Audit & Assurance: Materiality, Analytical Procedures & Remuneration

VerifiedAdded on 2023/04/25

|16

|2358

|440

Report

AI Summary

This report presents a comprehensive analysis of audit and assurance principles, divided into three key sections. The first section focuses on the case study of Cloud 9 Pty Ltd, detailing audit planning considerations for W&S Partners and calculating overall materiality based on net assets. The second part describes the analytical procedures applied to Cloud 9 Pty Ltd's financial statements, highlighting potential risk areas related to accounts receivable, property assets, and marketing expenditures. It also suggests steps to mitigate these risks. Finally, the report concludes with an examination of executive remuneration structures in ASX-listed companies within the retail industry, specifically Wesfarmers, Woolworths, and Caltex, discussing base salaries and compensation practices in light of corporate governance provisions and the Corporations Act 2001. Desklib offers a variety of solved assignments and study resources for students.

Running head: AUDIT AND ASSURANCE

Audit and Assurance

Name of the Student:

Name of the University:

Author Note:

Audit and Assurance

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDIT AND ASSURANCE

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................4

Part A.....................................................................................................................................4

Materiality..........................................................................................................................4

Part B......................................................................................................................................5

Analytical Procedure..........................................................................................................5

Part C......................................................................................................................................7

Remuneration.....................................................................................................................7

Compensation.....................................................................................................................8

Reference..................................................................................................................................10

Appendix:.................................................................................................................................11

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................4

Part A.....................................................................................................................................4

Materiality..........................................................................................................................4

Part B......................................................................................................................................5

Analytical Procedure..........................................................................................................5

Part C......................................................................................................................................7

Remuneration.....................................................................................................................7

Compensation.....................................................................................................................8

Reference..................................................................................................................................10

Appendix:.................................................................................................................................11

2AUDIT AND ASSURANCE

Executive Summary:

The report is divided into three parts. The first and the second part is based on the case study

of Cloud 9 Pty. Ltd. The report is commenced on the audit planning for the audit firm W&S

Partners. The report gives the calculation of overall materiality including stating the reason

for it. In the second part analytical procedure is described. Lastly, the report is concluded on

the remuneration structure of the listed companies. For this three companies that are listed in

the ASX exchange are Wesfarmers, Woolworth and Caltex ltd are from retail industry.

Executive Summary:

The report is divided into three parts. The first and the second part is based on the case study

of Cloud 9 Pty. Ltd. The report is commenced on the audit planning for the audit firm W&S

Partners. The report gives the calculation of overall materiality including stating the reason

for it. In the second part analytical procedure is described. Lastly, the report is concluded on

the remuneration structure of the listed companies. For this three companies that are listed in

the ASX exchange are Wesfarmers, Woolworth and Caltex ltd are from retail industry.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDIT AND ASSURANCE

Introduction

Auditing is the process or quality procedure to inspect or examinee in order to ensure

that the company has met the compliance requirement. To provide fair and true view opinion

auditor shall inspect the records of accounts, sales invoice any other statutory requirements

that has to be met by the company. Auditing is conducted by the independent auditor or team

of auditor those are qualified as chartered accountant. To put down his or her opinion on

verification of inspection of done on the basis of books of accounts and the monetary

statement auditor authentically check the support documents very well.

Introduction

Auditing is the process or quality procedure to inspect or examinee in order to ensure

that the company has met the compliance requirement. To provide fair and true view opinion

auditor shall inspect the records of accounts, sales invoice any other statutory requirements

that has to be met by the company. Auditing is conducted by the independent auditor or team

of auditor those are qualified as chartered accountant. To put down his or her opinion on

verification of inspection of done on the basis of books of accounts and the monetary

statement auditor authentically check the support documents very well.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDIT AND ASSURANCE

Discussion

Part A

Cloud 9 Pty Ltd was founded by R.A. McLellan at Sydney in the year 1980. The

company belonged to manufacturing as well as retailing industry. The company dealt in

manufacturing as well as retailing of special type of basketball shoes. The company was a

parent and had its subsidiary company in Brazil, Canada, Germany and China also. Through

providing comfort and durability shoes to the public of the countries it served it succeeded in

building up its reputation. The company had rhymed the comfort of its shoes with its name.

The tagline of the company was “ Our shoes was so comfortable, its feel like we are working

on cloud 9”. Recently the company is a wholesaler of athletic shoes to its priority consumers.

