MAA303: Audit and Assurance Case Study - Financial Analysis and Risks

VerifiedAdded on 2022/09/08

|9

|1527

|11

Case Study

AI Summary

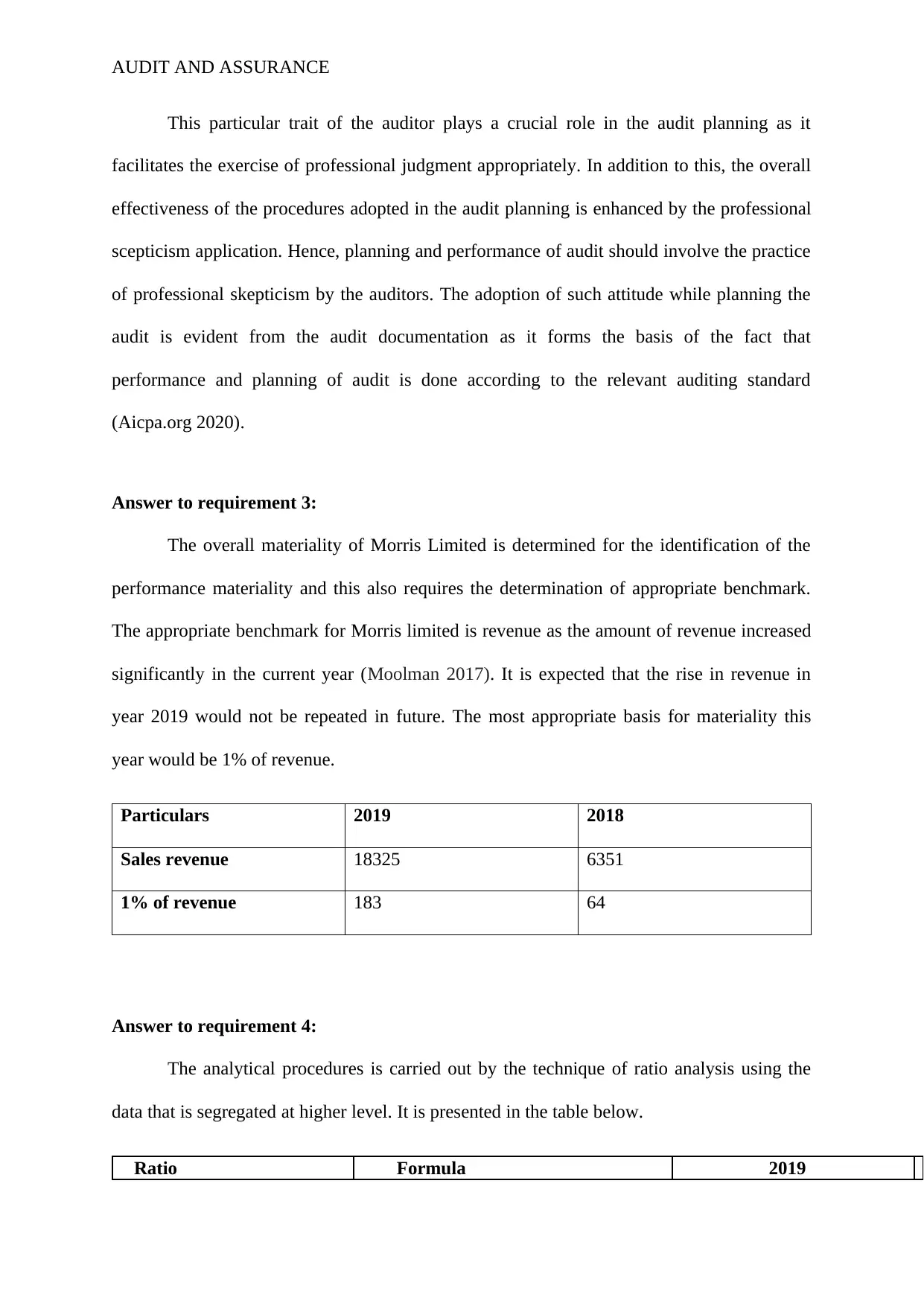

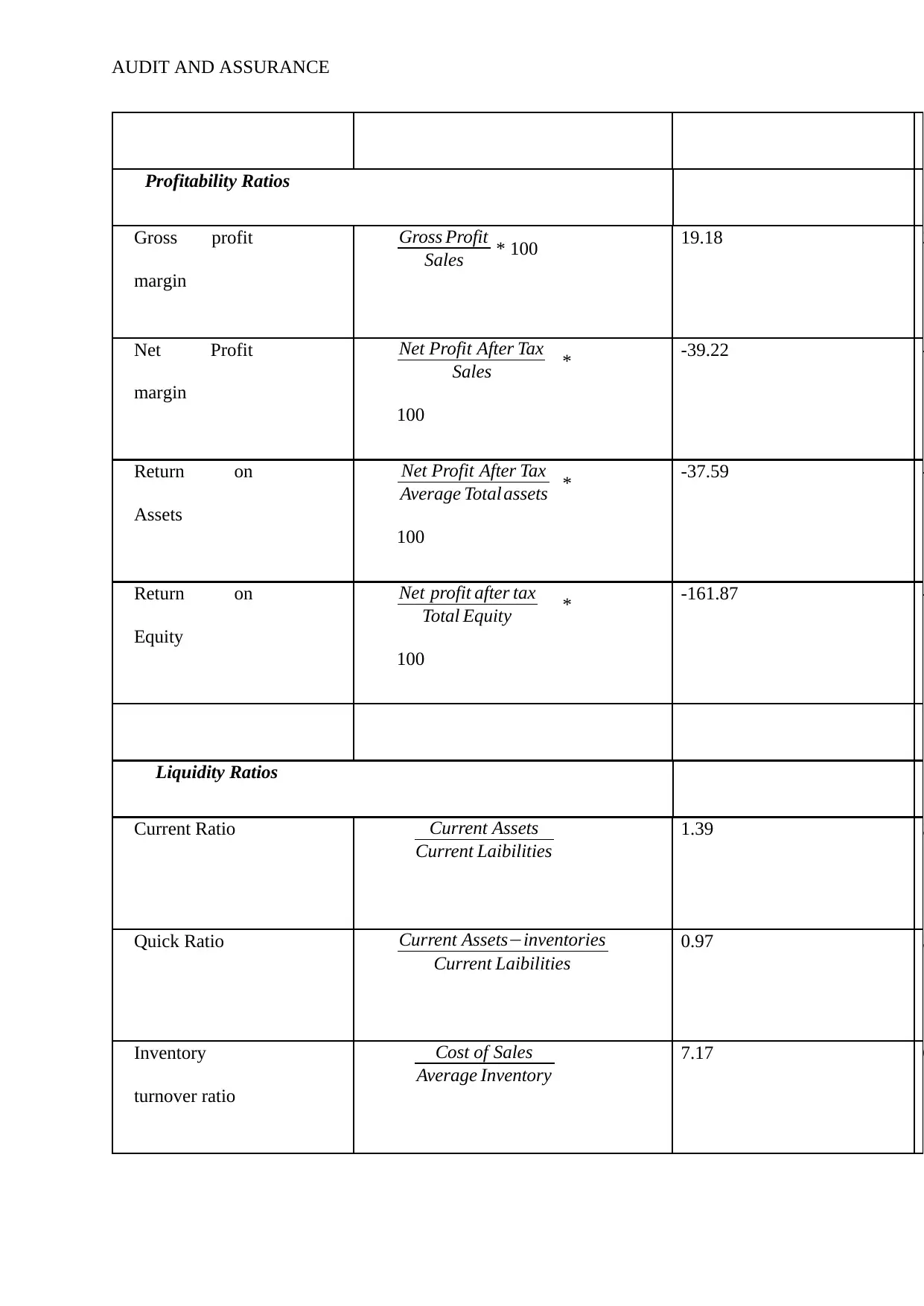

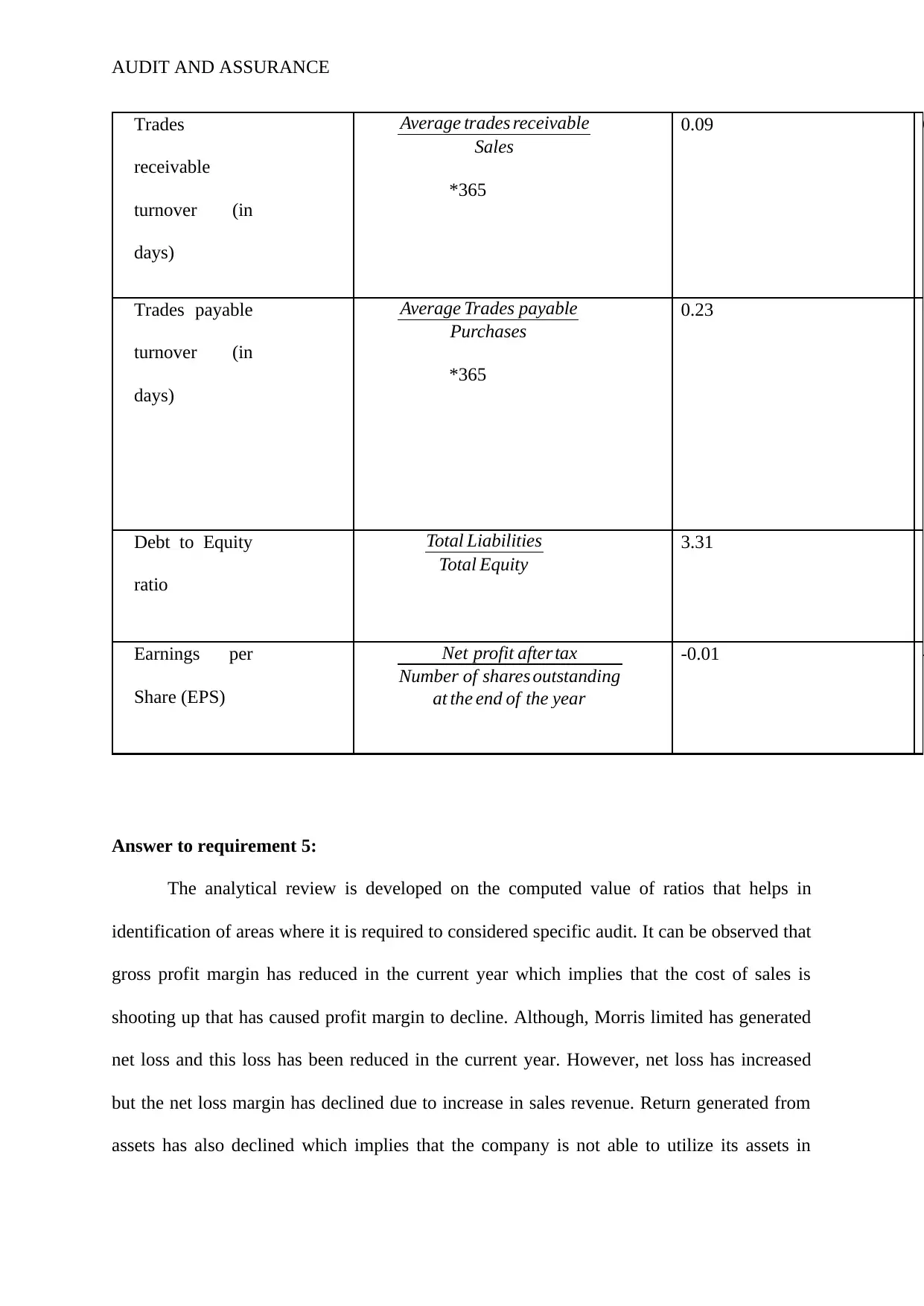

This case study analyzes the audit and assurance procedures applied to Morris Limited. The student begins by discussing the role of analytical procedures in risk assessment, highlighting the identification of material misstatements and unusual transactions. The importance of professional skepticism in audit planning and execution is then addressed. The determination of materiality, using revenue as a benchmark, is explained. A detailed ratio analysis is presented, comparing 2019 and 2018 financial data, including profitability, liquidity, and debt ratios. The student then interprets the ratio analysis, identifying key areas of concern for the auditors, such as declining gross profit margins, increasing debt, and liquidity issues. The analysis emphasizes the need for auditors to focus on sales revenue, inventory, current liabilities, and the company's loan and trade payables, along with the increasing cost of sales. The analysis is supported by relevant academic references.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.