Auditing and Assurance Report: Cloud 9 and Executive Pay Study

VerifiedAdded on 2023/04/20

|12

|2348

|466

Report

AI Summary

This report provides a detailed analysis of auditing and assurance principles, focusing on the financial performance of Cloud 9. It begins by defining and calculating planning materiality, crucial for determining the impact of misstatements. The report then delves into analytical procedures, using ratio analysis to assess Cloud 9's profitability, liquidity, and solvency. The profitability section examines EBIT and net profit margins, while the liquidity analysis assesses current and quick ratios. Solvency is evaluated through debt-to-equity and debt-to-total-assets ratios. Additionally, the report includes a case study on executive compensation in the mining industry, examining the remuneration of executives at BHP Billiton, Rio Tinto, and Newcrest Mining, linking pay to company performance, and drawing overall conclusions about Australian executive remuneration practices. The report uses the annual reports of the mining companies to assess the remuneration pattern of the key executives. The report provides insights into financial reporting, auditing practices, and corporate governance.

Running head: AUDINTING AND ASSURANCE

Auditing and Assurance

Name of the Student

Name of the University

Authors Note

Course ID

Auditing and Assurance

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDINTING AND ASSURANCE

Table of Contents

Answer to Part 1: Materiality.....................................................................................................2

Answer to question 1:.............................................................................................................2

Answer to Part 2: Analytical Procedure.....................................................................................3

Answer to A:..........................................................................................................................3

Answer to B:..........................................................................................................................6

Case Study 2:..............................................................................................................................6

How are executives paid in Mining Industries?.....................................................................6

Executives of companies that are paid most and the range of pay:.......................................7

Linkage with Executives pay with the company’s profit and share price performance:.......7

Overall conclusion of Australian company executive’s remuneration:.................................8

References:...............................................................................................................................10

Table of Contents

Answer to Part 1: Materiality.....................................................................................................2

Answer to question 1:.............................................................................................................2

Answer to Part 2: Analytical Procedure.....................................................................................3

Answer to A:..........................................................................................................................3

Answer to B:..........................................................................................................................6

Case Study 2:..............................................................................................................................6

How are executives paid in Mining Industries?.....................................................................6

Executives of companies that are paid most and the range of pay:.......................................7

Linkage with Executives pay with the company’s profit and share price performance:.......7

Overall conclusion of Australian company executive’s remuneration:.................................8

References:...............................................................................................................................10

