Comprehensive Auditing and Assurance Report on DIPL Case Study

VerifiedAdded on 2020/03/02

|10

|2560

|137

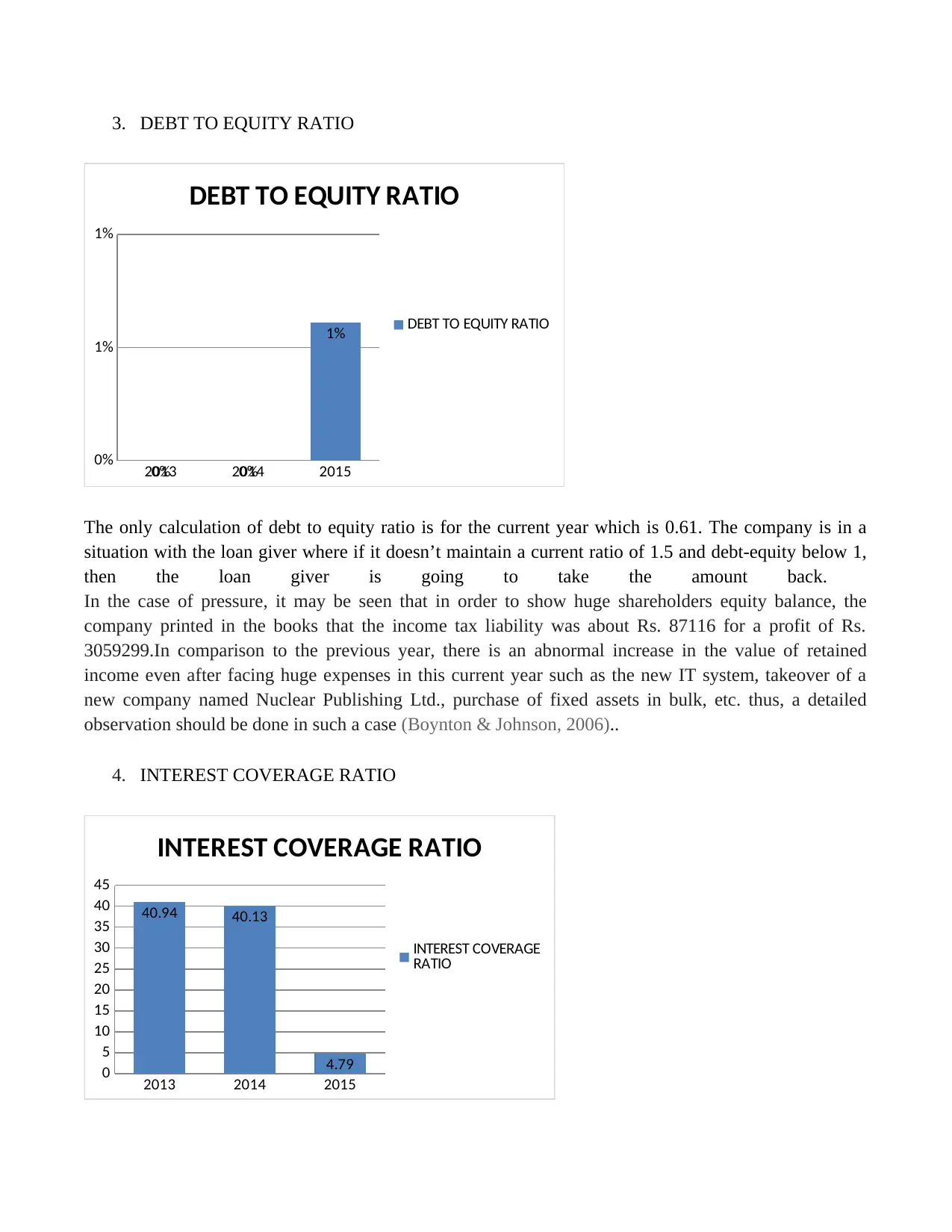

Report

AI Summary

This report presents an analysis of an auditing and assurance assignment, focusing on the DIPL case study. The report begins by outlining the analytical procedures employed by auditors to form an overall opinion on financial statements, emphasizing the importance of distinguishing between financial and non-financial information, and highlighting the use of ratios like current ratio, quick ratio, return on equity, and debt-to-equity ratio. The analysis reveals potential issues, such as inconsistencies in income tax calculations and unusual changes in interest coverage ratios. The report then delves into the dangers of material misstatement at both financial statement and assertion levels, discussing the valuation of inventory and the impact of pressure within the entity. The final section addresses the auditor's responsibility in ensuring the fairness of financial statements, identifying fraud risk factors and specific instances of fraud, such as the recognition of storage fees and the adoption of a new IT system, which may impact the audit report. The report provides a comprehensive overview of the audit process and financial analysis, including the identification of potential fraudulent activities.