In the year 2014, the company had manufactured its new product line named as Walk on

Cloud. The company purchases its stock in Us Dollar.

Materiality

The conception of materiality is narrowly related to the auditor’s attention of the side

by side of audit risk. The process of setting the level of risk while performing audit is based

on the inspection of the materials that is being misstated or is not been corrected by the

internal control system of the auditor`s clients. As soon as auditor identifies or assess the

materiality in the fiscal statements, auditor is required to plan for materiality. The materiality

amount should be higher than the performance materiality. Planning materiality must be

larger than performance materiality. The reason is because materiality sum belongs to fiscal

statement and performance materiality is the misstatement that is subjected to occur in the

statement. The materiality is calculated on the base of certain qualitative factors. There is a

basic threshold limit for calculating the materiality.

Discussion

Part A

Cloud 9 Pty Ltd was founded by R.A. McLellan at Sydney in the year 1980. The

company belonged to manufacturing as well as retailing industry. The company dealt in

manufacturing as well as retailing of special type of basketball shoes. The company was a

parent and had its subsidiary company in Brazil, Canada, Germany and China also. Through

providing comfort and durability shoes to the public of the countries it served it succeeded in

building up its reputation. The company had rhymed the comfort of its shoes with its name.

The tagline of the company was “ Our shoes was so comfortable, its feel like we are working

on cloud 9”. Recently the company is a wholesaler of athletic shoes to its priority consumers.

In the year 2014, the company had manufactured its new product line named as Walk on

Cloud. The company purchases its stock in Us Dollar.

Materiality

The conception of materiality is narrowly related to the auditor’s attention of the side

by side of audit risk. The process of setting the level of risk while performing audit is based

on the inspection of the materials that is being misstated or is not been corrected by the

internal control system of the auditor`s clients. As soon as auditor identifies or assess the

materiality in the fiscal statements, auditor is required to plan for materiality. The materiality

amount should be higher than the performance materiality. Planning materiality must be

larger than performance materiality. The reason is because materiality sum belongs to fiscal

statement and performance materiality is the misstatement that is subjected to occur in the

statement. The materiality is calculated on the base of certain qualitative factors. There is a

basic threshold limit for calculating the materiality.

5AUDIT AND ASSURANCE

Overall materiality is the opinion base for an auditor as because that helps auditor to

points out the importance factor that is presented in the statement as on whole. To the point

that manipulates the decision of an investor. It is assessed as portion of the preparation of the

audit as well as return to and reviewed all over the audit procedure. Usually, it will be

considered by applying a proportion to a selected standard such as Profit before Tax or net

assets. The auditor essentially prove decision in choosing the overall materiality level.

The overall materiality calculated for Cloud 9 Pty. Ltd is on Net asset because the

revenue earned by the company is basically from the asset of the company. The overall