2AUDINTING AND ASSURANCE

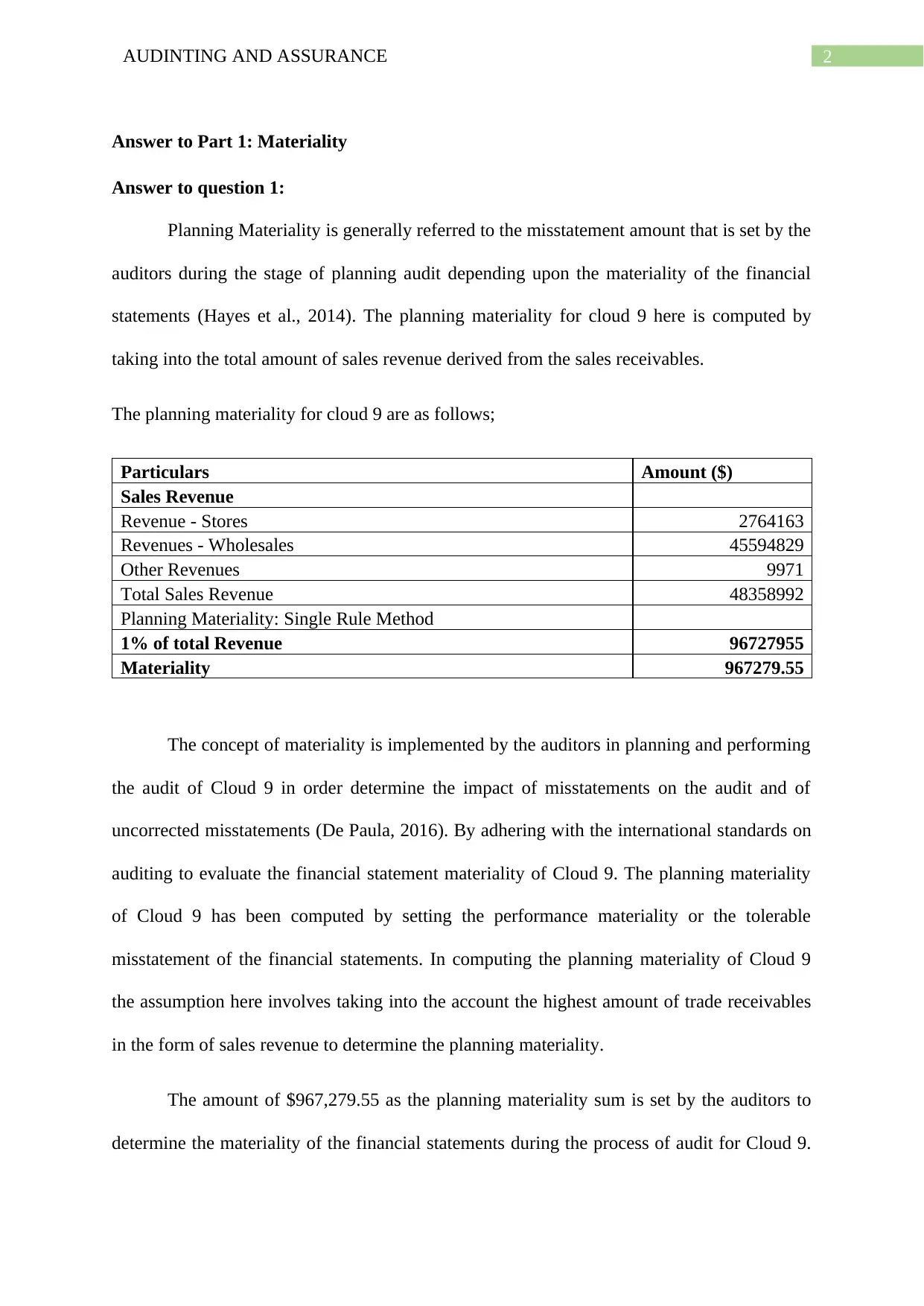

Answer to Part 1: Materiality

Answer to question 1:

Planning Materiality is generally referred to the misstatement amount that is set by the

auditors during the stage of planning audit depending upon the materiality of the financial

statements (Hayes et al., 2014). The planning materiality for cloud 9 here is computed by

taking into the total amount of sales revenue derived from the sales receivables.

The planning materiality for cloud 9 are as follows;

Particulars Amount ($)

Sales Revenue

Revenue - Stores 2764163

Revenues - Wholesales 45594829

Other Revenues 9971

Total Sales Revenue 48358992

Planning Materiality: Single Rule Method

1% of total Revenue 96727955

Materiality 967279.55

The concept of materiality is implemented by the auditors in planning and performing

the audit of Cloud 9 in order determine the impact of misstatements on the audit and of

uncorrected misstatements (De Paula, 2016). By adhering with the international standards on

auditing to evaluate the financial statement materiality of Cloud 9. The planning materiality

of Cloud 9 has been computed by setting the performance materiality or the tolerable

misstatement of the financial statements. In computing the planning materiality of Cloud 9

the assumption here involves taking into the account the highest amount of trade receivables

in the form of sales revenue to determine the planning materiality.

The amount of $967,279.55 as the planning materiality sum is set by the auditors to

determine the materiality of the financial statements during the process of audit for Cloud 9.

Answer to Part 1: Materiality

Answer to question 1:

Planning Materiality is generally referred to the misstatement amount that is set by the

auditors during the stage of planning audit depending upon the materiality of the financial

statements (Hayes et al., 2014). The planning materiality for cloud 9 here is computed by

taking into the total amount of sales revenue derived from the sales receivables.

The planning materiality for cloud 9 are as follows;

Particulars Amount ($)

Sales Revenue

Revenue - Stores 2764163

Revenues - Wholesales 45594829

Other Revenues 9971

Total Sales Revenue 48358992

Planning Materiality: Single Rule Method

1% of total Revenue 96727955

Materiality 967279.55

The concept of materiality is implemented by the auditors in planning and performing

the audit of Cloud 9 in order determine the impact of misstatements on the audit and of

uncorrected misstatements (De Paula, 2016). By adhering with the international standards on

auditing to evaluate the financial statement materiality of Cloud 9. The planning materiality

of Cloud 9 has been computed by setting the performance materiality or the tolerable

misstatement of the financial statements. In computing the planning materiality of Cloud 9

the assumption here involves taking into the account the highest amount of trade receivables

in the form of sales revenue to determine the planning materiality.

The amount of $967,279.55 as the planning materiality sum is set by the auditors to

determine the materiality of the financial statements during the process of audit for Cloud 9.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDINTING AND ASSURANCE

If any kind of material misstatement is noticed and the sum is equivalent to or higher than

computed amount, then in such situation adjustment would be required.