AUDITING AND ASSURANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

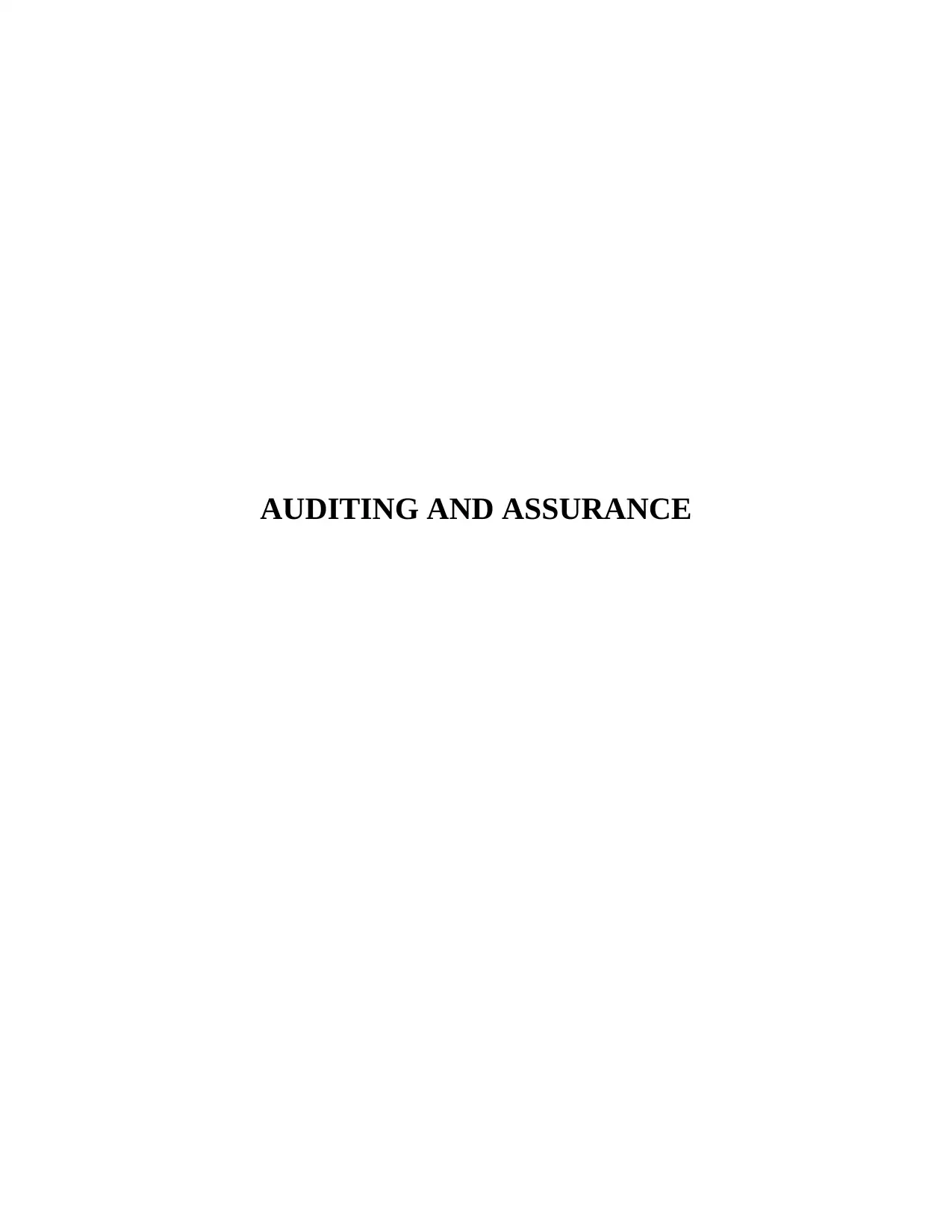

ANSWER 1:

Analytical procedures are the procedures performed by the auditor at the end of the year in order to help

the auditor create overall opinion regarding financial statements in his report. It is done to ensure that the

financial statements are in the perspective of the firm’s auditor. It helps to distinguish between financial

and non-financial information, and also to differentiate between this year's and the previous year’s

financial information (Basu, 2009). If any inconsistency or any physical changes are seen, then the

auditors may interrogate with the administration or those charged for it or proceed with the

administration of auditing charges in the audit process so that the detailed study of their observations is

inconsistent. According to the DIPL case study, the main fundamental ratios are calculated for the

analytical procedure so that the planning can be prepared based on this approach: -

1. CURRENTRATIO

2013 2014 2015

1.38

1.4

1.42

1.44

1.46

1.48

1.5

1.52

1.42

1.47

1.5

CURRENT RATIO

CURRENT RATIO

2013 2014 2015

0.76

0.78

0.8

0.82

0.84

0.86

0.88

0.9

0.92

0.94

0.96

0.830000000000

001

0.940000000000

001

0.850000000000

001

QUICK RATIO

QUICK RATIO

Analytical procedures are the procedures performed by the auditor at the end of the year in order to help

the auditor create overall opinion regarding financial statements in his report. It is done to ensure that the

financial statements are in the perspective of the firm’s auditor. It helps to distinguish between financial

and non-financial information, and also to differentiate between this year's and the previous year’s

financial information (Basu, 2009). If any inconsistency or any physical changes are seen, then the

auditors may interrogate with the administration or those charged for it or proceed with the

administration of auditing charges in the audit process so that the detailed study of their observations is

inconsistent. According to the DIPL case study, the main fundamental ratios are calculated for the

analytical procedure so that the planning can be prepared based on this approach: -

1. CURRENTRATIO

2013 2014 2015

1.38

1.4

1.42

1.44

1.46

1.48

1.5

1.52

1.42

1.47

1.5

CURRENT RATIO

CURRENT RATIO

2013 2014 2015

0.76

0.78

0.8

0.82

0.84

0.86

0.88

0.9

0.92

0.94

0.96

0.830000000000

001

0.940000000000

001

0.850000000000

001

QUICK RATIO

QUICK RATIO

The current ratio of the current year is 1.50, comparing to the previous years, which is 1.42 for

2013 and 1.47 for 2014, which indicates favorable conditions because the current ratio indicates

the liquidity of the company. However, the true sign of the liquidity of company is a quick ratio,

because the amount does not contain inventories which are done in order ensure that cash

available in the form of goods cannot be immediately converted into cash. However, the current

year's quick ratio is 0.85, which is less than that of the previous year 2014, which is 0.94, that

means the real cash is not available very much in hand if in this case, the company have to clear

its short-term transactions (Blank, 2014). This is not a good sign because the percentage of cash

in hand has decreased significantly in comparison to last year, which is an estimate of unusual

proceedings or company expenses than last year.