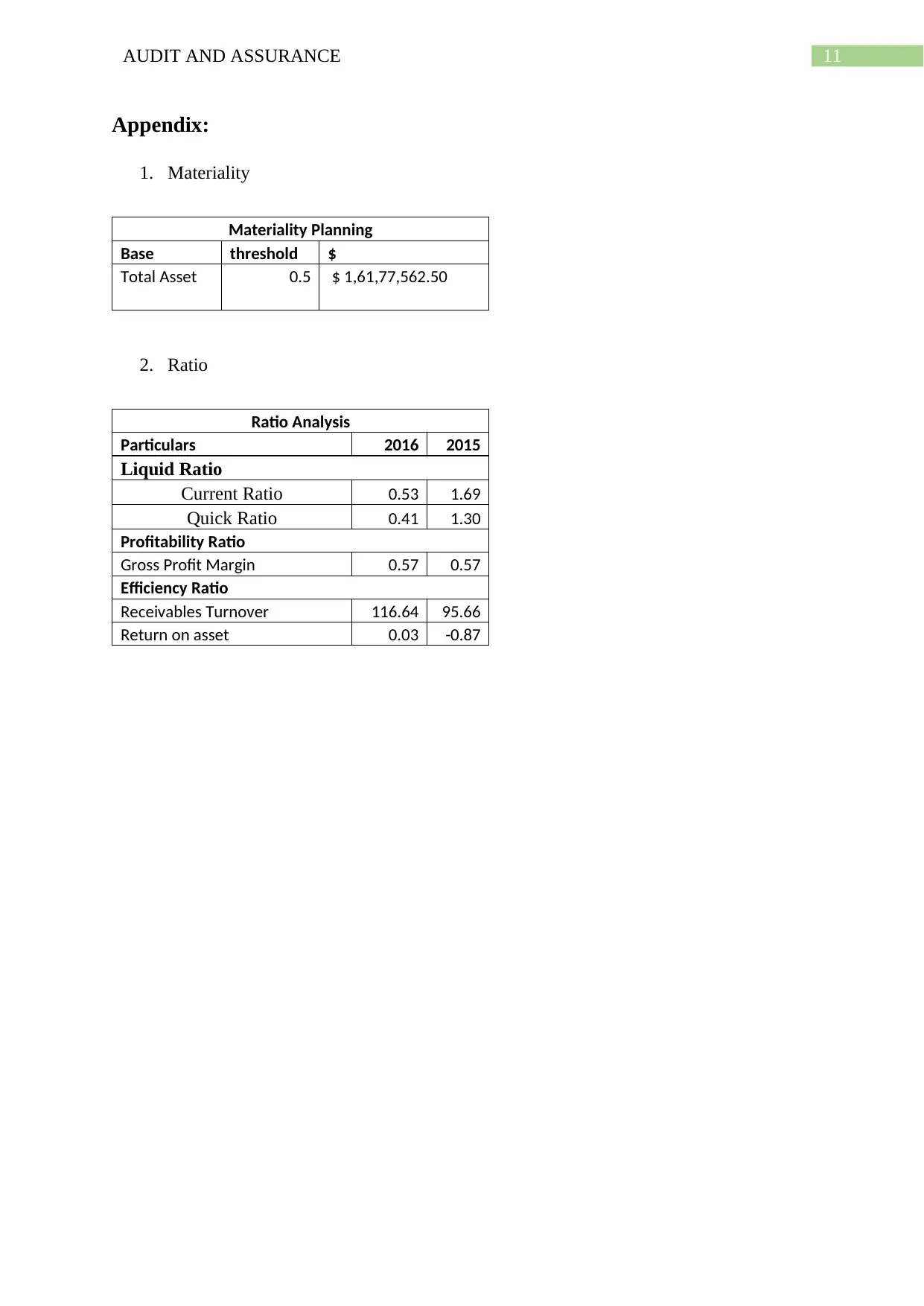

materiality resulted to $ 1,61,77,562.50 (Appendix-1)

Part B

Analytical Procedure

To review the financial statement of the company the frequently used too is ratio

analysis that is known as the analytical tool. The tool signifies the health of the financials of

the company. Same tool is used to review the financial health of Cloud 9 Pty Ltd. In this part

the risk that is involved with company is well discussed. In the case study some areas are

found to be under error zone as well as at risk. The steps to eliminate or decrease the error

that is found in the report is being discussed below.

Account

Head

Evaluation/ Analysis Auditing Risks Steps for Eliminating Risks

Accounts

Receivables

The quantity due to the

business by the clienteles

and consumers of the

corporation. The sum

The corporation

contract as well

as goods are

retailed

The business risk of the

company is high the auditor

need to carefully reevaluate

the amount of sales and the

Overall materiality is the opinion base for an auditor as because that helps auditor to

points out the importance factor that is presented in the statement as on whole. To the point

that manipulates the decision of an investor. It is assessed as portion of the preparation of the

audit as well as return to and reviewed all over the audit procedure. Usually, it will be

considered by applying a proportion to a selected standard such as Profit before Tax or net

assets. The auditor essentially prove decision in choosing the overall materiality level.

The overall materiality calculated for Cloud 9 Pty. Ltd is on Net asset because the

revenue earned by the company is basically from the asset of the company. The overall

materiality resulted to $ 1,61,77,562.50 (Appendix-1)

Part B

Analytical Procedure

To review the financial statement of the company the frequently used too is ratio

analysis that is known as the analytical tool. The tool signifies the health of the financials of

the company. Same tool is used to review the financial health of Cloud 9 Pty Ltd. In this part

the risk that is involved with company is well discussed. In the case study some areas are

found to be under error zone as well as at risk. The steps to eliminate or decrease the error

that is found in the report is being discussed below.