Evidences from the case study obtained suggest that Cloud has set the goal of

increasing the sales revenue by 3 per cent for the first five years however one of the success

critical factors for cloud 9 is to attain a 3 per cent increase in its growing share of Australian

footwear market (Louwers et al., 2015). The main purpose of setting the planning materiality

for Cloud 9 here is to recognize the performance materiality to assist the auditors in designing

the audit procedure forming a clear trivial threshold for the accumulating misstatements.

The present year decline in the revenue of Cloud 9 because of the fall in the specific

exceptional orders which appears difficult to rise in future. Furthermore, the overall decline

in the profit prior to tax results in conclusion that more appropriate basis for the materiality

this year would stand around 1% of the revenue (Kumar & Sharma, 2015). The justification

for the basis of computing the planning materiality for Cloud 9 is to set the overall level of

materiality to the accepted level. The planning materiality here reaches the conclusion that

adjustment is made to make sure that the financial statements of cloud 9 are true and fair.

Answer to Part 2: Analytical Procedure

Answer to A:

By using the analytical procedure and ratio analysis the financial position and

business risks of cloud 9 is assessed.

Profitability Ratios:

If any kind of material misstatement is noticed and the sum is equivalent to or higher than

computed amount, then in such situation adjustment would be required.

Evidences from the case study obtained suggest that Cloud has set the goal of

increasing the sales revenue by 3 per cent for the first five years however one of the success

critical factors for cloud 9 is to attain a 3 per cent increase in its growing share of Australian

footwear market (Louwers et al., 2015). The main purpose of setting the planning materiality

for Cloud 9 here is to recognize the performance materiality to assist the auditors in designing

the audit procedure forming a clear trivial threshold for the accumulating misstatements.

The present year decline in the revenue of Cloud 9 because of the fall in the specific

exceptional orders which appears difficult to rise in future. Furthermore, the overall decline

in the profit prior to tax results in conclusion that more appropriate basis for the materiality

this year would stand around 1% of the revenue (Kumar & Sharma, 2015). The justification

for the basis of computing the planning materiality for Cloud 9 is to set the overall level of

materiality to the accepted level. The planning materiality here reaches the conclusion that

adjustment is made to make sure that the financial statements of cloud 9 are true and fair.

Answer to Part 2: Analytical Procedure

Answer to A:

By using the analytical procedure and ratio analysis the financial position and

business risks of cloud 9 is assessed.

Profitability Ratios:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDINTING AND ASSURANCE

Particulars 2015 2014

EBIT 2999839 3565974

Net Sales 60572216 59910912

EBIT Margin 4.95% 5.95%

Net Profit Margin 2015 2014

Net Profit 2240959 3042608

Net Sales 60572216 59910912

Net Profit Margin 3.70% 5.08%

Profitability Ratios - EBITDA Margin

The profitability ratio for Cloud 9 is computed to determine the EBIT margin and Net

Profit Margin. The EBIT is a form of profitability ratio that determines the amount of

earnings generated by the business before interest and tax (Jacoby & Levy, 2016). The EBIT

margin for 2014 stood 5.95% while in 2014 it declined to 4.95%. The ratio represents decline

as Cloud 9 has witnessed an increase in the operating expenses. While the net profit margin

also represents a significant fluctuation in the year 2015 where the net profit margin lowly

stood 3.70% from the previous year figures of 5.08%. The decline in net profit margin is

contributed by the fall in profit before tax with significant rise in income tax expenses for

cloud 9 in 2015.

Liquidity Ratio:

Particulars 2015 2014

Current Assets 25110129 27433729

Current Liabilities 14833563 17133035

Current Ratio 1.69 1.60

Particulars 2015 2014

Current Assets 25110129 27433729

Less: Inventory 5830382 6263228

Quick Assets 19279747 21170501

Current Liabilities 14833563 17133035

Acid Test/Quick Ratio 1.30 1.24

Liquidity Ratios - Current Ratio

Quick Ratio

Particulars 2015 2014

EBIT 2999839 3565974

Net Sales 60572216 59910912

EBIT Margin 4.95% 5.95%

Net Profit Margin 2015 2014

Net Profit 2240959 3042608

Net Sales 60572216 59910912

Net Profit Margin 3.70% 5.08%

Profitability Ratios - EBITDA Margin

The profitability ratio for Cloud 9 is computed to determine the EBIT margin and Net

Profit Margin. The EBIT is a form of profitability ratio that determines the amount of

earnings generated by the business before interest and tax (Jacoby & Levy, 2016). The EBIT

margin for 2014 stood 5.95% while in 2014 it declined to 4.95%. The ratio represents decline

as Cloud 9 has witnessed an increase in the operating expenses. While the net profit margin

also represents a significant fluctuation in the year 2015 where the net profit margin lowly

stood 3.70% from the previous year figures of 5.08%. The decline in net profit margin is

contributed by the fall in profit before tax with significant rise in income tax expenses for

cloud 9 in 2015.