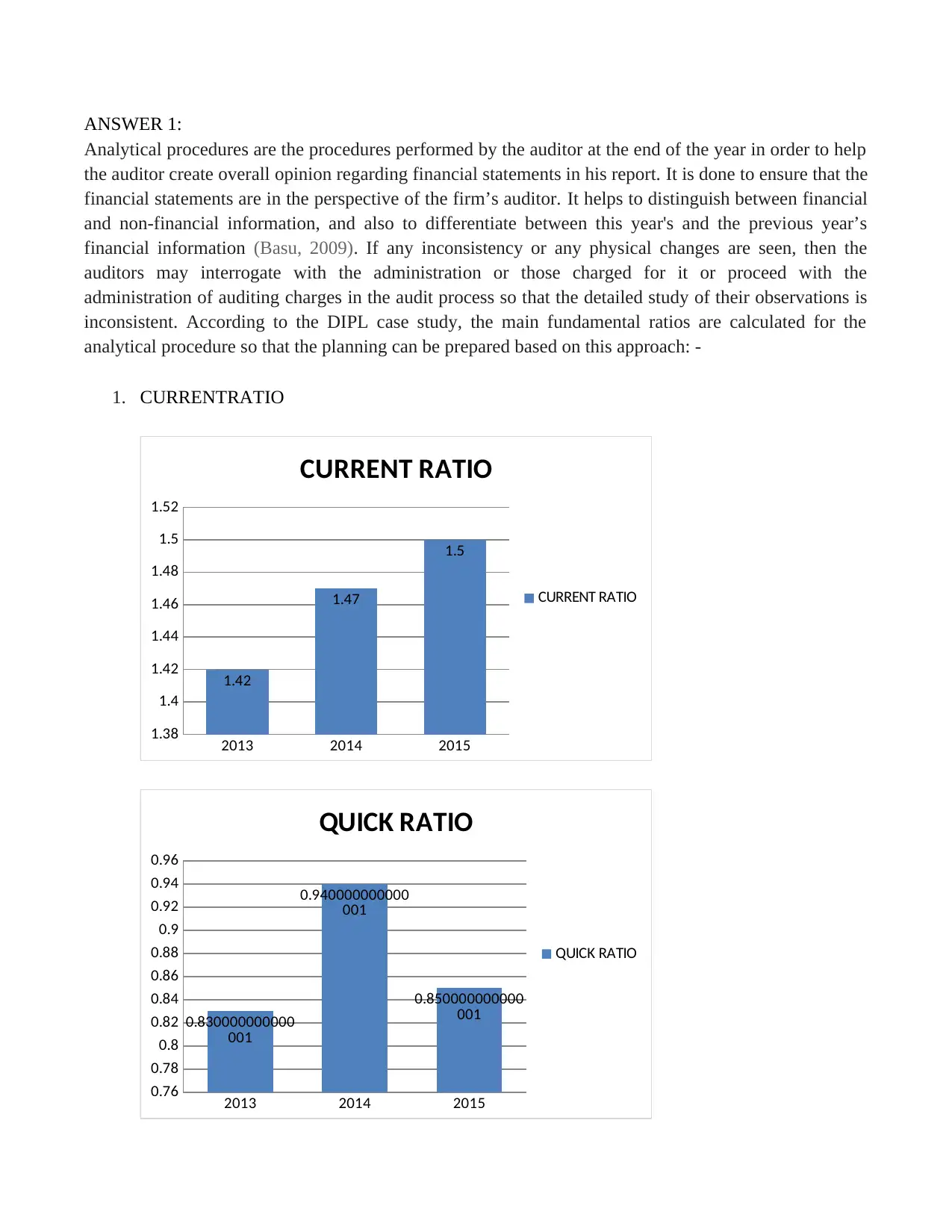

2. RETURN ON EQUITY

2013 2014 2015

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

25.78%

21.25%

24.26%

RETURN ON EQUITY

RETURN ON EQUITY

According to Equity percentage and Return on EPS calculation, profit before tax is Rs. 3059299

in 2015 but income tax is showing the amount of money as Rs. 87116 which is not possible

without any unnecessary change. It can also be done to show high net earnings as the EPS for the

current year is of about Rs. 132 but for the previous years, the EPS was as low as Rs. 104.85 for

2013 and Rs. 101.84 for the year 2014. It is necessary to evaluate this type calculation of PAT

(Profit After Tax) because the income tax calculation is very low, which can be used to display

high EPS so that the company can fulfill their sole objective of earning a profit by winning the

investor's trust. Also, these calculations of net earnings can be made high so that their return on

equity percentage increases as compared to the previous years because it states the amount of

return the investors receive on their investment.

