Audit Case Study: Assessing Materiality and Business Risks at Cloud 9

VerifiedAdded on 2023/04/25

|12

|1896

|301

Case Study

AI Summary

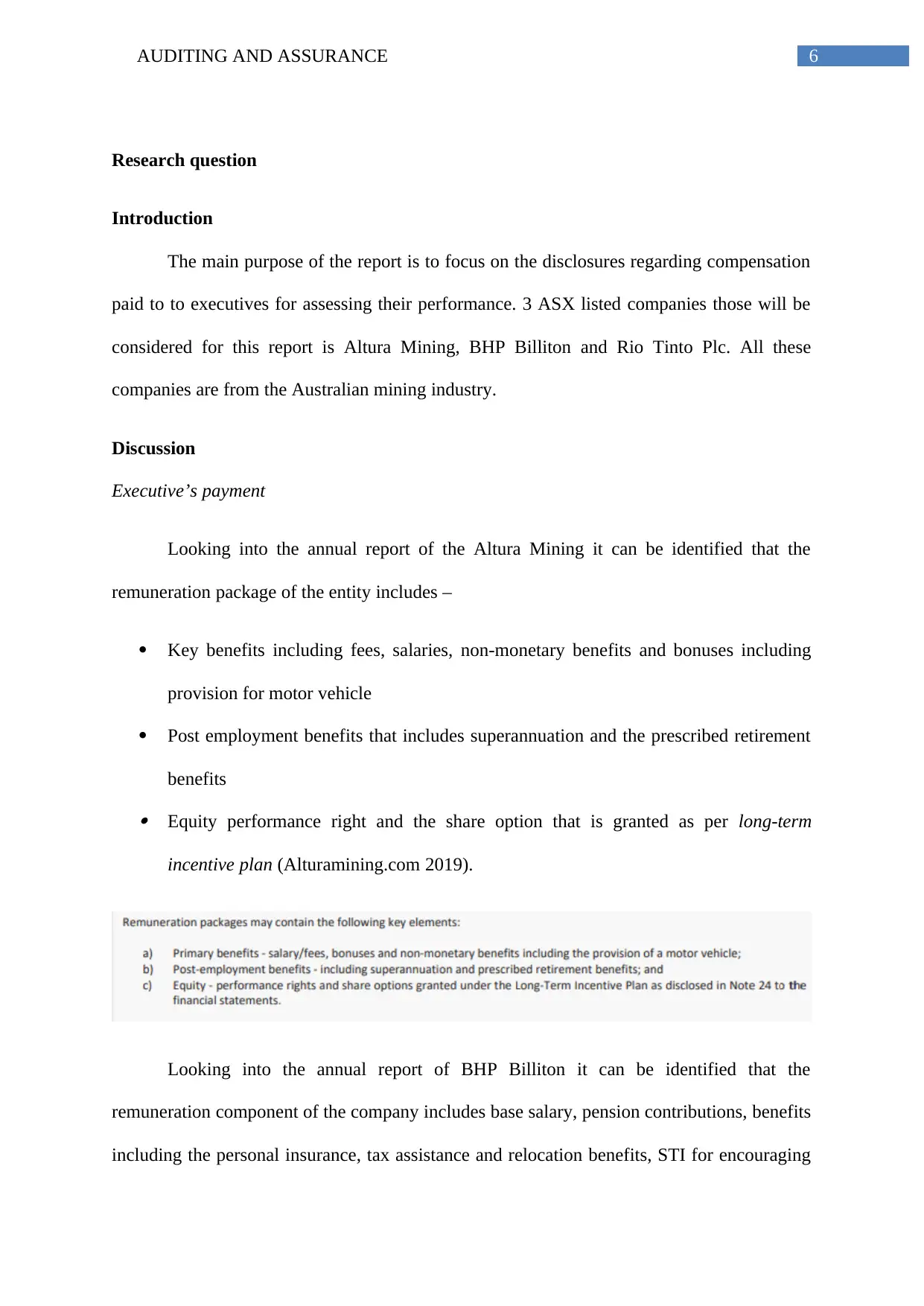

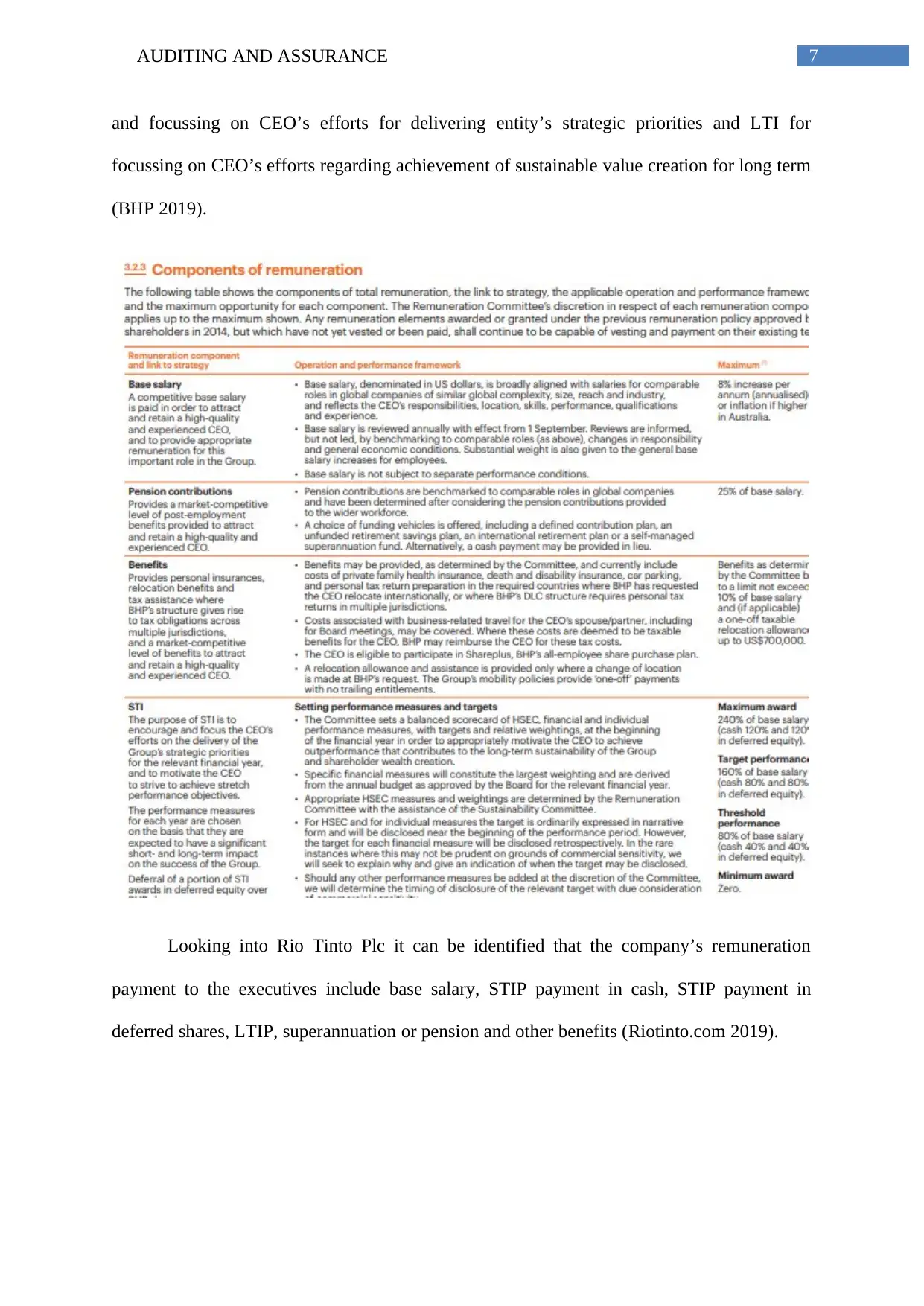

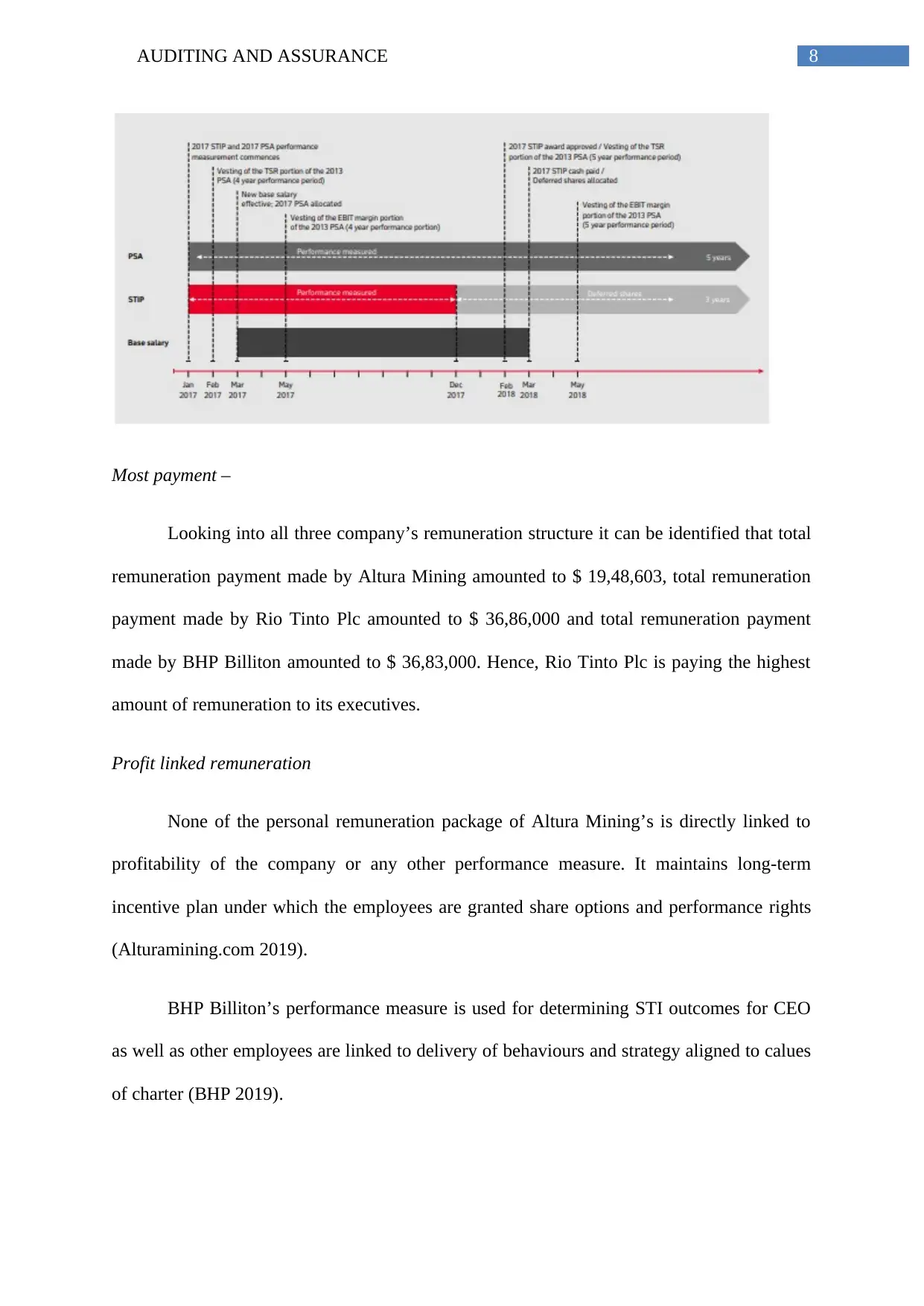

This case study provides a comprehensive analysis of the auditing and assurance processes for Cloud 9 Pty Ltd, a company engaged in the wholesale of athletic shoes. The study begins by determining the appropriate planning materiality (PM) base, suggesting total assets due to the significant impact of disposal proceeds on profitability. It then delves into analytical procedures, including ratio analysis to assess business risks, focusing on profitability, liquidity, efficiency, and solvency ratios. Special emphasis is placed on cash and trade receivables due to their susceptibility to fraud. Furthermore, the report examines executive compensation disclosures in three ASX-listed mining companies (Altura Mining, BHP Billiton, and Rio Tinto Plc), comparing remuneration structures and their links to company performance. The analysis reveals that while some companies have direct links between executive pay and profitability/share price, others rely on long-term incentive plans. Desklib offers a platform for students to access similar solved assignments and past papers.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.