Liquidity Ratio:

Particulars 2015 2014

Current Assets 25110129 27433729

Current Liabilities 14833563 17133035

Current Ratio 1.69 1.60

Particulars 2015 2014

Current Assets 25110129 27433729

Less: Inventory 5830382 6263228

Quick Assets 19279747 21170501

Current Liabilities 14833563 17133035

Acid Test/Quick Ratio 1.30 1.24

Liquidity Ratios - Current Ratio

Quick Ratio

5AUDINTING AND ASSURANCE

The liquidity ratio here represents the class of financial metrics that is used to

determine the ability of the debtors to pay its current obligations for debt without raising any

external capital (Zeff, 2016). To determine the financial position of Cloud 9 current ratio has

been computed. The current ratio for the company represent a positive increasing trend. On

the other hand, the quick ratio measures the ability of the company meet its both the short

term and long term obligations. The quick ratio computed here for cloud 9 represents that the

company has sufficient cash to meets its short term debt obligation as both current and quick

ratio stood greater than one.

Solvency Ratio:

Particulars 2015 2014

Current- Interest bearing liabilities 4549007 5097005

Non-Current-Interest bearing liabilities 900000 950000

Total Debt 5449007 6047005

Shareholders Equity 14703243 12671437

Debt to Equity Ratio 0.37 0.48

Particulars 2015 2014

Total Debt 5449007 6047005

Total Assets 30875612 31169397

Total Debt to Total Assets Ratio 0.18 0.19

Solvency Ratio - Debt to Equity Ratio

Total Debt to Total Assets Ratio

The debt to equity ratio for Cloud 9 represents that the company has lower proportion

of debts. From the perspective of pure risks, ratios that is below 0.4 or lower are treated as the

better debt ratios (Sin et al., 2015). The ratio for 2015 stood 0.37 which is below the risk level

of 0.4 and can be considered better for cloud 9. While the total debt to total ratio provides an

indication of financial leverage for cloud 9 as the ratio computed stood relatively stable for

both 2014 and 2015. The ratio is below one representing that lower proportion of asset is

financed by creditors or debt.

The liquidity ratio here represents the class of financial metrics that is used to

determine the ability of the debtors to pay its current obligations for debt without raising any

external capital (Zeff, 2016). To determine the financial position of Cloud 9 current ratio has

been computed. The current ratio for the company represent a positive increasing trend. On

the other hand, the quick ratio measures the ability of the company meet its both the short

term and long term obligations. The quick ratio computed here for cloud 9 represents that the

company has sufficient cash to meets its short term debt obligation as both current and quick

ratio stood greater than one.

Solvency Ratio:

Particulars 2015 2014

Current- Interest bearing liabilities 4549007 5097005

Non-Current-Interest bearing liabilities 900000 950000

Total Debt 5449007 6047005

Shareholders Equity 14703243 12671437

Debt to Equity Ratio 0.37 0.48

Particulars 2015 2014

Total Debt 5449007 6047005

Total Assets 30875612 31169397

Total Debt to Total Assets Ratio 0.18 0.19

Solvency Ratio - Debt to Equity Ratio

Total Debt to Total Assets Ratio

The debt to equity ratio for Cloud 9 represents that the company has lower proportion

of debts. From the perspective of pure risks, ratios that is below 0.4 or lower are treated as the

better debt ratios (Sin et al., 2015). The ratio for 2015 stood 0.37 which is below the risk level

of 0.4 and can be considered better for cloud 9. While the total debt to total ratio provides an

indication of financial leverage for cloud 9 as the ratio computed stood relatively stable for

both 2014 and 2015. The ratio is below one representing that lower proportion of asset is

financed by creditors or debt.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDINTING AND ASSURANCE

As cloud 9 has bought stocks in US Dollars the company may face the risk of

fluctuations in the values of foreign currency. The variation in the exchange rate would affect

Cloud 9 debt repayments and competitiveness of the footwear bought from US.

Answer to B:

While performing the audit of Cloud 9 it is noticed that the business may face certain

glitches in determining the ideal amount of stock for its stores for minimum availability of

the goods for its customers (Cook et al., 2016). Cloud 9 should place emphasis on the

physical count of inventory by reconciling the inventory count with the general level.