2013 and 1.47 for 2014, which indicates favorable conditions because the current ratio indicates

the liquidity of the company. However, the true sign of the liquidity of company is a quick ratio,

because the amount does not contain inventories which are done in order ensure that cash

available in the form of goods cannot be immediately converted into cash. However, the current

year's quick ratio is 0.85, which is less than that of the previous year 2014, which is 0.94, that

means the real cash is not available very much in hand if in this case, the company have to clear

its short-term transactions (Blank, 2014). This is not a good sign because the percentage of cash

in hand has decreased significantly in comparison to last year, which is an estimate of unusual

proceedings or company expenses than last year.

2. RETURN ON EQUITY

2013 2014 2015

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

25.78%

21.25%

24.26%

RETURN ON EQUITY

RETURN ON EQUITY

According to Equity percentage and Return on EPS calculation, profit before tax is Rs. 3059299

in 2015 but income tax is showing the amount of money as Rs. 87116 which is not possible

without any unnecessary change. It can also be done to show high net earnings as the EPS for the

current year is of about Rs. 132 but for the previous years, the EPS was as low as Rs. 104.85 for

2013 and Rs. 101.84 for the year 2014. It is necessary to evaluate this type calculation of PAT

(Profit After Tax) because the income tax calculation is very low, which can be used to display

high EPS so that the company can fulfill their sole objective of earning a profit by winning the

investor's trust. Also, these calculations of net earnings can be made high so that their return on

equity percentage increases as compared to the previous years because it states the amount of

return the investors receive on their investment.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

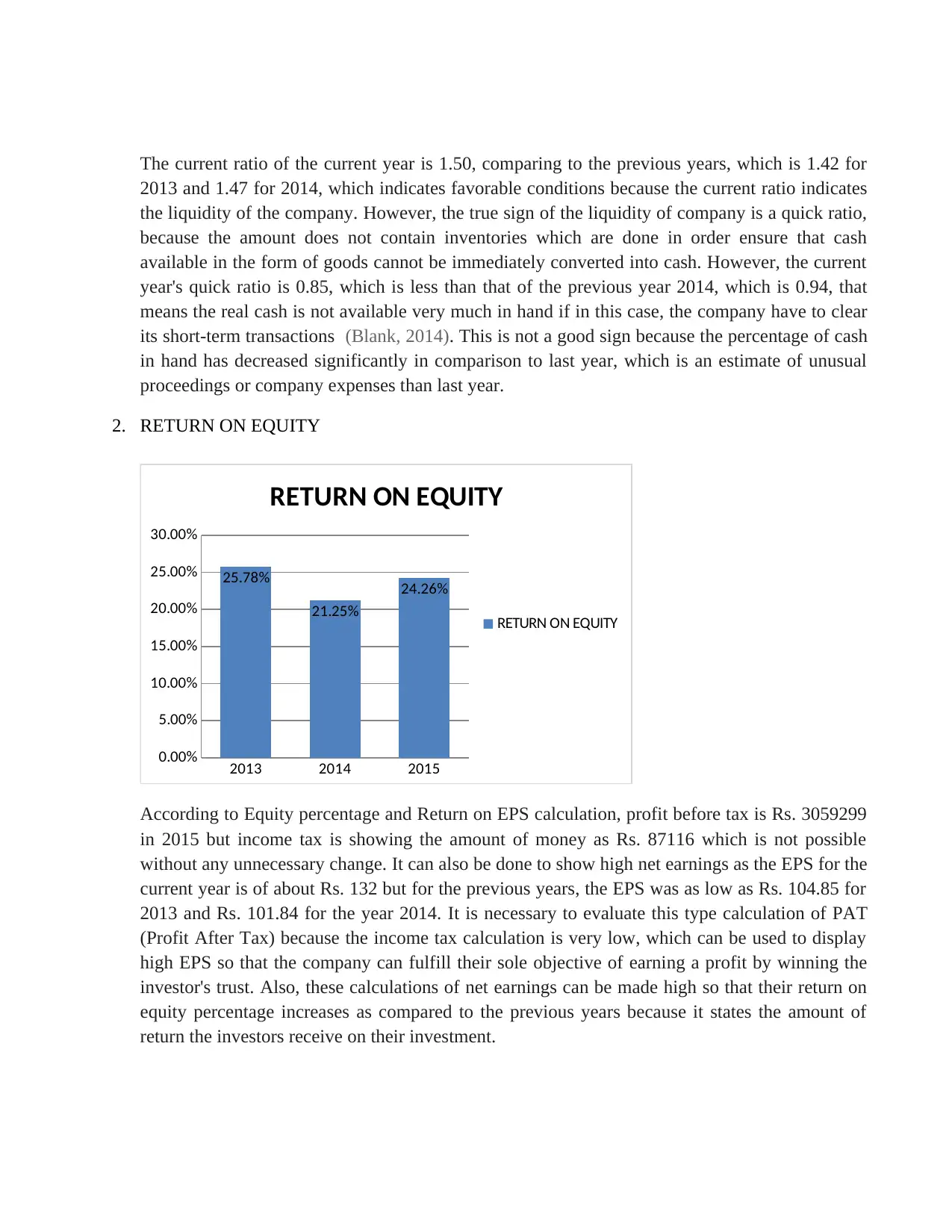

3. DEBT TO EQUITY RATIO

2013 2014 2015

0%

1%

1%

0% 0%

1%

DEBT TO EQUITY RATIO

DEBT TO EQUITY RATIO

The only calculation of debt to equity ratio is for the current year which is 0.61. The company is in a

situation with the loan giver where if it doesn’t maintain a current ratio of 1.5 and debt-equity below 1,

then the loan giver is going to take the amount back.

