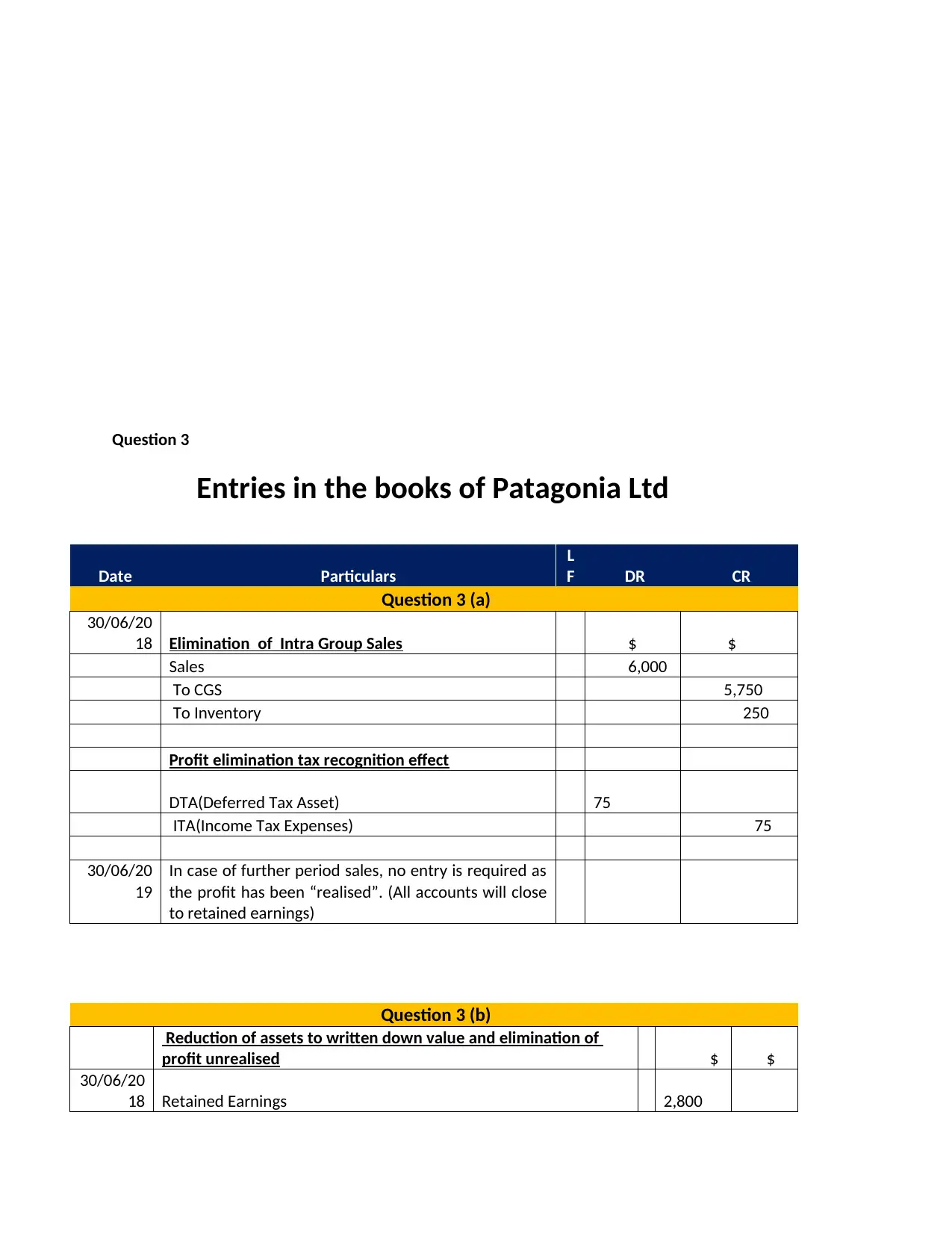

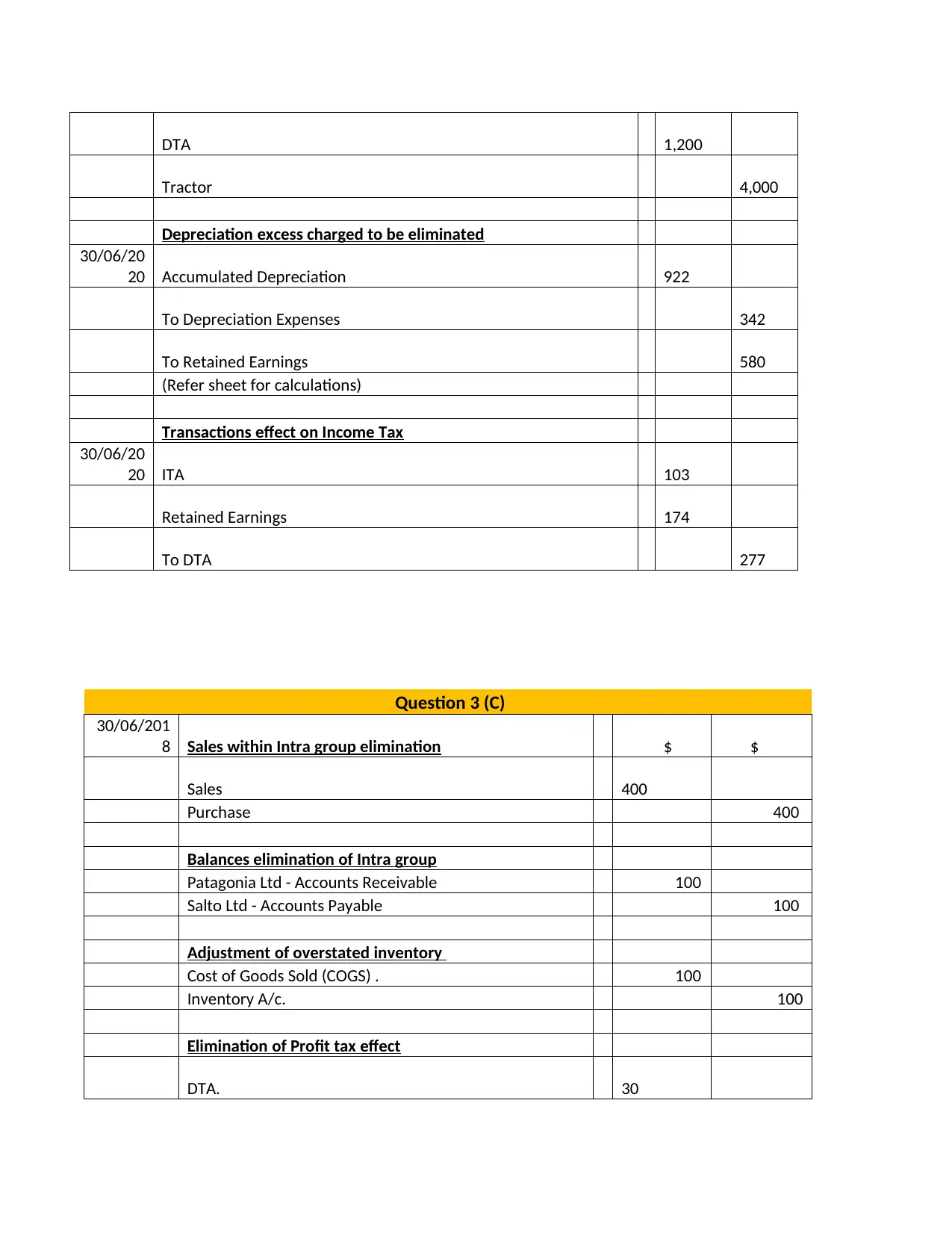

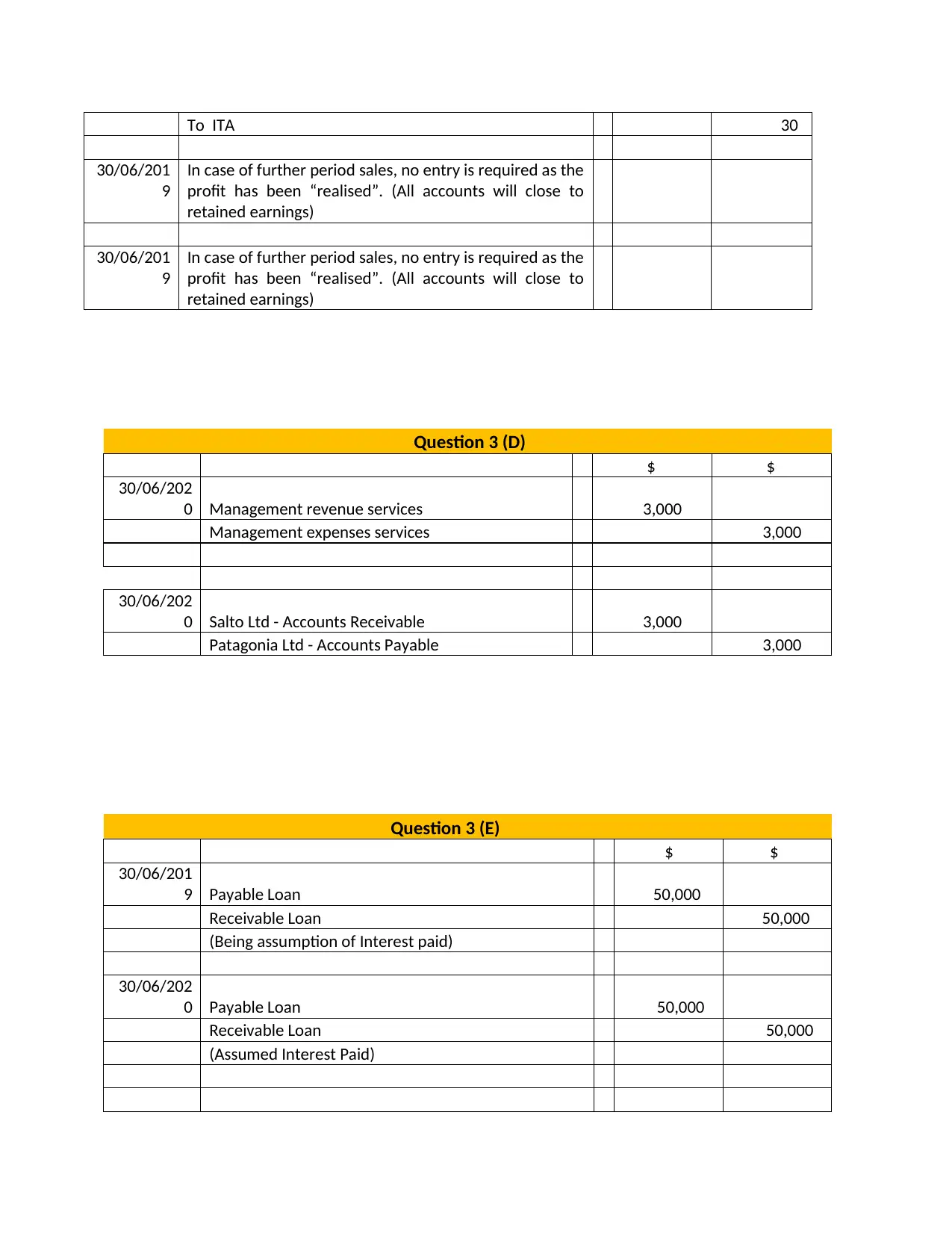

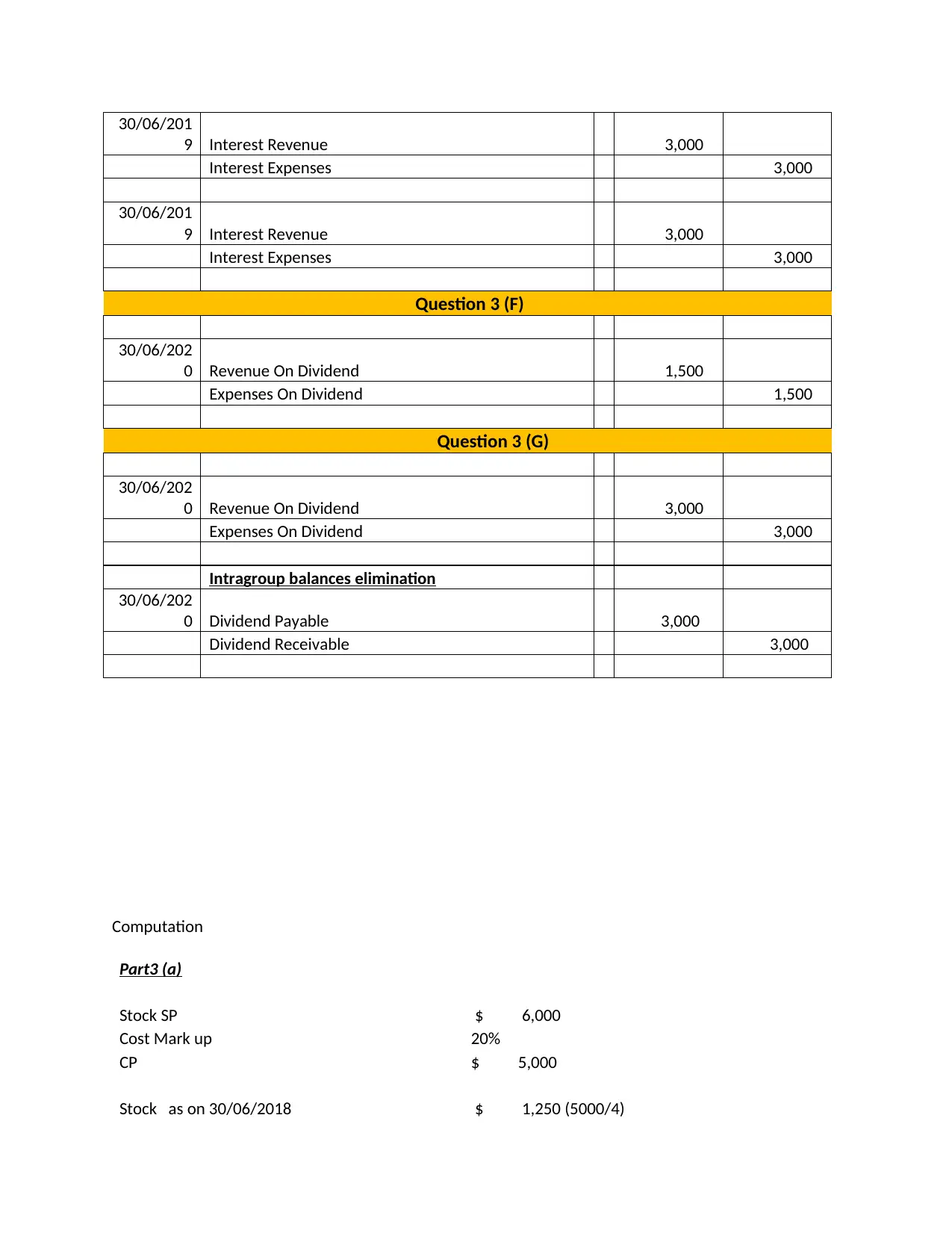

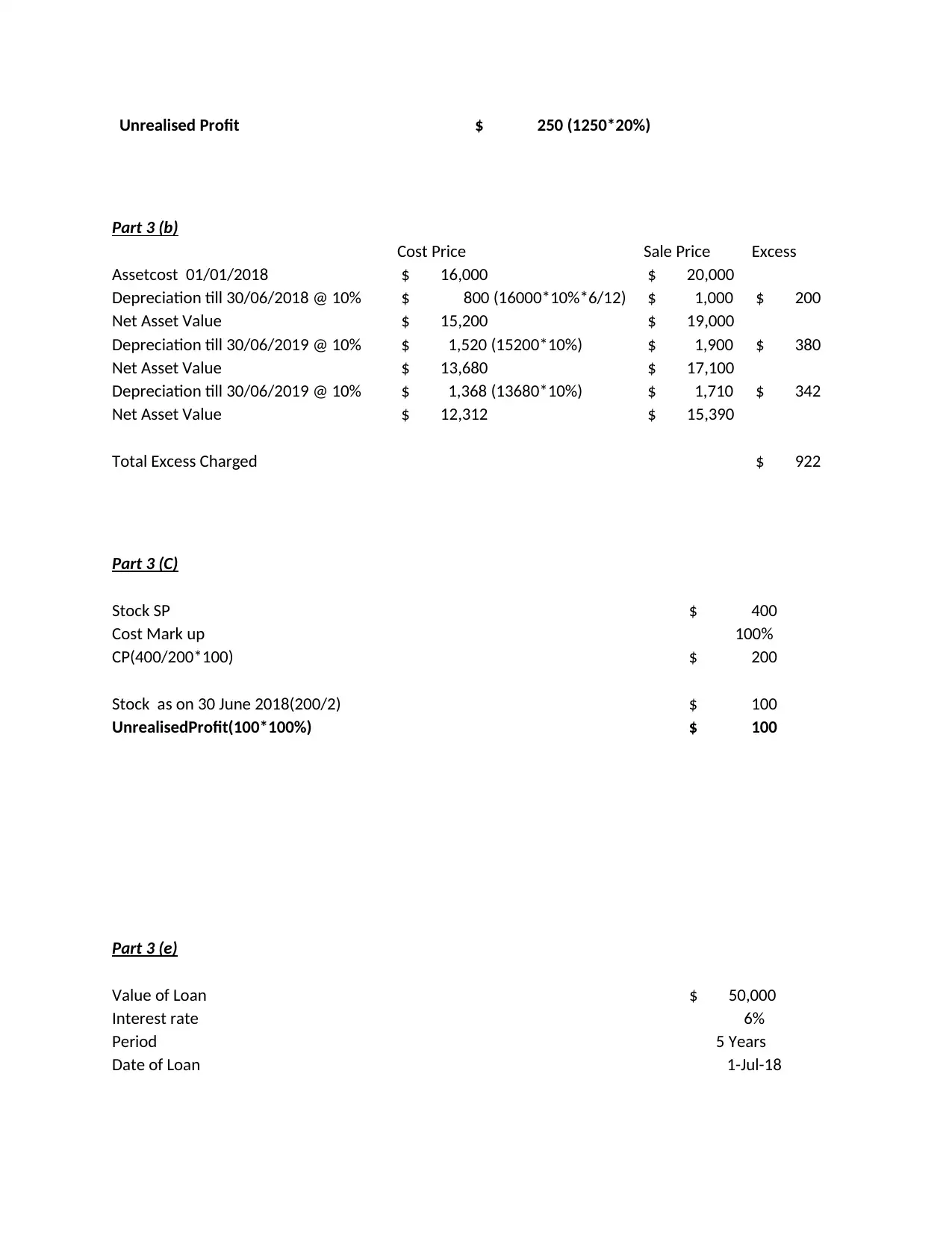

This assignment solution addresses various aspects of consolidated financial statements related to the potential acquisition of Soletta Ltd. It begins by explaining the purpose of consolidated financial statements, defining key terms like 'group,' 'parent,' and 'subsidiary,' and justifying the necessity of adjusting for intra-group transactions, particularly concerning inventory transfers. The solution then presents an acquisition analysis as of July 1, 2019, including the calculation of goodwill and the necessary journal entries. Furthermore, it details the elimination of intra-group sales, adjustments for unrealized profits on assets, and the treatment of management service revenues and expenses, loan transactions, and dividends within the consolidated entity. Computations for unrealized profit on stock and asset values are also provided, along with calculations for interest on loans. The solution references relevant sources for definitions and principles, ensuring a comprehensive understanding of the consolidation process.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.