Case Study 2:

To study the remuneration pattern of the key executives, the companies of mining

industries have been considered (Levy, 2016). The annual reports of BHP Billiton, Rio Tinto

and Newcrest mining for the financial year ended 2017 is studied.

How are executives paid in Mining Industries?

The executives at BHP Billiton, Rio Tinto and New Crest Mining provides that the

executives are paid fixed remuneration in the form of base salary, long term and short term

incentives. The executives are paid through the appropriate level of increasing shareholder

value by meeting or exceeding the objectives of both the individual and company. The

remuneration benefits generally include the participation in the pension plan or cash

allowance to contributes towards the pension plan (Jeppesen, 2018). Apart from the short and

long term incentives Rio Tinto pays is executives through bonus deferral where fifty per cent

of the short term incentive plan is delivered with the bonus deferred shares under the

employee investment program.

As cloud 9 has bought stocks in US Dollars the company may face the risk of

fluctuations in the values of foreign currency. The variation in the exchange rate would affect

Cloud 9 debt repayments and competitiveness of the footwear bought from US.

Answer to B:

While performing the audit of Cloud 9 it is noticed that the business may face certain

glitches in determining the ideal amount of stock for its stores for minimum availability of

the goods for its customers (Cook et al., 2016). Cloud 9 should place emphasis on the

physical count of inventory by reconciling the inventory count with the general level.

Case Study 2:

To study the remuneration pattern of the key executives, the companies of mining

industries have been considered (Levy, 2016). The annual reports of BHP Billiton, Rio Tinto

and Newcrest mining for the financial year ended 2017 is studied.

How are executives paid in Mining Industries?

The executives at BHP Billiton, Rio Tinto and New Crest Mining provides that the

executives are paid fixed remuneration in the form of base salary, long term and short term

incentives. The executives are paid through the appropriate level of increasing shareholder

value by meeting or exceeding the objectives of both the individual and company. The

remuneration benefits generally include the participation in the pension plan or cash

allowance to contributes towards the pension plan (Jeppesen, 2018). Apart from the short and

long term incentives Rio Tinto pays is executives through bonus deferral where fifty per cent

of the short term incentive plan is delivered with the bonus deferred shares under the

employee investment program.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDINTING AND ASSURANCE