Account

Head

Evaluation/ Analysis Auditing Risks Steps for Eliminating Risks

Accounts

Receivables

The quantity due to the

business by the clienteles

and consumers of the

corporation. The sum

The corporation

contract as well

as goods are

retailed

The business risk of the

company is high the auditor

need to carefully reevaluate

the amount of sales and the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDIT AND ASSURANCE

characterize the sum for

which imbursement is so far

to be acknowledged by the

business. The Days of

Accounts Receivable for the

company is about 116.64

days.

underneath the

credit auctions

method to its

consumers. The

business risk of

the corporation is

high in this

regard.

amount of debtors it is able to

realize. The auditor requires

to cautiously identify

dissimilar modules of the

explanation and arrange for

materiality concerning the

similar.

Property

Assets

The ratio for return on

property assets indicates the

competence in the

consumption of the assets

of the corporation. The ratio

for the company in the year

2016 is about 0.3% that has

revealed expansion on or

after the previous year data

of about -0.87%

The important

risk related with

such kind of asset

group is

concerning the

assessment of

assets and

appropriately

identifying of

assets.

The significant step tangled in

this kind of reviewing would

be to decrease the auditing

difficulty by starting a mutual

economic head and recording

classification. The auditor

essentially also exploit all the

leased assets of the firm that

is categorized as functional

leases. The capitalization of

the similar would give an

accurate and reasonable

opinion of the accounts.

Marketing

Expenditures

The marketing expenditure

is the entire marketing

outlays for the Cloud 9. The

ratio as well as the

The risk related

through such

expenditure

would be

The stages to decrease the risk

related with such kind of

expenditure is to measure the

record for the expenditures

characterize the sum for

which imbursement is so far

to be acknowledged by the

business. The Days of

Accounts Receivable for the

company is about 116.64

days.

underneath the

credit auctions

method to its

consumers. The

business risk of

the corporation is

high in this

regard.

amount of debtors it is able to

realize. The auditor requires

to cautiously identify

dissimilar modules of the

explanation and arrange for

materiality concerning the

similar.

Property

Assets

The ratio for return on

property assets indicates the

competence in the

consumption of the assets

of the corporation. The ratio

for the company in the year

2016 is about 0.3% that has

revealed expansion on or

after the previous year data

of about -0.87%

The important

risk related with

such kind of asset

group is

concerning the

assessment of

assets and

appropriately

identifying of

assets.

The significant step tangled in

this kind of reviewing would

be to decrease the auditing

difficulty by starting a mutual

economic head and recording

classification. The auditor

essentially also exploit all the

leased assets of the firm that

is categorized as functional

leases. The capitalization of

the similar would give an

accurate and reasonable

opinion of the accounts.

Marketing

Expenditures

The marketing expenditure

is the entire marketing

outlays for the Cloud 9. The

ratio as well as the

The risk related

through such

expenditure

would be

The stages to decrease the risk

related with such kind of

expenditure is to measure the

record for the expenditures

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDIT AND ASSURANCE

advantage would be

premeditated by the output

the expenditure is

producing in the procedure

of proceeds.

concerning

appropriate

sorting as well as

recording of

expenditures by

the company.

done and investigate whether

the expenditures owed does

not become unsettled by the

business.

Part C

Remuneration

The remuneration of business directors as well as executives is a subject that has concerned

significant attention from stakeholders, commercial groups along with the extensive public.

Fears have been elevated over unnecessary compensation put into practise, principally as we

expression nearly unparalleled chaos in world-wide monetary including equity markets. The

present global monetary calamity has emphasised the position of confirming that

remuneration correspondences are suitably organised and do not recompense extreme risk

taking otherwise encourage business insatiability. The crunch has also highlighted the

essential to keep a healthy controlling outline that encourages photograph as well as

answerability on remuneration performs, and improved aligns the benefits of stockholders

and the public with the presentation along with payment structures of Australia’s corporate

directors as well as executive.

advantage would be

premeditated by the output

the expenditure is

producing in the procedure

of proceeds.

concerning

appropriate

sorting as well as

recording of

expenditures by

the company.

done and investigate whether

the expenditures owed does

not become unsettled by the

business.

Part C

Remuneration

The remuneration of business directors as well as executives is a subject that has concerned

significant attention from stakeholders, commercial groups along with the extensive public.