In the case of pressure, it may be seen that in order to show huge shareholders equity balance, the

company printed in the books that the income tax liability was about Rs. 87116 for a profit of Rs.

3059299.In comparison to the previous year, there is an abnormal increase in the value of retained

income even after facing huge expenses in this current year such as the new IT system, takeover of a

new company named Nuclear Publishing Ltd., purchase of fixed assets in bulk, etc. thus, a detailed

observation should be done in such a case (Boynton & Johnson, 2006)..

4. INTEREST COVERAGE RATIO

2013 2014 2015

0

5

10

15

20

25

30

35

40

45

40.94 40.13

4.79

INTEREST COVERAGE RATIO

INTEREST COVERAGE

RATIO

2013 2014 2015

0%

1%

1%

0% 0%

1%

DEBT TO EQUITY RATIO

DEBT TO EQUITY RATIO

The only calculation of debt to equity ratio is for the current year which is 0.61. The company is in a

situation with the loan giver where if it doesn’t maintain a current ratio of 1.5 and debt-equity below 1,

then the loan giver is going to take the amount back.

In the case of pressure, it may be seen that in order to show huge shareholders equity balance, the

company printed in the books that the income tax liability was about Rs. 87116 for a profit of Rs.

3059299.In comparison to the previous year, there is an abnormal increase in the value of retained

income even after facing huge expenses in this current year such as the new IT system, takeover of a

new company named Nuclear Publishing Ltd., purchase of fixed assets in bulk, etc. thus, a detailed

observation should be done in such a case (Boynton & Johnson, 2006)..

4. INTEREST COVERAGE RATIO

2013 2014 2015

0

5

10

15

20

25

30

35

40

45

40.94 40.13

4.79

INTEREST COVERAGE RATIO

INTEREST COVERAGE

RATIO

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In the ratio of interest coverage, we observe a drastic reduction in interest rates by the company, which

accounts from 41% to 5%, which may be because of the huge expenditures the company is facing.