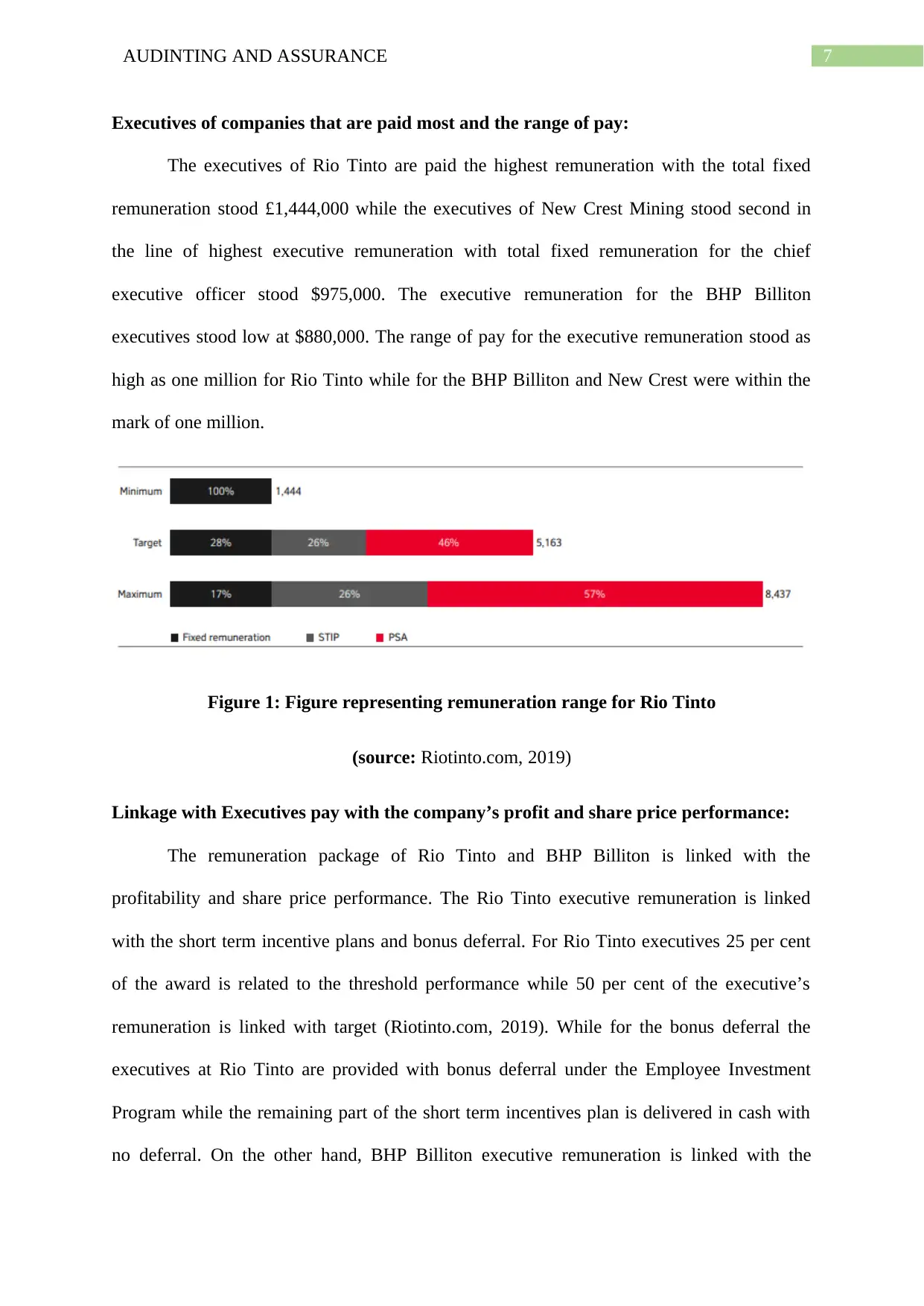

Executives of companies that are paid most and the range of pay:

The executives of Rio Tinto are paid the highest remuneration with the total fixed

remuneration stood £1,444,000 while the executives of New Crest Mining stood second in

the line of highest executive remuneration with total fixed remuneration for the chief

executive officer stood $975,000. The executive remuneration for the BHP Billiton

executives stood low at $880,000. The range of pay for the executive remuneration stood as

high as one million for Rio Tinto while for the BHP Billiton and New Crest were within the

mark of one million.

Figure 1: Figure representing remuneration range for Rio Tinto

(source: Riotinto.com, 2019)

Linkage with Executives pay with the company’s profit and share price performance:

The remuneration package of Rio Tinto and BHP Billiton is linked with the

profitability and share price performance. The Rio Tinto executive remuneration is linked

with the short term incentive plans and bonus deferral. For Rio Tinto executives 25 per cent

of the award is related to the threshold performance while 50 per cent of the executive’s

remuneration is linked with target (Riotinto.com, 2019). While for the bonus deferral the

executives at Rio Tinto are provided with bonus deferral under the Employee Investment

Program while the remaining part of the short term incentives plan is delivered in cash with

no deferral. On the other hand, BHP Billiton executive remuneration is linked with the

Executives of companies that are paid most and the range of pay:

The executives of Rio Tinto are paid the highest remuneration with the total fixed

remuneration stood £1,444,000 while the executives of New Crest Mining stood second in

the line of highest executive remuneration with total fixed remuneration for the chief

executive officer stood $975,000. The executive remuneration for the BHP Billiton

executives stood low at $880,000. The range of pay for the executive remuneration stood as

high as one million for Rio Tinto while for the BHP Billiton and New Crest were within the

mark of one million.

Figure 1: Figure representing remuneration range for Rio Tinto

(source: Riotinto.com, 2019)

Linkage with Executives pay with the company’s profit and share price performance:

The remuneration package of Rio Tinto and BHP Billiton is linked with the

profitability and share price performance. The Rio Tinto executive remuneration is linked

with the short term incentive plans and bonus deferral. For Rio Tinto executives 25 per cent

of the award is related to the threshold performance while 50 per cent of the executive’s

remuneration is linked with target (Riotinto.com, 2019). While for the bonus deferral the

executives at Rio Tinto are provided with bonus deferral under the Employee Investment

Program while the remaining part of the short term incentives plan is delivered in cash with

no deferral. On the other hand, BHP Billiton executive remuneration is linked with the

8AUDINTING AND ASSURANCE

performance shares which provides the strong alignment between the remuneration outcomes

and the interest of the BHP shareholders.