Fears have been elevated over unnecessary compensation put into practise, principally as we

expression nearly unparalleled chaos in world-wide monetary including equity markets. The

present global monetary calamity has emphasised the position of confirming that

remuneration correspondences are suitably organised and do not recompense extreme risk

taking otherwise encourage business insatiability. The crunch has also highlighted the

essential to keep a healthy controlling outline that encourages photograph as well as

answerability on remuneration performs, and improved aligns the benefits of stockholders

and the public with the presentation along with payment structures of Australia’s corporate

directors as well as executive.

8AUDIT AND ASSURANCE

Wesfarmers Woolworth Caltex

$2,000,000.00

$2,100,000.00

$2,200,000.00

$2,300,000.00

$2,400,000.00

$2,500,000.00

$2,600,000.00

Base Salary

Figure1: Salary structure of Wesfarmers, Woolworth and Caltex.

(Source: annual report)

Executives of the three companies mentioned above are in retail industry paid in cash and

bonus. In agreement to the section of 300A of the Corporations Act 2001.

Compensation

There are double main regions matter to corporate governance provisions that is

executive remuneration disclosure along with the payments at the dissolution level. The

Corporations Act essentials that the annual director’s statement include a remuneration

report, communicated in additional part. As per submission to the Corporations Act that are

related Corporations Regulations 2001, determination-manufacture conclusion payments are

protected at a entirety equivalent to twelve months of a director’s base income, from end to

end any closure reimbursement supplementary than the cap obliging stockholder

authorization. The Corporations Act situations that the managements of a business are to be

compensated on the terms as definite by the resolution. It is obligatory for the corporation to

reveal the payment sum paid when memberships cast 5 percent of vote in the common

meeting or there are hundred member existent in the meeting. In relation to Community

Wesfarmers Woolworth Caltex

$2,000,000.00

$2,100,000.00

$2,200,000.00

$2,300,000.00

$2,400,000.00

$2,500,000.00

$2,600,000.00

Base Salary

Figure1: Salary structure of Wesfarmers, Woolworth and Caltex.

(Source: annual report)

Executives of the three companies mentioned above are in retail industry paid in cash and

bonus. In agreement to the section of 300A of the Corporations Act 2001.

Compensation

There are double main regions matter to corporate governance provisions that is

executive remuneration disclosure along with the payments at the dissolution level. The

Corporations Act essentials that the annual director’s statement include a remuneration

report, communicated in additional part. As per submission to the Corporations Act that are

related Corporations Regulations 2001, determination-manufacture conclusion payments are

protected at a entirety equivalent to twelve months of a director’s base income, from end to

end any closure reimbursement supplementary than the cap obliging stockholder

authorization. The Corporations Act situations that the managements of a business are to be

compensated on the terms as definite by the resolution. It is obligatory for the corporation to

reveal the payment sum paid when memberships cast 5 percent of vote in the common

meeting or there are hundred member existent in the meeting. In relation to Community

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDIT AND ASSURANCE

Company further than rational imbursement of compensation shareholders authorization is

desirable. The compensation of Woolworths is on basis of self-insurance were concerning the

provision of identity-covered risk that is connected to the approximation of obligation that is

connected to the employees counting the entitlements and recompense of accountability

(Woolworthsgroup.com.au. 2019) An arduous bond is an settlement in this agreement the

predictable value of conference the accountabilities below the arrangement beyond the

financial benefit expectable to be recognised under it. The inevitable beneath a settlement

duplicate the least possible net custody of retreating from the arrangement hat is the inferior

of the value of filling it besides either recompense or penalties rising from dissatisfaction to

achieve it (Woolworthsgroup.com.au. 2019).

Company further than rational imbursement of compensation shareholders authorization is

desirable. The compensation of Woolworths is on basis of self-insurance were concerning the

provision of identity-covered risk that is connected to the approximation of obligation that is

connected to the employees counting the entitlements and recompense of accountability

(Woolworthsgroup.com.au. 2019) An arduous bond is an settlement in this agreement the

predictable value of conference the accountabilities below the arrangement beyond the

financial benefit expectable to be recognised under it. The inevitable beneath a settlement

duplicate the least possible net custody of retreating from the arrangement hat is the inferior

of the value of filling it besides either recompense or penalties rising from dissatisfaction to

achieve it (Woolworthsgroup.com.au. 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDIT AND ASSURANCE