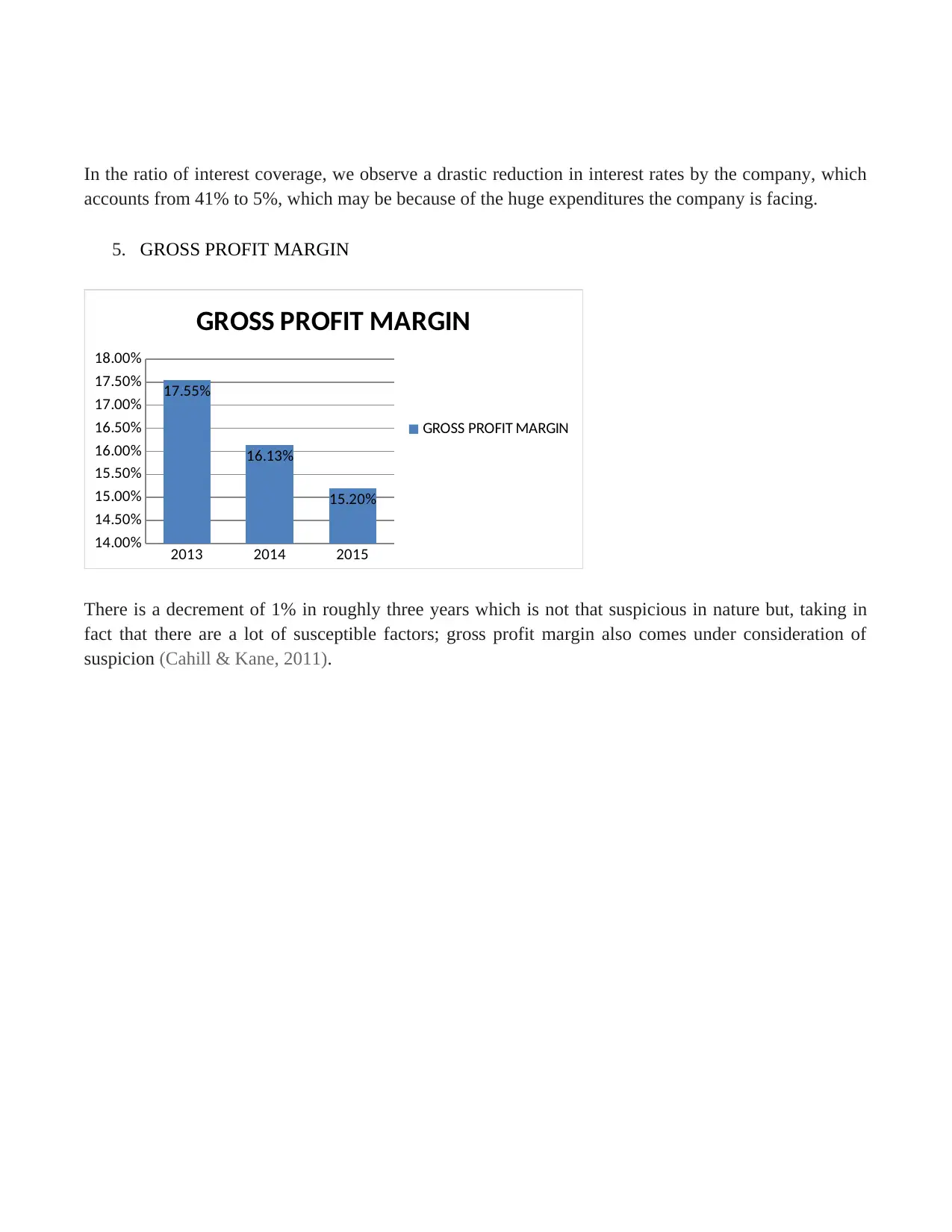

5. GROSS PROFIT MARGIN

2013 2014 2015

14.00%

14.50%

15.00%

15.50%

16.00%

16.50%

17.00%

17.50%

18.00%

17.55%

16.13%

15.20%

GROSS PROFIT MARGIN

GROSS PROFIT MARGIN

There is a decrement of 1% in roughly three years which is not that suspicious in nature but, taking in

fact that there are a lot of susceptible factors; gross profit margin also comes under consideration of

suspicion (Cahill & Kane, 2011).

accounts from 41% to 5%, which may be because of the huge expenditures the company is facing.

5. GROSS PROFIT MARGIN

2013 2014 2015

14.00%

14.50%

15.00%

15.50%

16.00%

16.50%

17.00%

17.50%

18.00%

17.55%

16.13%

15.20%

GROSS PROFIT MARGIN

GROSS PROFIT MARGIN

There is a decrement of 1% in roughly three years which is not that suspicious in nature but, taking in

fact that there are a lot of susceptible factors; gross profit margin also comes under consideration of

suspicion (Cahill & Kane, 2011).

ANSWER 2:

The danger of material misstatement refers to the risk that the financial statements have been erased or a

physical change may have occurred. The auditor has to detect the risk of physical mistake at two levels:

1. At the financial level:

Here, the identity of risk is completely relative to financial statements as a whole because it

covers risks such as incompetent control system, lack of capital required to continue the

business, unusual pressures, unusual transactions, hasty decisions, etc.

2. At the Assertion level: Here, two types of risks are involved - The underlying risk that refers to

the risk is caused by errors or fraud which are physically false and may be stated individually or

in aggregate and have a material effect other than the failures of control. Control risk refers to the

risk that indicates physical misconceptions existing in the books because it cannot be separated

or stopped to enter in the accounts of business books by the internal control system, which in

turn indicates the risk due to the failure of controls in the firm (GUPTA., 2016).

According to the given question, the two aspects contained in DIPL can be described in the following

two points:

Valuation of Inventory:

The Company evaluates raw materials according to the weighted average method. Now, the

valuation of the inventory directly affects the profitability of the company, because the incorrect

evaluation overstates or closing stock gets worse, resulting in higher or lower profits (PAVAN,

2014). For example, the closing stock is 20 units, whose opening stock is.100 units of Rs. 1000

and purchase 200 units of Rs.3000. After the average method, the stock valuation is Rs. 13.34

per unit, that is the closing stock of Rs. 267 but in fact, it is the purchase of 20 units where the

cost of one unit is Rs. 15 and so, the valuation value of the closing stock should be Rs. 300.

Thus, by following the average method, the lower closing stock price will be shown that will

lead to a decrease in overall profit. However, in the board meeting of June 2015, the company

had decided to change its valuation method based on the FIFO basis, which points to the cases

that it is trying to hide the money earned out of the wrong valuation of inventory. In addition, by

doing so, there is an increase of about 56% in inventory value, which indicates the high finishing

stock value as compared to the 2014 data, which shows high returns and thus shows the

company's better and stronger position which will help it for smooth future funding or to win the

trust of the investor or to satisfy the debtor that the company's earnings are a satisfactory

(Horngren, 2017).

The danger of material misstatement refers to the risk that the financial statements have been erased or a

physical change may have occurred. The auditor has to detect the risk of physical mistake at two levels:

1. At the financial level:

Here, the identity of risk is completely relative to financial statements as a whole because it

covers risks such as incompetent control system, lack of capital required to continue the

business, unusual pressures, unusual transactions, hasty decisions, etc.

2. At the Assertion level: Here, two types of risks are involved - The underlying risk that refers to

the risk is caused by errors or fraud which are physically false and may be stated individually or

in aggregate and have a material effect other than the failures of control. Control risk refers to the

risk that indicates physical misconceptions existing in the books because it cannot be separated

or stopped to enter in the accounts of business books by the internal control system, which in

turn indicates the risk due to the failure of controls in the firm (GUPTA., 2016).

According to the given question, the two aspects contained in DIPL can be described in the following

two points:

Valuation of Inventory:

The Company evaluates raw materials according to the weighted average method. Now, the

valuation of the inventory directly affects the profitability of the company, because the incorrect

evaluation overstates or closing stock gets worse, resulting in higher or lower profits (PAVAN,

2014). For example, the closing stock is 20 units, whose opening stock is.100 units of Rs. 1000

and purchase 200 units of Rs.3000. After the average method, the stock valuation is Rs. 13.34

per unit, that is the closing stock of Rs. 267 but in fact, it is the purchase of 20 units where the

cost of one unit is Rs. 15 and so, the valuation value of the closing stock should be Rs. 300.