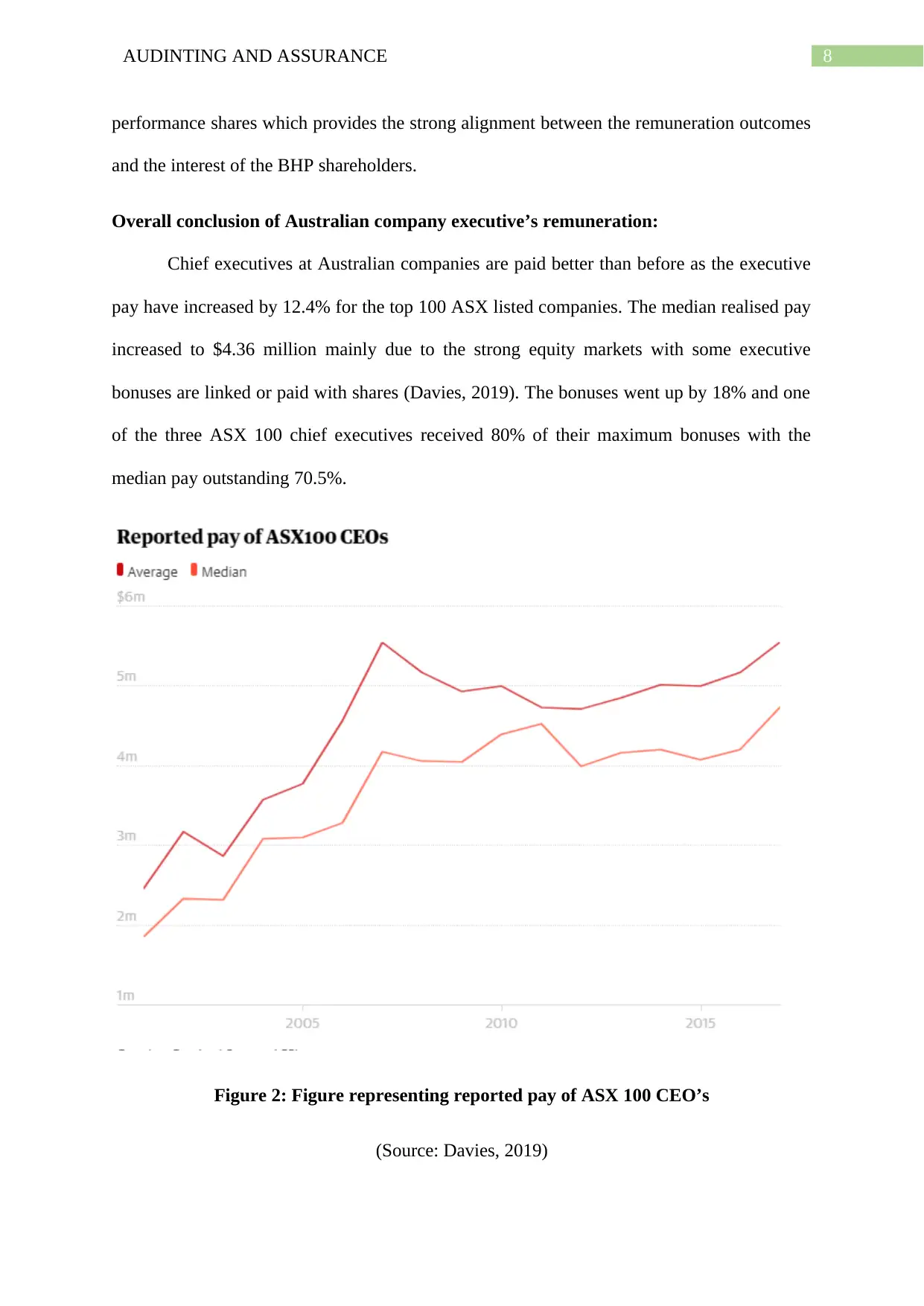

Overall conclusion of Australian company executive’s remuneration:

Chief executives at Australian companies are paid better than before as the executive

pay have increased by 12.4% for the top 100 ASX listed companies. The median realised pay

increased to $4.36 million mainly due to the strong equity markets with some executive

bonuses are linked or paid with shares (Davies, 2019). The bonuses went up by 18% and one

of the three ASX 100 chief executives received 80% of their maximum bonuses with the

median pay outstanding 70.5%.

Figure 2: Figure representing reported pay of ASX 100 CEO’s

(Source: Davies, 2019)

performance shares which provides the strong alignment between the remuneration outcomes

and the interest of the BHP shareholders.

Overall conclusion of Australian company executive’s remuneration:

Chief executives at Australian companies are paid better than before as the executive

pay have increased by 12.4% for the top 100 ASX listed companies. The median realised pay

increased to $4.36 million mainly due to the strong equity markets with some executive

bonuses are linked or paid with shares (Davies, 2019). The bonuses went up by 18% and one

of the three ASX 100 chief executives received 80% of their maximum bonuses with the

median pay outstanding 70.5%.