Reference

(2019). Microsites.caltex.com.au. Retrieved 27 January 2019, from

http://microsites.caltex.com.au/annualreports/2017/documents/17168_CALTEX_AS

X.pdf

(2019). Wesfarmers.com.au. Retrieved 27 January 2019, from

https://www.wesfarmers.com.au/docs/default-source/asx-announcements/2018-

annual-report.pdf?sfvrsn=0

(2019). Woolworthsgroup.com.au. Retrieved 27 January 2019, from

https://www.woolworthsgroup.com.au/icms_docs/195396_annual-report-2018.pdf

Australia.gov.au. (2019). Australian Accounting Standards Board | australia.gov.au. [online]

Available at: https://www.australia.gov.au/directories/australia/aasb [Accessed 26 Jan.

2019].

Houston, R.W., Peters, M.F. & Pratt, J.H., 1999. The audit risk model, business risk and

audit-planning decisions. The Accounting Review, 74(3), pp.281-298.

Icac.nsw.gov.au. (2019). [online] Available at: https://www.icac.nsw.gov.au/images/Ricco

%20Public%20Website/Exhibit%20R97.pdf [Accessed 26 Jan. 2019].

Icaew.com. (2019). [online] Available at:

https://www.icaew.com/-/media/corporate/files/technical/iaa/materiality-in-the-audit-

of-financial-statements.ashx [Accessed 25 Jan. 2019].

Johnstone, K., Gramling, A. & Rittenberg, L.E., 2013. Auditing: a risk-based approach to

conducting a quality audit. Cengage learning.

Knechel, W.R.& Salterio, S.E., 2016. Auditing: Assurance and risk. Routledge.

Reference

(2019). Microsites.caltex.com.au. Retrieved 27 January 2019, from

http://microsites.caltex.com.au/annualreports/2017/documents/17168_CALTEX_AS

X.pdf

(2019). Wesfarmers.com.au. Retrieved 27 January 2019, from

https://www.wesfarmers.com.au/docs/default-source/asx-announcements/2018-

annual-report.pdf?sfvrsn=0

(2019). Woolworthsgroup.com.au. Retrieved 27 January 2019, from

https://www.woolworthsgroup.com.au/icms_docs/195396_annual-report-2018.pdf

Australia.gov.au. (2019). Australian Accounting Standards Board | australia.gov.au. [online]

Available at: https://www.australia.gov.au/directories/australia/aasb [Accessed 26 Jan.

2019].

Houston, R.W., Peters, M.F. & Pratt, J.H., 1999. The audit risk model, business risk and

audit-planning decisions. The Accounting Review, 74(3), pp.281-298.

Icac.nsw.gov.au. (2019). [online] Available at: https://www.icac.nsw.gov.au/images/Ricco

%20Public%20Website/Exhibit%20R97.pdf [Accessed 26 Jan. 2019].

Icaew.com. (2019). [online] Available at:

https://www.icaew.com/-/media/corporate/files/technical/iaa/materiality-in-the-audit-

of-financial-statements.ashx [Accessed 25 Jan. 2019].

Johnstone, K., Gramling, A. & Rittenberg, L.E., 2013. Auditing: a risk-based approach to

conducting a quality audit. Cengage learning.

Knechel, W.R.& Salterio, S.E., 2016. Auditing: Assurance and risk. Routledge.

11AUDIT AND ASSURANCE

Appendix:

1. Materiality

Materiality Planning

Base threshold $

Total Asset 0.5 $ 1,61,77,562.50

2. Ratio

Ratio Analysis

Particulars 2016 2015

Liquid Ratio

Current Ratio 0.53 1.69

Quick Ratio 0.41 1.30

Profitability Ratio

Gross Profit Margin 0.57 0.57

Efficiency Ratio

Receivables Turnover 116.64 95.66

Return on asset 0.03 -0.87

Appendix:

1. Materiality

Materiality Planning

Base threshold $

Total Asset 0.5 $ 1,61,77,562.50

2. Ratio

Ratio Analysis

Particulars 2016 2015

Liquid Ratio

Current Ratio 0.53 1.69

Quick Ratio 0.41 1.30

Profitability Ratio

Gross Profit Margin 0.57 0.57

Efficiency Ratio

Receivables Turnover 116.64 95.66

Return on asset 0.03 -0.87

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.