Thus, by following the average method, the lower closing stock price will be shown that will

lead to a decrease in overall profit. However, in the board meeting of June 2015, the company

had decided to change its valuation method based on the FIFO basis, which points to the cases

that it is trying to hide the money earned out of the wrong valuation of inventory. In addition, by

doing so, there is an increase of about 56% in inventory value, which indicates the high finishing

stock value as compared to the 2014 data, which shows high returns and thus shows the

company's better and stronger position which will help it for smooth future funding or to win the

trust of the investor or to satisfy the debtor that the company's earnings are a satisfactory

(Horngren, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Unusual Pressure within the entity:

There are a lot of factors within the unit which indicates that the company is under unusual

pressure or a certain type of error or fraud, which the company is trying to hide from its people.

Such pressures can be described in the following points:

In January 2015, the company appointed a new internal audit team, while its books were closed

in June. This is doubtful because, in the middle of the year, such a step is adopted as it may have

been adopted to identify fraudulent activities that management already has an intuition about.

Also, its CEO changed in the same month. Thus such changes have to be further investigated by

the management and with the previous CEO (Griffin, 2009).

A loan of Rs. 7.5 million from BDO finance was taken from the company. It spent a huge

amount on the property but at the same time, it adopted a new IT system in the unit and even

took a company named Nuclear Publishing Ltd., despite the fact that the purchase price of the

plant and equipment already exceeds the load amount. Thus, the purpose of the loan and

expenditure made by the company is not appropriate. Also, it points to the unusual pressure that

some fraud risk factors do exist (Pitt, 2014).

There are a lot of factors within the unit which indicates that the company is under unusual

pressure or a certain type of error or fraud, which the company is trying to hide from its people.

Such pressures can be described in the following points:

In January 2015, the company appointed a new internal audit team, while its books were closed

in June. This is doubtful because, in the middle of the year, such a step is adopted as it may have

been adopted to identify fraudulent activities that management already has an intuition about.

Also, its CEO changed in the same month. Thus such changes have to be further investigated by

the management and with the previous CEO (Griffin, 2009).

A loan of Rs. 7.5 million from BDO finance was taken from the company. It spent a huge

amount on the property but at the same time, it adopted a new IT system in the unit and even

took a company named Nuclear Publishing Ltd., despite the fact that the purchase price of the

plant and equipment already exceeds the load amount. Thus, the purpose of the loan and

expenditure made by the company is not appropriate. Also, it points to the unusual pressure that

some fraud risk factors do exist (Pitt, 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ANSWER 3:

This is the responsibility of the auditor to follow their duties in such a way that to ensure proper

assurance that the financial statements are given to be true and fair, and also that the information given

in the statement is free from any misconstrued error and fraud (Hooks, 2011). Fraud is a legal

determination theory and the auditor is expected to not have enough expertise to make such legal

determination. Instead, the auditors are considered with the determination of the misunderstandings of

two things wrongly arising from it: First, from fraudulent financial reporting and secondly, by

misappropriations of assets.

Fraud risk factors are such situations that are generally present where there is a fraud. These are the

following conditions which may encourage a fraud risk factor:

i. Management or workers are encouraged to have an incentive or under pressure;

ii. Things are adequate to provide opportunity for conducting fraud; and

iii. Fraudsters involved are capable of rationalizing fraudulent activities carried out by them.

According to the study of the case given by DIPL, two identified frauds due to which the financial

reporting of the company is due, also for which the company is considered as an anesthetic and it has an

effect on the performance of audit report are as follows (Knechel, Salterio & Ballou, 2017):

Recognition of storage fees from 'E-book facilities’: The company used to charge an annual

"storage fee" to the publishers to keep their e-books on its website.

However, these storage charges were due 12 months in advance and were fully accredited in the

month of their invoice, despite the fact that they are being recognized in advance, thus,

misinterpretation of accounting theory. The revenue recognition concept says that revenue is to

be recognized only when it is being earned, which means either goods have been provided or

services have been performed (Messier, 2016). Thus, without really providing a service or

without actually completing the service period, revenue for such months will not be considered

and will be treated as 'advance from the publishers' under current liabilities. However, the

meeting of the board came to the conclusion of income identification only after the completion

of the transaction. However, due to the internal audit team, this change had come and it may

have to be covered for previous wrong beliefs because of which higher revenue is shown in the

market so that it can show a strong position in the market.

Adoption of New IT System:

The Company had put excessive pressure on the IT department to set up new computerized

systems in June 2015 when it closes its accounts. There was no clue at all about the fact that the

employees are properly trained for their work, or whether the new system has been tested before

This is the responsibility of the auditor to follow their duties in such a way that to ensure proper

assurance that the financial statements are given to be true and fair, and also that the information given

in the statement is free from any misconstrued error and fraud (Hooks, 2011). Fraud is a legal

determination theory and the auditor is expected to not have enough expertise to make such legal

determination. Instead, the auditors are considered with the determination of the misunderstandings of

two things wrongly arising from it: First, from fraudulent financial reporting and secondly, by

misappropriations of assets.

Fraud risk factors are such situations that are generally present where there is a fraud. These are the

following conditions which may encourage a fraud risk factor:

i. Management or workers are encouraged to have an incentive or under pressure;

ii. Things are adequate to provide opportunity for conducting fraud; and

iii. Fraudsters involved are capable of rationalizing fraudulent activities carried out by them.

According to the study of the case given by DIPL, two identified frauds due to which the financial

reporting of the company is due, also for which the company is considered as an anesthetic and it has an

effect on the performance of audit report are as follows (Knechel, Salterio & Ballou, 2017):

Recognition of storage fees from 'E-book facilities’: The company used to charge an annual

"storage fee" to the publishers to keep their e-books on its website.