Figure 2: Figure representing reported pay of ASX 100 CEO’s

(Source: Davies, 2019)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDINTING AND ASSURANCE

Overall, the annual report provides a clear data of the executive’s remuneration patter

by incorporating a detailed section relating to remuneration packages of executives. This

enables the users of financial information to gain a better understanding of the remuneration

policy and packages paid to the executives.

Overall, the annual report provides a clear data of the executive’s remuneration patter

by incorporating a detailed section relating to remuneration packages of executives. This

enables the users of financial information to gain a better understanding of the remuneration

policy and packages paid to the executives.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDINTING AND ASSURANCE

References:

Cook, W., van Bommel, S., & Turnhout, E. (2016). Inside environmental auditing:

effectiveness, objectivity, and transparency. Current Opinion in Environmental

Sustainability, 18, 33-39.

Davies, A. (2019). Australian top executive pay up 12% and bonuses up 18%, survey finds.

Retrieved from https://www.theguardian.com/australia-news/2018/jul/17/ceos-12-

pay-rise-routine-bonuses-tone-deaf-investor-group-says

De Paula, F. R. M. (2016). The principles of auditing a practical manual for students and

practitioners. Isaac Pitman & Sons, Ltd (1919).

Hayes, R. S., Gortemaker, H., & Wallage, P. (2014). Principles of auditing: an introduction

to international standards on auditing. Prentice Hall, Financial Times.

Jacoby, J., & Levy, H. B. (2016). The materiality mystery. The CPA Journal, 86(7), 14.

Jeppesen, K. K. (2018). The role of auditing in the fight against corruption. The British

Accounting Review.

Kumar, R., & Sharma, V. (2015). Auditing: Principles and practice. PHI Learning Pvt. Ltd..

Levy, H. B. (2016). Unsolved Problems in Auditing. The CPA Journal, 86(2), 24.

Louwers, T. J., Ramsay, R. J., Sinason, D. H., Strawser, J. R., & Thibodeau, J. C.

(2015). Auditing & assurance services. McGraw-Hill Education.

Riotinto.com. (2019). Retrieved from

https://www.riotinto.com/documents/RT_2017_Annual_Report.pdf

References:

Cook, W., van Bommel, S., & Turnhout, E. (2016). Inside environmental auditing:

effectiveness, objectivity, and transparency. Current Opinion in Environmental

Sustainability, 18, 33-39.

Davies, A. (2019). Australian top executive pay up 12% and bonuses up 18%, survey finds.

Retrieved from https://www.theguardian.com/australia-news/2018/jul/17/ceos-12-

pay-rise-routine-bonuses-tone-deaf-investor-group-says

De Paula, F. R. M. (2016). The principles of auditing a practical manual for students and

practitioners. Isaac Pitman & Sons, Ltd (1919).

Hayes, R. S., Gortemaker, H., & Wallage, P. (2014). Principles of auditing: an introduction

to international standards on auditing. Prentice Hall, Financial Times.

Jacoby, J., & Levy, H. B. (2016). The materiality mystery. The CPA Journal, 86(7), 14.

Jeppesen, K. K. (2018). The role of auditing in the fight against corruption. The British

Accounting Review.

Kumar, R., & Sharma, V. (2015). Auditing: Principles and practice. PHI Learning Pvt. Ltd..

Levy, H. B. (2016). Unsolved Problems in Auditing. The CPA Journal, 86(2), 24.

Louwers, T. J., Ramsay, R. J., Sinason, D. H., Strawser, J. R., & Thibodeau, J. C.

(2015). Auditing & assurance services. McGraw-Hill Education.

Riotinto.com. (2019). Retrieved from

https://www.riotinto.com/documents/RT_2017_Annual_Report.pdf

11AUDINTING AND ASSURANCE

Sin, F. Y., Moroney, R., & Strydom, M. (2015). Principles‐based versus rules‐based auditing

standards: The effect of the transition from AS2 to AS5. International Journal of

Auditing, 19(3), 282-294.

Zeff, S. A. (2016). Forging accounting principles in five countries: A history and an analysis

of trends. Routledge.

Sin, F. Y., Moroney, R., & Strydom, M. (2015). Principles‐based versus rules‐based auditing

standards: The effect of the transition from AS2 to AS5. International Journal of

Auditing, 19(3), 282-294.

Zeff, S. A. (2016). Forging accounting principles in five countries: A history and an analysis

of trends. Routledge.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.