However, these storage charges were due 12 months in advance and were fully accredited in the

month of their invoice, despite the fact that they are being recognized in advance, thus,

misinterpretation of accounting theory. The revenue recognition concept says that revenue is to

be recognized only when it is being earned, which means either goods have been provided or

services have been performed (Messier, 2016). Thus, without really providing a service or

without actually completing the service period, revenue for such months will not be considered

and will be treated as 'advance from the publishers' under current liabilities. However, the

meeting of the board came to the conclusion of income identification only after the completion

of the transaction. However, due to the internal audit team, this change had come and it may

have to be covered for previous wrong beliefs because of which higher revenue is shown in the

market so that it can show a strong position in the market.

Adoption of New IT System:

The Company had put excessive pressure on the IT department to set up new computerized

systems in June 2015 when it closes its accounts. There was no clue at all about the fact that the

employees are properly trained for their work, or whether the new system has been tested before

properly or not (Ramaswamy, 2015). It just wanted to change its existing system, due to which

transactions were being transferred from one system to another because of which many

transactions were lost in this process. This action of management indicates the existence of fraud

risk factors such as some fraudulent activity has been initiated and with the fear of internal audit

teams which will definitely be able to rectify it, the replacement of the entire system with new IT

system was management’s idea so that they can skip the transactions and declare it to transaction

lost due to less knowledge or incapability of accounting system, IT department and the

employees. In addition, the same action acts as an opportunity for employees or other members,

who can take advantage of messed up accounts and thus, misinterpret the cash balances or

conduct an activity which may help him to earn personal money on account of the firm and after

all this blame the department for being so careless regarding the transfer of accounts from old

system to the new accounting system (Khan and Jain, 2013).

transactions were being transferred from one system to another because of which many

transactions were lost in this process. This action of management indicates the existence of fraud

risk factors such as some fraudulent activity has been initiated and with the fear of internal audit

teams which will definitely be able to rectify it, the replacement of the entire system with new IT

system was management’s idea so that they can skip the transactions and declare it to transaction

lost due to less knowledge or incapability of accounting system, IT department and the

employees. In addition, the same action acts as an opportunity for employees or other members,

who can take advantage of messed up accounts and thus, misinterpret the cash balances or

conduct an activity which may help him to earn personal money on account of the firm and after

all this blame the department for being so careless regarding the transfer of accounts from old

system to the new accounting system (Khan and Jain, 2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References:

Basu, S. (2009). Fundamentals of auditing. Delhi: Pearson.

Blank, R. (2014). The Basics of Quality Auditing. Hoboken: Taylor and Francis.

Boynton, W., & Johnson, R. (2006). Modern Auditing. Hoboken: John Wiley and Sons.

Cahill, L., & Kane, R. (2011). Environmental health and safety audits. Lanham, MD:Government

Institutes.

Griffin, M. (2009). MBA fundamentals. New York, NY: Kaplan.

GUPTA. (2016). FINANCIAL ACCOUNTING FOR MANAGEMENT. [S.l.]: PEARSON EDUCATION

INDIA.

Horngren, C., Datar, S. and Rajan, M. (2017). Horngren's cost accounting. Harlow, Essex, England:

Pearson Education Limited.

Hooks, K. (2011). Auditing and assurance services. Hoboken, NJ: Wiley.

Knechel, W., Salterio, S., & Ballou, B. (2017). Auditing. New York: Routledge.

Messier, W. (2016). Auditing & assurance services. [Place of publication not identifiedMcgraw-Hill

Education.

Khan, M. and Jain, P. (2013). Management accounting. New Delhi, India: McGraw-Hill Education

(India).

Kumar, P. (2014). CA-IPCC Auditing and Assurance. Delhi, India: S. Chand Publishing.

Pitt, S. (2014). Internal audit quality. Hoboken: Wiley.

Ramaswamy, M. (n.d.). Finance for nonfinancial managers.

Basu, S. (2009). Fundamentals of auditing. Delhi: Pearson.

Blank, R. (2014). The Basics of Quality Auditing. Hoboken: Taylor and Francis.

Boynton, W., & Johnson, R. (2006). Modern Auditing. Hoboken: John Wiley and Sons.

Cahill, L., & Kane, R. (2011). Environmental health and safety audits. Lanham, MD:Government

Institutes.

Griffin, M. (2009). MBA fundamentals. New York, NY: Kaplan.

GUPTA. (2016). FINANCIAL ACCOUNTING FOR MANAGEMENT. [S.l.]: PEARSON EDUCATION

INDIA.

Horngren, C., Datar, S. and Rajan, M. (2017). Horngren's cost accounting. Harlow, Essex, England:

Pearson Education Limited.

Hooks, K. (2011). Auditing and assurance services. Hoboken, NJ: Wiley.

Knechel, W., Salterio, S., & Ballou, B. (2017). Auditing. New York: Routledge.

Messier, W. (2016). Auditing & assurance services. [Place of publication not identifiedMcgraw-Hill

Education.

Khan, M. and Jain, P. (2013). Management accounting. New Delhi, India: McGraw-Hill Education

(India).

Kumar, P. (2014). CA-IPCC Auditing and Assurance. Delhi, India: S. Chand Publishing.

Pitt, S. (2014). Internal audit quality. Hoboken: Wiley.

Ramaswamy, M. (n.d.). Finance for nonfinancial managers.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.